行政院國家科學委員會專題研究計畫 成果報告

不完全資訊下之策略性債務協商:理論與實證研究

研究成果報告(精簡版)

計 畫 類 別 : 個別型 計 畫 編 號 : NSC 99-2410-H-009-043- 執 行 期 間 : 99 年 08 月 01 日至 100 年 07 月 31 日 執 行 單 位 : 國立交通大學財務金融研究所 計 畫 主 持 人 : 郭家豪 計畫參與人員: 碩士班研究生-兼任助理人員:陸志瑋 博士班研究生-兼任助理人員:王鈺仁 報 告 附 件 : 出席國際會議研究心得報告及發表論文 處 理 方 式 : 本計畫涉及專利或其他智慧財產權,2 年後可公開查詢中 華 民 國 100 年 09 月 18 日

Introduction

The valuation of risky debt is central to theoretical and empirical work in corporate finance. There are many existing literatures such as Anderson and Sundaresan (1996) and Mella-Barral and Parraudin (1997) arguing that costless debt renegotiation never obtains inefficient liquidations at equilibrium for the financing of the firm. When a firm cannot pay off a loan, it is technically bankrupt1. Both the creditor and the firm may experience a Pareto-improvement in their positions by renegotiating the loan. By renegotiating the terms of the debt, the financially distressed firm can pay less than the originally-contracted interest payment and avoid the stigmatization of bankruptcy and the creditor can avoid the costs of taking the firm. Hence, debt renegotiation can eliminate inefficient liquidations. However, inefficient liquidations really occur in many markets even after renegotiation. This research is motivated by the empirical observation that banks do not always renegotiate and that costly bankruptcies are observed in many markets or countries.

Hackbarth, Hennessy, and Leland (2007) first used the trade-off theory between tax-shield and bankruptcy cost to explain these inefficient liquidations for weak firms (small/young corporations) after introducing market debts. They also showed that banks always accept strong firms’ renegotiation offers and never liquidate these firms

1 In practice, there exist some different definitions of bankruptcy or default. For example, the definition of the default applicable to the credit index includes restructuring, whereas the definition for CDS contracts on the reference entity does not.

no matter how the information on the debt contract conditions evolves over time. Their results are consistent with the findings of Blackwell and Kidwell (1988) that small firms issue privately placed debt almost exclusively and larger firms are more likely to issue market debt. Nevertheless, Bourgeon and Dionne (2007) argued that this scenario does not necessarily corresponding to the reality. They introduced asymmetric information on the LGD (loss given default) value at the renegotiation date to explain why banks do not renegotiate with strong firms under certain circumstances. They found that the presence of asymmetric information between banks and firms induces that banks will not always renegotiate with strong firms with a high LGD or a low liquidation value. Their model contributes to explain some empirical findings of Carey and Gordy (2009).

Nevertheless, much recent research has focused on perfect information models on the firm’s value for creditors. For examples, see Mella-Barral and Parraudin (1997), Bourgeon and Dionne (2007), and Hackbarth, Hennessy, and Leland (2007). However, indeed, there is asymmetric information between the firm and the creditor because it is typically difficult for the creditor to observe the firm’s value directly. Hence, the creditor must instead draw inference about the state variable from publicly available information. The state variable may be the firm’s value, the EBIT, the output price, or other specifications. As claimed in Duffie and Lando (2001), the creditor’s imperfect

information on the firm’s value makes default intensity is strictly positive at zero maturity because the creditor is uncertain about the nearness of current state variable to the trigger level at which the firm would declare default. The existence of the default intensity makes it reasonable that observed bond prices often drop abruptly at or around the time of default. Bond prices with perfect information instead converge continuously to its default-contingent value as default approaches. Moreover, yield spreads for risky firms’ debts with complete information climbs rapidly with maturity, but bond-market participants’ imperfect information on the firm causes a more moderate variation in yield spreads with maturity. And lots of empirical studies such as Fons (1994), Helwege and Turner (1999), and Sarig and Warga (1989) showed that severe variation in the shape of the term structure of yield spreads is seldom observed in bond markets.

In this research, we focus on the problem of the implications of strategic debt service with incomplete information. Under informational assumptions, we derive the creditor’s conditional distribution of the firm’s value, conditional default probability, and default intensity, explicitly accounting for the implications of imperfect information and renegotiation mechanism. Then, we show how the renegotiation bargaining power affects the debt value. In addition, we review related efficiency problem of debt issuing with imperfect information. To the best of our knowledge, the

proposed model here is the first structural model considering renegotiation with imperfect information and is consistent with a reduced-form representation.

Model

Throughout our analysis, we suppose that capital markets are frictionless and agents are risk neutral and can borrow and lend freely at a constant interest rate, r , but the bond-market information on the credit quality of the firm’s debt is incomplete. We consider a firm that produces a unit of output for sale with an incurring cost of w> . 0 As well as Mella-Barral and Parraudin (1997), the stochastic process p describing the output price of our given firm is modeled as a geometric Brownian motion, which is defined, along with all other random variables, on a fixed probability space

(

W, ,F P)

. In particular, , where 0t t

X = X +mt+sB (1) for B is a standard Brownian motion, a volatility parameter s > , and a parameter 0

(

,)

mÎ -¥ ¥ that determines the expected price growth rate

(

)

1 2

0

log t 2

t- éëE V V ùû= +m s . While in production at time t , the firm generates its net earnings flow

. (2) We also suppose that the bankruptcy may impair the firm’s efficiency. After

t X t p =e t t EBIT = p -w

bankruptcy, new owners of the firm can only generate earnings of 1pt 0w

x -x , (3) where x £1 1 and x ³ . The reason may be that the operation know-how of the 0 1 firm is not well-known to the new owner. Alternatively, one may regard the expected, discounted value of the reduction in net earnings as the direct cost of bankruptcy.

Because creditors or bondholders are not responsible for the operation of the firm, they are not kept fully informed of the status of the firm. However, they do understand that optimizing equity owners will force liquidation when the firm’s value falls to some critical threshold, g , or, equivalently, the output price falls to the corresponding critical level, p . c g is the scrapping value of the firm at liquidation if the firm

owner opts for liquidation. Because of the existence of a noisy accounting report of net earnings flow, creditors or bondholders may choose to estimate the true net earnings flow from the output price. However, it is not so easy to observe the output price process p directly because not only the incurring cost but also the output price belongs to the so-called “business secrets”. It is important to recognize that the interpretation of p and w in this research is made simply to aid exposition. Hence, it is not really appropriate to select p and w by examining data on the output price and cost.

observe the output price process p directly. Instead, they receive imperfect information on the output price. We assume that, at each observation time t , there is an observed noisy output price, given by ˆp , where t logp and logˆt p are joint t

normal. The observed noisy output price may come from the public information on the industrial average whole sale price. If creditors or bondholders want to calculate the firm’s value, the first thing that all they can do is to infer the true output price from the imperfect information which is publicly available. Specifically, we suppose that , where U is normal distributed and independent of t

t

X . The expectation of U is u and the variance of t U is t a . Conditional on X 2

starting at some level , we know

2 2 0

~ ( , )

t

Y Normal x +mt u a+ +s t . (4) Let W p denote the total value of the pure equity firm in the hands of its ( )t

initial equityholders, and X p denote the total value of the pure equity firm in the ( )t hands of the other owners after bankruptcy. Mella-Barral and Parraudin (1997) derived the following equations:

for ( ) for t c t t c t c t c p w p w p p p W p r r r r p p p l g m m g ì é ùæ ö - + - + ³ ï ê úç ÷ =í - ë - û è ø ï < î (5) 1 0 1 0 for ( ) for t x t t x t x t x p w p w p p p X p r r r r p p p l x x g x x m m g ì é ùæ ö - + - + ³ ï ê úç ÷ =í - ë - ûè ø ï < î (6) ˆ Ut X Ut t Yt t t p = p e =e + =e 0 x

where m = +m s2 2, ( ) 1 c w r p r r l g m l + = - -- , x 1 0 1 ( ) w r p r r l x g m l x + = - -- , and

l is the negative root of the quadratic equation l l( -1)s2 2+lm= . r

Results

Proposition 1. Under imperfect market, we assume the noisy accounting report of

assets is given by ˆ Ut Yt t t

p = p e =e , conditional on t > and the starting level t x . 0 The total value of the pure equity firm in the hands (i) of its initial equityholders,

ˆ ( )

ulnr

W p (unleveraged and no renegotiation), and (ii) of other owners after

bankruptcy, Xulnr( )p , under imperfect market are equal to ˆ

1 ˆ ( ) c c c c p w p w W p A A r m r g r m r l é ù = - +ê - + ú - ë - û ulnr (7)

( )

1 0 1 0 1 ˆ x x x x p w p w X p A A r r r r l x x g x x m m é ù = - +ê - + ú - ë - û ulnr (8) where ( ) 1 c w r p r r l g m l + = - -- , x(

m)

g x l l -+ -= r r r w px 1 0 1 , and A pij( )ˆt referto the Appendix, and l is the negative root of the quadratic equation

2

( 1) / 2 r l l- s +lm= .

Proposition 2. Under incomplete market, we assume the noisy accounting report of

assets is given by ˆ Ut X Ut t Yt t t

p = p e =e + =e , conditional on t > and the starting t levelx . If 0 Lwlnr( )p (with leverage and no renegotiation) and ˆ Vwlnr( )p respectively ˆ

denote the values of the firm’s debt and equity under these assumptions, then, if

/

b r

Lwlnr( )pˆ b r = (9) ˆ ˆ b V (p) W (p) r = -wlnr ulnr . (10)

If g <b r/ , the debt is risky and the expected values of the ˆ( )V p and ˆ( )t L p are t given by 1 1 0 ˆ ( ) b b b b b x wlnr x b x xb xb xb b x b p w b p w b A A for p p r r r r V p p w b p w b p B B B for p p r r r r p l l l m m m m ì - + -é - + ù < ï - ê - ú ë û ï = í æ ö é ù + + ï - - - ³ ç ÷ ê ú ï - ë - û è ø î (11) 1 0 1 1 0 1 0 ( ) ( ) (1 ) ˆ ( ) ( b b b x x x xb xb wlnr x x b b X p A for p p r r p w b A B B r r L p p w A B r r l l l x x m x x g m é ù +ê - ú < ë û + - - -= é ù +ê - + ú -ë û 0 ) ( ) xb x xb b xb b x b p b b B X p B for p p r r p l l ì ï ï ï ï ï ï í ï ï ï ï æ ö é ù ï + - ç ÷ ³ ê ú ï ë ûè ø î (12) where 0 1 ( ) 1 x w r p r r x g l m l x + = - -- , b 1 ( ) w b p r r l m l + = - -- , A pij( )ˆt and ˆ ( ) ijk t

B p refer to the Appendix, and l is the negative root of the quadratic equation

2

(1 ) / 2 r l -l s +lm= .

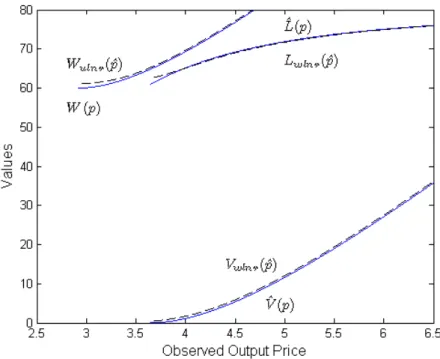

The prediction value, Wulnr( )p , ˆt Vwlnr( )p , and ˆt Lwlnr( )p from Proposition 1 ˆt

and 2 are illustrated in Figure 1. Even if outer investors know that the observed price is unbiased, they still feel frightened when the observed price decreases to p . As c

firm value because debtholders seem optimistic about the firm under this situation. It is familiar to the expected value of the debt and the equity value. However, inferior information will eventually decreases the debt value as the observed output price increases rapidly.

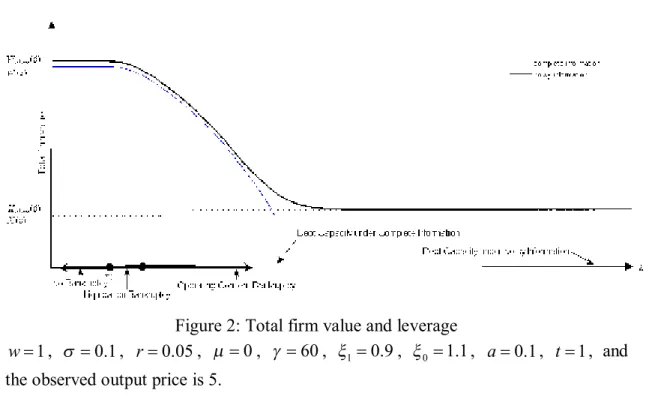

When the debt principal, b/r, is greater than the scrapping value, bondholders are the residual claimants, and the debt is risky. Because of the direct bankruptcy costs, the total firm value, ( ̂ ), which is defined by ( ̂ ) + ( ̂ ), will

decrease as b increases. Leverage generates losses from an ex ante point of view because of the direct bankruptcy costs it entails under complete market. From Figure 2, it is easy to see the difference between complete information market and noisy information market. When b is small, such that b r is smaller than g , the debt is

riskless, and the payment of the coupon does not affect debtholders’ estimation of the firm value under the unbiased observation price ( ( ̂ ) = ( ̂ )). When b

increases and b r becomes larger than g , leverage becomes costly because it may

results in early liquidation at p but not at b . If ≤ , the firm may goes to “liquidation bankruptcy,” which means debtholders will prefer to liquidate the firm than take over at bankruptcy. If pb > px, there is some difference in estimating the value of the debt because the bankruptcy occurs at p . When x pb > px, the firm is asserted to be “an operating concern bankruptcy”. When the output price hits p , b

bonderholders tend to take over the firm but not to liquidate the firm instantly. Note that there still is a debt capacity under noisy information since the total firm value eventually converges toXulnr as b increases.

We also want to consider how the value of the firm’s security is affected if debtholders and equityholders can renegotiate coupon payments. As the claim in Mella-Barral and Perraudin (1997), the firm will not liquidate at or but at when coupon payments can be renegotiated and equityholders can make take-it-or-leave-it offers to debtholders. Hence, we define

( ̂ ) ≡ ∫ ( ) ( ) ( | ̂ , , ) be the estimated total value of the firm

in the hands of other owners but liquidated at . Let us denote a as the equityholders’ bargaining power and 1- as the debtholders’ bargaining power. a

When a = , it indicates that equityholders can make take-it-or-leave-it offers to 1 debtholders. We shall assume that possible strategies for equityholders consist of piecewise right-continuous service flow functions of ˆp , the observation price. Under t

this situation, equityholders will pay the full coupon, b, as the observation price larger than a trigger price, ˆpa =1, and when the observation price is less than ˆpa =1,

equityholders can extract a surplus by offering debtholders a service flow less than b as long as the debt value exceeds ( ̂ ). When a = , debtholders will try to 0

because debtholders can make take-it-or-leave-it offers. Under this situation, debtholders will act as residual claimants who maximize the firm value subject to the constraints placed upon them by the ”outside option” of equityholders. Therefore, the debt value will equal to the firm value when the observed output price is less than

0

ˆpa = , and the equityholders will take these concessions as long as the equity value

does not become negative. Nevertheless, debtholders do not obtain all information on the firm, so they will ask debt value equal to ( ̂ ) =Wulnr( )p instead of ˆt

( )t

W p when the observed output price is less than ˆpa =0. Hence, as 0< < and a 1 ˆ ˆ

p< pa, the debt value will equal ( ̂ ) + (1 − ) ( ̂).

Let s p%( )ˆ be the optimal debt service flow function under noisy information

market. The intuitive explanation of the service flow function is that debtholders require a service flow from equityholders whose capitalized value is sufficient to dissuade them from bankruptcy in order to keep operating. Therefore, equityholders must provide enough income flow worth of ( ̂; ) = ( ̂) +

(1 − ) ( ̂) when ̂ < ̂ . From the above, we assume that

( ̂; ) satisfies the following PDE when ̂ ≥ ̂ ,

( ̂; ) = ̃( ̂) + ̂ ̂ ( ̂; ) + ̂ ( ̂; ) (13)

with the service flow function s p%( )ˆ where ˆm and s are the estimated mean and ˆ2 variance of the logarithm of the observed output price under noisy information market.

Our assumption implies that ( ̂; ) = ( ̂; ) (with leverage and with

renegotiation) for all ̂ < ̂ . No bubble condition includes limpˆ®¥ Lwlwr( ; )pˆ b

r a = .

Under this situation, equityholders know the real price of the output, so the value of equityholders is the real firm value minus the estimated value of debtholders, i.e.

ˆ ˆ

( , ; ) ( ) ( ; )

wlwr wlwr

V p p a =W p -L p a .

Proposition 3. Under incomplete market, we assume the noisy accounting report of

assets is given by ̂ = = = , and equityholders adopt the service flow

function, s p%( )ˆ . The values of equity, Vwlwr( , ; )p pˆ a , and debt, Lwlwr( ; )pˆ a , are as

follows:

( , ̂; ) = ( ) − ( ̂; ) (14)

where, if g ³b r/ , then debt is riskless, and Lwlwr( ; )pˆ a =b r/ . If g <b r/ , then the debt is risky, and

ˆ ˆ ˆ ˆ ˆ ( ; ) ˆ ( ; ) ˆ ˆ ˆ ˆ ( ; ) wlwr s wlwr t wlwr s b b p XW p for p p L p r r p XW p for p p l a a a a a a ì é ùæ ö ï +ê - úç ÷ > = í ë û è ø ï £ î (15)

where ˆpa is solved by L'wlwr(pˆa; )a =XW'wlwr(pˆa; )a , and ˆl is the negative root of the quadratic equation l lˆ ˆ( -1)sˆ2/ 2+lmˆˆ = . r

as- sets is given by ˆ Ut X Ut t Yt t t

p = p e =e + =e . If debtholders can make take-it-or-leave-it offers, then renegotiation will not occur, and the firm will declare

bankruptcy at p , i.e. the issuance of debt cannot generate an efficient outcome when b

the observation price is unbiased.

Conclusions

Our study shows that, if equityholders can make take-it-or-leave-it offers, then equityholders have to give up some equity value in order to convince the debtholders to lower the bond coupon, and debt values will approximate the firm’s taken-over value when the firm is in financial distress. Clearly, when the information on the product price is more transparent, there is less information asymmetry, and debtholders will require a lower information premium when equityholders want to renegotiate the debt service.

When debtholders can make take-it-or-leave-it offers, no matter how low the observation price is under the unbiased assumption, they will never renegotiate actively with the unbiased observation price. The observation price is the only source for debtholders to decide the renegotiation timing. Hence, they really care about the price being underestimated or overestimated, and these two situations will lead to opposite decisions. In order to avoid taking more risk, they are more passive, which

results in inefficient bankruptcy.

References

[1] Anderson, R. W., and S. Sundaresan, 1996, Design and Valuation of Debt Contracts, Review of Financial Studies, 9(1), 37_68.

[2] Beneish, M., and E. Press, 1995, Interrelation Among Events of Default, Contemporary Accounting Research, 12, 57_84.

[3] Blackwell, D., and D. Kidwel, 1988, An Investigation of Cost Differences between Public Sales and Private Placements of Debt, Journal of Financial Economics, 22, 253_278.

[4] Bourgeon, J.-M. and G. Dionne, 2007, On Debt Service and Renegotiation when Debt-Holders are More Strategic, working paper.

[5] Broadie, M., M. Chernov, and S. M. Sundaresan. 2007. Optimal Debt and Equity Values in the Presence of Chapter 7 and Chapter 11, Journal of Finance, 62(3) 1341_1377.

[6] Carey, M. and M.B. Gordy, 2008, The Bank as Grim Reaper:Debt Composition and Recoveries on Defaulted Debt, working paper.

[7] Denis, D. J., and V. T. Mihov, 2003, The Choice among Bank Debt, Non-bank Private Debt, and Public Debt: Evidence from New Corporate Borrowings, Journal of Financial Economics, 70, 3_28.

[8] Duffie, D., and D. Lando, 2001, Term Structure of Credit Spread with Incomplete Accounting Information, Econometrica, 69, 633_664.

[9] Fan, H., and S. M. Sundaresan, 2000, Debt Valuation, Renegotiation, and Optimal Dividend Policy, Review of Finance Studies, 13(4), 1057_1099.

[10] Fons, J. 1994, Using Default Rates to Model the Term Structure of Credit Risk, Financial Analysis Journal, 50, 25_32.

[11] Hackbarth, D., C.A. Hennessy, and H. E. Leland, 2007, Can the Tradeoff Theory Explain Debt Structure?, Review of Finance Studies, 20(5), 1389_1428.

[12] Helwege, J., and C. Turner, 1999, The Slope of the Credit Yield Curve for Speculative-Grade Issuers, Journal of Finance, 54, 1869_1884.

[13] Houston, J., and C. James, 1996, Bank Information Monopolies and the Mix of Private and Public Debt Claims, Journal of Finance, 51, 1863_1889.

[14] Johnson, S., 1997, An Empirical Analysis of the Determinants of Corporate Debt Ownership Structure, Journal of Financial and Quantitative Analysis, 32, 47_69. [15] Krishnaswami, S., P. Spindt, and V. Subramaniam, 1999, Information

Asymmetry, Monitoring, and the Placement Structure of Corporate Debt, Journal of Financial Economics, 51, 407_434.

[16] Lando, D., 2004, Credit Risk Modeling: Theory and Applications. Princeton University Press, Princeton.

[17] .E. LLarry and S. Martin, February 2008, Ambiguity, Information Quality, and Asset Pricing, Journal of Finance, 197_228

[18] Mella-Barral, P., andW. Perraudin, 1997, Strategic Debt Service, Journal of Finance, 52, 531_566.

[19] Sarig, O., and A. Warga, 1989, Some Empirical Estimates of the Risk Structure of Interest Rates, Journal of Finance, 46, 1351_1360.

[20] Schonbucher, P. J., 2003, Credit Derivatives Pricing Models: Models, Pricing, and Implementation. John Wiley & Sons, New York.

[21] Schuermann, T., 2005, What Do We Know about Loss Given Default? Recovery Risk: The Next Challenge in Credit Risk Management. Risk Books, London. [22] Sengupta, P., 1998, Corporate Disclosure Quality and the Cost of Debt, The

Accounting Review, 73, 459_474.

[23] Slovin, M., M. Sushka, and E. Waller, 1997, The Roles of Banks and Trade Creditors in Client-Firm Bankruptcy, working paper, Louisiana State University, Baton Rouge.

[24] Zhou, C., 2001, The Term Structure of Credit Spreads with Jump Risk, Journal of Banking and Finance, 25, 2015_2040.

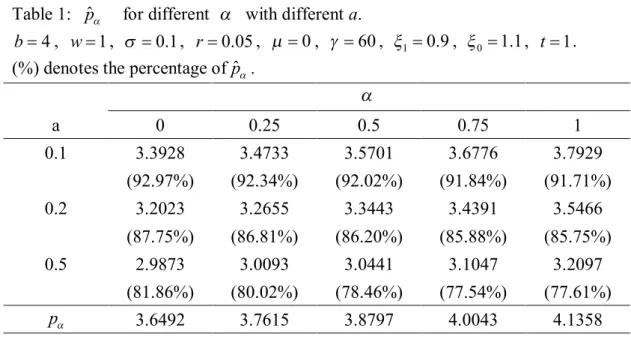

Table 1: ˆpa for different a with different a.

4

b= , w= , 1 s =0.1, r=0.05, m = , 0 g =60, x =1 0.9, x =0 1.1, t= . 1 (%) denotes the percentage of ˆpa.

a a 0 0.25 0.5 0.75 1 0.1 3.3928 3.4733 3.5701 3.6776 3.7929 (92.97%) (92.34%) (92.02%) (91.84%) (91.71%) 0.2 3.2023 3.2655 3.3443 3.4391 3.5466 (87.75%) (86.81%) (86.20%) (85.88%) (85.75%) 0.5 2.9873 3.0093 3.0441 3.1047 3.2097 (81.86%) (80.02%) (78.46%) (77.54%) (77.61%) pa 3.6492 3.7615 3.8797 4.0043 4.1358

Figure 1: Security valuation with no renegotiation 4 b= , w= , 1 s =0.1 , r=0.05 , m = , 0 g =60 , x =1 0.9 , x =0 1.1 , t = , 1 2.9194 c p = , pb =3.6492.

Figure 2: Total firm value and leverage 1

w= , s =0.1, r=0.05, m = , 0 g =60, x =1 0.9, x =0 1.1, a=0.1, t = , and 1 the observed output price is 5.

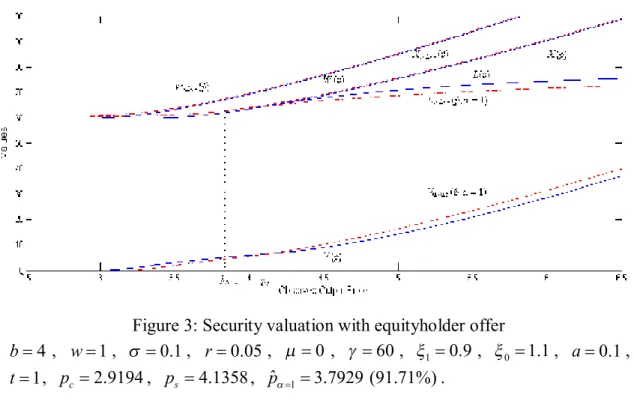

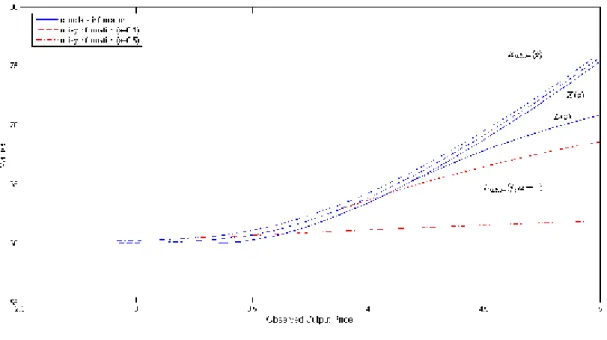

Figure 3: Security valuation with equityholder offer 4

b= , w= , 1 s =0.1, r=0.05, m = , 0 g =60, x =1 0.9, x =0 1.1, a=0.1, 1

Figure 4: Security valuation with equityholder offers and different a 4 b= , w= , 1 s =0.1 , r=0.05 , m = , 0 g =60 , x =1 0.9 , x =0 1.1 , t = , 1 2.9194 c p = , ps =4.1385 , pˆa =1(a=0.1) 3.7929 (91.71%)= , 1 ˆ ( 0.5) 3.2097 (77.61%) pa = a= = .

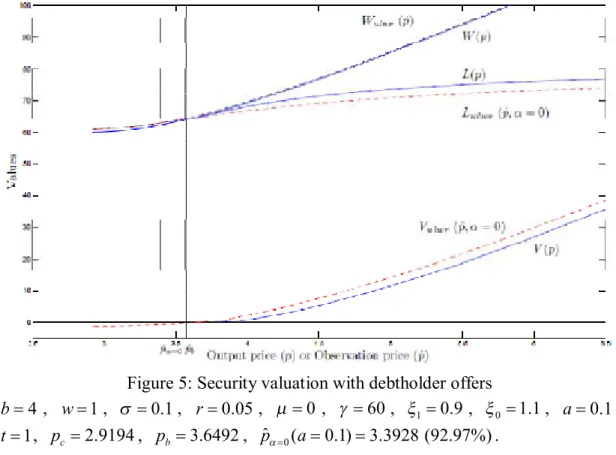

Figure 5: Security valuation with debtholder offers 4 b= , w= , 1 s =0.1, r=0.05, m = , 0 g =60, x =1 0.9, x =0 1.1, a=0.1, 1 t= , pc=2.9194, pb =3.6492, pˆa =0(a=0.1) 3.3928 (92.97%)= .

Self-Examination

When firms experience financial distress, equityholders may act strategically, forcing concessions from debtholders and paying less than the originally-contracted interest payment. This article incorporates a strategic debt service under imperfect information, which enables debtholders to receive the observation price instead of the real price, and develops simple closed-form expression for debt and equity values. We analyze the efficient implications of renegotiation, showing that debtholders will ask for information premium when equityholders can make take-it-or-leave-it offers, and debtholders will never renegotiate actively when they can make take-it-or-leave-it

offers. These findings inspirit our further empirical studies. We plan to write in more formal form and submit the paper to financial journals.

國科會補助專題研究計畫項下出席國際學術會議心得報告

日期:100 年 7 月 15 日

一、參加會議經過

此次 Multinational Finance Society 於義大利羅馬所舉辦之第十八屆學術研

討會,由 6/26 日開始至 6/29 日止共計四天,第一天 10:00 a.m.~12:30 p.m.

於 Hotel FENIX 接受參加研討會現場註冊並於 7 p.m.~10 p.m.舉辦接待歡迎會,

可以與世界各國參與研討會學者或專業人士交流討論。第二天 8:30 a.m.開始各

場次之學術論文發表討論,一天分四個時段,分別是 8:30 a.m.~10:15 a.m.、

10:30 a.m.~12:15 a.m.、2:15 p.m.~4:00 p.m.、4:15 p.m.~6:00 p.m.,每個

時段有八至十個論文研討議題場次同時進行,如 Asset Pricing、Banks、

Financial Crisis、Microstructure、Econometrics、Derivative Markets、

計畫編號

NSC99-2410-H-009-043

計畫名稱

不完全資訊下之策略性債務協商:理論與實證研究出國人員

姓名

郭家豪

服務機構

及職稱

國立交通大學財務金融研究所

助理教授

會議時間

100 年 6 月 26 日

至

100 年 6 月 29 日

會議地點

Rome, Italy

會議名稱

(中文)

(英文)18th Annual Conference of the Multinational Finance Society

發表論文

題目

(中文)

Monetary Policy、Cross Listing、IPOs、Funds、Liquidity、Insider Trading、

Payout Policy、Corporate Finance、Ownership Structure、International

Finance、Exchange Rates、Portfolio Management、Valuation、Bonds、Executive

Compensation、Corporate Restructuring、Interest Rates、Real Options &

Real Estate、Analysts、Corporate Governance、Capital Structure、Earnings

Quality、Credit Risk、Emerging Markets、Commodities、Option Markets、

Volatility 、 M&As 、 Behavioral Finance 、 Venture Capital 、 Hedging 、

Bankruptcy/Financial Distress 、 Cost of Equity Capital 、 Derivative

Markets、Hedge Funds、Option Models、Pension Funds、Market Efficiency

等,幾乎包含財務各個子領域研究範疇,研討會參與者可以自由選擇有興趣的

議題場次參加,除聆聽先端研究論文發表,也可以參與國際學者討論並互相交

換意見。第三天也是 8:30 a.m.開始各場次之學術論文發表討論,同樣一天分四

個時段,也是自由選擇有興趣的議題場次參加。在第二天的議程安排上,除了

各場次學術論文發表討論外、大會還安排重要學者 Prof. Subrahmanyam 演講,

精 彩 演 說 令 人 眼 界 一 開 , 收 獲 甚 豐 ; 第 三 天 的 議 程 安 排 也 有 Prof.

Constantinides 及 Prof. Shefrin 兩位重要學者發表 Keynote Speech,一樣令

人印象深刻。研討會於第四天正式結束,與會者紛紛互相留下各自連絡方式,

以便日後就有興趣之議題可以繼續討論或共同合作,在互道珍重後正式結束為

期四天之國際學術研討會。

二、與會心得

with Daily Price Limits”,本篇論文主旨在討論價格限制市場下的選擇權評價公

式,目前已推導得到在 Black-Scholes 模型下其封閉解,相較於文獻中已知的

finite difference method 或 Monte Carlo simulation 等數值方法,此封閉解

顯著具有計算速度上明顯優勢,論文於研討會發表後引起與會者熱烈討論,與

會者對此論文有諸多建議,如建議可以將公式解與 finite difference method

之解,兩者列表比較其結果之一致性;也可以於論文一開始先加入一敘述統計,

如一年內個股觸及漲跌停次數,說明發展此一選擇權評價模型與推導公式解之

重要性;也有與會者建議可以增加避險相關議題討論,相信在實務上應該可以

作出許多貢獻,如避險策略的擬定或計算避險部位的建立及調整上應有相當助

益。個人覺得此次參加國際學術研討會收獲甚豐,除開闊個人眼界外,透過與

國際學者專家的交流討論,對改善個人論文品質與可讀性,都有很大的助益,

有利於日後論文修改後投稿頂尖國際學術期刊,相信不管對學術研究或實務應

用都可以再作出更大的貢獻。另外,透過參與此次研討會,得以瞭解最新國際

學術研究議題趨勢與發展,也有益於日後個人研究議題的孕育成形,更是無形

的重要收獲,如有與會學者發表將景氣循環納入利率模型中,惟並未考量景氣

循環預測之不確定性,個人認為如能改善此一限制,則該議題未來應該可以有

很多繼續發展的空間。再者,由此次參加研討會中,也見識許多國際學者發表

論文或演說的技巧,對改善個人教學或演說的技巧甚有助益,從如何生動吸引

觀眾注意的口述方式及肢體語言,至充分說明研究議題之動機與重要性,都是

值得好好學習效法之處。

三、考察參觀活動(無是項活動者略):無。

四、建議

個人認為如要邁向國際頂尖學術研究,除了以發表論文於國際頂尖期刊之獎勵

誘因以外,應該搭配鼓勵國內學者專家參加國際學術研討會,或廣邀世界各國

學者參與於國內舉辦之學術研討會等配套措施,由於頂尖學術研究的產生往往

是經過許多學者腦力激盪互相討論後的結果,如能透過學術研討會,增加國際

學者專家與國內學者專家互相交流討論的機會,相信應該更有機會激盪出具頂

尖學術研究價值的議題,也更能明瞭國際學術研究趨勢與發展,進而促成國際

研究團隊的組成,增加國內學術研究於國際間的能見度與影響力。

五、攜回資料名稱及內容

MFC-18-Brochure 學術會議資料,內含本次學術會議議程及所有發表論文簡要內

容等。

六、其他:無。

國科會補助計畫衍生研發成果推廣資料表

日期:2011/09/17國科會補助計畫

計畫名稱: 不完全資訊下之策略性債務協商:理論與實證研究 計畫主持人: 郭家豪 計畫編號: 99-2410-H-009-043- 學門領域: 財務無研發成果推廣資料

99 年度專題研究計畫研究成果彙整表

計畫主持人:郭家豪 計畫編號: 99-2410-H-009-043-計畫名稱:不完全資訊下之策略性債務協商:理論與實證研究 量化 成果項目 實際已達成 數(被接受 或已發表) 預期總達成 數(含實際已 達成數) 本計畫實 際貢獻百 分比 單位 備 註 ( 質 化 說 明:如 數 個 計 畫 共 同 成 果、成 果 列 為 該 期 刊 之 封 面 故 事 ... 等) 期刊論文 0 1 40% 數 個 計 畫 共 同 成 果 研究報告/技術報告 0 0 100% 研討會論文 3 4 40% 篇 數 個 計 畫 共 同 成 果 論文著作 專書 0 0 100% 申請中件數 0 0 100% 專利 已獲得件數 0 0 100% 件 件數 0 0 100% 件 技術移轉 權利金 0 0 100% 千元 碩士生 1 0 100% 博士生 1 0 100% 博士後研究員 0 0 100% 國內 參與計畫人力 (本國籍) 專任助理 0 0 100% 人次 期刊論文 5 7 40% 數 個 計 畫 共 同 成 果 研究報告/技術報告 0 0 100% 研討會論文 2 4 40% 篇 數 個 計 畫 共 同 成 果 論文著作 專書 1 0 10% 章/本 數 個 計 畫 共 同 成 果 申請中件數 0 0 100% 專利 已獲得件數 0 0 100% 件 件數 0 0 100% 件 技術移轉 權利金 0 0 100% 千元 碩士生 0 0 100% 博士生 0 0 100% 博士後研究員 0 0 100% 國外 參與計畫人力 (外國籍) 專任助理 0 0 100% 人次其他成果

(

無法以量化表達之成 果如辦理學術活動、獲 得獎項、重要國際合 作、研究成果國際影響 力及其他協助產業技 術發展之具體效益事 項等,請以文字敘述填 列。) 無 成果項目 量化 名稱或內容性質簡述 測驗工具(含質性與量性) 0 課程/模組 0 電腦及網路系統或工具 0 教材 0 舉辦之活動/競賽 0 研討會/工作坊 0 電子報、網站 0 科 教 處 計 畫 加 填 項 目 計畫成果推廣之參與(閱聽)人數 0國科會補助專題研究計畫成果報告自評表

請就研究內容與原計畫相符程度、達成預期目標情況、研究成果之學術或應用價

值(簡要敘述成果所代表之意義、價值、影響或進一步發展之可能性)

、是否適

合在學術期刊發表或申請專利、主要發現或其他有關價值等,作一綜合評估。

1. 請就研究內容與原計畫相符程度、達成預期目標情況作一綜合評估

■達成目標

□未達成目標(請說明,以 100 字為限)

□實驗失敗

□因故實驗中斷

□其他原因

說明:

2. 研究成果在學術期刊發表或申請專利等情形:

論文:□已發表 □未發表之文稿 ■撰寫中 □無

專利:□已獲得 □申請中 ■無

技轉:□已技轉 □洽談中 ■無

其他:(以 100 字為限)

3. 請依學術成就、技術創新、社會影響等方面,評估研究成果之學術或應用價

值(簡要敘述成果所代表之意義、價值、影響或進一步發展之可能性)(以

500 字為限)

The valuation of risky debt is always central to theoretical and empirical work in corporate finance because debt financing plays an essential role in firm financing. In this research, we focus on the problem of the implications of strategic debt service with incomplete information. We reexamine related efficiency problems via renegotiation with imperfect information. Our study shows that, if equityholders can make take-it-or-leave-it offers, then equityholders have to give up some equity value in order to convince the debtholders to lower the bond coupon, and debt values will approximate the firm’s taken-over value when the firm is in financial distress. Clearly, when the information on the product price is more transparent, there is less information asymmetry, and debtholders will require a lower information premium when equityholders want to renegotiate the debt service.

When debtholders can make take-it-or-leave-it offers, no matter how low the observation price is under the unbiased assumption, they will never renegotiate actively with the unbiased observation price. The observation price is the only source for debtholders to decide the renegotiation timing. Hence, they really care about the price being underestimated or overestimated, and these two situations

passive, which results in inefficient bankruptcy. To the best of our knowledge, the proposed model here is the first structural model considering renegotiation with imperfect information. We believe that this research will contribute to the literature of related studies of debt service.