科技部補助專題研究計畫成果報告

期末報告

最適貨幣政策協作與景氣循環

計 畫 類 別 : 個別型計畫 計 畫 編 號 : MOST 105-2410-H-004-006-執 行 期 間 : 105年08月01日至106年07月31日 執 行 單 位 : 國立政治大學經濟學系 計 畫 主 持 人 : 黃俞寧 計畫參與人員: 碩士班研究生-兼任助理:范文俞 碩士班研究生-兼任助理:吳奕信 碩士班研究生-兼任助理:蘇醒文 碩士班研究生-兼任助理:陳建勲 大專生-兼任助理:雷歡榕 博士班研究生-兼任助理:林朕陞 報 告 附 件 : 出席國際學術會議心得報告中 華 民 國 106 年 10 月 31 日

中 文 摘 要 : 在此研究中,我們利用一個小型開放經濟體系的DSG模型,其中主要 包含了央行的資產負債表以便探討央行的外匯干預政策。在此架構 下,我們考慮央行同時採行兩種貨幣政策--貨幣成長率法則與管理 浮動匯率,以貼近台灣現況。研究結果顯示,相較於浮動匯率制度 ,管理浮動匯率在減緩名目匯率波動之餘,亦有助於穩定通貨膨脹 率。 中 文 關 鍵 詞 : 動態隨機一般均衡、貨幣成長率法則、管理浮動匯率

英 文 摘 要 : In this study, we establish a small-open-economy DSGE

model. We emphasize the central bank’s balance sheet where the central bank may conduct the regular monetary policy with the foreign exchange intervention. We consider the policy coordination involving monetary aggregate rule and managed floating exchange rate which is consistent with the current monetary policy regime of Taiwan. The dynamic

analyses show that the managed floating exchange rate which dampens the nominal exchange rate depreciation also helps stabilize the inflation rate.

英 文 關 鍵 詞 : dynamic stochastic general equilibrium (DSGE), monetary aggregate policy, managed floating exchange rate

Analyses of Monetary Policy Coordination with A DSGE

Framework

Yu-Ning Hwang

Department of Economics National Chengchi UniversityOct. 2017

Abstract

In this study, we establish a small-open-economy DSGE model. We emphasize the central bank’s balance sheet where the central bank may conduct the regular monetary policy with the foreign exchange intervention. We consider the policy coordination involving monetary aggregate rule and managed floating exchange rate which is consistent with the current monetary policy regime of Taiwan. The dynamic analyses show that the managed floating exchange rate which dampens the nominal exchange rate depreciation also helps stabilize the inflation rate.

Keyword:dynamic stochastic general equilibrium (DSGE), monetary aggregate policy, managed floating exchange rate

Correspondence: Yu-Ning Hwang, Department of Economics, National Chengchi University, Taipei 116,

1

1. Introduction

In small open economies where trades play an important role, central banks usually tend to stabilize the exchange rate movements to prevent the impacts of exchange rate fluctuations on trades. Therefore, the central banks of most countries implement managed floating exchange rate regime (such as Singapore and most Asian countries) through its participation on the foreign exchange market. Taiwan, as a typical small open economy with export and import taking up around 70% and 60% of the GDP respectively, the central bank also conducts the managed floating exchange rate regime.

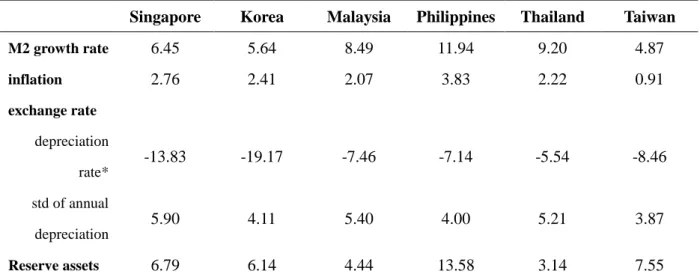

However, after the financial crisis in 2008, many central banks in advanced economies implemented quantitative easing. These expansionary policies have great impacts on emerging economies, particularly through the foreign exchange markets. In recent years, the large fund inflows to emerging economies have led to significant exchange rate appreciation in these small open economies, as shown in Table 1. As a result, the central banks which take actions to avoid significant exchange rate appreciation may lead to significant increase in foreign reserves, which in turn results in the increase in the money supply and the rise in inflation. Table 1 outlines the experiences that major Asian economies have undergone. As we can see, during the past years

Table 1: Average annual growth rate in foreign reserves, M2, inflation and exchange rate depreciation, 2010-2014

*: the negative number refers to the appreciation of the domestic currency against the US dollars. Source: World Bank; International Financial Statistics, IMF.

Singapore Korea Malaysia Philippines Thailand Taiwan

M2 growth rate 6.45 5.64 8.49 11.94 9.20 4.87 inflation 2.76 2.41 2.07 3.83 2.22 0.91 exchange rate depreciation rate* -13.83 -19.17 -7.46 -7.14 -5.54 -8.46 std of annual depreciation 5.90 4.11 5.40 4.00 5.21 3.87 Reserve assets 6.79 6.14 4.44 13.58 3.14 7.55

2

(2010-2014), there are significant increases in M2, inflation and foreign reserves, while the nominal exchange rate experienced significant appreciation with drastic fluctuation in these countries.

The experiences of emerging economies in past years show the tradeoff between controlling the monetary aggregate and stabilizing exchange rate fluctuations that monetary policy making may encounter, particularly under the significant foreign fund inflows. The primary policy instrument of the central bank of Taiwan is monetary aggregate targeting by setting the target for the growth rate of M2 with a fluctuation range of 2%. However, as a small open economy, the central bank of Taiwan also conducts the managed floating exchange rate regime to avoid drastic exchange rate fluctuations. In past years, to stabilize the exchange rate fluctuations due to large foreign fund inflows, the foreign reserves and monetary aggregates rise. The M2 growth rate has continuously reached the upper bound of the target.1 The massive fund inflows have led to the challenge to maintain the target of monetary aggregate.

The macroeconomic effects of quantitative easing (QE) have been widely discussed in the literature. Most of these papers use closed-economy models, and the impacts of QE on foreign countries are relatively rare.2 The current studies on QE’s impact fall on its impacts on emerging economies. For example, Chang, Liu and Spiegel (2015) discuss this issue for China to emphasize the decline in the foreign interest rate increases the cost of sterilization which leads to the increase in the monetary aggregate and inflation. Liu and Spiegel (2014) follow the similar framework to examine the combination of conventional monetary policy and capital account policies including taxing the fund inflows and sterilization may help stabilize the economy.

Alternatively, Escudé (2013) uses a dynamic stochastic general equilibrium (DSGE) model with the description of balances sheet of the central bank to examine the simultaneous implementation of two policy rules, the conventional interest rate rule and managed floating exchange rate. The balance sheet of the central bank includes the government bonds and foreign reserves. The intention of the central bank on the foreign reserve market will lead to the change in the foreign reserve (or bonds if it is sterilized) and money supply. The welfare analyses show that the simultaneous implementation of two monetary policy rules will help stabilize the economy and lead to greater welfare.

1 For example, the target of M2 growth rate in 2015 was set at the range between 2.5% and 6.5%. However,

the growth rate of M2 is above 6% every month in 2015.

3

With the similar framework, Escudé (2014) examines the trilemma in international finance and shows that the “impossible trinity” can be possible.

However, all the studies consider the interest rate rule. While the interest rate rule has been subject to severe criticism after the financial crisis, some studies have started to reexamine the performance of monetary aggregate management. For example, Hwang and McNelis (2015) show that the monetary aggregate rule can perform better in stabilizing consumption and asset price fluctuations than an interest rate rule. Similar results are found in Kelly, Binner, Chang and Tseng (2014) and Belongia, Binner, Tepper and Kelly (2014).

In this paper, we plan to focus on the examination of monetary policy coordination in response to the massive fund inflows to a small open economy. While the fund inflows may cause the problem for the central bank to maintain the monetary stability and exchange rate stability, we plan to examine the effects and welfare implications of alternative policy coordination. We will use the framework of Escudé (2013) to assess the fluctuations and welfare under the simultaneous implementation of the monetary aggregate rule, in contrast to the interest rate rule, and managed floating exchange rate. While the central bank of Taiwan conducts the monetary aggregate rule, this study may provide the policy implications for monetary policy coordination of Taiwan, instead of implementation of one single conventional policy, under massive foreign funds inflows.

This paper is structured as follows. We outline the model in Section 2. We state calibration in Section 3, conduct policy analyses in Section 4, and conclude in Section 5.

2. Model

In this study, we will use a small-open-economy DSGE model to examine how well the different monetary policy coordination may help stabilize the macroeconomic fluctuations under massive foreign fund inflows. We will follow Escudé (2013) to include the balance sheet of the central bank, and two monetary policy rules including the monetary aggregate rule and managed floating exchange rate.

2.1 Final goods market

Final goods are made from intermediate goods, produced in the home and foreign countries. Final goods are nontradable, and are used for household’s consumption,

4

investment and government spending. The composite goods, which are composed of

domestic goods d t

Q and imported goods f t Q :

1 1 1 1 1 Zt d Qtd f Qtf , (1)where d, f 0 represent the ratio of home and imported intermediate goods respectively. is the intratemporal elasticity of substitution between these two types intermediate goods. The demand function for the domestic and imported intermediate goods can be written as:

td d d t d t t P i Q i Q P , , f t f f t f t t P i Q i Q P (2) d d d t t t t P Q Z P ,

, f f f t t t t P Q Z P (3) where d

t Q i and f

tQ i stand for the domestic goods and imported goods of variety i.

is the elasticity of substitution among the individual goods. The corresponding prices are shown as follows:

1 1 1 1 , d d f f t t t P P P (4) where 1 1 1 1 0 , , v v j j t t P P s d s j d , f

d t P i and d tP are the home-currency prices of individual and aggregate domestic

goods, respectively, f

tP i and f t

P are the home-currency prices for the imported

goods. Pt is the aggregate price index. We assume that the imports are priced according

to the international prevailing price such that f * t t t

P S P where St is the nominal

exchange rate, expressed in units of the home currency of foreign currency and * t

P is the

5

2.2 Households

Household obtains utility from consumption and disutility from labor supply. The utility function can be characterized as below:

1 1 1 0 + , 1 1 1 M C N t j t j t t j N t C N M j C N M P E

(5)where Ct and Nt represent the consumption and labor supply in the period t

respectively. (0,1) is the intertemporal elasticity of substitution. C , N

and M stand for the intertemporal elasticity of substitution of consumption, inverse of the elasticity of labor supply, and elasticity of money. N

characterizes the disutility from labor supply.

Households provide capital Kt and labor Nt to firms for production. The capital can be accumulated with investment. The law of motion for capital is

1 1, (1 ) ,

t t t t t

K K K K I (6)

where (0,1) is the depreciation rate of capital and It is the investment in period t. The accumulation of capital will incur the adjustment cost Kt1,Kt so we can model the Tobin’s Q as the indicator of asset price. Kt1,Kt is specified as a convex function, (Kt1,Kt)Kt1Kt2 2Kt.

Moreover, households hold the home bonds H t

B with the interest rate it, and

foreign bonds f t

B with interest rate f t

i . We assume that the transaction of foreign bonds

incurs the risk premium:

* * 1 (1 ) ( ), f f f B t t t B t i i (7) where * * t , , f B f f f f t S Bt t P Yt t e bt t Yt et S Pt t Pt b Bt Pt

6

on the international capital market and et is the real exchange rate. Yt and btf are GDP

and real foreign bonds respectively. f ( f)

B t B

is the function of risk premium which is a convex function of the ratio of foreign bonds to GDP, f ( f )

B t B where 1 1, 0, 0 f f f f B B B B .

Therefore, the budget constraint of household can be written as:

1

1 1 1 1 1 , ( 1 ) ( 1 ) , h f t t t t t t t t t t t t K h f f t t t t t t t t t t t P C P I P K K M B S B T ax W N R K M i B i S B (8) where Wt and K tR are the nominal wage and rental rate on capital goods. t and Taxt

are the profit of firms and the lump-sum tax payment to the government.

Household will maximize the utility subject to the budget constraint Eq. (8) and capital accumulation process Eq. (6) with the Lagragian multiplier t and t

respectively. The first-order conditions are listed as below:

1 1 C 1 1 1 , C C C t t t t t i E (9)

1 1 C 1 1 , C C C f t t t t t t e i E e (10) C , C N t t t t W N P (11) 1 C , M C t t t t t M i P i (12) 1 1 1 1 1 , K t t t t t t R P (13)7 2 1 1 2 1 1 . I t t t t t t t t t t I I E I I (14) 1 1 t Pt Pt

. Letting qt t t , Eq. (13) and (14) can be written as:

1 1 1 1 , K t t t t t t R q q P (15) 2 1 1 1 2 1 1 1 . I t t t t t t t t t t t I I q q q E I I (16) t

q is Tobin’s q which represents the asset price in this model.

2.3 Intermediate goods

We assume that the intermediate goods markets are monopolistically competitive where firms produce heterogeneous goods for the final goods. Firms hire capital and labor for production:

1

( ) ( ( ) ) ( ( ) ) ,

t t t t

Q i Z K i N i (17) where Zt is the total factor productivity and is the elasticity of capital. The marginal cost associated with the production function is

1 1 ( 1 ) ( 1 ) . K t t t t M C R W Z (18)

The goods produced by the domestic firms will be sold domestically and to the foreign country. The home firm produces goods sold in both the domestic and foreign

markets. The foreign demand for the home intermediate goods X

t Q i of variety i is assumed as: * * X t X X t X t t P i Q i Q P and * * , 0, X X t t t t P Q X P (19)8

where PtX*

i is the firm’s export price and * X tP is the aggregate price index of

exported goods, both of which are denominated in the foreign currency. Pt is the foreign

(international) price. is the price elasticity of the aggregate exports. We assume that *

t

X is subject to a random shock.

Firms will set the prices for goods sold in the home country following Calvo’s staggered pricing which assumes that each firm may reset its price with a probability (1 ). As a result, on average, a proportion 1 of firms may change the price while

share of firms will maintain their prices. This implies the mean interval of price change is 1 1 . In period t, a typical firm i will reset the profit-maximizing price

d t

P i which maximizes the profit within the period t and t s when the price

remains valid. The optimal price that a typical firm sets is (the subscript i is dropped due to symmetry): , , , 0 , , , , 0 M C . , 1 . s d d t t s t t s t t s t s d flex t t s A t t s t t s t s E Q P E Q

(20) where ,

s

ts s ts t P Pt ts . d , t s tQ is the demand of goods under this price in

the period ts. and M Cts t, is the associated marginal cost. ts is the Lagragian multiplier in the period ts.

The price index for the domestic price will evolve following the dynamics:

1

1

,

1 1 1 , , d d d flex t t t t P P P (21)For the foreign country, we assume that the law of one price holds. Therefore,

*

X d

t t t

P P S .

9

We assume that the central bank issues money Mt and bonds for households Bth,

and holds the foreign reserves (denominated in foreign currency)Rt. The Balance sheet of

central bank can be written as

,

h

t t t t

M B S R (22)

Therefore, the central bank can change the money supply through open market operations. Also, the participation of central bank on the foreign exchange market will change the foreign reserves and money supply. This may also generate the quasi-fiscal surplus as stated below.

The flow income of the central bank can be written as:

* 1 1 1 1 1 1 1 1 1 (1 ) (1 ) ( ) , h h t t t t t t t t t t h t t t t t M B S R M i B i S R M B S R Q F (23) where * * 1 1 1 1 1 1 1 1 1 1 1 ( ) h [ (1 )] h , t t t t t t t t t t t t t t t Q F i S R S S R i B i S R i B S (24) t

QF is the quasi-fiscal surplus of the central bank. From Eq. (24), we can see that the

quasi-fiscal surplus includes the interest payment on the home bonds and interest revenues from foreign bonds.

We assume that the central bank transfers the quasi-fiscal surplus to the government, and thus the net wealth is constant which is assumed to be 0 for simplicity:

Mt Bth S Rt t Mt1 Bth1St R1t 1 0. (25)

We assume that the government spending is composed of goods resembling the consumption goods, with the lump-sum tax revenues from households and the quasi-fiscal surplus from the central bank. The government’s balanced budget can be stated as:

t t t

G T a x Q F (26)

10

Combining the budget constraint of households, central bank and government can generate the balance of payments of the nation (in foreign currency):

Rt Btf C At Rt1Btf1, (27)

where C At stands for the current account:

*

1 1 ,

f f

t t t t

C A i R i B T B (28)

where T Bt is the trade balance.

2.5 Monetary policy rules

We will follow the specification of Escudé (2013) by implementing two rules. However, since the central bank of Taiwan adopts the monetary aggregate rule by setting the target for the M2 growth rate, we will specify the rules for managing the money growth rate and nominal exchange rate depreciation as below:

0 1 2 3 , , 1 1 1 ( ) ( ) ( ) ( ) exp( ), 1 1 m t m t h t h t h t h m m t T m m g g Y e g g Y e (29) 4 0 1 2 3 1 ( ) ( ) ( ) ( ) ex p ( ), k k k k k S S t t t t t t t t T S S Y e r Y S S Y e r (30)

where gm t, Mt Mt1 Mt1 and gm are the growth rate of monetary aggregate and the targeted growth rate of money. St and S are the nominal exchange rate depreciation and its target, T

is the inflation target, Y is the steady-state output, e is the steady-state real exchange rate and r is the steady-state foreign reserve ratio to GDP.

m t

and S t

are the disturbances of monetary policy while m

and S

measure the

magnitude of these shocks to the policy. h0, h1, h2, h30 and k0, k1, k2, k3< 0 are the

policy parameters of these two rules. The negative values of these policy parameters imply that the central bank conducts the monetary policies to stabilize the macroeconomic fluctuations.

11

The market clearing condition of the goods market can be written as:

,

t t t t

Y C I G (31)

2.6 Exogenous shocks

There are exogenous shocks underlying this model which include shocks to

productivity, government spending, export demand, foreign inflation, foreign interest rate and financial friction on international capital market.

Zt ( 1Z ) ZZ t1 tZ (32) , l nGt l nG G Gl nt1tG (33) , * * * 1 l nXt l nX l nXt Xt (34) , * * * * * * * 1 ( 1 ) , t t t (35) * * * * 1 ( 1 i ) i i , t t t i i i (36) t ( 1 ) t1 t (37) , 3. Calibration

Most of the parameters are chosen following the conventional settings in the literature. In the steady state, we assume that the current account is balanced. The share of

the home produced goods in the foreign consumption *

X is adjusted to assure the

balanced current account. The market price of capital goods is assumed to be q 1, and the real exchange rate is specified as 1 in the steady state. is assumed to be 0.99, following most literature.

The share of import goods in the aggregate consumption f

is set to 0.3. We set the capital share in production 0 .3. The elasticity of intertemporal substitution, inverse of elasticity of labor supply and elasticity of real money demand is set as C 1, N 0 and M 1 for simplicity. Disutility of labor supply N is assumed to be 1. The depreciation rate of capital is specified as 0.025 (reflecting the annual depreciation

12

friction parameter t is assumed to be 0.0019 in the steady sate. The elasticity of

substitution among goods is assumed to be 1.1, such that the markup is about 11%. The elasticity of substitution between the domestic and imported goods and , , is set to 5 The degree of price stickiness is specified as 0.75, implying the average duration of price adjustment around 4 quarters.

We assume that the steady-state foreign reserve ratio to GDP is 0.76 which is the averaged foreign reserve ratio from 2003 to 2016 in Taiwan. As for the monetary aggregate rule, we assume that the policy parameter h0 0.6, h1 0.35, h2 0.1, and h3 0.02 , following the estimation for Taiwan by Hwang(2012). The policy parameters for the managed floating exchange rate rule are assumed to be k0 0.03,

1 0 .0 7

k , k2 0.08, h3 0.43 and h4 0.08.

4. Analyses

In the following analyses, we numerically examine the dynamics of alternative monetary policies under productivity shock and foreign interest rate shock respectively.

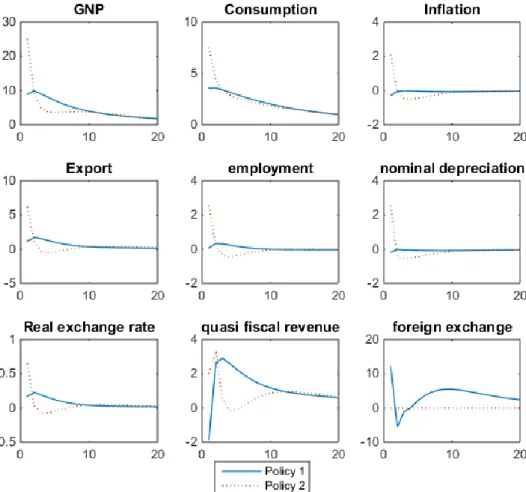

First, we consider a 1% positive shock to productivity with the AR(1) coefficient as 0.9. Figure 2 shows the impulse response functions under managed floating exchange rate and flexible exchange rate regime where the foreign reserve is held constant respectively while the monetary aggregate rule is in place. We can see that, under flexible exchange rate regime, there is greater depreciation rate in nominal and real exchange rates which benefits the export more, and thus leads to greater increase in output, consumption and employment than the managed floating exchange rate regime. Under managed floating exchange rate regime, in order to contain the exchange rate depreciation, the central bank has to intervene on the foreign exchange market. This has led to a temporary decrease in the foreign reserves. However, the quasi-fiscal revenues may benefit from the nominal depreciation of the home currency.

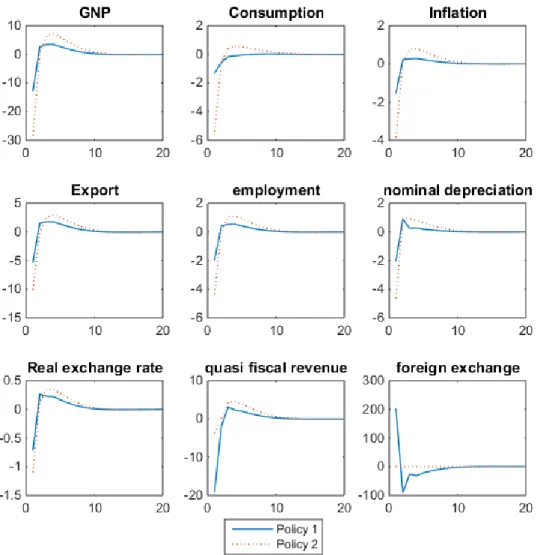

In face of the global trend of interest rate rise in the near future in the aftermath of the global financial crisis, we consider a quarterly 0.25% increase in the foreign interest rate. The impulse response functions under these two policies are outlined in Figure 3. The nominal exchange rate may appreciate upon shock, but depreciate right after. The depreciation helps the increase in export. However, under monetary aggregate rule, the central bank may conduct contractionary monetary policy in response to the increase in

13

the foreign interest rate. The rise in the interest rate leads to the decline in consumption. However, the central bank will intervene in the foreign exchange market to dampen the exchange rate depreciation under managed floating exchange rate regime. As a result, the increase in export fails to offset the decline in consumption under managed floating exchange rate regime. The output expansion is smaller if central bank conducts managed floating exchange rate regime. Again, to avoid the greater depreciation of home currency, the foreign exchange intervention will lead to a decline in foreign exchange. The quasi-fiscal revenue benefits from the higher foreign interest rate. It declines in the beginning due to home currency depreciation, but rises after the home currency starts to appreciate. In both cases of shocks, the managed floating exchange rate dampens the home depreciation and helps stabilizes the inflation. The inflation stabilization can be the potential benefits of managed floating exchange rate regime.

Note: Policy 1: monetary aggregate rule with managed floating exchange rate regime; Policy 2: monetary aggregate rule with flexible exchange rate regime.

14

Note: Policy 1: monetary aggregate rule with managed floating exchange rate regime; Policy 2: monetary aggregate rule with flexible exchange rate regime.

15

Conclusion

In this study, we use a small-open-economy DSGE model to evaluate the monetary policy in Taiwan. We emphasize the balance sheet of the central bank and thus the foreign exchange changes under foreign exchange intervention. Under this framework, the central bank may conduct policy coordination which involves the monetary aggregate rule and managed floating exchange rate regime. The simulation results show that the managed floating exchange rate regime which dampens the exchange rate fluctuation also helps stabilize the inflation.

In the future, we may further consider whether or not the monetary policy should respond to the change in asset price. This has become an important issue after the financial crisis. Moreover, while most emerging economies tend to accumulate great amount of foreign reserves to avoid drastic exchange rate depreciation, which is the lesson learned from the Southeast Asian financial crisis in 1997, it may worth a while for us to examine the foreign reserves more carefully in the future.

16

Literature Review

Belongia, Binner, Tepper and Kelly (2014), “Implementing Monetary Policy: Were the Central Banks Correct in Abandoning the Monetary Aggregates? ,” Working Paper.

Chang, C., Z. Liu, and M. M. Spiegel (2015), “Capital controls and optimal Chinese monetary policy,” Journal of Monetary Economics, 74, 1-15.

Chen, H., V. Cúrdia, and A. Ferrero (2012), “The Macroeconomic Effects of Large-scale Asset Purchase Programmes,” Economic Journal, 122, 289-315.

Devereux, M. B. and C. Engle (2003), “Monetary policy in the open economy revisited: price setting and exchange rate flexibility,” Review of Economic Studies, 70, 765-783.

Devereux, M. B. and J. Yetman (2014), “Capital controls, global liquidity traps, and the international policy trilemma,” Scandinavian Journal of Economics, 116(1), 158-189.

Devereux, M. B., P. R. Lane, and J. Xu (2006), “Exchange rates and monetary policy in emerging market economies,” Economic Journal, 116, 478–506.

Dib, A. (2010), “Banks, Credit Market Frictions, and Business Cycles,” Working Paper, Bank of Canada.

Escudé, G. J. (2013), “A DSGE model for a SOE with systematic interest and foreign exchange policies in which policymakers exploit the risk premium for stabilization purposes,” Central Bank of Argentina, Working Paper.

Escudé, G. J. (2014), “The possible trinity: optimal interest rate, exchange rate, and taxes on capital flows in a DSGE model for a small open economy,” Economics: The Open-Access,

Open Assessment E-Journal, 8(2014-25), 1-58.

Gali, J. and T. Monacelli (2005), “Monetary Policy and Exchange Rate Volatility in a Small Open Economy,” Review of Economic Studies, 72, 707-734.

Gertler, M. L. and P. Karadi (2011), “A Model of Unconventional Monetary Policy,” Journal of

Monetary Economics, 58(1), 17-34.

Hwang, Y. N. (2015), “Welfare Implications of Policy Responses to Foreign Monetary Expansion: Quantitative Assessment with a Dynamic Stochastic General Equilibrium Model,” Academia

17

Economic Papers, 43(3), 287-315.

Hwang, Y. N. (2012), “動態隨機一般均衡在台灣貨幣政策制定上之應用”, 中央銀行季刊, 35(1), 3-34.

Hwang, Y. N. and P. D. McNelis (2015), “Monetary Regimes and Share Price Volatility in East Asia,” Fordham University Schools of Business Research Paper.

Hwang, Y. N. and P. Y. Ho (2012), “Optimal monetary policy for Taiwan: a dynamic stochastic general equilibrium framework,” Academia Economic Papers, 40(4), 447-482.

Kelly, Binner, Chang and Tseng (2014), “Monetary Policy in Taiwan: the Implications of Liquidity,” Handbook of Asian Fiannce, 221-235.

Kollmann, R. (2002), “Monetary policy rules in the open economy: effects on welfare and business cycles,” Journal of Monetary Economics, 49(5), 989-1015.

Kollmann, Robert, Zeno Enders, and Gernot J. Müller (2011), “Global banking and international business cycles,” European Economic Review, 55(3), 407-426.

Liu, Z. and M. M. Spiegel (2015), “Optimal monetary policy and capital account restrictions in a small open economy,” Federal Reserve Bank of San Francisco, Working Paper Series, NO. 2013-33.

Obstfeld, M., J. C. Shambaugh, and A. M. Taylor (2005), “The Trilemma in History: Tradeoffs among Exchange Rates, Monetary Policies, and Capital Mobility,” Review of Economics and

Statistics, 87, 423-438.

Obstfeld, M., J. C. Shambaugh, and A. M. Taylor (2010), “Financial Stability, the Trilemma, and International Reserves,” American Economic Journal: Macroeconomics, 2, 57-94.

Obstfeld, M. and K. Rogoff (2000), “The Six Major Puzzles in International Macroeconomics: Is There a Common Cause?” NBER Macroeconomics Annual, ed. B.S. Bernanke and K. Rogoff, 15, 339-390.

Teo, W. L. (2009), “Estimated dynamic stochastic general equilibrium model of the Taiwanese economy,” Pacific Economic Review, 14(2), 194-231.

國科會補助專題研究計畫項下出席國際學術會議心得報告

日期: 106 年 10 月 15 日

一、參加會議經過

本人於當地時間 11 月 11 日抵達美國紐約,繼又轉機至會議地點 Hilton, Durham, North Carolina

參加會議,於 11 月 13 日下午報告” Implications of the Chinese Monetary Policy Reform: A Dynamic

Stochastic General Equilibrium Approach”一文,會議中就中國經濟改革現況與模型建置與與會專家進

行許多討論。除了全程參與會議之外,並利用會議期間中午、晚餐時間與來自美國各地,如 Arizona State

University 的 Hang Liu、George Mason University 的 Robert Axtell,以及大陸、台灣的學者進行交流。

由於 Durham 該地為美國著名的 research triangle,附近有 North Carolina State University, Duke

University, University of North Carolina at Chapel Hill 等三所知名大學,我便在 11 月 12 日下午與在該

計畫編號

MOST 105-2410-H-004-006 -

計畫名稱

最適貨幣政策協作與景氣循環

出國人員

姓名

黃俞寧

服務機構

及職稱

政治大學經濟系副教授

會議時間

105 年 11 月 11 日至

105 年 11 月 13 日

會議地點

Durham, North Carolina, USA

會議名稱

(中文)

(英文) Duke Forest Conference, 2016 (Economics in the Era of Natural

Computationalism and Big Data)

發表論文

題目

(中文)

(英文)

Implications of the Chinese Monetary Policy Reform: A Dynamic Stochastic General Equilibrium Approach會議地點巧遇、正在參加另一會議的高雄大學王學亮校長與丁一賢國際長一同前往杜克大學參訪。

二、與會心得

此會議為一專門探討大數據、實驗經濟學、computational economics 的研討會,會議中聆聽諸多 學者談論關於大數據的發展、實驗經濟學的演進,收穫甚豐。且由於該會議採取小型、有特定主題的 工作坊形式,與其他學者有更多機會有更進一步的討論與互動。三、考察參觀活動(無是項活動者略)

四、建議

五、攜回資料名稱及內容

六、其他

Welfare Implications of the Chinese Monetary Policy

Reform: A Dynamic Stochastic General Equilibrium

Approach

Yu-Ning Hwang

Department of Economics National Chengchi UniversityOct. 2016

Abstract

In this study, we establish an open-economy DSGE model with the frictional domestic credit market to conduct the welfare analyses of monetary policy reform plans of China. Currently, both the domestic credit market and international capital market are under various regulations. The progress of the gradual removal of these market regulations, which may crucially alter the transmission mechanism of domestic as well as foreign shocks, is important for the economic transformation of the Chinese economy. The welfare analyses generate important policy implications for the progress of policy reforms. The results suggest that, compared with domestic deregulations, opening capital account can be most critical as it makes the international transmission mechanism of shocks feasible.

Keyword : dynamic stochastic general equilibrium (DSGE), Chinese economy, economic transformation

Correspondence: Yu-Ning Hwang, Department of Economics, National Chengchi University, Taipei

105年度專題研究計畫成果彙整表

計畫主持人:黃俞寧 計畫編號: 105-2410-H-004-006-計畫名稱:最適貨幣政策協作與景氣循環 成果項目 量化 單位 質化 (說明:各成果項目請附佐證資料或細 項說明,如期刊名稱、年份、卷期、起 訖頁數、證號...等) 國 內 學術性論文 期刊論文 0 篇 研討會論文 0 專書 0 本 專書論文 0 章 技術報告 0 篇 其他 0 篇 智慧財產權 及成果 專利權 發明專利 申請中 0 件 已獲得 0 新型/設計專利 0 商標權 0 營業秘密 0 積體電路電路布局權 0 著作權 0 品種權 0 其他 0 技術移轉 件數 0 件 收入 0 千元 國 外 學術性論文 期刊論文 0 篇 研討會論文 0 專書 0 本 專書論文 0 章 技術報告 0 篇 其他 0 篇 智慧財產權 及成果 專利權 發明專利 申請中 0 件 已獲得 0 新型/設計專利 0 商標權 0 營業秘密 0 積體電路電路布局權 0 著作權 0 品種權 0 其他 0技術移轉 件數 0 件 收入 0 千元 參 與 計 畫 人 力 本國籍 大專生 0 人次 碩士生 4 協助相關資料收集、文獻回顧與模型建 構 博士生 1 協助模型建構 博士後研究員 0 專任助理 0 非本國籍 大專生 1 協助相關資料收集 碩士生 0 博士生 0 博士後研究員 0 專任助理 0 其他成果 (無法以量化表達之成果如辦理學術活動 、獲得獎項、重要國際合作、研究成果國 際影響力及其他協助產業技術發展之具體 效益事項等,請以文字敘述填列。)