Understanding China

Young-Chan Kim Editor

Chinese Global

Production

Networks in

ASEAN

Young-Chan Kim

Editor

Chinese Global Production

Networks in ASEAN

Editor

Young-Chan Kim

International Business and Economics Business School, University of Greenwich London

United Kingdom

ISSN 2196-3134 ISSN 2196-3142 (electronic) Understanding China

ISBN 978-3-319-24230-9 ISBN 978-3-319-24232-3 (eBook) DOI 10.1007/978-3-319-24232-3

Library of Congress Control Number: 2015958345 Springer Cham Heidelberg New York Dordrecht London © Springer International Publishing Switzerland 2016

This work is subject to copyright. All rights are reserved by the Publisher, whether the whole or part of the material is concerned, specifically the rights of translation, reprinting, reuse of illustrations, recitation, broadcasting, reproduction on microfilms or in any other physical way, and transmission or information storage and retrieval, electronic adaptation, computer software, or by similar or dissimilar methodology now known or hereafter developed.

The use of general descriptive names, registered names, trademarks, service marks, etc. in this publication does not imply, even in the absence of a specific statement, that such names are exempt from the relevant protective laws and regulations and therefore free for general use.

The publisher, the authors and the editors are safe to assume that the advice and information in this book are believed to be true and accurate at the date of publication. Neither the publisher nor the authors or the editors give a warranty, express or implied, with respect to the material contained herein or for any errors or omissions that may have been made.

Printed on acid-free paper

Springer International Publishing AG Switzerland is part of Springer Science+Business Media (www.springer.com)

Tai-shang (Taiwan Business) in Southeast

Asia: Profile and Issues

Alan Hao Yang and Hsin-Huang Michael Hsiao

1

Introduction

The rise of global capitalism has altered the geopolitical and geo-economic land-scapes of nation-states by reshaping the role of transnational actors and enhancing their functions. Much has been discussed on the emerging international connected-ness endorsed by the transnational actors and their networks. For example, the making oftransnational network of advocacy highlights the global concerns of human rights, social equality, and environmental sustainability endorsed by global civil societies and international nongovernmental groups (Rodrigues and Moog

2004; Avant et al. 2010). The transnational network of mobility nourished by immigrants enriches the people-centered connectedness between their mother countries and host societies (Geiger and Pe´coud2013; Biao et al.2013). Neverthe-less, this chapter is more interested in a third type of network,the transnational network of profit, shaped by private sectors. It is a transnational economic cluster intensifying the distribution of labor in global production network, fulfilling the needs of global commodity supply chain, and accumulating the transnational capitals of private sectors in terms of political and economic influence.

By discussing thetransnational network of profit with a specific focus on the role of the overseas Taiwan business in Southeast Asia, it argues that the global rise of overseas Taiwan business, also known by the nameTai-shang, has at least three contributions in the invested countries, that is, the industrial internationalization, capital trans-nationalization, and the facilitation of business and investment

A.H. Yang (*)

Asia-Pacific Division, Institute of International Relations, National Chengchi University, Taipei, Taiwan

e-mail:[email protected]

H.-H.M. Hsiao

Institute of Sociology, Academia Sinica, Taipei, Taiwan e-mail:[email protected]

© Springer International Publishing Switzerland 2016

Y.-C. Kim (ed.),Chinese Global Production Networks in ASEAN, Understanding China, DOI 10.1007/978-3-319-24232-3_11

networks at localities. In effect,Tai-shang’s rising in Southeast Asia is specifically embedded in the intertwined effect from the abovementioned contributions. They cast both economic and political influences in Southeast Asian countries.

First, in respect of industrial internationalization, any domestic industrial sector can no longer maintain autarkic when facing the acceleration of globalization and of regional integration. Consequently, it is “embedded in” the supply chain of global production network. For specific labor-intensive industries such as manufacturing and textiles products, the practice of “internationalization” is a way to maintain competitiveness among others. It is aimed at reducing the cost of production through seeking low cost of raw materials and overseas production bases featured with abundant resources or low-salary employment (McBeath

1999: 106). In this regard, overseas businessmen hence serve as media to push domestic industries outside their home countries.

Second, as for capital trans-nationalization, overseas business communities facilitate the development of bilateral/multilateral trade and investment, bringing external resources to domestic industries. This process implies two flows: to the investing countries, the exploration of overseas business network diversifies the international market while reducing the costs of raw materials and labors for their domestic headquarters; to the invested countries, foreign investors may inject international capitals, encourages new technological incorporation, creat employ-ment opporunities and human capitals—those imported fiscal and human capitals as well as technological spillovers, moreover, contribute to local economic growth (Kotrajaras et al.2011: 184).

Third, with the investment from overseas businessmen, it is plausible to help connect transnational business network bilaterally and regionally. By creating new production supply chain, ethnic business unions, and even the political-business ties, these transnational economic actors do not only operate lucrative activities but also act as interest groups to generate socioeconomic capacity to influence the government of host countries. Take China for example. Over the past years, China’s outbound investment has hit the record high, ranking as the third leading inves-tor throughout the world (Pitlo2015). Its state-owned enterprises (SOEs)per se as major contributors to critical infrastructures and public construction projects are not only seeking for economic benefits but working as the government outreach indirectly engaging in promoting bilateral political relations. Even those local SOEs with abundant resources enjoy more flexibility in pursuing international venturing with local companies and firms (Li et al. 2014: 996). Unlike these SOEs, small and medium enterprises (SMEs), though not directly supported by the government from mother countries, mostly have profound influence over the general public of the host countries.

For decades, the economic development in Southeast Asia has been shaped by enterprises from its Northeast Asian counterparts (Machado2003; Harwit2013). Up to the present, China’s business seems to exercise preponderant influence in Southeast Asia (Suryadinata2006,2007; Lee2014). China dispatches its SOEs to Southeast Asia, allowing these economic outreaches to execute its “Going Out Strategy” in deepening business networks at localities. For years, these Chinese enterprises have intensively collaborated with Southeast Asian governments by investing in critical

infrastructure such as railroads, highways, dams, and hydropower plants. In additions, these government-supported business groups actively interact with local overseas Chinese for the purpose of amplifying the profits.

Prior to the rise of Chinese SOEs in the region, the overseas Taiwan business (shang) appeared in Southeast Asia during the 1970s and 1980s, as the Tai-wanese economy grew with fast speed, spilling its economic influence over neigh-borhood countries. People often attribute overseas Taiwan business in the same category of those from China; nevertheless, we argue that the two groups have a distinct culture, identity, acumen, and strategy.

Tai-shang earned full international attention during the anti-China demonstra-tion in Vietnam on May 13, 2014 (known as the 513 incident). Under the author-itarian regime, organizing large-scale riot against foreign enterprises is rare in Vietnam. During the 513 incident, Tai-shang became a target of Vietnamese mobs; according to some international news reports, the Vietnamese demonstrators confused the Taiwanese enterprises with the Chinese ones, as both of their brands are marked in Chinese (Yu2014). However, this explanation is not pertinent for the Vietnamese society has been acquainted withTai-shang for decades. We argue that Tai-shang were served as scapegoats during the 513 anti-China riot due to the evasion of the Vietnamese government to directly challenge Beijing. Consequently, this incident again gave rise to the international concern on the contribution of Tai-shang in the region as well as its distinction from China.

Accordingly, this chapter sheds light on the presence ofTai-shang in Southeast Asia via four parts. The first part distinguishes China business and Taiwan business. The second part deals with incentives of Taiwanese investment in Southeast Asia. Then, this chapter will discuss the role of Tai-shang in regional integration of Southeast Asia. It proceeds to the survey of national profiles of Taiwan business in the region. Finally, the conclusion sums up the discussions by evaluating the contributions of and challenges facing Taiwan business in the region.

2

Comparing China and Taiwan Business

in Southeast Asia

Historically, the ethnic Chinese businessmen have long been regarded as the leading player in shaping Asia’s internal economic networks and trade links (Ptak

1999, 2004; Souza 2014). Even today, overseas Chinese are still dominant in economic and development agenda in most Southeast Asian countries based upon the individual family-based enterprises and related Chinese business networks (Folk and Jomo2003: 3). The People’s Republic of China’s rising further consol-idates this phenomenon as there are more and more businesses dispatching from China to Southeast Asia. Increasing amount of Sino–Southeast Asian trade from USD20 billion of 1995 to USD480.39 billion of 2013 justifies the upgrading relation from “the golden decade” (黃金十年) to “the diamond decade” (鑽石十年), a term invented by the Chinese Premier Li Keqiang in 2013 (ASEAN-China Center2015).

Such an acceleration can be regarded as the fast-growing influence of the Chinese government and its business in the region.

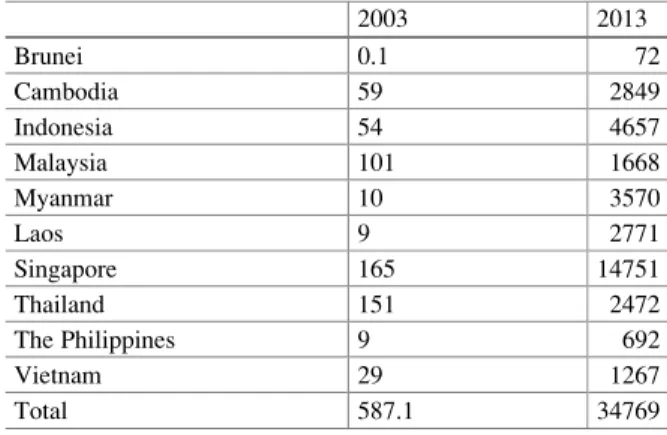

In 2014, China’s foreign exchange reserve has reached USD4.06 trillion, which puts China on the top of the world ranking. Meanwhile, China’s business continues to seek collaborations worldwide by promoting its state capitalism overseas. One may find the domestic configuration of state capitalism, known as a solid alliance between the Chinese government and its SOEs, operating in line with rent-seeking modalities. The foreign investment pattern of China is also duplicating this “China Model” (中國模式) to consolidate the alliance between the Chinese government and its overseas business groups shown as the complex of wealth and power (Callahan2013: 66–97). Moreover, China’s businesses, most of which are SOEs, are the overseas outreaches of Beijing’s “Going Out Strategy” by dedicating themselves in investing in its neighbors and beyond (Shambaugh2013: 174–175). In 2003, the amount of Chinese FDI in ASEAN countries is USD587.1 million, while in 2013, the amount had exceeded to USD34 billion (Table1).

Beijing has been actively engaging in global merger and acquisition (M&A) for years, targeting at grasping natural resources and technology-intensive industries (Pitlo2015). For instance, China business exerts political and economic influences in Southeast Asian countries by purchasing or merging companies, allying with local governments, or by monopolizing scarce resources such as potassium salt mine in Thailand and copper in Myanmar. In other words, China’s businessmen do not only pursue economic profits but also undertake strategic mission on behalf of their government. They become policy instruments to either strengthen national compet-itiveness or secure significant resources overseas (Li et al.2014: 989).

Different to overseas China business, the overseas Taiwan business (Tai-shang) manifests very different dynamics.Tai-shang went abroad for investment in the early 1970s and 1980s, most of which were original equipment manufacturer (OEM). Being the ruling regime of Taiwan, Kuomintang (KMT) inherited monop-olistic industries from Japanese colonialism. Those colonial legacies, including finance, energy, communication, and transportation sectors, were mostly transfused to KMT-led SOEs.Tai-shang were pressed by the expensive costs of production

Table 1 Chinese FDI in ASEAN countries: a comparison (USD millions)

2003 2013 Brunei 0.1 72 Cambodia 59 2849 Indonesia 54 4657 Malaysia 101 1668 Myanmar 10 3570 Laos 9 2771 Singapore 165 14751 Thailand 151 2472 The Philippines 9 692 Vietnam 29 1267 Total 587.1 34769

Source: Salidjanova et al. (2015: 7)

following the government’s lift of control over foreign exchange and the country’s fast-growing economy. They were also pushed by the rising domestic wage rate due to a significant appreciation of the New Taiwan Dollar (NTD) (McBeath 1999: 107). Those first to move outside the country were “declining industries” (夕陽產業) since they encountered the most challenges brought about by domestic social economic structure centralized by KMT.

Consequently, cheap costs of production and low wage in Southeast Asia caught the attention of Tai-shang. Once settled, Taiwan business invested and manufactured products made of textile, timber, metal, and electrics before exporting the products to the West and other countries. In the 1970s and 1980s, these SMEs did not benefit financial support from the Taiwanese government, nor did they have well-structured institution and fiscal capacity as large corporations. However, it was common to see some Taiwan business setting up branches illegally in Southeast Asia without the Taiwanese government’s permission (Interview

2015a). By all means, these Taiwanese SMEs were so mobile and independent that they succeeded to adapt themselves in Southeast Asia and generally entertain good ties with the local governments (Interview2012).

The “Go South Policy” (南向政策) was implemented by KMT regime under President Lee Teng-hui in 1994. It was a policy aiming to counterbalance Taiwan over investment in China. Since its “reform and opening” (改革開放) policy of 1978, China has been pushing for economic growth, making its market attractive to foreign investment. Initially, Tai-shang followed this trend and has enjoyed the advantages of culture and language affinity comparing to other foreign investors. However, the political tension between Taiwan and China also perpetuated. Pres-ident Lee Teng-hui hence exhortedTai-shang to shift their attentions and interest to Southeast Asia in order to neutralize the “magnet effect” (磁吸效應) of the Chinese economy to avoid over economic dependence of Taiwan.

It is also true that this “Go South Policy” was embedded with political implica-tion—boosting Taiwan–Southeast Asian relations in order to break through Taiwan’s diplomatic deadlock. Therefore, the Policy was regarded as the govern-ment push for KMT-led SOEs and private business to seek investgovern-ment projects in Southeast Asia, for example, Taiwan Salt Corporation, known as Taiyen, was pushed by the Ministry of Economic Affairs to collaborate with Indonesian coun-terparts and CPC Corporation to explore oil and gas projects in Indonesia, while Taiwan Sugar Corporation was persuaded to facilitate bilateral cooperation on sugar production in Vietnam (Hsiao and Kung 2002: 18). These governmental facilitations are rather strategic and political oriented, resulting in thousands of Taiwan business, most of which are SMEs, to invest in Southeast Asia.

3

Why Investing Southeast Asia?

From the perspective of geopolitics and geo-economics, the rise of Tai-shang in Southeast Asia reflects its strategic preferences. First, in terms of geography, Taiwan is relatively close to Southeast Asia, or we should say, located in Southeast

Asia. This geographical advantage facilitates the mobility of people between two sides. It takes less than 5 hours forTai-shang to fly to any capital cities in Southeast Asian countries from Taipei and then access to specific economic zone nearby. Moreover, it takes only a few hours forTai-shang in Southeast Asia to connect to neighboring countries, including China.

In terms of culture, Southeast Asian countries such as Thailand, Vietnam, and Singapore have long been influenced by Confucianism. This cultural affinity may reduce the gap between Taiwan business and Southeast Asian counterparts. It is easy forTai-shang in Southeast Asia to adapt to local societies than those in Latin America and the United States. Even to Muslim countries such as Indonesia and Malaysia, local societies are familiar with Chinese culture thanks to the presence of early ethnic Chinese immigrants and overseas Chinese businessmen, as “intermediaries” (McBeath1999: 123), providing a rather friendly environment forTai-shang.

In effect, the key reason for private entrepreneurs of choosing Southeast Asia as destination of investment is still economic. Taiwan business was attracted by rich resources and abundant young labors with low salaries in Indonesia, Malaysia, and Thailand. Since most of SMEs in Taiwan were labor-intensive and export-oriented industries, Southeast Asia was of specific incentive forTai-shang.

Finally, all Southeast Asian countries have experienced state-building processes. While striving for independence and national development, most of the new regimes were in need of foreign investments and economic inputs from major economies for the purpose of boosting economic growth and legitimizing their ruling. As a result, central and local elites in Southeast Asian countries mostly supportedTai-shang’s presence in their national economic agenda (Interview2012;

2015a). This enabled Taiwan to surpass NIEs, such as Hong Kong, South Korea, Singapore, when it comes to foreign investment in Southeast Asia.

All of the above reasons had stimulated many Taiwan businesses, the SMEs, to strategically move to Southeast Asia as early as the 1970s. To cope with regional and national dynamics in Southeast Asia, there was a second wave of investment in Southeast Asia. The SOEs and KMT-led corporation adopted new strategies that have paid more attention to local and regional markets, instead of emphasizing purely on export. Indeed, the integration progress of Association of Southeast Asian Nations (ASEAN) was equivalent to a market of 560 million people, providing more incentives forTai-shang.

4

The Rise of Tai-shang in ASEAN Economic Integration

The rise of Tai-shang corresponds to the process of economic integration in contemporary Southeast Asia. As ASEAN was established in 1967, this intergov-ernmental organization was aimed at promoting multilateral collaboration in eco-nomic development and sociocultural exchanges. Nonetheless, the lack of mutual trust hindered its member states from implementing joint economic undertakings (Ba2009). Until the 1970s, as ASEAN members agreed upon ASEAN Industrial Project (1976) and ASEAN Preferential Trading Arrangement (1977), a gradual

progress of economic integration had begun to commence. The presence of Tai-shang in ASEAN industries was mostly investing in food manufacturing and textile mills with specific focus on raw materials at localities.

In 1981, the ASEAN Industrial Complementation Scheme was declared. The industrial development became the key to economic growth to the region. The 1980s had also marked an era of domestic economic reforms among major Southeast Asian countries. Policy reforms and industrial projects promoted by governments in Malaysia, Indonesia, Singapore, Thailand, and Vietnam were targeting at attracting more foreign direct investments (FDIs), further triggering domestic and regional growth. Meanwhile, the rise of environmental awareness as well as the increase of wage in Taiwan became the domestic push forTai-shang to seek overseas produc-tion bases in the region. Increasing number of Taiwanese SMEs moved to Southeast Asia, mostly in Indonesia, Malaysia, Thailand, and the Philippines.

It was the promotion of free trade agenda, such as Common Effective Preferen-tial Tariffs (CEPT) and the making of ASEAN Free Trade Agreement (AFTA), which speeded up ASEAN economic integration in the 1990s. As clearly stated in ASEAN Vision 2020, ASEAN countries determined to (1) fully implement the AFTA and accelerate liberalization of trade in services, (2) realize the ASEAN Investment Area (AIA) and promote free investment flows, (3) intensify and expand subregional cooperation in existing and new subregional growth areas, (4) further consolidate and expand extra-ASEAN regional linkages for mutual benefit and cooperate to strengthen the multilateral trading system, and (5) reinforce the role of the business sector as the engine of growth (ASEAN1997). The new roadmap of Southeast Asian integration revealed an urgent need for external supports in terms of economic and investment inputs.

Against the backdrop, the KMT government in Taiwan began to advocate “Go South Policy” in the beginning of the 1990s. The Policy encouragedTai-shang to invest in Southeast Asia, the political purpose of which was to counterbalance the increasing investment flows toward China. The first term of “Go South Policy” was drafted as “the Guideline on Enhancing Economic and Trade Relations with South-east Asia” (加強對東南亞地區經貿工作綱領) which commenced in March 1994 and ended in December 1996. Brunei Darussalam, Indonesia, Malaysia, Singapore, Thailand, the Philippines, and Vietnam were the geographic foci. An expanded version had been advocated later in 1997 as “the Guideline on Enhancing Economic and Trade Relations with Southeast Asia, Australia, and New Zealand” (加強對東南 亞及紐澳地區經貿工作綱領) with the full coverage of all Southeast Asian coun-tries. As Asian financial crisis hit the region, Taiwan immediately supported a sub-regional proposal initiated by the Asian Development Bank and regional coun-tries such as Japan and Singapore to provide necessary short-term currency and exchange assistance to Southeast Asian countries (McBeath1999: 124). In 1998, Taipei announced a follow-up policy of “Concrete Measures on Plan of Action of Enhancing Southeast Asian Economic and Trade Cooperation” (加強推動東南亞經 貿行動方案具體措施), showing its political will to engage AFTA as well as the contenious governmental support toTai-shang in Southeast Asia. During 1993–2000, Taiwan business investment in Southeast Asia has exceeded USD44.8 billion with the average annual growth rate of 53.5 % (Ministry of Economic Affairs2001: 4).

When it came to 2003, the proposal of ASEAN Community envisaged by the Bali Concord II was adopted. A new vision of ASEAN Economic Community (AEC) aimed to transform Southeast Asia into a single market and integrated production base. The construction of AEC, for sure, is simultaneously embedded in the global free trade networks as well as in the regional dependency politics on China’s rising. China–ASEAN Free Trade Area (CAFTA), Regional Comprehen-sive Economic Partnership (RCEP), and the gradual realization of the Master Plan of ASEAN Connectivity later in 2010 facilitate a further constructed and interconnected Southeast Asia.

However, it is also true that Taiwan has been excluded from these active promotion of regional and bilateral FTA by ASEAN and regional powers such as China, Japan, and Korea. These intricate FTA network and business links will seriously disadvantage and challenge Tai-Shang due to higher import tariffs and market barriers (Zhao2011: 48). In this regard, Taipei turns to enhance its policy to seek for opportunities of signing economic cooperation agreement (ECA) with neighboring countries by activating joint feasibility studies with ASEAN counter-parts such as Indonesia, Malaysia, Thailand, the Philippines, and Vietnam. “Agree-ment between Singapore and the Separate Customs Territory of Taiwan, Penghu, Kinmen, and Matsu on Economic Partnership (ASTEP)” signed in November 2013 is one of the achievement between Taiwan and Singapore. It is believed that by pushing bilateral ECA with Southeast Asian counterparts, Tai-shang would be expecting to accelerate its integration in line with AEC and regional FTA networks.

5

Tai-shang in Southeast Asia: National Profiles

During the past decades, Taiwan business pays much attention to Indonesia, Malay-sia, Singapore, and Thailand, but less focus on those Indochinese countries such as Cambodia, Laos, and Myanmar due to their domestic political instability. The general investment pattern ofTai-shang is to establish production base at Southeast Asian countries, import machine components from Taiwan to the invested countries, and manufacture final products at localities, and then export to the United States, European countries as well as Taiwan (Yeh and Huang2015: 313). As ASEAN is rising as a single market, local Taiwanese investment has been shifted from export orientation to fulfill the domestic market and intra-regional needs.

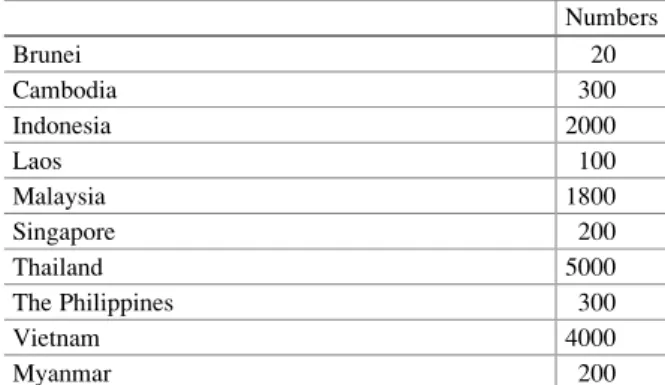

There is no official statistics on the number of Taiwan business in Southeast Asian countries due to some enterprises are registered as local companies but owned by Tai-shang. According to various sources of Taiwan’s Ministry of Eco-nomic Affairs and our fieldworks and interviews with Taiwanese business groups in Vietnam (Interview2015b), Malaysia (Interview 2015a), Laos (Interview 2013), Cambodia (Interview2012), and Thailand (Interview2015c), it is estimated that there are 5000 Taiwan companies in Thailand, 4000 in Vietnam, 2000 in Indonesia, and 1800 in Malaysia, while there are only 20 in Brunei (Table2).

Regarding the investment volume, Table3shows from 1952 to 2013, Vietnam prioritized No. 1 in Taiwan’s FDI in Southeast Asia with the amount of USD272.5 billion as 33.5 % of Taiwan’s investment in Southeast Asia. Indonesia came the second with the amount of USD153.6 billion as 18.9 %. Then, Thailand was in the third place with USD134.5 billion as 16.5 % (Table3).

The year of 2000 witnessed domestic regime change in Taiwan as KMT gov-ernment was replaced by the Democratic Progressive Party (DPP). As President Chen Shui-bian came into power, strategic focus of “Go South Policy” had been directed to tackle with challenges of Taiwanese investment in Southeast Asia with special focus on ICT and textile mill industries. DPP government re-announced Indonesia, Malaysia, Singapore, the Philippines, and Vietnam as key countries for Taiwan’s investment. Clearly, the new waves of “Go South Policy” was designed to counterbalance Taiwanese increasing investment in China. By pushing China Steel, Formosa Plastics Group, Uni-President and Pou Chen Group to Vietnam, Taiwan-ese government desired to constructively engage Southeast Asian markets and governments. While KMT reclaimed power in 2008, Southeast Asia was still of strategic interest to Taiwan, with more focus on promoting ECA with regional counterparts. Since 2000,Tai-shang significantly modified its investment strate-gies; Vietnam became the most favored investment destination of Taiwan business, followed by Singapore and Thailand. Also, there are increasing investment projects in Indochinese countries, especially Myanmar. The following discussion surveys national profiles of Tai-shang in Indonesia, Thailand, Malaysia, Vietnam, the

Table 2 Tai-shang in key

ASEAN countries Numbers

Brunei 20 Cambodia 300 Indonesia 2000 Laos 100 Malaysia 1800 Singapore 200 Thailand 5000 The Philippines 300 Vietnam 4000 Myanmar 200

Source: various sources

Table 3 Taiwanese FDI in ASEAN countries (1952–2013) (USD billions) Amount Percentage Cambodia 10.2 1.2 Indonesia 153.6 18.9 Malaysia 116.1 14.2 Singapore 106.1 13 Thailand 134.5 16.5 The Philippines 20.9 2.5 Vietnam 272.5 33.5

Source: Ministry of Economic Affairs (R.O.C.) (2014: 3) Tai-shang (Taiwan Business) in Southeast Asia: Profile and Issues 221

Philippines, Singapore, Cambodia, and Myanmar, based on trade and investment statistics of Taiwan’s Ministry of Economic Affairs and the authors’ interviews.

5.1

Indonesia

Interestingly, the year of 2000 can be regarded as a watershed in the development of Taiwan business in Southeast Asia. Before 2000, Tai-shang invested the most in Indonesia with 855 projects worth of USD12.77 billion (Table4). This was because Indonesia was rich of natural and human resources. Accordingly, factories set up by Tai-shang were mostly labor-intensive and resource-oriented industries such as pulp and paper, textile, and mining. For example, Taiwan helped establish industrial park in Batam Island in 1990. In 1996, Taiwan’s leading SOE, China Petroleum, also invested in energy exploration and development, In 1997 and 1998, Taiwanese outbound investment in Indonesia reached USD3.4 billions and USD2.2 billions respectively (McBeath 1999: 121–122). As the Indonesian government continues encouraging foreign investment in local infrastructure and labor-intensive industries, it is still popular to Taiwan business during 2001–2014. Tai-shang continuously contributes 770 projects (No. 2) as USD3.9 billion (No. 3) in Indonesia (Table5).

Table 4 Taiwanese investment in key ASEAN countries (1948–2000) (USD millions) Project/rank Amount/rank Cambodia 168 (7) 427.52 (7) Indonesia 855 (3) 12,774.15 (1) Malaysia 1786 (1) 9225.66 (3) Singapore 316 (6) 1391 (5) Thailand 1553 (2) 10,351 (2) The Philippines 824 (4) 982.08 (6) Vietnam 524 (5) 5202.48 (4) Source: compiled by the authors with reference to BOI (Thailand), MIDA (Malaysia), NSCB (the Philippines), BKPM (Indonesia), MPI (Vietnam), CIB (Cambodia), and MOEA (Taiwan)

Table 5 Taiwanese investment in key ASEAN countries (2001–2014.6) (USD millions) Project/rank Amount/rank Cambodia 318 (5) 610.12 (7) Indonesia 770 (2) 3910.79 (3) Malaysia 644 (4) 2539.48 (5) Singapore 206 (7) 9537.26 (2) Thailand 648 (3) 3146.72 (4) The Philippines 232 (6) 1124.2 (6) Vietnam 2320 (1) 22,408.61 (1) Source: compiled by the authors with reference to BOI (Thailand), MIDA (Malaysia), NSCB (the Philippines), BKPM (Indonesia), MPI (Vietnam), CIB (Cambodia), and MOEA (Taiwan)

In recent years, in addition to Foxconn’s great interest in telecommunication sec-tors,Tai-shang has also paid more attention to Indonesian domestic market as this emerging economy is rising.

5.2

Thailand

Thailand was the second investment destination ofTai-shang before 2000. How-ever, being suffered by Asian financial crisis, Taiwanese outbound investment in Thailand decreased in the late 1990s. Among 1553 projects in operation,Tai-shang had invested USD10.35 billion in Thailand. Cultural similarity and societal hospi-tality constitute two important factors forTai-shang to invest in Thailand. Up to 2015, it is estimated that there are at least 5000Tai-shang stationing in Thailand, some of them are operating by their second generation, conducting a more localized strategy (Interview2015c). Taiwan business considered Thailand as the base for developing a variety of businesses ranging from basic iron and steel manufacturing to SMEs as human resources, chemistry, electronics, textile mills, food manufactur-ing, and service industries. New domestic needs concentrate on service industries which attract new type of Tai-shang to Thailand. During 2001–2014, Taiwan business launched 648 projects (No. 3) worth of USD3.1 billion (No. 4) in Thailand. While Myanmar is lifting domestic regulation to foreign investment, along with the rise of wage and political instability in Thailand, increasing number of Tai-shang considers to invest in Myanmar. Nevertheless, as Thailand enjoys various FTA with major economies in Asia-Pacific and beyond, the overall invest-ment environinvest-ment it is still attractive and favored by Taiwan business.

5.3

Malaysia

Tai-shang had invested the most projects in number in Malaysia (1786 projects as USD9.22 billion), making Malaysia as the third investment destination in Southeast Asia before 2000. Well-developed infrastructure and clearly defined regulations for foreign investment were advantages of Malaysia. In addition, theTai-shang were attracted by abundant natural resources and a stable political situation in Malaysia. Therefore, increasing investments were contributing to machinery and equipment manufacturing, electronic parts and components manufacturing, textile mills, and banking and insurance since 1988. However, the lack of labor force in 1994 and the Asian financial crisis in 1997 diversified Taiwanese investments from Malaysia to Vietnam and China. The changing focus of Taiwanese investment in Malaysia also highlights a shift from textile mills and manufacturing sectors to financial service one. According to Taiwan’s Ministry of Economic Affairs, more than 70 % of Taiwanese FDI are targeting at domestic financial service sector (Yeh and Huang

2015: 317). Currently, Tai-shang reinforces investments in service sector and

catering industry as a result of the government policy on promoting service industries (Interview2015a). From 2001 to 2014, Tai-shang contribute 644 projects (No. 4) as USD2.5 billion in Malaysia, with a specific focus on basic metal manufacturing.

5.4

Vietnam

Before 2000, Vietnam only attracted 524 investment projects (No. 4) with the amount of USD5.2 billion (No. 5) from Taiwan. Since the 1980s, Vietnamese government welcomed Taiwanese investment and its first economic and cultural office, known as informal embassy, was installed in Hanoi in 1992 (Leifer2001: 181). With the continuous support of “Go South Policy,” Vietnam became No. 1 investment destination for Taiwan business in Southeast Asia in the 2000s. During 2001–2014, there were 2320 projects (No. 1) and USD22 billion instilling in Vietnam. A variety of SMEs, such as wearing apparel and clothing accessories manufacturing, electronic parts and components manufacturing, furniture, tourism, as well as banking and financing, are stationing in Vietnam for decades. Up to 2015, Taiwan ranks as No.4 foreign investor in Vietnam. Tai-shang are mostly stationing in the South surrounding Ho Chi Minh city. After 513 accident happened in 2014, Vietnamese government scrutinized foreign investment regulation and policy, providing more business incentive and favors for loclaTai-shang. The purpose is to keep Taiwanese investment at localities. Other than SMEs, ICT industries, such as Formosa Ha Tinh Steel Corporation (FHS) also invests new plant at Vung Ang Economic Industrial Zone in Ha Tinh.

5.5

The Philippines

Taiwan business invested 824 projects as USD982 million in the Philippines before 2000, focusing on manufacturing, textile mills, electronic parts and com-ponents manufacturing, and computer, electronic, and optical products manufacturing. Recent trend shows increasing investment has been contributed in fabricated metal products manufacturing. In 2006, as Taiwan and the Philip-pines signed a memorandum of understanding (MOU) with regard to the con-struction of economic corridor by the Subic Bay Metropolitan Authority (SBMA) and the Clark Development Corp. (CDC) of the Philippines and the Export Processing Zone Administration of Taiwan (Go2006), a wider range of industries had been invested in the bay area such as motor vehicles and parts manufacturing, electronic parts and components manufacturing, chemical material manufactur-ing, food processmanufactur-ing, banking and insurance, and shipping industry. From 2001 to 2014, Tai-shang has contributed 232 projects (No. 6) worth of USD1.1 billion in the Philippines.

5.6

Singapore

Singapore is of strategic interest toTai-shang in terms of geo-economic consider-ation and skilled labor. In terms of geography, Singapore is acting as a Asia-Pacific financial and economic center, attracting various headquarters of multinational corporations to station in. Taiwanese companies such as China Airline and Eva Air, for example, consider Singapore as their regional hubs. With regard to skilled labor, Taiwan’s leading semiconductor foundries, TSMC and UMC, had established plants in Singapore. Before 2000, there were 316 projects as USD1.3 billion invested by Taiwan business in Singapore, including manufacturing, elec-tronic parts and components manufacturing, and banking and insurance. In recent years, domestic banks in Taiwan also set up branches in Singapore, such as the Bank of Taiwan, First Bank, CTBC Bank, Mega Bank, E. Sun Bank and etc. During 2001–2014, Singapore attracted 206 investment projects (No. 7) from Taiwan with the amount of USD9.5 billion (No. 2). The signing of ASTEP in 2013 further enhances Taiwan-Singapore economic and trade cooperation. ASTEP has been regarded as a cornerstone for Taiwan’s forthcoming engaging in the Trans-Pacific Partnership (TPP) led by the United States and the Regional Comprehensive Economic Partnership (RCEP) led by ASEAN.

5.7

Cambodia

Taiwan had 168 investment projects worth of USD427 million in Cambodia before 2000. These projects specifically focused on textile products manufacturing and shoemaking industry. During 2001–2014, 318 projects (No. 5) as USD610 million (No. 7) were invested by Taiwan business. A special initiative is the Manhattan Special Economic Zone (MSEZ) located at the borderland between Cambodia and Vietnam. MSEZ was the first special economic zone in Cambodia, initiated and operated by Tai-shang, the Manhattan International Co., Ltd. (MIC). More than 50 % of enterprises in MSEZ are from Taiwan, including SHEICO, Towa, and Kingmaker Footwear. In addition to the development of special economic zone, real estate has recently been of specific interest of localTai-shang competing with China, Korea, and Japan, as the Cambodian government is promoting urbanization and market liberalization in Phnom Penh (Interview2012).

5.8

Myanmar

Due to political constraints and the Burmese government’s “One China Policy,” Taiwan business was not allowed to invest in Myanmar. Most of Tai-shang, therefore, were from Cambodia and Vietnam to invest in manufacturing,

agriculture, shoemaking, banking and financing, and joint venture in industrial park (Interview2013). However, Taiwanese government began to promote investment in Myanmar since 2012, regarding Myanmar as a new frontier of Tai-shang. In 2013, the DICA of Myanmar government has approved the investment status of Taiwan business. Accordingly, an overseas office of the Taiwan External Trade Development Council has been installed in Yangon for the purpose of promoting FDI in the country. A recent project has been developed by the Taiwan Electrical and Electronic Manufacturers’ Association (TEEMA), with specific focus on the proposal of building an industrial park in Southern Myanmar. Although Myanmar has been regarded as a rising economy and emerging market, its domestical political instability, the poor quality of infrastructure, and its closer relationship with China are the main concerns hindering Taiwanese investment. Up to 2015, Taiwan business such as Taiwan Hon Chuan Group, Pou Chen Group, and Asia Optical kick off the investment project and new producion line. In order to attract more Taiwanese foreign investment, Myanmar Trade Office has been installed in Taipei in June 2015.

6

Conclusion: Tai-Shang

’s Contributions and Challenges

As one of the earliest foreign investors in Southeast Asia, Taiwan business has at least made five contributions to Southeast Asian countries and to Taiwan as well. First, in terms of economic growth, the investment from Tai-shang has helped increase GDP of many host countries. For example, the contribution of FDI to Vietnam’s GDP increased from 2.1 % in 1989 to 18.7 % in 2008. Moreover, the contribution of Taiwan business in developing countries in Southeast Asia also met the strategic goal of narrowing the developmental gap among ASEAN states.

Second, in terms of regional production network, the active presence of Tai-shang in Southeast Asia has facilitated the global–regional–local nexus of produc-tion chain, especially in textiles, ICT, and electronics manufacturing.

Third, the increasing volume of Taiwanese investments also promoted bilateral trade between Taiwan and Southeast Asian countries. More open international markets have been favorable for both Taiwan and its Southeast Asian counter-parts. The even closer economic ties between Taiwan and Southeast Asia facilitated by Tai-shang would definitely contribute to Taiwan’s further engagement in regional grouping and trade integration despite of its political predicament set by China.

Fourth, in terms of labor market, ten thousands ofTai-shang stationing physi-cally in Southeast Asia are mostly SMEs. They have been providing millions of job opportunities for local people, training them become skilled labors.

Most importantly, Tai-shang has facilitated political interconnectedness between Taiwan and Southeast Asia. The economic corridor between Taiwan and the Philippines and the Taiwan Industrial Park in Hanoi are showcasing positive relationships between Taiwan and Southeast Asian governments. Economic

projects are maneuvered as the only means of engaging ASEAN under the political constraint of “One China Policy” partially upheld by China.

During the past decades, structural changes in Southeast Asia brought new challenges to Taiwan business, such as Asian financial crisis, anti-Chinese move-ments, underdeveloped infrastructure at localities, rising environmental concerns, and the difficult labor management issues. These setbacks once discouraged Tai-wanese investors to engage in Southeast Asia. However, as ASEAN Community is in the making and the domestic legalization of employment contract law in China has been implemented, quite a number ofTai-shang have begun either to shift their branches to Southeast Asia or even moved to Southeast Asian countries all together.

Meanwhile, as Southeast Asia is of importance politically and economically, new challenges faced byTai-shang are also the challenges to Taiwan. First, a more sophisticated investment arrangement should be taken into account in line with ASEAN economic integration and its regional trade agreement (RTA) initiatives. It is imperative for the new generation of Tai-shang to incorporate the benefits of AEC into its roadmap of internationalization.

Second, an enhanced public–private partnership (PPP) between the Taiwanese government and Taiwan business should be practiced in implementing “Go South Policy.” The lack of cross-sectorial coordination mechanism as the setback for Tai-shang should also be avoided. In September 2015, as the DPP Chairperson Tsai Ing-wen announces her “New Go South Policy” (新南向政策), it has been regarded as a multi-faceted impetus to Taiwan’s further regionalization and globalization. Also, the emerging policy initiatives and discourses showcase Taiwan’s concerns for being a part of regional grouping. New elements will be added based upon an enhanced PPP to further integrate Taiwan into Southeast Asian localities whereTai-shang will be the key intermediators to facilitate Taiwan’s integration into the region.

Third, a higher standard of investment should be considered. The rise of envi-ronmental concerns and social justice for labor rights have long been ignored in Tai-shang in Southeast Asia. It is necessary for Tai-shang to respond and adapt to new standard and regulations of host societies.

Fourth, industrial upgradation is inevitable. Taiwan’s long-term benefits gained from OEM and ODM in global production network have been undermined due to its shirking interest. Facing this challenge, Taiwan business should emphasize its Taiwanese branding and localize in ASEAN market.

Finally, moving fromTai-shang 1.0 toward Tai-shang 2.0 needs more strategic alliance and international collaboration. As proposed by Japanese and Korean enterprises and their governments in Southeast Asia, a new generation of Tai-shang should seek for long-term cooperations with other foreign investors so as to consolidate the production network and to work closely to improve investment environment of host countries.

References

ASEAN (1997) ASEAN vision 2020. ASEAN. http://www.asean.org/news/item/asean-vision-2020

ASEAN-China Center (2015) ASEAN-China relations. ASEAN-China Center, Apr 2015.http:// www.asean-china-center.org/english/2015-04/13/c_13365143.htm

Avant D, Finnemore M, Sell SK (eds) (2010) Who governs the globe? Cambridge University Press, New York

Ba AD (2009) (Re)negotiating East and Southeast Asia: region, regionalism, and the association of Southeast Asian Nations. Stanford University Press, Stanford, CA

Biao X, Yeoh BSA, Toyota M (eds) (2013) Return: nationalizing transnational mobility in Asia. Duke University Press, Durham

Callahan WA (2013) China dreams: 20 visions of the future. Oxford University Press, New York Folk BC, Jomo KS (2003) Introduction. In: Jomo KS, Folk BC (eds) Ethnic business: Chinese

capitalism in Southeast Asia. RoutledgeCurzon, London, pp 1–24

Geiger M, Pe´coud A (eds) (2013) Disciplining the transnational mobility of people. Palgrave Macmillan, Basingstoke

Go MV (2006) Taiwan pushes for more access to RP market. PhilStar, 21 Oct 2006.http://www. philstar.com/business/364135/taiwan-pushes-more-access-rp-market

Harwit E (2013) Chinese and Japanese investment in Southeast and South Asia: case studies of the electronics and automobile industries. Pac Rev 26(4):361–383

Hsiao H-HM, Kung I-C (2002) History, character and future development of Taiwanese business. In: Hsiao H-HM, Wang H-Z, Kung I-C (eds) Taiwanese business in Southeast Asia: network, identity and globalization. Asia-Pacific Research Program, Academia Sinica, Taiwan, pp 11–32

Interview (2012) Former president, Taiwanese business association in Cambodia. Phnom Penh, 12 Dec 2012

Interview (2013) Taiwanese businessman. Vientiane, 20 July 2013

Interview (2015a) Former president, Taiwanese business association in Malaysia. Kula Lumpur, 4 June 2015

Interview (2015b) Taiwanese businessman. Hanoi, 4 Aug 2015 Interview (2015c) Investment officer of Thailand. Taipei, 12 June 2015

Kotrajaras P, Tubtimtong B, Wiboonchutikula P (2011) Does FDI enhance economic growth? New evidence from East Asia. ASEAN Econ Bull 28(2):183–202

Lee KC (2014) Golden dragon and purple phoenix: the Chinese and their multi-ethnic descendants in Southeast Asia. World Scientific, Singapore

Leifer M (2001) Taiwan and South-East Asia: the limits to pragmatic diplomacy. China Q 165:173–185

Li MH, Cui L, Lu J (2014) Varieties in state capitalism: outward FDI strategies of central and local state-owned enterprises from emerging economy countries. J Int Bus Stud 45:980–1004 Machado KG (2003) Japanese transnational production networks and ethnic Chinese business

networks in East Asia. In: Jomo KS, Folk BC (eds) Ethnic business: Chinese capitalism in Southeast Asia. RoutledgeCurzon, London, pp 213–236

McBeath GA (1999) Foreign direct investment (FDI) management and economic crisis in Asia: Taiwan’s changing strategy. Manage Int Rev 39:105–135

Ministry of Economic Affairs (R.O.C.) (2001) Report to‘the guideline on enhancing economic and trade relations with Southeast Asia, Australia, and New Zealand’, 25 Apr 2001

Ministry of Economic Affairs (R.O.C.) (2014) The 7th guidelines on enhancing economic and trade relations with Southeast Asian countries, July 2014

Pitlo LB III (2015) Chinese infrastructure investment goes abroad. Diplomat, 6 Aug 2015.http:// thediplomat.com/2015/08/chineseinfrastructure-investment-goes-abroad/

Ptak R (1999) China’s seaborne trade with South and Southeast Asia, (1200–1750). Ashgate, Aldershot

Ptak R (2004) China, the Portuguese, and the Nanyang: Oceans and routes, regions and trade (c. 1000–1600). Ashgate, Aldershot

Rodrigues M, Moog G (2004) Global environmentalism and local politics transnational advocacy networks in Brazil, Ecuador, and India. State University of New York Press, Albany, NY Salidjanova N, Koch-Weser I, Klanderman J (2015) “China’s economic ties with ASEAN: a

country-by-country analysis.” US-China Economic and Security Review Commission: A Staff Report, 17 May 2015

Shambaugh D (2013) China goes global: the partial power. Oxford University Press, New York Souza GB (2014) Portuguese, Dutch and Chinese in maritime Asia, c.1585-1800: merchants,

commodities and commerce. Ashgate, Aldershot

Suryadinata L (ed) (2006) Southeast Asia’s Chinese businesses in an era of globalization: coping with the rise of China. Institute of Southeast Asian Studies, Singapore

Suryadinata L (2007) Understanding the ethnic Chinese in Southeast Asia. Institute of Southeast Asian Studies, Singapore

Yeh JT, Huang YL (2015) FTA between Taiwan and ASEAN countries: potential issues and factors. In: Hsu K (ed) ASEAN community and Taiwan: retrospect and prospect. Taiwan ASEAN Center, Taipei, pp 309–340

Yu M (2014) Inside China: anti-Chinese riots hit Taiwan. Wash Times, 23 May 2014,http://www. washingtontimes.com/news/2014/may/23/inside-china-anti-chinese-riots-hit-taiwan/?page¼all

Zhao H (2011) Taiwan-ASEAN economic relations in the context of East Asian regional integra-tion. Int J China Stud 2(1):39–54

India and China: “Awakening Giants”

Towards a Win–Win Future?

Manjira Dasgupta

. . . “Two of the oldest and still extant civilizations, (India and China were), for Europeans, legendary seats of immense wealth and wisdom right up to the eighteenth century.. . . Somewhere between the mid-eighteenth century and early nineteenth centuries, both these countries became, in the European eyes, bywords for stagnant, archaic, weak nations . . . .. By 1960s . . . they were independent republics supposedly launched on their path of development, but both suffered devastating famines.. . . These two countries were “basket cases” in the then fashionable terms of international diplomacy”.

. . . “Within the following forty years we are discussing China and India not as failures nor for their ancient wisdoms, but as dynamic modern economies. The Economist has to write editorials to tell the world not to be afraid of China’s economic power. American legislators pass laws to prevent their businesses outsourcing work to India’s software and telecommunication services. China ranks as the second largest economy in terms of GDP in PPP dollars. Together the two countries account for 19.2 % of world GDP—China 11.5 % and India 7.7 %”.

—Lord Meghnad Desai (2003) . . . “China and India have now become poster children for market reform and globalization in parts of the financial press, even though in matters of economic policy toward privatisation, property rights, and deregulation and lingering bureaucratic rigidities both countries have demonstrably departed from the economic orthodoxy in many ways. This has not escaped the attention of the Heritage Foundation. . . . . . both are relegated to the group described as “mostly unfree”. . . Of course, not many have pointed out that the economic (particularly growth) performance of these two “mostly unfree” countries in terms of economic freedom seem to have been much better than that of most others”.

—Pranab Bardhan (2014, pp. 7–8)

M. Dasgupta (*)

Maharaja Sayajirao University of Baroda, Vadodara, Gujarat, India e-mail:[email protected]

© Springer International Publishing Switzerland 2016

Y.-C. Kim (ed.),Chinese Global Production Networks in ASEAN, Understanding China, DOI 10.1007/978-3-319-24232-3_12