伊斯蘭銀行和一般銀行的比較研究:以甘比亞和英國為例 - 政大學術集成

69

0

0

全文

(2) 伊斯蘭銀行和一般銀行的比較研究:以甘比亞和英國為例 Comparative Study on Islamic and Conventional Banks: Cases in The Gambia and United Kingdom. 研究生:杜荷萍. Student: Habibatou Drammeh. 指導教授:蔡政憲. Advisor: Jason Cheng-Hsien Tsai. 學. ‧ 國. 立. 政 治 大 國立政治大學. ‧. 商學院國際經營管理英語碩士學位學程 碩士論文. er. io. sit. y. Nat. A Thesis. n. a to International MBA Program Submitted iv l C n U NationalhChengchi University engchi. in partial fulfillment of the Requirements for the degree of Master in Business Administration. 中華民國一○二年十二月 December 2013.

(3) Acknowledgements I wish to take this opportunity to express my sincere gratitude to professor Jason Cheng-Hsien Tsai for the continuous support, patience, enthusiasm, motivation and guidance in the preparation of this Thesis work. I would not have been able to finish this dissertation without his invaluable supervision which assisted me all the time of the research and writing of the thesis.. 政 治 大. Above all, I would like to thank my family especially my husband (Mr. Alieu B. Saine) for. 立. allowing me to travel all the way from The Gambia to Taiwan to pursue my IMBA program. I. ‧ 國. 學. owe it extremely to the Taiwanese Government for granting me an ICDF (International Corporation and Development Fund) scholarship. I never would have been able to complete an. ‧. IMBA program this fast without their support.. y. Nat. er. io. sit. I am most grateful to some staff of the Central Bank of the Gambia for their support in providing me with data needed for this thesis work. Finally, I would like to thank National Chengchi. n. al. Ch. i n U. v. University IMBA office particularly my program Manager Frank Chang for making life easy and worth living in Taiwan.. engchi. i.

(4) Abstract Comparative Study on Islamic and Conventional Banks: Cases in The Gambia and United Kingdom By Habibatou Drammeh This research paper investigates the performance of Islamic and Conventional banks in The. 政 治 大. Gambia and United Kingdom for the periods 2008/2009 to 2012. Islamic banking is conceived. 立. by many as a recent phenomenon which in the last few decades attracted lots of attention and. ‧ 國. 學. discussions. Islamic banking is a system of banking that is in consistent with Islamic law (Sharia). Islam does not allow the payment or acceptance of interest charges (Riba) in banking. ‧. activities such as lending and depositing of money. Whiles Conventional banks deal with. Nat. sit. n. al. er. io. and risk sharing).. y. Interest, Islamic banks method of operation is strictly based on Sharia principles (profit, loss. Ch. i n U. v. The objective of this study is to analyze and investigate the impact of the financial crisis on the. engchi. performance of some Islamic and Conventional banks in The Gambia and United Kingdom. Financial ratios are used to measure Profitability, Liquidity and Financial Leverage of the banks. The empirical results of the analysis showed that the Islamic banks selected for the study generally fared better than their counterpart Conventional banks in terms of Liquidity and Financial Leverage during and after the financial crisis. Among other findings, the selected Conventional Banks in this study are found to be relatively more profitable than their peer Islamic banks from 2008/2009 to 2012.. Keywords: Sharia, Islamic banks, Conventional banks, Riba, Financial crisis ii.

(5) TABLE OF CONTENTS 1. Introduction .......................................................................................................................... 1 1.1. Importance of the Research ............................................................................................. 2 1.2. Research Question ........................................................................................................... 3 1.3. Conceptual Framework.................................................................................................... 3. 政 治 大. 1.4. Research Limitation ......................................................................................................... 3. 立. 2. Background Information ..................................................................................................... 5. ‧ 國. 學. 2.1. Introduction to Islamic and Conventional Banking......................................................... 5. ‧. 2.2. Historical Perspective of Islamic Banking ...................................................................... 6. sit. y. Nat. 2.3. Conventional Banking Defined ....................................................................................... 9. n. al. er. io. 2.4. Difference between Islamic and Conventional Banking ............................................... 10. Ch. i n U. v. 2.5. Islamic Banks Modes of Financing ............................................................................... 12. engchi. 3. Literature Review ............................................................................................................... 15 4. Banking Sector in The Gambia and United Kingdom .................................................... 18 4.1. Country Overview ......................................................................................................... 18 4.1.1. The Gambia ............................................................................................................ 18 4.1.2. United Kingdom ..................................................................................................... 23 4.2. Banking Sector .............................................................................................................. 28 4.2.1. The Gambia ............................................................................................................ 28. iii.

(6) 4.2.2. United Kingdom ..................................................................................................... 32 5. Performance Evaluation Criteria ..................................................................................... 34 5.1. Methodology.................................................................................................................. 34 5.2. Liquidity ........................................................................................................................ 36 5.2.1. Current Ratio (CR) ................................................................................................. 37 5.2.2. Cash to Deposit Ratio (CDR) ................................................................................. 37. 政 治 大. 5.2.3. Loan to Deposit Ratio (LDR) ................................................................................. 38. 立. 5.3. Profitability .................................................................................................................... 38. ‧ 國. 學. 5.3.1. Return on Assets (ROA) ......................................................................................... 39 5.3.2. Return on Equity (ROE) ......................................................................................... 39. ‧. 5.4. Financial Leverage ........................................................................................................ 39. y. Nat. n. al. er. io. sit. 5.4.1. Debt-to-Asset Ratio (DAR) .................................................................................... 40. v. 6. Empirical Analysis .............................................................................................................. 41. Ch. engchi. i n U. 6.1. The Gambia ................................................................................................................... 41 6.1.1. Liquidity ................................................................................................................. 41 6.1.1.1. Current Ratio ................................................................................................... 41 6.1.1.2. Cash to Deposit Ratio ...................................................................................... 42 6.1.1.3. Loan Deposit Ratio .......................................................................................... 45 6.1.2. Profitability ............................................................................................................. 46 6.1.2.1. Return on Asset ................................................................................................ 46 6.1.2.2. Return on Equity.............................................................................................. 47 6.1.3. Financial Leverage ................................................................................................. 47 iv.

(7) 6.1.3.1. Debt-to-Asset Ratio ......................................................................................... 47 6.2. United Kingdom ............................................................................................................ 48 6.2.1. Liquidity ................................................................................................................. 48 6.2.1.1. Current Ratio ................................................................................................... 48 6.2.1.2. Cash to Deposit Ratio ...................................................................................... 49 6.2.2. Profitability ............................................................................................................. 50 6.2.2.1. Return on Assets .............................................................................................. 50. 政 治 大. 6.2.3. Financial Leverage ................................................................................................. 51. 立. 6.2.3.1. Debt-to-Asset Ratio ......................................................................................... 51. ‧ 國. 學. 7. Results and Conclusions..................................................................................................... 53. ‧. Reference ................................................................................................................................. 55. n. er. io. sit. y. Nat. al. Ch. engchi. v. i n U. v.

(8) List of Figures and Tables Figure 1: GDP Growth over Period 1991 to 2012 (The Gambia) ............................................ 21 Figure 2: Import Partners (The Gambia) .................................................................................. 22 Figure 3: Export Partners (The Gambia) .................................................................................. 23 Figure 4: GDP Growth over Period 1991 to 2014 (UK) .......................................................... 27 Figure 5: Import Partners (UK) ................................................................................................ 27 Figure 6: Export Partners (UK) ................................................................................................ 28. 治 政 Figure 7: Current Ratio and Cash to Deposit Ratio (The 大 Gambia) .......................................... 41 立 Figure 8: Growth in Cash and Bank Balances (Ecobank) ........................................................ 43 ‧ 國. 學. Figure 9: Treasury Bills and Sukuk .......................................................................................... 44. ‧. Figure 10: Loan to Deposit Ratio (The Gambia) ...................................................................... 45 Figure 11: Return on Assets and Return on Equity (The Gambia) ........................................... 46. y. Nat. er. io. sit. Figure 12: Debt to Asset Ratio (The Gambia) .......................................................................... 48 Figure 13: Current Ratio (UK) ................................................................................................. 49. n. al. Ch. i n U. v. Figure 14: Cash to Deposit Ratio (UK) .................................................................................... 50. engchi. Figure 15: Return on Assets (UK) ............................................................................................ 51 Figure 16: Debt to Asset Ratio (UK) ........................................................................................ 52. vi.

(9) Table 1: Difference between Islamic and Conventional Banking ............................................ 10 Table 2: Basic Data and Key Economic Indicators for the Year 2012 (The Gambia) .............. 19 Table 3: GDP Decomposition by Sector (The Gambia) ........................................................... 20 Table 4: Basic Data and Key Economic Indicators for the Year 2012 (UK) ............................ 25 Table 5: GDP Decomposition by Sector (UK) ......................................................................... 25 Table 6: Commercial Banks in The Gambia............................................................................. 30 Table 7: The Gambia Financial Soundness Indicators ............................................................. 31. 政 治 大. Table 8: Selected Banks for the Analysis ................................................................................. 34. 立. Table 9: Financial Ratios Selected for the Study ...................................................................... 36. ‧ 國. 學. Table 10: Current Ratio and Cash to Deposit Ratio ................................................................. 41 Table 11: Cash and Bank Balances (Ecobank) ......................................................................... 43. ‧. Table 12: Treasury Bills and Sukuk .......................................................................................... 44. y. Nat. sit. Table 13: Loan to Deposit Ratio ............................................................................................... 45. n. al. er. io. Table 14: Return on Assets and Return on Equity .................................................................... 46. i n U. v. Table 15: Debt to Asset Ratio ................................................................................................... 47. Ch. engchi. Table 16: Current Ratio (UK) ................................................................................................... 49 Table 17: Cash to Deposit Ratio (UK)...................................................................................... 50 Table 18: Return on Assets (UK) .............................................................................................. 51 Table 19: Debt to Asset Ratio (UK).......................................................................................... 51. vii.

(10) 1. Introduction The rationale behind this piece of research is to investigate and make a comparison between Islamic and Conventional banks and their performance in the recent global financial crises. This work will not only make a case study of The Gambia but will also enlighten about the performances of some Conventional and Islamic banks in the United Kingdom. Section 1 of this thesis will provide a background information of Islamic and Conventional Banks and how each system operates in the financial industry. It is important to note that banks perform a very. 治 政 significant role in our society. They actually perform the大 role of an intermediary. That is, they 立 help to move funds from the surplus sector of the economy (depositors) to the people who need ‧ 國. 學. money (borrowers) in order to do business. Banking over the years had contributed positively. ‧. to the wellbeing of people around the globe. It is good to know that financial institutions have not only done well to the society. In fact, they had also contributed tremendously to the recent. y. Nat. er. io. sit. financial crisis. Ganesh (2008) in an article published in the “The Economic Times” blamed banks for being the primary cause of the crisis. This he said was due to the excessive use of. n. al. Ch. leverage and bad lending principles.1. engchi. i n U. v. In history, the earliest banking systems began with Conventional banks. 2 However, as the number of Muslims in the world increase, most countries had embraced the Islamic system of banking in order to satisfy the Muslim minority. In evaluating the difference in performance of Islamic and Conventional banks, this work intends to measure performance in terms of Liquidity, Profitability and Financial Leverage. This study is going to focus on the financial. 1. http://articles.economictimes.indiatimes.com/2008-10-05/news/28398857_1_lending-standards-property-. prices-financial-crisis 2. http://en.wikipedia.org/wiki/History_of_banking. 1.

(11) years of 2008/2009 to 2012. The reason for choosing this period is that much of the global recession was underscored within this period. Great Britain, European Union and the United States of America were predominantly affected by the crisis. This period resulted in a proliferation of new regulatory policies as intervention and an antidote to rescue countries affected by the crisis. It also witnessed closure of some banks around the globe which casted the destiny of most countries’ economies in a precarious situation.. 政 治 大 banking whose activities are in line with the principles of sharia (Islamic ruling). Islam does 立 According to the Institute of Islamic Banking and Insurance, Islamic banking is a system of. ‧ 國. 學. not allow the payment or acceptance of interest charges (Riba) in banking activities such as lending and depositing of money. Furthermore, it prohibits trading in any activity that is. ‧. considered contrary to the principles of Islam.3 It is however important to note that Islamic. sit. y. Nat. banking is not restricted to Muslims only.. n. al. er. io. 1.1. Importance of the Research. i n U. v. This piece of research is very important given the recent global economic and financial. Ch. engchi. upheavals which rendered the lives of many around the globe in a precarious state. This crisis became a catalyst that increased youth unemployment. Banks have been identified as one of the main forces behind the catastrophes. The outcome of this novel research will enlighten and illuminate the impact of the financial crisis on some Islamic and Conventional banks in The Gambia and United Kingdom.. 3. http://www.islamic-banking.com/what_is_ibanking.aspx. 2.

(12) 1.2. Research Question . Did the only Islamic bank in The Gambia perform better than its Conventional bank peers in the recent global financial crisis?. . How well did Islamic banks in the United Kingdom perform during the recent global financial crisis?. 1.3. Conceptual Framework. 政 治 大 you with Background Information. The research framework maps out the structure and order the research is presented. The next. 立. section on this paper provides. about Islamic and. ‧ 國. 學. Conventional banking. Section 3 presents the Literature Review, Section 4 provides you with an overview of the banking Sector in The Gambia and United Kingdom. Section 5 explains the. ‧. Methodology used. Sections 6 and 7 provides an Empirical Analysis and Results and. sit. y. Nat. Conclusions respectively.. n. al. er. io. 1.4. Research Limitation. i n U. v. It is important to mention and note the methodological constraints of this thesis work. The thesis. Ch. engchi. was primarily limited by the inability of the researcher to access Annual Financial Reports of the only Islamic Bank in The Gambia (Arab Gambia Islamic Bank (AGIB)). The research relied entirely on data accessed from the Central Bank of The Gambia and this includes Income statements, Balance Sheet Statements and Cash Flow statements. Access to AGIB’s annual reports would have provided the researcher with enough information to the Financial Notes. The Financial Notes are supplementary information added to the end of the financial statements, which assist to explain specific items in the financial statements (http://en.wikipedia.org). In addition to the above, the sample size of Islamic banks in the Gambia is limited to only one Islamic bank. This is because there exist only one Islamic bank in The Gambia. The analysis of 3.

(13) the performance of Islamic and conventional banks in The Gambia would have been more interesting if the researcher was able to use equal numbers of Islamic and conventional banks for the study.. 立. 政 治 大. ‧. ‧ 國. 學. n. er. io. sit. y. Nat. al. Ch. engchi. 4. i n U. v.

(14) 2. Background Information 2.1. Introduction to Islamic and Conventional Banking It is essential to mention again that Islamic and Conventional banks are both Financial Intermediaries that transfer funds from depositors to investors in the financial market. In the Muslim world, Islamic banking is considered as an alternative to Conventional banking in order to exonerate Muslims from exploitation in the name of profit making by the Conventional banks. Whiles Conventional banks deal with Interest, Islamic banks method of operation is strictly. 治 政 based on Sharia principles (profit, loss and risk sharing).大 Islamic banking deals with asset based 立 transactions which means that its transactions must be backed by some assets. Hanif (2011) ‧ 國. 學. states that Riba (interest) is not only forbidden in Islam but in all revealed religions. Therefore,. ‧. interest is not allowed in Islamic Banking. A student of Darul-Uloom, Bury, U.K (1998 to 2001) mentioned that, the meaning of Interest as used in the Arabic language means to excess or. y. Nat. io. sit. increase. He said “in the Islam terminology, Interest means effortless profit or that profit which. n. al. er. comes free from compensation or that extra earning obtained that is free of exchange”.4. Ch. engchi. i n U. v. Andrews (2010), the modes of operation of Islamic banking are based on Laws and regulations which are found in the Holy Quran (Holy Book of Muslim) and the Sunnah (saying) of the last Prophet Muhammed S.A.W. The rule of justice is vital in the transactions of Islamic banking. In fact, Profit and losses are shared between and among parties involved in a transaction. Complete risk on transactions’ is not just transferred to one party. Therefore, a bank for example does not take all the risk, by promising the provider of the funds returns regardless of whether the transaction makes money or not. Islamic banking is typically based on a fair play.. 4 http://www.inter-islam.org/Prohibitions/intrst.htm#Definition. 5.

(15) The growth in Islamic banking over the years had been remarkable. Islamic banking after several decades had gain recognition and had been established in many countries around the globe including non-Muslim countries. Nations like Iran and Sudan have officially converted their Conventional banking systems to Islamic banking systems (Dr. Fikret Hadžić).5 Aggarwal and Yousaf (2000) states that Islamic banking systems are present in over sixty countries, most of them operate in the Middle East and Asia. In addition, Islamic banking had caught the attention of many International Conventional banks who now have opened Islamic banking. 政 治 大. windows in order to satisfy the increasing demand for Islamic banking products and services.. 立. Vizcaino (2013), said the United Kingdom aims to be the first non-Muslim nation to integrate. ‧ 國. 學. Islamic Bonds in its financial market. This is considered an opener for promotion of Islamic banking in the UK and to encourage new investments into the country.6. sit. y. ‧. Nat. 2.2. Historical Perspective of Islamic Banking. io. er. Islamic finance and banking had been regarded by many as a recent phenomenon. However,. al. the origin of Islamic finance dated back since the inception of Islam. This is evident in the Holy. n. v i n book of Muslims (Al Quran). If C youhread the Quran you e n g c h i U will at least come across four verses. where Allah (God) mention Riba (interest). A Student of Darul-Uloom, Bury, U.K (1998 to 2001) mentioned one of them found in Sura Al-baqarah verse nos. 275 to 279 “Those who devour usury (interest) will not stand except as stands one whom the Satan by his touch has driven to madness. That is because they say, "trade is like usury (interest)", but Allah has permitted trade and has forbidden usury (interest)". Verse 276 "Allah will deprive usury of all blessing, and. 5. http://www.bbi.ba/web/index.php?option=com_content&view=article&id=56&Itemid=199&lang=en. 6. http://www.telegraph.co.uk/finance/newsbysector/banksandfinance/10410467/Britain-to-become-first-. non-Muslim-country-to-launch-sharia-bond.html. 6.

(16) will give increase for deeds of charity, for he does not love any ungrateful sinner." later in verse 278 the Quran mention "Oh you who believe! Fear Allah and give up what remains of your demand for usury (interest) if you are indeed believers”. Consequently in verse 279 he says "If you do not, take notice of war from Allah and his Messenger “Sallallahu Alaihe Wasallam” but if you repent you shall have your capital sum. Deal not unjustly and you shall not be dealt with unjustly".7. 政 治 大 and Christianity. In Judaism, Israelites among themselves were not permitted to ask for any 立 It is interesting to note that Riba (interest) is not only forbidden in Islam but also in Judaism. ‧ 國. 學. additional sum on top of the principal amount of the sum lent in transactions. However, they were not forbidden to charge interest in their dealings with the gentiles. The reason for this was. ‧. that at the time there were no laws among the gentiles which prohibited the practice of interest.. y. sit. io. n. al. er. (Ziauddin Ahmad).. Nat. Therefore, Jews were allowed to recover interest from people who charged interest from them. i n U. v. According to Judaism, The Talmud (B. M. 61b) dwells on Ezek. xviii. 13 (Hebr.): "He has lent. Ch. engchi. on usury; he has taken interest; he shall surely not live, having done all these abominations"; on the words with which the prohibition of usury in Lev. xxv. 36 closes: "Thou shalt be afraid of thy God"; and on the further words in which Ezekiel (l.c.) refers to the usurer: "He shall surely suffer death; his blood is upon him"; hence the lender on interest is compared to the shedder of blood.8. It is mentioned in the Old Testament of the Bible that "Thou shalt not lend upon usury to thy. 7. http://www.inter-islam.org/Prohibitions/intrst.htm. 8. http://www.jewishencyclopedia.com/articles/14615-usury. 7.

(17) brother; usury of money, usury of victuals, usury of anything that is lent upon usury." [Deuteronomy 23:19]. It’s vital to mention that the practice of Islamic banking in the modern financial market gain popularity in recent years, precisely in the 1980’s. The sector since then had been growing and recently acquired a considerable share of global financial activities. Majeed (2013) asserts that Islamic banking and Finance sector today is growing at an annual rate of 15-20%, which makes. 政 治 大 not only banks but all other Islamic financial service providers such as Islamic Mutual Funds, 立. it the fastest growing industry in the world.9 The extraordinary growth in this industry involves. ‧ 國. 學. Islamic Bonds-Sukuk, Islamic Insurance-Takafu, Islamic Credit Cards, Islamic Wealth Management, Islamic Private Equity and other components of the Islamic financial system.. ‧. Islamic banks operates in many countries around the globe and its transactions volume by the. sit. y. Nat. end of 2008 had reached USD951 Billion (Hanif (2011)). It is not surprising that the novel. io. al. er. developments in Islamic banking has drown a lot of attention and becomes an area of interest. n. to developed economies such as The United Kingdom, United States of America, and other western nations.. Ch. engchi. i n U. v. One of the reasons for the existence of Islamic Development Bank (IDB) in 1973 by the Organization of Islamic Countries (OIC) was basically to inspire economic development and to create social progress of member states and Muslim communities separately as well as jointly in line with the rule of Sharia (Islamic law).10 Gafoor (1995) mentioned that the earliest form of interest free bank (Islamic banking) was founded in Dubai (Dubai Islamic Bank) in 1975.. 9. http://www.islamicbankinst.com/resource-paper.html. 10http://www.isdb.org/irj/go/km/docs/documents/IDBDevelopments/Internet/English/IDB/CM/Publications. /CapitalMarketCooperation.pdf. 8.

(18) Dubai Islamic Bank was the first modern commercial Islamic bank in the world. The purpose for this was to establish an institution where Muslims can be provided a whole range of Islamic banking services.. 2.3. Conventional Banking Defined Conventional banking system play an important role in the economic development of most nations. It had over the years mediated between borrowers and savers in the financial market.. 政 治 大 and investing most of those deposits, either by making loans to individuals and firms or by 立 They play a key role in the financial system by taking in deposits from individuals and firms. ‧ 國. 學. buying securities, such as government bonds etc. Most people rely on borrowing money from Conventional banks when they purchase items such as cars or homes. Similarly, many firms. ‧. rely on Conventional bank loans to meet their staff salaries.. y. Nat. sit. According to the capitalist system, the return for using money is interest. Therefore the major. n. al. er. io. source of revenue and cost of funds to Conventional banks is charging interest on deposits and. i n U. v. through lending. Interest is a prime driver of profit for Conventional banks. Of course both. Ch. engchi. Conventional and Islamic banks operate in the same societies. Consequently, both institutions offer a wide range of products and services to their customers. Products and services of Islamic banks will be mention later in this thesis work. However, at this point it is important to mention a common Conventional financing method since it contribute immensely to the economic development of countries.. Debt financing: Debt is usually a Conventional commercial bank loan on which borrowers are expected to repay both interest (cost of the debt) and principal (loan amount) at maturity of the debt. Lenders normally charge a pre-determined rate of interest which is set by adding an. 9.

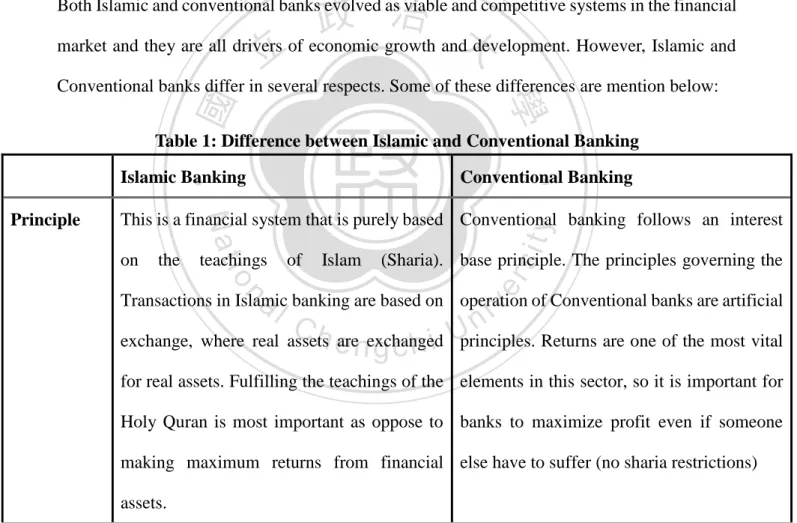

(19) "interest margin". The interest margin generally represent the banks' return on investment and or income. The disadvantage or risk associated with this kind of transaction is that the lender faces losing 100% of the loan to the borrower if the borrowers’ project fails to perform. In addition, lenders and or banks have little or no opportunity to increase returns and face the possibility of losing entire investments.11. 2.4. Difference between Islamic and Conventional Banking. 政 治 大 market and they are all drivers of economic growth and development. However, Islamic and 立. Both Islamic and conventional banks evolved as viable and competitive systems in the financial. ‧ 國. 學. Conventional banks differ in several respects. Some of these differences are mention below: Table 1: Difference between Islamic and Conventional Banking. ‧. Islamic Banking. Nat. teachings. Islam. (Sharia). base principle. The principles governing the. n. al. of. sit. the. io. on. y. This is a financial system that is purely based Conventional banking follows an interest. er. Principle. Conventional Banking. i n U. v. Transactions in Islamic banking are based on operation of Conventional banks are artificial. Ch. engchi. exchange, where real assets are exchanged principles. Returns are one of the most vital for real assets. Fulfilling the teachings of the elements in this sector, so it is important for Holy Quran is most important as oppose to banks to maximize profit even if someone making maximum returns from financial else have to suffer (no sharia restrictions) assets.. 11. http://www.prophecyfinancial.com/securities.htm. 10.

(20) Profit. and Islamic banking encourages profit and loss Transactions in Conventional banking are. loss Sharing sharing. This act promotes social solidarity. based on pre-determined rate of interest. There is mutual trust between bank and Since profit and loss are not shared, bank and customer.. its customer both safeguard their interest. This sometimes leads to impulsive reactions in financial dealings.. Interest. Interest is prohibited in the operation of Interest not prohibited. 政 治 大. Islamic banks Islamic. 立 strictly. principles. encourage Conventional banking allows trading in. 學. ‧ 國. Speculative. transactions investments that have a social and an ethical speculative instruments such as derivatives. benefit to society. It requires a complete It also allows investment in alcohol. of. contract. terms.. ‧. transparency. Any. y. Nat. n. al. speculative instruments such as derivatives. Ch. engchi. are forbidden. It also prohibits investment in. er. io. terms are prohibited. Therefore, trading in. sit. uncertainty about price, delivery and other. i n U. v. sectors classified as inappropriate on moral grounds by the Quran. Some examples of these sector include, trading in alcohol, gambling, or drugs. Islamic tax Islamic banks serve as Zakat collectors for Does not deal with zakat (ZAKAT). many Muslims and they also pay out their zakat.. 11.

(21) Penalty. Extra money is not levied on defaulters in It can charge additional money (penalty and. charges. Islamic Banking. What is collected from compounded interest) in case of defaulters. defaulter is a small compensation and the proceeds from this compensation are given out as charity.. Borrowing. For the Islamic banks, it must be based on a. For interest-based commercial banks,. Sharia approved underlying transaction.. borrowing from the money market is. 政 治 大 relatively easier.. 立Source: <http://zaharuddin.net>. ‧ 國. 學. 2.5. Islamic Banks Modes of Financing. ‧. It is clear from the explanations above that Islamic banks prohibit the payment and acceptance of Interest. Now we want to know how Islamic banks make money if they charge no interest.. y. Nat. n. al. er. io. banks. These are:. sit. Ahmad and Pandey (2010) describe some products and services commonly offered by Islamic. I.. Ch. engchi. i n U. v. Murabaha (Trade with Markup or Cost Plus Sale). This is a contract agreement for the selling of goods. It is a cost plus sale contract in which the bank for example purchase an asset at the request of the customer. The bank then sells the asset to the customer on a deferred sale base by adding some profits thereon. Therefore, Murabaha is not a loan on which interest is charged. In fact in Bai' Murabaha purchase contracts were bank buys commodities on behalf of a customer and resell those commodities to the same customer at a cost plus sale basis, the contract agreement requires the bank to disclose to the customer its cost and profit margins.. 12.

(22) II.. Mudaraba ( Trustee Finance Contract). This is a partnership contract in which an investor/bank provides capital to an entrepreneur for investment purpose and the entrepreneur offers his labor or expertise. Profit or loss generated from this kind of agreement are shared between the bank and the entrepreneur at a certain predetermine ratio.. III.. Musharaka ( Partnership or Joint Venture). 政 治 大 projects. Profits and losses from the project are shared evenly to the amount of investment. An 立 This is a contract agreement between two or more people to finance long term investment. ‧ 國. 學. example of a Musharaka contract is when a customer is involved in a long term project but does not seek full bank financing of the project, instead he/she contributes some of his/her own equity. ‧. capital. Since the bank is not the only party that provides funds for the project, the two parties. sit. y. Nat. will be involved in a profit and loss sharing. The profits will be shared in accordance with. io. al. n. IV.. er. predetermined ratios, whiles losses are borne in proportion to equity participation.. Ijara wa iqtina (Leasing Contract). Ch. engchi. i n U. v. This is a leasing agreement. Under this agreement, a customer (Lessee) for example approaches a bank (Lessor) with a request to lease a particular asset or property. The Lessor purchases the asset or building and leases it to the customer for an agreed lease rental payment, together with the customer agreement to make lease payments towards the purchase of the asset from the lessor at the end of the leasing period. The right of ownership of the asset or property remains with the Lessor until lessee completes payment at the end of the leasing period.. 13.

(23) V.. Istisna’ a (Leasing Contract). This is a contract of exchange before delivery. It is a sale contract in which the commodity or product is transacted before it comes into existence. For example when someone place an order to a manufacturer to manufacture, construct or make something according to the specifications provided. If the manufacture agrees to manufacture the goods for the purchaser, then the transaction of Istisna comes into existence. An important aspect for the validity of Istisna is that the price is fixed with the consent of the parties and that necessary specification of the. 政 治 大. commodity (intended to be manufactured) is fully settled between them.. 立. Qard-e-hasna (Benevolent Loan or Interest free Loan). ‧ 國. 學. VI.. This is a loan that is totally free of interest to the borrower. Islamic banks provide such a facility. ‧. with a zero return loan and are allowed to charge the borrowers a service fee to cover the. sit. y. Nat. administrative expenses for handling the loan. These types of loans are negative net present. io. er. value investments to Islamic banks and are only limited to the poor sections of society such as needy students or small rural farmers.. n. al. Ch. engchi. 14. i n U. v.

(24) 3. Literature Review The Global Financial Crisis (phenomena) of 2008 to 2009 has been considered by many economics as the worse financial crises since the great depression of 1930’s.12 Several studies since then had been conducted to examine the impact of the crises on the performances of Islamic and Conventional banks. Amba and Almukharreq (2013) revealed that the financial crisis of 2008 to 2009 had drawn a lot of attention to Islamic banking as Conventional banks were hit hard. It is interesting to note here that in the beginning of the phenomenon, while. 治 政 conventional banks were suffering from the effect of the 大crisis, Islamic banks kept on their 立 stability and enjoyed profits. Consequently, Islamic banking caught a lot of people’s attention ‧ 國. 學. as the ideal banking system since it prohibits interest and operates on the basis of profit and risk. ‧. sharing. However, as the phenomenon became universal, the biggest Islamic banks in the Islamic region began to feel the impact and eventually ended up with some losses.. sit. y. Nat. n. al. er. io. Addawe (2012) research results indicated that Islamic banks fared better than their counterpart. i n U. v. Conventional banks during the recent global financial crisis. Due to the difference in the modes. Ch. engchi. of financing and corporate governance of the two banking systems, Islamic banks were less affected by the crisis than Conventional banks. The reasons for being less affected by the crisis are that Islamic banking transactions were asset backed transactions. In addition to this, Islamic banks avoided trading in speculative instruments as well as selling of debt. They also avoided trading in toxic assets and all their finances were based on a profit and loss sharing.. Parashar and Venkatesh (2010) stated that before the global financial crisis, conclusions were. 12. Two top economists agree 2009 worst financial crisis since great depression; risks increase if right steps. are not taken. (February 29, 2009). Reuters. Retrieved 2009-09-30, from Business Wire News database. 15.

(25) made by many researchers that the performances of Islamic banks by and large were better than those of their counterpart Conventional banks. However, there were other researchers who maintain that Islamic banking is too young to conclude that argument. According to them the financial crisis did not only affect Conventional banks but affected Islamic banks as well. In fact Islamic banks they said suffered more than Conventional banks in terms of Capital Ratio, Leverage and Returns on Average Equity. On the other hand Conventional banks did suffer more than their Islamic peers in terms of Returns on Average Assets and Liquidity.. 政 治 大. Consequently, their conclusions were that for the four years period (i.e. 2006 to 2009) used for. 立. the study, overall Islamic banks outperformed their counterpart Conventional banks in the times. ‧ 國. 學. of the crisis.. ‧. Although Islamic banking to a larger extend gain recognition in the 21st century, it is interesting. sit. y. Nat. to note that this sector had been growing steadily far back in the nineties. This is why Iqbal. io. er. (2001) conducted a research which compared Islamic and Conventional banks and their growth. al. and performance in the nineties. Twelve banks of Conventional and Islamic banks were chosen. n. v i n for the study. In order to have aC fairhcomparison of the e n g c h i Utwo set of banks, Iqbal choice of the twelve Conventional banks were selected from the same country where the Islamic banks were. chosen. The study covers eight years period (1990 to 1998), in which growth and performance of both Islamic and Conventional banks were evaluated. In the study, he tested a number of hypothesis and perceptions using empirical data. He also used a number of key ratios for the analysis. His conclusions were that in general, Islamic banks were fairly more capitalized, profitable and stable. Therefore, the profit ratio of Islamic banks compared favorably with international standards. However, he mentioned that since Conventional banks depositors were guaranteed their principal amounts, and thus bear less risk than their counterpart Islamic bank. 16.

(26) depositors, the depositors of Islamic banks would truly expect a higher rate of return to compensate for the extra risk they take.. Smolo and Mirakhor (2010) mentioned that both Keynes and Minsky argued that a system dominated by interest-based debt contracts is inherently unstable. They further in their research stated that the financial crisis was caused by a number of factors such as easy money, uncontrolled growth of credit and debt, lax regulation and supervision, innovation of complex. 政 治 大 transparency, predatory lending and high leverage. Although the Islamic Financial Industry (IFI) 立 and opaque financial products, mismanagement of risks involved, lack of disclosure and. ‧ 國. 學. was not totally resistant to the crisis, however it was less affected compared to the Conventional systems. Therefore, a lot of attention was shifted to IFI as an alternative system. They concluded. ‧. by saying that although the crisis had limited impact on IFI, there are many lessons that should. n. al. er. io. sit. y. Nat. be learned from it to prevent IFI from committing the same mistake.. Ch. engchi. 17. i n U. v.

(27) 4. Banking Sector in The Gambia and United Kingdom 4.1. Country Overview 4.1.1. The Gambia The Republic of The Gambia is a very small West African country with a population of about 1.8 Million people. In a country profile report, Alisa Alston and Marianne Moukhtara describe the Gambia as belonging to the Ghana, Songhai, and Mali Empires several decades ago. According to them, The Gambia became a British colony in 1888, and continued so until. 治 政 independence in 1965. The country moved from being大 a constitutional monarchy within the 立 British Commonwealth to an independent Republic half a decade later. The Gambia has a 13. ‧ 國. 學. geographical feature long narrow territory, following the path of The Gambia River. The. ‧. Country is bordered by the North Atlantic Ocean and Senegal. The Country has a land Square 11,295 square Km.14. sit. y. Nat. n. al. er. io. The population life-Expectancy of The Gambia in 2012 was 63.82 years. 15 The country’s. i n U. v. economy largely depends on service sector such as Financial Institutes, Tourism (represented. Ch. engchi. by hotels and restaurants sectors), Animal Husbandry, and Farming. The country belongs to the Least Developing Countries (Human Development Index). Long-term policy objectives of the country for economic growth and development are enshrined in the Vision 2020 national blue print.. 13. http://fic.wharton.upenn.edu/fic/africa/Gambia%20Final.pdf. 14. (https://www.cia.gov ). 15. http://www.indexmundi.com/the_gambia/life_expectancy_at_birth.html. 18.

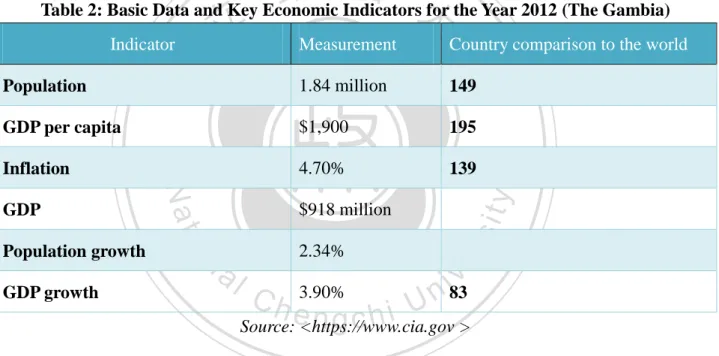

(28) Macroeconomic Data The Gambia has limited natural resources and a young agricultural system. The economy is characterized by traditional subsistence agriculture and an ancient dependence on groundnut as its main export product. 16 According to a report by the World Trade Organization, The Gambia's natural resource deposits consist not only agricultural products, fish, cotton lint and palm carnal but also kaolin, tin, ilmenite, rutile, and zircon, though these remain largely unexploited.. 195. 4.70%. 139. $918 million. n. al. 2.34%. GDP growth. Ch. y. $1,900. sit. io. Population growth. Nat. GDP. 149. er. Inflation. 1.84 million. ‧. GDP per capita. 學. Population. ‧ 國. 治 政 Table 2: Basic Data and Key Economic Indicators大 for the Year 2012 (The Gambia) 立 Measurement Country comparison to the world Indicator. 3.90%. engchi. i83v n U. Source: <https://www.cia.gov > GDP: This entry gives the gross domestic product (GDP) or value of all final goods and services produced within the country in a given year.. 16. https://www.cia.gov/library/publications/the-world-factbook/geos/countrytemplate_ga.html. 19.

(29) Table 3: GDP Decomposition by Sector (The Gambia) Indicator. Measurement. Agriculture % of GDP. 22.3%. Industry % of GDP. 18.3%. Services % of GDP. 59.5% Source: < https://www.cia.gov >. The major drivers of economic growth in The Gambia continue to be Agriculture, Services and. 政 治 大. remittances from workers overseas. Historically, the country relies on groundnut as its major. 立. export product and the sector in 2012 as indicated on table 3 accounted for about (22.3%) of. ‧ 國. 學. GDP, and it employed 70% of the labor force (Programme for Accelerated Growth and Employment, (2012 to 2015)).17 Less than half of the arable land in The Gambia is used for. ‧. cultivation. This consequently leads to a lot of potential land areas left unused. However, the. Nat. sit. y. country’s sea port had contributed to the creation of major re-export trade. In addition to this,. n. al. er. io. the country’s natural beauty and closeness to Europe had made it the largest tourist destination. i n U. v. center in West Africa.18 Service sector as seen from table 3 represents 59.5% of GDP.. Ch. engchi. The service sector in The Gambia includes Financial Institutions, Insurance Companies, Tourism and other Service providers. Tourism being the main foreign exchange earner in the country constituted 14.7% of GDP in 2009 (Programme for Accelerated Growth and Employment, (2012 to 2015)). The sector is not expected to recover in 2012 and 2013 due to the weak economic conditions in European Union countries, the main origin of The Gambia. 17. http://eeas.europa.eu/delegations/gambia/documents/about_us/page_2012_2015_en.pdf. 18. https://www.cia.gov/library/publications/the-world-factbook/geos/countrytemplate_ga.html. 20.

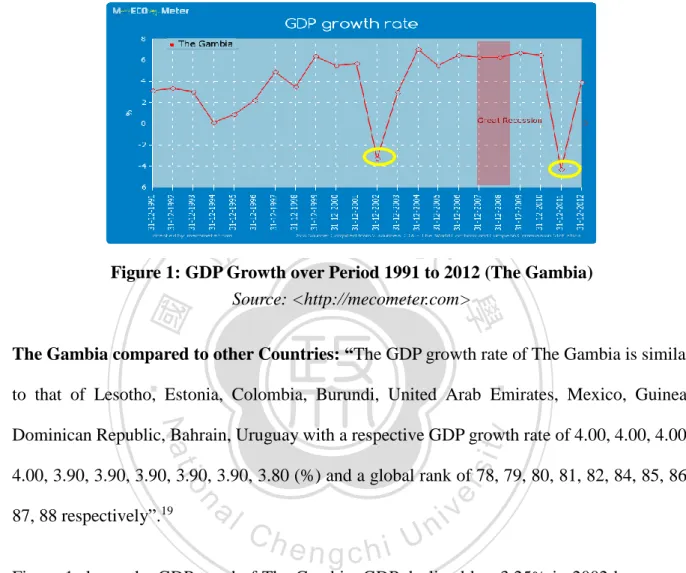

(30) tourist. Industry accounts for 18.3% of GDP.. 立. 政 治 大. ‧ 國. 學. Figure 1: GDP Growth over Period 1991 to 2012 (The Gambia) Source: <http://mecometer.com> The Gambia compared to other Countries: “The GDP growth rate of The Gambia is similar. ‧. to that of Lesotho, Estonia, Colombia, Burundi, United Arab Emirates, Mexico, Guinea,. y. Nat. sit. Dominican Republic, Bahrain, Uruguay with a respective GDP growth rate of 4.00, 4.00, 4.00,. al. n. 87, 88 respectively”.19. er. io. 4.00, 3.90, 3.90, 3.90, 3.90, 3.90, 3.80 (%) and a global rank of 78, 79, 80, 81, 82, 84, 85, 86,. Ch. engchi. i n U. v. Figure 1 shows the GDP trend of The Gambia. GDP declined by -3.25% in 2002 because of drought, but recovered in 2003. The performance of the economy after 2002 had been steady partly due to strong growth in agriculture, largely because of good rains.20 The GDP growth in 2009 was 6.7% compared to 6.5% growth in 2010. This decline was driven by the poor weather conditions and insufficient rains. In 2011 the country came up with a policy document aimed to strengthen the macroeconomic environment needed to enhance rapid growth in GDP. Based. 19. CIA - The World Facebook, European Commission Statistics. 20. http://www.accessgambia.com/information/economic-profile.html. 21.

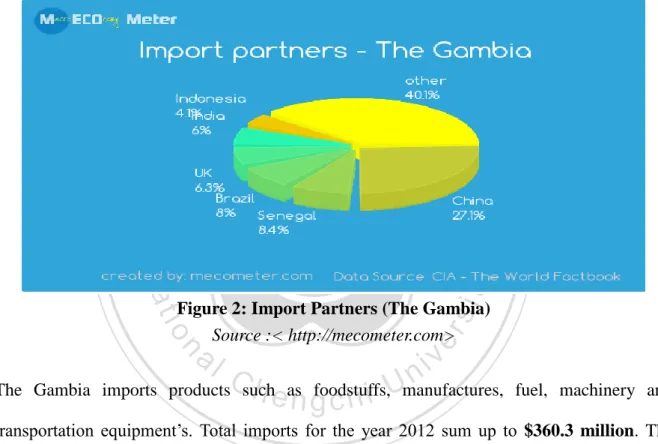

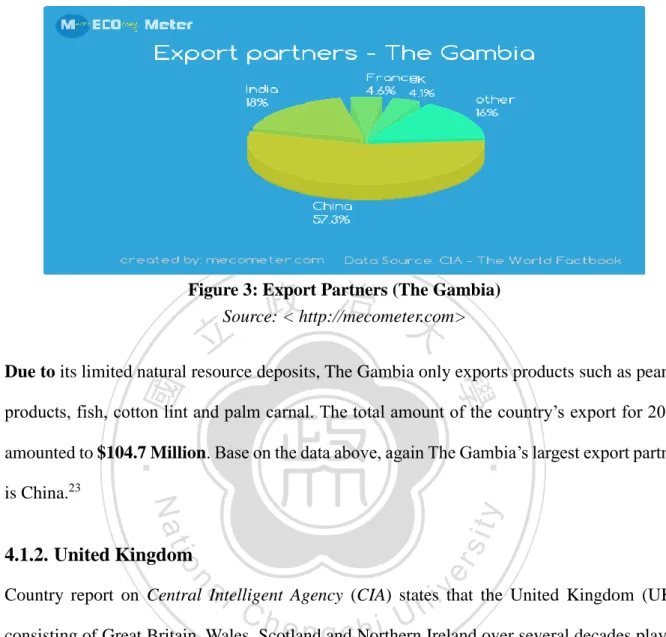

(31) on this, GDP was projected to grow at a rate of 5.5%.21 However, there was a sucking and huge decline in GDP from 6.5% in 2010 to -4.3% in 2011. The country’s GDP improved a little in 2012 from -4.3% to 3.9%, despite the decrease in GDP from the tourist sector and the unfavorable weather conditions the country experience that impacted negatively on its agricultural produce. The Gambia in 2012 had a GDP ranking of 83.22. 立. 政 治 大. ‧. ‧ 國. 學 sit. y. Nat. er. io. Figure 2: Import Partners (The Gambia) Source :< http://mecometer.com>. al. n. v i n C h as foodstuffs,Umanufactures, products such engchi. The Gambia imports. fuel, machinery and. transportation equipment’s. Total imports for the year 2012 sum up to $360.3 million. The Gambia’s largest import partner in 2012 is China.. 21. Report on the proceedings of the resource mobilization and investment conference on the Gambia’s. programme for accelerated growth and employment (page) 2012 -2015 22. http://mecometer.com/country/the-gambia/. 22.

(32) 政 治 大. Figure 3: Export Partners (The Gambia) Source: < http://mecometer.com>. 立. ‧ 國. 學. Due to its limited natural resource deposits, The Gambia only exports products such as peanut products, fish, cotton lint and palm carnal. The total amount of the country’s export for 2012. sit. y. Nat. is China.23. ‧. amounted to $104.7 Million. Base on the data above, again The Gambia’s largest export partner. n. al. er. io. 4.1.2. United Kingdom. i n U. v. Country report on Central Intelligent Agency (CIA) states that the United Kingdom (UK),. Ch. engchi. consisting of Great Britain, Wales, Scotland and Northern Ireland over several decades played a leading role in the creation and development of parliamentary democracy and in advancing literature and science. At the time of the 20th century and after the two world wars, it is evident that the UK lost its strength and even more when the Irish Republic withdrew from the Union. These were hard times for the UK, as the second half of the century observed not only a disintegration of the Empire, but the UK strived to rebuild itself into a modern and prosperous. 23. http://mecometer.com/country/the-gambia/economy/. 23.

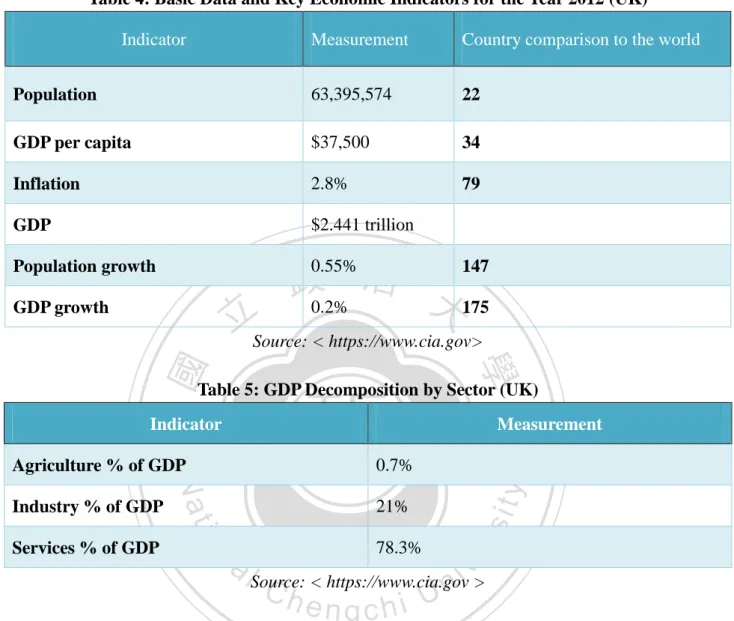

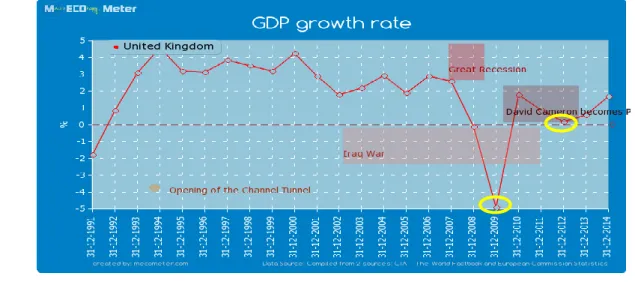

(33) European Union.24. UK is a member of the EU even though it keeps itself from taking part in the Economic and Monetary Union of the EU. It is one of the founding father of the Commonwealth, and NATO. The UK is located at the Western part of Europe, between the North Atlantic Ocean and the North Sea; Northwest of France. It has a total land area of 243, 610 square km.25 The natural resource deposits of the UK are Coal, Petroleum, Natural Gas, Iron Ore, Lead, Zinc, Gold, Tin,. 政 治 大 population life expectancy is 80.29 years. Distribution of its religious sets are thus: Christian 立 Limestone, Salt, Clay, Chalk, Gypsum, Potash, Silica Sand, Slate, and Arable Land. The. ‧ 國. 1.6%, unspecified or none 23.1% (CIA The World Factbook).. 學. (Anglican, Roman Catholic, Presbyterian, Methodist) 71.6%, Muslim 2.7%, Hindu 1%, other. ‧. Macroeconomic Data. y. Nat. sit. In Europe, UK is the third largest leading economy after Germany and France (EU business. n. al. er. io. (2013)).26 Agriculture in the UK plays a pivotal role in sustaining its food basket. It produces. i n U. v. about 50% of the food need of the country and uses a labor force of less than 2%. United. Ch. engchi. Kingdom’s agricultural sector is highly mechanized and intensive. The sector is very efficient and meets the European standard.27. 24. https://www.cia.gov/library/publications/the-world-factbook/geos/uk.html. 25. https://www.cia.gov/library/publications/the-world-factbook/geos/uk.html. 26. http://www.eubusiness.com/europe/uk. 27. https://www.cia.gov/library/publications/the-world-factbook/geos/uk.html. 24.

(34) Table 4: Basic Data and Key Economic Indicators for the Year 2012 (UK) Indicator. Measurement. Country comparison to the world. Population. 63,395,574. 22. GDP per capita. $37,500. 34. Inflation. 2.8%. 79. GDP. $2.441 trillion 0.55% 147 政 治 大 0.2% 175. Population growth GDP growth. 立Source: < https://www.cia.gov>. ‧ 國. 學. Table 5: GDP Decomposition by Sector (UK) Measurement. 0.7%. Agriculture % of GDP. y 78.3%. n. al. Ch. sit. 21%. er. io. Services % of GDP. Nat. Industry % of GDP. ‧. Indicator. i n U. v. Source: < https://www.cia.gov >. engchi. The global financial crisis in 2008 left a huge mark in the economy of the UK simply because it affected its financial systems, which were important economic drivers of the country. The home prices plummeted, high consumer debt, and the global economic downturn compounded UK’s economic difficulties. This further affected the prices of mortgages thus making life the most miserable. To overcome these difficulties, the UK government putted in place a number of measures to stimulate the economy and stabilize the financial systems. Some of these measures include: (I) Nationalization of part of the banking system, (II) cutting of taxes. 25.

(35) temporally, (III) suspension of public sector borrowing rules, etc.28. There had been higher than expected growth in the service sector of the UK in 2012, which speculators at the time believe would help the UK from the thorns of economic recession. At some point there were hopes that the economies were picking up and overcoming the troubles. According to a business survey in 2012, the UK’s dominant service sectors, which included hairdressers, banks and transport systems enjoyed a jump in activity for the first 3 months of. 政 治 大 Manufacturing sector which gave a lot of hope that the economy of the UK will avoid recession 立 the year 2012. In addition to this, the survey revealed a similar trend in the Construction and. ‧ 國. 學. (The Guardian (2012)).29. Agriculture in the UK uses about 70% of its total land area and it contributed 0.7% to 2012. ‧. GDP, see table 5 above. It’s interesting to note that despite the support received from the. y. Nat. sit. European Union in terms of skilled farmers, high technology, subsidies and fertile soil, the UK. n. al. er. io. still produces less than 60% of food its people consume. On top of the above issues, the. i n U. v. country’s farm earning is pretty low, due to low prices at the farm gate. It has gotten to a level. Ch. engchi. that fewer young people can actually meet the expenses of the rising capital requirement of entry into farming and more of these people are discouraged by the low earnings. 30. 28. https://www.cia.gov/library/publications/the-world-factbook/geos/uk.html. 29. http://www.theguardian.com/business/2012/apr/04/strong-uk-services-sector-survey. 30. http://en.wikipedia.org/wiki/Agriculture_in_the_United_Kingdom. 26.

(36) 政 治 大. Figure 4: GDP Growth over Period 1991 to 2014 (UK) Source: < http://mecometer.com >. 立. ‧ 國. 學. Figure 4 illustrate the GDP trend of the UK. Growth rate in 2012 was 0.2% with a global ranking of 175. Due to the 2009 global financial crisis, the country’s GDP went down the drain to -. ‧. 4.90%. This however improved in 2010 to 1.80%. Consequently, from 2010 to 2012 there had. y. Nat. n. al. Ch. engchi. er. io. subdued business investment weight on the economy.31. sit. been a continuous decline in GDP which was associated with weak consumer spending and the. i n U. v. Figure 5: Import Partners (UK) Source: < http://mecometer.com>. 31. http://en.wikipedia.org/wiki/Agriculture_in_the_United_Kingdom. 27.

(37) The UK imports goods such as manufactured goods, machinery, fuels; foodstuffs. Its highest import partners are Germany. Its total importation for the year 2012 stood at $642.6 billion.. 立. 政 治 大. ‧ 國. 學. Figure 6: Export Partners (UK) Source: < http://mecometer.com>. ‧. The products the country exports are manufactured goods, fuels, chemicals; food, beverages,. y. Nat. sit. tobacco. Germany again is its major export partner. Exports in the UK for the year 2012. n. al. er. io. constituted $474.6 billion.. 4.2. Banking Sector. Ch. engchi. i n U. v. 4.2.1. The Gambia The Gambia financial system over the years had developed rapidly and it is noticeably liberalized now. Direct controls have been removed and the economy’s interest rates are freely determined by the forces of demand and supply. The country has no stock exchange market. However, commercial banks are the dominant providers of financial services in the country.. The numbers of banks in the country increased from 4 in 2001 to 14 in 2009 (IMF Country Report No. 12/17(2012)). In response to the weakening environment in the financial systems in 2010, the Central Bank of The Gambia announced to raise banks capital requirements from 28.

(38) GMD60 Million (2.2 Million dollars) to GMD150 Million (5.5 Million dollars) by end 2010, and to GMD200 Million (7.4 Million dollars) by end-2012 (IMF Country Report No. 12/17(2012)). All banks complied with the new regulation. Banks in The Gambia are adequately capitalized and liquid with an average risk-weighted capital adequacy ratio of 25.6% in June 2011, which is above the 8% minimum requirement stipulated by the 2003 Financial Institutions Act of the Central Bank of The Gambia.32. 政 治 大 banks, one is Islamic and 11 Conventional banks. The largest commercial bank both in size and 立 At present, there are 12 banks (two dropped out in the earlier 2011 to 2013). Out of these 12. ‧ 國. 學. asset is a foreign subsidiary of the United Kingdom based Standard Chartered Bank, which is 25% Gambian owned (Alisa Alston, Marianne Moukhtara). In 2011, only one Conventional. ‧. bank was majority – owned by Gambian Nationals (Trust Bank Gambia Limited).33 Most of. sit. y. Nat. the new banks that came in from 2007 to 2009 are foreign owned Nigerian banks, which. io. n. al. er. produced substantial Foreign Direct Investments for the country.. i n U. v. The chief executive of one of the Nigerian banks (Guaranty Trust Bank Gambia (GTB)), Lekan. Ch. engchi. Sanusi in August 2011, was reported as saying in the African Banker news online that the banking system in the Gambia witnessed improvements and that customers are now exposed to robust and competitive banking and improved service delivery. According to the GTB chief executive, some Nigerian banks had recorded major achievements in profitability, branch network expansion and product differentiation. One of the discoveries in The Gambia that makes banking interesting to Nigerian banks is what the report called “goldmine in the business. 32. www.africaneconomicoutlook.org. 33. http://www.africaneconomicoutlook.org/. 29.

(39) of cash shipments”. The process, led mainly by Nigerian banks operating in the country under an agreement with Credit Suisse, involves the transfer of large quantities of foreign currencies by traders and importers on weekly basis to beneficiaries abroad.34. The banks in The Gambia can be categorized in to three groups. Group 1 composed of three large banks which constituted about 57% of total assets and loans in the industry at end of December 2010. Group 2 comprise three median banks which accounts for about one fourth. 政 治 大 and 23% of loans of the industry (IMF Country Report No. 12/17 (2012)). Commercial banks 立. (¼ ) of total assets and loans. Group 3 consists of six small banks that account for 20% of assets. ‧ 國. 學. in The Gambia offer a variety of banking services such as trade finance and credit, dealing in foreign exchange and equity participation and deposits. Other financial systems in the country. sit. y. Nat. Bureaus.. ‧. include Insurance Companies, Micro Finance Institutions and several Foreign Exchange. er. io. Table 6: Commercial Banks in The Gambia. n. a Company iv l C n Standard Chartered Bank Gambia Ltdh e ngchi U. Year Established 1894. Arab Gambia Islamic Bank. 1994. Trust Bank Ltd. 1997. First International Bank. 1999. Guaranty Trust Bank Gambia Ltd. 2002. International Commercial Bank. 2005. Access Bank Gambia Ltd. 2007. 34. http://africanbusinessmagazine.com/african-banker/reforms/banking-in-west-africa. 30.

(40) Eco-bank (Gambia) Ltd.. 2007. Bank Sahelo‐Saharienne Pour L’investissement et le commerce. 2008. Oceanic Bank (Gambia) Ltd. (Liquidated). 2008. Bank PHB. 2008. Sky Bank Gambia Ltd. 2008. Zenith Bank Gambia Ltd. 2009. Prime Bank Gambia Ltd (Liquidated). 2009. 政 治 大. Source: < http://fic.wharton.upenn.edu/fic/africa/Gambia%20Final.pdf >. 立. 2007 2008. 2011. 19.6. 18.8. 24.5. 24.8. 20.0. y. 21.0. 19.0. 27.0. 25.6. 10.4. 13.7. 12.3. 14.5. 12.7. 5.8. 4.3. 7.5. 6.4. 4.5. 0.1. -1.6. 0.4. 1.2. Return on Equity (average). 36.4. 0.8. -24.9. 1.8. 5.8. Net Interest income to gross income. 43.7. 35.3. 37.0. 41.3. 37.4. Operating expenses to gross income. 47.0. 65.8. 62.0. 58.2. 57.8. Regulatory capital to risk weighted assets. 22.5. Nat. n. al. sit er. io. Nonperforming loans to total gross loans. i n U. v. Nonperforming loans net of provisions to 2.8 capital Earnings. 2010. June. Tier-1 capital to risk weighted assets.35. Asset Quality. 2009. ‧. Capital Adequacy. ‧ 國. Indicator. 學. Table 7: The Gambia Financial Soundness Indicators (In percent, unless otherwise indicated). Ch. engchi. & Return on Assets (average). profitability. 35. Tier-1 capital is larger than regulatory capital due to the supervisory deduction from premises. revaluation.. 31.

(41) Liquidity. Exposure to FX risk. Liquid assets to total assets. 45.0. 43.6. 35.7. 47.9. 38.6. Liquid assets to short-term liabilities. 74.9. 70.9. 62.1. 68.4. 59.4. Net open FX position to capital. 36.9. 19.1. 6.4. -0.4. -2.9. Source: < International Monetary fund (IMF Country Report No. 12/17, 2012)> The industry’s asset quality has weakened over the years, and provisioning has not kept up. Nonperforming loans increased from 5% to total loans and advances in 2005 to 14.5% at end of 2010. However, in June 2011 Nonperforming loans fell by 2%. Profitability deteriorated,. 政 治 大. turning negative in 2009, but began to pick up in 2010. From 2007 to 2009, return on assets. 立. (ROA) and return of equity (ROE) dropped from 4.5% to -1.6% and from 36.4% to -24.9%. ‧ 國. 學. respectively. Both ratios changed positive from 2010, reaching 1.2 and 5.8 respectively by June. ‧. 2011, owing to banks efforts to improve their portfolios (IMF Country Report No. 12/17 (2012)).. sit. y. Nat. 4.2.2. United Kingdom. al. er. io. Several years ago before the financial crisis, UK financial sector grew very fast, in fact it grew. v. n. twice as fast as the country’s economy as a whole (Burgess (2011)). The present size of financial. Ch. engchi. i n U. sector in the UK shows how heavily the UK economy relies on financial services. Currently banks incorporated in the UK are 163 banks. Number of banks incorporated outside the European Economic Area (EEA) authorized to accept deposits through a branch in the UK are 80 banks. Furthermore, number of banks incorporated in the EEA entitled to accept deposits through a branch in the UK are 73 banks.36 Therefore, there is no doubt that the financial sector has a significant influence on the real economy of the UK.. Islam is the second largest religion in the UK. Results of the United Kingdom census 2011. 36. http://www.bankofengland.co.uk/pra/Pages/authorisations/banksbuildingsocietieslist.aspx. 32.

(42) suggested that the Muslim population in the UK had reached 2.7 million, 4.8% of the total population.37 Before 2000, there were no Islamic bank facilities available to Muslims in the UK even though the Muslim population wanted to spend their lives according to their religion. Ahmad (2008) states that Islamic banking in the UK commenced in 2003. From then to date, there are numerous banks in the UK that offer Sharia compliant instruments of banking. The major ones are Bank of London and Middle East plc. (BLME) and Islamic Bank of Britain. BLME is the largest Islamic bank in EU and the UK and has received several awards for being. 政 治 大. the best Islamic bank in the EU (Islam 101).38 In addition to these two Islamic banks is Ahli. 立. United Bank, which over the years received a number of awards too. The bank is not strictly. ‧ 國. 學. Islamic but does offer a sharia compliant loan to its customers.. ‧. According to the British National Party, sharia compliant banks in the UK offer no-interest. sit. y. Nat. transaction to Muslims, whereas the British people encounter increasing interest burdens on. io. al. er. banking transaction. Sharia compliant banks moreover, had enjoyed tax relief from the. n. government of UK on sharia compliant mortgages, which the British party considers. Ch. 39. discriminating to the non-Muslim population.. engchi. i n U. v. 37. http://en.wikipedia.org/wiki/Islam_in_the_United_Kingdom. 38. http://learnislam1.blogspot.tw/2011/06/best-islamic-banks-in-uk.html. 39. http://www.bnp.org.uk/news/islamic-banking-sector-britain-now-bigger-pakistan. 33.

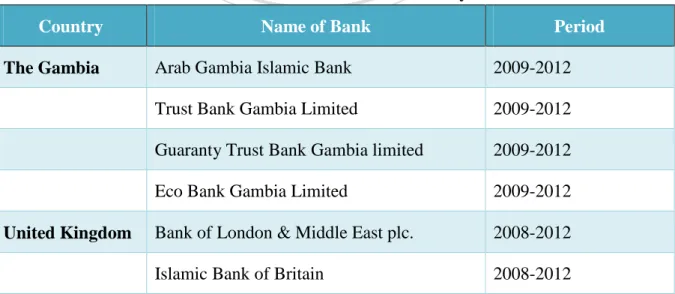

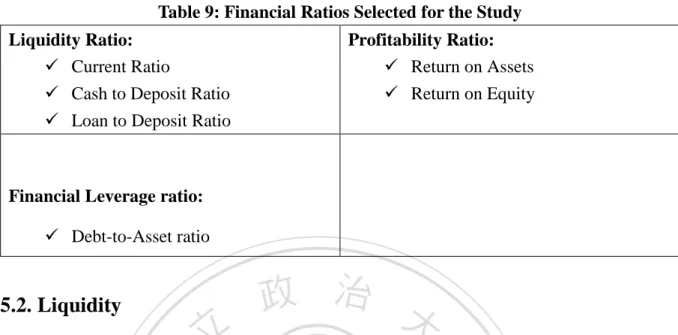

(43) 5. Performance Evaluation Criteria 5.1. Methodology This requires gathering relevant data from the financial statements of banks and to conduct a comparative analysis of the results. Complete data on bank especially AGIB in The Gambia was not readily available from the bank. Therefore, most of the data used in this research is collected from the Central Bank of the Gambia (CBG). Data is compiled from income statements and balance sheets of the chosen banks. The use of financial ratio in measuring bank. 治 政 performance is common in research works. This study大 is therefore aimed at conducting an 立 empirical analysis and to use financial ratios to determine the performances of selected Islamic ‧ 國. 學. and Conventional banks both in The Gambia and UK. Four major banks which include three. ‧. Conventional banks and one Islamic bank are selected in The Gambia. Moreover, four banks which include two Islamic and two Conventional banks are selected in the UK. Data for banks. y. Nat. er. io. sit. in the UK each year is collected from their annual reports (Income and Balance Sheet Statements). Financial information from 2008/2009 to 2012 are used for the study. The names. n. al. Ch. i n U. of the banks selected for the study are mention in table 8.. engchi. v. Table 8: Selected Banks for the Analysis Country The Gambia. United Kingdom. Name of Bank. Period. Arab Gambia Islamic Bank. 2009-2012. Trust Bank Gambia Limited. 2009-2012. Guaranty Trust Bank Gambia limited. 2009-2012. Eco Bank Gambia Limited. 2009-2012. Bank of London & Middle East plc.. 2008-2012. Islamic Bank of Britain. 2008-2012. 34.

(44) China Construction Bank UK ltd. 2008-2012. British Arab Commercial Bank plc.. 2008-2012. The criteria used to select banks for the study are thus: . Selected the only Islamic bank in The Gambia and compare it with a group of three Conventional banks. Trust Bank Gambia is chosen because it’s the only bank majority owned by Gambians. Guaranty Trust bank is chosen because out of the current Nigerian. 政 治 大 market by the CBG. Consequently, Eco Bank Gambia is selected for the study simply 立 banks in existence, it is the first bank to be granted license to operate in The Gambian. ‧ 國. 學. because it’s the only Pan African bank in the country and had over the years done well. In addition to these features, they are chosen owing to the fact that they are part of the. ‧. dominant banks that contributed about 82% of total industry assets and loans (IMF. y. sit. The Islamic banks selected in the UK for this study are chosen because they are the best. io. er. . Nat. Country Report No. 12/17 (2012)) which makes them systematically important banks.. al. v i n C h it to the top 150 fact that its parent company made e n g c h i U banks “worldwide ranked by asset n. Islamic banks in the UK.40 Furthermore, China Construction Bank is chosen based on the. sized”. 41 Moreover, British Arab Commercial Bank is chosen because it is one of the Conventional banks incorporated in the United Kingdom, a wholesale bank and a leading provider of trade and project finance for Arab markets. The financial ratios selected to compare the performance of Islamic and Conventional banks are thus:. 40. http://learnislam1.blogspot.tw/2011/06/best-islamic-banks-in-uk.html. 41. http://www.cba.ca/contents/files/statistics/stat_bankranking_en.pdf. 35.

(45) Table 9: Financial Ratios Selected for the Study Liquidity Ratio: Current Ratio Cash to Deposit Ratio Loan to Deposit Ratio. Profitability Ratio: Return on Assets Return on Equity. Financial Leverage ratio: Debt-to-Asset ratio. 5.2. Liquidity. 立. 政 治 大. Liquidity provides information about a firm’s ability to meet its short term obligations as and. ‧ 國. 學. when they fall due. Liquidity is important for a firm’s survival, because its helps a firm avoid defaulting on its short term liabilities. When a company cannot collect cash or short term funds. ‧. from its customers on a regular and timely basis, the company will soon experience financial. y. Nat. sit. distress. Therefore, the higher the liquidity of a bank, the greater its ability to meet its short. n. al. er. io. term obligation. This is an indication that the bank is doing well. Consequently, liquidity. i n U. v. problems can arise when a bank’s withdrawals significantly exceed its deposits over a short. Ch. engchi. period of time (Samad and Hassan (2000)).. Several ratios are used by banks and other companies to measure liquidity, but in this study the following ratios will be used:. 36.

(46) 5.2.1. Current Ratio (CR) This is the ratio of current assets to current liabilities.. CR =. Current Assets. (1). Current Liabilities. Typical values for current assets differ from firm to firm and from industry to industry. Short term creditors would prefer a higher current ratio since it will reduce their risk exposures.. 治 政 大 of a firm are more than twice its assets are used to grow the business. When the current assets 立 current liabilities, it is an indication that the company has enough cash to pay its short term Whereas shareholders would prefer a lower current ratio so that more of the firms short term. ‧ 國. 學. debts. This is quite encouraging for the firm.42. ‧. 5.2.2. Cash to Deposit Ratio (CDR). Nat. sit. y. This is the ratio of total cash balances against total deposits in a bank. Therefore too much of it. n. al. er. io. can result to a bank losing profits, so most banks try not to hold too much, instead they try to. i n U. v. find a balance in their positions. Furthermore, they cannot afford to hold less cash.. 𝑪𝑫𝑹 =. 𝑇𝑜𝑡𝑎𝑙 𝑐𝑎𝑠ℎ. Ch. engchi. 𝑇𝑜𝑡𝑎𝑙 𝐷𝑒𝑝𝑜𝑠𝑖𝑡. (2). Cash plays an important role in the liquidity of a bank. However, holding a lower than necessary of cash reserves could lead to a distress and failure to meet short term obligations. Therefore, deposits trust to a bank is enhanced when the bank maintains a higher cash deposit ratio (Samad and Hassan (2000)).. 42. http://www.netmba.com/finance/financial/ratios/. 37.

(47) 5.2.3. Loan to Deposit Ratio (LDR) This is the ratio between a bank’s total loans to its total deposits. The formula is equal to. 𝑳𝑫𝑹 =. 𝐿𝑜𝑎𝑛. (3). 𝐷𝑒𝑝𝑜𝑠𝑖𝑡. Generally when LDR ratio is lower than 1, it means that the bank uses its own deposits to make loans to its customers, without any outside borrowing. However, when a banks LDR is greater. 治 政 大 Banks may not be earning an at higher interest rates, rather than relying on its own deposits. 立 optimal return when the ratio is too low. When the ratio is too high, the bank may lack liquidity. than 1, it implies that the bank borrows money and in turn used the money to lend to customers. ‧ 國. 學. to comply in meeting its short term obligations.43. ‧. 5.3. Profitability. sit. y. Nat. This is one of the most frequent financial measure of a firm’s success in generating profits. It is. n. al. er. io. used to compute a firm’s bottom line and returns to its investors. Profitability determines the. i n U. v. overall efficiency and performance of a bank. It measures the difference between revenues and. Ch. engchi. cost. This study is going to use two variables to measure profitability. For these ratios, the higher the value, the more desirable it is for the firm. A higher ratio indicates that the bank is doing well and is good at generating profits, revenues and cash flows. The ratios are going to assess the ability of a firm to generate income after offsetting all its cost and expenses during a specific time period.. 43. http://en.wikipedia.org/wiki/Loan-deposit_ratio. 38.

(48) 5.3.1. Return on Assets (ROA) This measures how efficient a firm uses its assets to generate profits. The formula is thus:. 𝑹𝑶𝑨 =. 𝑁𝑒𝑡 𝑖𝑛𝑐𝑜𝑚𝑒. (4). 𝑇𝑜𝑡𝑎𝑙 𝑎𝑠𝑠𝑒𝑡𝑠. ROA tell us what a firm can do with its assets. That is how much money they earn on each asset they control. Its shows how a firm can convert its assets into earnings. The higher the ratio, the. 治 政 大 its use of assets to generate profits. 立. better the performance of the firm. A lower ratio is an indication of managerial inefficiency in. ‧ 國. 學. 5.3.2. Return on Equity (ROE). This measures the Rate of Return as a percentage of shareholders equity. ROE is defined as. y. Nat. sit. 𝑁𝑒𝑡 𝑖𝑛𝑐𝑜𝑚𝑒. io. 𝑆ℎ𝑎𝑟𝑒ℎ𝑜𝑙𝑑𝑒𝑟𝑠 𝐸𝑞𝑢𝑖𝑡𝑦. n. al. (5). er. 𝑹𝑶𝑬 =. ‧. follows:. Ch. i n U. v. ROE shows how well a firm uses shareholder’s funds to generate earnings growth. High ROE. engchi. indicates better managerial performance. Therefore, the higher the ROE compared to the industry, the better for a firm.. 5.4. Financial Leverage This measures the solvency of the company. It also measures the extent to which a company uses long term debt. Companies with very high leverage ratios are usually considered to be at. 39.

(49) risk of bankruptcy. Financial leverage is not always bad because it can lead to an increase in return on shareholders’ investment.44. 5.4.1. Debt-to-Asset Ratio (DAR) Debt is a measure of total debt to total asset. This tells us how much a company depends on debt to finance assets. It also shows how much debt a company has on its balance sheet compared to its assets. The formula is thus: 𝑇𝑜𝑡𝑎𝑙 𝐷𝑒𝑏𝑡 𝑇𝑜𝑡𝑎𝑙 𝐴𝑠𝑠𝑒𝑡. 立. 政 治 大. ‧. n. al. er. io. sit. y. Nat. 44. (6). 學. ‧ 國. 𝑫𝑨𝑹 =. Ch. engchi. http://www.readyratios.com/reference/debt/#ref835. 40. i n U. v.

數據

+7

相關文件

世界銀行(World

Contribute to the global LMS community and inform about the challenges and opportunities for executing computer- based assessment using the LMS platform in Hong Kong secondary

and Jorgensen, P.l.,(2000), “Fair Valuation of Life Insurance Liabilities: The Impact of Interest Rate Guarantees, Surrender Options, and Bonus Policies”, Insurance: Mathematics

位於沿江中路 193 號,建於 1924 年,現為廣州人民銀行分行。中央銀行原為「聯俄容共」政策的

Teacher extends the discussion of a series of cash flows to uneven cash flows and explains the calculations of future and present value of a series of uneven cash flows. PPT#56

For example, even though no payment was made on the interest expenses for the bank loan in item (vi), the interest expenses should be calculated based on the number of

interactions between Europe and Asia in Medieval Times—3: Developments in trade and civilisation of Islam from the 7th to 15th centuries

• If the same monthly prepayment speed s is maintained since the issuance of the pool, the remaining principal balance at month i will be RB i × (1 − s/100) i. • It goes without