新加坡的金融中心發展-內部與外部因素 - 政大學術集成

100

0

0

全文

(2) 新加坡的金融中心發展-內部與外部因素 Singapore’s Financial Cluster in Light with Internal and External Forces 研究生 : 何杰鴻. Student: Jérôme Jean Maurice Hernad. 指導教授 : 姜家雄. Advisor: Alex Chiang. 治 政 國立政治大學 大 碩士論文. 學. ‧ 國. 立 亞太研究英語碩士學位學程. io. sit. y. ‧. Nat. A Thesis. er. Submitted to International Master’s Program in Asia-Pacific Studies. al. n. v i n C h Chengchi University National engchi U. In partial fulfillment of the Requirement For the degree of Master of Arts. 中華民國 103 年 7 月 July 2014.

(3) Acknowledgements. I would like to express my greatest appreciation and thanks to my advisor Dr. Alex Chiang who has been of a tremendous help through his encouragements and valuable comments. Without his support and guidance this project would not have been possible. I would also like to thank my committee members, Dr. Chang Wenyang and Dr. Chiou Yi-hung for their constructive feedbacks. Special thanks to the Secretary of the International Master's Program in AsiaPacific Studies, Grace Tsao. Owing to her kindness and dedication, she was always able to guide me.. 治 政 大not least, words cannot express research, and helped me put pieces together. Last but 立parents, Patrice Hernad and Dr. Francine Hernad, for all of how grateful I am to my. I would especially like to thank my friends who were always there through my. ‧. ‧ 國. 學. their sacrifices, and advice that incented me to strive towards my goal.. Jérôme, Jean, Maurice Hernad. Nat. n. al. er. io. sit. y. Taipei, Taiwan. Ch. engchi. i. i n U. v.

(4) Abstract. The Republic of Singapore has long had a voluntary policy of developing its financial sector, and making it an essential part of its economy. This thesis aims at filling in the gaps of the current knowledge about Singapore’s financial cluster, through an in-depth analysis of Singapore’s unique set of banking and financial regulations, and recent developments that include the education of financial managers, the rise of. 政 治 大 The time frame used to analyze it spans from the liberalization of 立. Islamic finance, and the internationalization of the Renminbi.. Singapore’s financial and banking sector, which started in 1999, till 2014.. ‧ 國. 學. The framework of Porter’s ‘Diamond model’ has been used to outline the. ‧. strength, and weaknesses of the financial cluster.. Shortcomings and successes of Singapore’s financial cluster have. y. Nat. sit. been evaluated by analyzing primary sources available, and by examining. er. io. the local environment.. n. a Singapore’s financial cluster still lacks critical v mass in comparison to that of its. i l C n rival, Hongh e Kong. Furthermore, ngchi U. weaknesses remain in. regards to the educational level of financial and banking managers. The recent developments to set Singapore as an offshore Renminbi center can only be acclaimed, however its main focus on the People’s Republic of China, needs to be broadened, to include the overall Southeast Asian region.. Key words: Singapore, finance, banking, cluster. ii.

(5) 論文摘要. 新加坡共和國(以下簡稱新加坡)長期以來致力推動該國金融產 業的自主性發展,並強化該產業成為國家經濟動能的要角。 本論文擬深度剖析新加坡獨特的銀行與金融法規,並分析新加 坡在金融業經營管理人才的教育培訓、伊斯蘭金融體系的崛起、人 民幣國際化等政策面向所做的努力,以彌補現有學術領域對該國金 融業研究的不足和缺口。. 政 治 大 1999 年,截至 2014 立年為止;而在分析架構方面,我們採用 Michael 本文所採用的分析期間從新加坡啟動金融業自由化開始的. ‧ 國. 學. Porter 的產業鑽石模型來勾勒出新加坡金融業的產業競爭優勢。 此外,我們藉由檢驗已取得的原始資料與當地市場的條件分. ‧. 析,進一步評估存在於新加坡金融體系的潛在風險和成功要素。. sit. y. Nat. 從本文分析結果顯示,新加坡金融業仍缺乏於其競爭對手-香. er. io. 港所擁有的關鍵性經濟規模;此外,該國在金融業經營管理人才的. a 培訓成效上仍然不足。 n. iv l C n hengchi U 儘管新加坡政府宣稱將推動該國成為人民幣的境外金融中心,. 然而該政策僅著重在中華人民共和國的市場開發,並非擴展及整個 東南亞區域。. iii.

(6) TABLE OF CONTENTS Chapter 1.. Introduction ............................................................................................ 1. 1.1 Overview ........................................................................................................... 1 1.2 Purpose of the research ..................................................................................... 2 1.3 Theoretical framework ...................................................................................... 3 1.3.1 Cluster theory ............................................................................................. 3 1.3.2 Porter’s diamond model ............................................................................. 4 1.3.2.1 Overview .............................................................................................. 4 1.3.2.2 Demand conditions ............................................................................... 5 1.3.2.3 Factor conditions .................................................................................. 5. 政 治 大 1.3.2.5 Firm strategy, structure and rivalry ...................................................... 6 立 1.3.2.6 Limitations of Porter’s diamond model ................................................ 6 1.3.2.4 Related and supporting industries ........................................................ 6. ‧ 國. 學. 1.3.3 Summary .................................................................................................... 7 1.4 Literature review ............................................................................................... 7. ‧. 1.5 Background information ................................................................................... 9 1.5.1 Development stages of the Republic of Singapore .................................... 9. y. Nat. sit. 1.5.1.1 The path to self-governance and independence.................................... 9. al. er. io. 1.5.1.2 The Republic of Singapore’s first industrial revolution and the. n. following turmoil ............................................................................................. 11. Ch. i n U. v. 1.5.1.3 The second industrial revolution: A hazardous journey ..................... 12. engchi. 1.5.1.4 The 1991 Strategic Economic Plan: a turning point ........................... 14 1.6 Chapters layout ............................................................................................... 16 Chapter 2.. Emergence of Singapore as a Full-bodied Financial and Banking. Cluster, and Performance from 1997 to 2013 .............................................................. 17 2.1 The 1997 Asian Financial Crisis: a wake up call for Singapore’s financial center ........................................................................................................................ 17 2.1.1 Impact on Asia ......................................................................................... 17 2.1.2 Impact on Singapore................................................................................. 19 2.1.3 Impact on the Singapore Dollar................................................................ 20 2.1.4 Impact on Singaporean banks .................................................................. 22. iv.

(7) 2.1.5 Impact on the Stock Exchange of Singapore (SES) and the Singapore International Monetary Exchange Limited (Simex) ............................................ 22 2.2 Liberalization of Singapore’s Financial and Banking Market: Singapore’s answer to the 1997 Asian Financial Crisis ............................................................... 23 2.2.1 First phase of the reform .......................................................................... 24 2.2.1.1 Qualifying Full Banks ........................................................................ 24 2.2.1.2 Restricted banks.................................................................................. 25 2.2.1.3 Offshore banks.................................................................................... 25 2.2.2 Second phase of the reform ...................................................................... 25 2.2.2.1 Outcome for local banks ..................................................................... 26 2.2.2.2 New license scheme for foreign banks ............................................... 26. 治 政 大..................................................28 2.3 Specificities of Singapore’s financial cluster 立 2.3.1 Asian Dollar Market ................................................................................. 28 2.2.2.3 Outcome for foreign banks ................................................................. 27. ‧ 國. 學. 2.3.1.1 Asian Currency Units ......................................................................... 28 2.3.1.2 Asian Dollar Bond Market ................................................................. 31. ‧. 2.3.2 The Banking Act and the Trust Companies Act: guarantors of Singapore’s status as a “tax heaven” ................................................................... 33. Nat. sit. y. 2.3.2.1 Singapore’s Banking Act .................................................................... 33. er. io. 2.3.2.1.1 Impact of the 2008 financial crisis on the Banking Act............... 34 2.3.2.2 Singapore’s Trust Companies Act ...................................................... 35. n. al. Ch. i n U. v. 2.3.3 Summary .................................................................................................. 36. engchi. 2.4 Case study of the impact of the liberalization on three banks operating in Singapore ................................................................................................................. 36 2.4.1 Recent performance of Singapore’s domestic banks ............................... 37 2.4.2 Singapore’s “Big Three” from 1997 to 2013 ........................................... 38 2.4.2.1 DBS .................................................................................................... 38 2.4.2.2 OCBC ................................................................................................. 39 2.4.2.3 UOB .................................................................................................... 40 2.4.2.4 Summary............................................................................................. 40 2.5 Evaluation of the evolution of Singapore’s banking and financial market ..... 43 2.5.1 Singapore’s foreign exchange market ...................................................... 43 2.5.2 Singapore’s stock market ......................................................................... 44 2.5.2.1 Attractiveness of SGX for foreign companies.................................... 45 v.

(8) 2.5.2.2 The ASEAN Trading Link ................................................................. 46 2.5.3 Private banking and wealth management in Singapore ........................... 47 2.5.3.1 Private banking ................................................................................... 47 2.5.3.1.1 The importance of HNWIs ........................................................... 48 2.5.3.2 Wealth management ........................................................................... 50 2.5.3.2.1 Influence of CPF on Singapore’s wealth management industry .. 52 Chapter 3.. Factor Conditions and Global Linkages at Play in Singapore’s. Financial Cluster .......................................................................................................... 53 3.1 Introductory remarks ....................................................................................... 53 3.2 Education and capacity building: a crucial factor condition ........................... 53 3.2.1 Educational offer aimed at the banking and financial sector ................... 54. 政 治 大 Industry Competency Standards, and of the Wealth Management Institute .... 55 立 3.2.2 Scholarships programs ............................................................................. 56 3.2.1.1 Impact of the Institute of Banking and Finance, of the Financial. ‧ 國. 學. 3.2.3 The issue of skilled labor immigration in light with the performance of the local workforce in the banking and financial sector ...................................... 56. ‧. 3.3 Islamic Finance ............................................................................................... 58. y. Nat. 3.4 The Renminbi factor ....................................................................................... 60. sit. 3.4.1 The internationalization of the RMB: historical development ................. 60. er. io. 3.4.2 Where does Singapore stand in the race to become a major RMB offshore. al. n. v i n C hits internal financialUmarket, is it too late for 3.4.3 As China develops engchi Singapore to enter the competition? .................................................................... 63 center? .................................................................................................................. 62. Chapter 4.. Conclusion ........................................................................................... 64. 4.1 Concluding remarks ........................................................................................ 64 4.1.1 Evaluation of Singapore’s financial cluster: strengths and weaknesses .. 65 4.2 Policy recommendations ................................................................................. 66 References. .............................................................................................................. 67. Appendix. .............................................................................................................. 85. MAS statement on measures to liberalise commercial banking and upgrade local banks 17 May 1999 (Monetary Authority of Singapore, 1999)............................... 85. vi.

(9) LIST OF FIGURES AND TABLES. Figure 1. Porter’s Diamond Model ................................................................................ 5 Figure 2. GDP Growth (annual %) .............................................................................. 18 Figure 3. Evolution of License Scheme from 1999-2004 ............................................ 27 Figure 4. Popularity of ACUs from 1997 to 2014 ....................................................... 30 Figure 5. Size of Singapore’s Non-SGD Corporate Debt Market, from 1997 to 2012 (SGD, in billion) .................................................................................................. 32 Figure 6. Evolution of Total Assets Held by DBS, OCBC, and UOB from 1997 to 2013 (SGD, in million) ........................................................................................ 42. 治 政 1998, 2001, 2004, 2007, 2010, and 2013. ............................................................ 43 大 立 with the most Millionaires per Capita (% of total Figure 8. Top 10 Countries Figure 7. Share of Global Daily FX Turnover in Singapore, Hong Kong, and Japan in. ‧ 國. 學. population). .......................................................................................................... 49 Figure 9. Assets Under Management in Singapore from 1997 to 2012 (SGD, in. ‧. trillion) ................................................................................................................. 52. n. er. io. sit. y. Nat. al. Ch. engchi. vii. i n U. v.

(10) List of Acronyms. ACU: Asian Currency Unit ADB: Asian Dollar Bond Market ASEAN: Association of Southeast Asian Nations ATM: Automated Teller Machine BIBF: Bangkok International Banking Facility CEO: Chief Executive Officer CNH: Offshore Renminbi CNY: Onshore Renminbi CPF: Central Provident Fund. 政 治 大. DBS: Development Bank of Singapore. 立. DBU: Domestic Banking Unit. ‧ 國. 學. ESSEC: É cole Supérieure des Sciences É conomiques et Commerciales (Higher School of Economics and Business). ‧. ETF: Exchange-Traded Funds EU: European Union. Nat. sit. y. FICS: Financial Industry Competency Standards. io. al. n. FT: Foreign Talent. er. FSDF: Financial Sector Development Fund. GDP: Gross Domestic Product. Ch. engchi. HNWI: High-Net-Worth Individual. i n U. v. HSBC: The Hongkong and Shanghai Banking Corporation IBF: Institute of Banking and Finance ICT: Information and Communication Technology IFSB: Islamic Financial Services Board INSEAD: Institut Européen d'Administration des Affaires (European Institute of Business Administration) MAS: Monetary Authority of Singapore MNC: Multinational Corporation MOU: Memorandum of Understanding MRT: Mass Rapid Transit NASDAQ: National Association of Securities Dealers Automated Quotations viii.

(11) NEER: Nominal Effective Exchange Rate NPL: Non-Performing Loans OCBC: Oversea-Chinese Banking Corporation OECD: Organisation for Economic Co-operation and Development QFB: Qualifying Full Bank RMB: Renminbi SDCB: Singapore Dollar Corporate Bond Market SES: Stock Exchange of Singapore SESDAQ: Stock Exchange of Singapore Dealing and Automated Quotation SGD: Singapore Dollar SGX: Singapore Exchange. 治 政 大 SIMEX: Singapore International Monetary Exchange 立 UAE: United Arab Emirates SME: Small and Medium Enterprises. ‧ 國. 學. UBS: Union Bank of Switzerland UOB: United Overseas Bank. ‧. UK: United Kingdom USA: United States of America. y. Nat. n. al. er. io. sit. USD: United States Dollar. Ch. engchi. ix. i n U. v.

(12) Chapter 1. Introduction. 1.1 Overview Since the emotional time when former Prime Minister Lee Kuan Yew, the Father of Singapore, cried on "Television Singapura” after the separation from the Federation of Malaysia in 1965, Singapore has achieved tremendous growth, being a booming financial hub, and leading to improved living standards for the whole population. Nowadays the island through technocratic and pragmatic ruling has started to be considered, for the leaders of some countries, as a model to follow, for instance. 治 政 大have had more to do with urban should be kept in mind that the city-state’s policies 立 governance, rather than traditional policies enforced in a country mixing urban and. inspiring former Thai Prime Minister Thaksin Shinawatra (Jones, 2008). Yet, it. ‧ 國. 學. non-urbanized areas.. The Singapore Miracle can be explained through a better understanding of the. ‧. Developmental State (Liow, 2012). The Developmental State gives a good grasp at how the Republic has handled policy making, mixing an elite bureaucracy that was. y. Nat. sit. given scope to effectively taking initiatives, with market-conforming methods of state. al. n. (Stubbs, 2009).. er. io. intervention in the economy, and with pilot organizations to control industrial policies. Whilst most of. v i n C h Tigers, to some the Asian e n g c h i U extent,. moved away from the. Developmental State model in the 1990’s, Singapore was slower to abandon it compared to South Korea. As a result the Developmental State has forcibly shaped the country and the local financial cluster, and has remained in some ways a persistent influence (Stubbs, 2009). It has until today been successful, and it has translated into high capital accumulation, and strong levels of investment in various sectors, among which the financial sector. Some debate whether Singapore has been as much of a Developmental State as Taiwan, South Korea, and Japan, preferring to label the city-state as a "growth oriented autocratic regime” (Hayashi, 2010). Whatever is the label given to. 1.

(13) Singapore, it has clearly adopted policies and regulations that are quintessential of the Development State, and that have helped the rise of an efficient financial center.. 1.2 Purpose of the research This thesis will aim at looking at the impact of policies adopted in the financial sector from 1997 onward through the prism of the cluster theory, in the light of internal and external forces. I wish to shed the light on the links between these three variables, and analyze how they work altogether in the financial cluster that Singapore forms. The most important internal forces considered are the regulatory and legislative environments, and the local workforce involved in the sector.. 政 治 大 internationalization 立 and the rise in the. The main external forces taken into account are the rise of Islamic finance,1 the RMB 2. ‧ 國. 學. Individuals (HNWIs)3 in Asia.. number of High-Net-Worth. The year 1997 marked the start of the Asian financial crisis, while Singapore withstood the crisis relatively well compared to neighboring countries. It nevertheless. ‧. prompted the city-state to liberalize its financial service sector. Consequently since. y. Nat. 1999 the government has decided to enforce a series of policies to make finance a. sit. leading economic force, part of Singapore’s “twin engine of growth", on par with. er. io. manufacturing (Teo & Ang, 2001 p.361). Measures on how to implement these. al. n. v i n Ch May 17, 1999 statement, “Liberalising Banking and Upgrading Local e n gCommercial chi U. changes were made public by the Monetary Authority of Singapore (MAS)4 in its. Banks” (cf. Appendix) (Monetary Authority of Singapore, 1999).. 1. Islamic finance follows the principles of the Shariah, i.e. prohibition of getting involved in the payment or collection of interest charges. Thus if companies need capital, they would have to ask an investor to provide capital, at the end of the deal the capital-owner would receive a share of profits agreed upon before the signing of the deal. 2 The RMB (Renminbi) is the Chinese national currency. 3 HNWI is an individual with a net worth of more than 1 million USD (not including the primary residence). 4 The Monetary Authority of Singapore acts as Singapore’s central bank, but also as its financial regulatory authority (in most countries, these two functions are held by two different institutions). As the MAS holds these two major roles, any of the policies it launches have considerable impact on Singapore’s financial cluster. 2.

(14) Singapore has long been overlooked by academics that seem to prefer Hong Kong as their subject of research when it deals with finance clusters. However, Singapore, due to its nature as a country per se, has a clearer path ahead; on the contrary to Hong Kong that will see after June 30, 2047 the end of the Hong Kong Basic Law, which so far has allowed the Special Administration Region to be considered as a safe point of entry to the Chinese market. Therefore this research will aim at answering the following question: “In what measure the successful liberalization of Singapore’s financial cluster has been influenced by internal and external forces?” Throughout my research I will limit myself to the most relevant historical events (policies and developments) that have shaped Singapore’s financial sector, in. 治 政 analyzed. Concerning the data collection process,大 I will use primary and secondary 立 sources.. order to more clearly outline the connections and interactions between the variables. ‧ 國. 學. I hope this thesis will bring a more holistic approach to the current body of literature, by focusing on a broader set of variables, and adopting a case study. ‧. approach when necessary. As a result, I wish to make clearer the mutually beneficial spillover effects between these variables and Singapore’s financial sector.. sit. y. Nat. n. 1.3.1 Cluster theory a l. er. io. 1.3 Theoretical framework. Ch. engchi. i n U. v. There has been extensive research made by academics on clustering effects. The concept of cluster originates from previous researches focused on “Industrial district”, as first mentioned in Becattini’s paper entitled “Sectors and/or Districts: Some Remarks on the Conceptual Foundations of Industrial Economics” (1989). The emergence of “Industrial districts” is due to the combination of many factors, including economy of scale, multi-sectorial industries, stable environment, and abundance of labor. All that can foster the rise of whole areas called “Industrial districts”, unlike Clusters that are identified as geographic areas where a group of similar businesses are located. Efficiency and practicality are seen as the primary reasons leading to clusters’ development. Academics like Camagni (1991) developed the idea of clusters linked to the notion of “knowledge spillover”, where companies and institutions learn from each 3.

(15) other due to their close geographical location, and the subsequent ease with which information circulates. As far as Cooke (2003) and his followers are concerned, they drew more attention to “local knowledge spillovers”. Grabher (1993) interestingly added, to the current existing knowledge when speaking about clusters, a stress on “traded linkages” that increase economies- of scale. Porter (2000) on his side focused on how companies are interconnected in a specific field; most interesting is his use of the “external linkage” theory that studies synergies between local government, universities, etc. Martin (2003) for his part emphasized the “innovative milieu” that puts forward the discovery of new processes and technologies as the foundation for an optimal cluster. The ideas of a “global linkage” trend as developed by Grabher (1993), and the “global pipeline” as discovered by Bathelt, Malmberg and Maskell. 治 政 to develop on their own, secluded are no longer seen as isolated entities that seem 大 立 from the outside world, but also as phenomena that appear thanks to external factors. (2004) emphasize more on clusters through the prism of globalization. Thus clusters. ‧ 國. 學. Those last two developments of the cluster theory have strongly impacted the study of cluster areas as they show that clusters would be nothing without their overseas. ‧. interconnection. This thesis will therefore include an in-depth study of Singapore’s financial cluster in consideration to the latest regional and international developments. y. Nat. er. io. sit. in the financial world.. n. 1.3.2 Porter’s diamond a model 1.3.2.1 Overview. iv l C n hengchi U. Michael Porter in his book published in 1990 and entitled “The competitive advantage of nations” developed what is now known as the “diamond model”. This model aims at identifying and proving the existence of clusters in some specific areas and industrial sectors. His methodology can be divided into two steps, first identifying booming industries located in specific locations. The second step aims at proving the existence of a competitive advantage through the historical analysis of four main variables: demand conditions; factor conditions; related and supporting industries; and firm strategy, structure and rivalry. Government and chance are sometimes added, but are not crucial, which if taken into consideration would make it a five-variable model (Porter, 1990). 4.

(16) This model has so far been the only one used to study clusters in academic research, therefore it is worth reviewing it in order to better grasp the true essence of what a cluster is, but also to understand the limitations of this model.. Figure 1 Porter’s Diamond Model Demand conditions. Firm strategy, strucutre and rivalry. Factor conditions. 政 治 大. 立. ‧ 國. 學. Related and supporting industries. Source: Kaplan Financial Knowledge Bank, 2012.. ‧ sit. y. Nat. 1.3.2.2 Demand conditions. al. er. io. Demand in the home country is seen as vital to ensure that the industry in. n. which the cluster is specialized has a clear understanding of the needs of the. Ch. i n U. v. customers (individuals, firms, and government). The greater the demand is, the. engchi. greater the competition is, which means incentives for constant innovation and quality. For instance, in the financial sector the more locals have high standards and are educated concerning the financial products they consume, the more local banks and asset management firms will develop sophisticated investment vehicles fitting in with their needs (Porter, 1990, p. 82).. 1.3.2.3 Factor conditions Simple factor attributes, as plentiful natural resources or abundant workforce, constitute positive conditions. However factor conditions can be cultivated, such as the educational level of manpower, transportation infrastructure, pro-business legal environment, etc. In a financial cluster, this would translate with the need to have 5.

(17) access to a large pool of trained financial managers and bankers. Fast Internet broadband speed would also be crucial to ensure that “high-frequency trading” (HFT), which is usually operated within 30 milliseconds or less, is processed without any problems (Porter, 1990, pp. 79-82).. 1.3.2.4 Related and supporting industries Related and supporting industries are essential to ensure that clusters provide main industries with a full array of services and technologies indispensable to the optimal run of firms. Thus the cluster behaves like a one-stop shop where no external help is needed, hence positioning the cluster as a world-level hub. In the banking sector this would mean lower transaction costs thanks to readily available. 政 治 大. technologies in the same location (Porter, 1990, pp. 82-83).. 立. ‧ 國. 學. 1.3.2.5 Firm strategy, structure and rivalry. Firms with a long-term strategy are determinant as they focus on research, and. ‧. state-of-the-art services and products, thus ensuring a recurrent flow of customers. Rivalry to some extent is good as it guarantees that the cluster will grow past its. Nat. sit. y. natural factor endowment through increased competition. Consequently a free market. io. er. ensuring the lowest entry barriers, fair competition, and a strong legal framework should be put forward to ensure that for instance, a financial cluster and its institutions. n. al. Ch. i n U. v. have management structures as lean and organic as possible (Porter, 1990, pp. 83-86).. engchi. 1.3.2.6 Limitations of Porter’s diamond model Michael Porter developed the diamond model and the cluster theory, through a close study of ten developed countries, which consequently leaves Davies and Ellis (2000) wondering whether his work applies to developing countries, as there is no use of a control group. Furthermore, the existence of clusters can be debated in the case of small-scale and open economy; as whatever competitive advantage could exist, firms have no real choice about their location, such as in Singapore (a country with a total land area of a bit more than 687 square-kilometers, nearly 47 times smaller than Taiwan).. 6.

(18) Furthermore, in his book entitled the “The competitive advantage of nations” Porter was rather pessimistic about the case of Singapore that he viewed as a cluster whose only strong point was its factor conditions. This however has been proved wrong since he published his book, as the Republic has shown considerable ability in fostering the rise of two successful clusters, one in manufacturing, and the other in the financial sector. What’s more, he also missed the importance of multinational corporations (MNCs), which in some countries are more important than local companies, such as in the Singaporean banking sector (Yetton, Craig, Davis, & Hilmer, 1992). All in all, we can say that the diamond model has until today been the only major tool to analyze clusters, yet there are a few drawbacks linked to the non-. 政 治 大. scientific path used. Heavy reliance on deduction leads some academics to consider it as a non-relevant method.. 立. ‧ 國. 學. 1.3.3 Summary. To conclude, this thesis will primarily use the Porter’s diamond model as its. ‧. theoretical background, with a specific focus on factor conditions. The other three. io. n. er. 1.4 Literature review. al. y. sit. Nat. variables will be to a lesser degree used in this research.. Ch. i n U. v. The following literature review aims at specifically analyzing the literature. engchi. written about the liberalization of Singapore’s financial sector since 1998, and its subsequent development. This reform has tremendously changed the shape of the sector, and has led it to its successful stage. I will of course look at the shortcomings of current research, the debate over whether it qualifies or not as a cluster, and the study of external and internal forces that have shaped Singapore as the world level financial center it is now. First thing that is noticeable is the lack of academic research on the topic since the mid-2000s. While there is substantial information published by the Monetary Authority of Singapore, little has been done to analyze the data available. What’s more, papers that have aimed at researching the local financial cluster failed to include the various elements that have built it. Thus giving an incomplete image of the varied actors at play. 7.

(19) Torgovykh, Weinblum, Müller and Maier (2013) attempted to study Singapore’s financial cluster using Porter’s diamond model. However they applied it to Singapore’s business environment and not to the financial sector itself. Their most interesting finding is about the private banking sector, as they see banking secrecy as the city-state’s main competitive advantage; the Trust Companies Act and the Banking Act being crucial to enforce full secrecy. In relation to higher educational policies they advise Singapore’s government to improve the education level of current wealth managers, and the creation of more degrees and certifications suiting the specific needs of the industry at all levels, from bank clerks to traders. Kuah (2008) in “Working Paper Series” published by the University of Manchester while clearly stating that small-scale economies can be analyzed through. 治 政 大 workforce has a positive sector. The concentration of highly skilled and specialized 立 impact on the performance of banking and financial institutions; furthermore they can the diamond model, also outlines that in Singapore location is key for the financial. ‧ 國. 學. also more easily get together to lobby the government into adopting favorable policies.. ‧. Malcolm Cook, in the book entitled “Banking reform in Southeast Asia: The region’s decisive decade” (2008) gives a clear chronological account of the evolution. y. Nat. sit. of the situation in Singapore, however it mostly focuses on the regulatory evolution. al. er. io. concerning the banking sector, and slightly discusses the results (2008). Thus omitting. n. several crucial variables.. Ch. i n U. v. Denis Hew in “Capital markets in Asia: Changing roles for economic. engchi. developments” (2005) wrote one of the most complete accounts of Singapore’s financial center to date. It focuses on the overall historical development, including the legislative environment. It deals as well to some extent with Singapore’s stock market, local and foreign banks, the bond market, etc. However, due to its publication almost a decade ago, it misses on the 2008 financial crisis. Furthermore it does not include information about the training of employees, Islamic banking, or the RMB liberalization. The Economic Review Committee, in “Positioning Singapore as a pre-eminent financial centre in Asia” (2002), gives a convincing in-depth overview of the strengths and weaknesses of Singapore as a financial center. The lack of a diversified financial sector, and sufficiently large stock market is thoroughly discussed. On top of that the shortage of industry-specific qualifying programs for employees in the sector 8.

(20) is dealt with. On a rosier note, wealth and asset management are identified as the strongest elements, and risk management is seen as a potential future key player in Singapore’s financial district. Ong Chong Tee in “Singapore’s policy of non-internationalization of the Singapore dollar and the Asian dollar market” (2003) stresses the importance of the establishment of the Asian Currency Unit and the Asian Dollar Market as a tool to internationalize the activities of the local banks in the early development of the financial cluster until today. He also points out the poor performance of managers in the finance and banking sector that is lower than in the Philippines according to studies. Hence the heavy reliance of the city-state on foreign workers, and the limitations of this model on the long-run. Contrarily, Zahidi, Bloom, Milligan, Guzzo,. 治 政 of human capital to face coming the workforce that is the best prepared in terms 大 立 challenges, as competition on the international stage increases. & Harding (2013) in the “The Human Capital Report” underlined that the country has. ‧ 國. 學. To conclude we can say that most of the current literature outlines Singapore’s status as an overachiever. Yet, none studies Singapore’s financial cluster combining. ‧. local and regional perspectives altogether.. y. Nat. io. sit. 1.5 Background information. n. al. er. In order to better understand the uniqueness of Singapore as a city-state, this. i n U. v. part will briefly introduce the different development stages that it has been through.. Ch. engchi. 1.5.1 Development stages of the Republic of Singapore 1.5.1.1 The path to self-governance and independence The modern history of the city of Singapore truly started when Stamford Raffles colonized what was then known as Singapura or Temasek in 1819. Shortly after the settlement of Singapore, the island was able to take advantage of its natural deep-water harbor, its key location alongside the Malacca Straits, and the intense trade that took place between Europe and its colonies. As a result, “entrepot trade” became the key to the early rise of the city. The takeover of the colonized island by the East India Company in 1858 further reinforced the sole reliance of the local economy on trade. 9.

(21) Following the “Straits Settlement”, the Indian Office of the British Governor took over and ruled altogether Singapore, Penang and Malacca. It somewhat pushed Singapore to diversify in the manufacturing sector, and the service industry. However, as World War II happened, the Japanese troops took over Singapore, and from 1942 to 1945 the economy drastically suffered. After Japan surrendered, the British went back, and it’s not until 1959 that Singapore was allowed some degree of selfgovernance. The first election saw the People’s Action Party (PAP) takeover the government with Lee Kuan Yew at its head, and it marked the start of the PAP’s single-handed rule that has been going on since then (Turnbull, 1989). Lee Kuan Yew’s party did not rest on its laurels and in order to prevent the island from falling into the communists’ hands adopted a set of policies to resolve the. 治 政 大 Board (HDB), helped tackle board -a state-governed body-, the Housing Development 立 rampant poverty and unemployment, thanks to the “Five-Year Building Programme”. various problems that plagued Singapore. The establishment of the first statutory. ‧ 國. 學. that built thousands of subsidized flats. This high-profile policy was enforced alongside the “Five Year Education Plan”, which reduced illiteracy and laid the. ‧. foundations necessary for the rise of the “Singapore’s miracle”. The Singapore Polytechnic, and other vocational schools hereby established, set the path to the. y. Nat. sit. forthcoming industrialization. The famous stance of the island against corruption is. er. io. not new either; it also dates back to the early days of the PAP when it enforced an “Anti Corruption Law”, which gave the judiciary power wide investigation and. al. n. enforcement powers.. Ch. engchi. i n U. v. The first “State Development Plan” was launched in 1961, and was promoted by the newly established Economic Development Board (EDB), another statutory board. It was planned to last over a three-year span, and it identified the areas in which Singapore benefited from a clear competitive advantage (ship building, small appliances manufacturing, steel and chemical industry, etc.). It advocated an importsubstitution strategy aimed at tapping in the large Malaysian market. In order to promote labor-intensive sectors, the EDB also drafted policies that would attract Foreign Direct Investments (FDI). In 1963 following a referendum Singapore gained independence from the British colonial empire, and seventeen days later Singapore merged with its neighbor to form the Federation of Malaya. However the PAP did not get along with the United Malays National Organization (UMNO) that wanted to establish pro-Malay policies. 10.

(22) Following the ethnic riots of 1964, the Federation of Malaysia expelled Singapore in 1965, because of fears of a pro-Chinese coup against the UMNO (Lee, 2008).. 1.5.1.2 The Republic of Singapore’s first industrial revolution and the following turmoil Singapore’s forced independence from Malaysia did not affect Singapore’s economy that had, at the time, a Gross Domestic Product (GDP) per capita more than double of Malaysia’s, and manufacturing already accounted for a bit more than 19% of its total GDP (United Nations Statistics Division, n.d.; World Bank, 2014c). Furthermore, the city-state was ready to face future challenges thanks to earlier PAP’s. 政 治 大 The separation from Malaysia meant that the government had to move away 立. industrial policies and its two statutory boards, the HDB and EDB.. from its first State Development Plan, and adopt an export-oriented growth model, as. ‧ 國. 學. it could no longer rely on Malaysia’s domestic market. This period was called the “First Industrial Revolution”. This new path did not go without some major issues. In. ‧. 1971 the UK, that still had a military base in the island, announced its intention to. y. Nat. close it. Since British military was one of the principal employers of the island, the. sit. news stirred grave concerns. As a consequence, the PAP decided to attract foreign. er. io. heavy-industry companies, and Japan proved to be a major ally. The former colonial. al. n. v i n C hled Mitsubishi Heavy shipbuilding companies, which e n g c h i U Industries and Mitsui to start operating in Singapore (Lee, 2000). power established many trading companies, and also helped strengthen the local. The First Industrial Revolution, with the support of the EDB, saw an improvement in the industrial skills of the local workforce through the “Manpower and Training Unit” and the “Overseas Training Program”, both established in 1971. The EDB was also highly efficient in attracting investments from overseas by working as a “one-stop shop” for willing investors, especially since it had been alleviated from its considerable work-load thanks to the creation of the Development Bank of Singapore (DBS), and to the Jurong Town Corporation (JTC), a new statutory board (Teo & Ang, 2001). The creation of Asian Currency Units allowed the financial service sector to rise as well, by attracting foreign financial institutions, in permitting the trade in US Dollars or other major foreign currencies (Lee, 2000). 11.

(23) All those measures reflected in the changing economic structure of Singapore, manufacturing grew tremendously, helped by the relocation of many factories from Hong Kong to Singapore, due to the political turmoil in China at that time. As a result, in 1973 manufacturing reached 22,3% of the GDP, and the Per capita GDP at current prices (US dollars) had attained $1,929, nearly triple that of Malaysia’s. Finally, GDP growth averaged 12,7% annually from 1965 to 1973 (United Nations Statistics Division). As the local business class did not seem to be willing to shift from their traditional focus on shipping and logistics, there was a concomitant increase in state intervention by means of a “big push” strategy, As the country reached a state of full employment, concerns emerged about the spiraling wages and the unsustainability of the labor-intensive orientation of the. 治 政 growth model (Cahyadi, Kursten, Weiss, & Yang, 大 2004). While globalization started, 立 it became less and less competitive to attract FDI in the low-skilled sector as fierce economy, consequently the country attempted to adopt a more capital-intensive. ‧ 國. 學. competition emerged from other Asian countries that took part in the global production network. The EDB moved to attract more technology-intensive businesses,. ‧. such as in engineering, high-end electronics, and petroleum processing. The borders were also opened to attract foreign talents, and offset the shortage of labor. Yet this. y. Nat. sit. strategy coincided with the First Oil crisis of 1973, the effects of which lasted until. al. er. io. 1976. As a result the industrial upgrade strategy had to be delayed, growth slowed. n. down from 11,1% in 1973 to an annual average of 6,2 % from 1974 to 1976 (United. Ch. Nations Statistics Division).. engchi. i n U. v. 1.5.1.3 The second industrial revolution: A hazardous journey As the world’s economy recovered the flow of FDI went back to normal after 1976, the turn towards more capital-intensive industries was resumed and in 1979 the Vocational and Industrial Training Board was set up to level up the skills of the workforce. Simultaneously, the Joint Industrial Training Scheme was enforced with the help of multinational corporations in order to provide them with highly soughtafter skilled employees. While in appearance this strategy appeared as a success as the growth rate went up, this was mostly due to the rise of Singapore in the financial service sector, and the construction sector.. 12.

(24) Thus, in 1980 the “Economic Development Plan for the Eighties” was published and it kick-started what is now known as the Second Industrial Revolution. All the statutory boards were put to the task to diversify the industrial structure of the country: Information and Communication Technology (ICT), pharmaceuticals, medical instruments, etc. The EDB was particularly successful in attracting MNCs in those sectors, and the city-state became a crucial link in the region in high-end industrial production. In order to ensure that productivity would follow and that wages went up, the government decided to enforce a high-wage policy from 1979 until 1984. Simultaneously, the Trade Development Board (TDB) was founded in 1983, with the aim of strengthening indigenous companies by helping them to expand their business abroad. This board had other beneficial effects on the economy, and. 治 政 Education-wise lots of efforts were made 大 to continually make sure that the 立 workforce had the appropriate technical skills. Some universities were transformed. further setting Singapore as an international trading hub (Ramcharan, 2002).. ‧ 國. 學. into Technological Institutes, the brightest students were sent abroad, many faculty members were recruited from the West, and joint projects such as the French-. ‧. Singapore Training Institute were set up.. While at first it seemed that the Second Oil crisis did not have much impact on. y. Nat. sit. the economic performance of the island, oil-refining and ship-building were severely. al. er. io. hit. What’s more the high-wage policy (1979-1984) led to an unsustainable situation. n. as wages increased faster than productivity. Many companies instead of upgrading. Ch. i n U. v. their business had simply relocated to the Malaysia hinterland, or Indonesia. As a. engchi. consequence, in 1985 the country was hit with its first recession, the GDP contracted by 0,6% and the following year GDP only grew by 1,3% (World Bank, 2014a). In reaction, in 1986 “The Singapore Economy: New Directions” was published and advised the PAP to make services a clear part of its growth strategy, pushing for tax incentives in order to ensure MNCs would settle their regional headquarters there. The “SME [Small and Medium Enterprises] Master Plan” was also launched in 1988 to make sure that indigenous companies would restructure. High wages, which had pushed the country into the 1985 recession, were frozen for two years, the corporate tax was lowered, and the flexi-wage system was enforced, automatically regulating people’s income based on various performance indexes. Luckily the economy went back on track, and from 1986 to 1990 the country thanks. 13.

(25) to its new found luck in the tertiary sector enjoyed an average GDP growth of 8.7% (Toh & Tan, 1998).. 1.5.1.4 The 1991 Strategic Economic Plan: a turning point The Strategic Economic Plan published in 1991 can be seen as a turning point for Singapore. Thus, it mentioned for the first time many key ideas that have long lastingly shaped the city-state. It was a long-term plan that aimed at making Singapore a high-income nation within the following 30 years. It also listed the ways to make the Republic a global city. Thereby, “The Riau Islands, Johor, Singapore Growth Triangle” was mentioned for the first time as a possible hinterland for. 治 政 identified possible clusters (Toh & Tan, 1998). 大 立the country was concerned about the low productivity of its In the early 1990’s. Singaporean businesses. Singapore positioned itself as a key regional force, and. ‧ 國. 學. service sector (including the financial sector), while it encompassed 39% of workers, the economic output only represented 9% of the GDP. As a response the Singapore. ‧. Productivity and Standards Board was created in 1996 to increase the economic output of service workers (Ministry of Trade and Industry, 2006).. Nat. sit. y. While the local workforce was already well educated the government. io. er. launched the “National Technology Plan” in 1991 to deepen locals’ scientific and technological knowledge, followed by the 1996 “National Science and Technology. n. al. Ch. i n U. v. Plan”. The government came to the realization that the population being limited the. engchi. country would have to resort to hiring foreign talents, thus starting the constant growth of foreign workers in the island (Ministry of Trade and Industry, 2006). Regionalization was also set as a priority. Singapore had long overlooked its neighbors and mostly targeted Western markets. Thus a series of policies were enforced to better help Singapore to become a regional hub, such as the “regionalization of Singaporean enterprises programme” (Pereira, 2001). All these efforts paid off, and in 1993 the GDP growth reached 11.5%. However, the 1997 Asian financial crisis disrupted the growth model set by the 1991 Strategic Economic Plan. Whereas in 1997 the GDP growth was still of 8.5%, in 1998 the country’s GDP contracted by 2.3%, luckily the economy bounced right back in 1999 and grew by 6.9% (World Bank, 2014a). Most of Asia’s currencies and stock markets were severely hit, yet Singapore remained largely unaffected by the crisis, 14.

(26) that situation led the Singapore Dollar (SGD) to strengthen in comparison to other regional currencies. Consequently the island’s regional competitiveness worsened, so the government decided to reduce labor costs. The newly established Committee on Singapore’s Competitiveness advised the country to keep developing its wellestablished financial service sector and diversify in venture capital and fund management, and to also turn to new high-growth hub services that include healthcare, media, education, etc. The “Productivity Action 21” plan was simultaneously launched in order to ensure that the local workforce would finally reach the list of the top 10 most productive nations in the service and manufacturing sector (Tan, 2002). This plan confirmed the island’s turn towards attracting more foreign talents in order to help achieve its goal. The 1990’s also saw the nation. 治 政 大among the most attractive and leading to plans to make Singaporean universities 立 competitive in the world.. develop into a more knowledge intense model, with higher education at its core,. ‧ 國. 學. Those measures were highly successful as service exports grew by an annual average of 9.9% between 1985 and 2001. In 1993 more than a hundred foreign banks. ‧. had set branches in the city-state. By 1998 the local financial market started to open up, and foreign banks were allowed to enter the lucrative retail-banking sector. y. Nat. sit. (Economic Review Committee, 2002).. al. er. io. The years 2001, 2002, and 2003 witnessed several external shocks, the. n. technology bubble collapsed, the USA were hit by the 09/11 attacks, and the SARS. Ch. i n U. v. epidemic broke out. As a consequence in 2001 the GDP contracted by 1.2%, in 2002. engchi. the economy bounced back to a meager 4.2% GDP growth, and in 2003 the GDP grew by 4.6% (World Bank, 2014a). As a result, as early as 2001 the government set a new Economic Review Committee, and in 2003 it released a series of recommendation in order to truly build the city as a global hub. Six fields were picked out and much emphasis was put to make them flourish: international links, the local business environment, knowledgedriven sectors, the service and manufacturing sector, human capital, and job displacement (Ministry of Trade and Industry, 2003). Accordingly in 2006 the real growth of financial services was of 9,2%, Singapore became the sixth largest private banking center worldwide (Singh, 2012). At the same time the manufacturing sector still represented 27% of the annual GDP, an impressive performance for such a small island (World Bank, 2014c). 15.

(27) This period of rapid expansion was again halted in 2008, as the subprime mortgage crisis hit the USA and impacted other international markets. That year the GDP grew by only 1.7%, and in 2009 it contracted by 0.8% (World Bank, 2014a). While on the financial front Singapore was enforcing many proactive measures such as guaranteeing all deposits, a stimulus package representing 8.2% of the GDP was launched (ADB Asia Capital Market Monitor, 2009). The government also took advantage of the lower level of economic activity to implement the “Skills Programme for Upgrading and Resilience”. This plan aimed at improving the knowledge of the local workforce, and seizing new opportunities when the economy bounced back (Ministry of Manpower Singapore, n.d.). The city-state did not have to wait for too long as in 2010 the GDP increased by a spectacular 14.8% (World Bank,. 治 政 大released its latest report. In the In 2010 the Economic Strategies Committee 立 past most reports had solely targeted how to improve the business environment and 2014a).. ‧ 國. 學. the economic output of the local workforce. Yet the 2010 recommendations moved away from their traditional focus and called for a more inclusive growth, in order to. 2010).. ‧. decrease the ever-growing income inequalities (Ministry of Trade and Industry,. sit. y. Nat. er. io. 1.6 Chapters layout. al. n. v i n explaining the details of theC thesis, framework for the research U h eproviding n g c haitheoretical. This thesis will be comprised of four chapters. First, an introduction,. and literature review to support it; second, an overview of how Singapore emerged as a full-bodied financial and banking cluster, and an evaluation of key sectors performance from 1997 to 2013; third, an in-depth analysis of emerging factor conditions which have been at play: education and capacity building, Islamic finance, and the Renminbi factor. And finally, a conclusion addressing the research questions, summarizing major attributes, evaluating strengthts and weaknesses regarding Singapore’s financial and banking cluster.. 16.

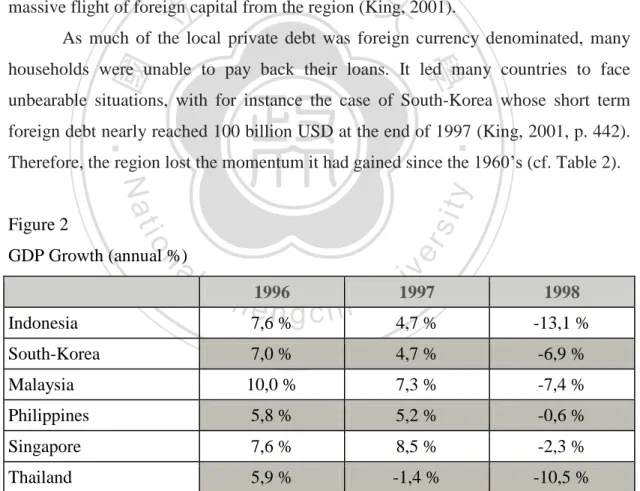

(28) Chapter 2. Emergence of Singapore as a Full-bodied Financial and Banking Cluster, and Performance from 1997 to 2013. 2.1 The 1997 Asian Financial Crisis: a wake up call for Singapore’s financial center The 1997 Asian Financial Crisis having had a tremendous impact on the regional and Singaporean financial market, it is therefore crucial to understand its development and consequences.. 2.1.1 Impact on Asia. 立. 政 治 大. On July 2, 1997 Thailand’s national currency, the Baht, followed a downward. ‧ 國. 學. spiral (CNN Money, 1997). In the coming days and weeks most countries in the region were severely hit as well. The Philippines, Malaysia, Indonesia and South. ‧. Korea reached their lowest points that same year too (Beeson & Rosser, 1998). On a lesser note Taiwan, Hong Kong and Singapore weathered through the hard times. sit. y. Nat. better.. io. er. The situation started to look bleak in Asia as early as 1996. The macroeconomic situation in Thailand had already started to worsen. The Thai Baht in. n. al. i n U. v. parallel to the USD, to which it was pegged at the time, appreciated by 21% against. Ch. engchi. the Japanese, American, and German currencies between April 1995 and December 1996 (Moreno & Federal Reserve Bank of San Francisco, 1997). Hence making the Thai Baht one of the world’s most overvalued currencies. As a consequence Thailand’s exports lost their competitiveness on the international market, shrinking by 0.2% in 1996 especially in the textile sector (Lai, 2000, p. 68), leading to a 7.9% deficit of the country’s current account (Tan, 1999, p. 1). As a consequence, Thailand’s stocks and property markets began to tumble, further weakening local financial institutions. In spring 1997 heavy pressure started to be felt on the Bath, as locals wanted to insure themselves against the risk they had taken by borrowing in foreign currency denominated loans (Beeson & Rosser, 1998).. 17.

(29) To preserve the value of the Bath, the central bank spent a massive amount of its foreign reserve through USD “forward contracts” 5 , which proved costly and eventually deadly for governments’ foreign reserves. The announcement of forthcoming massive losses by Finance One, one of the largest Thai banks, prompted the government to let the Bath float freely, as the Thai central bank could no longer afford to keep afloat its banking and monetary system. This ended the long-lasting peg of the Bath to the USD (King, 2001, p. 441). So, the Thai currency lost most of its value overnight, as it had previously been kept artificially at a high level when pegged to the much stronger USD, linked to the mature American market. In the following two weeks, Malaysia and the Philippines unpegged their. 治 政 大 2001). massive flight of foreign capital from the region (King, 立 As much of the local private debt was foreign currency denominated, many. currencies as well, and South Korea did similarly afterwards, thereby provoking. ‧ 國. 學. households were unable to pay back their loans. It led many countries to face unbearable situations, with for instance the case of South-Korea whose short term. ‧. foreign debt nearly reached 100 billion USD at the end of 1997 (King, 2001, p. 442). Therefore, the region lost the momentum it had gained since the 1960’s (cf. Table 2).. al. er. io. sit. y. Nat. Figure 2. n. GDP Growth (annual %). Indonesia. C h 1996 e7,6n%g c h i. v i1997 n U. 1998. 4,7 %. -13,1 %. South-Korea. 7,0 %. 4,7 %. -6,9 %. Malaysia. 10,0 %. 7,3 %. -7,4 %. Philippines. 5,8 %. 5,2 %. -0,6 %. Singapore. 7,6 %. 8,5 %. -2,3 %. -1,4 %. -10,5 %. Thailand 5,9 % Source. United Nations Statistics Division, n.d.. “Forward contracts” are contracts made between two parties to buy or sell an asset (referred to as the 'underlying’) at a specified price (referred to as the 'forward price’) on a future date. They do not trade on a centralized exchange and are therefore regarded as over-the-counter (OTC) instruments. There is no money exchanged until the settled date. 5. 18.

(30) The catastrophic domino effect of the crisis can be blamed on the underdevelopment of local financial systems. They were not ready to withstand the massive inward flow of foreign capital that occurred before the crisis in their local economies. Local banks at the time heavily relied on USD denominated short-term loans, and their risk management strategies were inadequate. For instance, in the 1990’s the Thai government had settled the “Bangkok International Banking Facility” (BIBF) that was in charge of providing local banking institutions with foreign funds. However the BIBF activities were not closely supervised, which resulted in an uncontrolled growth of foreign currency denominated short-term debt that was used to invest in long term projects, which equaled to incompatible debt maturity 6 (King,. 治 政 Furthermore, due to the heavy inflow of大 foreign investors in local stock 立 markets, the crisis spread fast in Asia. Fund managers and private investors who had 2001, p. 443).. ‧ 國. 學. to cover their losses in Thailand, sold their assets in other Asian markets that had not yet deflated too much, thus further inducing a domino pattern (Tan, 1999, p. 4).. ‧. All in all, at the dawn of the crisis there were three distinctly salient problems in Asia: asset bubbles in the real estate and stock market, shrinking exports, and. y. Nat. sit. opaque governmental and banking decision-making processes. Thus paving the way. er. io. for the massive crisis that followed.. n. a. l C 2.1.2 Impact on Singapore. hengchi. i n U. v. Contrarily to the situation in most countries of the region at that time, Singapore’s economy was not as hardly hit by the crisis as other nations (cf. Table 1), with the exception of Taiwan. This was due to the careful building of the financial sector since the mid 1960’s. The city-state had also in the previous boom years been exempt from a massive inflow of capital from abroad, preventing too much of a lending explosion (Garrido, 2005, p. 29). Yet, overall the country suffered, and unemployment more than doubled, to balloon to 4.4% in December 1998 (Tan, 1999, p. 5). For that reason, Singapore chose to improve the economy’s competitiveness. For instance, the wage system was. 6. Maturity refers to the date when the final payment of a financial instrument is due to be paid. 19.

(31) reformed in order to make it more flexible and responsive to allow companies to remain profitable in times of economic hardship (Jin, 2000). The government at first for the 1998-1999 budget did not plan to launch a stimuli package; actually a surplus was still expected. Only small tax cuts were planned to boost competitiveness. However as the economy did not show signs of recovery, the government decided to launch a second set of policies to help domestic companies, thus mostly aiming at resorbing the surge of the unemployed. The “cost reduction package” was probably the boldest move from the government, by reducing costs of doing business7 by 15%, it was worth more than 10 billion (SGD) in total (Tan, 1999, p. 8). These measures, though costly, did not increase Singapore’s debt as it had in its good years generated large budget surplus. 治 政 大 its attractiveness. materialized, and the banking sector was able to rebuild 立 While helping the local economy, the Republic of Singapore also sought to. (Garrido, 2005, p. 33). Luckily, the expected effects of the successive plans. ‧ 國. 學. help the whole region to recover as fast as possible. In August 1997 Singapore, alongside other countries, provided a rescue package worth US$17.1 billion to. ‧. Thailand, and it did the same in November 1997 this time to help Indonesia with a 38 billion USD package. It also took part into the IMF sponsored “New Arrangement to. Nat. sit. y. Borrow” aimed at giving the IMF access to extra funding in case the international. al. er. io. monetary system would be at risk of collapsing. It injected 340 million USD in the. n. overall 34 billion USD program (Jin, 2002). These moves all showed the willingness. Ch. i n U. v. of Singapore to truly engage into any international plans aimed at resorbing the. engchi. effects of the 1997 Asian financial crisis.. 2.1.3 Impact on the Singapore Dollar The Singapore dollar is pegged to an undisclosed currency basket of Singapore’s “major trading partners and competitors” (Monetary Authority of Singapore, 2001d, p. 2). The official exchange rate of the SGD is calculated following the nominal effective exchange rate 8 (NEER), and allowed to fluctuate within an. Cost of doing business (CODB) refers to the cost of operating one’s business, this generally includes taxes, salaries, bills, and rent. 8 The NEER is the quote for a currency versus a weighted value of currencies traded within an index of currencies (weighed according to the balance of trade). The NEER differs from the “real exchange 7. 20.

(32) “undisclosed policy band 9 ” (Monetary Authority of Singapore, 2001d, p. 2). This solution allows for a more flexible monetary policy in case of crisis, in comparison to the Hong Kong Dollar that is completely pegged to the USD. As a result, while no drastic devaluation was undertaken, the SGD’s policy band was modified to allow greater volatility. Following this careful policy the NEER had as early as 1999 recovered its average NEER (Jin, 2000). In 1997, the Singapore dollar found itself in a middle ground situation, where the national currency lost ground to the USD, the Japanese Yen, the British Pound, and Deutschemark, but appreciated against other Asian currencies, such as Malaysia’s Ringgit and the South-Korean Won (Jin, 2000). Because of the sudden fall of other regional currencies against the Singapore. 治 政 大 domestic exports declined expensive currency, and the fall in regional consumption, 立 in the region. The situation would have been way worse, had the government not. dollar, the erosion of exports’ competitiveness consecutive to a comparatively more. ‧ 國. 學. pushed for market expansion in all continents for its high-tech manufactured goods (Garrido, 2005, p. 35). The ASEAN-4 (Indonesia, Malaysia, Philippines, and. ‧. Thailand) at that time represented almost a third of Singapore’s exports. Singapore’s response however was nothing like that of its neighbors, it did not. y. Nat. sit. drastically change its monetary policy during the crisis, as speculators in the end. er. io. chose to attack other currencies, which had weaker fundamentals, such as South Korea’s Won. This can be credited to the conservative lending policies of the. n. al. Ch. i n U. v. Monetary Authority of Singapore (MAS). Before the crisis, its monetary decisions. engchi. were highly trusted, and the Singapore Dollar in 1997 was still seen as a safe heaven due to the island’s sound macroeconomic environment: no external debt, large foreign exchange reserves, budget surpluses, high savings rates, current account surplus (20.9% of GDP in 1998) (Jin, 2000). What’s more, the MAS has long opposed the internationalization of the SGD, arguing that it has to parallel the growth of the real economy, thus preventing a risk of capital flow instability. While all forms of exchange control were totally removed in 1978 (Tee, 2003, p.93), until today this policy has safeguarded the SGD from. rate” (RER), which reflects the value of a currency corrected according to local purchasing power. This also contrasts with the “nominal exchange rate” (NER), which is the official exchange rate. 9 A policy band refers to a currency system that allows a currency’s exchange rate to fluctuate between pre-established limits. It is a system in-between a fixed exchange rate and a floating exchange rate. 21.

(33) suffering from any catastrophic speculative attack. Even though some complain that it hinders the growth of the Singapore Financial cluster.. 2.1.4 Impact on Singaporean banks As might be expected, Singaporean financial institutions had to overcome some difficulties during the crisis. Due to their investments in South East Asia they had to proceed to asset depreciation, and witnessed a sharp increase in nonperforming loans (NPL) 10 to around 10% in 1998. Luckily, the region only represented 20% of domestic banks’ assets, and “loan exposure to Malaysia, Indonesia, Thailand, South Korea and the Philippines in March 1999 was 34.7 billion SGD, or 12.5% of their total assets” (Jin, 2000, p. 9).. 政 治 大 more than 16%, they did 立not suffer losses to the point of going bankrupt. They were. Banks in Singapore having an average capital adequacy ratio11 (CAR) of a bit. ‧ 國. 學. more than able to withstand the losses, and still posted benefits in 1998 (Tan, 1999). However, financial services got affected by the recession for the year following the crisis, while the business sector continued to grow (Jin, 2000). All in all, banks while. ‧. having to digest the losses from NPL, the sector was not as badly hit as in South. y. Nat. Korea or Indonesia, thus showing resilience through effective capital management. er. io. sit. techniques (Garrido, 2005, p. 29).. n. a l Exchange of Singapore i(SES) 2.1.5 Impact on the Stock v and the Singapore n U i (Simex) e n g c hLimited International Monetary Exchange. Ch. On a year-to-year trend, from July 2, 1997 Singapore’s stock market, which at the time comprised the Stock Exchange of Singapore (SES) and the Singapore. NPL (sometimes referred as “bad debt”) are loans on which the borrower stops making payments (usually for three months), and consequently leads to default. Individual countries have different regulations concerning classification into NPL. However, “loan loss provision” is usually set aside by financial institutions to cover potential losses from money lending activities. Two options exist to handle NPL, either including them in one’s balance sheet (loss account), or selling them to asset management companies (AMCs) that will reclaim whatever may be. NPL ratio reflects the overall health of banks, the smaller it is, the better the quality of outstanding loans. 11 The Capital Adequacy Ratio (CAR) refers to the amount of capital versus the credit exposure. Regulations have been set worldwide in order to ensure that banks have a minimal CAR in order to lower systemic risk exposure, and safeguard customers. 10. 22.

(34) International Monetary Exchange Limited (Simex), lost more than 45% (Tan, 1999). This resulted in severe losses on the side of private investors. Singapore's brokerage firms were also severely shaken by a unilateral decision taken by the Malaysian government enforcing tight exchange control. The Kuala Lumpur Stock Exchange in mid-1998 was also concerned by protectionist measures, thus all transactions involving shares of Malaysian companies were no longer allowed to be conducted outside of Malaysia. As a consequence Central Limit Order Book International, which so far in Singapore was in charge of such transactions suffered dramatic losses (Jin, 2000).. 2.2 Liberalization of Singapore’s Financial and Banking Market: Singapore’s. 政 治 大. answer to the 1997 Asian Financial Crisis. 立. Singapore was already a blossoming financial cluster before the start of the. ‧ 國. 學. 1997 Asian financial crisis, however the unprecedented events led the MAS and the Singaporean government to look for ways to strengthen local banks, and reinforce the. ‧. attractiveness of the city-state as a hub for foreign banks in Asia.. Walter Russell Mead theorized this fierce competition to attract foreign capital. Nat. sit. y. in the financial sector with the notion of "millennial capital” (Mead, 2004, p. 74). It. io. er. reflects the aim of many cities to attract foreign capital, and become financial clusters, hence making it a necessity for Singapore’s financial cluster to reform after the 1997. n. al. Ch. i n U. v. financial crisis. This was especially urgent, as many protectionist measures had been. engchi. enforced in favor of Singaporean banks after Singapore’s independence. Thus, as early as 1997 Singapore launched a Financial Sector Review Group to look for suitable strategies to reinvigorate the asset management industry, and formulate policies (Chew, 2001, p. 570). As a result, the MAS released the “Statement on Measures to Liberalise Commercial Banking and Upgrade Local Banks” on May 17, 1999. It was a two-phase plan, the first phase being enforced from 1999 to 2001, and the second one from 2001 to 2004 (Monetary Authority of Singapore, 2001b). This two-step liberalization process allowed for the MAS and the government to assess progress and challenges after the first two years, in order not to destabilize the local banking landscape.. 23.

(35) 2.2.1 First phase of the reform The first phase had three clear goals: starting the liberalization of the banking market, upgrading banks governance, and lifting the 40% limit that foreign investors were subjected to when acquiring the shares of a domestic bank (International Law Office, 1999). Although this limit was subsequently lifted, up until today no Singaporean bank has been taken over by a foreign player, as it is unlikely the government would approve. Foreign shareholders must get approval from the MAS and the government when seizing more than 5%, 12% and 20% of a local banking institution (Bureau of Economic and Business Affairs, 2013, p. 5). This shows that the MAS is still focused on encouraging the rise of a homegrown financial industry, thus reflecting the long. 政 治 大 These goals, which 立 in appearance seem to send a clear message to the market. term vision of the government.. ‧ 國. 學. that Singapore is ready to let foreign and local banks play on a level playing field, were consequently counterbalanced by many regulations.. The most important change made in 1999 to allow Singapore to increase its. ‧. international attractiveness, was to reshuffle its licenses scheme for foreign financial. y. Nat. institutions into three distinct categories: qualifying full banks (QFBs), restricted. sit. banks, and offshore banks. This was a welcome move as new licenses had only been. n. al. er. io. issued in 1970 and 1983 (Monetary Authority of Singapore, 2001c).. Ch. 2.2.1.1 Qualifying Full Banks e n g c h i. i n U. v. The new QFB license was aimed at granting banks that under the previous system held a full bank license, or aspiring ones, greater privilege: . The opening of up to 5 branches, and ATMs in 10 different locations.. . The possibility to share ATMs networks with other QFBs.. In order to qualify as a QFB several aspects are first considered: credit rating, and the “commitment to contributing to Singapore’s development as an international financial centre”, etc (International Law Office, 1999). This last statement can leave some to wonder in what measure the government would estimate the banks’ commitment to Singapore’s long-term plan. To further complicate things, the MAS 24.

數據

Outline

Theoretical framework

Development stages of the Republic of Singapore

The 1997 Asian Financial Crisis: a wake up call for Singapore’s financial

Liberalization of Singapore’s Financial and Banking Market: Singapore’s

Asian Dollar Market

The Banking Act and the Trust Companies Act: guarantors of

Private banking

Education and capacity building: a crucial factor condition

The Renminbi factor

Policy recommendations

相關文件

Prime and sub-prime factors of employee’ voluntary turnover in boom phase of industry: Empirical evidence from banking sector of

Promote project learning, mathematical modeling, and problem-based learning to strengthen the ability to integrate and apply knowledge and skills, and make. calculated

Apart from European civilisation, the Islamic civilisation has also made significant contributions to the history of civilisation. Though communication

In the context of public assessment, SBA refers to assessments administered in schools and marked by the student’s own teachers. The primary rationale for SBA in ICT is to enhance

Wang, Solving pseudomonotone variational inequalities and pseudocon- vex optimization problems using the projection neural network, IEEE Transactions on Neural Networks 17

Menou, M.著(2002)。《在國家資訊通訊技術政策中的資訊素養:遺漏的層 面,資訊文化》 (Information Literacy in National Information and Communications Technology (ICT)

Chow (Eds.), Changing classroom and changing schools: Study of good practices in using ICT in Hong Kong schools(pp. Hong Kong: Centre for Information Technology in School

Do you agree with the proposed changes for the Compulsory Part of Information and Communication Technology curriculum.. Agree Disagree