A Monetary Policy Rule for Developing Countries

23

0

0

全文

(2) Abstract. The purpose of the study is to develop a prudent behavior index in order to shed light on the significance of central bank independence (CBI) as a monetary policy rule for developing countries. Many published studies have found that while CBI is beneficial for highly industrialized nations, it does not appear to help developing countries.. This raises the. following possibilities: there may be flaws in the many studies that have been done on the subjects, or there may be some characteristics of developing countries that cause them to respond differently to CBI. Exhaustive literature review of this study has concluded that the measures of CBI previously used, mainly legal or proxy measures, are flawed.. The prudent. behavior index which serve as a proxy for the behavioral measures of CBI have been developed in this research. The conclusion drawn from the empirical findings is that, with respect to inflation, a prudent behavior index is both explanatory and prescriptive has been identified, tested, and found to be predictive. That is, a developing country that follows the rule embodied in the prudent behavior index is likely to have an inflation rate that is both lower and more stable than the average experience.. An additional question arises concerning the possible trade-off. between inflation and the level of output.. While this complex question will receive no. definite answer from this modest study, some evidence is offered that a country that follows the rule will not only suffer no penalty in terms of output, but may in fact even enjoy a bonus in the form of a higher level of output.. JEL Classification: H21, E62, O16 Keywords: Central Bank Independence, Prudent Behavior Index, Inflation, Economic Growth. 2 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(3) 1. Introduction High inflation in the 1970s and 1980s led to accelerated research on the control of. monetary policy by central banks.. It was formerly believed that a dependent central bank. enabled policymakers to achieve various goals: high employment, financing with budget deficits, attainment of balance of payments objectives, and low interest rates.. This thinking. often led to rapid increases in the money supply, fueling inflation. A suggested solution for the inflationary bias is to grant independence to the central bank and to give it a mandate to achieve price stability. governments to misuse monetary policy.. This might offset the tendency of. Pre-committing the central bank to price stability. strengthens its position in pursuing and maintaining low and stable inflation.. And insulating. the central bank from political influence allows its independent chief executive officer to act in a prudent manner so as not to increase the money supply excessively. Developing countries have been plagued with high and fluctuating rates of inflation in recent decades.. One study found that for the 1979-93 period, 122 developing countries had. average inflation rates that were four times the average of 20 OECD countries (Fry, Goodhart, and Almeida, 1996).. Frequent devaluations of currencies, low rates of foreign investment,. slow growth, and continuing poverty have been attributed, at least in part, to these high rates of inflation.. While there is great variation among developing countries, a search for the. causes of, and cures for, inflation that are peculiar to developing countries is gaining increasing attention.. 2. Previous Research. A number of studies have examined the efficacy of independent central banks in maintaining a low and stable rate of inflation in developing countries (Cukierman, 1992; Cukierman, Webb, and Neyapti, 1992; Cukierman, Kalaitzidakis, Summers, and Webb, 1993; Cukierman and Webb, 1995; Fry et al., 1996; Fry, 1998; Sikken and de Haan, 1998). Although several of these (and many others) found that CBI is associated with lower inflation in industrialized countries, none of them found such a relationship for developing countries.. 3 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(4) As alternatives to measures of legal requirements, proxies for CBI, as well as behavioral measures, have been used. Proxies have concentrated on the tenure of the chief operating officer (governor) of the central bank (Cukierman, 1992; Cukierman et al., 1992; Cukierman and Webb, 1995; and Fry et al., 1996).. Behavioral measures have included. monetization of government deficits ( Sikken and de Haan, 1998), neutralization of government credit extended by the central bank (Fry et al., 1996; Fry, 1998), and sterilization of foreign asset inflows (Fry, 1998). None of these, however, have developed prescriptive rules for central bank policy.1. The purpose of this study is to provide a rule for. performance by the central banks of developing countries that can be legislated and will result in both lower levels and variability of inflation.. 3 3.1. Conceptual Framework Prudent Behavior and Central Bank Independence It is often assumed that insulation of the management of the central bank from the. political process will lead central bankers to act prudently. To pursue a monetary target that will maintain price stability, the central bank acts to control asset expansion.. If government. credit demands would otherwise produce inflationary expansion of domestic assets, the central bank can react by resisting such demands or by squeezing private credit (this is termed neutralization in Fry, 1998). Woolley (1984) offered two definitions of CBI: a central bank is independent from political pressure (political independence) if it can set policy instruments without prior approval from other actors and if, for some minimal time period (say, a calendar quarter), the instrument settings clearly differ from those preferred by other actors. Functional independence relates to the ability to achieve the objectives of the central bank. The political definition is impractical for a study of developing countries, since it would require detailed knowledge of the political history, as it relates to the central bank, of each country, 1. In critiquing Fry, Folder (1998) stated that what is lost in the approach, however, is a clear, direct institutional or policy proposal. Since independence is not understood as a statutory phenomenon, there is no way to legislate for it.. 4 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(5) such as is given in the minutes of the Open Market Committee of the Fed and U.S. congressional hearings. The functional definition suffers from the fact that there are other actors operating independently who affect the outcomes of a central bank decisions. Still, if the central bank achieves goals that appear to follow prudent banking practice, one can say that functional independence has been established. Thus, effective prudent behavior by monetary authorities is a proxy for CBI. Fry (1998) considered a successful outcome for an independent central bank to be the neutralization of government credit demands.. Sikken and de Haan (1998), on the other hand,. considered a rise in the money stock in response to a budget deficit to be a success, in terms of the hypothesis they were testing. This study also seeks a behavioral measure to assess the independence of central banks in developing countries, based on prudent behavior exhibited by these banks.. 3.2. Williamson Monetary Policy Rules Three rules of monetary policy which refer to the response of a monetary authority to. changes in foreign reserves have been identified by Williamson (1995). The first is to hold the domestic component of the monetary base (M0) constant, so that M0 varies in direct correspondence with the central bank holdings of foreign reserves; this is the marginal currency board rule, or MCR. The second is to keep foreign reserves a constant proportion of total assets of the central bank; if foreign exchange reserves fall, domestic assets (usually domestic government debt) are reduced by the same percentage; this is the gold standard rule, or GSR.. The third is to insulate M0 from foreign reserves. By use of fiscal policy,. changes in foreign reserves may be sterilized; this is the exogenous monetary base rule, or EMR. Under MCR, an imbalance in a country balance of payments (BOP) will have a direct and equal effect on M0, and a larger effect on the money supply (M1, M2, etc.).. Under GSR,. an imbalance in the BOP will have a direct and enlarged effect on M0, and an even larger effect on the money supply.. But under EMR, an imbalance in the BOP will have no. necessary effect on M0 or the money supply.. 5 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(6) Williamson has pointed out that the benefits of currency boards can be achieved without monetary reforms if a central bank follows MCR.2. In this case, M0 is tied directly. to the nation overall BOP.. 3.3. Definition of Prudent Behavior In order to see what rules central banks are following, one can examine changes in the. composition of their balance sheets. A devaluation increases foreign assets relative to domestic assets in the balance sheet without any change in monetary policy.. In order to. better define prudent behavior, foreign assets measured in U.S.$ are used in place of foreign assets in terms of national currency, since this reduces balance sheet distortion caused by devaluation. An examination of the statistics for a sample of 20 selected developing countries indicates that both foreign assets in U.S.$ and domestic assets increased for the period 1990 to 1996 in many of the countries.. So as to make the rules symmetrical, the following. modification is made to define prudent behavior. If the foreign assets of the monetary authority, in U.S.$, rise by a percentage that is as great or greater than domestic assets in local currency, the monetary authority is judged to exhibit prudent behavior. If foreign assets rise by a percentage less than that of domestic assets, as measured above, then the behavior is imprudent.. Domestic assets may rise or fall, but cannot rise relatively more than foreign. assets. In the case of a deficit in the BOP, domestic assets must fall (relatively) at least as much as foreign assets. The quantitative measure, for a country central bank, is labeled DIFF, the difference between the growth rate of foreign assets in U.S.$ (FA$) and the growth rate of domestic assets in local currency (DA). It is an index of prudent behavior according to the monetary policy rules.. For a given country, if DIFF is greater or equal to zero, the central bank is. judged to exhibit prudent behavior. If DIFF is negative, the behavior is imprudent.. The. relation between DIFF and the Williamson monetary policy rules is shown in Figure 1. 2. As a. A currency board holds no domestic assets, such as government securities, so foreign equal total assets. The monetary base is equal to the foreign assets of the currency board (Hanke and Schuler, 1994).. 6 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

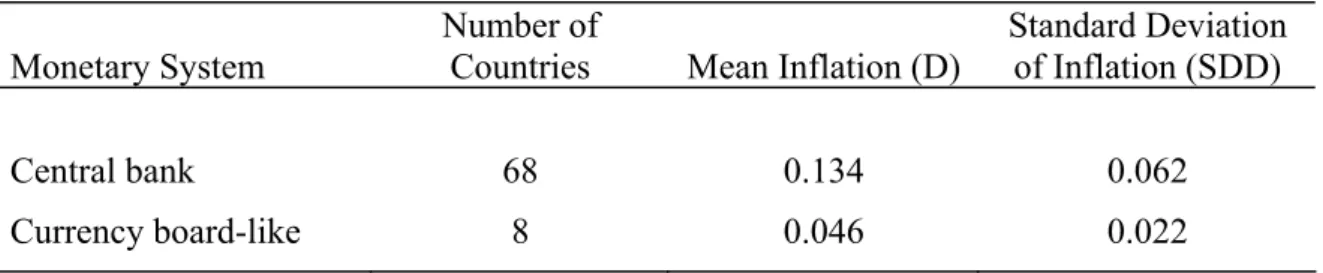

(7) central bank moves from zero toward a positive number, its actions approach the MCR. The basic hypothesis of this study is based on the preceding analysis: for any given developing country, inflation will be lower, the greater the value of DIFF. To put it more simply, the more closely a central bank actions approximates MCR, the less the inflation. Central Bank Behavior:. Imprudent. Prudent. Negative. 0. Williamson Monetary Policy Rules:. Positive. GSR. DIFF. Toward MCR. Figure 1. Relationship among Prudent Behavior, DIFF, and Williamson Policy Rules. 4. Empirical Implementation. A sample of developing countries was drawn from International Financial Statistics (CD-ROM and various issues for 1999). countries in three categories.. The selection procedure was to screen out. First, those with central banks that do not have autonomous. monetary policy decisions and do not, therefore, provide independent observations on monetary policy; these include joint central banks and those that use another country currency.3. Second, those with currency boards or currency board-like authorities, whose. balance sheets are of a prescribed composition, and automatically follow the rule.4 countries with inadequate data.. Third,. All other developing countries were included.. Data inadequacy and discontinuity was the greatest hurdle.. Many countries do not. report certain data series, such as real GDP or population. Others carry out substantial reforms of their banking systems, resulting in discontinuous series on balance sheet items.5 3. Bank of the Central African States, Central Bank of West African States, and Eastern Caribbean Central Bank are examples of joint central banks. Panama uses the U.S. dollar, aside from coins. 4. Hong Kong and Singapore are well-known examples of countries with currency boards.. 5. Malaysia provides an example. The assets and liabilities of the central bank were changed substantially in 1992, as a result of a restructure of the banking system.. 7 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(8) Yet others change their reporting methods to the International Monetary Fund, such as reclassifications of assets and liabilities, also resulting in discontinuities.6 The second, and interrelated choice was the time period.. Because this study. concentrates on inflation, a period without major international crises and with fairly general growth was deemed desirable the early nineties seemed appropriate on this score, while 1997 on did not.. With regard to the beginning of the period, 1990 seemed appropriate for a. number of reasons.. First, Inspection of the IFS data revealed many structural changes in the. financial systems of developing countries in the decade preceding 1990; these happen continually, but were especially prevalent in the 1980s. Therefore, several countries with major discontinuities immediately prior to 1990. Second, there was a strong rise in the popularity of CBI as new banking legislation, in particular calling for independent central banks, was introduced in many developing countries in the early 1990s (Maxfield, 1997). There were ten times as many constitutional moves toward CBI in three years, 1990-92, as in the previous ten years. There was, finally, a growing interest in currency board systems in the 1990s, which ruled out many developing countries from a study of CBI.. Monetary. authorities in two categories were excluded from the selection process: those in joint central banks (Bank of the Central African States, Central Bank of West African States, and Eastern Caribbean Central Bank) and those with currency board-like systems (little or no domestic assets).. The former were ruled out because the individual central banks in the joint. institutions do not make decisions on monetary policy.. For the latter, their inclusion would. bias this study toward a successful result, because such countries have lower inflation.. The. average inflation rate for those with central banks was nearly three times that of countries with currency board-like systems (Table 1). inflation over the period.. A similar pattern is found for the variability of. In addition, currency board-like systems are very prudent (the. DIFF index would equal the rate of growth of foreign assets).. So the period 1990-96 was. chosen for study. The prudent behavior rule, described above, is implemented by creating an index, 6. Vanuatu included most of the domestic assets held by the central bank as a negative entry in other liabilities until 1994, when they were transferred to the asset side as positive items.. 8 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(9) labeled DIFF.. The first step is to compute the average percentage change in foreign assets. of the central bank, converted into U.S. dollars (to reduce distortions caused by devaluation or depreciation of the local currency), for 1990-96.. Then a similar average is computed for. domestic assets, and the prudent behavior index, DIFF, representing the rule, is computed as the difference between the two.7. If the average percentage change in adjusted foreign. assets of a central bank is the same as the average percentage change in domestic assets, DIFF is zero and the central bank is following the gold standard rule.. Table 1. Comparison of Central Banking and Currency Board-Like Systems, 1990-96 Number of Countries. Mean Inflation (D). Standard Deviation of Inflation (SDD). Central bank. 68. 0.134. 0.062. Currency board-like. 8. 0.046. 0.022. Monetary System. The relation between this index, called DIFF, and inflation was then examined.. The. measure of inflation adopted is D, the rate of depreciation in the real value of money, proposed by Cukierman (1992, p. 418). In year t, d(t) = 1-1/(1 + πt) = πt / (1 + πt), where πt is the percentage change in consumer prices, and D is the geometric average of the d(t) within each country for the 1990-96 period.8 Sixty-six developing countries were found that met the criteria described.. A series of. tests were then carried out in an attempt to identify additional determinants of inflation (data mining).. The only variable that proved relevant is Latin America (R), a dummy variable. representing countries that were formerly colonies of Spain or Portugal.9 7. The averages were the slopes of regression estimates of semilog trend equations.. 8. Justification for the use of D is two-fold: the real losses on holding money balances are more accurately represented by D then by pi; and D moderates the effect of outliers on regression results. A few countries reported negative changes in consumer prices, no change, or negligible increases; in this case regression estimates of semilog trend equations were used.. 9. Barro (1995) has shown that prior colonial status is closely associated with inflation. During the 1960-90 9 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

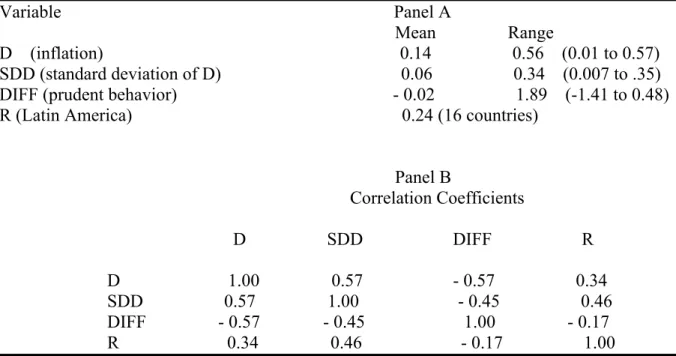

(10) The salient characteristics of the sample are shown in Table 2.. D, SDD (standard. deviation of D), and DIFF have wide ranges and are significantly correlated with one another.10. It is revealing to compare some of the characteristics of the 66 developing. countries that had central banks with the 8 countries, found in the sample selection process that had currency board-like systems.. The classification of these 8 countries was based on. the absence of domestic assets on the balance sheets of their monetary authorities during the 1990-96 period. Table 2. Summary Characteristics of 66 Developing Countries, 1990-96 Variable. Panel A Mean Range 0.14 0.56 (0.01 to 0.57) 0.06 0.34 (0.007 to .35) - 0.02 1.89 (-1.41 to 0.48) 0.24 (16 countries). D (inflation) SDD (standard deviation of D) DIFF (prudent behavior) R (Latin America). Panel B Correlation Coefficients. D SDD DIFF R. D. SDD. DIFF. 1.00 0.57 - 0.57 0.34. 0.57 1.00 - 0.45 0.46. - 0.57 - 0.45 1.00 - 0.17. R 0.34 0.46 - 0.17 1.00. Source: Derived from International Monetary Fund, International Monetary Statistics, various issues in 1998 and 1999.. 5. Regression Results. The two models used to test the basic hypothesis of this study are: D = b1 + b2(DIFF) + b3(R). (1). SDD = c1 + c2(DIFF) + c3(R). (2). period former Spanish or Portuguese colonies had inflation rates more than twice as high as those of former British or French colonies. 10. The critical level of /r/ is 0.25 at the 5 percent level and 0.32 at the 1 percent level, for 60 degrees of freedom.. 10 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(11) The hypothesis translates into the statement that b2 and c2 are negative; support is shown by the estimates reported in Table 3. Table 3. Level and Variability of Inflation, Prudent Behavior, and Latin America 66 Developing Countries, 1990-96 (t-values in parentheses). D = 0.118 (9.86). Panel A: Level of Inflation 0.198DIFF + 0.062R (-5.30) (2.51). -. R-squared = 0.39. Panel B: Variability of Inflation SDD = 0.046 ( 5.81). -. 0.091DIFF + (-3.71). 0.063R (3.88). R-squared = 0.35. The index of prudent behavior, DIFF, is negative and significantly different from zero (at 0.1 percent) for both the level and variability of inflation. A change of DIFF from 0 (GSR, the gold standard rule) to a value of +0.1 would reduce the average level of inflation by 2 percentage points and the average variability of inflation by 1 percentage point. The Latin America dummy is positive and significant for both models. Although there is much unexplained variation in each equation, a series of tests of likely candidates for additional explanatory variables, such as budget deficits, exchange rate arrangements, and financial market development, were unrewarding. A deterrent to adoption of the prudent behavior rule would be if economic growth were negatively affected.. A simple experiment was conducted by changing the dependent. variable of the basic model from D or SDD to G, the average rate of growth of real GDP per capita during the 1990-96 period: G = d1 + d2(DIFF) + d3(R). (3). While this formula makes no pretension to be a complete growth model, it may shed some light on the question of a tradeoff between inflation and growth.. The sample size is reduced. to 53 for measurement of formula (3) owing to the lack of data on real GDP, population, or. 11 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(12) both for 13 countries of the 66.. The result of the experiment, shown in Table 4, indicates a. positive, though small, beneficial effect of prudent behavior on growth. Table 4. Growth, Prudent Behavior, and Latin America 53 Developing Countries, 1990-96 (t-values in parentheses). G = 0.040 + 0.020DIFF (12.68) ( 2.29). 5.1. +. 0.002R ( 0.43). R-squared = 0.09. Tests for other determinants It would be desirable to identify other variables that would improve the fit of the. equations and thereby furnish further insight into the factors that determine the level and variability of inflation. Rather than sift through a large number of regression equations containing different possible independent variables, a procedure used in Fry (1998) is followed here.. First, a number of possible influences on inflation are identified and. measured for the sample countries. Then, a series of tests are carried out to determine whether or not each new variable has an additional impact on the basic model.. This is done. by ranking countries (for which observations on the candidate variable are available) according to the size of the candidate variable, such as the Cukierman legal index of CBI. Next, a group of countries that score highest (on the legal index, for example) and another group, of equal size, that score lowest, are singled out.. The two groups are then combined. into a subsample and the following equation is estimated: D = b0 + b1 DIFF + b2 L.DIFF. (4). L = 0 for the high group and L = 1 for the low group; b1 is the coefficient for the combined groups, b2 is the shift parameter, and (b1 + b2) is the implied coefficient for the low group.. The dummy variable identifying countries in Latin America is omitted from the. model because of problems of multicollinearity: for some variables, Latin American countries are clustered in either the high or the low group. The null hypothesis is b2 = 0, implying that the candidate variable has no impact on the. 12 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

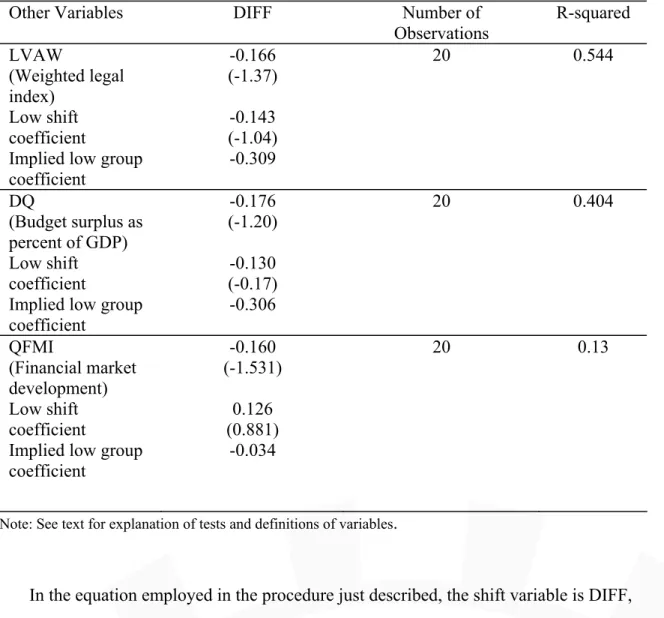

(13) relation between D and DIFF (the real depreciation of money balances and prudent behavior). That is, the relation between D and DIFF is the same for countries with high values of the candidate variable as for those with low values. Results for three possible discriminants are shown in Table 5.. The first variable. examined, LVAW, is a weighted index of legal independence (Cukierman et al., 1992). This index, used by other researchers, is available for 35 countries in the sample of this study. Among the 35, the top ten have the highest values of the index, the bottom ten the lowest values.. Here the shift coefficient is not significantly different from zero (for 17 degrees of. freedom, the critical value of Student’s “t” is 2.11 at the 5 percent level). This is similar to the result found by Cukierman et al. (1992) for 51 developing countries. The second variable, DQ, is the government budget surplus or deficit, measured as a percentage of gross domestic produce (GDP), for the 1990-96 period. were found in the IFS data.. Complete observations for 43 countries. The relative deficit was calculated for each year; the seven year. average was then calculated.. The mean for the 43 countries is 2.6 percent of GDP; the. values range from a surplus of 3.1 percent to a deficit of 9.3 percent. for DQ is also not significant.. The shift coefficient. This finding is consistent with the finding of Sikken and de. Haan (1998) that the impact of budget deficits on the monetary base is not significant for most measures of CBI. In the third section of Table 5, the level of financial market development is assayed as well-developed financial markets are more likely to have independent central banks.. Fry,. Goodhart, and Almeida (1996) classified the development of the money, bond, and equity markets in each country in the Bank of England group, based on responses to the questionnaire regarding CBI and other banking practices.. Each market (money, bond,. equity) was placed in one of four classes: number 1 is the least developed and number 4 is the most developed. country.. The variable QFMI in Table 5 is the average of the four classes for each. There are 23 matches between the Bank of England group and the basic sample of. this study. The shift coefficient between the general pattern and the least developed markets is not statistically significant, so the financial market development index is rejected as a discriminating variable.. 13 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(14) Several other possible variables were examined using the same procedure, but none were found to be significant.. These other variables are: LVAU, an unweighted measure of. legal independence (Cukierman, 1992); two measures of the turnover of central bank governors, covering the 1950-89 and the 1980-89 periods (Cukierman et al., 1992); political vulnerability of the central bank governor (Cukierman and Webb, 1995); development of the money market (Fry, Goodhart, and Almeida, 1996); and budget surplus as a percentage of government expenditures (IFS). Table 5. Tests for Other Determinants, Selected Developing Countries, 1990-96 (t-values in parentheses) Other Variables. DIFF. LVAW (Weighted legal index) Low shift coefficient Implied low group coefficient DQ (Budget surplus as percent of GDP) Low shift coefficient Implied low group coefficient QFMI (Financial market development) Low shift coefficient Implied low group coefficient. -0.166 (-1.37). Number of Observations 20. R-squared. 20. 0.404. 20. 0.13. 0.544. -0.143 (-1.04) -0.309 -0.176 (-1.20) -0.130 (-0.17) -0.306 -0.160 (-1.531) 0.126 (0.881) -0.034. Note: See text for explanation of tests and definitions of variables.. In the equation employed in the procedure just described, the shift variable is DIFF, while the intercept is the average for both the high and the low groups. Each of the tests was also run letting the intercepts vary between the high and low groups.. 14 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics. In this exercise, as in.

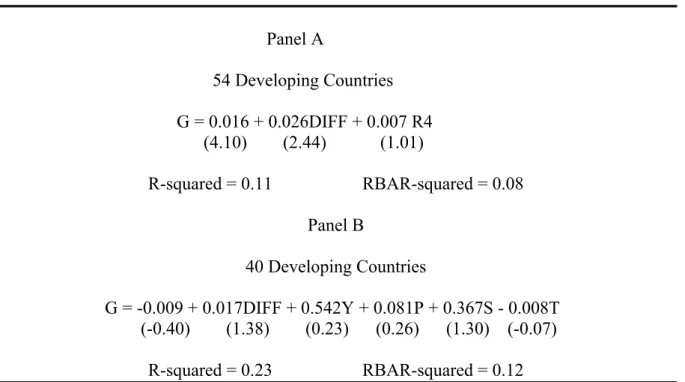

(15) the earlier procedure, none of the shift coefficients is significantly different from zero.. 5.2. DIFF and Output High inflation rates cause inefficient resource allocation and discourage investment.. So to the extent that CBI reduces inflation, it should also result in higher growth (Cukierman et al., 1993).. This is sometimes thought to occur only in the long run, however, while an. output-inflation tradeoff holds in the short run. Evidence on this point in connection with CBI is mixed: several studies have found no relation between CBI, however measured, and growth in industrialized countries (Grilli et al., 1991; De Haan and Sturm, 1992; Alesina and Summers, 1993; Cukierman et al., 1993).. But in developing countries, when turnover of the. governor is used as a proxy for CBI, a positive relation with output growth was found by Cukierman et al. (1993).. All these studies appear to be measuring long run developments.. An examination of the relation between output growth and the index of prudent behavior presented in this study, DIFF, may shed some light on this area of study, but should not be expected to provide definitive answers to the many questions that have been raised. Only 54 of the 68 countries in the basic sample had complete data on real GDP and population, from 1990 to 1996, in the IFS reports.. Growth rates of real per capita GDP were. computed for these 54 countries with a semi-log equation. When these growth rates (G) are regressed on DIFF and R4, the overall association is low (R-squared = 0.11, Table 6). The dummy variable for Latin American countries, R4, is not significantly related to the growth rate, but the coefficient of DIFF is positive and significant, at the 5 percent level.. This. finding is consistent with the finding of Cukierman et al. (1993), that a (different) proxy for CBI is also associated with growth in developing countries.. No relation was found between. the variability of growth and DIFF. It would be desirable to test the validity of CBI as a positive influence on economic growth with a more complete model.. Other influences have been identified as determinants. of growth in cross-section studies (Barro, 1997 Chapter 1; Cukierman et al., 1993): 1.. Initial levels of physical capital and natural resources.. The lower the ratio of. capital to labor, the greater the returns to increases in physical capital. As a proxy for this. 15 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(16) ratio, GDP per capita is used.. A low GDP per capita is associated with subsequent higher. 3growth rates if the capital-labor ratio rises. In addition, convergence of GDP per capita may occur across countries under certain conditions.. So a low GDP per capita indicates the. potential for faster growth, on both counts. Table 6. Growth and DIFF: Two Estimates of the Relationship (t-values in parentheses). Panel A 54 Developing Countries G = 0.016 + 0.026DIFF + 0.007 R4 (4.10) (2.44) (1.01) R-squared = 0.11. RBAR-squared = 0.08 Panel B. 40 Developing Countries G = -0.009 + 0.017DIFF + 0.542Y + 0.081P + 0.367S - 0.008T (-0.40) (1.38) (0.23) (0.26) (1.30) (-0.07) R-squared = 0.23. RBAR-squared = 0.12. Note: G = growth rate of real GDP per capita; R4 = Latin American countries; Y = 1990 GDP per capita in millions of U.S. dollars; P = 1990 primary school enrollment ratio (multiplied by 0.001); S = 1990 secondary school enrollment ratio (multiplied by 0.001); T = 1989-95 rate of change in terms of trade.. 2. capital.. Initial levels of human capital.. The theoretical basis is similar to that for physical. Initial enrollment ratios for primary and secondary education are proxies for human. capital, in that they indicate the ability of a developing country to productively utilize advanced technology imported from abroad. 3.. Change in the terms of trade.. A rise in the average price of a country exports,. relative to the average price of its imports, provides the funds for investment in both physical and human capital. Initial (1990) per capita GDP figures in U.S. dollars were calculated from data in IFS. Primary and secondary enrollment ratios for 1990 were obtained from the United Nations. 16 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(17) Educational, Scientific and Cultural Organization 1995 Statistical Yearbook.. Terms of trade. figures for 1996 are available for only a few countries in the basic sample, so the 1989-95 period was used.. Annual values for this period were collected from the World Bank, World. Development Report, 1992-98 issues. Rates of change for 1989-95 were computed with a semi-log trend equation. Complete information is available from the several sources for only 40 countries.. A. regression estimate of the relation between growth in output (G), and the variables just discussed, as well as DIFF, is not encouraging. None of the variables has a coefficient that is significantly different from zero, and R-squared adjusted for degrees of freedom is only 0.12.. 6. Conclusions Many studies of monetary policy in recent decades concentrated on central bank. independence (CBI) as a key factor in controlling inflation. While most of these covered only industrialized countries, a small number examined developing countries.. A notable. finding is that legal requirements for CBI are associated with lower inflation in industrialized countries, but the association does not hold for developing countries. As a result, behavioral measures have been used as proxies or as direct measures of CBI.. Proxies include measures. of the tenure of the governor both frequency of turnover and turnover associated with changes in government.. Direct measures include the ability of the central bank to neutralize credit. demands of the government and to sterilize changes in foreign assets in order to maintain stability in the monetary base. The prudent behavior index, labeled DIFF, was devised by this study. to a significant degree, inflation rates across the sample.. DIFF explains,. It also explains the variability of. inflation over time for individual countries: this is a problem that is sometimes identified as being at least as harmful as the level of inflation.. At a given value of DIFF, Latin American. countries have significantly higher levels of inflation.. This phenomenon, which has been. discussed by others (Barro, 1995), is (mechanically) accounted for by a dummy variable.. 17 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics. A.

(18) series of analyses with other variables, undertaken in an attempt to provide a better fit to the sample data, yielded no encouraging results. The conclusion drawn from this effort is that, with respect to inflation, a prudent behavior index which is both explanatory and prescriptive has been identified, tested, and found to be predictive. That is, a developing country that follows the rule embodied in the prudent behavior index is likely to have an inflation rate that is both lower and more stable than the average experience. An additional question arises concerning the possible trade-off between inflation and the level of output.. While this complex question will receive no definitive answer from this. modest study, some evidence is offered that a country that follows the rule will not only suffer no penalty in terms of output, but may in fact even enjoy a bonus in the form of a higher level of output.. 18 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(19) REFERENCES. Akland, A.H. (May 1998), Central Bank Independence and Growth, Canadian Journal of Economic, 2, 303-17. Alesina, A. (1988), Macroeconomics and Politics, in National Bureau of Economic Research Macroeconomics Annual, Cambridge, MA: MIT Press, 3, 13-52. Alesina, A. (April 1989), Politics and Business Cycles in Industrial Democracies, Economic Policy, (8), 55-98. Alesina, A. and Summers, L. (May 1993), Central Bank Independence and Macroeconomic Performance, Journal of Money, Credit, and Banking, 25(2), 151-62. Bade, R. and Parkin, M. (October 1988), Central Bank Laws and Monetary Policy, Working Paper, Department of Economics, University of Western Ontario. Bagehot, W. (1873), Lombard Street: A Description of the Money Market, New York, Charles Scribner and Sons. Banian, K.; Laney, O.L. and Willett, D.T. (March 1983), Central Bank Independence: An International Comparison, Economic Review, Federal Reserve Bank of Dallas, 13, 199-217. Barro, J.R. (May 1995), Inflation and Growth, Bank of England Quarterly Bulletin, 166-177. Barro, J.R. (1997), Determinants of Growth: A Cross Country Empirical Study, Cambridge: MIT Press. Barro, J.R. and Gordon, David. (August 1983a), A Positive Theory of Monetary Policy in a Natural Rate Model, Journal of Political Economy, 91(4), 589-610. Barro, J.R. (January 1983b), Rules and Discretion and Regulation in a Model of Monetary Policy, Journal of Monetary Economics, 12, 101-122. Bennett, G.G.A. (September 1995), Currency Boards: Issues and Experiences, Finance and Development, 39-42. Burdekin, C.K.R. and Wohar, E.M. (1990), Monetary Institutions, Budget Deficits and Inflation: Empirical Results for Eight Countries, European Journal of Political Economy, 6, 531 -551.. 19 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(20) Chowdhury, R.A. (1991), The Relationship Between the Inflation Rate and Its Variability: The Issues Reconsidered, Applied Economics, 23, 993-1003. Corsetti, G.; Pesenti, P. and Roubini, N. (September 1998), What Caused the Asian Currency and Financial Crisis? A Macroeconomic Overview, Unpublished. Cukierman, A. (1992), Central Bank Independence: Theory and Evidence, Cambridge, MA: MIT Press. Cukierman, A.; Webb, B.S. and Neyapti, B. (1992), Measuring the Independence of Central Banks and Its Effect on Policy Outcomes, World Bank Economic Review, 6(1), 353-98. Cukierman, A.; Kalaitzidakis, P.; Summers, L. and Webb, B.S. (December 1993), Central Bank Independence, Growth Investment, and Real Rates, Carnegie-Rochester Conference Series on Public Policy, 39, 95-140. Cukierman, A. and Webb, B.S. (1995), Political Influence on the Central Bank: International Evidence, The World Bank Economic Review, 9 (3), 397-423. Debelle, G. and Fischer, S. (1995), How Independent Should a Central Bank Be? in Jeffrey C. Fuhrer, ed., Goals, Guidelines, and Constraints Facing Monetary Policymakers, Federal Reserve Bank of Boston (Boston), Conference Series No.38, 195-221. De Haan, J. and Sturm, J.E. (September 1992), The Case for Central Bank Independence, Banca Nazionale del Lavoro Quarterly Review, (182), 627-649. Eijffinger, C.W.S. and Schaling, E. (March 1993), Central Bank Independence in Twelve Industrial Countries, Banca Nationale del Lavoro Quarterly Review, (184), 49-89. Eijffinger, C.W.S. and Schaling, E. (May 1993), Central Bank Independence: Theory and Evidence, Center for Economic Research, Discussion Paper No.9325, Tilburg University, The Netherlands. Eijffinger, C.W.S. and Schaling, E. (January 1995), The Ultimate Determinants of Central Bank Independence, Paper presented at the CentER Conference Positive Political Economy: Theory and Evidence, Tilburg, 23-24. Eijffinger, C.W.S. and De Haan, J. (May 1996), The Political Economy of Central-Bank Independence, Special Papers in International Economics, No.19, International. 20 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(21) Finance Section, Department of Economics, Princeton University, Princeton, New Jersey. Fischer, S. (1995), Central Bank Independence Revisited, American Economic Review, (Papers and Proceedings), 85, 201-206. Forder, J. (1998a), The Case for An Independent European Central Bank: A Reassessment of Evidence and Sources, European Journal of Political Economy, 14, 53-71. Forder, J. (1998b), Central Bank Independence, Conceptual Clarifications and Interim Assessment, Oxford Economic Papers, 50(3), 307-334. Froyen, T.R. and Waud, N.R. (1995), Central Bank Independence and the Output-Inflation Tradeoff, Journal of Economics and Business, 47, 137-149. Fry, J.M.; Goodhart, A.E. C.and Almeida, A. (1996), Central Banking in Developing Countries, London: Routledge. Fry, J.M. (1998), Assessing Central Bank Independence in Developing Countries: Do Actions Speak Louder than Words? Oxford Economic Papers, 50(3), 512. Fuhrer, C.J. (January/February 1997), Central Bank Independence and Inflation Targeting: Monetary Policy Paradigms for the Next Millennium? New England Economic Review, Federal Reserve Bank of Boston, 19-36. Goodhart, A.E.C. and Huang, H. (1998), Time Inconsistency in a Model With Lags, Persistence, and Overlapping Wage Contracts, Oxford Economic Papers, 50(3), 378-396. Grilli, V.; Masciandaro, D. and Tabellini, G. (October 1991), Political and Monetary Institutions and Public Financial Policies in the Industrial Countries, Economic Policy, 13, 341-92. International Monetary Fund. (September 1998), International Financial Statistics on CD-ROM, Washington D.C.: IMF Publication Services. International Monetary Fund. (1998), International Financial Statistics, Washington D.C.: IMF Publication Services. International Monetary Fund. (February 1999.), International Financial Statistics, Washington D.C.: IMF Publication Services.. 21 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(22) International Monetary Fund. (May 1999), International Financial Statistics, Washington D.C.: IMF Publication Services. Jenkins, A.M. (June 1996), Central Bank Independence and Inflation Performance: Panacea or Placebo? Banca Nazionale del Lavoro Quarterly Review, 49(197), 241-270. Kydland, E.F. and Prescott, C.E. (June 1977), Rules rather than Discretion: The Inconsistency of Optimal Plans, Journal of Political Economy, 85(3), 473-492. Loungani, P. and Sheets, N. (August 1997), Central Bank Independence, Inflation, and Growth in Transition Economies, Journal of Money, Credit, and Banking, 29(3), 381-399. Mangano, G. (1998), Measuring Central Bank Independence: A Tale of Subjectivity and of Its Consequences, Oxford Economic Papers, 50, 468-492. Maxfield, S. (1997), Gatekeeper of Growth: The International Political Economy of Central Banking in Developing Countries, Princeton: Princeton University Press. McCallum, T.B. (1997), Crucial Issues Concerning Central Bank Independence, Journal of Monetary Economics, 39, 99-112. Miller, H.M. (1998), The Current Southeast Asia Financial Crisis, Pacific-Basin Finance Journal, 6, 225-233. Phelps, S.E. (August 1967), Phillips Curves, Expectations of Inflation and Optimal Employment Over Time, Economica, 34, 254-281. Pollard, S.P. (1993), Central bank Independence and Economic Performance, Federal Reserve Bank of St. Louis Review, 75, 21-36. Posen, A. (1998), Central Bank Independence and Disinflation Credibility: A Missing Link, Oxford Economic Papers, 50(3), 335-359. Rogoff, K. (November 1985), The Optimal Degree of Commitment to a Monetary Target, Quarterly Journal of Economics, 100(4), 1169-90. Roubini, N. (March 1991), Economic and Political Determinants of Budget Deficits in Developing Countries, Journal of International Money and Finance, Supplement, 10, S49-S72. Sargent, J.T. and Wallace, N. (1981), Some Unpleasant Monetarist Arithmetic, Federal. 22 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(23) Reserve Bank of Minneapolis Quarterly Review, 5, 1-17. Schaling, E. (1995), Institutions and Monetary Policy: Credibility, Flexibility and Central Bank Independence, Brookfield: Vermont, Edward Elgar Publishing Limited. Schwartz, J.A. (1992), Do Currency Boards Have a Future? Twenty-second Wincott Memorial Lecture delivered at Bisshop Partridge Hall, Church House, Westminster, Thursday, 29 October 1992.. Published by The Institute of Economic Affairs for The. Wincott Foundation. Sikken, B. J. and De Haan, J. (1998), Budget deficits, Monetization, and Central Bank Independence in Developing Countries, Oxford Economic Papers, 50, 493-511. United Nations. (1995), United Nations Educational, Scientific, and Cultural Organization Statistical Years, Lanham: UNESCO and Bernan Press. Walsh, C. (September 22, 1995), Output-Inflation Tradeoffs and Central Bank Independence, Federal Reserve Bank of San Francisco Weekly Letter, No. 95-31. Williamson, J. (September 1995), What Role for Currency Boards? Institute for International Economics, Washington D.C. Woolley, T.J. (1984), Monetary Politics, The Federal Reserve and the Politics of Monetary Policy, Cambridge: Cambridge University Press. World Bank. (1992-1998/1999), World Development Report, New York: Oxford University Press.. 23 第五屆全國實證經濟學論文研討會 The 5th Annual Conference of Taiwan's Economic Empirics.

(24)

數據

+2

相關文件

•In a stable structure the total strength of the bonds reaching an anion from all surrounding cations should be equal to the charge of the anion.. Pauling’ s rule-

‘What Works and for Whom: A Review of OECD Countries’ Experiences with Active Labour Market Policies’, Swedish Economic Policy Review, 8(2): 9-56. ‘Do Wage Subsidies

A) the approximate atomic number of each kind of atom in a molecule B) the approximate number of protons in a molecule. C) the actual number of chemical bonds in a molecule D)

This study primarily represents a collaborative effort between researchers and in-service teachers in designing teaching activities and developing history of mathematics

Miroslav Fiedler, Praha, Algebraic connectivity of graphs, Czechoslovak Mathematical Journal 23 (98) 1973,

and Jorgensen, P.l.,(2000), “Fair Valuation of Life Insurance Liabilities: The Impact of Interest Rate Guarantees, Surrender Options, and Bonus Policies”, Insurance: Mathematics

a) Visitor arrivals is growing at a compound annual growth rate. The number of visitors fluctuates from 2012 to 2018 and does not increase in compound growth rate in reality.

files Controller Controller Parser Parser.