科技部補助專題研究計畫成果報告

期末報告

智慧資本之發展:宏觀與微觀研究-董監事社會網絡之經濟結果

(第3年)

計 畫 類 別 : 整合型計畫 計 畫 編 號 : MOST 102-2410-H-004-158-MY3 執 行 期 間 : 104年08月01日至105年10月31日 執 行 單 位 : 國立政治大學會計學系 計 畫 主 持 人 : 詹凌菁 共 同 主 持 人 : 金成隆 計畫參與人員: 碩士班研究生-兼任助理人員:李元傑 碩士班研究生-兼任助理人員:吳佩珊 碩士班研究生-兼任助理人員:秦如慎 碩士班研究生-兼任助理人員:余友亭 報 告 附 件 : 出席國際學術會議心得報告中 華 民 國 106 年 01 月 18 日

中 文 摘 要 : 本研究探討董事連結關係對於具備產業知識的會計師所提供的高品 質審計服務之需求。以台灣獨特的情況—會計師查核報告須揭露兩 位簽證會計師以及所屬之會計師事務所,作為本研究之資料來源。 實證結果發現,當公司的董事與聘請產業專家會計師的其它公司之 董事連結程度愈高時,其簽證會計師更換為產業專家會計師的可能 性愈高。由於高度投資於研發的公司通常會延攬具備相關經驗的董 事,對高品質審計服務的需求也較高,因此前述的現象多存在於此 類的公司。此外,本研究發現董事連結程度愈高並且更換簽證會計 師為產業專家會計師的公司,其重編財報的可能性較低,尤其是研 發密集的公司。綜合上述,這些發現證實了董事連結對於公司是否 聘任產業專家會計師以及公司財報的品質皆具外溢效果。再者,本 研究顯示在查核報告上揭露簽證會計師,對於董事在做審計相關決 策時,提供了有用的資訊,而這些發現有助於瞭解美國公開公司會 計監督委員會要求查核報告揭露簽證會計師姓名對於會計師之聘任 與審計品質可能造成的影響。 中 文 關 鍵 詞 : 董事網絡關係、董事會連結、產業專家會計師、審計品質 英 文 摘 要 : This study investigates how board networks affect

directors’ demand for high-quality audit services

indicated by auditors’ industry-specific knowledge. Based on the unique data in Taiwan, where audit reports are issued in the name of two signing auditors as well as the audit firm, we find that a focal company is more likely to change its auditors to those with industry expertise either at the audit firm or at the audit partner level when there is an increase in interlocking directors’ connections to other firms that retain industry-specialist auditors. Such evidence exists mainly among firms with high R&D

investments, as these companies tend to look for directors with relevant experience and have a greater demand for high quality audit services. Moreover, we find that firms

experiencing an increase in interlocking directors’ connections and a change to auditors with industry specialists are associated with a lower likelihood of restatements, especially among high R&D-intensive firms. Together, these findings substantiate the spillover effect of interlocked boards on corporate decisions related to the demand for auditor industry specialization and on the quality of financial statements. Moreover, our study contributes to the Public Company Accounting Oversight Board’s debate over the mandatory disclosure of the engagement partner’s identity in the audit report by showing that disclosing the engagement audit partner could provide useful information to a board of directors in making audit-related decisions.

1

Interlocking director and auditor changes: Auditor industry specialization

Abstract

This study investigates how board networks affect directors’ demand for high-quality audit services indicated by auditors’ industry-specific knowledge. Based on the unique data in Taiwan, where audit reports are issued in the name of two signing auditors as well as the audit firm, we find that a focal company is more likely to change its auditors to those with industry expertise either at the audit firm or at the audit partner level when there is an increase in interlocking directors’ connections to other firms that retain industry-specialist auditors. Such evidence exists mainly among firms with high R&D investments, as these companies tend to look for directors with relevant experience and have a greater demand for high quality audit services. Moreover, we find that firms experiencing an increase in interlocking directors’ connections and a change to auditors with industry specialists are associated with a lower likelihood of restatements, especially among high R&D-intensive firms. Together, these findings substantiate the spillover effect of interlocked boards on corporate decisions related to the demand for auditor industry specialization and on the quality of financial statements. Moreover, our study contributes to the Public Company Accounting Oversight Board’s debate over the mandatory disclosure of the engagement partner’s identity in the audit report by showing that disclosing the engagement audit partner could provide useful information to a board of directors in making audit-related decisions.

Keywords: director network, board interlocks, industry-experienced auditors, audit quality JEL classification: M41, M42, G30

2

1. Introduction

Prior research indicates that auditors’ industry expertise is a key determinant of client satisfaction with audits. In order to be proactively involved in the business and to anticipate the accounting issues that will affect the client firm, auditors must thoroughly understand the business and industry, and auditors with industry expertise are expected to be more responsive to the client’s needs.1 Indeed, the importance of having knowledge specific to a client’s industry is supported by

global audit firms, as summarized in the highlights below.

“We’ve built dedicated teams around each industry we serve, tapping professionals who have spent

years in senior positions with leading companies. Their experience brings a strategic and practical

perspective on what works — and what doesn’t. Our teams include high-profile luminaries who are

widely recognized as leaders in their industries, bringing the profound knowledge and cutting-edge

insight required to meet today’s biggest challenges.” (Deloitte)

“You’re competing in a complex environment encompassing technology, supply chains, skilled

workers, accounting standards, competitors, and probably more than a handful of regulators and tax

authorities. Our industry-focused network is designed to anticipate and address your business needs.” (PWC)

1 A survey conducted by Behn et al. (1997) shows that controllers are concerned about having to train a new audit team

each year due to the lack of knowledge of the industry in which the client operates. To improve audit service quality and to reduce audit team turnover, audit partners are expected to be more proactively involved in the client’s business.

3

As auditing is a professional service that is relationship-driven, managers may be inclined to hire auditors who are more compliant regarding their wishes, resulting in the concern that external auditors may end up being advocates for the management. As one of the most important functions of the board of directors is the selection of external auditors, we begin by exploring if a firm is more likely to select auditors who are industry specialists when it shares a director with another firm that retains auditors with industry expertise. Director interlocks are seen as a communication mechanism through which companies share information about acceptable and effective corporate practices. Directors holding multiple directorships may bring knowledge of accounting firms and auditors that could be of economic benefit to the focal company. Through their effective monitoring of corporate decisions regarding external audit services, we argue that interlocking directorates act as an essential conduit of information regarding the benefits of having auditors who are industry specialists.

Prior evidence generally confirms that industry specialists can provide their clients with better audit and non-audit services (e.g., Owhoso et al., 2002; Bedard and Biggs, 1991). A number of studies document that earnings quality is higher for clients audited by industry specialists than for those audited by non-specialists (e.g., Balsam et al., 2003; Krishnan, 2003; Myers et al., 2005; Chin and Chi, 2009). In addition, industry specialists exhibit greater compliance with auditing standards than non-specialists (O’Keefe et al., 1994) and are less likely to be associated with SEC (the US Securities and Exchange Commission) enforcement actions (O’Keefe et al., 1994; Carcello and Nagy, 2004). We investigate if a firm’s propensity to switch to industry-specialist auditors, at either the

4

audit firm or the partner level, spreads through interlocked boards, which would in turn affect audit quality. In doing so, we intersect and contribute to two strands of literature: (a) the impact of the social network formed through interlocking directorates on corporate practices (e.g., Hirshleifer and Teoh, 2009; Stuart and Yim, 2010; Garmaise and Moskowiz, 2003; Brown, 2011) and (b) the role of the board of directors in monitoring the selection of auditors (e.g., Cohen et al., 2010; Beasley et al., 2009; Fiolleau et al., 2013). There is currently little empirical evidence on the influence of directors on audit-related decisions, and we fill this gap. Our goal is to provide a deeper understanding of the factors that enable firms to utilize interlocking directors’ knowledge and experience by focusing on the following two issues. First, we explore whether interlocking directors’ outside experience is indeed a resource that influences firms’ decisions to appoint auditors with industry expertise. Second, we examine the financial reporting benefits that the focal firms incur in utilizing interlocking directors’ knowledge.

To test our predictions, we use a sample of listed firms in Taiwan. In contrast to the US, where only the auditing firm’s name is stated, audit reports in Taiwan must have two signing auditors (lead and concurring auditor) as well as the auditing firm’s name. The availability of this additional data provides us with a unique setting for investigating the alleged effect of interlocked boards on the choice of industry specialists at the audit firm and audit partner levels. We find that the focal firm’s propensity to change to industry specialists at the audit firm level (or partner level) is greater when

5

there is an increase in shared director connections between the focal firm and another firm that retains audit firm-level (or partner-level) specialists.

The extent to which interlocking directors having an influence on the switch to industry specialist auditors may depend on the nature of company-specific attributes. Firms facing similar economic environments may have preferences for similar director characteristics. These similarities or preferences may result in a higher frequency of industry-specialist auditors in board-linked firms. Prior studies indicate that companies with growing opportunities are more likely to acquire and utilize interlocking directors’ relevant experience (e.g., Diestre et al., 2015) and they also tend to have a greater demand for a higher quality of audit services (e.g., Godfrey and Hamilton, 2005; Mascarenhas et al., 2010). Firms with high R&D investments tend to have particular opportunities for growth. Our results show that the propensity to switch to industry-specialist auditors either at the audit firm or the partner level when there is an increase in interlocking directors exists mainly among high R&D-intensive firms.

To gain insights into the potential benefits of the effects of interlocking directors’ influence on auditor choice, we further investigate whether the focal firm is associated with better financial reporting quality when the increase in interlocked directors with relevant outside experience of industry-specialist auditors is accompanied by a change to an audit firm or audit partner with industry expertise. Our empirical results indeed confirm this conjecture and show that such benefits are

6

associated with a lower likelihood of restatements, which is more prevalent among firms with high R&D intensity.

In additional analyses, we further investigate whether interlocking directors bring in other benefits to the focal company by investigating their impacts on the focal firm’s bargaining power in the audit pricing process. The results show that initial engagements are associated with lower audit fees, and this is more pronounced among companies that experience both an increase in interlocking directors who are connected to other companies that appoint auditors with industry expertise and a change in auditors to those with industry expertise. These findings are consistent with prior literature, suggesting that clients tend to enjoy an audit fee discount when they make a voluntary auditor switch (e.g., DeAngelo, 1981). Together, our evidence implies that interlocking directors with greater exposure to industry-specialist auditors may take the opportunity to contribute to the improvement of the focal company’s financial reporting quality by suggesting a change to industry-specialist auditors, and they may also play a role in negotiating audit fees.

We contribute to the literature on accounting and board social networks in several ways. First, we find that there is an association between the preference for industry-specialist auditors and directors’ social networks. Specifically, we provide evidence that a firm’s accounting practices can spread from one firm to another via board-based social networks. Next, we document that the financial reporting quality of the focal company is better when the increase in interlocking directors is accompanied by a change to auditors with industry expertise. In other words, there is an audit

7

quality spillover effect that spreads through board interlocks. Our findings also contribute to the literature on corporate governance by documenting that a firm’s external governance mechanism (i.e., external networks via interlocked boards) complements its internal monitoring system. In turn, this external governance mechanism has a significant effect on the firm’s earnings and audit quality. In addition, our study responds to the ongoing dispute regarding managers’ influence on the auditor selection process (Cohen et al., 2010; Beasley et al., 2009; Fiolleau et al., 2013). Consistent with Beasley et al. (2009), our results imply that board members with relevant external experience do play an important monitoring role in ensuring the audit quality of the focal company. Lastly, the findings have implications for the Public Company Accounting Oversight Board’s (PCAOB) debate over the mandatory disclosure of the engagement partner’s identity in the US (PCAOB, 2009, 2011). Increased transparency regarding the engagement partner’s identity could reduce the uncertainty associated with the evaluation of partner-specific information. Our findings suggest that such transparency provides an opportunity for the general public to evaluate the audit partner’s industry experience, and that the board of directors could then incorporate this information into their decisions. Taken together, our findings have important policy implications for regulators and both providers and consumers of audit services.

The remainder of this paper is organized into five sections. Section 2 describes the institutional background and reviews relevant literature. Section 3 describes our research design, sample selection,

8

and data sources. Section 4 reveals the empirical results and findings. Section 5 presents our conclusions.

2. Literature and hypotheses

2.1 Auditing practices in Taiwan

A number of studies have indicated that industry knowledge and expertise in auditing are derived from the auditing firm’s human capital investment in accounting professionals with experience based at the city level (Francis et al., 1999; Solomon et al., 1999). In this study, we take advantage of a research setting that allows us to go further and identify audit partner-level industry specialists. In contrast to the US, where the audit report bears the signature of the audit firm and the city in which the audit firm is located, the audit report in Taiwan is issued in the names of not only the audit firm but also the two signing auditors. The Taiwanese Securities and Futures Bureau (“TSFB”; similar to the SEC in the US), through Article 2 of the Criteria Governing Approval for Auditing and Certification of Financial Reports of Public Companies by Certified Public Accountants (“CGAAC”), stipulates that the financial reports of public companies in Taiwan must be audited by practicing certified public accountants from audit firms and signed by the practicing auditors.2 In addition, to

2The TSFB has stipulated four policy directives for the purpose of administering and supervising securities issuance,

securities trading and futures trading; facilitating national economic development; protecting investors’ interests; developing the futures market; and maintaining futures trading orders. These are as follows: (1) to foster the sound development of the capital markets and to encourage fundraising through public offerings of securities; (2) to improve the operation of the securities and futures markets and to ensure a fair and efficient market environment; (3) to promote the

9

enhance the credibility of audit quality, the TSFB amended the CGAAC in 1982 and mandated that the financial reports of listed companies should be jointly audited and signed by two practicing auditors as well as the audit firm, commencing in the year 1983. In parallel with the requirements set by the TSFB, the Statement of Auditing Standard No. 33, Auditor Report on Financial Statements, also requires audit reports to be signed by two independent auditors and the auditing firm. In practice, joint auditorship is often characterized by a lead auditor, who imposes quality standards, and a “second auditor” (or concurring auditor) of a lower caliber (Piot and Janin, 2007). Such joint auditorship not only reinforces auditor independence but also has the advantage of offering a second look at the auditing diligence.

In Taiwan, auditors are governed by the Security and Exchange Act, Business Accounting Law, and Certified Public Accountant Law. As the two signing auditors and the audit firm co-sign the audit report, they are held jointly liable for the potential civil liability and administrative sanctions arising from fraudulent financial statements. In addition, the signing auditors would be deemed to have joint criminal responsibility in such an event.3 This unique institutional environment provides us with a

natural laboratory in which to investigate whether information transmitted via interlocked

development of the securities service industries and to facilitate the flow from savings into investment; and (4) to regulate certified public accountants and to enhance their professional standards (http://www.sfb.gov.tw/e1-2.asp).

3 See, for example, Articles 32 and 174 of the Security and Exchange Act, Articles 71 and 72 of the Business Accounting

Law, and Articles 39 and 40 of the Certified Public Accountant Law. In the well-known Procomp scandal in Taiwan, which involved fraudulent financial statements and top management fraud, managers were subject to criminal charges, and the signing partners were all suspended from practicing for two years. In addition, the auditing firms were subject to substantial civil monetary penalties.

10

directorates has an impact on the focal company’s demand for audit services provided by industry specialists at the audit firm level and the audit partner level.

2.2 Literature and predictions

Interlocking directorates

The board of directors plays a key role in managerial oversight and provides advice and guidance on corporate strategy. Because of the important role the board plays in key business decisions, board members themselves are often the executives of other firms, or they have significant business, legal, or political experience. The limited pool of qualified candidates also contributes to the fact that it is common for a board member to sit on the boards of more than one firm. Directors’ knowledge varies not only with the nature of their focal firm experience, but also with their outside experience, in terms of the number and status of their outside affiliations (Shropshire, 2010). Directors with more outside experience are expected to have broader exposure to and awareness of accounting practices. As such, board connections between firms can be beneficial if they facilitate the efficient transfer of information and knowledge.4

4 As discussed in Shropshire (2010), the degree to which the diffusion of information through interlocked directors

affects the focal firm may depend on several factors, such as interlocking directors’ depth of focal firms experience and their committee membership at the focal firm. We address this issue in the additional analyses.

11

Little work to date explores the effect of board interlocks on accounting practices.5 Brown

(2011) examines whether social connections influence the pattern of tax shelter adoption, and finds that network ties via board interlocks increase the likelihood of adopting the corporate-owned life insurance shelter. Chiu et al. (2013) find that earnings management is more likely to happen in firms that share a director with another firm that is managing earnings, and that this kind of contagion effect is stronger when the shared director has a leadership role or holds an accounting-relevant position. Our study fills the void in the literature by investigating whether interlocked directors’ relevant experience is associated with the focal firm’s decision to switch to industry-specialist auditors either at the audit firm or partner level and whether this is accompanied by an improvement in the focal firm’s financial reporting quality.

Auditor switching

Determinants of auditor choice have been widely discussed in the auditing literature (e.g., Francis and Wilson, 1988; Beattie and Fearnley, 1995; Johnson and Lys, 1990; Francis et al., 1999; Abbott and Parker, 2000; Beasley and Petroni, 2001). Several studies also document the relationship between firm characteristics and the demand for higher audit quality in the form of brand-name (e.g.,

5 The extant literature on interlocking boards focuses primarily on the effects of these social networks on different areas

of finance, such as the adoption of poison pills and golden parachutes (Davis, 1991; Davis and Greve, 1997), option backdating (Bizjak et al., 2009), synchronicity (Khanna and Thomas, 2009), going private (Stuart and Yim, 2010), M&As (Cai and Sevilir, 2012), venture capital (Hochberg et al., 2007), strategic alliances (Robinson and Stuart, 2007), and entering lending markets (Garmaise and Moskowiz, 2003). These studies generally support the argument that corporate behavior spreads through the board of directors networks.

12

Chaney et al., 2004; Kim et al., 2003) and industry-specialist (e.g., Mascarenhas et al., 2010) auditors. However, these empirical studies rarely consider social ties or personal relationships involved in business decisions. Auditing is a professional service that is relationship-driven and sensitive to market expectations and perceptions. Based on a survey of audit partners regarding the information that they believed to be most important in the development of professional services, Hooks et al. (1994) found that client referrals and recommendations were deemed the most important information source, followed by referrals from within their own firms, business contacts, a reputation for expertise, referrals from former colleagues, and contacts made through non-business organizations.

There has been concern that an external auditor is often an advocate for the management rather than an independent agent protecting shareholders’ interests. In the US, despite clear requirements on auditor selection under SOX, a recent survey shows that it is the managers who dominate the auditor selection process, and that audit committees merely participate in meetings with prospective audit partners and assess their suitability (Cohen et al., 2010).6 In other words, post-SOX, Big 4 audit

partners still believe that managers, rather than the audit committee, are the key driver of auditor selection. In contrast, Beasley et al.’s (2009) survey of audit committee members shows that audit committees are taking responsibility for auditor selection as stipulated by SOX, which is consistent with the regulatory view (Beasley et al., 2009). Despite the regulator’s concern over management’s influence on auditor selection, it is difficult to empirically determine the extent to which managers

6 A survey carried out by Fiolleau et al. (2013) suggests that hiring an affiliated auditor does not necessarily result in

13 participate in and control the process.

When auditor switching is initiated by a client, a common explanation is that the company is searching for favorable treatment from the auditor (i.e., opinion shopping) or a reduction in audit fee. For example, if a company’s financial condition has been deteriorating, it may switch to a new auditor to suppress negative information or to avoid a going concern opinion (Kluger and Shields, 1989; Chow and Rice, 1982; Eichenseher and Shields, 1983). In this case, the decision to switch auditors will signal poor financial prospects and will be negatively perceived by the market. However, there are other possible reasons for switching auditors, including that a company may switch to a higher-quality auditor in order to provide more credible information to investors and creditors. In fact, empirical evidence shows that market participants react positively to an auditor switch from non-specialist to industry-specialist auditors (Knechel et al., 2007).

The role of industry-specialist auditors

Auditors that are industry specialists are likely to have the incentive and the ability to provide high-quality audit services. Prior studies document that industry-focused audit firms invest more in technologies, physical facilities, personnel, and organization control systems that can improve the quality of their audits for the industries in question (e.g., Simunic and Stein, 1987). In addition, industry-experienced auditors are better able to detect errors within their industry specialization than outside of it (Owhoso et al., 2002; Bedard and Biggs, 1991). There is evidence from the US, Australia,

14

Taiwan, and Hong Kong showing that a Big N auditing firm’s national industry expertise results in a market premium over the fees paid to other auditing firms (Craswell et al., 1995; DeFond et al., 2000; Francis et al., 2005). Industry-specialist auditors exhibit greater compliance with auditing standards than non-specialists (O’Keefe et al., 1994) and are less likely to be associated with SEC enforcement actions (Carcello and Nagy, 2004). Research also indicates that earnings quality is better for client firms audited by industry specialists than by non-specialists (Balsam et al., 2003; Krishnan, 2003, 2005; Chen et al., 2005). Overall, these studies confirm that audit firm-level industry expertise offers value to clients, and that capital markets view audits provided by industry specialists as being of higher quality.

Despite the prevailing evidence regarding the high-quality audit services provided by industry specialists at the audit firm level, it is the auditors in individual offices who actually contract with the clients and conduct the auditing services, rather than the entire auditing firm. Empirical evidence shows that the higher audit fees charged by the Big N industry specialists are driven mainly by particular offices based in specific cities (Ferguson et al., 2003; Francis et al., 2005). Reichelt and Wang (2010) further find that earnings quality, measured as accruals and the frequency of meeting or beating analysts’ earnings forecasts, is higher for firms audited by industry experts, whether the city office or the entire national firm is the expert. In contrast, earnings quality of firms audited by national firms that are industry specialists but where the individual offices are not specialists is not significantly different from that of firms audited by non-specialists.

15

As mentioned in Section 2.1, audit reports in Taiwan are issued in the names of both the audit firm and also the two signing auditors. Prior studies show that differences in audit quality due to industry expertise are primarily attributable to the signing partner being a specialist, rather than the audit firm itself specializing in an industry, and that the clients of the signing auditors who are industry specialists tend to have better audit quality (Chin and Chi, 2009; Chi and Chin, 2011). We follow this line of research and investigate whether interlocking directors who are connected to firms audited by industry specialists will also demand high-quality auditors proxied by industry specialists either at the audit firm level or lead partner level.

We focus on the influence of interlocking directorates on the decision to switch to industry-specialist auditors for the following three reasons. First, examining whether interlocking directors’ relevant knowledge and experience influences a change in auditor adds to our understanding of the relative power of directors and management in the decision over auditor selection. As management may dominate the auditor decision, and their influence over such decisions is difficult to observe from outside the firm, we acknowledge that the power of the board relative to the managers may be stronger under certain circumstances. Second, managers may not prefer industry-specialist auditors. That is, management may be more inclined to hire an auditor who is more accommodating and allows them some degree of flexibility to attain earnings goals without jeopardizing their stewardship of the shareholders’ investments (Abbott and Parker, 2000; Williams, 1988). As non-specialist auditors have less expertise and reputational investment in the industry, they

16

are more likely to comply with the managers’ wishes. Management may also wish to avoid paying the premium associated with an industry specialist. Third, interlocking directors’ experience obtained at other organizations may increase the chances of the directors being acquainted with industry-specialist auditors, and enable them to provide more detailed knowledge about auditors’ backgrounds and professional experience. Given that an auditor switch tends to involve a request for proposals, directors’ knowledge of and acquaintance with auditors may play an influential role in the final auditor appointment decision. We argue that interlocking directors who have seen the benefits of appointing industry-specialist auditors at other firms are likely to share this experience and provide advice in board discussions.7 Findings of our study could complement recent survey- and case-based

studies of managers’ continued influence on auditor selection (e.g., Cohen et al., 2010; Beasley et al., 2009; Fiolleau et al., 2013).

Predictions

We propose that interlocked directors’ experience with and knowledge of industry-specialist auditors obtained from other organizations serves as an alternative source of information in the decision of auditor choice. Interlocking directors are likely to have more opportunities to be acquainted with auditors, gain experience from participating in board-level discussions of auditor

7 Discussions held by the authors with Big 4 audit partners and managers affirmed that referrals and recommendations

made through acquainted directors is an alternative channel for the development of professional services. It is possible that directors holding multiple board positions recommend auditors’ services to potential clients, supporting our conjecture about information transmission regarding industry-focused audit services among interlocked directors.

17

appointments, and directly perceive the quality of audit services provided by industry-specialist auditors. Interlocking directors with relevant experience at other firms may generate a force for a change to industry-specialist auditors, especially when a firm demands a higher level of audit quality. The reasons are as follows. First, one of the main motivations for becoming a director is to play a useful role and be helpful to the firm (e.g., Boivie et al., 2012). The resource dependence perspective of corporate boards also suggests that firms rely on directors as a way to reduce the inherent uncertainty associated with corporate decisions. In line with this logic, firms with a greater demand for high-quality audit services are likely to utilize this source of information as a way to reduce any uncertainty associated with the choice of auditors. Having access to audit-related information at other companies provides interlocked directors with more detailed information about the characteristics and background of specific auditors, which may enable them to recommend auditors with experience relevant to the needs of the focal company. Second, companies facing uncertainty associated with the decision to change auditors are inclined to look for trustworthy auditors, something that is less likely to be perceivable by just anyone in the industry. In a field study by Fiolleau et al. (2013), interviews with audit partners revealed that a critical factor for them in developing their proposals was assembling a team not only with industry experts and firm leadership, but also with established client relationships. As networks of personal relationships could influence the choice of auditors, we argue that interlocking directors are conducive to the establishment of an auditor-client trust relationship, which may increase the likelihood of a firm selecting auditors with industry expertise. This leads to

18 our first hypothesis.

H1: An increase in interlocking directors who serve in other firms that retain industry-specialist

auditors increases the likelihood of the focal firm switching auditors to industry specialists either at

the audit firm or partner level.

Firms can rely on several sources of information as a way to mitigate and overcome uncertainties associated with corporate decisions. They can either rely on their own learning from previous experience or obtain vicarious knowledge by accessing the experiences of other companies. We consider whether imitation behavior in an interlocking network is more likely to occur among companies with high growth opportunities. Prior studies show that firms with growth opportunities tend to look for directors who have relevant experience (e.g., Diestre et al., 2015), and they are also likely to appoint industry-specialist auditors (Godfrey and Hamilton, 2005; Mascarenhas et al., 2010). Firms with high investments in R&D tend to have operations that are difficult or costly to replicate, and thus are considered to have greater opportunities for growth. R&D activities are generally long-term in nature, high risk, and difficult to measure, and their value mainly depends on future outcomes. As such, agency problems could occur if managers fail to invest in positive Net Present Value (NPV) projects or transfer wealth arising from R&D investments away from stakeholders. Prior studies indicate that the demand for better audit quality is associated with agency costs (e.g., Francis et al., 1999). Godfrey and Hamilton (2005) find that R&D intensity is positively associated with firms’ choices of specialist auditors proxied by whether the auditor is an industry market leader,

19

a top-tier auditor, or specialized in auditing R&D contracts. We expect that the appointment of industry-specialist auditors can be part of the monitoring system used by the board of directors. If interlocking directors’ experience with high-quality audit services leads to a change to industry-specialist auditors for the focal company, we expect such auditor change to exist mainly among companies with high R&D investments. This leads to the following hypothesis:

H2: Interlocking directors’ effect on auditor changes exists mainly among firms with high R&D

investments.

One may argue that directors’ ties could be harmful to shareholders and that coordinated action among directors is possible when directors are interlocked. This arises from the concern that interlocks between directors may compromise their effectiveness and lead them to favor directors’ or managers’ interests over shareholders’ interests. Prior studies show that shareholders react negatively to interlocks (Devos et al., 2009), and this is perhaps justified by interlocked firms’ tendencies to engage in actions beneficial to management but harmful to shareholders (Bizjak et al., 2009; Davis, 1991; Frankforter et al., 2000).

As such, there are likely to be two competing mechanisms within the relationship between interlocking directorates and audit quality, i.e., the monitoring incentive versus the collusion effect. On the one hand, interlocking directors could take the opportunity to make a contribution and force a change in the focal firm to ensure that shareholders’ benefits are protected. A change to industry-specialist auditors is likely to be associated with improved audit quality. On the other hand,

20

when directors’ independence is compromised, the influence may be detrimental to shareholders’ interests as industry-specialist auditors may be more compliant regarding the wishes of the directors – which could be independent of or aligned with management’s wishes – which may impair the quality of the audit service. We conjecture that the benefit of having interlocking directors outweighs the potential collusion effect as industry-specialist auditors would be reluctant to risk their reputations. Therefore, we further hypothesize that companies with board interlocks to firms that retain industry-specialist auditors are likely to have better audit quality if they switch to industry-specialist auditors. We use the likelihood of accounting restatements as a proxy for audit quality, as restatements arising from the violation of GAAP impose greater costs on companies and investors compared to other proxies of audit quality, such as discretionary accruals and going concern reports (e.g., Palmrose et al., 2004; Myers et al., 2005). Using a sample of listed firms in Taiwan, Chin and Chi (2009) find that signing auditor experts, either alone or in conjunction with firm-level experts, are associated with a lower likelihood of accounting restatements. We expect that firms that have an increase in interlocking directors with connections to other firms that retain industry-specialist auditors and also experience a change of auditors from non-industry specialists to industry specialists, either at the audit firm level or lead partner level, are associated with better audit quality, as indicated by a lower likelihood of accounting restatements. This leads to our inference regarding the potential impact of interlocking directors on audit quality.

21

H3: Firms that experience an increase in interlocking directors who serve in other firms that retain

industry-specialist auditors and also a change to industry-specialist auditors are associated with a

lower likelihood of accounting restatements.

3. Research design and data

3.1 Model

Interlocked directors and the selection of industry-specialist auditors

To investigate whether information is shared between interlocked boards regarding high-quality services provided by industry-specialist auditors, we run the following logistic model at the audit firm and partner levels, respectively.

AUDITCHANGE α α ∆SPELINK α ∆SIZE α ∆LEV α ∆ROA α ∆LOSS α ∆CURRENT

α ∆QUICK α ∆ATURN α ∆CAPINT α ∆ISSUE α ∆PE α ∆OPCYCLE

α ∆DIR α ∆INDEP α ∆DUAL α ∆BOARD Year fixed effects

Industry fixed effects ε 1

We measure AUDITCHANGE at either the audit firm or partner level. AUDITCHANGE_audit firm is a

dummy indicator equal to one if there is both a change in audit firm and a change from a non-industry-specialist to an industry-specialist audit firm, and zero otherwise. AUDITCHANGE_lead

22

non-industry-specialist to an industry-specialist lead partner, and zero otherwise. We allow for a three-year period to ensure the dependent variable captures an actual change in both auditor and auditor industry-specialization designation. Prior studies have found that more experienced auditors are more capable of recognizing irregular errors and detecting material misstatements (e.g., Kaplan et al., 2008). We define the lead partner as the signing auditor with the longer tenure with the client, following Liu and Wang (2008).8 If both auditors have the same tenure, the firm is considered to have

appointed an industry expert if at least one of the signing auditors is an industry specialist. Our industry classification follows the classification of the Taiwan Economic Journal. For an industry to be included in our sample, a minimum of ten companies are required. Following previous studies (e.g., Gramling and Stone, 2001; Krishnan, 2003; Chin and Chi, 2009; Balsam et al., 2003), we use market share as a proxy for industry expertise, measuring market share using the total assets of clients within the industry that are audited by the auditing firm (or partner).9 We define industry specialists

as the two highest-ranked audit firms or partners from each industry-year.

8 Anecdotal evidence documents that the lead auditor is responsible for recruiting the client and carrying out the main

audit work. However, concurrent auditors generally lack experience and expertise and only help with reviewing the audit work. As it is difficult to identify the lead partner from Taiwanese audit reports, other researchers have considered the first auditor to be the lead auditor, as he/she usually has more experience than the second auditor (e.g., Chi and Chin, 2011). We find that around 75 percent of the first auditors in our sample have more experience than the second auditor. Untabulated results using the first auditor named in the audit report as the lead auditor (rather than identifying the lead auditor by tenure) lead to similar conclusions.

9 For the sake of robustness, we also use sales-based measures as alternatives. The untabulated results support our main

23

Our variable of interest in Equation (1), ΔSPELINK, is the change in the number of board links the focal firm has with other firms that retain audit firms that are industry specialists (ΔSPELINK_audit firm) or lead partners that are industry specialists (ΔSPELINK_lead partner). To be

consistent with our dependent variable measure, all independent variables are measured as the difference from year t-3 to year t. Following prior studies (e.g., Mascarenhas et al., 2010; Chaney et al., 2004; Godfrey and Hamilton, 2005), we control for changes in several company-specific characteristics that are related to auditor choice, the presence of industry-specialist auditors, and the demand for higher audit quality. SIZE is the natural log of sales; LEV is total liabilities divided by total assets; ROA is net income divided by total assets; LOSS is a dummy variable equal to one if net income is negative, and zero otherwise; CURRENT is current ratio calculated as current assets divided by total assets; QUICK is quick ratio measured as current assets less inventory divided by current liabilities; ATURN is asset turnover calculated as sales divided by total assets; CAPINT is capital intensity calculated as gross property, plant, and equipment scaled by sales; ISSUE indicates a significant increase in outstanding shares, which is equal to one if the number of outstanding shares increases by more than ten percent, and zero otherwise; PE is the price-to-earnings ratio; and OPCYCLE is the operating cycle measured as a day’s sales in inventory and receivables divided by thirty. We further control for changes in several corporate governance indicators. DIR is the proportion of shares held by directors and supervisors; INDEP is the proportion of independent directors on the board; DUAL is a dummy indicator taking the value of one if the CEO and the

24

president are the same person, and zero otherwise; and BOARD is board size. If there were to be a spillover effect of high-quality audit services through information sharing, we would expect to see positive coefficients of ΔSPELINK at the audit firm and audit partner levels. That is, interlocking boards form a social network through which board members carry corporate practices from one company to another, and this acts as an effective channel for transmitting auditor choice decisions.

Further, we argue that firms with growing opportunities proxied by R&D intensity are more likely to acquire and utilize interlocking directors’ experience and also have a greater demand for a higher quality of audit services provided by industry-specialist auditors. To test this assertion, we run Equation (1) for two sub-samples, i.e., high vs. low R&D investments, based on the yearly median values of R&D intensity (R&D expenditures over sales). We predict that the coefficient of ΔSPELINK is positive for firms with high R&D investments, as companies with high growth opportunities have a greater demand for high-quality auditors in order to reduce agency costs associated with transfers of future R&D investments, and the verification of R&D expenditures occur in relation to value-adding activities, placing a greater emphasis on interlocking directors’ outside experience with auditors who are industry specialists.

Interlocked directors and audit quality

25

auditors on the audit quality of the focal company. We measure audit quality using the probability of making an accounting restatement. Prior studies show that restatements are an acknowledgement that prior financial reports were not in accordance with GAAP (Palmrose and Scholz, 2004) and indicate reduced credibility of accounting information. To test H3, we create a dummy indicator, FIRMDUM, equal to one for firms that experience both an increase in interlocking directors from year t-3 to year t and a change of auditors from non-industry specialists to industry specialists, and zero otherwise, and perform the following logit model:

RESTATE α α FIRMDUM α SIZE α LEV α ROA α LOSS α CAPINT α PE α OPCYCLE α DIR α INDEP α DUAL α BOARD α FSPE Year fixed effects

Industry fixed effects ε 2

where RESTATE equals one if a firm restates its financial reports, and zero otherwise.

We include several firm-specific control variables that could affect the quality of earnings and further control for the presence of an industry specialist at the focal company at the audit firm level (FSPE). FSPE is a dummy variable equal to one if the focal company is audited by an industry-specialist audit firm. We expect SIZE, ROA, and FSPE to be negatively associated with audit quality (Chi and Chin, 2011), and LEV and LOSS to be positively associated with earnings management activities that would result in lower audit quality (Burns and Kedia, 2006). A firm’s growth rate may have a negative impact on the ability of its internal control structure and accounting

26

system to properly record and value its transactions (Beasley, 1996), leading to a negative relationship between PE and audit quality. We also include the proportion of shares held by directors and supervisors (DIR), the proportion of independent directors on the board (INDEP), duality (DUAL), and board size (BOARD) as corporate governance control variables. We expect that firms that experience an increase in interlocking directors’ connections and also a change to industry specialist auditors is associated with better audit quality, and we predict a negative coefficient of FIRMDUM in Equation (2).

3.2 Description of data

Data for companies listed on the Taiwan Stock Exchange during 2003-2009 are obtained from the Taiwan Economic Journal database. The original sample is 8,801 firm-year observations. Our regression models capture changes in audit firms and partners, which requires our sample firms to have at least three years of data. After excluding missing accounting, market-based, and corporate governance data, the final sample consists of 6,639 firm-year observations.10 The electronics sector

provides the largest number of observations (57.54 percent), followed by chemical and biotechnology (6.42 percent). To control for outliers, all continuous variables except for the board link indicators are winsorized at the top and bottom one percent of observations.

10 We also perform a robustness check using the sample of listed companies audited by Big 4 firms, which makes up 83

27

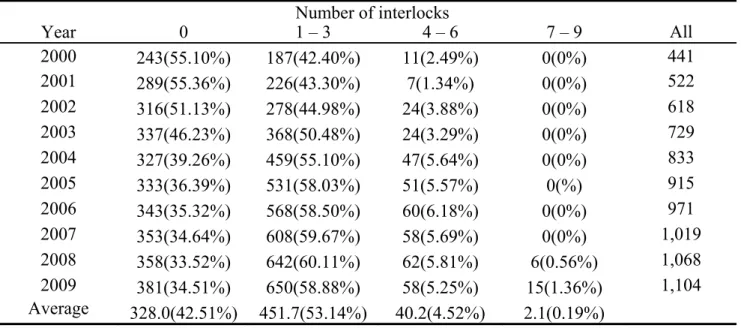

[TABLE 1 ABOUT HERE]

To provide some background on the pervasiveness of companies sharing common directors, Table 1 illustrates the number of board interlocks in each year from 2000 to 2009. On average, 42.51 percent of the sample firms are isolated in that none of their directors serve on the boards of other public firms during the year in question. However, the trend is for more firms to be connected to at least one other firm through board interlocks towards the end of the period.

Table 2 provides summary statistics for the sample. Around 7.4 percent of the firms change their audit firms to industry specialists (AUDITCHANGE_audit firm), and 1.6 percent change lead

partners from non-specialists to specialists (AUDITCHANGE_lead partner). The mean value of the

change in the number of board links with other firms that appoint industry-specialist auditors at the audit firm level is 0.316 (ΔSPELINK_audit firm) and the lead partner level is 0.007 (ΔSPELINK_lead

partner). The sample firms become less profitable as indicated by the negative mean and median values

of ΔROA. However, the positive mean and median values of ΔCURRENT, ΔQUICK, and ΔATURN suggest that the firms increase their liquidity and are more efficient in their operations. Regarding corporate governance indicators, we find that there is a decrease in director shareholdings, as indicated by the mean and median values of ΔDIR.

28

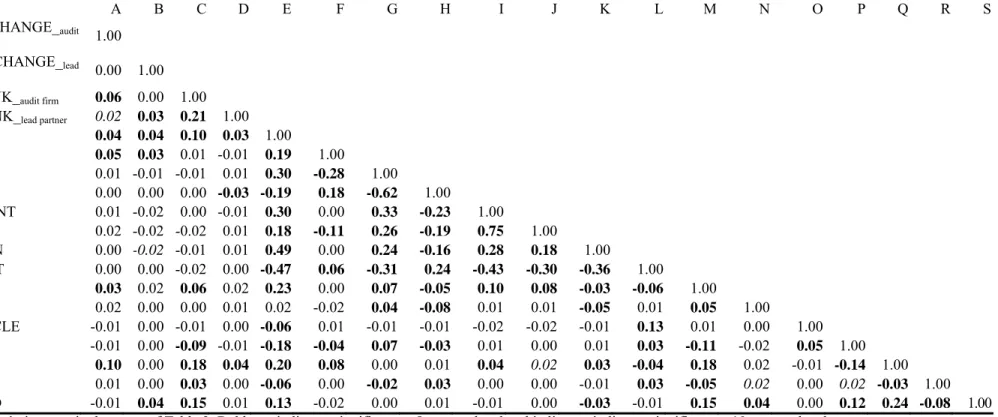

Table 3 reports the Pearson correlations between the main variables. The results indicate that the change in the number of interlocking directors connected to other firms that retain industry-specialist audit firms (ΔSPELINK_audit firm) is positively correlated with audit change at the

audit firm level (AUDITCHANGE_ audit firm). The change in the number of interlocking directors

connected to other firms that retain lead audit partners with industry expertise (ΔSPELINK_lead partner)

is also positively correlated with auditor changes at either the audit firm level (AUDITCHANGE_ audit

firm) or the lead partner level (AUDITCHANGE_ lead partner). These results of the univariate analyses

suggest that there is a spillover effect of industry-focused audit services arising from directors’ outside experience at both the audit firm and lead partner level. Among the control variables, we find that auditor changes to industry specialists either at the audit firm level or lead partner level are associated with greater company size and leverage. Of the corporate governance variables, we find that an increase in the proportion of independent directors on the board is associated with a greater likelihood of changing audit firms to industry specialists and an increase in board size is associated with a greater likelihood of changing lead partners to industry specialists.

[TABLE 3 ABOUT HERE]

4. Empirical results

29

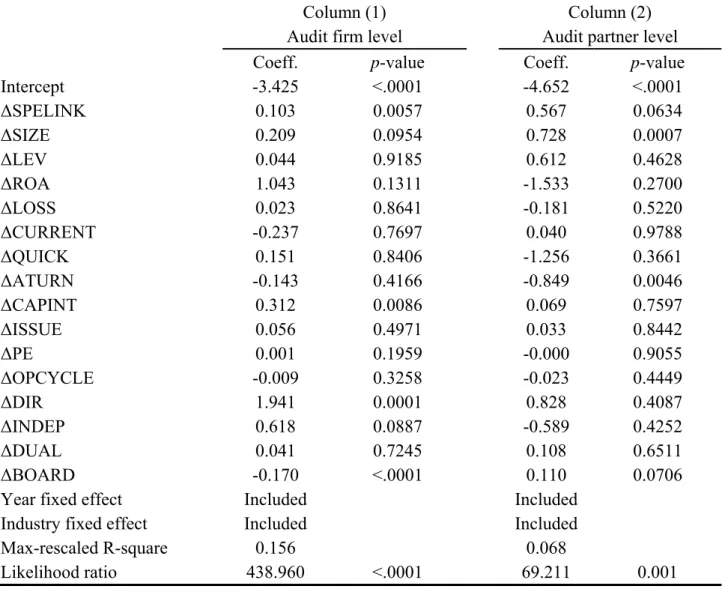

Table 4 reports the results regarding the relationship between interlocked boards and auditor change. In column (1), ΔSPELINK_audit firm captures the strength of the spillover effect of interlocking

directors on the switch to audit firms that are industry specialists. Its coefficient is significantly positive (0.103, p-value = 0.0057) after controlling for several firm-specific characteristics, corporate governance features, and year and industry fixed effects. This indicates that there is a greater tendency to switch to industry-specialist audit firms if there is an increase in number of directors at the focal firm who also serve on the boards of other companies that have acquired audit services provided by industry-specialist audit firms. Among the firm and corporate governance characteristics, the changes in CAPINT, DIR, and INDEP are positively associated with a change to audit firms with industry expertise, while the change in BOARD is negatively associated with auditor changes at the audit firm level. To provide further insights into the economic significance of the results, marginal probabilities are calculated for the likelihood of switching auditing firms to industry specialists when the control variables are set to their median values. The mean likelihood is 4.54 percent when the firm is linked through more interlocked boards to other firms that retain audit firms with industry expertise.

[TABLE 4 ABOUT HERE]

We further examine whether there is an association between auditor changes to a lead auditing partner who is an industry specialist and changes in interlocking directors who serve on the board of other firms that retain a lead partner who is an industry specialist. As mentioned in Section 3, we

30

consider the auditor with the longest tenure with the client to be the lead partner. If both auditors have the same tenure, we take both into account. SPELINK_lead partner is the number of directors’ links a

firm has with other firms that have retained a lead partner with industry expertise. The results in column (2) are generally consistent with those at the audit firm level, while the R-square is relatively lower (0.068). The coefficient of ΔSPELINK_lead partner is significantly positive (0.567, p-value =

0.0634). Looking at the control variables, we find that an increase in firm and board size is positively associated with the switch to audit partners who are industry specialists, while an increase in asset turnover is negatively associated with the likelihood of switching to a lead partner who is an industry expert. To gauge the economic magnitude of the results, we calculate the marginal probabilities of changing to a lead partner who is an industry specialist. The mean likelihood of switching to a lead partner who is an industry expert is 1.26 percent when the firm is linked through increased interlocking directors connected to other firms that retain a lead partner who is an industry specialist, representing a decrease of 3.28 percent compared to the corresponding likelihood at the audit firm level. Overall, the findings in Table 4 indicate that firms with directors who are connected to other firms that appoint auditors with industry expertise have a high propensity to switch to industry experts at the audit firm or lead partner level. Untabulated results using dummy indicators to capture interlocks with firms retaining industry expertise at the audit firm and lead partner levels are generally similar to our reported results.11

11 In our sample, we do not find any incidences of interlocking directors being previous partners of the appointed audit

31

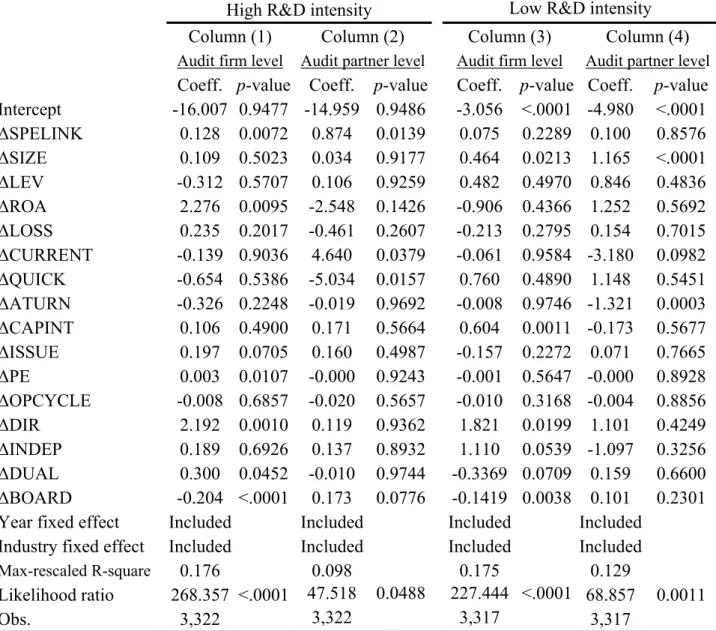

Prior studies indicate that companies with growing opportunities tend to have greater demand for a higher quality of audit services (e.g., Godfrey and Hamilton, 2005; Mascarenhas et al., 2010), and they are also more likely to acquire and utilize interlocking directors’ relevant experience (e.g., Diestre et al., 2015). Thus, the extent to which interlocking directors having an influence on the switch to industry-specialist auditors may depend on a firm’s growth opportunities. We run audit change regressions for firms with high R&D investments and firms with low R&D investments separately. Columns (1) and (2) of Table 5 report the results of high R&D intensity firms. The coefficient ΔSPELINK is positive and significant in the regression of audit change either at the audit level (0.128, p-value = 0.0072) or lead partner level (0.874, p-value = 0.0139). However, we do not find similar evidence in Columns (3) and (4) for firms with low R&D intensity. To assess the economic magnitude of the results among firms with high R&D investments, we again calculate the marginal probabilities of changing to industry-specialist auditors. In untabulated analyses, we find that the mean likelihood of switching to industry specialists is 4.41% at the audit firm level and 1.12% at the lead partner levels. Of the control variables, we find that for high R&D intensity firms, an increase in ROA, ISSUE, PE, DIR, and DUAL is positively associated with the likelihood of switching to industry specialist auditors at the audit firm level, while an increase in current ratio (CURRENT) and board size (BOARD) is positively associated with the change to industry specialist auditors at the lead partner level.

32

The findings in Tables 4 and 5 strongly confirm our conjecture that information regarding the potential benefits of industry-focused audit services will be transferred to other firms through shared directors. There is a greater spillover effect of such information when the focal firms face greater growth opportunities.

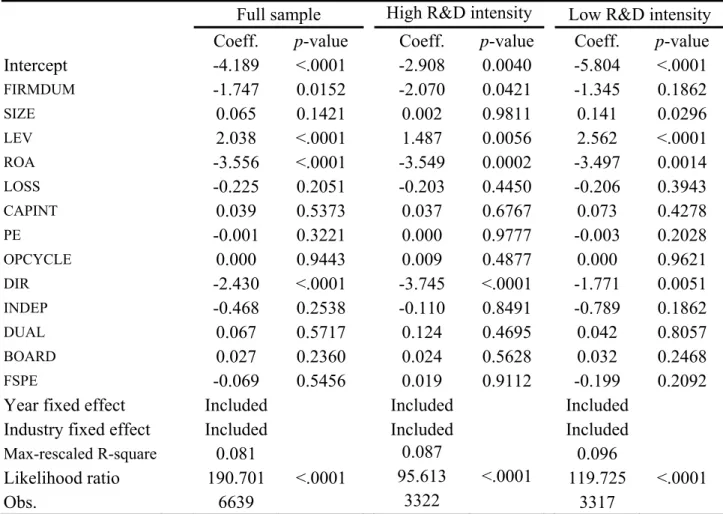

4.2 Audit quality

Table 6 reports the influence of interlocking directors and auditor changes on the focal company’s audit quality. Column (1) reports the findings of the full sample. We find that the coefficient of FIRMDUM is negative and significant (-1.747, p-value = 0.0152), indicating that firms that experience both an increase in interlocking directors’ connections to other firms that retain industry specialist auditors and a change in auditors to industry specialists in the past three years are less likely to restate their financial statements. Of the control variables, we find that more profitable firms and firms with greater director shareholdings are less likely to restate financial statements, while firm leverage is positively associated with the likelihood of restatements.

[TABLE 6 ABOUT HERE]

We further perform the audit quality analyses for high R&D investment and low R&D investment firms separately. Among high R&D-intensive firms, we find that those that experience an increase in interlocking directors’ links to industry-specialist auditors and a change of auditors from non-industry specialists to industry specialists are less likely to restate financial statements as

33

indicated by a significantly negative coefficient of FIRMDUM (-2.080, p-value = 0.0421). However, we do not find similar evidence among firms with low R&D investments.

Taken together, our findings suggest that directors’ outside experience with industry-specialist auditors not only results in the focal firm having the same preferences regarding audit services, but it also helps those directors to play a greater monitoring role over the financial reporting quality of the focal company. Moreover, the results support our conjecture that interlocked board members in firms with high growth opportunities carry more weight as an information source than they do in firms with low growth opportunities, as these firms are more likely to acquire and utilize directors’ experience (Diestre et al., 2015) and have a greater demand for industry-specialist auditors (Godfrey and Hamilton, 2005).

4.3 Further analyses

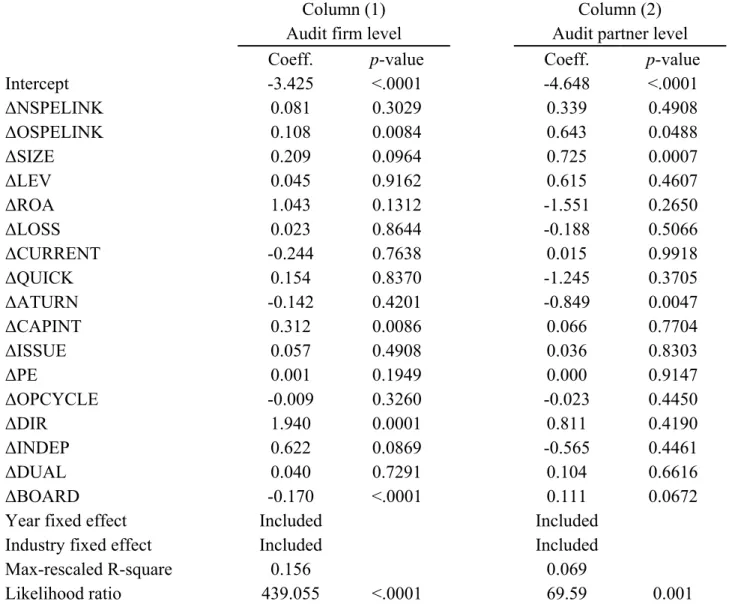

Interlocking directors’ depth of focal company experience

Prior studies have indicated that more experience at the focal company gives directors advantages in controlling the flow of information in the corporate decision-making process (Shropshire, 2010; Finkelstein, 1992). As such, interlocking directors’ knowledge of the focal company, gained through their tenure, may increase their ability to diffuse knowledge obtained from outside firms. Thus, we further examine whether the results in Table 4 are affected by the interlocking directors’ tenure with the focal company. Panel A of Table 7 reports the results of auditor changes at

34

the audit firm and lead partner levels of industry specialists. ISPEINK is the number of board links via directors who triggered SPELINK_audit firm or SPELINK_lead partner and have been with the focal

company for more than three years, while OSPELINK is the number of board links via directors who triggered SPELINK_audit firm or SPELINK_lead partner and have joined the focal firm in the last three

years.12 We find that the coefficient of ΔISPEINK is significantly positive both at the audit firm and at

the lead partner level (0.108, p-value = 0.0084; 0.643, p-value = 0.0488), while the coefficient of ΔOSPEINK is insignificant. These findings suggest that the results in Table 4 are mainly driven by longer-tenured directors with knowledge of industry-specialist auditors. This is as expected, since longer-tenured directors may enjoy greater power and positioning on the board relative to newly appointed directors, which could help facilitate the diffusion of practices from outside firms.

[TABLE 7 ABOUT HERE]

Different levels of directors’ connections

Prior studies show that the effect of auditor industry specialists on audit quality is driven by a combination of audit firm and partner expertise (Chin and Chi, 2009; Chi and Chin, 2011). Chin and Chi (2009) argue that signing partners who are industry specialists are likely to have the most essential and direct effect on audit quality, and find that the association between Big 4 industry expertise and the likelihood of accounting restatements is mainly driven by the partner-level industry

12 According to Company Act §195 in Taiwan, a single term of service must not exceed three years and directors may then

be re-elected. Thus, firms in Taiwan generally hold elections every three years to re-elect all directors unless there is an unexpected event that necessitates an interim election.

35

experts, in particular the signing auditors. In light of this prior evidence, we further investigate whether information transmission regarding auditors that are industry specialists differs depending on whether directors’ connections to other firms that retain industry specialist auditors is at the audit firm level only, the lead partner level only, or a combination of both, and perform the following logistic regression:

AUDITCHANGE α α BOTH α FIRMONLY α PARTNERONLY α ∆SIZE α ∆LEV α ∆ROA

α ∆LOSS α ∆CURRENT α ∆QUICK α ∆ATURN α ∆CAPINT α ∆ISSUE α ∆PE α ∆OPCYCLE α ∆DIR α ∆INDEP α ∆DUAL α ∆BOARD Year fixed effects Industry fixed effects ε 3

where BOTH is a dummy variable equal to one if there is both an increase in interlocking directors’ connections to other firms that retain industry specialists at the audit firm level and an increase in interlocking directors’ connections to other firms that retain industry specialists at the lead partner level, and zero otherwise. FIRMONLY is a dummy variable equal to one if there is an increase in the interlocking directors’ connection to other firms that retain industry specialists at the audit firm level only, and zero otherwise. PARTNERONLY is a dummy variable equal to one if there is an increase in the interlocking directors’ connection to other firms that retain industry specialists at the lead partner level only, and zero otherwise. Consistent with Equation (1), we allow for a three-year period to capture an actual change in both auditor and auditor industry specialization. We expect the

36

information transmission effect to be the strongest when the connections are at both the audit firm level and lead partner level.

Panel B of Table 7 shows the results of our regressions in which we compare different levels of interlocking directors’ connections. In Column (1), the coefficients of BOTH and FIRMONLY are positively significant. Untabulated analyses reveal that the coefficient of BOTH is significantly different from that of FIRMONLY (p-value = 0.099), indicating that firms with both increasing interlocking directors’ connections to other firms that retain industry specialists at the audit firm level and increasing interlocking directors’ connections at the partner level have the highest likelihood of changing audit firms to industry specialists compared to FIRMONLY. Column (2) shows the results of auditor change of the focal company at the lead partner level. The coefficients of BOTH and PARTNERONLY are positive and significant, while the difference between these two coefficients is insignificant. This suggests that the likelihood of a focal firm changing to industry-specialist auditors at the lead partner level is higher for firms when there is an increase in their interlocking directors being connected to other firms that retain industry-specialist auditors at the lead partner level only or an increase of connections at both the audit firm and partner levels. These results also imply that if a firm’s board is linked to a firm that appoints auditors who are industry experts, then it is inclined to have the same preference, i.e., industry-specialist auditors at the audit firm level or partner level.

37

Following the passing of Sarbanes-Oxley Act (SOX) in the US, which emphasizes the role of independent directors and the function of the audit committee in safeguarding the integrity of a firm’s financial reporting system, Taiwan also initiated a corporate board reform in the year 2002. The Taiwan Stock Exchange started to require all newly listed companies to have at least two independent directors. In addition, all listed companies were required to disclose information on their directors’ independence. The Securities and Exchange Act was revised in the year 2006, giving public companies the option to choose whether to have independent directors and whether to establish audit committees.13 According to the Regulations Governing the Appointment of Independent Directors

and Compliance Matters for Public Companies, independent directors must have at least five years of work experience and have a commerce, law, accounting, or finance background related to the business needs of the company. According to the Securities and Exchange Act in Taiwan, all independent directors are members of the audit committee. The total number of audit committee members should not be less than three, and at least one of them must have an accounting or finance background.

Prior research indicates that audit committees can potentially take actions related to the external auditor that may result in a higher level of audit assurance or coverage (Abbott et al., 2003; Abbott and Parker, 2000). For instance, audit committee members can persuade management to select a more knowledgeable auditor with a greater reputation and demand a greater quantity of audit effort

13 Since the year 2006, the Financial Supervisory Commission required all public financial companies and non-financial

listed companies with shareholders’ equity greater than NT$50 billion to have at least two independent directors, with the total number of independent directors making up no less than one-fifth of the total number of board members.

38

from the incumbent external auditor (Simunic and Stein, 1996). In contrast to the situation in the US, audit committees are not that pervasive in Taiwan. Among our sample firms, we find that firms established audit committees since the year 2007, and we only find 30 companies with audit committees during the period 2007-2009. Due to the small number of firms with audit committees, we perform tests based on the number of links connected via independent directors instead. The duties of independent directors include monitoring the internal audit process and the retention or dismissal of external auditors and accounting, auditing, and financial officers. Therefore, following the extensive corporate governance reform in Taiwan, we would expect independent directors to take a more proactive role in audit-related decisions. Based on Equation (1), we measure ΔSPELINK_independent directors as the change in the number of interlocking independent directors that the

focal firm has with other firms that retain auditors who are industry specialists and run the analyses for the period 2007-2009. Untabulated results show that the coefficient of ΔSPELINK_independent

directors is significantly positive at the audit firm level (0.145, p-value = 0.0616), indicating that an

increase in the number of interlocking independent directors could increase the likelihood of the focal firm changing its audit firm to an industry specialist.

Audit fees

We further investigate whether companies pay a premium or enjoy a discount in audit fees to their new auditors in the presence of interlocking directors. Prior studies suggest that, when a client

39

voluntarily switches auditors, it initially enjoys lower audit fees because non-incumbent auditors will “low-ball” or discount the initial audit engagement to earn the right to future fee premiums (DeAngelo, 1981). As auditors’ incentives to charge a premium or to pass on scale economies is likely to depend on their relative bargaining power with the client (Mayhew and Wilkins, 2003; Casterella et al., 2004), we expect that directors with experience appointing industry specialists could enhance the focal firm’s bargaining power, and thus moderate the effects of industry specialization on the audit fee premium. Companies in Taiwan are not required to disclose audit fees unless they meet one of the following three criteria stipulated in the Regulations Governing Information to be Published in Annual Reports of Public Companies. First, companies must disclose both audit and non-audit fees and also the items of non-audit services if the non-audit fees are higher than one quarter of the audit fees. Second, if a change in audit firm results in lower audit fees, companies should disclose the audit fees in the year before and the year after the change and provide the reasons for the change. Third, companies should disclose the change in audit fees in dollars and in percentage terms, and provide the reasons, if there is a decrease in audit fees and the reduction is greater than 15%. Despite this, we find that there is a trend of increasing disclosure of audit fees on a voluntary basis. The sample we use to examine the relation between interlocking directors and audit fee is reduced to 1,809 observations, and we find that around 52% of the observations are voluntary disclosures.14 The audit fee model is as follows:

14 From the year 2009, companies have been able to choose whether to disclose audit fees as a specific amount or in an