The Impact of Share Holding and Ability of

Managers on the Firm Value of State-Owned

Enterprises in China- An Application of Financial

Agency Theory

Szu-Lang Liao

National Chengchi University

Jimmy Y.T. Tsay

National Taiwan University

Ming-Lei Chang

Chung Kuo Institute of Technology

Abstract

This study aims to investigate the corruption and collusion problems occurring in the reforms of state-owned enterprises in China, and to analyze how this problem affects the performance of state firms. Using the idea of principal-supervisor-agent relationships, we analyze the decay of officials control over state-owned enterprises resulting from the change that employees, managers and the public are now allowed to hold shares of state-owned enterprises, and they can claim the residual rights of the enterprises. From our analysis, the corruption and collusion between officials and managers may not become less serious. The performances of state-owned enterprises will not be improved even after the introduction of the shareholder system. We use a game-theoretical model involving public, government officials and enterprise managers, focusing on political considerations to study the effect of ownership structure of state-owned enterprises.

Keywords: agency relationship, state-owned enterprise, shareholding, compensation

Introduction

Reforms of state-owned enterprises in China began in 1978 and have proceeded through several stages. Thefirststagewastheperiod of“releasing powerpolicy” from 1978 to 1986, which included enlargement of the power of the managers and connecting the profit of enterprises with the payment of the managers and the employees. Thesecond stagewasthe“contractsystem”from 1987 to 1992,which continued the releasing power policy and extended more control to the managers and the employees. In this period, the government asked for a certain amount of profit to be returned and left the operational strategies to enterprise managers. The third stage,which began in 1993 and continuestoday,isthe“firm and shareholdersystem”, which tries to make distinct relations between the government and the enterprises. Looking into these reforms, we can find that most of the reforms are related to the releasing in personnel matters, asset management and allocation of profits.

In all of these phases, the government actually controls the management of the enterprises, and the enterprises therefore bear some additional responsibilities, including redundant employees and social welfare of the employees. Even after the reforms of the shareholder system, it is still hard to eliminate these problems. A survey of 34 million local enterprises in 1994 showed that over 16.9 thousand schools and 3,619 medical agencies are managed under these enterprises. Their annual expenses reached 1.5 billion RMB for education, 2 billion RMB for medical care, 17 billion RMB for retirement benefits and 5 billion RMB for housing.1 Furthermore, from 1988 to 1994, the nation-wide fees, including welfare, retirement, severance pay and subsidies, increased at the rate of 16.9%, and the cost of per employee increased from 40.1 RMB to 356.2 RMB. From 1980 to 1994, the retirement and medical expenses were 26.4% higher than the cost of wages. In 1994, the retirement and medical expenses reached 164.62 billion RMB, which was 31.8% of the total amount of the wages. Although 20% of all employees have lost their jobs for the past six years, there are still 20% of unnecessary workers in state-owned enterprises (Huang and Yang, 1999). According to Lian (1999) estimation, one-third of all workers, i.e. 20 million workers, would have to leave

1

their jobs in order to solve the problem of redundant employees.

This research analyzes the problems of corruption and collusion between the government officials who monitor and control the stated-owned enterprises and the managers of stated-owned enterprises. We continue the research in Shleifer and Vishny (1993, 1994), and focus on political consideration to study the reforms of the stated-owned enterprises in China subject to political influences. We set up a game-theoretical model between the public, the political officials, and the enterprise managers. The model is built under two basic assumptions. First, because the public is disorganized, the supervisors (government officials) gather into interest groups and become an internal corruption chain. Second, we assume that the relation between the government officials and managers is governed by incomplete contracts, so that the residual rights of control rather than incentive contracts become the critical determinant of resource allocation (Grossman and Hart, 1986). Under these assumptions we derive implications of bargaining between government officials and enterprise managers on the enterprises’ activities. In particular, we focus on the transfer between the bureaucratic sector and stated-owned enterprise sector.

This research attempts to associate the changing process of the state-owned enterprises’ownership with theircorruption and performance. Therefore,itextends the studies of Andvig and Moene (1990) and Shleifer and Vishny (1993, 1994) with the consideration on internal bribery (Basu et al. (1992) and Bac (1998)) based on the assumption of incomplete contract (Grossman and Hart 1986). It also redefines the gross and net transfer payments under the consideration of the subsidy characteristics in China. Moreover, the significance of official rank, the proportions of the shareholding by managers and others (i.e. non-government shareholders) are discussed here, and some adjustments of the officials and manager utility function are made to fit the current types of state-owned enterprises under socialism in China.

The conclusions of this research are distinct from those of Shleifer and Vishny (1994), who concluded that the government transferred expenditure, T, and the number of redundant empolyees, L, are irrelevant to the shares held by managers. In contrast, after revising transfer expenditure, adjusting the utilities of officials and

managers, and adding the shares held by non-government holders, this research concludes that the percentage of shares held by managers and employees affects the number of redundant employees. It also concludes that the percentage of shares held by non-government and non-managers holders and that held by managers affect how much subsidies a corporation can win from government. To be specific, in our model, increasingα, which is the shares of institutional and individual investors, is helpfulto reduceofficials’influenceson companies. Although thiscould possibly cause a reduction of subsidies from the government, the extra social responsibilities would be decreased, and the inefficient policies demanded by officials could be avoided. Managers have to input more effort to win the trust of small investors with the increases of α. In addition, because corporation stocks are not tradable on the market but can be transferred through negotiation, investors would prefer long-term investment and be more capable to influence the operation of companies via shareholders’assemblies.

Asfortherelationship between bribery amountand managers’sharepercentage, Shleifer and Vishny (1994) concluded that under control by politician, the equilibrium of bribery is increasing in α; whereas under manager control, the equilibrium bribe is independent of α. In this research, however, the amount of bribery from managers to officials depends upon the corporate earnings because the utility functions of manager and officials are adjusted. This research proves that, under official control, in more profitable state-owned enterprises, the degree of corruption will increase according to the proportion of shares held by managers. Under manager control, in a deficit state firm, the amount of bribery has a positive relation with the shares of the managers.

Following the introduction and literature review, Section Three presents models and focuses on the government officials’ control over personnel matters and the resulting corruption. In this section, it is assumed that officials have the right to assign the managers. Thus, the managers hope to have the right to hire the employees or to reduce the number of employees, it is necessary to bribe the officials. Section Four discusses the competition for the power among different managers of the enterprises before they are assigned. The last section presents conclusions and limitations of the study.

Literature Review

Corruption is a complex and multidimensional phenomenon. Formal studies of corruption are built on two theoretical grounds, one is the economics of crime and law enforcement and the other is the principal-agent relationship. Becker (1968) claimed that the incentive to engage in a crime depends on the expected rewards, explaining that since crime is inherently risky, the probability of being caught and convicted would affect the incentive for engaging in illegal behavior. His study has important contribution in the economics of crime and punishment. Krueger (1974) discussed the rent-seeking problem from economic point of view. Becker and Stigler (1974) were the first to introduce a principal-agent model of corruption. Banfield (1975) and Rose-Ackerman (1975) have further extended that analysis. The major development in the second body of theory is the extension of the classic principal-agent framework to include principal-supervisor-agent relationships, as proposed by Tirole (1986) and Laffont (1990). The new principal-supervisor-agent theory has stimulated many papers exploring various aspects of private organizations, with possible collusion among the members. However, the existing models of private organizations in previous studies shed little light on the collusion and corruption problems in the state-owned enterprises, due to the complexities stemming from the bureaucratic politicians who control them.

Lui (1986) and Cadot (1987) both discussed bribery in public organizations. Lui (1986) provided how multiple equilibriums can arise when the effectiveness of repression is inversely related to the prevalence of corruption. Cadot (1987) set up a simple game in which players are either a government official or a candidate, and the government official grants the candidate permission conditional on a test. This model analyzes the bureaucratic corruption under different assumptions about the information setsofplayers. However,Cadot’smodelofasymmetricinformation refersonly to thecandidate’sinformation on hisown type,and neitherofthesetwo papers considers the problem of internal corruption. Basu et al. (1992) and Bac (1998) considered the possibility of internal bribery. Bac defines external corruption as an individual, isolated act of corruption that occurs in the transaction

between the client and the street-level bureaucrat. Typical examples are extortion and bribery. On the other hand, internal corruption is a form of collusion transforming the organization into an internal market of systematized sharing of proceeds from corruption. In this paper, we adopt Bac’s idea about internal corruption in order to discuss how government officials accept bribes when there were changes in the ownership pattern of stated-owned enterprises in China. Other articles discussing corruption such as Andvig and Moene (1990) and Shleifer and Vishny (1993) presented various models of bribery focusing on the ownership or organizational arrangement as a determinant of corruption. These models explain how similar structures can create different levels of corruption.

Shleifer and Vishny (1994) are similar to our analysis in that they consider the bargaining between politicians and managers and explain many general typical facts about the behavior of state firms. We apply their idea to the model in this paper, which considers the ranking of officials, the proportion of the shareholding by managers, making some adjustments to fit the socialist system of stated-owned enterprises in China.

The model in this research mainly uses the concept in Shliefer and Vishny (1994), regarding the behavior of managers and politicians towards the state firms, their commercialization and privatization. Shliefer and Vishny proposed explanations for many facts about the subsidies to state-owned enterprises and bribes from managers to politicians. In the process of reforming state-owned enterprises in China, the primary ownership has been shifted from government officials to stockholders of enterprises, and this model of Shliefer and Vishny also concerns the above problem. However, they build the model in a democratic environment, so that politicians must cater to interest groups such as labor unions, rather than to average median voters. In contrast, because state-owned enterprises in China are built and operated under principles of socialism, so this research redefines the gross and net transfer payment under the consideration of the subsidy characteristics of China. In addition, we also discuss the significance of official rank, the proportions of the shareholding by managers and others (i.e. non-government shareholders), and we make some adjustment of the officials and manager utility function to fit the type of state-owned enterprises under socialism in China.

Redundant Employees, Subsidies and the Corruption

1. Basic Model

We present a game-theoretical model between the public, the political officials, and the enterprise managers. These models are built under three basic assumptions. First, because the public is disorganized, the government officials gather into interest groups and become an internal corruption chain. Second, we assume that the relation between the government officials and managers is governed by incomplete contracts, so that the residual rights of control rather than incentive contracts become the critical determinant of resource allocation (Grossman and Hart, 1986). Third, we avoid the discussion of bankruptcy in state-owned enterprises. According to surveys conducted by Wang (2001) on state-owned enterprises in 31 different industries from 1980 to 2001, the number of samples dropped from 769 in the first survey to 681 in the second one. In this period, 13 out of the 88 sampled state-owned enterprises went bankruptcy, 27 were transformed to cooperative share-holding company, 41 were merged and 7 were unaccounted for. In their survey of 2000, another 239 sampled state-owned enterprises disappeared from the sample of 681 in the second survey. The corporations that disappeared can be divided into three categories: one is those which were merged into other state-owned enterprises, privatized enterprises and liquidated. Privatization includes those firms sold to private corporations (generally to high-level managers of enterprises), merging into village corporations, and being taken over by foreign corporations or transformed into stock corporations.2 State-owned enterprises that were bankrupt or liquidated are excluded from this model, but those that are privatized are included because this research focuses on how officials and managers re-allocate and negotiate the personnel and profit allocation powers with the reform of state-owned enterprises. By discussing and measuring the variables of redundant employees, we can observe

2

The survey were divided into three periods, the first period is 1980-1987, including 769 samples; the second period was 1990-1994, including 681 samples; and the third period was 2000-2001, including 442 samples.

the change of the performance of state-owned enterprises with the lessening control of officials on enterprises managers.

Under these assumptions we derive the implications of bargaining between government officials and enterprise managers on the enterprises’ activities. In particular, we focus on the role of transfer between the bureaucratic sector and stated-owned enterprise sector, and the performance of state-owned enterprises during the reforms. An alternative approach to these issues is to focus on asymmetric information and incentive contract. These areas have been pursued by Laffont and Tirole (1993).

Most literature on the relationship between ownership and performance shows that the agency relationship in a private company, composed of principal and many small shareholders, is economically efficient. (Holderness et al. 1999), but even under the reform of ownership structure, state-owned enterprises’multi-level agency relationship is still quite different from that of private companies. First of all, the principal of state-owned enterprises is that all the citizens of China are supposed to share the residual rights. Thus, the number of owners is too large for them to run or supervise state-owned enterprises directly; so they have to entrust the company to delegates (upper agents). The delegates, then, entrust the company to superintendents in the central government, and they finally entrust its management and supervision to local governments. In brief, the state-owned enterprises are run through five levels of trusteeship: the entire people –National Assembly –State Council –state-owned enterprises superintendent –board of directors –managers. It is the upper level agents, rather than direct elections, that decide the key agents in the first-level system from the initial consignors to agents in central government; as a consequence, the agents in the system have more authority, making the agency relationship a reverse one. In other words, the agents at one level, to a greater extent, are giving services to the higher authorities rather than to upper-level agents.

If we roughly define persons from the level of initial principal to that of agents in central government as the principal level, and the agents from central government to ultimate agents as the controlling level; it is clear that the persons who have real influence on the performances of state-owned enterprises are those from the level of central government agents to that of the ultimate agent, and that those who can

actually dominate over the reform of state-owned enterprises are officials from both central and local governments. The principal and the levels they represent do not, in reality, possess residual rights according to the law and the voting right as the only way of supervision lacks an effective monitoring mechanism. The model in this research focuses on the analysis of the influence of the relationship between officials and managers on the performance of state-owned enterprises when the personnel power and power to allocate profits of state-owned enterprises change.

According to a document of the 15thParty National Assembly, “Theremustbe delegatesofemployeesin theboard ofdirectorsand board ofsuperintendents… … in state-invested and stock holding state-owned corporations.”. Therearesimilar regulations in the Corporation Act and related documents. This information indicates two aspects. For one, it is the CCP that sets up major directions for the reform of state-owned enterprises; it is the decisions and declarations of policy that lead and dictate this socialist country, and there is actually CCP involvement in state-owned enterprises. The other aspect is that the employees and the labor unionsplay very crucialroles. PresidentJiang Jemin oncepointed outthat“We mustfully rely on theworkersand respecttheirposition asmaster… … laborunion and workers assembly’s functions of democratic decision-making, managing and supervisormustbebroughtinto fullplay.” Itisthusperceived thattheimportance of workers in a state-owned corporation is evident, although their actual role in the boards of directors or superintendents is limited. The dilemma of state-owned enterprises’socialburden appearseven moredifficultto solve,becausetheproblem of redundant employees is based on those workers and labor unions.

In the management framework of the stated-owned enterprises in China, the government officials and managers actually have the influence on the operational decisions of the state-owned enterprises. The government officials play two differentroles,thefirstisasthepeople’sagent. ThepeopleofChina empower the central government officials to manage the assets of the enterprises, and the government officials authorize subordinate departmental officials take different responsibilities in controlling the state-owned enterprises. Through this authorization process, some government officials become the agents of higher officials; and they again empower some control rights to the managers of the

state-owned enterprises. In some aspects, the government officials are the agents of the people, but the government officials play the principal or supervisor role in executing the management policy of state-owned enterprises.

In discussing the relationship between the corruption and ownership structure in the state-owned enterprises under the principal-supervisor-agent relationship, we concentrate on the behavior of the government officials and the enterprise managers in the issue of redundant employees. Here the characteristics of the government officials are defined in the position of a supervisor. They control and manage the state firms directly, and they have the right to assign the enterprises’ managers, monitor the performance of managers. The people of China (the real principal) are too fragmentary to gather together and present or protect their own benefits.

We begin with a simple model to analyze political officials’ influence on enterprises. There are two players, the government official and the manager of the stated-owned enterprise, and both are risk neutral. These two participants bargain over the decision of the enterprises. In this model, we do not discuss the agency problem between the manager and the non-state shareholders of firm by assuming that managers serve their own interests.

Government officials, as we discussed above, ask the state-owned enterprises to take the responsibility to absorb more employees than they actually need to function. This can solve the serious problem of unemployment caused from the large-scale development of heavy industry. Since a low rate of unemployment is used to indicate good performance of government officials, we assume that the officials can obtain political benefit from redundant or unneeded employment L with a dollar value of B(L), where L denotes the excess employment of the enterprise, the employees in excess of those needed to efficiently produce its output. We assume that these redundant employees produce nothing, but the enterprise pays each of these employee wage, denoted as w. Presumably, w exceeds the (effort-adjusted) average market wage.

The officials demand the enterprise to employ as much as possible labor L, since they derive political benefits B(L) and thus the officials will offer subsidies to the enterprise. To improve their performance rating, the officials use the subsidies as a means of exchange. Officials hope that by means of transfer payment the state

firms will be willing to hire more redundant employees, and try to make up the earnings deficiency caused by the unneeded wage burden.

The state-owned enterprises are subordinate to the central or local governments, and all the profits of the enterprises are the public financial resources. Even under thepracticeof“tax forprofit”and “shareholding system”, the government can get income by taxes and share a large percentage of the earnings after tax. Whether the earnings of state firms are deficient (negative) or not, the government official has the power to subsidize the enterprises, while the amount of subsidy depends on some economic policy or the relation between theenterprises’managersand theofficials. Here we define the subsidies as being not only direct monetary payments, but also offering zero-rate or lower rate cost of capital, free land or factories, and lower prices for the input materials.

In the negotiation process between the officials and the enterprises managers about the amount of subsidies and the number of redundant employees, we consider the rank of the officials to be an important factor, since higher rank officials can obtain more subsidies with less cost. The cost of net transfer would be affected by the power of the individual officials. So the net subsidy, denoted as T, is not costless to the government officials, who must persuade the higher rank officials of the Ministry of Finance, the Central Bank, the Administration Bureau of state Property or other related government departments. We assume that the cost to the officials of making the net transfer T is C(T).

Theofficial’sutility (measured in monetary unit)can berepresented by

b U: ) ( ) ( ) (L g p C T B Ub (1) where

L :number of redundant employees

B(L):official’sderived politicalbenefitfrom excessemployment P :rank of the government official

T :net transfer payment (net subsidy) g(p) :influence of rank on cost

C (T):cost paid for the net transfer

Assume that B'(L)0, and B''(L)0. P denotes the government official’s rank, p〔0 , 1〕. The higher the rank, the bigger p is; and assume that

1

)

(

0

p

g

and g'(p)0. The political cost to the government official of making the net transfer T is Cb(T). Assume that Cb(T) is influenced by the rank of the official, and Cb(T)=g(p)C(T), where C'(T)0,C''(T)0。The net subsidy would help the state-owned enterprises somehow, and this will improvetheenterprises’profitability. Butthenettransferand thegrosstransferare different, since gross transfer payment is taken back through taxation or surplus sharing. So in this model, we put the tax rate and the state sharing percentage in order to clarify the relation between net and gross subsidies. The primary factor affecting the utilities of officials and the managers is the net transfer payment.

The net transfer T can be further rewritten as:

T =t-〔(1–α–β)(1–i) +i〕〔π+t-wL〕 (2)

where

T : net transfer payment t : gross transfer payment

α : proportion of the non-state and the non- manager’sshares β : proportion of the share that the manager holds or the profit shared

1–α–β: proportion of profit shared by the state L : number of redundant employees

w : wage

i : tax rate

π : net profit before tax under optimal employment

Since π is the net profit before taxation, we assume that π is the maximum profit under the optimal employment. In equation (2), assume that ,

0,1,

1

represents the government’sshared proportion ofeithertheprofitsor the government shareholding. When

0

, the enterprise is owned by the state. Ifα+β=1, then the enterprise is owned by the private sector. In addition, i represents the tax rate, which is zero before the “tax for profit” policy. The enterprise is allowed to reserve a proportion β, and the remaining profit must be returned to the government. Butwith thepracticeof“tax forprofit”policy,the government subsidy was partially returned from the tax. Since the government holds

1

, if α﹦0, β﹦0 and i﹦0, the government has the full right of the enterprise, and the revenue was totally returned, so T﹦wL–π. The net transfer payment is the profit from the enterprise minus the redundant employee wage burden. It is reasonable that when a state firm hires more unneeded employees will obtain more net subsidy, no matter how the net profit (under optimal employment) is. If the enterprise is fully private, then α+β=1. Furthermore, if i >0, then T﹦t–i (π+t–wL), which is the gross transfer minus the tax from the enterprise. Under the existence of taxation, we assume that the different forms of transfer will increase the net profit before tax. In addition, wL are the wages paid to the redundant employees, and under this assumption, w

w

,w

is the average wage in the labor market.Theutility ofenterprise’smanagerisgiven by afixed salary,denoted asA,and his share of the net profit after tax. No matter what the ownership structure is under the“powerreleasing policy”,“contractsystem”or“shareholdersystem ”,weassume that the managers have β proportion of the net profit. When managers have no equity under“powerreleasing policy”,“contractsystem”or“shareholdersystem ”, in more profitable firms they can still divert resources such as cars or housing for personal consumption. A more profitable state firm means that the manager has good performance and can more easily obtain personal benefit from promotions, control more resources and have more negotiation power. So managers still care about profits. However, we cannot ignore the situation where someone takes the position of manager and finds the enterprise facing serious deficits. In this case, the manager can still get a positive fixed wage, so we assume that A is positive.

Themanager’sutility function (measured in monetary unit) is given by

m

U

:m

where

π : net profit before tax under the optimal employment

A : the fixed wage of the manager β : share of the manager

i : tax rate

Because β is the proportion of shares of the manager, β would be the percentage that the manager gains from the net profit of the enterprise. Without loss of substantive generality, we restrict attention to the case where β>0. This includes not only the managers holding shares but also considers the extent to which the manager gains from the net profit of the enterprise.

From thegovernmentofficial’sstandpoint,theenterprisesabsorb the redundant employees and take social responsibility, thus increasing his own benefit. If the enterprise is willing to absorb more redundant employees, then the government official will be more willing to seek more subsidies. But from the manager’s position, to hire unneeded employees causes the enterprise bear more wage burden and lower the net profit. Therefore, the official and the manager bargain over L and T. In the next section, we allow a situation where the manager and official bribe each other, and when bribes cannot be offered, b is set to zero. We will examine a Nash bargaining game between the official and manager with their utilities, where the bribery amount is denoted by b. Since managers pay the bribes out of their own pocket, the cost of bribe b is exactly b. There are many forms of corruption, for example, monetary payment or sharing common interest both in politics and operation. The bribe b could be larger or smaller than zero, and b>0 indicates that the manager pays a bribe to the official, whereas b<0 indicates the converse.

In equations (2) and (3),α and β describethesharepercentage(theownership) oftheenterprise’snetprofit,and weassumethatthegovernmentofficialownsthe control right over T, but that L can be controlled either by the official or the manager. The control right over L determines the threat points in the negotiation process. Under a planned economy, the control right over L belongs to the official and the statetakesallthenetprofitasthepublicfinancialrevenue(α iszero and β iscloseto zero). Under the practice of some reform policies, such as the power releasing

policy or the contract system, the manager has some personnel rights, but the officialsstillhold thelargerpartofL. Themanagercaresabouttheenterprise’snet profit since he can gain somebenefitfrom theprofit(α iszero and β ispositive). After adopting the shareholder system, the control rights over L are apparently shifted from the officials to the manager, so the officials, representatives of the state share, still can influence the manager to hire more employees (through regulation of L or offering management positions). The ownership of net profit belongs to the managerand theshareholder(α and β arepositive).

2. Behavior of the Manager and Government Officials without

Corruption

(1) The Government Officials Decides the Level of Redundant Employees

In the first stage, considering that the corruption does not exist, and b=0, we compute the allocation of T and L before bribes. At this stage the government official decides the level of L, and the manager can only accept it. The purpose is to find out what T and L allocate without bribery under the centrally planned economy or under the power-releasing policy. These allocations decide the threat points for the government official control structure. When the government official has the control rights over both T and L, he chooses L and T by solving the following problem. To concentrate the analysis on subsidies and redundant employees, we exclude the discussion of tax rate and set i=0.

)

(

)

(

)

(

,B

L

g

p

C

T

Max

T L

(4) s.t.A

(

t

wL

)U (5)Themaximization oftheofficial’sutility would faceaproblem,which isunder a constraint that the manager will be kept to his reservation utility of U . If U is higher, the manager’sability israted higher.

Assume that the equations (4) and (5) both have maximizing solutions, we can get the first order condition as follows:

W L B'( )

T=(α+β)〔 U - A - 〕+WL (7)

In view of equation (6), the most appropriate level for L is decided by the marginal utility per dollar that the redundant employee brings. This is equal to the cost of subsidy per unit multiplied by the proportion of the non-state and manager share holding. When government official has control rights over L, he will try as much as possible to keep the firm down to zero net profit, and use the cash flow of the enterprise to hire extra labor until the political benefit of doing so exactly offsets the marginal political cost of getting extra transfer.

(2) The Manager Decides the Level of Redundant Employees

If the government official has no influence on the manager’s decisions, the manager has the control right over the redundant employees. At this stage, the outcome is determined by the Nash equilibrium in which the manager and the officials choose L and T with no cooperation. The manager will maximize his own utility in deciding L, as shown in equation (8). Equation (9) can obtain the transfer T chosen by the government officials.

L= argmax A+β(π+t-WL) (8)

T= argmax B(L)-g(p) C(T) (9)

However, in equations (8) and (9), when the manager is not controlled by the official, and

0

, the best choice for manager is such that L=0. As for the manager, more subsidies can increase his utility. But the official will not spend the subsidies on an enterprise which does not want to take social responsibility, so the best choice for T is T=0. Unless the government official and the manager have the coordination or the factor of corruption b, and try to share the benefits, the result would be no cooperation between the manager and the official, this means no subsidies and no redundant employees. In this case, the Nash equilibrium is L=0, T=0.(3) Cooperation between the manager and the official

Here we consider the case where the government official and the manager cooperate and trust each other. Under this cooperative situation, we assume that the

monetary utility of the manager and the official can be completely transferred by this cooperative relation. Either the increase in subsidies or the increase in the redundant employees could make the joint utility increase. With full transferable utilities, the cooperation between the manager and the official will solve the following combined utilities of government official and manager:

)

(

)

(

)

(

)

(

,B

L

g

p

C

T

A

t

wL

Max

T L

(10)Solving the above equation yields the following first-order conditions: W L B'( ) (11)

)

(

)

(

p

C

'T

g

(12)Underthecooperativesituation,thegovernmentofficials’gain from oneunitof the redundant employee would be equal to the unneeded wage cost to the manager, themanager’sgain from one-dollar transfer payment would be equal to the official’s cost for the subsidy. The unneeded employment and transfer decision are completely separable. Analyzing equation (11) , we can find that under α﹦0 (total shares belong to the state, during the period of centrally planned economy), or

0

(shares include non-state owners), the number of suitable redundant employees is the official’smarginal benefit,and isequalto themanager’s share for the wage burden cost. This means that the manager and the official raise the number of redundant employees to the point where the marginal political benefit of an extra employee is equal to the marginal cost, which is his wage. Equation (12) tells us that under the case whereαis equal or close to zero, the official and manager will draw the cash out of the public financial expense until the marginal cost of getting an extra dollar is exactly equal to one dollar.3. Bargaining with Corruption between the Manager and the

Government Official

This section considers a case where corruption exists between the official and manager, so we introduce the factor b, representing the bribery amount. To push the manger to absorb more L, the officials will use transfer payment as compensation.

The managers will try to ask the officials to subsidize and decrease the extra labor the enterprise has to hire. So the official and the manager will bargain with L and T. This corruption problem is very serious between the state-owned enterprises managers and the officials.

There are many forms of corruption. It could be money payment or sharing interest in politics and business operation. So we assume the bribe b are not only the monetary form but also the non-financial benefit. Because the officials, supervisors,monitorand reportthemanagers’performance,they can decidewhich firms should practice shareholder system or merger, and which managers should get promotions. On the other hand, the officials control many resources that will allow the manager to reduce operating cost or increase market share. Since managers pay the bribes out of their own pockets, the cost of bribe b is exactly b. The bribe b could be larger or smaller than zero, and b>0 indicates that the manager pays a bribe to the official, whereas b<0 indicates the converse. When there is corruption, the utility of the official is

b

T

C

p

g

L

B

U

b

(

)

(

)

(

)

and the utility of the manager is

b

wL

t

A

U

m

(

)

To compute the equilibrium when the government official and the manager are allowed to bribeeach other,weexaminetwo differentcasesofgovernmentofficials’ controloverL and themanagers’controloverL.

(1) The Government Official Controls L

From equations (6) and (7), the optimal solutions of L and T indicate the most appropriate number of employees and subsidies when the control right belongs to the official. The optimal redundant employees and subsidies in equations (6) and (7) are denoted as L* and *

T , under these choices, the utilities of the government official and the manager will be *

(

*,

*)

T

L

CE

b and * * *)

,

(

L

T

U

CE

m

, respectively. The incremental utility of the government official from bargaining is given by )] ( ) ( ) ( [ ) ( ) ( ) (L g p C T b B L* g p C T* B (13)and the incremental utility of manager from bargaining is given by

*

)

(

t

WL

b

U

A

(14)The Nash bargaining solution is to maximize the product of (13) and (14) over L, T and b, as in equation (15):

*

* * , , ) ( ) ( ) ( ) ( ) ( ) ( ) ( U b WL t A T C p g L B b T C p g L B Max b T L (15)The first order conditions of equation (15) are :

(

)

(

)

(

)

(

)

(

)

(

)

U

)

(

* * *T

C

p

g

L

B

b

T

C

p

g

L

B

W

b

WL

t

A

L

B

(16)

( ) ( ) ( ) ( ) ( ) ( )

) ( ) ( * * * T C p g L B b T C p g L B U b WL t A T C p g (17) ) ( ) ( ) ( ) ( ) ( ) ( ) ( * * * T C p g L B b T C p g L B U b WL t A

(18)

( ) ( ) ( ) ( ) ( ) ( ) ( )

2 1 ~ A t WL U* BL g pCT B L* g pCT* b (19)Equation (19) shows that the optimal b~ is the manager and government official split the gains from resources. If we substitute the equilibrium b~ into equation (16) and (17), then

w L B )( (20) )( ) (p C T g (21)

Under bargaining, if the government official and the manager share the gains of transaction, then we can get equations (20) and (21), which are equal to the optimal

choices of L and T in equations (11) and (12). The redundant employment and transfer decision are completely separable. Under the allowance of bribes, the decisions on L and T are governed by the combined utilities of the official and the manager to maximize the resources under their cooperative control. Thus under this case, α is equal or close to zero, which will make the official and manager draw cash out of the public financial expenses until the marginal official cost of the last dollar is equal to one dollar, and employ extra labor until the marginal political benefit is equal to the wage that the manager should bear. The problem of striving forgovernmentresourceswould bemoreseriouswhen theofficial’srank ishigher because his cost of getting extra transfer is lower. The manager and the official use bribes to divide the surplus in order to allocate resources efficiently. But with the increasein α (non-state shares), the subsidies are decreased. This implies that with full bribery, if the non-state shareholders controlled the enterprises, and the state, manager and the employees inside the enterprise do not hold most shares, then the transfers will decrease.

(2) The Manager Controls over L

According to the redundant employees controlled by the manager, we can determine, from equations (8) and (9), that the optimal choices of T and Lare both zero:

,

b0

,

0

0

bL

T

U

U

U A T L Um( , ) m 0,0 ,Therefore, with the manager’s control over L, the threat point utility of the manager is A+βπ, whereas the threat point of the government official is zero. The outcome of Nash bargaining is an efficient point, found by solving equation (22): Max L T b, ,

b

WL

t

b

T

C

p

g

L

B

(

)

(

)

(

)

(

)

(22) The first-order conditions are

t WL b

W

B L g p CT b

L B( )

( )

( )( ) ( ) (23)

t WL b

B L g pC T b

T C p g ( ) ( ) ( ) ( ) ( ) ) ( (24)

( ) ( ) ( ) ( )

2 1

ˆ t WL B L g p C T

b (25)

4. Analysis and Comparative Statics

From equations (23), (24) and (25), we can get the same results as equations (20) and (21). (Here

bˆ

represents the manager’scontrol over L, and the equilibrium bribe amount under bargaining). Thus we can see that no matter whether the government official or the manager is corrupt, the optimal number of redundant employees and the subsidies are shown to be the same. This conclusion is presented in proposition 1.Proposition 1: Even though we release the right of personnel control or profit sharing rate to the manager, with the allowance of bribes, the manager will collude with the official, and the equilibrium amount of L and T are under the cooperative choice of manager and officials.

Regardless of who has control over L, the officials and the managers internalize the full cost of making inefficient decisions. When the official controls L, he effectively pays for higher L in terms of lower bribes, and hence he can raise L up to the cooperation level. When the manager controls L, he pays for higher L in terms of political and financial benefit, such as political promotion or more transfer payments.

Therefore, in both privately and publicly owned systems, if corruption exists, the participants would still negotiate and bargain for the utility maximization. This means when the reform of the state-owned enterprises aims to adjust the allocation of earnings and release personnel authority to the managers, if the control by the official still exists, including the management and evaluation or the amount of subsidies, the managers would choose to collude with the officials. Regardless of whether the initial level of redundant employees is determined by the manager or the officials, collusion would always exist. After the collusion, the two participants would get the same number of redundant employee and subsidies as in the case of cooperation. Therefore, if the state-owned enterprises still belonged to the government or if government officials still have influence on the enterprises, corruption problems

would always occur between government officials and the managers. Thus the state-owned enterprises could not eliminate their role in social welfare and social protection, and the efficiency of a state-owned enterprise depends on the combined utilities of the government official and the manager.

This result is different from the Shleifer and Vishny (1994), who determined that with full corruption, public ownership is not a problem. The allocation of resources is independent of either allocation of profit rights or the control rights over L. But in this paper, we conclude that the optimal redundant employees and transfer payment are decided by two different conditions. The shares of managers can affect the equilibrium level of redundant employees. Both the manager and non-state shareholding can influence the amount of T. Our model emphasizes that with the allowance of corruption, the optimal L and T are the same as the situation where the manager and the official cooperate with each other. This result has an important implication. After some reforms in state-owned enterprises in China, if government officials still have power in these state firms, and with full bribery, the ownership may influence the optimal level of L and T, but it cannot change the collusion between managers and officials. That is, either adopting the shareholder system or the power releasing policy, the combined utilities of the officials and the manager still affect the objective function of the enterprise, and make the state firms bear unnecessary social burden. The failures of the releasing power policy and contract system demonstrate this position. Until November 1994, the percentage of state firms operating with deficits was 41.4% (according to the government budget revenue), the shortfall was 27.6% of that in 1993.3 This poor performance did not change in 1996, when the net profit of the state firms was 41,750 million RMB; a reduction of 42.5% compared with 1995. The amount of deficiency was 72,670 million RMB; compared with 1995, this amount was an increase of 31.5%.4

The financial status of many state-owned enterprises is becoming worse in the process of reform. Even though a stock system has been adopted, the performance

3

Tun, 1995, p40.

4

improvement is not significant.

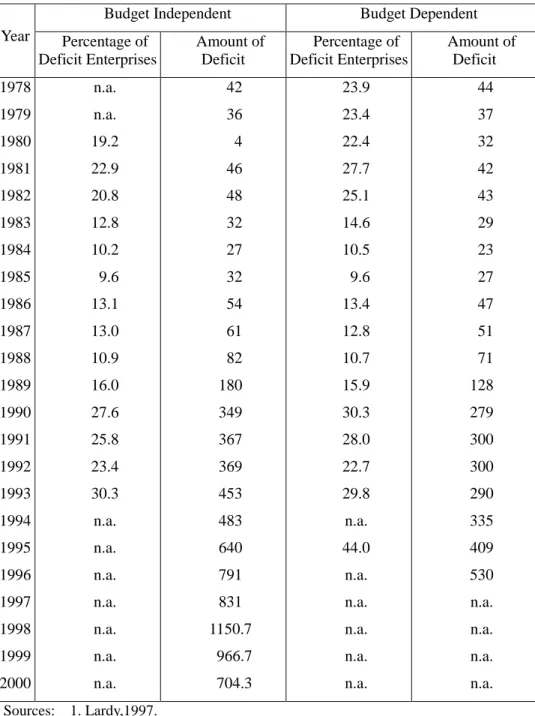

Table 1 illustrates the deficits in two different kinds of industrial state-owned enterprises: independent accounting industrial state-owned enterprises, and national budget dependent enterprises. According to Table 1, the deficit percentages of both kinds of enterprises continued to decrease in the first few years of reform and reached their lowest point of less then 10% in 1985. Afterward, they climbed to reach the peak in 1998, when the record-breaking deficit was 115 billion RMB.

The amount of deficit declined in 1999 and 2000, but the total amount of deficit still reached 70 billion. With the gradual opening of price mechanism since 1980s, the deficit amount had increased by 35 times from 1985 to 1998, which means that the deficits are not caused by price distortion. In addition to state-owned industrial enterprises, as inferred from the total amount of all independent accounting enterprises of 134.1 billion RMB, the deficit of non-industrial state-owned enterprises was 51 billion RMB in 1997.

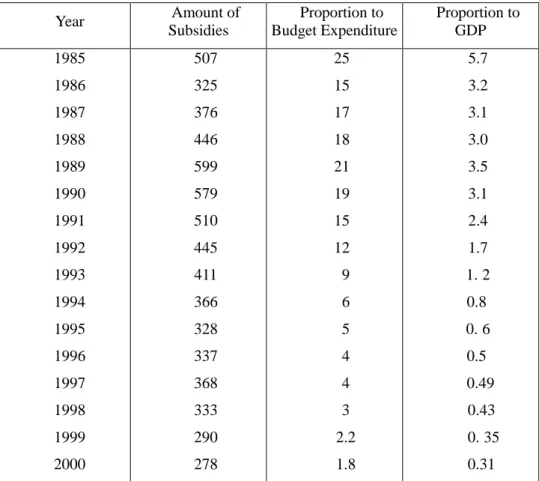

Referring to Table 1 and Table 2, since 1989 the deficits of most state-owned enterprises have been subsidized by bank loans instead of governmental subsidies. The amount of subsidies, hence, has been decreasing since 1989, without bringing too much burden on the economy as it appeared. However, the real situation is that the enterprises with deficits were compelled to ask for loans from banks to maintain their business under the tight subsidy policy of Department of Finance.

The deficits of state-owned enterprises shown in Table 1 and Table 2 could be greatly underestimated because most enterprises, rather than paying the interest, have additional interest payable to the new loan. Therefore, further analysis based on liability is necessary.

Table 1 Deficit of State-Owned Industrial Enterprises (1978~2000)

Unit: 100 Million RMB Budget Independent Budget Dependent

Year Percentage of Deficit Enterprises Amount of Deficit Percentage of Deficit Enterprises Amount of Deficit 1978 1979 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 n.a. n.a. 19.2 22.9 20.8 12.8 10.2 9.6 13.1 13.0 10.9 16.0 27.6 25.8 23.4 30.3 n.a. n.a. n.a. n.a. n.a. n.a. n.a. 42 36 4 46 48 32 27 32 54 61 82 180 349 367 369 453 483 640 791 831 1150.7 966.7 704.3 23.9 23.4 22.4 27.7 25.1 14.6 10.5 9.6 13.4 12.8 10.7 15.9 30.3 28.0 22.7 29.8 n.a. 44.0 n.a. n.a. n.a. n.a. n.a. 44 37 32 42 43 29 23 27 47 51 71 128 279 300 300 290 335 409 530 n.a. n.a. n.a. n.a. Sources: 1. Lardy,1997.

2. The amount of deficit (budget independent) 1978-2000: China Industrial

Statistical Year Book (2001), p.24.

Table 2 Government Subsidies to Deficit State-owned Corporations (1985-2000) Unit: 100 Million RMB Year Amount of Subsidies Proportion to Budget Expenditure Proportion to GDP 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 507 325 376 446 599 579 510 445 411 366 328 337 368 333 290 278 25 15 17 18 21 19 15 12 9 6 5 4 4 3 2.2 1.8 5.7 3.2 3.1 3.0 3.5 3.1 2.4 1.7 1. 2 0.8 0. 6 0.5 0.49 0.43 0. 35 0.31

Source: China Industrial Statistical Year Book (2001), p.247.

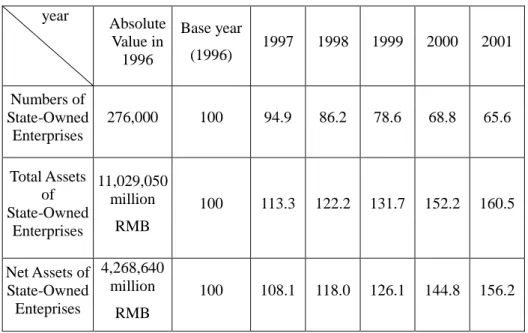

Table 3 shows that the number of state-owned enterprises is decreasing, while their total assets are increasing. New state-owned enterprises are often small ones and the number of medium or large ones is decreasing with their reconstruction. Since 1983, the subsidies from government for current assets of state-owned enterprises have been decreasing, and the state-owned enterprises have been starting to borrow a great deal from the banks. According to Table 4, operating funds transferred from the government have decreased sharply since 1983. The central government announced that they would no longer provide the enterprises with capital of investment of fixed assets at the end of 1984. In 1988, nearly half of the assets of

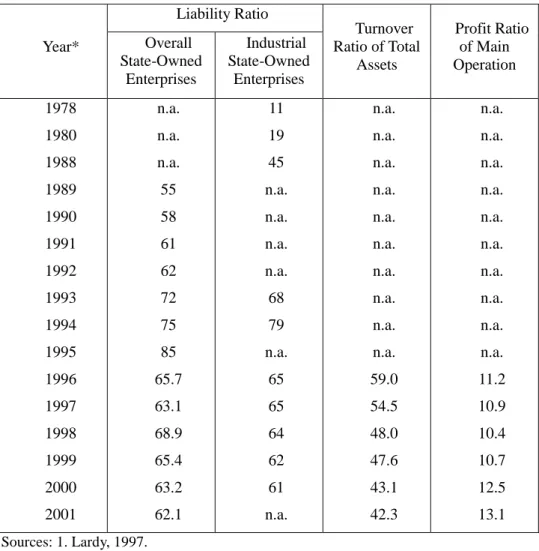

state-owned enterprises were liabilities, most of which were loans from banks. The liabilities of state-owned industrial enterprises were two-thirds of their total assets in 1993, and 85% in 1995. In recent years, the liability ratio of state-owned enterprises has been maintained at around 65%. However, as seen from the increasing total assets in Table 3, their trend to increase was clear between 1997 and 2001. The total assets increased from 11.2905 trillion RMB in 1996 to 17.701625 trillion RMB in 2001. Although the growth rate of total assets is similar to that of net assets, except for 2001, the first was often been greater than the latter, meaning that the deficits of enterprises did not improve. In addition, Table 4 also shows the inefficient use of capital in state-owned enterprises.

Table 3 Number and Total Assets of State-owned Enterprises (1996~2001)

year Absolute Value in 1996 Base year (1996) 1997 1998 1999 2000 2001 Numbers of State-Owned Enterprises 276,000 100 94.9 86.2 78.6 68.8 65.6 Total Assets of State-Owned Enterprises 11,029,050 million RMB 100 113.3 122.2 131.7 152.2 160.5 Net Assets of State-Owned Enteprises 4,268,640 million RMB 100 108.1 118.0 126.1 144.8 156.2

Table 4 The Indicators of Financial Status of State-owned Enterprises Unit: % Liability Ratio Year* Overall State-Owned Enterprises Industrial State-Owned Enterprises Turnover Ratio of Total Assets Profit Ratio of Main Operation 1978 1980 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 n.a. n.a. n.a. 55 58 61 62 72 75 85 65.7 63.1 68.9 65.4 63.2 62.1 11 19 45 n.a. n.a. n.a. n.a. 68 79 n.a. 65 65 64 62 61 n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. 59.0 54.5 48.0 47.6 43.1 42.3 n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. 11.2 10.9 10.4 10.7 12.5 13.1 Sources: 1. Lardy, 1997.

2. Chen and Zhan ,2001.

3. China Industrial Statistical Year Book (2001), p.24. n.a.: not available

The total liability of state-owned enterprises has been decreasing for the past two years, mainly becauseenterpriseswith largedeficitshavebeen “abandoned” (bankrupt, liquidated or privatized) or have been merged at the request of governmental officials into enterprises with surpluses. To sum up, enterprises adopting a stock system have high liability ratios; their use of capital is inefficient; and the growth of profit is limited. In fact, the official data clearly underestimates the liabilities ratios for the following reasons. The first is that the liabilities between enterprises, i.e. triangle debts, are not taken into consideration; the second is

that non-state-owned enterprises’liabilitiesarenotincluded;and thethird isthatthe underestimated depreciation ratio causes the total assets to be overestimated.

The government control and monitoring systems of state firms are still maintained under the shareholder system. The state still holds most of the shares of enterprises, and the officials, as the representatives of the state shares, can easily use their power to ask managers and enterprises to assist in their political or personal activities. As for the manager, in order to obtain financial or political benefit, he chooses to collude with the officials no matter how many shares he owns. Sometimes, both the manager and the officials harm the other shareholders or the enterprise by sharing benefits with each other. So if the Chinese government wants to improve the performance of the stated-owned enterprises by the shareholder system, the state would loosen the control rights from the officials over state-owned enterprises.

Furthermore, from equations (20) and (21), we can obtain the relation between the rank of the official and the values of T and L ; it is 0

P L and 0 ) ( ) ( ) ( ) ( T C p g T C p g P T

. Secondly, we can also obtain partial derivatives of

equations (20) and (21), we get 0 L , 0 T , 0 T .

From the above analysis, we can obtain the next proposition:

Proposition2: No matter whether it is the manager or the official who controls the level of redundant employees, under the collusion of managers and officials, the number of redundant employees has nothing to do with the rank of the official. But the subsidy standard increases with the rank of the official.

The model setting may cause this result. But for the officials, asking the state firms to carry social burden can solve their problem and give them good performance ratings. This common political benefit would not differ between higher or lower rank officials. The decisions on L and T are decided by the combined utilities of the official and the manager to maximize resources under their cooperative control. As for the level of redundant employees L, analyzing equation (21), we can determine that the official and manager will draw cash out of the public financial sources until

the marginal official cost of the last dollar is equal to one dollar under the case thatα is equal or close to zero. The striving for government resources problem would be moreseriouswhen an official’srank ishighersincethecostofgetting extratransfer is lower, dueto thecostofofficial’ssubsidiesisdecreasing with therank p. Under the same cost, the higher rank government official offers more subsidies, which will be reflected on themanager’schoiceof L. In order to increase the amount of redundant employees, the high-ranking government official must release more “good will”, which means more subsidies under lower cost. The relation between the bribe and the rank of officials, and will be discussed later.

Proposition3: With the increase of the shares held by managers, the optimal choice for L would decrease. The struggle for the subsidy would increase with β, and decreasewith α.

This means that no matter who has power over the personnel, when the manager’swelfaredependsmoreon thenetprofitofthestatefirm,hewilldecrease the unneeded labor to increase the profit. But he also tries his best to fight for more subsidies. In the process of bargaining, the manager and the official will be compensated by bribes. Analyzing the practice of shareholder system, the officials are willing to coordinate with the policy because the officials still have power over the stated-owned enterprises. Thestate’sambiguousdeclaration thattheproperty of state firms still belongs to the people in China gives the officials a basis to guide the overall shareholder process. Increasing the shares held by managers seems to release the social burden of the state firm, however, the state still holds the largest shares of the firms, and officials can influence the operational decision of enterprises. Even though the shares held by state are decreased, through regulations or transfer payments, government officials’ control power still exists in state firms. The increase of the shares of managers will make the managers care more about the net profits,and henceitmay begood fortheenterpriseperformance. Themanager’s behavior can be affected in two different ways. One is that the manager will try to decrease the extra employees, which can be observed when the unneeded labor of some state firms are forced to leave their positions especially after the implementation of the shareholder system which would cause another social problem. For the officials have the power to influence the operational decisions of state firms,

themanager’sdissolution oftheemployeesisundertheconsideration ofofficialand manager combined utilities. The cost of the officials will be compensated by the bribes from the managers, which is the other tactic that the manager will adopt. So the officials and the managers are still the real controllers of the enterprises.

In the official’s position, when the non-state proportion α increases, the optimal subsidies T would decrease. From the above relation, we can see that with the decrease of the state shares, the government official has less control over the enterprise, and the enterprise would depend less on subsidies from the government, which means that the government bears less responsibility for the enterprise. On the other hand, when the non-state and non-manager shares increase, the non-state shareholdersmusttry to getrid oftheofficials’influenceorbecometherealowner of the firm and lead the operation to pursue profit maximization.

To explain the relation between the bribe, net profit and the shares, from equations (19) and (25) we can obtain:

2 2 1 ~ T WL b (26)

2 2 ) ( 2 ) ( ) ( ˆ b T WL (27)

2 2 ~ b WL T (28) 2 ) ( 2 ) ( ˆ b WL T (29)If the net profit is positive (i.e. (π-WL)>0), the manager will increase the amount of bribe according to the extent of his own share holding. This means that the corruption amount between the manager and the government official will increase with the increase of β. The above collusion will not change whether the government official or the manager owns the control right over L. If the official owns the control right over L, under the condition that the net profit is positive, equation (26) is positive. If the control right over L belongs to the manager, under the condition that the net profit is positive and [()2] is positive, equation (27) is positive. This proves that in more profitable stated-owned enterprises, the

corruption relation will increase according to the share of the manager. Therefore, no matter whether it is under the contract system or shareholder system, if the control from the government officials still exists, the corruption will be more and more seriouswith theincreaseofthemanager’sshares.

On the contrary, when the net profit is positive (i.e. (π-WL+T)>0), that indicates that the corruption amount between the manager and the government official will decrease with the increase of non-state and non-manager shares. The above collusion will not change whether it is the government official or the manager who owns the control right over L.

If the enterprise is totally owned by government (α=0), and the official has the control right over employment, then when the net profit is less than zero (i.e. (π -wL)<0 ), we can see that the corruption will decrease with the share holding of the manager. But when α>0, and ] 0

) ( [ 2

WL T , with the increase of subsidies,thepositiverelation between theamountofmanager’ssharesoftheand the bribe is obvious.

If the manager decides the level of the redundant employees, it means that the managerownsthecontrolrightoverL,and when theenterprise’snetprofitisless than zero (i.e. (π-wL)<0), the amount of corruption will increase with the increase of shares of the manager when α=0. When α>0, and [()2]<0, the bribe amount has a positive relation with the shares of the manager. But with α>0, and [()2]>0, the bribe amount has a negative relation with the shares of the manager.

The above relationships are summarized in proposition 4.

Proposition4: When a state-owned enterprise is more profitable, it is more possible for the manager to collude with the official, and offer higher bribes. But in the state firm with deficits, the manager is less willing to bribe the officials, and the non-state shareholders have active motivation to bribe the officials for rescuing the firms.

Generally, if the profit of the optimal number of the employees, π, which is enough to afford the excess burden caused by the redundant employees (that is when (π-WL)>0), no matter whether the decision on the number of redundant

employees is held by the officials or the managers, then it is more possible for the manager to collude with the officials. On the contrary, if (π-WL)<0, then no matter whether it is the government official or the manager who decides the number of the redundant employees, the relation between the bribe and shares of the manager is not certain, but depends on the net transfer.

As for the more profitable enterprises, the managers would promise to increase the number of the redundant employees, with the increasing of the transfer payment, this benefits not only the enterprises but also the manager. Therefore, if the redundant employees are affordable, the manager will be more willing to collude with the officials, and the more profit in the enterprises, the more serious the consequence. On the other hand, after the implementation of the shareholder system,increasing manager’ssharesmay makethem caremoreabouttheprofits. For that reason, the manager may bargain with the officials to decrease the extra employees, using a bribe as exchange. That is why the manager is more willing to collude with the officials. This collusion can make it easier for the manager to negotiate with the officials to reduce the social burden, and yet obtain the same or greater transfer.

From the equations (19) and (25), we have:

0 ~ u b , 0 ~ L b , 0 ~ T b , 0 ˆ L b , 0 ˆ T b (30)

We can obtain proposition 5 from the relation of the reserved utility of the manager and the amount of corruption.

Proposition 5: When a government official controls L, a less able manager would be more willing to collude the government official and would be more willing to pay a higher bribe. In addition, no matter who controls the number of the redundant employees, when the transfer payment is higher and the redundant employees are lower, the amount of bribery would be higher.

From the above analysis, we can see that in the reform policy of state-owned enterprises, the officials’ power appears in different forms, and uses different methods to influence the operation of firms. Even after the implementation of the shareholder system, officials still are the representatives of the state shares, giving them power to control the enterprise, including the appointment of managers. The

less able managers will pay higher bribes to make up for their inferiority. In this weak bargaining circumstance the manager has to give more, and bribing officials is one way to obtain control over an enterprise.

From equations (19) and (25), we can obtain:

)) ( ) ( )( ( ) ( ) ( ( 2 1 ~ * ' '' T C T C p g T C p g p T p b (31) 0 ) ( ) ( ) ( ) ( 2 1 ˆ '' ' p T p T T C p g T C p g p b (32)

If the government officials control the level of the redundant employees, and if the corruption is effective, then the transfer payment will increase, which is

) ( ) (T C T*

C . With higher-ranking officials, a manager is more willing to pay a bribe. Therefore, the more authoritative the more serious the situation of corruption will be. When the manager controls the number of the redundant employees, no matter whether there is an increase in transfer payment or a decrease in the number of redundant employees, in order to cooperate with the higher ranking official, the manager will be willing to pay a higher bribe.

Conclusion

We seek to explain the factors that affect the collusion between managers and government officials. These factors include the share holding proportion of the manager, the degree that the officials control the enterprise, and the ability of the managers. The goal of this research primarily focuses on the problems caused by collusion and corruption, so it is very difficult to give empirical investigation. Due to the difficulty of collecting data, this study uses models for prediction.

We obtain that no matter whether the enterprises are publicly or privately owned, and no matter whether it is government officials or managers who hold the employment power, in the situation of corruption they will maximize the combined utilities of the officials and the managers under full bargaining. If the profit of the enterprise is large enough to cover the burden of the redundant employees, then no matterwho holdsthepower,asthemanager’sshareholding increases,therewillbe