A Look at Asymmetric Payments between Board Members and Shareholders

Wuchun Chi [email protected] Department of Accounting National Chengchi University

Taipei, Taiwan, R.O.C. Chung-Yuan Hsu [email protected] Department of Accounting National Chengchi University

Taipei, Taiwan, R.O.C. Wan-Ying Lin* [email protected] Department of Accounting National Chengchi University

Taipei, Taiwan, R.O.C.

This Version: December 25, 2006 ___________________________

*Corresponding author. Department of Accounting, National Chengchi University, 64, Zhi-nan Road, Section 2, Wenshan, 11605, Taipei, Taiwan, Republic of China. Email: [email protected]. Phone: (886) 2-29393091 ext. 81130. Fax: (886) 2-29387113. The paper has benefited from comments of workshop participants at National Chengchi University and National Taiwan University. We gratefully acknowledge the financial support from National Science Council (Project No. NSC94-2416-H-004-037) and the valuable assistance from Chao-Jung Chen.

A Look at Asymmetric Payments between Board Members and Shareholders Abstract: Board members may well be the instigators of potential conflicts of interest since they are simultaneously the setters and receivers of both board remuneration and dividends. They may act for their own personal benefit at the expense of external shareholders. We investigate the impact of ownership structure, board structure and control deviation on payment asymmetry where excessively high remuneration is paid to board members but considerably lower dividends are distributed to shareholders. We find strong evidence confirming that the larger the shareholdings of board members and outside blockholders are, the less asymmetric the payments are. With controlling family members on the board and a higher percentage of seats held by independent board members, there is a slight reduction in the likelihood and severity of asymmetric payments. In addition, with board seat-control deviation measured as the difference between controlling shareholders’ voting rights in the board meeting (counted by heads) and that in the shareholders’ meeting (counted by shares held), it is abundantly clear that the larger the board seat-control deviation is, the higher the degree of payment asymmetry. However, the conventional deviation between voting rights and cash flow rights has no significant effect on payment asymmetry. While prior research has primarily focused on board-manager agency issues, the board-shareholder perspective could be even more important because it is the board, not the managers, that is the most directly delegated agent of shareholders. Thus, this study enhances our understanding of the determinants that reduce the conflicts of interest between board members and external shareholders.

Keywords: asymmetric payments, board compensation, ownership structure, board structure, control deviation

1. INTRODUCTION

With its focus on the corporate board, this study explores one source of conflicts of interest between board members and external shareholders. Common sense wisdom has it that a corporate board, as the most directly delegated agent of shareholders, should not use its position of trust and confidence to further its personal interests, such as by authorizing excess compensation for themselves at the expense of shareholders. Although studies in the extant literature on the function of the board have mainly focused on how it interacts with other agents (e.g., managers and auditors) who are monitored by the board, to have a more complete picture of board effectiveness, evaluating the function of the board exclusively on how it reacts to the performance of managers and the opinions of auditors (e.g., management turnover or dismissal of auditor) is simply not enough.1 We take the position that investigating behaviors that are directly related to the board itself are of particular importance, especially when they pertain to decisions that result in conflicts of interest between board members and shareholders.

Since corporate boards are responsible for making and monitoring major strategic, operational and managerial decisions (Johnson, Daily and Ellstrand 1996),2 their performance is critical to firm success (Coles, Daniel and Naveen 2006) and , in fact, is considered the core of corporate governance (OECD 1999, 2004).3 To the best of our knowledge, however, only a limited number of studies have examined conflicts of interest between board members and external shareholders.

To this end, we use Taiwanese listed companies as our sample and explore how board characteristics affect the likelihood and the extent of payment asymmetry, as

1For example, Florou (2005) finds that effective governance increases the likelihood of the dismissal of the chairman when the chairman is involved in the appointment of a failing CEO. Klein (1998) reported that board committee structure influences firm performance. Helland and Sykuta (2005) show that boards with a higher proportion of outside directors do a better job of monitoring management. Werner, Tosi and Gomez-Mejia (2005) show that ownership structure (owner-controlled versus manager-controlled) affects pay-performance sensitivity. Carcello and Neal (2000) find that the greater the percentage of affiliated directors on the audit committee, the lower the probability that the auditor issues a going-concern report. Carcello and Neal (2003) further find that audit committees with greater independence, greater governance expertise and lower stock holdings are more effective in shielding auditors from dismissal after the issuance of new going-concern reports.

2 Johnson, Daily and Ellstrand (1996) attribute the agency/control role, the strategic decision and policy support role and resources acquirer as three main functions to the board members.

3 Responsibility of corporate board has been incorporated as an important aspect by several institutes

providing corporate governance grading systems, such as the Institutional Shareholder Services, Credit Lyonnais//Lyonais Securities-Asia and Standard & Poor’s.

demonstrated in excessive compensation to the board and comparatively meager dividends to shareholders.4 We define whether board members have excessive compensation relative to external shareholders. Payment asymmetry exists when a firm’s dividend payout ratio is less than the industry median and its board’s remuneration is more than the industry median. We adopt the presence of asymmetric payment as the variable of interest in this study. The observation that board members have excessive remuneration, while their shareholders receive only modest dividends suggests that the board procures a windfall at the expense of shareholders. A relatively greater discrepancy in payment asymmetry between shareholders and their delegated agent, the board, is indicative of a more severe agency problem. The fairness of resource distribution between board members and external shareholders falls into corporate governance because with weak governance, self-oriented incentives on the part of the board that leave outside shareholders vulnerable to conflicts of interests cannot be effectively eliminated.

In fact, for controlling owners, the most effective way to increase and exercise their influence over decision-making is to gain seat control. We empirically show that a deviation between board seat control and voting rights (hereafter, seat-control deviation; for detailed definitions, see section 3) can significantly explain the likelihood and severity of asymmetric payment. However, we cannot find the same evidence for a deviation between voting rights and cash flow rights (hereafter, voting deviation), a traditional measure of deviation of the one-share-one-vote principle (La Porta, Lopez-de-Silances, Shleifer and Vishny 2002). As Taiwan is a country with civil (code) law, unlike those with common law, ownership is highly concentrated and outside investors have little protection (La Porta, Lopez-de-Silances and Shleifer 1999). Therefore, the evidence of not being able to support the effect of traditional measure of deviation is essential for a comprehensive understanding of corporate governance for companies worldwide with similar circumstances.

Research on the value of corporate governance has mostly centered on the shareholder’s perspective (e.g., Gompers, Ishii and Metrick 2003), the bondholder’s

4 In Taiwan, basic corporate governance is a two-tier structure that consists of directors and supervisors,

both are elected by shareholders. Directors are responsible for ensuring compliance with laws and regulations, avoiding conflicts of interest and overseeing the overall management of a company's business. Supervisors are responsible for the effective monitoring of a company's board and management. We use the term “board members” to indicate both directors and supervisors.

perspective (e.g., Ashbaugh-Skaife, Collin and LaFond 2006) and the minority owner’s perspective (e.g., Bates, Lemmon and Linck 2006). This study adds to the third string of research by investigating how various characteristics of ownership and board structure reduce conflicts between internal and external shareholders.

The role of board members of large publicly-held companies has been the focus of corporate governance issues (Lin 1996), but with few exceptions (e.g. Dalton and Daily 2001; Hassan, Christopher and Evans 2003), the available evidence as to the extent to which board compensation effectively aligns board interests with shareholders’ interests is largely anecdotal (Kaback 1996). To fill this gap, we conduct empirical research to investigate asymmetric payment between board members and shareholders using Taiwanese listed companies as our sample due to data availability.5 What raises considerable concern for Taiwanese companies are the discrepancies in compensation schemes between executive and non-executive board members.

Commonly, the boards of Taiwan listed companies contain a mix of inside, outside and independent directors (Hsu and Lin 2006).6 Based on our preliminary analysis, over the 2001-2005 period, the composite ratios of board members of these Taiwan listed firms are 59%, 30.20% and 10.80% for inside, outside and independent members, respectively. With respect to the form of board remuneration, non-executive directors (i.e. outside and independent directors) normally only receive a cash package, whereas inside board members (i.e. executive directors) are eligible for an employee bonus based on earnings in addition to the cash package shared by all members.7 As staff compensation

committees are not standard to the boardrooms of Taiwanese companies, board members set their own compensations, as specified in the firms’ articles of incorporation.8 This is made more controversial by the fact that board members are also the setters of a

5 Information about board directors is publicly available in various sources, including annual reports and

prospectus provided by publicly-held companies, survey reports of Taiwanese business groups released by the China Credit Information Service, Ltd. (a private institute) and the database of Commerce Industrial Services Portal (http://gcis.nat.gov.tw/index.jsp) at the Ministry of Economic Affairs, Taiwan.

6 Hsu and Lin (2006) conduct a series of case studies on Taiwanese business groups. They document that

boards of Taiwanese companies are commonly composed of inside (executives, controlling family members, past employees or employees from affiliated companies), outsideand independent bodies (as required by the Securities and Exchange Law of Taiwan, independent board members shall hold shares of less than 1%).

7 Some firms specify that their executive directors are not entitled to cash package remuneration.

8 Some firms specify a ratio that is a fixed number or a minimum or maximum ratio to distributable

company’s dividend policy. In other words, the fact that board members are simultaneously the setters and receivers of compensation and dividends puts the board on the spot as they confront a tradeoff between board compensation and dividends for themselves. For instance, board members with a small number of shares likely tend to favor more generous board compensation, which -- in the eyes of external shareholders -- constitutes an unfair payment. By contrast, board members with a significant proportion of shares likely to have less of a tendency to permit unfair payments, given that they can receive a considerable amount in dividends.

In addition to investigating payment asymmetry between board members and shareholders, we examine the effect of other governance variables on the likelihood and the extent of payment asymmetry. These variables include the role of outside blockholders, the number of independent board members, the role of controlling family members on the board and seat-control and voting deviations. In addition, as control variables, we incorporate return on assets, stock return, firm size, leverage, board size, institutional investor shareholdings and whether CEO is simultaneously the chair of the board.

As regards ownership structure, we find that, ceteris paribus, asymmetric payments are less likely when board members or outside blockholders own relatively more shares. With respect to board structure, we find weak evidence that the dominance of controlling family members on the board and the percentage of seats held by independent board members reduce the extent to which asymmetric payments are made. The evidence also shows that seat-control deviation is positively related to the asymmetric payment. In other words, the greater seat-control deviation is, the more severe the problem of asymmetric payment is. In short, we find that firms with strong governance exhibit a lesser degree of unfair payment behavior. To the best of our knowledge, this study is the first to demonstrate that the characteristics of ownership and board structure can affect board members’ propensity to maximize their own benefits by making asymmetric payments.

The unique features of this paper are two-fold. Firstly, previous studies on the effectiveness of the board have mainly focused on how the board interacts with the agents monitored by the board. We investigate the behaviors directly related to the board itself, especially board decisions vis-à-vis payment that results in conflicts of interest between

board members and outside shareholders. Secondly, we provide empirical evidence on seat-control deviations (a new measure) versus voting deviations (a traditional measure) for ultimate control deviation. For controlling owners, to expand and exercise their influence over decision-making, obtaining seat-control is the most effective way. We show that seat-control deviation can statistically explain unfair payment, while voting deviation cannot. This suggests that, compared to voting deviation, seat-control deviation is a considerably more important indicator to explain conflicts of interest vis-à-vis payment among shareholders.

The remainder of the paper is organized as follows. Section 2 describes the role of governance in mitigating conflicts between board members and outside shareholders. Section 3 explains issues related to the research design. Section 4 describes the sample and presents the descriptive statistics. Section 5 reports the empirical findings, and section 6 provides the results of the sensitivity checks. Section 7 concludes the study and makes some suggestions for future research.

2. OWNERSHIP STRUCTURE, BOARD STRUCTURE AND UNFAIR PAYMENT Previous literature shows that ownership and board structure are important when examining agency issues involving shareholders. This section first reviews prior studies and develops the research hypotheses.

Ownership and board structure have been investigated in different research contexts, including firm value (Coles et al. 2006), operating performance (Bhagat and Black 2002; Fich and Shivdasani 2006), cost of capital (Anderson, Mansi and Reeb 2003), credit rating (Ashbaugh-Skaife et al. 2006), pay-for-performance relationship (Werner, Tosi and Gomez-Mejia 2005), corporate failure (Parker, Peters and Turetsky. 2002; Lee and Yeh 2004), informativeness of earnings (Fan and Wong 2002), dividends (Francis, Schipper and Vincent 2005) and earnings quality (Wang 2006).9 Although the empirical findings show that ownership and board characteristics do matter in the above contexts, it is noted that none of these studies has placed the board itself at front and center of their

investigation. More specifically, studies focusing on opportunistic behaviors directly

9 Samples used in these studies are different. For instance, Fan and Wong (2002) investigate firms in East

Asian economies. Francis, Schipper and Vincent (2005) examine the U.S. dual class firms, and Wang (2006) studies founding family ownership of the U.S. companies.

related to the board as the dependent variable are scarce.

Board compensation is another context in which to investigate the behavior directly related to the board. Main, Bruce and Buck (1996) and Conyon and Peck (1998) report a significantly positive correlation between firm performance and board remuneration. But, this does not guarantee that there is no conflict of interest between board members and shareholders. In this regard, Hassan et al. (2003) find that there has been steady growth in directors’ remuneration against deteriorating return on equity, suggesting that board directors have experienced an increase in remuneration at the expense of shareholders’ returns. In addition, Business Weekly (2004) reports that for a large portion of Taiwanese listed companies, board members behave indolently in terms of receiving unusually high compensation regardless of performance.10 Therefore, which factors account for conflicts of interest between board members and shareholders is worthy of investigation.

The authorization of asymmetric payment is selected as our dependent variable since total returns allocated among board members and shareholders in a specific year are fixed, and this constitutes a board-shareholder’s conflict. The scenario where the board sets the dividend and board compensation policies provides us with an ideal research setting that allows us to shed light on factors reducing such conflict. We contend that an in-depth understanding of the rationale behind making asymmetric payments is sure to enhance our knowledge on how ownership structure and board structure affect such conflicts between board members and external shareholders.

Next, we discuss the role of ownership structure and board structure in the practice of a board’s making asymmetric payments and then develop our research hypotheses. We define measures that gauge the composition of shareholding as ownership structure variables (i.e. stocks held by board members and outside blockholders) and measures that describe the composition of boards as board structure variables (representation of independent board members and controlling family members). Finally, we explain the association between the likelihood of there being asymmetric payments and control deviations -- both seat-control deviations and voting deviations.

2.1 Ownership structure

10 Business Weekly is a well-known financial publication with wide readership in Taiwan

Stocks held by board members. The entrenchment effect and alignment effect are two

competing arguments conventionally adopted by research on how ownership influences agency problems (Shleifer and Vishny 1997). To explain, the entrenchment effect argues that large inside shareholders in firms with concentrated ownership will have greater incentives to maximize their own gains at the cost of other shareholders. Against this, the alignment effect contends that large inside shareholders may monitor management more thoroughly and thus carries potential benefits to all shareholders. Convincing evidence supporting both the entrenchment effect (e.g., Fama and Jensen 1983; Morck, Shleifer, and Vishny 1988; Claessens et al. 2002) and the alignment effect (e.g., Demsetz and Lehn 1985) has been well documented.

In this study, we adopt the position of alignment effect to explain the relationship between board ownership structure and asymmetric payment. The necessary premise to validate the entrenchment effect would require a sacrifice of wealth of principal to benefit the agent. In a general context, the principal and agent are different players of a game. But in our setting, the role of the board and that of shareholders overlap a great deal if board members are also large shareholders. A conflict of interest would be more severe if fewer stocks were held by board members because, in that case, they would have a greater incentive to maximize their own compensation rather than the dividends of shareholders, resulting in a higher tendency to make asymmetric payments. However, such behavior is expected to be less likely if board members are also large shareholders. Therefore, we believe that the alignment effect is more applicable in the present study.

Though not exactly in the same setting as ours, Elson (1993) shows that firms with compensation committee members that have high equity ownership are less likely to overcompensate corporate executives; this is in line with the argument that board members with greater equity investment in the firm develop shareholder-like interest, which reduces the possibility and severity of asymmetric payments. Based on the alignment effect, we predict that the greater the shareholding of the board is, the less tendency there is for and the less severe is the practice of making asymmetric payments: H1: The percentage of shares held by board members is negatively related to the

likelihood (severity) of asymmetric payment.

blockholders play a positive role in corporate governance. In an extensive survey on blockholders and corporate control, for instance, Holderness (2003) points out that blockholders have the incentive and opportunity to monitor management and thus enhance a firm’s expected cash flows that accrue to all shareholders. As the effectiveness of the board is critical to a firm’s success (Coles et al. 2006), extending Holderness’ conclusion, we expect that outside blockholders also have a strong incentive to monitor the board. To capture the monitoring effect of outside blockholders on deterring the board from making asymmetric payments, we further include the shareholding of outside blockholders. Specifically, we hypothesize that both the likelihood and severity of making asymmetric payment are negatively related to the shareholdings of outside blockholders.

H2: The percentage of shares held by blockholders is negatively related to likelihood (severity) of asymmetric payment.

2.2 Board Structure

Role of independent board members. The perceived extent of a breach in trust heavily

relies on how well corporate boards can fulfill their responsibilities. The influence of board independence on the functions of corporate governance has attracted the attention of regulators, academia and practitioners alike. For instance, empirical evidence on whether board structure affects firm value has been mixed. Some studies have shown that the role of independent board members in corporate governance is positive (e.g., Borokhovich, Parrino and Trapani 1996; Cotter, Shivdasani and Zenner 1997),11 while others do not find support for such role (Yermack 1996, Hermalin and Weisbach 1988, Bhagat and Black 2002).

The lack of independence and absence of incentive may give rise to somewhat uncommitted behavior on the part of corporate boards (Jensen and Meckling 1976; Tirole 2005).12 With respect to the issue of independence, executives or controlling owners may handpick independent board members from among their personal friends or from social

11 More specifically, the positive effect of outside directors has been found in certain research contexts, like

management turnover (Weisbach 1988; Borokhovich et al. 1996), anti-takeover provisions (Brickley, Coles and Terry 1994) and negotiating takeover premiums (Byrd and Hickman 1992; Cotter et al. 1997).

12 According to Tirole (2005), the lack of independence and absence of incentives are two of the many

networks outside, yet close to, the firm. In other words, independent board members may actually only be “independent” in name –i.e., on the “outside,” not on the “inside.”

As for the lack of incentive, considering that board members with high equity investment in the firm may be highly influenced by potential financial interests, it is stipulated in the Securities and Exchange Law of Taiwan that the maximum number of stocks held by an independent board member must be limited to one percent of the firm and that an independent board member cannot be employed by that company.13 In other words, independent board members receive neither extra income from an employee bonus package nor handsome dividends. It is expected that there are two possible factors influencing asymmetric payments. For independent board members, the payment asymmetry results in a tradeoff between an increase in wealth and a tarnish of reputation. The asymmetry between responsibilities assumed and remuneration compensated may therefore motivate independent board members to set, or at least with little incentive to object to, more generous compensation. As such, this asymmetry would prompt independent board members to act in such a way that benefits them even if that is detrimental to shareholders. We acknowledge both the positive and negative effects of independent board members on payment asymmetry. However, based on the goal of having independent board representation and the concern about reputation, this study predicts a negative direction between the percentage of representation of independent board members and the likelihood and severity of the asymmetric payment.

H3: The percentage of independent board members is negatively related to the likelihood (severity) of asymmetric payment.

Role of controlling family members. According to existing theories and empirical

research findings, family ownership possibly affects governance-related issues in two ways: the entrenchment effect (wealth depriving) or the alignment (monitoring) effect. The alignment effect is more applicable in this setting because greater board compensation results in less revenue from dividends. In addition, Wang (2006) finds evidence that the founding family is associated with higher earnings quality. Wang (2006

13 Readers are referred to “Regulations Governing Appointment of Independent Directors and Compliance

Matters for Public Companies” for detailed information on qualifications for independent board members. In brief, Article 2 of this regulation defines the expertise qualifications of independent board members, and Article 3 further stipulates the electing qualifications for independent board members.

p.653) mentions that he cannot conclude whether this finding is a result of the demand for greater earnings quality from family firms (the entrenchment effect) or of the supply of greater earnings quality by family firms (the alignment effect). If the impact of family board members complies with the alignment effect in our study, then the findings in Wang (2006) can be interpreted as a result of the alignment effect.14

Prior studies have determined whether a company is family-owned or not based on the type of ultimate controllers, using shareholdings as the cutoff (e.g., 10% or 20%). We argue that it is the board meeting (seat control) rather than shareholder meeting (voting control) that has the real power of control when it comes to reaching major decisions, such as those pertaining to board compensation and dividends as well as operations and investment and other financing activities. We believe that seat control is a better concept to define whether a company is family-owned. We depart from previous studies by defining firms as family-controlled if 50 percent (or more) of the board members are members of the same family.

The reasons we use a dummy variable instead of number of shares to indicate a family-controlled company because the latter approach will give rise to a double count problem. Shares owned by a controlling family will be included in shareholdings of either board members (if the family members are on the board) or outside blockholders (if the family members are outside the board). Were we to adopt this conventional measure, it would inflate the effect of family ownership. Therefore, we adopt a dummy approach.

In that the history of the TSEC, founded in 1962, is significantly shorter than that of the NYSE, founded in 1792, it is reasonable to assume that family membership is equivalent to founding family membership in Taiwan. In fact, Hsu and Lin (2006) report that, for most Taiwanese listed companies, the controlling families are the founding families.15 As founding family companies show greater concern about the preservation of their family names (Anderson et al. 2003), compared to their non-family-controlled

14 Wang (2006, p.653) concludes the paper, “it is unclear whether higher earnings quality is a result of the

demand for greater earnings quality from family firms or a result of the supply of greater earnings quality by family firms.” Given that founding family is associated with high earnings quality, the former can be referred to as the entrenchment effect, while the latter can be referred to as the alignment effect.

15 Hsu and Lin (2006) survey 14 of the top 50 Taiwanese business groups and find that there are 11

family-controlled business groups. They further show that the controlling families are all the founding families.

counterparts, family-controlled companies are more likely to forgo short-term benefits (Wang 2006). Thus, we predict that the interests of family-controlled companies (usually also founding family companies in Taiwan) are more-closely aligned and that those companies have stronger incentives to monitor the board. To be more precise, this study hypothesizes that family-controlled firms are less likely to agree to asymmetric payments. Hence, we postulate:

H4: Family-controlled companies are negatively related to the likelihood (severity) of asymmetric payment.

2.3 Deviation between Ownership and Control

Shleifer and Vishny (1997) argue that large shareholders have incentives to maximize their own benefits at the cost of other shareholders. It has been shown theoretically and empirically that joint ownership and control creates greater agency conflicts (e.g., Fama and Jensen 1983; Morck et al. 1988).16 La Porta et al. (2002) and Claessens et al. (2002)

show that a high deviation of cash flow rights from voting rights has a negative effect on firm performance and shareholder value. Those studies suggest that pyramid and cross-holding structures broaden the difference of voting rights from ownership for firms in East Asian economies. Based on a sample of firms in seven East Asian economies, Fan and Wong (2002) find that the deviation of control from ownership creates agency conflicts between controlling owners and outside investors, which results in a greater self-oriented reporting incentive by controlling owners. Francis, Schipper, and Vincent (2005) also find that, compared to single class stocks, dual class firms with higher separation of cash flow rights from voting rights have lower earnings quality; while there exists evidence to show that dual stocks have higher informativeness of dividends.

As for ownership structure, it is possible to categorize a firm as a widely-held company based on an academic definition (e.g., La Porta et al. 1999; Claessens et al. 2002).17 However, ownership structure aside, publicly-held or not, in reality, every company must have an authority (an individual or a group of people) who is responsible for making the

16 Morck et al. (1988) report that mangers’ and shareholders’ interests are more aligned as managerial

ownership increases. They also find that mangers’ interests begin to diverge from those of shareholders as their equity stakes continue to grow.

17 Based on shareholdings, La Porta et al. (1999) classify ultimate owner into five types: (1) a family or an

individual; (2) the State; (3) a widely-held financial institution; (4) a widely-held corporation; or (5) miscellaneous.

final or ultimate decisions. Under the traditional definition, for widely-held companies, we are led to the conclusion that no one has the authority. However, it is not reasonable to assume that there is no one to account for shareholders, and therefore in every company, there should be at least one individual who has this authority. This study defines this individual (or a group of people) as the controlling owner(s). The details for the identification of the controlling owners are provided in the next section.

It is critical for controlling owners to have seat control in order to increase and exercise their influence in board decisions. Controlling owners have advantages in terms of obtaining information and using the resources of the firm (e.g. registrant of shareholders) to gather critical and incremental proxy votes, which gives rise to a further deviation between voting rights and seat-control rights. Seat-control deviation represents the most effective way to control shareholders and in turn obtain excess control, which further inflates controlling owners’ power over board decisions. In other words, when voting deviation is kept constant, seat-control deviation further deteriorates the one-share-one-vote principle. Hence, different from previous studies, we employ seat-control deviation in addition to voting deviation to measure the influence of controlling shareholders.

We provide guidelines as to how to calculate seat-control and voting deviations. First, assume that the voting right, cash flow right and seat-control right of the controlling owner of Company A are 20%, 13% and 60%, respectively (with six out of 10 board members (60%) controlled by the controlling owner). In this case, seat-control deviation is 40% (i.e. 60% minus 20%), while voting deviation is 7% (i.e. 20% minus 13%). A higher voting deviation indicates a greater violation of the one-share-one-vote principle. Traditional wisdom has it that voting deviation represents the asymmetric distribution between capital invested and power of control. Nevertheless, the actual power of the vote is exercised through the board. We believe that seat-control deviation further gauges the difference between actual (seat-control right, 60% in this example) and nominal (voting right, 20%) power exercised by the ultimate owner. More specifically, with the same voting right, a higher seat-control deviation means less stability for the controlling owners to exercise their influence in board decisions. That some owners have a higher seat-control deviation is mainly due to their use of proxy votes to inflate their short-term

power. A power-inflated management is usually more focused on personal benefits, and as a consequence, it behaves more myopically, which in this study typifies behavior associated with payment asymmetry. In sum, we posit that for boards with either higher voting or higher seat-control deviations, the board members are more inclined to initiate asymmetric payment.

H5: Voting deviation is positively related to the likelihood (severity) of asymmetric payment.

H6: Seat-control deviation is positively related to the likelihood (severity) of asymmetric payment.

3. DEFINITION OF THE VARIABLES AND RESEARCH DESIGN

3.1 Measurement of the dependent variables: UFDM and UFRK

To measure asymmetric payments, we let that the dummy variable UFDM take the value of one if a firm’s dividend payout ratio is less than its industry median and its board’s remuneration (scaled by net earnings) is greater than its industry median, and zero otherwise. Therefore, UFDM = 1 indicates a sign of asymmetric payment. In the development of UFDM, we focus on nonfinancial companies with positive earnings that pay dividends and board compensation.18

Next, we explain UFRK, a variable ranking the severity of payment asymmetry. If

UFDM has a value of zero, then UFRK is equal to zero. By contrast, if UFDM has a

value of one, then the following three steps are taken to define UFRK. First, for this subgroup, we categorize the observations on the basis of board compensation level (scaled by net earnings) into ascending quintile rank, each with a given value from 1 to 5 (Q1_Board ~ Q5_Board). The higher the given value, the higher the board compensation level of the firm. Second, following the same approach, we classify the observations on the basis of dividend payout ratio into descending quintile rank, each with a given value from 1 to 5 (Q1_Dividend ~ Q5_Dividend). The higher the given value, the lower the dividend payout ratio of the firm. Third, we multiply Qi_Board by Qj_Dividend (where i

18 There are two additional scenarios for payment, namely (1) firms with a net loss pay the board

compensation but no dividends; and (2) firms with positive earnings pay the board compensation but no dividends. The former is excluded because it is reasonable to compensate board members even if the company is experiencing a net loss. As for the latter, that firms with positive earnings do not pay any dividends may be due to their intention to retain their capital to take advantage of future investment opportunities, which is expected to bring them future growth.

and j = 1,…, 5) to determine their multipliers. Finally, we rank these multipliers and form deciles to obtain the value of UFRK. Firms in the top decile (decile 1) have the lowest level of payment asymmetry (UFRK =1), while firms in the bottom decile (decile 10) have the highest level of payment asymmetry (UFRK =10). In other words, the higher the

UFRK, the more severe the payment asymmetry is. To sum up, UFDM = 0 indicates that UFRK = 0. However, if UFDM = 1, then UFRK has a range from one to ten.

Although an increase in either index Qi_Board or Qj_Dividend increases the extent of payment asymmetry, it is reasonable to assume that the incremental effect of unfair board compensation (dividend), Qi_Board (Qj_Dividend), is much more severe for a dividend status (board compensation) at a much more unfair level. For example, when we take the first derivative of (Qi_Board × Qj_Dividend) with respect to Qi_Board, the result of Qj_Dividend implies that the more severe the status of Qj_Dividend is, the greater is the negative impact of Qi_Board on making asymmetric payments.19

3.2 Measurement of the independent and controlled variables

We explain the factors related to the likelihood and severity of payment asymmetry. It is our expectation that for board members (BDSH) and outside blockholders (BLKSH) who own relatively more stocks of the firm, a relatively higher percentage of seats held by independent board members (INDST) and the family-controlled firm (FMDM) reduce the likelihood and severity of payment asymmetry. We also predict that firms with a greater voting deviation (VMCF) or seat-control deviation (STMV) have an increased likelihood and severity of payment asymmetry.

To be specific, BDSH and BLKSH represent the percentage of shares held by board members and outside blockholders, respectively. We define outside blockholders as non-board member and non-executive shareholders whose shareholdings are either in the

19 This note provides a numerical example that compares two approaches, namely that which involves

multiplication versus that with addition. Suppose that Qi_Board = 1 and Qj_Dividend = 3 (i.e., its product 3 = 1 × 3). With a one-unit increase in Qi_Board (i.e., from 1 to 2), the increased product is 3 (new product 6 = 2 × 3). If the status of Qj_Dividend is changed from 3 to 4 and Qi_Board remains 1, then its product changes to 4 (1 × 4). A one-unit increase in Qi_Board (i.e., from 1 to 2) produces 8 (2 × 4); then, the increased product becomes 4 (from 4 to 8). For the same incremental Qi_Board (from 1 to 2), the incremental effect on payment asymmetry is 3 (when Qj_Dividend = 3) is lower than 4 (when Qj_Dividend = 4). When the approach with addition, i.e., Qi_Board + Qj_Dividend, is adopted, the incremental effect of Qi_Board on payment asymmetry is independent with the level of Qj_Dividend. In our numeric example, the marginal effect equals one. Our main findings are qualitatively unchanged if the approach with addition is used.

top 10 or over 5%. When 50% (or above) of the board members are all from a specific family, we define such companies as controlling families. FMDM, a dummy variable, indicates whether a company has a controlling family on the board (one for controlling family and zero otherwise).

From the ultimate controller perspective, the variable VMCF measures the difference between voting rights and cash flow rights, while STMV measures the difference between the seat-control rights and voting rights of controlling owners. Three major steps are used to identify the ultimate controller: (1) The largest shareholder (family members, if any, are included) is identified based on shares owned. The largest owner is defined as the largest shareholder and his family members (if any). (2) It is determined whether the largest owner is on the board: (2-1). If the largest owner is on the board and also serves as chair of the board or CEO, then he/she is defined as the ultimate controller. (2-2) If the largest owner is on the board but serves neither as chair of the board nor as CEO, then the chair of the board (family members, if any, are included) is defined as the ultimate controller; (3) Seat-control, traced at the ultimate controller level, is calculated. Seat control includes the ultimate controller’s family members, managers from the firm and its affiliated companies as well as representatives of other family-invested businesses, if any.20 Voting deviation and seat deviation both at the ultimate controller level are also calculated.21

Additional explanatory variables are added into our models based on a survey of prior research related to corporate governance. While many studies find that firm value decreases as board size increases (e.g. Yermack 1996; Eisenberg, Sundgren and Wells 1998), Coles et al. (2006) document that larger firms, diversified firms and firms that rely more on debt financing benefit from having larger boards. We include board size (BDSZ) to control for its potential effects on governance. Duality of CEO and chair of the board (DUAL) is included because, under the agency theory framework, a CEO with such a dual role can exercise significant control over board decisions (Fama and Jensen 1983). In addition, the percentage of shares held by domestic (INST) and foreign (FINST) institutional investors are included to control for their monitoring effect on board

20 The names of family members, managers and representative are all available in company financial

statements.

effectiveness (Almazan, Hartzell and Starks 2005).22 The percentage of executives on the board (MGST) is included to control for managers’ influences on board decisions (Lasfer 2006).23 Finally, it is a common practice in Taiwan that board members take a personal loan from a bank and use the shares of the firm as collateral. As loan redemption will be called for if a difference presents between the loan taken and the market value of the stocks pledged; there exist manipulative incentives for board members to defy such financial pressure, which in turn may weaken the monitoring effect from board members. The percentage of shares pledged by board members (PLDG) is incorporated to control for such possible impacts.24

3.3 Research design

We employ two measures to capture payment asymmetry between board compensation and outside investors’ dividends. The variable UFDM, a dummy variable, measures the likelihood of there being payment asymmetry, while the variable UFRK gauges the severity of payment asymmetry based on a 0-10 scale. Using UFDM (UFRK) as the independent variable, we employ the Probit (Tobit) model to serve our research purposes. Since UFDM is an indicator variable, we use the Probit regression model to estimate the effects of factors that affect the likelihood of payment asymmetry. Because several values of UFRK equal zero, it is more appropriate to use the Tobit specification to perform our analysis (Greene 2003).25

To investigate the effect of ownership and board structure on unfair payment, equation (1) represents our basic regression model. The dependent variable Y represents UFDM or

UFRK in the Probit or Tobit model, respectively.

22 Almazan, Hartzell, and Starks (2005) examine the role of active institutional investors on monitoring

costs in the context of executive compensation.

23 It is suggested that managers, through their shareholdings, entrench their position, thereby reducing the

monitoring power of the board. Almazan, Hartzell and Starks (2005) examine the relationship between board structure and managerial ownership. Since the focus of this study is on the board and managerial holdings, if managers are also board members, their shareholdings are included in shareholdings by board members. We adopt the percentage of representation of managers on the board rather than shareholdings to capture the essence of this effect.

24 A listed firm is required to file a report with the Taiwan Stock Exchange Corporation (TSEC) and Gretai

Securities Market (GTSM) when its board members take a loan from a bank and use the shares of the firm as collateral. In addition, the percentage of shares pledged must be disclosed in a firm’s annual report. The TSEC and GTSM in Taiwan are analogous to the NYSE and NASDAQ in the U.S.

25 We also employ the ordinary least squared and ordered Probit regression models to explore the

ε PLDG β MGST β FINST β INST β DUAL β BDSZ β STMV β VMCF β FMDM β INDST β BLKSH β BDSH β α Y + + + + + + + + + + + + + = 12 11 10 9 8 7 6 5 4 3 2 1 0 (1) where:

Y = UFDM (the likelihood) or UFRK (the severity ) of payment asymmetry;

BDSH = percentage of shares held by board members;

BLKSH = percentage of shares held by outside blockholders; INDST = percentage of independent members on the board;

FMDM = one if the firm is a family-controlled firm, and zero otherwise;

VMCF = voting deviation, measured by voting right minuses cash flow right;

STMV = seat-control deviation, measured by seat control right minuses voting

right;

BDSZ = number of board members;

DUAL = one if the CEO simultaneously serves as chair of the board, and zero

otherwise;

INST = percentage of shares held by domestic financial institutional investors;

FINST = percentage of shares held by foreign financial institutional investors;

MGST = percentage of executives on the board; and

PLDG = percentage of shares pledged by board members.

Except for FMDM and DUAL, which are dummy variables, the remaining independent variables in equation (1) are all in percentage terms. Based on our hypotheses, we predict the signs of the coefficients of BDSN, BLKSH, INDST and FMDM (β1 to β4) are negative,

while those of STMV and VMCF (β5 and β6) are positive. For the Probit (Tobit) analysis

in equation (1), a positive coefficient indicates that its corresponding variable has a deteriorating effect on the likelihood (severity) of payment asymmetry.

4. SAMPLE AND DESCRIPTIVE STATISTICS

We define a firm as having payment asymmetry if that firm has positive earnings and fully meets three conditions: (1) the dividend payout ratio is greater than zero; (2) the dividend payout ratio is less than the firm's industry median; and (3) the total compensation of the board members, scaled by net earnings, is more than the firm's industry median.

distribution of Taiwanese listed companies over the 1997-2005 period. The original number of observations is 10,306 in total, but after firms in the banking and financial industries, firms with insufficient data on the corporate governance variables and firms that experienced a net loss and distributed no dividends are excluded, the final sample consists of 5,457 observations. Upon further analysis, in the final sample, there are 1,368 observations of firms that satisfy our definition of firms with payment asymmetry. The 1,368 observations (i.e., UFDM = 1) are then ranked from one to ten (i.e., UFRK = 1,…, 10) based on the severity of payment asymmetry.

(Table 1 around here)

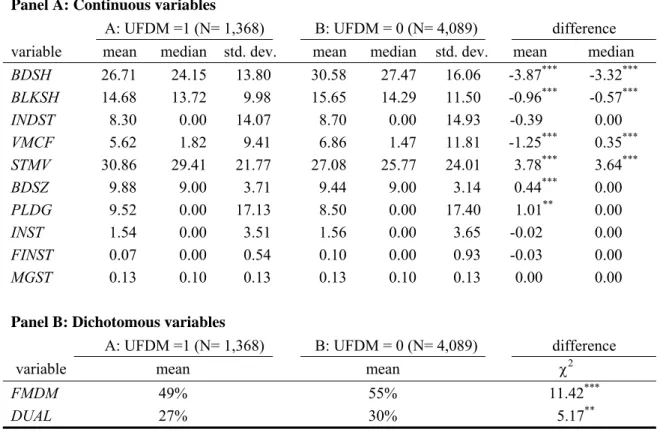

The descriptive statistics for the explanatory variables in the analysis are reported in Table 2, where column A (UFDM = 1) shows the group with payment asymmetry (N = 1,368) and column B (UFDM = 0) its counterpart (N = 4,089). In Panel A (B), we present the basic statistics for the continuous (dichotomous) variables. The average (median)

BDSH is 26.71% (24.15%) for the UFDM = 1 sample and 30.58% (27.47%) for the UFDM = 0 sample. The univariate comparison shows that the mean (median) difference

-3.87% (-3.32%) is significant at the p<0.01 (0.01) level. Since the percentages of share (both mean and medium) held by board members in column A are significantly lower than those in column B, it is consistent with H1. This implies that higher stock ownership by board members decreases the possibility of there being payment asymmetry.

The mean of BLKSH is 14.68% for the UFDM = 1 sample and 15.65% for the UFDM = 0 sample. Consistent with H2, relative to the group with payment asymmetry, the

UFDM = 0 sample has statistically greater BLKSH (p-value < 0.01). As regards the

median, the results are qualitatively similar. The difference in INDST between the two samples is insignificant. That is, we find no evidence to support H3. As firms in the

UFDM = 1 sample have a significantly lower percentage (49% vs. 55%; Panel B) for FMDM (p-value < 0.01), H4, which postulates that having controlling family members on

the board diminishes the likelihood of payment asymmetry, is supported.

We next discuss the effect of voting and seat-control deviations on the likelihood of payment asymmetry, i.e., H5 and H6. With respect to voting deviation (VMCF), we find mixed evidence from the mean and median tests. Comparing the means, we find that the higher the VMCF, the less likelihood of payment asymmetry there is (5.62% vs. 6.86%).

However, from the median test, we obtain the opposite finding (1.82% vs. 1.47%). On account of the inconclusive test results, we cannot confirm that H5 holds. Turning to seat-control deviation (STMV), we note the significant results of the mean (30.86% vs. 27.08%) and median (29.41% vs. 25.77%) tests strongly support H6. More specifically, the likelihood of there being payment asymmetry is less for firms with less deviation in seat-control. To sum up, based on our univariate test results, except for H3 and H5, all our hypotheses are supported.

Finally, we briefly report the two-group comparisons using our control variables. Firms with payment asymmetry tend to have a larger board size (BDSZ) and a higher percentage of stocks pledged by board members (PLDG). The differences between the two groups in

INST, FINST and MGST are insignificant.

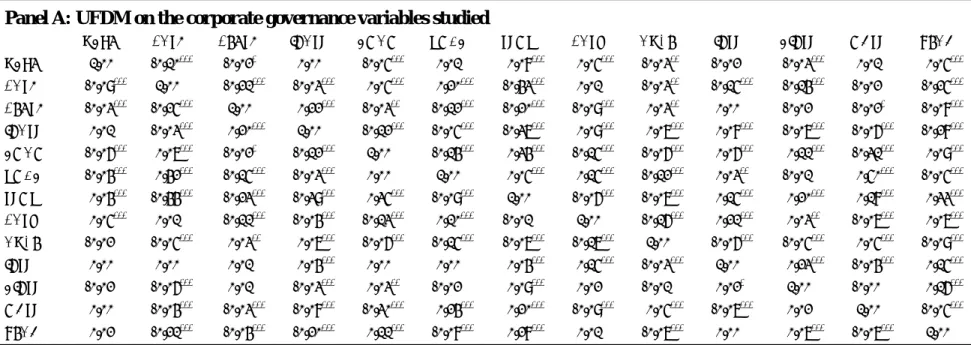

Table 3 provides the correlation matrix for the variables investigated with UFDM (shown in Panel A) and UFRK (shown in Panel B) as the dependent variables. The upper half on the right of the matrix reports the Spearman correlation coefficients, while the lower half on the left of the matrix reports the Pearson correlation coefficients. Consistent with the descriptive statistics in Table 3, both the Spearman and Pearson correlations results (in Panel A) indicate that the variable UFDM is significantly positively associated with STMV, BDSZ and PLDG. In comparison, the variable UFDM is significantly negatively correlated with BDSH, BLKSH, FMDM and DUAL. Regarding VMCF, while the Pearson correlation reveals a negative relation to UFDM, the Spearman correlation shows no association. The same conclusions also apply for the variable UFRK (in Panel B).

In all, Table 2 and Table 3 report that the likelihood of payment asymmetry is significantly associated with a lower percentage of shares held by board members and outside blockholders. The likelihood of payment asymmetry is also characterized by higher seat-control deviation. In addition, firms with controlling family members on their board are evidently less inclined to have payment asymmetry. These univariate tests show that all our hypotheses are supported, except for H3 and H5.

5. REGRESSION RESULTS

asymmetric payments as a function of the characteristics of ownership and board structure. To test the predicted relations between the characteristics of ownership and board structure and the likelihood of payment asymmetry (UFDM), we employ a Probit model. With respect to the test of the severity of payment asymmetry (UFRK), we adopt a Tobit model.

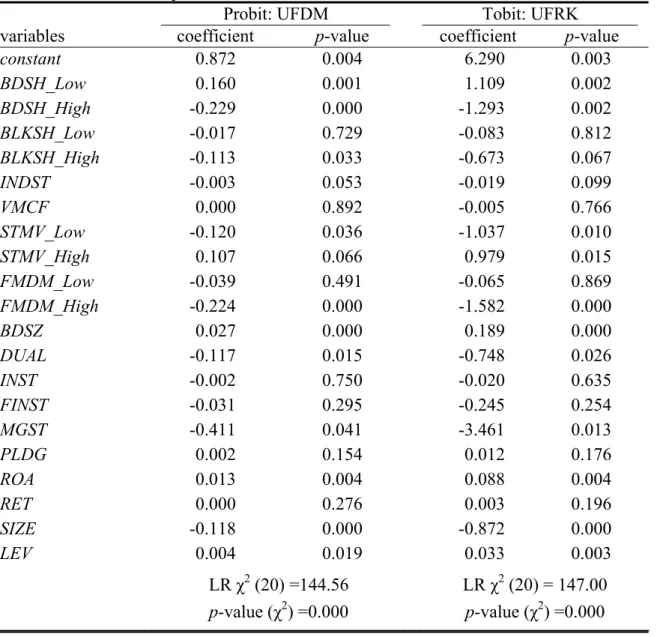

The UFDM-column in Table 4 presents the results from our Probit regression model for the likelihood of payment asymmetry. The model adequately distinguishes the binary outcome (Chi-squared = 124.25, p-value < 0.01), and an unreported overall fit of 75% (with 0.5 as the cutoff) is achieved. Consistent with H1, we find significance in the predicted direction at p-value < 0.01 for the coefficient of BDSH. Thus, the percentage of shares held by board members diminishes the possibility of there being payment asymmetry.

As concerns the role of outside blockholders, the coefficient of BLKSH, as expected, is significantly and negatively related to UFDM at the <0.01 level. We therefore again find evidence in support of H2 that posits that outside blockholders have a positive effect on reducing the likelihood of payment asymmetry. However, INDST is not found to be a significant predictor, which is inconsistent with H3. This finding does not allow us to conclude that independent board members can help to reduce the possibility of there being payment asymmetry. The negative coefficient of FMDM is significant (p-value < 0.01) and in the expected direction, fully supporting H4 that having controlling family members on the board reduces the propensity permit payment asymmetry.

The tests of H5 and H6 examine how control deviation affects payment asymmetry. With voting deviation used to measure the entrenchment effect, the insignificant coefficient of VMCF indicates that this traditional measure, widely used in prior studies, does not have power to explain the likelihood of payment asymmetry. However, using seat-control deviation, the results are consistent with our initial prediction that seat-control deviation raises the possibility of payment asymmetry. Therefore, compared to voting deviation, seat-control deviation does indeed explain the likelihood of payment asymmetry.

Regarding the severity of payment asymmetry, the overall result from the Tobit model is significant (Chi-squared = 119.79, p-value < 0.01). The UFRK-column in Table 4

further shows that the severity of payment asymmetry is significantly and negatively associated with BDSH, BLKSH and FMDM with p<0.01. Combining the results in the

UFDM and UFRK columns, we find that the percentage of shares held by board members

and outside blockholders as well as having controlling family members on the board all decrease not only the likelihood of there being payment asymmetry but also its severity. The variable INDST has no effect on payment asymmetry. Aside from that, the coefficient of VMCF is insignificant at the conventional level, while that of STMV is significantly and positively related to UFRK with p<0.10. In sum, we find evidence to support H1, H2, H4 and H6, but not H3 and H5.

Finally, we briefly document the findings on the control variables in this study. The significantly positive coefficient of BDSZ in the Probit (Tobit) model indicates that board size, measured in terms of the number of board members, increases the possibility (severity) of payment asymmetry. Contrary to conventional wisdom, the significantly negative coefficient of DUAL in the Probit (Tobit) model indicates that when there is a CEO who also serves as chair of the board, there is a decreased possibility (severity) of payment asymmetry. The reason for this may be that for a company with DUAL = 1, in a normal situation, the CEO must own enough shares to allow himself to both be elected chair of the board and be nominated CEO. We conjecture that for a CEO who also is a large shareholder, it is not in his/her best interests to make asymmetric payments. In addition, a CEO is normally entitled to an employee bonus, which is usually substantial, and therefore may be less concerned about board compensation. The variables PLDG,

INST and MGST are not found to be significant. As regards FINST, it does not

significantly explain the likelihood of payment asymmetry, but it can explain the severity of it.

6. FURTHER ANALYSIS

Based on prior research, we acknowledge the potential effects of firm performance and firm characteristics on payment asymmetry and add return on assets, market return, firm size and leverage in our further analysis. In addition, we also consider a nonlinearity check.

firm performance as well as the basic firm characteristics on payment asymmetry are controlled for. Specifically, we incorporate yearly industry-median-adjusted return on assets (ROA) and market-adjusted return (RET), firm size (SIZE) and leverage ratio (LEV) in equation (1) as additional control variables. As well-performing firms may pay more to reward their board members, we add ROA and RET into equation (1). Regarding SIZE and LEV, because firms smaller in size have less political costs (Watts and Zimmerman 1986) and firms with higher leverage are more influenced by debt covenants constraining their dividend payout ratios (Fenn and Liang 2001), they have an increased likelihood of payment asymmetry. In addition, as firms with more debt tend to have less free cash flows, we expect that SIZE and LEV have negative and positive signs, respectively.

Table 5 reports the results of the sensitivity checks. We find that the coefficients of

BDSH, BLKSH and STMV are consistent with those in Table 4, therefore, H1, H2 and H6

hold. As for H4, supported in Table 4, the coefficients of FMDM in Table 5 (-0.071 for the Probit and -0.536 for the Tobit) reveal that their explanatory power is reduced to the one-tailed significance level (p-value < 0.10). However, for H3, which is not supported in Table 4, the coefficients of INDST in Table 5 (-0.003 for the Probit and -0.015 for the Tobit) reveal that they are significant at the one-tailed level (p-value < 0.10). We still find no evidence to confirm that there is an association between VMCF and payment asymmetry. Combining evidence from Table 4 and Table 5, we note strong evidence to support H1, H2 and H6. We find weak evidence in favor of H3 and H4, but we cannot find evidence to support H5.

With respect to the control variables, we find that the coefficients of MGST (-0.374 for the Probit and -2.833 for the Tobit) are significant at the two-tailed level (p-value <0.10). One possible reason that MGST (the seat percentage of executives on the board) decreases the likelihood of payment asymmetry is that executives are entitled to receive a bonus and are therefore less concerned about board compensation. As for the newly-added control variables ROA, RET, SIZE and LEV, we find that the accounting-based performance, ROA, is significantly associated with the likelihood and severity of payment asymmetry. However, the market-based performance, RET, has no incremental explanatory power. Finally, Table 5 reveals that political cost, proxied by

asymmetry.

On the question of potential nonlinearity problems, Anderson et al. (2003) document a nonlinear relation between ownership and firm performance, and Wang (2006) reports the same finding but with a focus on earnings quality. So that our findings are not subject to nonlinearity issues, we further examine whether the relations between payment asymmetry and the variables of interests in this study are nonlinear. We use a dummy variable approach to untangle this issue.

Using BDSH as an example, we first equally divide the observations into High, Median and Low, i.e. into three subsamples based on shareholdings of board members. Second, we generate two dummy variables, BDSH_Low and BDSH_High. BDSH_Low equals one if that observation falls into the lowest subsample (i.e., the Low subgroup), and zero otherwise. Similarly, BDSH_High equals one if that observation falls into the highest subsample (i.e., the High subgroup), and zero otherwise. This means we adopt the Middle subgroup as the benchmark to conduct the nonlinearity check. The direction of the coefficient of BDSH_Low (BDSH_High) indicates the difference in the board member shareholding effect on payment asymmetry between the lowest (highest) subgroup and the middle subgroup. In addition, in cases where the coefficients of BDSH_Low and

BDSH_High are significant and their signs are in the same direction, it indicates that the

relationship between BDSH and payment asymmetry is nonlinear. Based on the same reasoning, BLKSH_High and BLKSH_Low (STMV_High and STMV_Low) are further derived from BLKSH (STMV).

In the case of FMDM, we further divide the sample into three subgroups, and we assign firms with FMDM = 0 to the FMDM_Low subgroup and those with FMDM = 1 into the FMDM_High and FMDM_Middle subgroups on the basis of the median percentage of controlling family members on the board. In our major finding, since

INDST and VMCF are not related to payment asymmetry, we conduct no further analysis.

Therefore, we use the following regression model to explore the potential nonlinearity effect on the issue of asymmetric payment following the dummy variable approach.

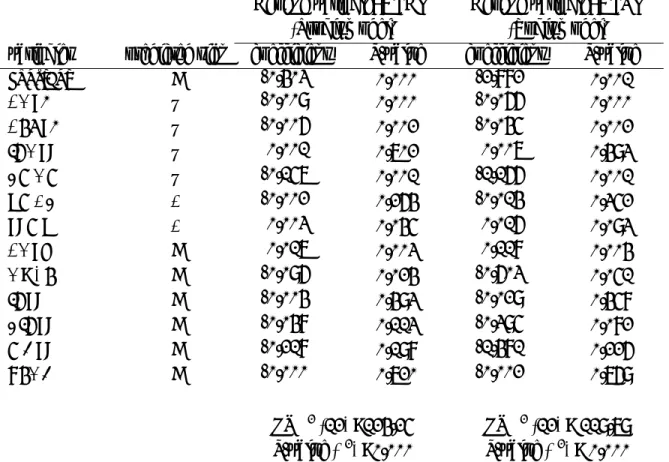

ε RET ROA PLDG MGST FINST INST DUAL BDSZ High STMV Low STMV VMCF High FMDM Low FMDM INDST High BLKSH Low BLKSH High BDSH Low BDSH Y + + + + + + + + + + + + + + + + + + + = 18 17 16 15 14 13 12 11 10 9 8 7 6 5 4 3 2 1 0 _ _ _ _ _ _ _ _ β β β β β β β β β β β β β β β β β β α (2) Table 6 presents the results of the nonlinearity tests. When the coefficients of the variables underscored with Low and High have opposite directions, it is indicative of a linear relation. When the coefficients are both significant and in the same direction, there is a potential nonlinearity problem. As shown in Table 6, for each variable, the coefficients attached to Low and High are either in opposite directions (i.e. BDSH and

STMV) or in the same direction but insignificant (i.e. BLKSH and FMDM). Hence, we

conclude that our findings are not sensitive to the potential nonlinearity problem. 26

Finally, our non-tabulated results show that our main conclusions are qualitatively unchanged when those firms with net earnings that do not pay dividends are included.

7. CONCLUSIONS

Against the backdrop of the OECD’s plea for corporate boards to be responsible for aligning key executive and board remuneration with the longer-term interests of their company and its shareholders (OECD 2004, p.24), this study examines whether and how

ownership structure, board structure and deviation between ownership and control affect

the fairness of payments between board members and shareholders. By examining the asymmetric payment between board and shareholders, this study contributes to the line of research on board effectiveness vis-à-vis minority shareholders. To structure our analysis, we construct six research hypotheses related to the determinants of payment asymmetry.

Three major findings emerge from our analysis. First, we find how ownership structure affects payment asymmetry. Admittedly, there is a tradeoff between board remuneration and dividends (if the board member is also a large shareholder), but given that the total amount of payment available for distribution is fixed, we find that the smaller the

26 We also perform Ramsey RESET (regression specification error test) on equation (2). The purpose of

RESET is to detect omitted variables and incorrect functional form, and the results suggest that our linear model is adequate.

monetary reward received by shareholders in the form of dividends, the greater is the severity of payment asymmetry. More specifically, we find compelling evidence to support our first hypothesis that the percentage of shares held by board members is negatively associated with the likelihood and extent of payment asymmetry. On the question of the role of outside blockholders, we also find convincing evidence to substantiate the second hypothesis that larger shareholding by outside blockholders diminishes the likelihood and extent of payment asymmetry.

Second, we show how board structure influences payment asymmetry, the bases of our third and fourth hypotheses. We only find weak evidence that these two factors have an effect on reducing payment asymmetry.

Finally, we find evidence on how deviation between ownership and control affects asymmetric payment. While our fifth hypothesis postulates that the conventional measure, voting deviation, affects payment asymmetry, our sixth hypothesis posits that the new measure, seat-control deviation, does affect unfair payment. What our empirical results confirm is worth noting: although the conventional measure does not have the ability to explain payment asymmetry, by all means the new measure, seat-control deviation, does have the explanatory power.

To check for robustness, we perform additional sensitivity tests, which include incorporating accounting- and market-based performances as well as several firm characteristics into our basic model. We also conduct test of nonlinearity. The results of these additional analyses fully support the conclusions discussed above.

Our study contributes to the extant literature on the effectiveness of boards. We formally document factors affecting payment asymmetry, one of the core governance principles underscored by the OECD (1999, 2004). Prior literature has mainly focused on how the board interacts with other agents (e.g., executive and auditor), while ignoring the board per se. This paper is unique in large measure because it investigates situations where the self-interests of the board predominate with the result that it constitutes a potential conflict of interest between the board and the external shareholders.

Several caveats must be considered when interpreting the findings of this study. First, although our findings have implications for board effectiveness, on account of expected institutional differences across countries, caution should be taken before making any

generalizations based on our conclusions. For example, La Porta et al. (1998, 2000, 2006) document cross-country differences in legal institutions and investor protection, and Shleifer and Wolfenzon (2002) analytically examine investor protection and equity markets. In fact, earnings management (Leuz, Nanda and Wysocki 2003) and disclosure incentives and their effects on the cost of capital (Franncis, Khurana and Pereira 2005) around the world are different. We believe that it would be fruitful to re-examine issues surrounding payment asymmetry in a cross-country context. Finally, also promising would be an examination of the economic consequences of payment asymmetry, such as the cost of capital and analyst ratings.

References

Abdullah, S. N. 2006. Directors’ remuneration, firm’s performance and corporate governance in Malaysia among distressed companies. Corporate Governance 6 (2): 162-174.

Almazan, A., J. C. Hartzell, and L. T. Starks. 2005. Active Institutional Shareholders and Costs of Monitoring: Evidence from Executive Compensation. Financial Management 34 (4): 5-34. Anderson, R. C., S. A. Mansi, and D. M. Reeb. 2003. Founding family ownership and the agency

cost of debt. Journal of Financial Economics 68: 263–285.

Ashbaugh-Skaife, H., D. W. Collins, and R. LaFond. 2006. The effect of corporate governance on firms’ credit ratings. Journal of Accounting and Economics 42: 203-243.

Bates, T. W., M. L. Lemmon, and J. S. Linck. 2006. Shareholder wealth effects and bid negotiation in freeze-out deals: Are minority shareholders left out in the cold? Journal of

Financial Economics 81 (2006): 681-708.

Bhagat, S. and B. Black, 2002.The non-correlation between board independence and long-term firm performance. Journal of Corporation Law 27 (2): 231-273.

Borokhovich, K. A., R. Parrino, and T. Trapani, 1996, Outside directors and CEO selection.

Journal of Financial and Quantitative Analysis 31: 337-355.

Brickley, J. A., J. L. Coles, and R.L. Terry, 1994. Outside directors and the adoption of poison pills. Journal of Financial Economics 35: 371-390.

Byrd, J. W., and K. A. Hickman. 1992. Do outside directors monitor managers? Evidence from tender offer bids. Journal of Financial Economics 32: 195-222.

Carcello, J.V. and T. L. Neal. 2000. Audit committee composition and auditor reporting. The

Accounting Review 75 (3):453-467.

Carcello, J. V. and T. L. Neal. 2003. Audit committee characteristics and auditor dismissals following “New” going–concern reports. The Accounting Review 78 (1):95-117.

Claessens, S., S. Djankov, J. Fan, and L. H. P. Lang. 2002. Disentangling the incentive and entrenchment effects of large shareholdings. Journal of Finance 57 (6): 2741-2771.

Claessens, S., S. Djankov, and L. H. P. Lang. 2000. The separation of ownership and control in East Asian corporations. Journal of Financial Economics 58 (1-2): 81-112.

Coles J. L., N. D. Daniel, and L. Naveen. 2006. Boards: Does one size fit all? Journal of

Financial Economics. (forthcoming)

Conyon, M.J. 1997. Corporate governance and executive compensation. International Journal of

Industrial Organization 15: 493-509.

Conyon, M.J., and S. I. Peck. 1998. Board control, remuneration committee, and top management compensation. Academy of Management Journal 41 (2): 146-157.

Cotter, J., A. Shivdasani, and M. Zenner. 1997. Do outside directors enhance target shareholder wealth during tender offer contests? Journal of Financial Economics 43: 195-218.

Dalton, D.R., and C. M. Daily. 2001. Director stock compensation: An invitation to conspicuous conflict of interest? Business Ethic Quarterly 2 (1): 89-108.

Demsetz, H. and K. Lehn. 1985. The structure of corporate ownership: causes and consequences,

Journal of Political Economy 93: 1155-1177.

Eisenberg, T., Sundgren, S., and M. T. Wells. 1998. Larger board size and decreasing firm value in small firms. Journal of Financial Economics 48: 35-54.