Developing Digital Content Industry

in

Taiwan

Yu, Hsiao-Cheng; Tsai, Hsin-Hann

National Chiao Tung

University,

GraduateInstitute of Management ofTechnology, Taiwan,

ROCAbstract-According to predictions by

PriceWaterHouseCoopers in 2004, the average global annual growth rateof digital video & audio products (VOD, MOD., etc) will reach 235%, wireless contents will reach 91%, and digital archives will reach 84%. This is due to the advancement, cost

reduction and availability of the enabling technologies e.g. digital processing, digital storage and digital telecommunications. The development of Digital Content Industry (DCI) requires fine culture, initiative ideas, respect of intellectual property (IP) rights, and telecommunications infrastructure, which are all very dependent on government supportive policies. This study summarized the government policies, progresses, and obstacles in the development of Taiwan's DCI. Comparisons with those in other countries, including the U.S., EU, Japan, and Korea will be provided. Taiwan DCI's opportunities and challenges will be discussed; strategies and recommendations will be provided based on

Taiwan'suniqueresourcesandcompetitive advantages.

I.INTRODUCTION

The era ofknowledge-based economy is different from other ICT industries and past ones. These industries

emphasize knowledge innovation and rely on the different agents of production: technology, knowledge, innovation

capacity,andhigh-intense capital. Inthisperiodoftime,the

speed of innovative technology and initiative ideas are the

key success factors because the period of validity of

knowledge is not fixed (ever changing), and the mass

production of commercial products are needed. A fast

development ofnew knowledge and innovative technology canaccelerate the rotation ofexisting goods and the speed of

production can become faster as new knowledge brings in

new technology. As a result, technology and products that

are rapidly rotated will be led to fierce competition among

enterprises.

The characteristics of knowledge-based economy that

enterprises should adapt to are broken down into three

categories. First is the acceleration of innovation. In knowledge-based economy, the speed of innovation in

enterpriseshavetobe faster than theircompetitors inorderto dominate in the market and to gain enough returns before competitors can promote a new knowledge product.

Acceleration can save the cost of working and increase the cash flow. Second is the difference with ICTindustry. The main stream ofindustry inknowledge-based economy is the focusonIIS (Innovation intensiveservice, Chen, H.C., Shyu, J.Z. [1]), i.e. the enterprise leverages the market domination

through innovative technology anduses new service models

to develop diversified products, services, and market

expandability. Lastbutnot least,this posture ofindustry in

knowledge-based economy is considered a pioneer and a

radical innovation process [2][3], and the industrial environment is highly dynamic, hostility, and low

heterogeneous.' Hence, the enterprises in this environment are profited by continuous innovation and diversified products.

In digital content industry, these industries digitalize pictures, texts, videos, audios, and data compiled as one, which differs from other ICT industries. These pictures,

texts, videos, audios, and data are integrated by being digitalized to become new products or services. Compared

with other ICT's value-chains, digital content is a creative industry that is undergoing rapid changes. Many creative

companies and organizations are already engaged in the production and distribution of Digital Content because of the

general usefulness of new technologies. These companies are increasingly being used in traditional industries, thus

blurringthe definition ofsome sectors. [4]

The development of digital content industry relies on creative ideas and innovation, including content and

technology. Therefore, the driver of profit from digital contenthas to be done through ongoing content innovation;

i.e. the creative companies that provide fresh contents are

playingthe moreimportantroles. Taiwan's governmenthas declared that digital contentwill be the highest value-added andcompetitive industryinthe future and willidentify digital content asthe "star" coreandpotential industry for Taiwan's economic developments in knowledge-based economy. There are numerous fields indigitalcontentand the niche for Taiwan's creative industry shall be discussed in this study.

The following topicsare divided into 6 sections: section II is the model of innovation and profit

chain,

section III willanalyze the digital content industry, section IV is the Taiwan'sdigitalcontentposture inglobal market,and section

Vwill conclude these discussions.

II.INNOVATION IN KNOWLEDGE-BASED ECONOMY

The characteristics of knowledge-based economy are progressive technology, intensive knowledge capital input, and innovation. These factors are known to be the crux of industry. Comparing with ICT sector, the emphasis of

industry inknowledge economy is not costreduction or the scale of economy. In contrast, thecontentis also the existing

factor which includes the determinant and the acceleration of

contentinnovation.

Dynamism indicates therateofchangeintheindustry, the unpredictability of the behavior of customers and competitors and the shifts in the industry's technological conditions. [5]. Hostilitycreates anunfavorable

climate, featuring intense competition for limited resources or market

opportunities. [3]. Heterogeneity indicates the diversity of the market

A. Thetransitionofindustry

Technology innovation that dominates market advantages is the goal for ICT sectors for either hardware or software. For ICT sector in developing countries, the capacity of manufacturing is the index for evaluation, but in industrial countries, such as the United States, Scandinavian nations,

and Japan, the focus is on R&D expenditure. However, in recent years, OECDhas declared the forthcoming of the era ofknowledge-based economy. The ICT sector will aim for knowledge capital instead of traditionalproduction factors, [7] therefore innovative intensive service providing will be the mainstream of ICT sector instead of manufacturing with creative industries. The creative industries aim at content providing and continuous innovation,but aim differently with R&D expenditure because of the rating of innovation [8] [9] [10][1 1], includingthe EU Innovation Scoreboard.

According to the British government's Department of

Culture, Media and Sport defines creative industries as

activities that have their origin inindividual creativity, skill,

andtalent,whichgivesapotentialfor wealth andjob creation

throughout the generations and exploitations ofintellectual property.These include the followingkey sectors: advertising,

architecture, artandantiques market, crafts, designs, designer fashion, films, interactive leisuresoftware, music, performing

arts,publishing, software, television,and radios [12][13]. The status of creative industries developmentsreflects the score of knowledge economy and digitalization. The production of creative industries isknowledgeandinnovation,

whichare intensive and have aesthetic activity [13]. Hence it is not like other ICT sector's productions that can be mass produced and pursued for cost leadership and also aim at market orientation and customers' needs, which is the way toward customization. There are a lot of fields in creative industries, and each one has the ability to become the dominant proportion in this industry. The diversity and

uniquenessare also characteristics of this industry, soit isan advantage for small-medium sized countries that need

Internaliqou noQvation

development like Taiwan, Korea, and South East Asian countries. Since creative industries provide services and products made by ideas innovation, the profit model is different with other ICT manufacturing value-chain and will be discussed in thenextparagraph.

B.Profit chain ofInnovation

Innovation can be regarded as the providing of new services and products through the use of new knowledge,

which includes invention and commercialization in creative industries. [14] The crux of innovation lies in the

accelerating speed of knowledge that is being created and accumulated. [7] A related characteristic of knowledge

economy growth that has become increasingly evident from theearly 20thcenturyand onwards is the growing importance

of intangible capital (also called intellectual capital). In

total productive wealth and at macroeconomic levels, the rising relative share of GDP attributes to intangible

capital.[15] Intangible capital basically falls into two main

categories: services fordigitalized contents(in movie, mobile,

radio, etc), and added-valued application products, such as

digital archives, publications, e-book, etc.

The profit of creative industries mainly comes from

intangible capital, which is different from ICTgoodsthat can be priced by the market. The value of ideas is subjective

and differs greatly with the production orientation strategy.

Corporations should offermore innovativeproducts, services, ordiversifiedgoodsforearning higher profits. Accordingto

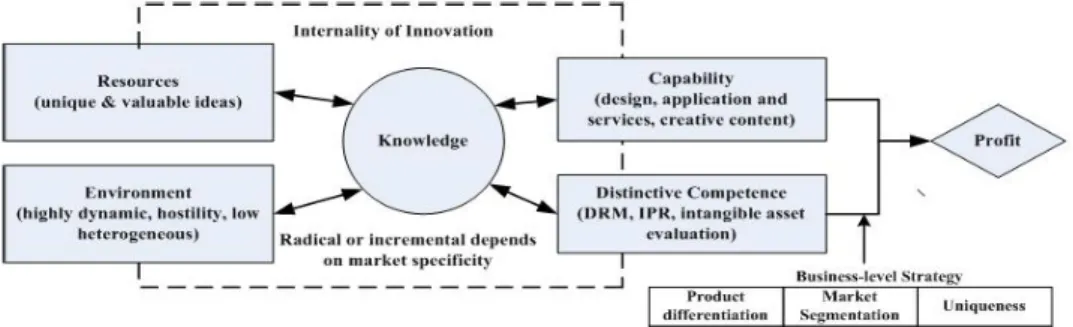

the profit-chain offered by Afuah [14], knowledge (idea initiative) is the mainkeysuccessfactorcorporations relyon, and this represents the "distinctive competence" and

"capability",whichcan satisfymarket needs andcanseparate itself between other competitors. The environment of creative industries is highly dynamic, hostile, and low

heterogeneous, so the profit-chain of this industry can be shown below.

CapAbifity~~~~~Prfi

fdinendatpio Segmnation

and

-Radlea orinfrtmentaldipe'ends

unmnarketspechiflity

Fig.1.Profit-Chain of InnovationinCreative Industries

III. OVERVIEW OF CREATIVE INDUSTRIES

Uniqueness

and initiativecapability

are stressed in creative industries, and scale ofproduction is not the maingoal for corporations; i.e. the success in this industry is determinedbythe acceptance ofproductionfrom themarket,

hence, small-medium sized countries can establish the

competitive advantages in this area like Taiwan, Singapore,

Hong Kong,NewZealand,Korea,etc. As ScottandStorper

[16] observe "there is mounting evidence that creativity and

learning have a distinctive geography, with regions playing

cumulatively significant improvement in industrial products and processes". The creative industries have all the characteristics of high-tech industries. They require a well-developed ICT infrastructure to serve their clientele and interaction with an IT manufacturing base to create and target

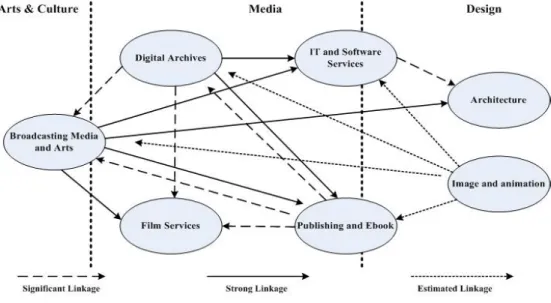

theirproducts. Creative sub-sectors, such as the process of movie making and electronic games, depend on local and international networking in order to develop commercially successful products that enhance their market prospects. The nature of such localnetworking is presented below.

_ _ _ _ -F 0 ____ ____ ____ ___*

Slgnihtkant Liikage StragLinkiage EstlimatedLinkage

Fig.2.Networkingamongcreative industries

Source:Yusuf, Shahid, and Nabeshima,Kaoru,[17]; modifiedby author

A.Definition and market scale ofDigital Content Industries Being highly export-oriented and dependent on personal

contacts with buyers, reliance of creative industries on

networking is greater than manufacturing firms.[17] Cultural-products industrial agglomerations around the world

are becoming increasingly caught up with one another in global webs of co-productions, joint ventures, creative

partnerships, and so on. In this manner, productive

combinations canbe established andcandraw onthespecific competitive advantages of diverse clusters without

compromising the underlying force ofagglomeration itself. [18]

1) Definition of Digital Content Industries

Creative industries can also be called Digital Content Industries since products from them are made through digitalization and involve the form ofcreativity. A recent

European study defines the Digital Content Industries as

"including net-business which delivers digitized information (text, data, image, audio, and video)." The core of the

Digital ContentIndustries can be identified as the converged

traditional media sector, e-publishing,anddigitalaudio visual industries. While the former Digital Content Industries

produced digitized text, data and images, the latter Digital

Content Industries focuses on digitized television, voice and video sequences. [4]

2)The scaleof digitalcontentmarket

The creative economy and Digital Content are closely

connected. As noted above, identifying those that make an

industry successful is defining theindustry. Another way of looking at Digital Content is to identify those parts of the creative economy that are digitized, or becoming digitized. Most of the activities are identified as being in the creative economy that uses digital inputs or produces digital goods

and services to a greater or lesser extent. The least digital activity in the list is most likely craft. Activities, such as

software and video games,are nowalmostuniversally digital,

while the transacted part of activities, such as music, are becoming heavily digitized (where CDs and DVDs now dominate, although there are still significant sales of vinyl records, which are considered analogue forms). The

challenge is in determining what proportions of these activities have beendigitized.

According to the statistics forecasting for global entertainment and media market, the scale of market of DigitalContentIndustries has reached 1.13 trillion US dollars and will continue to growto 1.18trillion US dollars in 2004. The semiconductor industries are only at 0.215 trillion US

dollars, 1/19 comparedtoDigitalContentIndustries. Figure

3 and4 arepredictions ofDigitalContentIndustries inglobal market, and one noticeable point is that Digital Content Industries in Asian countries are growing rapidly, and the

figure shows that these small-medium countries build their

ESAsia

Pacific

1,400,000

1,200,000

1,000,000

mim_

800,000

600,000-

400,000-

200,000-0

=E

EU

E

U.S.

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Fig.3.Forecasting the scale ofDigitalContentIndustriesinglobal marketSource:PricewaterhouseCoopers,2004 -=---ThemeParks -X- Magazine -+- Radio *- TV Networks 250,000 200,000 150,000 100,000 ... , 50,000 0 *-Consumer books -- -Video Games _-eoRecorded Music FilFim * N ews paper - -Internet Advertisement TV Distribution (unit: $ millions) 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 Fig.4.Forecasting the scale ofDigitalContentIndustriesineachcategory

Source:PricewaterhouseCoopers,2004

B. Profit-chain ofDigitalContentIndustries

Digital Content is about creativity. Digital Content is about assisting creative processes throughout the economy because it accelerates the spread of ideas. It makes ideas, knowledge, and information easier to store, distribute, and

access. As mentioned above, the investment of Digital

Content Industries are almost intangible capital and substantial financial support. Venture Capitalin ICTsector

has been developing for many years, but the VC forDigital

Content Industries is still in an initial stage. ICT sectors

pursuethe costleadership and market demands,therefore, the investment in ICT manufacturing profits quickly from the market. However, Digital Content Industries are different from ICT sectors since the products of this industry are

unique, diverse, and not mass produced. The most

important point about Digital Content Industries is that idea initiatives emphasize quality and market acceptance, hence the time horizon will belonger than manufacturing and return

of investments.

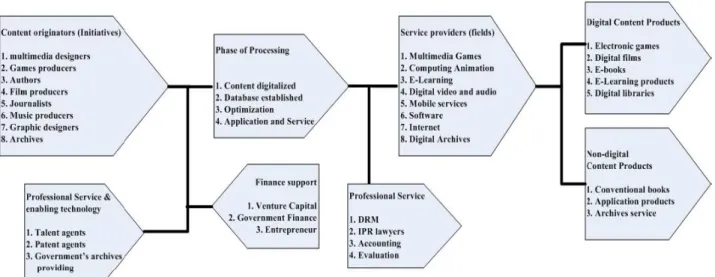

The profit chain of Digital Content Industries contrasts with ICT manufacturing in that the profit-chain of digital content is a kind of "value innovation" that focuses on content, which is not like an assembly line that occurs in manufacturing. In the following graph, the profit-chain of Digital Content Industries is shown.

Fig.5.Value-chain ofDigitalContentIndustries

Source:MIC, 2005; modifiedby author

IV.TAIWAN DIGITAL CONTENT'S STATUS

Digital Content Industries (DCIs) in Taiwan include

categories, suchasvideos, games,publishers, andlearning by applying sides, which also discriminates core and staff industries. Core industries use applications, such as video and audio, computing animation, multimedia games,

e-learning, mobile services and digital archives. Another

applicationis staffindustrythat includes contentsoftware and

internet services. The production value of Taiwan DCI in 2003 has reached 1983 billion NT dollars and is expectedto

exceed over 2300 billion NT dollars in 2004. [19] and the average annualgrowthrateshave been 22%. [17]

Accordingtothe statistics from MOEA, the companies in DCI are in the range of around 1600s and are expected to

grow to over 3000. There are about 33 thousand employers

and will most likely expand to about 40 thousands thereby offering more working opportunities. In application and

services, the export ratio of DCI inproductionvalue is 12% now, yet the DCI companies predict that this number will continuetogrowto30%.

A. Governmentkpolicyfor development

Digital content index can measure the level ofanation's

knowledge economy and digitalization. It can not only improve traditional ICT sectors and the intensity for

knowledge, which resolves in higher added-value, but also enhance Taiwan's DCI'scompetition advantagesintheglobal

market. For this reason, Taiwan's government has declared that DCIs are one of "Two trillion and Twin star industries" and has startedto pushrelatedpolicies and bills that include the environment, human capital, financial support, R&D,

global marketing, and applications. First of all, "Digital

Content Industries Promotion andDevelopment Office" has beenprogrammingthepoliciesandstrengthening cooperation

between industries and academic institutes. Second ofall,

the government has created "Digital Content Institute" for

developing human resources for industries and cooperating

with universities. Third ofall, it promotes the "Center for evaluation ofDigitalContentand investment services." The value ofdigital content has yetto become the standardprice

in the market, so the evaluation center will offer objective pricing services for allintangible assets. Fourth of all is the

offering of service for loan orfinancial support. Lastbutnot

least is the offering of national archives (including pictures,

arts, historian source material, metadata, etc.) to companies

for add-valued applications, like the worthy Chinese

drawings that are appliedon the decorations, handkerchiefs,

tableware ordishware. These drawings are very popularand

arehighly acceptedininternationalmarket.[19]

In aglobalizing world,government policy hasto compete

need to capitalize on existing opportunities that are likely to

emerge, but also contribute to the future dynamism of these companies. The question facing major cities that seek to

strengthen innovative capacity is what kind of models they

can use as points of reference, what kind ofmeasures they can take to enhance attraction for firms, and, particularly, how to create clusters of industries and services that can

accelerateanindustriesgrowth.

Governmentsplay an important roleinDCIs becausethey are highly uncertain and intensive capital investments, like

filmproducing ormusic, database establishing, etc.Theseare

notpossible for justa few companies tohandle. Therefore, in the early stage of industry development, governments

should have established the mechanism for assisting DCIs, like policy guidance, financial support, enabling technology imports or transferring, or community formation. DCIs

need amount ofcapital investment, and, most definitely, the

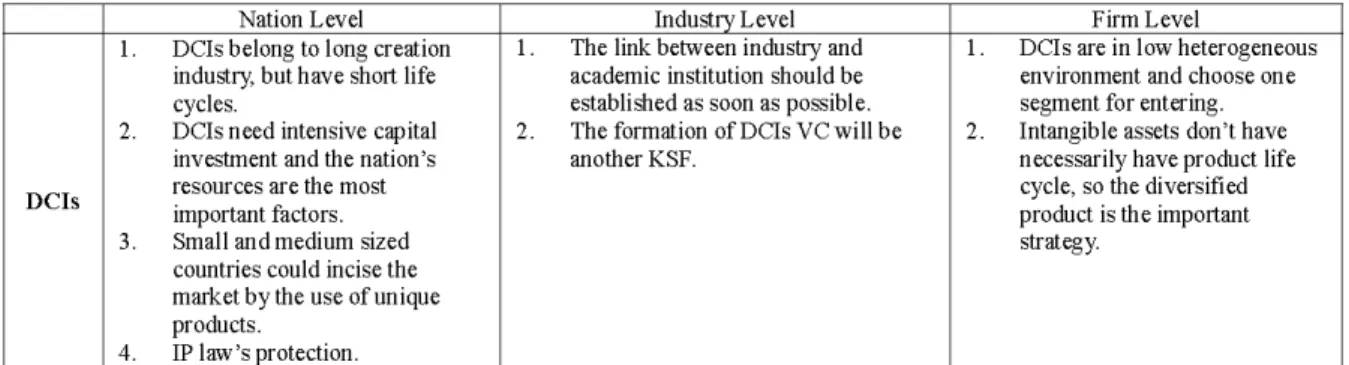

time horizon ofreturning investment. Accordingto the locus of industry leadership, these ways can define the DCIs'

strategies, which are broken down into three levels: nation,

firm, industry, and comparison between Taiwan and others

countries' policies for understanding the differences in strategy. The locus ofindustry leadershipisexplainedinthe

followingtables.

Taiwangovernment's DCIpolicy is divided into six main

parts and 27issues, and thepolicy framework is constructed

on the specific technology it is setting rules for. Taiwan

DCI policy tries to be well-rounded and invests a large

amount of money for improving the industry development.

However, from the locus ofindustry

leadership,

the DCIs arein an indefinite situation and is still immature; hence, the

DCIs are not like other ICT products and should therefore

follow a standard, which fulfills applications oftechnology.

Therefore, it needs intensive capital to be the pioneer that

ventures into the market. DCIs market has both "clear

market segmentation" and "distinctive competence," which is becoming the two most important factors for producing uniquecontent. Becomingthe first countrytomoveinto the

market, Taiwan's policy strategies aretoinvest in technology

exploitation, creative human resources, and global market

promotion. Not only do related policies subsidy for new

start-up companies in DCIs, but also convenes the

relationship between industries and academy, like "Technology Development Program in Academia," and "Industry-academia Corporation Platform."

In financial support, the venture capital in Taiwan differs from that of the U.S. and other European countries. These countries positively encourage newstart-up companies; even

the companies aren't as strong as the other more stable

companies. The companies inDCIs or cultural creative are

mostly small and medium sized and are short on funds for

R&D and innovation. At that time, the DCIs were to be

regarded as the national's level industry, and the government

hadtoraise the financialsupportfor these creative companies. The strategies of MOEA in Taiwan are to raise the fundsby

government, which includes tax incentive, loan support,

introducing foreign investment, and different industries alliance. They also wish to improve the constantly growing industries.

Nowadays thereare alot ofcountries, liketheU.S., U.K.,

Japan, East Asia, Australia, India, etc. that are actively

developing and promoting the DCIs because itcanhelp push

and pull on growing industries, especially the more

traditional ones and ICT sectors because digitalization needs

innovative technology to work efficiently. However, there

are many fields that are included in DCIs and depend on

limited resources. Governments should seek for a proper

strategy to develop the most competitive industry. A good example of this technique is the U.S.. The country owns the

film'sproduction technology, market,channel, and ideas, and

this is the oneadvantagethat other countries haveahard time

competing with, especiallysmall and medium sized countries, like Taiwan, Singapore, Korea, etc.. In Innovative Intense Services (IIS), dominatingasection is verydifficult for small

countries, but Taiwan's semiconductors industriesare leaders

intheir fields.

TABLE1.LOCUSOFINDUSTRYLEADERSHIP IN DCIS

Nation Level Industry Level FirmLevel

1. DCIs belongtolong creation 1. Thelinkbetweenindustry and 1. DCIsareinlowheterogeneous industry, but have short life academic institution should be environment and chooseone

cycles. establishedas soon aspossible. segmentforentering. 2. DCIs need intensivecapital 2. The formation ofDCIsVCwill be 2. Intangibleassetsdon't have

investment and the nation's anotherKSF. necessarily have product life

DCIs resources arethemost cycle,sothe diversified

important factors. product is theimportant

3. Small and medium sized strategy.

countries could incise the marketby theuseofunique products.

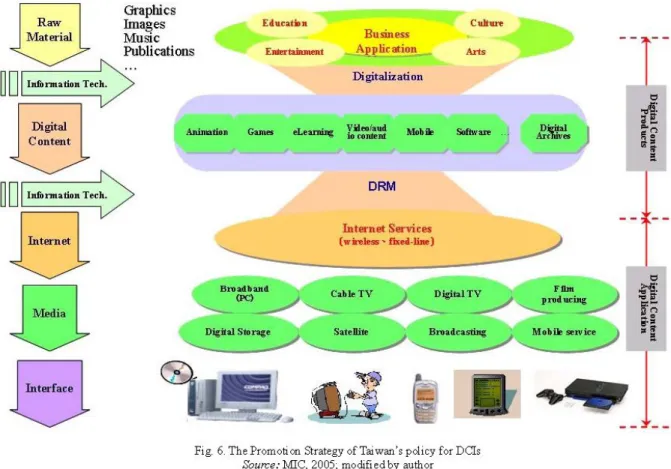

RaW

TJmage§

MAteiOfal Muisic Pijblicatims WlItn.fnitio Tech I 7'1~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~ I Xniif lDimFig.6.The Promotion Strategy of Taiwan'spolicy forDCIs Source:MIC, 2005; modifiedby author

TABLE2. INTERNATIONAL DIGITAL CONTENT POLICIES

Canada Korea Japan U.K. Taiwan

Public CH MCT & MIC MITI DTI MOEA

Promotion Telefilm Canada KCIPC

|Institution | NFB | KIPA DCAJ DCF DCPDO

Institution NFB KGDI

TV, FilmandNew Games, Cultural Games,Software, TV,Film, Games,Animation, media Content,Digital Film,Music, Publications. Video/Audio,

Emphasis content Publications, Internetservice,

Services. Digital Archives,

Software

Source:MOEfA, 2004

B. Focus on Taiwansniche

InTable 2, it isclearlyshown that countriesemphasizethe

development ofDCIs the most ontheir own vantage points

because of the limitation of the nation'sresource. Itis hardto coverall fields, but theenablingtechnology is thekey factor

forindustry developments. The

enabling technology

canbedivided into two parts: one is industry used in technology,

like appliedsoftware orvideo/audiotech,anddigitalized tech;

two is interface technology, like hardware,

telecommunications, and internet infrastructure. As the

Korean policy states, the government plans to invest about 6100 Korean dollars on the multimedia technology-support centerfordevelopingVirtualRealityandComputer Graphics technology to improve on-line game's quality thereby attracting more players. That is also why theU.K. focus on publications and media since they have a large amount of archives andaflourishingmediaindustry, and these are good

foundations for developing DC. These policy decisions show that inDCIs, evenleaders intechnologylike theU.S.,it is hard to achieve a goal such as "winner takes all." Each country has to put their limited resources on the most

efficient itemtobringinasubstantialamountofprofit. The theory of locus in industry leadership clearly defines

the DCI'spositionandsituation, and like thedevelopingtech and bio-chips, this kind ofindustry is still in the process of

growing and contains many risks, therefore, can the

development of technology accompany with the industry growing? DCPDO(Digital Content Promotion and

Development Office)[20] has investigated and analyzed

Taiwan's environment and policy for developing DCIs, and

throughthe expert's andcompanies' opinions, they presented areport about the KSFs of Taiwan'sDCIs. Inthis study, the report is used to compare with the status quo of the global market, and the expert's opinions and analysis of the risks of

these factors are shown in the following. In this study, it assumesthat there are numerous variables foranalyzing these KSFs. High risks indicate that it is not the right time to

develop this issue inTaiwan, and it is known thathighrisks also mean that this issue is in high dynamic and hostility.

Lowrisks are more adequate for Taiwan's status quo and can gradually be developed. The vantage point means that it is the critical factors that have the ability to easily influence the

developmentsofindustry.

TABLE3. THE ANALYSIS OF DCIS' KEY SUCCESSFACTORS(KSFS)INTAIWAN

Issues KSFs High risk Lowrisk Vantage Point

Digital 1.established fixedusers /

Video/Audio 2. killer application software /

Application 3. human resource incubating

Games 1. encourage new start-ups /

2. has to be creative content Animation 1. technology development

2. creative ideas andtopic

eLearning 1.usefulcontentandeasyuse /

2. should expand the target of application Mobile

service

1.broadband infrastructure2. content and service renewal 1.incubating human resource

Software 2. Corporation with foreignsoftware producers 3.key and most userssoftware exploit

Internetservice 1.well-done infrastructure(high speedandcapacity)

2. mature userscommunity 1. rich raw archives or materials

Digital Archives 2.applicationand servicespromotion 3. global marketing strategy

4.continuouscontentinnovation Financial

aSupportn

1.governmentpolicysupport2. loan incentives / /

upportS3.VC m

Source:DCPDO, 2005;modifiedbyauthor

FromtheanalysisinTable 3, the wholeDCIsenvironment has existed as a high risk in

Taiwan,

and the governmentshould choose the profitable fields to invest, like Korea's

emphasis is simply on internet services and on-line gaming

enhancement. Immoderate divergent resources allocations

arethe cause forinadequate industries development, and can

also postpone the time for theproducts' to enterthe market.

In fact, DCIs need the demand side market orientation and the acceptance of ideas to decide the viability of digital content companies. Some fields like Digital Video/Audio, DigitalGames, Software,andInternet Services,arealmost all in high risk, and these fields need fresh ideas; otherwise, it will be difficult to get a high added-value. Moreover, the broad market size will be ableto ensurethe survival ofDCIs,

and Taiwan's domestic markets are constrained and export orientation canhelp solve these problems; hence, the human

resources incubating and management will also be a large

investment. Therefore, Taiwan'sgovernmentshouldponder

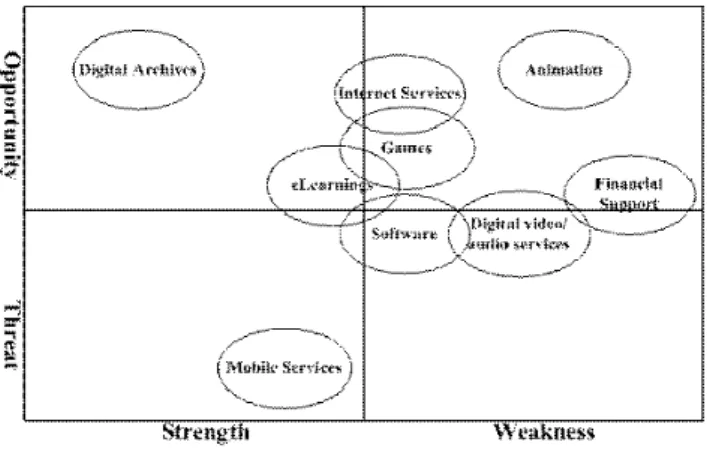

pmthese issues inpolicydecisionmaking. Inthisstudy,the SWOT analysis ofDCIs from the research of KSFs is shown below.

Fromthe SWOTanalysis, itcanbe concluded that Taiwan

DCIs obvious advantages are the opening of the China market and the linguistic familiarity. The China market has

a high acceptance for new innovative commodities, and the

Olympics Game 2008 is coming soon, so the national pride

has beenrisingand it doesn'tmatter ifthe person is Chinese

or a foreigner,bothare enthusiastic about Eastern Culture. It

will be a very good opportunity to promote Taiwan's DCIs

through different fields. Moreover, DCIs need creative human resources or talent agents, and the most important

factor is the aesthetics incubating for innovation. DCIs are

like "artifacts imbued withimaginativeaesthetic and semiotic

content."[21] Although there are some universities or

institutions doing arts, the relationship between arts and industries are seldom built on, causing a shortage of innovative talent supply and a source of innovation. Another point is that the limitation of domestic market size and lack ofemphasis on the demand-side of the market are problems DCIs have encountered. DCIs products are high-value added when comparedto ICTs', but the demand side is limitedbythe market scale andcan not beexpanded. Thus, theglobal marketing strategy andgovernment support.

Lastly, the government should have a focus strategy on the most profitable field because each issue of DCIs needs

enormouscapitalinvestments

After analyzing the information, it clearly shows the

advantages and disadvantages of Taiwan's DCIs, and also indicates which issues will be more proper for Taiwan to develop. Digital Archives and eLearnings are more advantageous than other issues because of its low risk and

popular materials for doing applications and services. SWOT matrix for analyzing the issues' position in DCIs is

TABLE4. SWOT ANALYSIS OF TAIWAN DCIS

Issues Strength Weakness Opportunity Threat

1. Creativefilm 1. Small domestic 1. China would be the 1. Channelsareownedin Digital producer market target market U.S. or others. Video/Audio 2. Linguistic 2. Enabling tech. hard 2. VOD's usage is 2. bad film producing

Application familiarityin film todevelop growing environment

Application

~~~~~~~3.

Lack of sufficientcapital

1. PCpenetrations 1. Lack ofenabling 1. The ratio ofPChas 1. Koreahasdeveloped arehigh tech. forquality. beengrowingin on-linegamewell.

2. Low costfor 2. Insufficient ideas for China. 2. DRMwill beaserious

Games producing creating 2. On-line game will problem in China. 3. Lack of capital become the

4. Lack of TV games main-stream

experience

1. OEMfrom 1. Lack of creative 1. Internal demand 1. Lack of aesthetic internationalfilm ideas. has beengrowing education

company. 2. Smallcompanies inChina. 2. Government supportis

2. Skillhas lack talent and 2. 2008Olympics is insufficient.

Animation advantages capital. coming. 3. Korea'shas been

3. Lack oflong-term 3. Corporation with mature.

incubation international

companies for entering China.

1. Large amountof 1. On-line 1. GlobalCAGRis 1. China hascooperated

producers. authorization hasnot growingrapidly. withcompanies

2. Government passed the 2. China market has (SmartForce)for

eLearning policysupport legislation. opened. expansionof domestic

eLearning 3. Leading posture 2. The usage habits 3. Integration of market.

inChinese didn't build. contentin many 2. "On-Line School" has

linguistics. 3. Small domestic fields. openedinChina

market

1. The holder of 1. Where is the 1. Chinesecontent 1. I-mode haspenetrated

ratio of cellular platform? could bepopularin into the world market. phone has been 2. Standard is owned China. 2. Integration of software

Mobile service over

107%.

byenterprises.

and hardware.2. 3Ghasopened. 3. Content resources areseriously insufficient.

4. Lack of database.

1. Fullexperience of 1. Lack ofR&Dability 1. Broad Chinese 1. India&China producing 2. Lack ofmanagement linguistic market positively developed

Traditional ofsoftware 2. Government softwareindustry.

Software Chinese version 3. Lack ofmarketing bridgesthe local 2. Full talentpoolof software. strategyand and international other countries.

2. Agent of software experience companies.

1. Infrastructure 1. Mechanism of 1. Wireless has been 1. Strong

well-done. E-commerce notyet popular. competitivenesswith

Intres2. Usage ratio has established. 2. China internet intl. mainenterprise.

beengrowing 2. Internetsecurity infrastructure has 2. Where isprofit

rapidly. 3. willingness for beenrapidly model?

on-linepayment established.

1. Linguistic 1. small scaleeconomy 1. Application and 1. Usage interface familiarity 2. DRMprotectsthe servicescan integration 2. Popular materials IP. rapidlypenetrate 2. marketingstrategy

Digital Archives 3. manyPublishers 3. lack ofplatform the market.

4. Government 2. Thenewmarket of

policysupport China hasopened.

Fig.7.SWOTmatrix of TaiwanDCIs

C. Discussion

With China opening their market to the world, the Chinese will become the largest group ofinternet users, and the content points out Chinese will help the market grow at

double the speed. DCIs have the cultural compatibility and

uniqueness, so it is the vantage point for Taiwan's DCIs

developingto become thepioneers of China'sdigital content

market. Globalization forces China to enter the information

technology era. Meanwhile,the infrastructure andtechnology

are rapidly growing; furthermore, the ratio of users of information technology is becoming much higher. These are the factors and conditions that foreign companies positively invest capital and human resources in. For example, Hong Kong, it is the transition center for globalization of culture, but the small scaled economy can lead to an expansion ofDCIs into the market. Yet, Taiwan has the vitalposition and has more creativeabilitythan others. Therefore, Taiwan has the potential and opportunities to

explore China's market and eventually entering the global

market.

Taiwan has the crux channel of Chinese digitalcontent, and the culturalsimilarity canhelp Taiwan DC companies to

do verticalintegrationmore easily: from creation to channel, toinverse the traditional value-chaintocapturethe dominants of the market in order to defend the Western countries

monopoly. During that time, Taiwan's government should

help the DCIs to build up the global marketing strategy systemandcreatesufficient financial support.

Afteranalyzing DCIs issues, for more efficientresource utilization, Digital Archives andapplication and services are to befirst priorities inthe process ofpolicy making. Digital

Archives is one part ofDCIs, but it will offer the wholeDCIs developmentanimportant database. Application and services become high added-value products or services and will

expand to other issues by offering new ideas and creation. Traditional archives' applicationand servicesare likereplicas

of famouspaintings orarts,but thedigitalization willrapidly

increase the value of these archives, likeprinting thesymbol or signs of Chinese paintings onto wallpapers, cards,

counterpanes, or other decorations. Even the price of those

can become higher than that of before, and the most

important factor is that many people will collect these products by paying a higher price.

The goal of Digital Archives is to prevail and diffuse the

exquisiteculturalapplications. The arts have theiruniqueness,

so the market segmentation will be very obvious and the

companies could offer differentprices and levels ofproducts

to dominate the market. For the overall effect, Digital

Archives will have a two dimensional influence: one is on human and social science.[22] It means that through the Digital Archives applications, aesthetics will be combined with the technology for education and mold the palate for

spurringthe new ideas andinnovation; twois on theindustry

and economy. Digital Archives can transfer cultural heritage into valuable information and commodities, and it would be the accommodation for digital databases like

developing animation, software,orfilmproducing.

Nowadays, the composition of Taiwan DCIs is almost made up of SMEs, but lack industry leadership. Though SMEsareflexible anddevelopingtheirownunique products, they have difficulty facing the challenges of international

companies. Consequently, the government should assist

Digital Archives companies to establish a transaction platform to refer the archives to products added-value then distribute themtothe channels.

I I

Fig.8.Transaction Platform ofDigital Archives

V.CONCLUSION

The output ofDigital Archives has offered the DCIs an amount of materials and database. Taiwan is locatedat the critical position for the transition of Chinese content.

Taiwan has the potential human resource and enough raw materials; however, it is a lack of a well-planned policy to

promote the Digital Archives. DCIs in Taiwan have many factors and barriers to break, like resource allocation, financial support, technology innovation, etc., and the most importantfactor is theexplorationof customers' needs. For

this reason, there are two considerations for promoting Digital Archives;the first consideration is the inducement for

industry and customers' needs, and the other is the

improvement of environment. First of all, the

government

should understand the industries needs and bridge therelationship between industries, talents pool, and market. The output ofDigital Content is verysubjective andunique, so the mechanism of value-identification should be established

Lastly, the improvement of environment is focused on the

policy making. DCIs are the high capital intensive and the government has to assist the development of the industry by policy support, especially the financial support and the government should establish a transaction platform for the capturing of resources and output promotion. DCIs are the main leading and incubating industry in Taiwan's economic plan and invest much of its time on the relationship between the government, industries, and market. The market should be well-done and will have more competitive advantages inthe global market.

REFERENCES

[1] Cheng, H.C. and Shyu, J.Z., "Innovation Intensive Service as actors

of Platform StrategyAdaptedtoEmerging IndustryDevelopment,"in PaperspresentedatPICMET'04, 2004.

[2] Shyu, J.Z., Cheng, H.C. and Lei, H.C., "Interlinking the National Systems of Innovation andKnowledge Economy", Sci-Tech Policy

Review, Science and Technology Information Center of Taiwan,

2005.

[3] Zahra, ShakerA.,"TechnologyStrategy and Financial Performance: examining the Moderating Role of the Firm's Competitive Environment," Journal ofBusinessVenturing, 11,pp.189-219,1996. [4] Allen Consulting Groups, Digital Content: Creativity plus

Connectivity,Australia,2003.

[5] Zahra, Shaker A., "Environment, Corporate Entrepreneurship, and Financial Performance: aTaxonomicApproach", JournalofBusiness

Venturing,vol.8(4),pp.319-340,1993.

[6] Zahra, Shaker A., "Predictors and FinancialOutcomes ofCorporate Entrepreneurship: An Explanatory Study," Journal of Business

Venturing,vol.6(4),pp.259-285, 1991.

[7] OECD,Innovation in theKnowledge Economy,OECDPublications, Pariss,2004.

[8] Griliches, Z., "Patent statistics as economic indicators: a survey," JournalofEconomic Literature, 28, pp. 1661-1697, 1990.

[9] Griliches,Z.;R&DandProductivity: The Econometric Evidence. The University of Chicago Press, Chicago, 1998.

[10] Hausman, J., Hall, B.H. and Griliches, Z., "Econometric models for count data with an application to the patents R&D relationship," Econometrica, 52, pp. 909-938, 1984.

[11] Hitt, M.A., Hoskisson, R.E. and Kim, H., "International diversification: effects on innovation and firm performance in

product-diversifiedfirms," Academy ofManagement Journal, 40, pp.

767-798,1997.

[12] DCMSCreative Industries TaskForce, CreativeIndustries:Mapping Document, DCMS,London,1998.

[13] Drake, Grahm, "This Place gives meSpace: Place andCreativityin

the CreativeIndustries," Geoforum, 34,pp.511-524,2005.

[14] Afuah, Allan, Innovation Management: Strategies, Implementation,

andProfits, Oxford University Press, Inc., 1998.

[15] Abramovitz, M. andDavid, P.,"American Macroeconomic Growth in the Era of Knowledge-Based Progress: The Long-Run

Perspective,"An Economic Historyof UnitedStates: The Twentieth Century. 3,Cambridge UniversityPress, NewYork,pp.1-92,2000. [16] Scott, A. J. andStorper, M.,"Regions, Globalization,development,"

Regional Studies, vol.37(6-7),pp.579-593, 2003.

[17] Yusuf, Shahid and Nabeshima, Kaoru, "Creative Industries in East

Asia,"Cities,vol.22(2),pp.109-122, 2005.

[18] Scott, A. J., "Cultural-products industries and urban economic development:Prospectsforgrowthand market contestation inglobal context.",Working Paper, CA:University of California-LA,2003. [19] MOEA, WorkingPaperofTaiwanDigitalContentIndustries, MOEA,

Taiwan,2005.

[20] DCPDO, Working Paper of Taiwan Digital Content Industries,

MOEA,Taiwan,2005.

[21] Scott, A. J., The Cultural Economy ofCities, Sage Publications,

London,2000.

[22] Hsiang, Jieh; Chen, Hsueh-hua; and Cheng, Dun-fung, "The Forecasting of Digital Archive's ApplicationinIndustry", conference by MOEA, Taiwan,2002.