i

國 立 交 通 大 學

企業管理碩士學位學程

碩 士 論 文

PT. SINAR MAS AGRO RESOURCE AND TECHNOLOGY Tbk

於棕櫚油業的買家和供應商關係

BUYER AND SUPPLIER RELATION IN PALM OIL FORESTRY IN

PT. SINAR MAS AGRO RESOURCE AND TECHNOLOGY Tbk

研 究 生:Ronny Kurnia

指導教授:黃仕斌

ii

BUYER AND SUPPLIER RELATION IN PALM OIL FORESTRY IN

PT. SINAR MAS AGRO RESOURCE AND TECHNOLOGY Tbk

研 究 生:邱平林

Student:

Ronny Kurnia指導教授:黃仕斌

Advisor: Professor Kevin Huang

國 立 交 通 大 學

管理學院

企業管理碩士學位學程

碩 士 論 文

A Thesis

Submitted to Master Degree Program of Global Business Administration College of Management

National Chiao Tung University In partial Fulfillment of the Requirements

For the Degree of Master

in

Business Administration 2011

Hsinchu, Taiwan, Republic of China

i

Abstract

As the world population increases, the demand for food is growing year by year as well, in accordance with the population grow. The demand for crude palm oil (CPO) has increased tremendously during the past 10 years.

Palm oil is the most traded vegetable oil in the international market. Palm Oil is widely used in various sectors in numerous products, including cooking oil, instant noodles, pastries and baked goods, biodiesel, oleo chemicals, and processed foods. Indonesia is the largest producer of palm oil in the world, followed by Malaysia, Thailand, Nigeria and Colombia.

This case study will present the relationship between buyer (PT SMART Tbk, an integrated palm-based consumer company) and supplier (oil palm plasma farmers, or “smallholders”), to find out what benefit the suppliers gain from this partnership. Are the suppliers benefiting from this business with increased income? From the buyer’s perspective, what is the extent of their contribution to the CPO production? This study will use interviews conducted by the author with palm oil farmers to address these concerns and answer the following questions: Is it true that palm oil plantations in rural areas really manage to reduce poverty?

This case study may prove beneficial for people in different underdeveloped countries that share the same climate with Indonesia as one of the potential solutions to reduce poverty in rural areas and increase their country’s GDP.

In addition, this case study fills a gap in the available research about the palm oil industry by addressing its effects of rural poor who chose to become oil palm plasma farmers. While many publications have examined the palm oil industry and investment in palm oil production, this

ii

investigation aims to approach the subject from the overlooked perspective of the rural laborers, covering how the palm oil farmers started their plantation and how their new work has affected their income and quality of life.

iii

Acknowledgement

I hereby would like to thank to my family, my friends, my classmates, my instructor, Prof Kevin Huang, and all the professors in the GMBA program of NCTU. I could not have finished my MBA degree without their support.

iv

TABLE OF CONTENTS

Abstract………i Acknowledgements………iii Table of Contents………iv List of Figures……….vi List of Tables………vii Notations………...viii Chapter 1. Introduction………1 1.1 Research background……….………...…1 1.2 Research objective……….…………...………3 1.3 Research framework……….………...……….…………4 1.4 Research structure………..……...………51.5 Significance of study and potential contributions………...………6

Chapter 2. Industry review………7

2.1 Palm oil history and benefit……….……..…………..……..7

2.2 Global Supply and Demand of Palm Oil………..………8

2.3 Palm oil Industry in Indonesia……….……….…………..10

2.3.1 Palm oil companies in Indonesia………..10

2.3.2 Palm oil Supply Chain in Indonesia………..11

2.3.3 The economic benefits of palm oil to Indonesia……….…..…………12

2.3.4 Palm oil and rural area development in Indonesia………...18

Chapter 3 Case Company PT. Sinar Mas Agro Resource and Technology Tbk………20

3.1 Company introduction………20

3.2 How partnership and relationship scheme………22

3.3 Obstacles and challenge in implementation palm oil plantation………...……….24

3.4 Solution in Obstacles……….…….…25

3.5 RSPO principles and criteria for sustainable palm oil production………27

3.6 Government policy………28

v

4.1 Interview method……….………...31

4.2 Interview by phone……….………32

4.2.1 Interview palm oil smallholder and company………33

4.3 Summary from interview……….………...37

4.4 Secondary data collection………37

4.5 Research Methodology………38

Chapter 5. Analysis………39

5.1 Benefit to farmers………39

5.2 Contribution of Palm Oil to Local Economies and Small Land Holders………46

5.3 Return on investment from palm oil production………..…….….46

5.4 Returns on investment from Palm Oil Production……….………49

5.5 Partnership...………..….……50

Chapter 6. Conclusion...53

References………..54

vi

LIST of Figures

Figure 1: Flow chart of research structure………...………5

Figure 2: Tree to table-the palm oil process………8

Figure 3: Projection of world Palm Oil Supply and Utilization………9

Figure 4: Palm oil supply chain ……….………..……….…12

Figure 5: Structure of the Indonesia’s Economy, 1960 to 2005………13

Figure 6: Indonesia Commodity Share of Agriculture production, 2009………13

Figure 7: World producers of palm oil by country………14

Figure 8 Plantation pattern Palm Oil………21

Figure 9: Plasma transmigration scheme………22

Figure 10: KKPA Partnership scheme……….23

vii

List of Tables

Table 1: List of Major Player Palm oil companies in Indonesia………..…….….……11

Table 2: Indonesian Agriculture 2004-2009………15

Table 3: Palm Oil production 2004-2009………16

Table 4: Palm Oil Location and Area 2000-2009………17

Table 5: PT SMART Tbk, Plantation, harvest and CPO production………40

Table 6: PT SMART Tbk, Plantation location (hectares)……….……….………40

Table 7: Total cost to set up palm oil plantation in rural area Sumatra and Kalimantan...41

Table 8: Installment debt principal and interest payments schedule per hectare of farmers participating………...42

Table 9: Farmer income from palm oil per hectare………….………..43

Table 10: Comparison of projected earnings for plasma producers compared with those of their previous jobs………..44

viii

NOTATIONS

ADB Asian Development Bank

ARD Agriculture and Rural Development

BPS Central Statistics Agency

CPO Crude Palm Oil

FAO Food and Agriculture Organization

FFB Fresh Fruit Bunches

GDP Gross Domestic Product

Ha Hectare

IDR Indonesia Rupiah Currency

IFAD The International Fund for Agricultural Development

KKPA Corporative that giving credit to palm oil farmers

PT. SMART Tbk PT. Sinar Mas Agro Resource and Technology Tbk

PK Palm kernel

1

Chapter 1

Introduction

1.1 Research background

This paper presents the relationship between buyer (palm oil production companies, like PT. Sinar Mas Agro Resource And Technology Tbk.) and supplier (oil palm plasma farmers, or “smallholders”) in Indonesia’s palm oil industry in order to analyze how the partnership benefits each party, with particular focus on those benefits gained by the farmers. A key issue is this partnership’s value creation and whether sustainable palm oil production can increase the living standard of palm oil farmers while simultaneously increasing their CPO production. This study will also address some reasons why Indonesia has become the leading palm oil producer over the past of 10 years.

As the world population increases, the demand for food is growing year by year as well, in accordance with the population grow. The demand for crude palm oil (CPO) has increased tremendously during the past 10 years. CPO is used widely in various industries, including cosmetics and detergents, chemicals, and livestock. Its use has grown such that industries depend on CPO production, and this makes CPO price increase every year.

Indonesia’s increasing palm forestry has grown to make the Indonesian palm oil industry the largest in the world. Indonesia exports CPO all around the world. One of the factors in the meteoric rise of its palm oil industry over the last decade is the mutually beneficial relationship

2

between buyer and seller. There are many journal articles that review the palm oil industry, but none of these discuss or study how the partnership and how much benefit the farmers gain from it. Mutual benefit is undoubtedly one of the reasons why this industry has become so successful. Most of the published discussion is limited to palm oil’s economic benefit and contributions to reducing poverty.

Today in Indonesia, there are 18 big companies that invest in palm oil forestry, but only five of them do end to end palm oil integrated from upstream to downstream. This case study will focus on the biggest integrated company in Indonesia’s palm oil industry, PT. Sinar Mas Agro Resource And Technology Tbk.

Indonesia, with population of 241 million people, has become forth most populous country in the world. Poverty and unemployment are two of the most critical issues facing Indonesia right now and will remain so for years to come. In March 2011, according to Badan Pusat Statistik, the Indonesian government statistical bureau, Indonesia’s poverty rate is 12.49%, which means more than 30 million people are still below the poverty line. The majorities of them, 63.20 %, are in rural areas and depend on the agricultural sector for their livelihood; the remaining 36.80% reside in cities.

This buyer and supplier relationship involving several party motivation, farmers as smallholders , palm oil industries and also Government, The basic reason why farmers (smallholders) want to do the corporation with Palm Oil Industries, they want to increase their welfare, some of these farmers previously they received transmigration program from governments. Government give them 2 Ha lands, they have right to cultivated with rubber, but because the results not as their expected. As the Company motivation from company why they want to give palm oil plantation

3

credit scheme to smallholders, by doing this scheme, they confident that can maximize CPO production by offering palm oil plantation credit scheme to local farmers community land, base on their data that farmers that managing their own palm oil plantation will have higher motivation the result production yield increase better compare with plantation that only manage by company, in the other hand government has different motivation too, The milestone start in 1980, Government started faculties between private industries and farmers. Government motivation in encouraging investment in rural area especially in palm oil industries to open their factory in rural area and also reducing population density in city by transmigration programs, creating new employments , increasing welfare and in the same time help increase GDP by increasing CPO exports.

1.2 Research objective

The objectives of this paper, in terms of buyer and seller relations in palm oil forestry conducted by PT. Sinar Mas Agro Resource And Technology Tbk. are as follows:

- To find out how this partnership between buyer (PT. Sinar Mas Agro Resource And Technology Tbk.) and supplier (palm oil farmers) originated.

- To find out how these palm oil farmer in poor rural area were able to start their palm oil businesses

- To find out what benefit the palm oil farmers get from this partnership, particularly in the form of improved income; from the buyer’s perspective, to find out how big their contribution is to CPO production.

4

- To find out how big the scale of the palm oil production is, both from company plantations and from farmers’ plantations, as well as the fresh fruit bunch (FFB) harvest.

- To find out, through interviews with independent palm oil producers, whether or not it is true that palm oil plantations in rural area are able to reduce poverty.

1.3 Research framework

In this research, we want to examine the relationship between buyer (PT. Sinar Mas Agro Resource And Technology Tbk.) and supplier (independent palm oil farmers) in their supply chain. Moreover, we want to see how the integration of partnership and benefit to company and smallholders. In this research, author will do interview smallholders and company, In order to avoid variation of the data, this paper will focus on one Company: PT. Sinar Mas Agro Resource And Technology Tbk. (Secondary data derives from annual report the years 2006-2010) and Nonprofit organization journal.

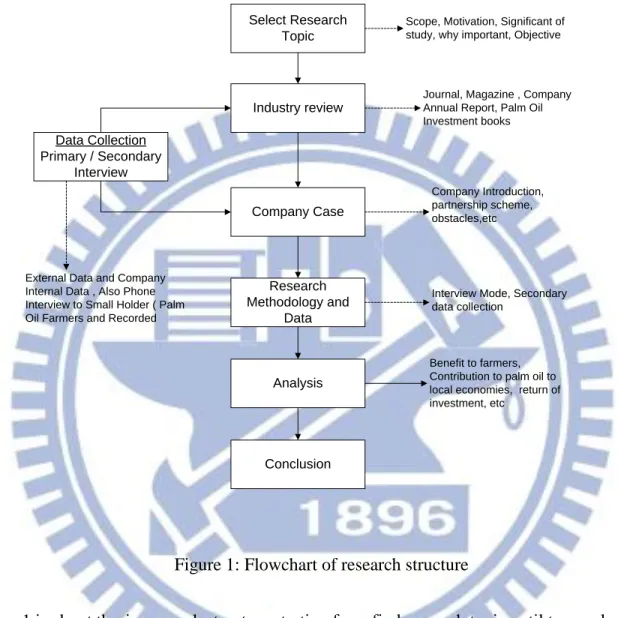

5 1.4 Research structure Select Research Topic Data Collection Primary / Secondary Interview Industry review Company Case Analysis Research Methodology and Data

Scope, Motivation, Significant of study, why important, Objective

Journal, Magazine , Company Annual Report, Palm Oil Investment books

Company Introduction, partnership scheme, obstacles,etc

Interview Mode, Secondary data collection

External Data and Company Internal Data , Also Phone Interview to Small Holder ( Palm Oil Farmers and Recorded

Conclusion

Benefit to farmers, Contribution to palm oil to local economies, return of investment, etc

Figure 1: Flowchart of research structure

Figure 1 is about thesis research structure starting from find research topic until to conclusion divided base on chapter.

6

1.5 Significance of this study and potential contribution

One of the potential solutions to reduce poverty in rural areas, increase living standards in rural areas and encourage transmigration from cities to rural areas for people that live under poverty.

Palm oil can grow in tropical weather; some countries with tropical climates still have poverty rates above 20%. This case study hopefully can offer one of the potential solutions to reduce poverty.

A lot of journals and books have discussed the palm oil industry and investment in palm oil production, but it is quite difficult to find information about how the palm oil farmers started their plantation and how much their income levels changed after beginning their palm oil production. This study’s primary focus is on these unaddressed aspects of the palm oil industry in Indonesia.

7

Chapter 2

Industry review

2.1 Palm oil history and benefit

Palm oil (from the African oil palm, Elaeis guineensis) has long been recognized in West African countries, and is widely used as cooking oil. European merchants trading with West Africa occasionally purchased palm oil for use in Europe, but since the oil was of a lower quality than olive oil, palm oil remained rare outside West Africa. In the Asante Confederacy, state-owned slaves built large plantations of oil palm trees, while in the neighboring Kingdom of Dahomey, King Ghezo passed a law in 1856 forbidding his subjects from cutting down oil palms. Palm oil and palm kernel oil are composed of fatty acids esterified with glycerol. The Palm oil is a rich source of carotenoids, the pigment found in plants and animals, from which it derives its deep red color. The major component of its glycerides is palmitic acid, a saturated fatty acid. The palmitic acid looks like a viscous semi-solid at tropical climate temperatures and a solid fat in temperate climates. Both are high in saturated fatty acids, about 50% and 80%, respectively. The oil palm gives its name to the 16 carbon saturated fatty acid palmitic acids found in palm oil; monounsaturated oleic acid is also a component of palm oil, while palm kernel oil contains mainly lauric acid. It is the largest natural source of tocotrienol, part of the vitamin E family and also high in vitamin K and dietary magnesium.

8

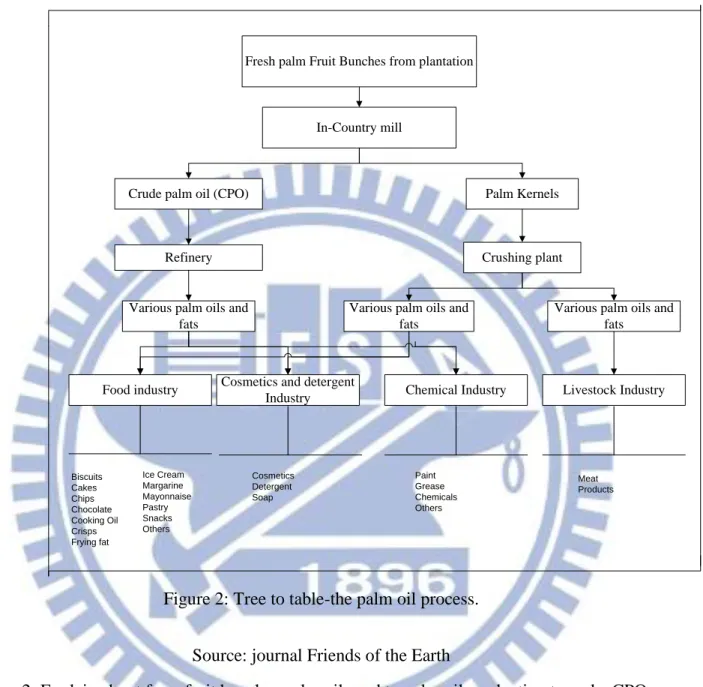

Fresh palm Fruit Bunches from plantation

In-Country mill

Crude palm oil (CPO) Palm Kernels

Refinery Crushing plant

Various palm oils and fats

Various palm oils and fats

Various palm oils and fats

Food industry Cosmetics and detergent Chemical Industry Livestock Industry Industry Biscuits Cakes Chips Chocolate Cooking Oil Crisps Frying fat Ice Cream Margarine Mayonnaise Pastry Snacks Others Cosmetics Detergent Soap Paint Grease Chemicals Others Meat Products

Figure 2: Tree to table-the palm oil process.

Source: journal Friends of the Earth

Figure 2: Explain about from fruit bunches palm oil send to palm oil production to make CPO and palm kernels derivative until to final products to customers

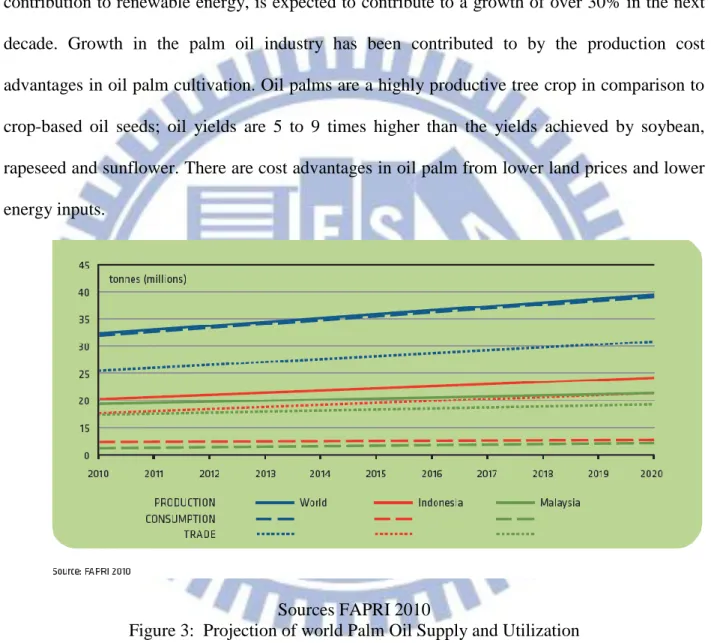

2.2 Global Palm Oil Supply and Demand

Increased returns from a strong global demand for vegetable oils are expected to encourage investment in the palm oil industry, leading to continued growth over the medium term, with

9

global consumption expected to increase over 30% in the next decade. By 2020, global consumption and production of palm oil is expected to increase to almost 60 million tons. The health characteristics and cost competitiveness of palm oil, coupled with its potential contribution to renewable energy, is expected to contribute to a growth of over 30% in the next decade. Growth in the palm oil industry has been contributed to by the production cost advantages in oil palm cultivation. Oil palms are a highly productive tree crop in comparison to crop-based oil seeds; oil yields are 5 to 9 times higher than the yields achieved by soybean, rapeseed and sunflower. There are cost advantages in oil palm from lower land prices and lower energy inputs.

Sources FAPRI 2010

Figure 3: Projection of world Palm Oil Supply and Utilization

Figure 3: Explain about Forecasting palm oil to 2020 Demand and Supply world production of palm oil.

10

2.3 Palm oil Industry in Indonesia

Based on 2010 statistical data, the agriculture sector contributed 16.5% to Indonesia’s GDP, and palm oil accounted for 5.6%. In Indonesia, oil palm plantations are considered by the government a major factor in alleviating the problems of poverty and unemployment and contributing to economic growth. This sector is considered able to provide employment and improvement of the welfare rural habitants. The latest regulations promoting biofuels, both for domestic energy needs and for export, are delivering a positive message regarding palm oil production.

2.3.1 Palm Oil Companies in Indonesia

There are several multinational companies in the palm oil industry in Indonesia, but basically only five large, private companies and one government organization participate in palm oil forestry, other palm oil companies enter into alliances with these five major companies.

11

Table 1: List of major players in the palm oil industry in Indonesia

Sources: http://duniaindustri.com/agroindustri/442-daftar-45-perusahaan-cpo-terbesar-di-indonesia.html

Table 1: Explain about only 18 Companies palm oil in Indonesia base on the ranking size of total land area in Indonesia and size of their plantation in Indonesia

2.3.2 Palm Oil Supply Chain in Indonesia:

Plantation core plasma, or PRI (Perkebunan Inti Plasma), provides one of the implementation frameworks used for all palm oil plantations in Indonesia.

NoCompany Name CPO Force (tons)Total Land Area in

Indonesia Land planted in Indonesia 1PT. Sinar Mas group / PT Golden Agri Resources 15,000.00 320 463 113 562 2Wilmar International Group 7,500.00 210 000 64,700.00 3PT. Plantation Nusantara (PTPN) IV 6,675.00

4Astra Agro Lestari group / PT Astra Agro Lestari Tbk 6,000.00 192 375 125 461

5Minamas Plantation Group 6,000.00

6Musim Mas Group 6,000.00

7Ntara Nusa PT Perkebunan (PTPN) III 5,650.00

8Asian Agri group / Raja Garuda Mas 5,000.00 259 075 96,330.00

9Duta Palma group 5,000.00 65,800.00 25 450

10

Salim group / PT Salim Plantations / Indofood group / PT

IndoAgri 5,000.00 1,155,745.00 95,310.00 11PT. Plantation Nusantara (PTPN) V 4,380.00

12

Lonsum group (PT PP London Sumatra Indonesia) / gun

Group 4,000.00 245 629 78,944.00

13PT. Plantation Nusantara (PTPN) XIII 3,295.00 14Permata Hijau Sawit Group 3,000.00

15Best Agro Group 2,000.00

16PT Socfindo / Socfin Group 2,000.00 17PT. ToIan Three / SIPEF Group 1,600.00

12

Figure 4: Palm oil supply chain

Sources: Roundtable on Sustainable Palm Oil

Figure 4: Explain about palm oil supply chain structure from plantation harvesting send to palm oil mill production, then resulting CPO, also consume domestics and export to over sea markets finally until to retailers.

2.3.3 The economic benefit of palm oil in Indonesia.

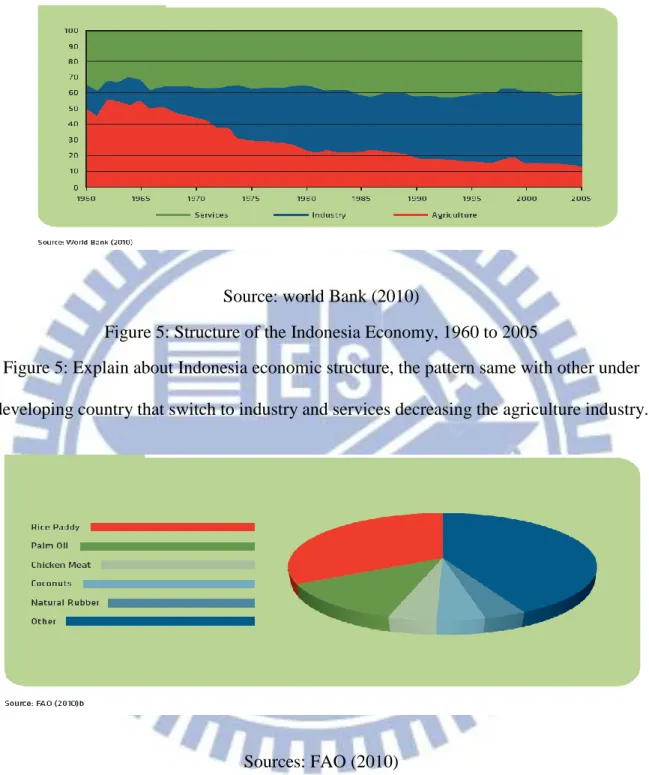

Agriculture’s contribution to the Indonesian economy has followed a trend of relative decline. Indonesia’s major agricultural products include: rice, paddy, palm oil, chicken meat, coconut and rubber; with major exports including Indonesia’s palm oil, rubber, palm kernel oil, cocoa and coffee. The contribution of agriculture to GDP has steadily decreased over the past 20 years. In 2008, the agriculture sector contributed 14.4 percent of GDP, as compared with around 22.5 percent in 1988, and 18.1 percent in 1998.

13

Source: world Bank (2010)

Figure 5: Structure of the Indonesia Economy, 1960 to 2005

Figure 5: Explain about Indonesia economic structure, the pattern same with other under developing country that switch to industry and services decreasing the agriculture industry.

Sources: FAO (2010)

Figure 6: Indonesia Commodity Share of Agriculture production, 2009

Figure 6: explain about Indonesia agriculture commodity share, palm oil is the biggest agriculture production

14

Source : Http://www.indexmundi.com/agriculture/?commodity=palm-oil&graph=production

Figure 7: World country producers’ palm oil

Figure 7: explain about world ranking production palm oil , as we can see number one is Indonesia, follow by Malaysia.

15 Source: Indonesia Ministry Agriculture

Table 2: Indonesia Agriculture 2004-2009

Agriculture 2004 2005 2006 2007 2008 2009 Sweet potatoes 184,546.00 178,336.00 176,507.00 176,932.00 174,561.00 183,874.00 Sugar cane 344,793.00 381,786.00 396,441.00 427,799.00 436,505.00 441,440.00 Corns 3,356,914.00 3,625,987.00 3,345,805.00 3,630,324.00 4,001,724.00 4,156,706.00 Melon fruits 2,287.00 3,245.00 3,189.00 3,637.00 3,109.00 4,627.00 Tabaco 438,253.00 448,858.00 445,365.00 453,292.00 456,471.00 467,400.00 Bean Field 565,155.00 621,541.00 580,534.00 459,116.00 590,956.00 721,499.00 Orchard 2,260,464.00 1,221,524.00 1,120,630.00 1,229,102.00 1,320,679.00 1,308,199.00 Rose garden 3,750,349.00 3,989,487.00 536,445.00 1,690,659.00 951,870.00 614,480.00 Orchard 2,260,464.00 1,221,524.00 1,120,630.00 1,229,102.00 1,320,679.00 1,308,199.00 Spinach 34,371.00 36,952.00 42,847.00 43,774.00 44,711.00 44,975.00 Tea plantation 143,965.00 140,538.00 135,590.00 133,734.00 127,712.00 123,506.00 Palm Oil 5,284,723.00 5,453,817.00 6,594,914.00 6,766,836.00 7,363,847.00 8,248,328.00 Rices 11,922,974.00 11,839,060.00 11,786,430.00 12,147,637.00 12,327,425.00 12,883,576.00 30,549,258.00 29,162,655.00 26,285,327.00 28,391,944.00 29,120,249.00 30,506,809.00

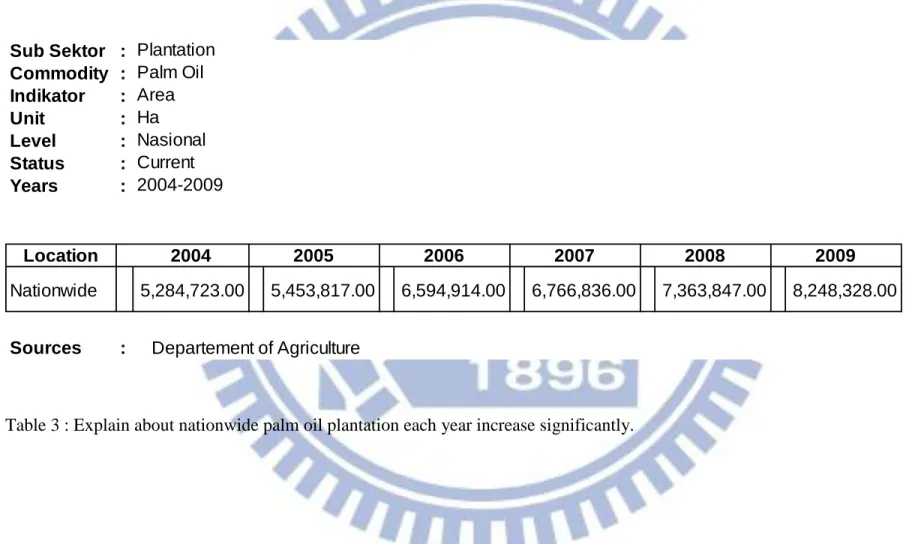

Table 2 : Explain from 2004 to 2009 , Agriculture production in Indonesia , each year we can see that palm oil increasing and others also decreasing since farmers try to find which one more benefit for them.

16

Source: Indonesia Departement of Agriculture Table 3 Palm Oil production 2004-2009

Sub Sektor : Plantation Commodity : Palm Oil

Indikator : Area Unit : Ha Level : Nasional Status : Current Years : 2004-2009 Location Nationwide 5,284,723.00 5,453,817.00 6,594,914.00 6,766,836.00 7,363,847.00 8,248,328.00

Sources : Departement of Agriculture

2005 2006 2007 2008 2009

2004

17 Table 4: Palm oil location area 2000-2009

Sources: Indonesia Department Agriculture

Sub Sektor : Commodity : Indikator : Unit : Level : Status Number : Years : Location Nanggroe Aceh Darussalam 218,493.00 252,114.00 257,684.00 262,151.00 249,011.00 254,261.00 308,560.00 274,822.00 287,038.00 313,745.00 Sumatera Utara 785,732.00 869,074.00 886,612.00 919,680.00 844,882.00 894,911.00 979,541.00 998,966.00 1,017,574.00 1,044,854.00 Sumatera Barat 229,575.00 266,387.00 270,047.00 306,496.00 279,798.00 282,518.00 315,618.00 291,734.00 327,653.00 344,352.00 Riau 805,646.00 1,047,644.00 1,238,106.00 1,319,659.00 1,340,036.00 1,277,703.00 1,547,942.00 1,620,882.00 1,673,553.00 1,925,344.00 Jambi 406,315.00 422,503.00 429,209.00 456,327.00 372,804.00 403,477.00 568,751.00 448,899.00 484,137.00 489,384.00 Sumatera Selatan 557,849.00 496,950.00 516,928.00 502,481.00 497,933.00 548,678.00 630,214.00 682,730.00 690,729.00 775,339.00 Bengkulu 60,899.00 66,730.00 70,409.00 80,218.00 126,252.00 147,125.00 165,221.00 163,455.00 202,863.00 224,651.00 Lampung 97,445.00 119,803.00 131,362.00 137,721.00 145,542.00 148,535.00 157,229.00 152,409.00 152,511.00 153,160.00 Bangka Belitung 91 89,225.00 90,065.00 94,886.00 119,635.00 130,037.00 133,284.00 172,227.00 185,508.00 141,897.00 Kepulauan Riau 0 0 0 0 6,849.00 13,698.00 6,933.00 6,678.00 8,256.00 2,645.00 Jawa Barat 12,350.00 6,251.00 6,251.00 6,242.00 8,070.00 8,744.00 9,831.00 10,550.00 11,531.00 12,140.00 Banten 6,304.00 14,080.00 16,983.00 19,200.00 12,614.00 14,076.00 14,077.00 14,894.00 14,894.00 15,023.00 Nusa Tenggara Timur

0 [ 4 401,761.00 0 0 0 0 0 0 0 0 Kalimantan Barat 363,269.00 389,006.00 406,372.00 416,807.00 358,175.00 381,791.00 492,112.00 451,400.00 499,548.00 602,124.00 Kalimantan Tengah 196,801.00 217,666.00 221,034.00 241,615.00 401,663.00 434,481.00 571,874.00 616,331.00 870,201.00 1,091,620.00 Kalimantan Selatan 120,694.00 129,673.00 138,634.00 141,638.00 172,650.00 134,621.00 243,451.00 257,862.00 290,852.00 312,719.00 Kalimantan Timur 128,256.00 144,567.00 191,146.00 201,871.00 171,581.00 201,236.00 237,765.00 339,294.00 409,566.00 530,552.00 Sulawesi Tengah 33,593.00 40,976.00 47,029.00 43,743.00 48,236.00 48,334.00 48,431.00 52,298.00 47,336.00 65,055.00 Sulawesi Selatan 73,376.00 77,363.00 83,085.00 78,932.00 13,925.00 16,018.00 24,490.00 15,708.00 15,944.00 17,407.00 Sulawesi Tenggara 13,286.00 13,286.00 13,285.00 4,078.00 [4 ] 4,106.00 466 2,966.00 18,912.00 21,033.00 21,669.00 Gorontalo 0 [ 4 42,032.00 0 0 0 0 0 0 0 0 Sulawesi Barat 0 0 0 0 52,476.00 57,476.00 75,154.00 115,906.00 94,319.00 107,249.00 Papua 48,105.00 50,137.00 52,817.00 49,812.00 51,051.00 39,090.00 29,736.00 29,736.00 27,657.00 26,256.00 Papua Barat 0 0 0 0 11,540.00 16,540.00 31,734.00 31,144.00 31,144.00 31,142.00 4,158,079.00 5,157,228.00 5,067,058.00 5,283,557.00 5,288,829.00 5,453,816.00 6,594,914.00 6,766,837.00 7,363,847.00 8,248,327.00 Sources : 2005 Departement of Agriculture 2002 Current Status 2000-2009 2000 2001 2003 2004 2006 Perkebunan Palm Oil Area Ha 2007 2008 2009 Nasional

18

Table 4: explain about production are in Indonesia , including the size of the land , we can see that some area increase significantly years by years.

2.3.4 Palm oil and rural development in Indonesia

Poverty in Indonesia is largely a rural occurrence. In 2009, of 32.5 million Indonesians living below the national poverty line, 20.6 million were located in rural areas. The percentage of poor in rural areas of Indonesia vastly outweighs that of their urban counterparts, with over 17.3% of the rural population below the poverty line, as compared with 10.7% in urban areas. This overall poverty rate doesn’t account for the millions who live just above the poverty line.

The International Fund for Agricultural Development (IFAD) found that the poorest people in rural areas tend to be farm laborers working on other peoples’ land, and smallholders on small plots of land less than 0.5 hectares. Over half of Indonesia’s population is located in rural areas. In 2002, agriculture represented two thirds of rural employment and contributed to almost half of rural household income (wages and farming income). A study showed that agricultural GDP growth in Indonesia is beneficial in reducing poverty, particularly in rural areas. Specifically, annual growth of 1% was found to reduce total poverty by 1.9 percentage points (urban poverty by 1.1 percentage points and rural poverty by 2.9 percentage points)

In 2008, it was estimated that employment created by palm oil production in Indonesia could potentially reach over 6 million lives and pull them out of poverty.

In 2009, it was noted that over the past decade, industry expansion—specifically palm oil—has been a significant source of poverty alleviation through farm cultivation and downstream

19

processing. The plantation and harvesting of oil palm is labor intensive, and as such, the industry contributes a significant portion of employment in many rural regions.

Additional benefits to palm oil workers have included secure income as well as access to healthcare and education. Palm oil production provides many of the rural poor with a sustainable income, especially with key palm oil developments in regions, such as Sumatra and Riau, with significant percentages of rural poor.

20

Chapter 3

Case company PT. Sinar Mas Agro Resources and Technology Tbk

3.1 Company introduction

Established in 1962, and listed on the Indonesia Stock Exchange in 1992, PT Sinar Mas Agro Resources and Technology Tbk (hereafter referred to as “SMART” or “the Company”) is one of the largest, publicly-listed, integrated palm-based consumer companies in Indonesia, with total sales of Rp 20.3 trillion, and net income of Rp 1.3 trillion in 2010. The Company’s primary activities range from cultivating and harvesting oil palm trees, to processing fresh fruit bunches (FFB) into crude palm oil (CPO) and palm kernel (PK), to refining CPO into industrial and consumer products such as cooking oil, margarine and shortening.

The Company cultivates approximately 138,100 hectares of oil palm plantations in Indonesia, including plasma. Fifteen mills extract CPO and PK from FFB, with a total capacity of 3.7 million tons per annum. Part of SMART CPO is processed further into value-added bulk, industrial and branded products through their own refineries, with a total capacity of 1.4 million tons per annum. A significant portion of SMART PK is crushed in SMART kernel crushing plants, which have an annual capacity of 444 thousand tons, producing higher-value palm kernel oil and palm kernel meal.

The Company employs more than 45,000 people in Indonesia, of which 16,000 are direct employees, 16,000 are smallholders, and 13,000 are casual workers. SMART’s oil palm estates

21

are all located in Sumatra and Kalimantan. The operations are well supported by the Company’s own research and development centre (SMART Research Institute or “SMARTRI”), and its affiliate’s high-yielding seed garden.

Apart from their employees, many more people depend indirectly on the plantations for their livelihood. For example, SMART also helps to develop micro-economies by providing indirect employment to local entrepreneurs near its estates by using local transporters to move its products, and engaging local contractors for land preparation and planting.

SMART also distributes, markets, and exports palm-based consumer products. Besides bulk and industrial oil, SMART’s refined products are also marketed under several brands, such as Filma and Kunci Mas. Today, these brands are recognized for their high quality and command significant market share in their respective segments in Indonesia.

Plantation Society

Palm oil Factory

Plantation society waiting scheduled

Plantation society scheduled

Sources: Komaba studies in Human Georaphy Vol 19 1-16 2008 Figure 8: Plantation Pattern Palm Oil

22

Figure 8: explain about palm oil plantation pattern , all the harvest result will send to palm oil facility for processing become CPO.

3.2 How partnership and relationship scheme

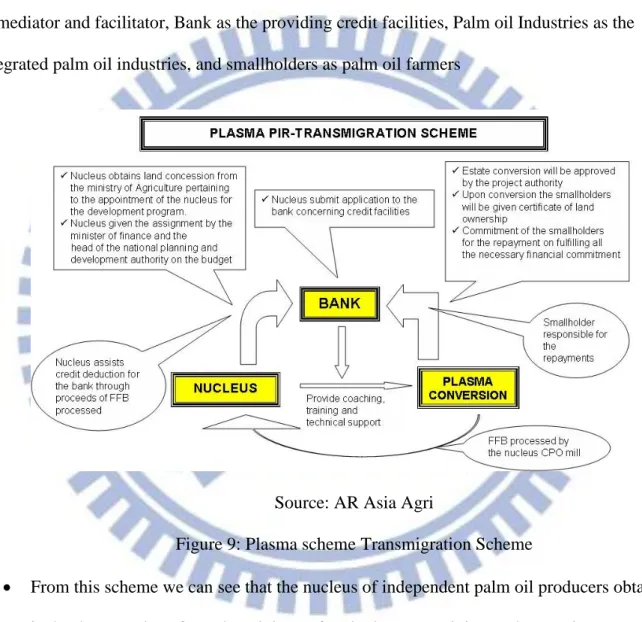

Basically there are 2 main relationship schemes in doing implementation between Government as mediator and facilitator, Bank as the providing credit facilities, Palm oil Industries as the integrated palm oil industries, and smallholders as palm oil farmers

Source: AR Asia Agri

Figure 9: Plasma scheme Transmigration Scheme

From this scheme we can see that the nucleus of independent palm oil producers obtains its land concessions from the ministry of agriculture, pertaining to the appointment of the nucleus for development programs.

Upon conversion, the smallholders will be given certificate of land ownership.

23

Providing training even fertilizer.

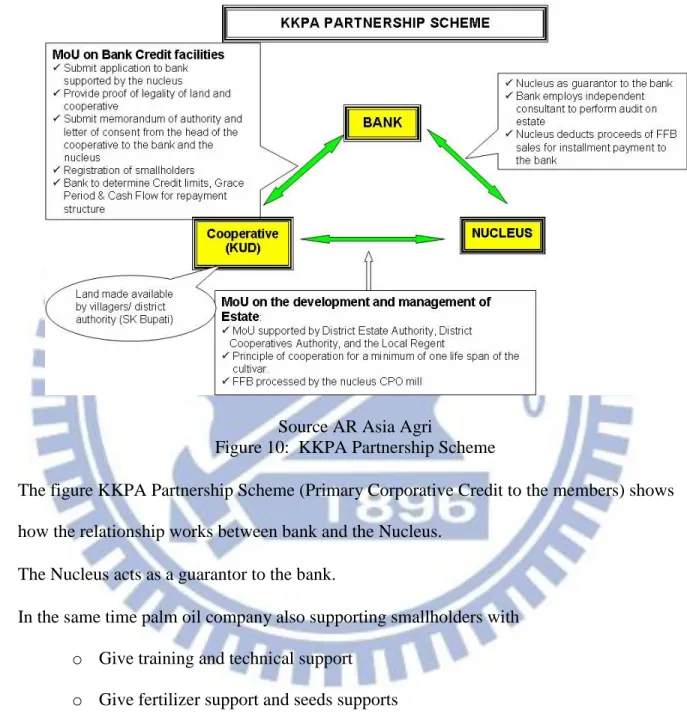

Source AR Asia Agri

Figure 10: KKPA Partnership Scheme

The figure KKPA Partnership Scheme (Primary Corporative Credit to the members) shows

how the relationship works between bank and the Nucleus.

The Nucleus acts as a guarantor to the bank.

In the same time palm oil company also supporting smallholders with o Give training and technical support

24

3.3 Obstacles and challenge in implementation palm oil plantation

About the obstacles and challenge that face in the Palm Oil Industries in Indonesia, I write down short and brief information, since my case study limited to palm oil industry and relationship with the farmers. Here are some common obstacles and challenges in palm oil industry, not all the palm oil plantation area run smoothly, some of them have some obstacles in several aspects.

Economic aspect

The gap between actual result with potential result

Debt

o There are still many farmers who bound by corporate debt

Declining prices and rising costs

In some area there is no clarity about the pricing of palm oil

Not well absorbed by the interests of sustainable palm oil certified Environment aspect

Deforestation

Loss of biodiversity

The use of chemicals without properly use safety equipment potentially negative impact on farmer’s health

25

Social aspect

Land right

o Local community land right

Indigenous peoples and local communities

Violation of human right

Plantation workers

Child labor

Safety issues

3.4 Solution in obstacles:

Before roundtable on sustainable palm oil was formed, the problem and obstacles in palm oil industry consider higher. Some critic come from Green peaces organization and also come from end user buyer such as Unilever Company.

In response to the urgent and pressing global call for sustainably produced palm oil and solving the obstacles, the Roundtable on Sustainable Palm Oil (RSPO) was formed in 2004 with the objective promoting the growth and use of sustainable oil palm products through credible global standards and engagement of stakeholders

RSPO is composed of ordinary members in seven different sectors, Affiliate

26

The seven sectors of Ordinary Members are:

Oil Palm Growers

Members examples here : PT. Sinar Mas Agro Resource And Technology Tbk, PT. Sampoerna Agro, etc

Palm Oil Processors and/or Traders

Members examples here : AarhusKarlshamn AB, Bakels, Bio Oil Energy S.L, Itochu Corporation , Nexsol, etc

Consumer Goods Manufacturers

Members examples here: Arnott’s Biscuits Ltd, Avon Products Inc , Cadbury P&G, Pepsi Co, Sheiseido Company limited, SK Chemical Ltd , Unilever, etc

Retailers

Members examples here : Carrefour, Marks and Spencer, IKEA, Dutch Food Retail Association, Wal-Mart Store, Inc

Banks and Investors

Members examples here : HSBC Bank , ANZ Banking Group limited, Credit Suisse AG, Rabobank, Standard Chartered Bank

Environmental/Nature Conservation NGOs

Members examples here : WWF Organization, Fauna& Flora International, The Zoological Society of London, etc

Social/Developmental NGOs

27

RSPO is a not-for-profi-t association that unites stakeholders from seven sectors of the palm oil industry - oil palm producers, palm oil processors or traders, consumer goods manufacturers, retailers, banks and investors, environmental or nature conservation NGOs and social or developmental NGOs - to develop and implement global standards for sustainable palm oil

Such multi-stakeholder representation is mirrored in the governance structure of RSPO such that seats in the Executive Board and project level Working Groups are fairly allocated to each sector. In this way, RSPO lives out the philosophy of the "roundtable" by giving equal rights to each stakeholder group to bring group-specifi-c agendas to the roundtable, facilitating traditionally adversarial stakeholders and business competitors to work together towards a common objective and making decisions by consensus

3.5 RSPO Principles and Criteria for Sustainable Palm Oil Production

Principle 1: Commitment to transparency

Principle 2: Compliance with applicable laws and regulation

Principle 3: Commitment to long-term economic and financial viabilit

Principle 4: Use of appropriate best practices by growers and millers

Principle 5: Environmental responsibility and conservation of natural resources and biodiversity

Principle 6: Responsible consideration of employees and of individuals and communities affected by growers and mills

Principle 7: Responsible development of new planting

28

3.6 Government policy

Government considering palm oil industry as strategy country development the vision developed in oil palm development “Development of system and the Palm Oil Agribusiness

Competitiveness Empowerment, democracy, Sustainable and Decentralized.

Medium term policy , In order to obtain optimal benefits in palm oil agribusiness development national oil , National policy for period 2005-2010 are as follows:

1. Productivity and Quality improvement policy palm

This policy is intended to increase productivity plants as well as the quality of palm oil gradually, both of which produced by farmers and large plantation planters. Implementation of policies to improve productivity and quality of coconut palm can be reached through: rejuvenation of oil palm, development of seed technology-based industries and markets, increased surveillance and testing of seed quality, protection palm germ plasma, development and stabilization institutional farmers.

2. Downstream Industry Development and Improvement Added Value palm oil.

This policy is intended to Indonesia palm oil exports are not again in the form of raw materials (CPO), but in the form of processed products, so that the value added enjoyed in the country and the creation new jobs. Application of industrial development policy downstream is taken among others by:

1. Facilitate the establishment of a refinery-scale integrated MCC 50-10 tons TBS / h in areas that have not been associated with the processing unit and cooking oil palm factory establishment (MGS) small-scale centers CPO production plant has been no MGS.

29 2. Development of downstream industries in palm oil production centers. Prospects and Direction of Agricultural Development of Palm Oil 24

3. Increased cooperation in the field of promotion, research and development and human resources development with the state CPO.

4. Facilitate the development of biodiesel.

5. Development of market research and market intelligence to strengthen competitiveness. This policy is necessary given the fragility of the cooking oil market in Indonesia and the magnitude of economic costs and social costs of these food shortages in the domestic and shaking of position Indonesia as a reliable supplier of palm oil in world markets

C. Strategy

In accordance with objective of agricultural development, goals and objectives development of oil palm agribusiness strategy, Strategic objective:

1. Increase food security 2. Community

a. Vertical Integration of oil palm plantation and agro industries that products derived typed food, such as cooking oil and butter.

b. Horizontal integration with oil palm plantations livestock and or crops

3. Foster business plantation in rural

a. Community empowerment in development palm oil processing business b. Encourage the provision of facilities and infrastructure palm oil processing c. Increase utilization resources plantation

d. Increasing production and productivity of the garden palm oil through technological innovation

30 e. The provision of supporting infrastructure and facilities, especially in transport infrastructure and to oil palm plantations and infrastructure processing

f. Development of business diversification

g. Eradication Pest Plant Organisms (OPT) and protection of plantation resources Palm

31

Chapter 4

Research Methodology

The methodology used in this research using interview method and involved carrying out a wide–ranging review of secondary sources and internal data sources.

4.1 Interview Method

Due the distance between respective parties, this study’s interviews can only be conducted between interviewer and palm oil farmers over the telephone, Main reason to use interview to know how they do it.

I. Find qualification criteria for candidate

1. Knowledgeable: worked on or owned palm oil plantation for more than 8 years.

II. How to do the interview:

1. List down all the questions

a. Name and profession?

b. Location?

c. Why did they become palm oil farmers?

d. How they start their work as palm oil farmers?

32

f. With which company or companies have they partnered?

2. Explain first the purpose of this interview and ask permission

3. Use tape recorder, start record

4. Ask one question at a time

5. Attempt to remain as neutral as possible

6. Encourage responses

7. Provide transition between major topics

8. Make all the notes from the interview recording into typed results

4.2 Interviews by phone.

Telephone interviews were conducted via phone with palm oil farmers in order to sample some direct data of palm oil farmers and the effects that palm oil production has had on their standard of living. Telephone interviews, rather than questionnaires, allow for open-ended questions, which will be serve to ascertain whether or not the buyer-seller partnership really allows mutual benefit for SMART and the plasma farmers. The interviews to follow were conducted in Indonesia on November 12th, 2011 with three palm oil farmers that have owned plantations of two hectares or more, for more than 8 years. The method for conducting the interviews is:

1. Tape record the dialogue

2. Transcribe exactly what was said during the interview and translate to English 3. List the interview questions and responses

33

From the interview with the farmers, this study seeks to find out about the partnership palm oil farmers have with palm oil companies and what the benefits they receive. The author of this study conducted the following interviews and will be referred to as “Author” in the follow English translations of the interview transcripts.

4.2.1 Interview palm oil smallholder and company A. Interview with Mr. Tejo, a palm oil smallholder Author: Good afternoon, Pak Tejo.

Mr.Tejo: Yes, good afternoon. Author: Is this Mr. Tejo? Tejo: Yes, I’m Mr. Tejo.

Author: I got information that Mr. Tejo runs a business in palm forestry; can you tell me how long have you owned and managed your palm forestry business?

Mr. Tejo: Yes right, I have been running a palm oil forestry business in north Palembang City since 10 years ago. In the years 2000, I used to work in others’ fields tilling crops.

Author: Then why did you suddenly change to palm oil forestry?

Tejo: Because I heard about the ownership program for palm forestry from the cooperative of Sinar Mas Company, and before that I didn’t have any money to start.

Author: How about your income after you became a palm oil farmer—did your income increase? Tejo: Greatly increased, Sir. Before, my monthly income was only less than 300.000 IDR (around 35 USD). This month my income is more than 5,000,000 IDR (approximately 600 USD), and each year it increases. I can get more income because I can do intercropping farming with palm oil and other vines. From palm oil forestry alone I can get 4 million rupiah per month.

34

Author: Do you feel lucky to have become a part of the palm oil partnership program?

Tejo: I started into palm oil forestry with zero capital. This is all from starting with zero capital, all because of hard work and support from Sinar Mas Company cooperative.

B. Interview with Mr. Sarwin a palm oil smallholder Author: Hello, good Afternoon, Mr. Sarwin.

Sarwin : ‘Good afternoon’ from whom?

Author: I just called Mr. Tejo, He informed me that you are a palm oil farmer. Sarwin : Yes, how can I help you?

Author: Could you explain to me about your current job exactly?

Sarwin: I’m a palm oil farmer in North Palembang, have been for more than 10 years. My palm oil forestry has increased from 2 hectares to 10 hectares now.

Author: What do you feel about working in partnership with a palm oil company? Do you feel lucky or not? With whom are you working?

Sarwin : Every year my income increases significantly, I started without any capital. This is all because of the support from Sinar Mas Company. Here people used to be poor, with very low income. My income in year 2000 was only 500,000 IDR (less than 60 USD) per month. Now it increased greatly. For sure I get a lot of benefit. From the beginning I got support from the palm oil company (Sinar Mas Group).

Author: If you don’t mind, how much is your income now?

Sarwin: After 10 years of palm oil forestry, now I can enjoy the results: My palm oil forestry is 10 hectares, and every month my income is 40,000,000 IDR (around 4500 usd ). If the market prices are going up, that’s what I like.

35

Author: Do you have bad moments working as a palm oil farmer?

Sarwin: Bad and good, of course, a lot, Sir. When the market prices of palm oil drops, automatically my income reduces. Actually we have minimum pricing, but sometimes if world market prices drop, it will still affect us; I have to sell cheaply.

C. Interview with Mrs Suminem a palm oil smallholder Author: Good afternoon Mrs. Suminem

Suminem: Yes, Where are you from?

Author: I just call Mr. Sarwin, I want to ask you about your palm oil forestry and your work as a palm oil farmer. Why did you become a palm oil farmer?

Suminem: Because I had empty land. Then, 8 years ago, I got into the palm oil forestry program. Now, I have become more prosperous.

Author: Can you explain to me how you do the partnership?

Suminem: From opening my palm oil forestry, they gave me forestry credit, fertilizer, nursery, and a lot of technical support. I didn’t need to pay for the next 4 years, according to the agreement with the cooperative from PT SMART Tbk. Now I can enjoy the result. As you know, palm oil farmers that own palm oil lands will produce better results than palm oil lands owned by a company.

D. Interview with Mr Joko, Operational Manager palm oil Industries

Author: Hallo Pak Joko, How are you today? Could you tell us why your Company Smart Tbk , have the cooperation or relationship with smallholder farmer? Why need this? Why your company’s Smart Tbk bother to give credit scheme? Why not just expand plantation by company.

36

Joko: We have several reason for doing cooperation with these smallholders farmer, first according to our experiences FFB yield palm, there is significant percentages different around 20%, higher FFB harvest compare with plantation that manage by palm oil industries, why they can give higher production yield, I think because of they have better motivation, they think they need to manage cultivated their land maximum. Second reason because we cannot easily open new plantation area, we need get do many papers works and permit to pass from government, for sure government encouraging palm oil industries should collaboration with Transmigration area. Third reason, I think just I said previously, Government encourages and facilitating between local people (Smallholders) and us palm oil industries. Government also give support to us and local community, Government give them free land and rice, This is transmigration program , government move them high density area to rural area in others island for example in Kalimantan island, also government supporting us to cooperated with this transmigration people.

Author: Do you think is it useful or working well this cooperation or this relationship? How about the future do you think keep continue this?

Joko: Well my position as operational manager, I have limited capacity to answer all your question, Base on my experience as operation manager in palm oil company I need to go to plantation area, I see a lot of improvement from the society welfare to in rural area developments, and we also hire a lot local people become our employee. Until now we still doing mutual benefit partnership, for sure I think will be bigger in the future.

37

4.3 Summary from interview:

Base on the interview with 3 small holders and one production manager palm oil Company, writer can conclude that both party whether as small holder and palm oil company , they want to work together because they think benefit that they will get, base on this interview w , both party gain benefits.

4.4 Secondary Data Collection

The data in this study will focus on secondary data and internal company sources data, which is derived from the following sources:

Indonesia strategic vision for agriculture and rural development

Word Growth Report for Indonesian Palm Oil Benefit, February 2011

Ministry of Agriculture of the Republic of Indonesia

Food and Agricultural Policy Research Institute, World Oil Seeds and Products, 2010.

Agribusiness development and palm oil sector in Indonesian journals

PT Sinar Mas Agro Resource and Technology Tbk, Annual report, 2008-2010

Investment in Palm oil industry in Indonesia, 2009.

The limitation of collecting some of this data is that some companies do not publish confidential information. So the data used herein will be based only on the data that is available from the Company to the public and investor information.

38

4.5 Research Methodology

The methodology used in this case study research involves conducting a wide-ranging review of secondary sources data and internal company data. Most of the data in this research is from years 2005-2010. The contextual literature search included the history of palm oil, the importance of palm oil to Indonesia’s GDP contribution, research papers, palm oil journals and reports, palm oil books, company annual reports, and company press releases. The research of this paper primarily focuses on literature addressing Indonesia’s strategic vision for agriculture and rural development. It seeks to see use this information to ascertain how much rural farmers’ income changed from before they were palm oil farmers to after they started palm production, and how they made their transition and also using interview method.

39

Chapter 5

Analysis

5.1 Benefit to farmers

The analysis of data regarding the benefit to palm oil farmers from their partnership and relationship with buyers in the palm oil industry will include the following:

1. PT. Sinar Mas Agro Resource And Technology Tbk. a. Total planted area 2006-2010

b. Total planted Nucleus and plasma production 2006-2010 c. FBB Harvested 2006-2010

d. CPO production

2. Total palm oil plantation per hectare by palm oil farmers 3. Total cost funding from bank / investor to palm oil farmers 4. When farmer need to pay their investors

5. How much the farmers earn as income 6. Other benefits, if any

40

Table: 5

PT SMART Tbk, plantation, harvest, and CPO production

Sources: PT. Smart Tbk Annual Report 2010

From table 5 above, we can see that plasma palm oil farmers of CPO producing for PT SMART Tbk contributed 18.6 % of the company’s total production. In 2010, areas planted by plasma farmers increased 8%, an average yearly increase of 5.75% over 5 years.

Table: 6

PT SMART Tbk, Plantation location (hectares)

Plantation location ( hectares) 2010 2009 2008 2007 2006 41,132.00 41,254.00 39,505.00 39,210.00 38,984.00 0% 4% 1% 1% 24,260.00 23,815.00 23,349.00 23,200.00 23,319.00 2% 2% 1% -1% 67,457.00 66,207.00 63,910.00 61,234.00 55,747.00 2% 3% 4% 9% 5,245.00 3,202.00 2,053.00 1,546.00 -39% 36% 25% 100% Sumatra plasma Kalimantan Nucleus Kalimantan plasma Sumatra Nucleus

41

Table 6 above shows the significant area for plasma plantations has grown substantially on Kalimantan Island. The main reason for this is that Kalimantan is the second biggest island in Indonesia, and it mostly still contains rain forest. Accordingly, the population in that area is likely low income per capita. Palm oil plantations are generally located in rural areas because palm requires huge tracts of land for cultivation. The land in rural areas is still relatively cheap and the government has given it to farmers who move out of cities to cultivate it as part of a government transmigration program.

Table: 7

Total cost to set up palm oil plantation in rural areas of Sumatra and Kalimantan

No Description Cost in IDR

1 Plantation Construction 32,702,800.00

2 Land Certificated 1,200,000.00

3 Admin & Notary 1,000,000.00

4 Manajement fee 5% 1,721,200.00

5 Bank Interest 8,609,500.00

45,233,500.00

Total

Sources: Palm oil investment book

Based on table 7, in order to cover the cost of opening 2 hectares of palm oil plantation, a farmer can get the credit from a cooperative for 4 years with very low bank interest. The farmer will then interest in year 4 and repays the entirety of the principal and interest by year 9.

42

Table: 8

Installment debt principal and interest payments per hectare of farmers participating

Years Interest fee in IDR Principal installments in IDR

4 500,000.00 -5 1,000,000.00 -6 1,000,000.00 5,258,500.00 7 3,000,000.00 6,967,400.00 8 8,699,220.00 8,370,220.00 9 10,438,160.00 Total 14,199,220.00 31,034,280.00 Grand total 45,233,500.00 Sources Palm oil investment book

In table 8, we can see the detailed payment schedule for farmers repaying the corporative, totaling less than 46,000,000 IDR over 9 years.

43

Table: 9

Assumption of Farmer income for palm oil per hectare.

Palm oil ages Production TBS/KG/Ha/Years Prices/Kg(IDR) Income/Ha (IDR)/Years

After paid installment

program /years Income/ months/Ha 4 5,000.00 1,548.00 7,740,000.00 7,740,000.00 645,000.00 5 8,000.00 1,641.00 13,128,000.00 13,128,000.00 1,094,000.00 6 12,000.00 1,740.00 20,880,000.00 14,621,500.00 1,218,458.33 7 15,000.00 1,844.00 27,660,000.00 17,692,600.00 1,474,383.33 8 17,000.00 1,965.00 33,405,000.00 16,335,560.00 1,361,296.67 9 20,000.00 2,072.00 41,440,000.00 31,001,840.00 2,583,486.67 10 20,000.00 2,196.00 43,920,000.00 43,920,000.00 3,660,000.00 11 20,000.00 2,328.00 46,560,000.00 46,560,000.00 3,880,000.00 12 20,000.00 2,468.00 49,360,000.00 49,360,000.00 4,113,333.33 13 20,000.00 2,618.00 52,360,000.00 52,360,000.00 4,363,333.33 14 20,000.00 2,773.00 55,460,000.00 55,460,000.00 4,621,666.67 15 18,000.00 2,939.00 52,902,000.00 52,902,000.00 4,408,500.00 16 18,000.00 3,116.00 56,088,000.00 56,088,000.00 4,674,000.00 17 18,000.00 3,302.00 59,436,000.00 59,436,000.00 4,953,000.00 18 18,000.00 3,501.00 63,018,000.00 63,018,000.00 5,251,500.00 19 17,000.00 3,711.00 63,087,000.00 63,087,000.00 5,257,250.00 20 17,000.00 3,933.00 66,861,000.00 66,861,000.00 5,571,750.00 21 15,000.00 4,169.00 62,535,000.00 62,535,000.00 5,211,250.00 22 15,000.00 4,419.00 66,285,000.00 66,285,000.00 5,523,750.00 23 14,000.00 4,685.00 65,590,000.00 65,590,000.00 5,465,833.33 24 14,000.00 4,880.00 68,320,000.00 68,320,000.00 5,693,333.33 25 12,000.00 5,264.00 63,168,000.00 63,168,000.00 5,264,000.00 26 12,000.00 5,579.00 66,948,000.00 66,948,000.00 5,579,000.00 27 12,000.00 5,979.00 71,748,000.00 71,748,000.00 5,979,000.00 28 7,000.00 6,300.00 44,100,000.00 44,100,000.00 3,675,000.00 29 5,000.00 6,800.00 34,000,000.00 34,000,000.00 2,833,333.33 Total 389,000.00 1,295,999,000.00 1,252,265,500.00 Average 15,560.00 51,839,960.00 50,090,620.00 Farmer's Income/HA

Sources: palm oil investment book

Base on table 9, the palm oil farmer’s income increases significantly each year. These income figures are consider very high income for the farmers that previous earner less than 550,000 IDR (estimate around 60 USD ) per month and lived on less than 500,000 IDR per month (estimate around 55 USD) per months. By the fourth year, the income has increased to more than 1,200,000 IDR (estimate around 140 USD) per month. And each subsequent year increases significantly.

44

Table 10:

Comparison of assumption projected earnings for plasma producers compared with those of their previous jobs.

Palm oil ages

Yearly Income become Plasma ( Palm Oil farmers) in IDR Income/ months/Ha in IDR Estimated Yearly Income in IDR Estimated Monthly Income in IDR 4 7,740,000.00 645,000.00 6,480,000.00 540,000.00 5 13,128,000.00 1,094,000.00 6,868,800.00 572,400.00 6 14,621,500.00 1,218,458.33 7,280,928.00 606,744.00 7 17,692,600.00 1,474,383.33 7,717,783.68 643,148.64 8 16,335,560.00 1,361,296.67 8,180,850.70 681,737.56 9 31,001,840.00 2,583,486.67 8,671,701.74 722,641.81 10 43,920,000.00 3,660,000.00 9,192,003.85 766,000.32 11 46,560,000.00 3,880,000.00 9,743,524.08 811,960.34 12 49,360,000.00 4,113,333.33 10,328,135.52 860,677.96 13 52,360,000.00 4,363,333.33 10,947,823.65 912,318.64 14 55,460,000.00 4,621,666.67 11,604,693.07 967,057.76 15 52,902,000.00 4,408,500.00 12,300,974.66 1,025,081.22 16 56,088,000.00 4,674,000.00 13,039,033.14 1,086,586.09 17 59,436,000.00 4,953,000.00 13,821,375.13 1,151,781.26 18 63,018,000.00 5,251,500.00 14,650,657.63 1,220,888.14 19 63,087,000.00 5,257,250.00 15,529,697.09 1,294,141.42 20 66,861,000.00 5,571,750.00 16,461,478.92 1,371,789.91 21 62,535,000.00 5,211,250.00 17,449,167.65 1,454,097.30 22 66,285,000.00 5,523,750.00 18,496,117.71 1,541,343.14 23 65,590,000.00 5,465,833.33 19,605,884.77 1,633,823.73 24 68,320,000.00 5,693,333.33 20,782,237.86 1,731,853.15 25 63,168,000.00 5,264,000.00 22,029,172.13 1,835,764.34 26 66,948,000.00 5,579,000.00 23,350,922.46 1,945,910.20 27 71,748,000.00 5,979,000.00 24,751,977.81 2,062,664.82 28 44,100,000.00 3,675,000.00 26,237,096.48 2,186,424.71 29 34,000,000.00 2,833,333.33 27,811,322.26 2,317,610.19 Total 1,252,265,500.00 383,333,360.00 Comparation 327%

Become Palm oil farmers (Plasma ) Stay with their old jobs in rural area

45

Table 10 shows the tremendous benefit gained by farmers who switch to palm oil production. Palm oil farmers (Plasma) earned an incredible 327% more over the course of 29 periods by producing palm oil than they would have with the crops they were previously producing.

Other benefit of palm oil production: 1. Reduces unemployment

2. Changes from premier sector homogeny, opening second tier business opportunities with more variety, from daily trading of goods to services.

3. Increases the standard of living in rural areas.

Based on the data shown in table 11, it can be seen that plasma farmers contribute a significant percentage of PT SMART Tbk’s total palm oil production, averaging 18.6% annually.

Table: 11

Contribution to PT SMART Tbk, production CPO

2,452,527.00 2,459,212.00 2,085,188.00 2,025,010.00 1,897,807.00 Nucleus 1,977,461.00 1,972,085.00 1,676,382.00 1,688,383.00 1,575,068.00 Plasma 475,066.00 487,127.00 408,806.00 336,627.00 322,739.00 percentage contribution 19% 20% 20% 17% 17% FFB Harvested ( tons)

46

5.2 The Contribution of palm oil to local economies and small land holders

Palm oil provides employment for many small landholders, with over 6.7 million tons of palm oil produced by smallholders in 2008. In 2006, it was found that around 1.7 to 2 million people worked in the palm oil industry. In 2008, the Indonesian palm oil commission found that over 41% of total palm oil plantations were owned by smallholders, with a further 49%owned by private plantations; the remaining 10% is owned by the government. The palm oil industry makes a substantial contribution to rural incomes, particularly small land holders. In 1997, the average net income of oil palm smallholders was seven times that of farmers involved in subsistence production of food crops.

5.3 Success story about palm oil farmers with cooperation with palm oil industries

In the age of 46 years old Mr. Kasimin just starting his new life , while many people have started to reduce workplace productivity and think about getting ready to rest in the old days, the father of five children that otherwise would take. Armed with a unanimous determination to admit a very simple goal, “foraging”, then departed with his wife and children followed government transmigration program to Kalimantan Island in 1992, for palm oil transmigration program. Location at Beloyang village, Melawi district west Kalimantan provinces.

Before Mr. Kasimin in java island cultivate rice or corn crops are increasingly limited their area, then this transmigration program Mr. Kasimin cultivate a wider area for palm oil, which is 2Ha. Mr. Kasimin also gets a modest house in the land area of 0.5 Ha. However, despite getting more land plus house facilities, was the story early in the resettlement area is not “beautiful” as imagined.

At the first, an area of 2 ha land was not yet fully-owned by Mr.Kasimin. As new start pack, Mr.Kasimin acts as palm oil plantation workers PT. Sinar Dynamic Kapuas (SDK) and salary of