法人說明會與董監事連結之關聯 - 政大學術集成

78

0

0

全文

(2) 立. 政 治 大. ‧. ‧ 國. 學. n. er. io. sit. y. Nat. al. Ch. engchi. i n U. v. .

(3) 立. 政 治 大. ‧. ‧ 國. 學. n. er. io. sit. y. Nat. al. Ch. engchi. i n U. v.

(4) Abstract In the field of social network, board interlock is a reliable communication channel for board of directors to transfer corporate information, which further influences the strategies or practices adopted by the firms.. Conference calls have. become a widely used medium for Taiwanese managers to communicate corporate information to the public in the past two decades.. This study investigates whether. board interlock as a social network affects corporate disclosure policies in terms of their decision to hold conference calls.. By using the data from listed companies in. 政 治 大 through interlocked directors 立are more likely to hold conference calls.. Taiwan during 2000 to 2009, the results indicate that firms tied to other call firms Moreover, I. ‧ 國. 學. find that interlocking independent directors are positively associated with the decision of holding conference calls by the focal company.. These findings are robust to. ‧. changes in the measures of board interlocks and conference calls.. Our additional. n. al. The findings in this study generally support the. er. io. influenced by board interlocks.. sit. y. Nat. analysis also indicates that the information disclosed in conference calls may be. i n U. v. argument that board interlocks are associated with the spread of corporate practices.. Ch. engchi. Keywords: Board interlock, Conference call, Social network, Voluntary disclosure.

(5) Index. Index .......................................................................................................................... I Tables ........................................................................................................................ II 1. Introduction ....................................................................................................... 1. 3.. Literature review ............................................................................................... 5 2.1 Conference calls background and related literature ................................. 5 2.2 Background and related literature on board interlocks .......................... 13 Research design ............................................................................................... 18 3.1 Hypothesis development ...................................................................... 18 3.2. 3.3 3.4 Research Results .............................................................................................. 30 4.1 Descriptive Analyses ............................................................................ 30. 學. 4.. 政 治 大 Variable descriptions ............................................................................ 22 立 Research Method ................................................................................. 27 Data collection ..................................................................................... 21. ‧ 國. 2.. ‧. 4.2 Correlation Analysis ............................................................................. 44 4.3 Regression results ................................................................................ 47 4.4 Additional analysis ............................................................................... 58 5. Conclusions ..................................................................................................... 66 References ............................................................................................................... 68. n. er. io. sit. y. Nat. al. Ch. engchi. I. i n U. v.

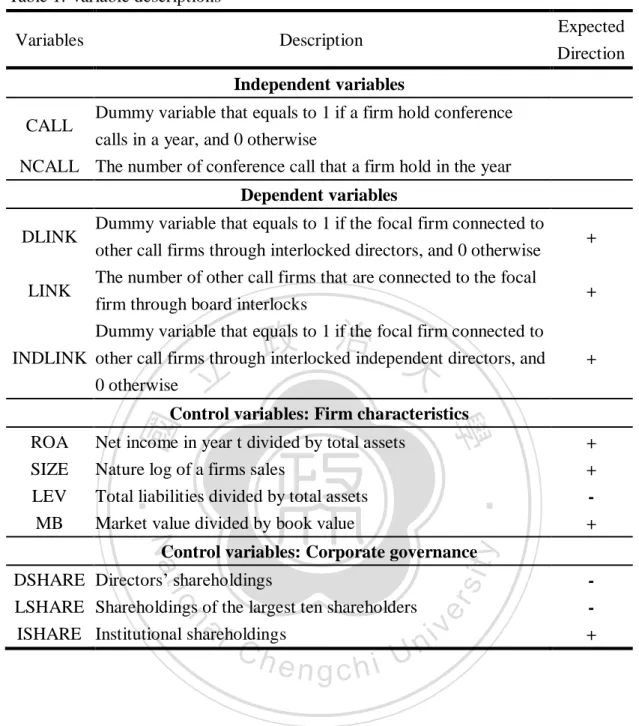

(6) Tables Table 1. Variable descriptions ................................................................................. 26 Table 2. Sample distribution ................................................................................... 32 Table 3. Yearly distribution of conference calls ....................................................... 33 Table 4. Industrial distribution of conference calls .................................................. 34 Table 5. Yearly distribution of the number of other call firms linked to the focal firm ....................................................................................................................... 37 Table 6. Industrial distribution of the number of other call firms linked to the focal firm ................................................................................................................ 38 Table 7. Yearly distribution of independent director links ....................................... 40 Table 8. Industrial distribution of independent director links ................................... 41 Table 9. Descriptive statistic ................................................................................... 43. 政 治 大. Table 10 Correlation analysis ................................................................................. 45 Table 11. The decision to hold conference calls and the focal firm’s link to other call firms ............................................................................................................... 49 Table 12. The decision to hold conference calls and the number of other call firms linked to the focal firm ................................................................................... 50. 立. ‧ 國. 學. ‧. Table 13. The frequency of conference call and the focal firm’s link to other call firms ............................................................................................................... 51 Table 14. The frequency of conference call and the number of other call firms linked to the focal firm .............................................................................................. 52 Table 15. The decision to hold conference calls and independent board link ........... 54. er. io. sit. y. Nat. al. n. Table 16. The frequency of conference calls and independent board link ................ 55 Table 17. The frequency of conference calls and independent board link, excluding firms without directors’ link ............................................................................ 56 Table 18. An alternative measure of conference call and the focal firm’s link to other call firms ........................................................................................................ 59. Ch. engchi. i n U. v. Table 19. An alternative measure of conference call and the number of other call firms linked to the focal firm .......................................................................... 60 Table 20. An alternative measure of conference calls and independent directors links ....................................................................................................................... 61 Table 21. An alternative measure of interlocked independent directors and the decision to hold conference calls..................................................................... 63 Table 22. An alternative measure of interlocked independent directors and the frequency of conference call ........................................................................... 64. II.

(7) 1. Introduction This study examines the relation between conference calls and board interlocks. Board interlock is a communication channel that is formed when one board of director sits on multiple boards simultaneously and transfers the information from one board to another.. These interlocking boards create the connections between firms and. these connections form a network that transfers reliable information (Galaskiewicz and Wasserman, 1989).. Social network theory suggests that a firm’s decisions or. 政 治 大 The purpose of this study is to investigate that whether board interlock 立. behaviors are influenced by information spread through social network (Haunschild, 1993).. network affects a firm’s disclosure policy related to conference calls.. ‧ 國. 學. Prior studies identify the spread of financial strategies through board interlock.. ‧. Davis (1991) and Davis and Greve (1997) show that the spread of poison pill and. y. sit. al. n. with board interlocks.. er. Bizjak et al. (2009) indicate that option grants backdating is associated. io. interlock.. Nat. golden parachute during the take-over wave in U.S in 1980s are associated with board. i n U. v. Khanna and Thomas (2009) show that firms that have. Ch. engchi. interlocking directorates are particularly likely to have synchronous returns.. In the. field of accounting, Brown (2011) finds that board interlocked ties increase the likelihood that firms adopt tax shelter.. Davison et al. (1984) and Chin and Chan. 2012) provide evidence that board interlocking directors affect the choice of auditors. Based on these researches, I focus on the likelihood of holding conference calls among listed companies in Taiwan through the interlocking board networks. Information asymmetry between the management and outside investors is a long-concerned agency problem and leads to higher cost of capital.. Voluntary. disclosure is one mechanism established to mitigate information asymmetry. 1.

(8) Specifically, for firms that rely heavily on external financing, reducing cost of capital is the major incentive to disclose corporate information voluntarily (Verrecchia, 1983; Donnelly and Mulcahy, 2008). Conference call in Taiwan has become a widely used voluntary disclosure in the last two decades.. Taiwan has a special industrial environment in that high-tech. industry (or the electronic industry in my sample) is the most important industry in the development of economy.. The high level of innovation activities in these high-tech. companies are not reflected on their financial statement as the values of innovative. 政 治 大 This exacerbates the information 立 asymmetry between managers and investors and activities are difficult to be verified and assessed under current accounting principles.. ‧ 國. To better communicate the firm. 學. makes firms’ external financing more difficult.. value to investors and reduce information asymmetry and cost of capital, Taiwanese. ‧. managers have incentives to voluntarily disclose information through conference calls. io. sit. y. Nat. (Chin et al., 2007).. n. al. er. The interactive characteristic of conference call leads to more effective. i n U. communication than other types of voluntary disclosure.. Ch. engchi. v Many studies find that. conference call helps mitigate the information asymmetry between inside managers and outside investors by increasing firm-specific information available to the market (Tasker, 1998; Bowen et al., 2002; Brown et al., 2004; Kimbrough, 2005).. Investors. are more confident to invest firms when corporate information is easier to obtain, which in turn would reduce costs of capital (Diamond and Verrecchia, 1991; Healy and Palepu, 2000; Francis et al., 2008). This study concentrates on the argument that information about disclosure policies on conference calls are transferred through board interlocks.. As board interlock. serve as a reliable, valuable and imitable information resource between firms, a firm’s 2.

(9) behavior can be affected by observing other firms’ (Galaskiewicz and Wasserman, 1989; Barney, 1991; Haunschild, 1993).. Under the growing trend in using. conference calls as a voluntary disclosure medium in Taiwan, firms tied to other firms that hold conference calls have chances to observe the information about conference calls and know better about the importance of this voluntary medium.. Specifically,. these interlocked directors have chances to observer the decision process of holding conference calls in interlocked firms and the expected benefits of reducing information asymmetry between management and outside investors.. Thus, I expect. 政 治 大 decision to hold conference calls. The sample consists of listed firms in Taiwan 立. a positive association between focal firms’ interlocked ties to other call firms and its. from 2000 to 2009 and we use Logistic regression and Zero-Inflated regression to test. ‧ 國. 學. our hypotheses.. The results of this study support the argument that the spread of. ‧. corporate practices are positively associated with board interlock networks.. sit. y. Nat. Specifically, I find that focal firms connected to other call firms through board. io. more frequently.. er. interlock are more likely to hold conference calls and tend to hold conference calls This result is more prounced when the connection is through the. al. n. v i n C h This evidence implies focal firms’ independent directors. that interlocked directors engchi U. with different board positions have different impacts on a firm’s disclosure policy.. In additional analysis, we provide a preliminary analysis on the content of conference calls and finds that interlocked directors may influence the information disclosed in conference calls.. Overall, these empirical results suggest that a firms’ disclosure. policy regarding the decision to hold conference calls is affected by interlocking ties, particularly among interlocked boards through independent directors. This study makes several contributions to the corporate disclosure and social network literature.. First, this study links the voluntary disclosure and social network, 3.

(10) and in particular, conference calls and board interlocks.. Prior researchers have. identified a positive association between board interlock and the spread of corporate practices but not disclosure practices.. Second, I further distinguish different board. positions to examine the effect of independent director interlock on conference calls. The finding that firms tied to other call firms through independent directors are more likely to hold conference calls implies that independent directors play a better monitoring role in a firm’s disclosure policy over other interlocking directors.. Third,. in contrast to prior studies on conference calls or board interlock that focus mostly in. 政 治 大 interlocks are relatively less investigated. The results in Taiwan are consistent with 立 evidences from US or European area.. Fourth, the additional analyses shed further. ‧ 國. the US or Europe, I use the data in Taiwan where conference calls and board. 學. insights to the impact of share directors on the type of information disclosed in. ‧. conference calls.. y. Section 2 describes the. sit. Nat. The remainder of this study is organized as follows.. n. al. In section. er. io. related literature and background on conference calls and board interlock.. i n U. v. 3, I develop hypotheses based on prior research and construct the regression models.. Ch. engchi. Section 4 reports the descriptive statistical analysis, correlation analysis and empirical results.. Section 5 concludes.. 4.

(11) 2. Literature review 2.1 Conference calls background and related literature 2.1.1 Conference calls as a voluntary disclosure mechanism Corporate information can be disclosed through different ways, including voluntary disclosure and mandatory disclosure.. Mandatory disclosures, such as. yearly financial reporting or other regulatory filings, are seen as the minimum requirement for listed companies and contain mostly financial and backward-looking information.. 政 治 大. Thus, mandatory disclosures may not capture all the relevant. 立. information about the firm’s performance and future perspective.. On the other hand,. ‧ 國. 學. voluntary disclosures, such as management forecasts, conference calls, press release, internet sites, and other corporate reports, tend to be a better channel for corporate. ‧. management to communicate firm performance and forward-looking information to. er. io. sit. y. Nat. the public.. In the perspective of disclosure theory, firms that rely more on external financing. al. n. v i n C h information voluntarily have the incentives to disclose reliable (e.g., Verrecchia, 1983) engchi U and these voluntary disclosures help mitigate the information asymmetry between the firm management and outside investors and reduce a firm’s cost of capital.. Healy. and Palepu (1993) argue that firms whose stock is undervalued by public capital markets have incentives to expand disclosures to communicate firm value to the market.. Frankel et al. (1995) find a positive relation between firms’ tendencies to. access capital market and to disclose earning forecast.. They indicate that financing. firms have greater incentives to voluntarily disclose information than non-financing firms, suggesting that market force provide incentives for more disclosure.. 5.

(12) Diamond and Verrecchia (1991) show that revealing public information to reduce information asymmetry can reduce a firm’s cost of capital by attracting increased demand from large investors due to increased liquidity of its securities.. Healy and. Palepu (2000) document three types of capital market effect of voluntary disclosure: improved liquidity for firms’ stock in the capital market, reduction in firms’ cost of capital, and increased following by financial analysts.. Francis et al. (2005) indicate. that, by using a sample from 34 countries other than U.S., firms in industries with greater external financing needs have higher voluntary disclosure levels and that an. 政 治 大 Moreover, they find that voluntary disclosure incentives operate 立. expanded disclosure policy for these firms leads to a lower cost of both debt and equity capital.. independently of county-level factors, suggesting that the effectiveness of voluntary. ‧ 國. 學. disclosure in gaining access to lower cost external financing around the world.. The findings of these studies support the idea that voluntary. y. Nat. and cost of capital.. ‧. Francis et al. (2008) find a significant negative relation between voluntary disclosure. n. al. er. io. sit. disclosure help reduce information asymmetry and firm’s cost of external financing.. i n U. v. Among all types of voluntary disclosure, conference call has the interactive. Ch. engchi. characteristic that makes communication even more effective and efficiency than other voluntary disclosure.. Thus, this study focuses on using conference calls as a. voluntary disclosure mechanism and examines its relationship with interlocked boards. 2.1.2 The content of conference calls In recent years, conference calls have become a very common voluntary disclosure medium to communicate relevant corporate information to the public.. A. conference call typically consists two sections: presentation by management and question and answer between the audience and the management (Frankel et al. 1999; 6.

(13) Hollander et al. 2010; Matsumoto et al. 2011). In presentation section, managers will first share information they wish to disclose or emphasize to the participants, such as manager’s interpretation of firm performance and additional voluntary disclosure.. In the question and answer section, also called “discussion” section. (Matsumoto et al., 2011), participants have the opportunities either to ask questions about the firm or question information disclosed by the managers in the presentation section.. This discussion section is a forum for analysts or investors who participate. in the call to communicate with the firm managers face-to-face.. 政 治 大 ideal channel for inside managers 立. Due to this. interactive characteristic, conference calls, comparing to other types of voluntary disclosure, provide an. to convey corporate. they need (Hollander et al. 2010).. 學. ‧ 國. information to the public and for outside investors and analysts to request information Matsumoto et al. (2011) find that both. ‧. presentation and discussion sections provide incremental information, but the. y. Nat. discussion sections have greater information content than presentations, suggesting. er. io. They also find that managers provide more information during. al. n. discussion sections.. sit. that bigger benefit of conference calls comes from analysts’ involvement in the. the presentation when firm. v i n Ch performance is poor, but the engchi U. discussion session is. relatively more informative than the presentation under these circumstances 1.. Their. research findings indicate that, comparing to issuing an earnings press release, the primary benefits of hosting a conference call is due to the discussion section with analysts. Some recent studies investigate the linguistic information content in conference calls.. 1. Frankel et al. (2010) find a positive relation between conference call linguistic. Matsumoto et al. (2011) indicate that managers are either not able to anticipate the information needs of analysts in the case of bad performance or unwilling to voluntarily disclose poor performance information in the presentation session. 7.

(14) tone and returns.. Mayew and Venkatachalam (2011) analyze conference call audio. files, by using vocal emotion analysis software, and find evidence that managerial vocal cues contain useful information about a firm’s fundamentals, incremental to both quantitative earnings information and qualitative soft information conveyed by linguistic content.. By using the computer aided content analysis to examine the. incremental informativeness of quarterly conference calls, Price et al. (2011) find that linguistic tone in conference calls is a significant predictor of abnormal returns and trading volume.. 政 治 大 Hollander et al. (2010) find 立strong support to the assumption that investors interpret Some research focuses on other perspectives of call content. For example,. In other words, investors equate no news with bad news.. ‧ 國. 學. silence negatively.. Chin. et al. (2007) demonstrate that, by using the data in Taiwan, firms with more. ‧. innovative firms are more likely to discuss innovative activities during conference. al. er. io. 2.1.3 The economic consequences of conference calls. sit. y. Nat. calls. 2. n. v i n C hcalls reduce the information The argument that conference asymmetry between engchi U. the inside mangers and outside investors, and increase the information available in the capital market has been demonstrated in prior studies.. Tasker (1998) suggests that. quarterly conference calls resolve the information asymmetry problem between manager and outside shareholders.. Frankel et al. (1999) find evidence that share. prices are unusually volatile and the average trade size is higher during conference calls. 2. These results suggest that material information is released in conference calls. See Chin et al. (2007) footnote 1:” Taiwan’s national R&D expenditures relative to gross domestic product rank ninth in the world. (See China Times, the best selling newspaper in Taiwan, August 24, 2002). Taiwan’s outbound patent filings in the U.S. rank fourth in 2000, following only the U.S., Japan, and German. These statistics show that innovation activities in Taiwan are very frequent compared to the world level.” 8.

(15) and investors trade on the information. informative corporate disclosures.. In other words, conference calls provide. More specifically, Brown et al. (2004) indicate. that information asymmetry is negatively associated with conference call activity. Based on the above viewpoints, informative disclosure in conference calls could lead to economic consequences.. Bowen et al. (2002) provide evidence that the. managers disclose more information during the conference calls quarters and that this information difference leads to the decrease in analysts’ forecast error and dispersion and the effect will persist through the next quarter’s earnings announcement.. 政 治 大 conference calls than do analysts 立 with stronger forecasting performance.. Additionally, analysts with weaker prior forecasting performance benefit more from Consistent. ‧ 國. 學. with the intention of Bowen et al. (2002), Kimbrough (2005) finds evidence that conference calls add to the total amount of information that analysts use about. ‧. forthcoming earnings.. Kimbrough (2005) further demonstrates that the initiation of. sit. y. Nat. conference calls significantly decreases the post-earning announcement drift and the. n. al. er. io. proportion of delayed market reaction to the earning’s announcements, implying that. i n U. v. the conference calls result in more timely analyst and investor responses to the future. Ch. e n g cChin h i et al. (2007) find that the more. implications of current earnings surprises.. R&D-related information disclosed in a conference call, the more likely the call is to affect the stock market returns of the firm’s stock. In the case of M&A transaction, Kimbrough and Louis (2011) examine the relation between management’s decision to hold a conference call at the merger announcement and the initial market reaction to the announcement. They find that bidders that hold conference calls at merger announcements experience substantially higher announcement returns than they would have experienced otherwise.. Kimbrough and Louis (2011) also indicate that. the superior announcement reaction is related to the fact that conference calls provide 9.

(16) a greater volume of information and place greater emphasis on forward-looking details.. Moreover, there is no evidence that this superior announcement. subsequently reverses. 2.1.4 Characteristic of conference calls firms Many research studies have tried to identify the relation between firm characteristics and its holding of conference calls.. Tasker (1998) shows that firms. with less informative financial statement are more likely to host a conference call than are firms with more informative statements.. These firms use conference calls as a. 政 治 大. voluntary disclosure channel to better communicate their performance and prospects. 立. to analysts and large outside shareholders.. Frankel et al. (1999) state that firms that. ‧ 國. 學. hold conference calls tend to be relatively larger, more profitable, more heavily followed by analysts and access the capital markets more often than other firms.. ‧. Bushee et al. (2003) indicate. io. sit. Nat. have higher market-to-book ratio than other firms. 3. y. These firms are more likely to be in high-tech industries, to grow more rapidly, and to. n. al. er. that firms providing open conference calls to meet the demand of nonprofessional. i n U. v. shareholders and these firms tend to be in high-tech industries and have greater. Ch. engchi. number of stockholders, lower institutional ownership, lower analyst following, higher average share turnover and greater revenue volatility than firms providing calls to a more restricted audience. 4. Firms with higher recorded intangible assets are less. likely to provide open calls because these firms disclose more complex financial information to more sophisticated users. Chin et al. (2007) find that cumulative abnormal returns that arise from conference calls are positively associated with the level of and the changes in 3. See Frankel et al. (1999) for detailed discussions. Bushee et al. (2003) define open conference calls as those have availability and timing generally well publicized. 10 4.

(17) innovation investments, implying that firms with more innovative activities are more likely to hold conference calls, consisting with prior research that shows high-growth firms are more likely to hold conference calls and hold them more frequently.. Chin. et al. (2008) indicate that corporate governance mechanisms under concentrated ownership structure have an impact on firms’ decisions to hold conference calls. The likelihood and frequency to hold conference calls are higher for firms with less control divergence and firms with second largest shareholders but lower for firms with higher percentage of controlling owners’ seats on the board. 5. Kimbrough and. 政 治 大 are particularly strong for economically significant deals where the intensity of 立 Louis (2011) find evidence that, in the merger and acquisition transactions, incentives. investor demand for supplemental information is pronounced.. Additionally,. ‧ 國. 學. stock-for-stock mergers are more likely to hold conference calls because the cost of a. Based on the above studies, firms. sit. y. Nat. post-announcement value of the bidder’s stock.6. ‧. stock-based merger and the likelihood of its completion are directly tied to the. io. er. are more likely to hold conference calls generally are larger, more profitable, more heavily followed by analysts and more likely to be in high-tech industries.. n. al. Ch. n U engchi. iv. In. addition, these firms are those with more informative financial statements, higher market-to-book ratio, greater number of stockholders, lower institutional ownership, higher average share turnover, greater revenue volatility, more innovative activities, less control divergence.. Furthermore, firms access more to capital markets, grow. more rapidly and engaged in stock-for-stock M&A transactions are more likely to hold conference calls.. 5. Chin, Lin and Liang (2008) define second largest shareholders as shareholder with the standing to sue under Taiwan Corporate Law 214. 6 Kimbrough and Louis (2011) indicate that all bidders have incentives to effectively communicate the rational for their proposed transaction due to the well-documented cost of capital benefits of forthcoming disclosure. The incentives are particularly strong for economically significant deals and stock-based mergers. 11.

(18) 2.1.5 Conference calls in Taiwan Chin et al. (2007) argue that the innovative activities and future economic benefits related to innovative activities are increasing in Taiwan, but the lack of accounting recognition of innovation activities reduces the financial statement informativeness.. They state that, under this circumstance, managers in Taiwan have. incentives to voluntarily disclose private information to better communicate firm value to investors.. Their research indicates that the growth of conference calls from. 1997 to 2002 reflect a tendency to adopt conference calls as effective disclosure practices.. 立. 政 治 大. Turing to the regulatory perspective, the information released in conference calls. ‧ 國. 學. in Taiwan is regulated by the Taiwan Stock Exchange (TWSE, hereafter) Procedures for Verification and Disclosure of Material Information of Companies with Listed. ‧. Securities and Gre Tai Securities Market (GTSM, hereafter) Procedures for. y. Nat. n. al. According to these two procedures,. er. io. Securities7, from 1992 and 1994 respectively.. sit. Verification and Disclosure of Material Information of Companies with GTSM Listed. i n U. v. the disclosures date, time, venue, or financial and business related information that are. Ch. engchi. not yet been entered into Market Observation Post System8 are deemed as material information for listed companies on TWSE and GTSM.. Additionally, with respect. to investor conferences and press conferences, the companies should comply with particulars including: (1) Firms shall make applications to TWSE or GTSM if they want to hold or attend a conference call during the trading hours; (2) Information about the date, time, venue and relevant information of the conference call shall be published at least one day prior to the date of conference call; (3) The press release. 7. Gre Tai Securities Market is the Over-the-Counter (OTC) market in Taiwan. Market Observation System is a website, http://mops.twse.com.tw/mops/web/index, is constructed by TWSE. 12 8.

(19) and financial and business information shall be input to Market Observation Post System before the call or at least during the non-trading hours before the conference call on the day of the call; (4) The content of conference call shall not exceed those entered to Market Observation Post System or reported to authorities.. We can imply. from these regulations that the Taiwanese authorities regard the information release in conference calls as material information and shall be regulated carefully.. 2.2 Background and related literature on board interlocks 2.2.1 Board interlock- A social network. 政 治 大 Board interlock is formed by having the same individuals sit on multiple boards 立. of directors (e.g., Useem 1984; Davis 1992).. In other words, an individual who sits. ‧ 國. 學. on the boards of more than one organization simultaneously or subsequently create These interlock ties between firms. ‧. interlock ties between these firms (Davis 1992).. y. sit. io. n. al. er. behaviors.. Nat. form a type of social network that facilitate the diffusion of information, ideas and. i n U. v. The study of board interlock arises from the theory of social network which. Ch. engchi. argues that information and behaviors are transmitted among individuals and further influence the actions or decisions of others.. Based on the network theory, if. companies share the same directors, information and experiences will be transferred between these companies through the communication of these directors and influence other firms’ structures and practices.. Useem (1984) states that director interlocks act. as a channel which managers can receive an optimal scan of the latest business practices and overall business environment.. Granovetter (1985) argues that, as. individual behavior, economic behavior is socially embedded in that the actors of such economic behaviors are affected by their relation to other actors. 13. Haunschild and.

(20) Beckman (1998) points out that, the interlock board directors carry less weight as an information source for large firms and central firms because these firms have more accesses to information.. The director ties are thus an important communication. mechanism and a source of information that influences firms’ behavior. Social learning theory (Bandura, 1977) specifically argues that observers of transmitted information imitate the behaviors of others.. Just as connection between. individuals lead to imitation of individual behaviors, the connection between firms lead to the imitation of corporate practices.. Galaskiewicz and Wasserman (1989). 政 治 大 ideas and are familiar information 立 channels that decision makers trust.. further indicate that network ties between organizations act as pipes to disseminate Because. ‧ 國. 學. these decision makers trust interlocking network, they are more likely to mimic other firms’ practices or strategies that pass through interlocking ties.. Barney (1991) also. ‧. documents that interlocking directorship is a resource which is valuable, scarce,. y. sit. Haunschild (1993) performs empirical tests on acquisition. io. competitive advantage.. n. al. er. Nat. imperfectly, imitable and lack of substitutability and contributes to a firm’s sustainable. i n U. v. activities and further find direct evidence that managers are imitating the acquisition. Ch. engchi. “models” of firms to which they are tied through directorships. 9. Haunschild and. Miner (1997) show that imitation behaviors are more likely to happen across board interlock networks when there is no alternate sources of information.. These. researches support the social network theory and indicate that interlock network is an influential communication medium for managers to share information about corporate practices. 2.2.2 The effect of board interlock 9. Haunschild (1993) argues that firm managers are exposed to the acquisition activities of other firms when they sit on those firms’ boards. For these managers, the acquisition activities of firms to which they tied serve as models, examples to imitate or emulate. Specifically, information about general acquisition know-how rather than acquisition opportunities is transferred through interlock ties. 14.

(21) The other stream of literature focuses on the economic consequences of board interlock.. Since the board directors are often the highest decision-making position,. the information spread through interlocking network will give these decision maker new ideas and further lead to structural or strategical influences to the firm.. Davis. (1991) points out that the direct contact through interlocks is the mechanism responsible for the spread of the poison pill in that a company is more likely to adopt poison pills if it shares directors with the companies that have adopted poison pills. 10 Davis and Greve (1997) show that the adoption of golden parachute by firms with. 政 治 大 that firms migrate from NASDAQ. more interlocking ties increase the rate of other firms’ adoption. 11 Rao et al. (2000) indicate that the likelihood. 立. to NYSE are. strengthened by director links to NYSE firms and weakened by director links to. ‧ 國. 學. NASDAQ firms.. Bizjak et al. (2009) find strong evidence that a firm is more likely. Khanna and Thomas (2009) show that. sit. y. Nat. that previously backdated its stock options. 12. ‧. to begin backdating option grants if the firm has a director who is tied to another firm. io. interlocks are likely to have synchronous returns 13.. al. Stuart and Yim (2010) find. v i n idea C that companies which h e n g c h i U have. n. evidence supporting the. er. firms that have interlocking directorates or are part of the same network of director. interlocking directors. exposed to the private equity deal are more likely to receive private equity offers. Cai and Sevilir (2012) suggest that the board connectedness create greater values 10. Davis (1991) indicates that poison pill is a takeover defense issued by a firm’s board of directors that can dramatically increase the cost that a hostile buyer would have to pay to acquire the firm. 11 Golden parachutes are contracts that award generous severance packages (typically three years' salary) to top executives whose employment ends following a takeover. By comparing the adoption of golden parachute and poison pills by US firms during the takeover wave in 1980s, Davis and Greve (1997) show that both structural embeddedness—social ties among firms—and cultural embeddedness—norms of directors—shape individual actions and the process of aggregation. 12 Bizjak et al. (2009) state that the practice of backdating involves that the board of directors “looking back” in time to select favorable dates to grant stock option awards (e.g., when the stock price was at its lowest). By doing so, firms can make it appear that the option award was granted at an earlier date and at a lower exercise price compared to the actual date that award was approved. 13 Khanna and Thomas (2009) show that pairs of firms that have one or more directors in common are more likely to have returns that move in the same direction in any one week and higher correlation coefficients, after controlling for ownership ties, common industry effects, business group effects, and overall trends in returns. 15.

(22) during mergers and acquisition transactions by providing information advantage to the acquirer, limiting the competition from outside bidders, facilitating deal-making or better operation performance of the combined firms after the deal completion. Research shows that board interlocks have an impact on accounting policies. Chiu et al. (2010) indicate that a firm has a higher possibility to restate earnings in a given year if it shares the same director with another firm that restated earnings either in that same year or within the past two year.. Furthermore, this earnings. management contagion is stronger when the firm’s shared director has a more. 政 治 大 Brown (2011) finds that. important relevant position, such as the board chairman, audit committee member or. 立. audit committee chairman.. network ties via board. ‧ 國. as a tax shelter.. 學. interlocks increase the likelihood that firms adopt the corporate-owned life insurance Other studies investigate the influence of interlocking directors on. ‧. external auditing and corporate governance.. Davison et al. (1984) show a significant. sit. y. Nat. relationship between the number of interlocking directors in a company and the. n. al. er. io. probability that these interlocked companies are audited by the same public. i n U. v. accounting firm as the focal company, implying that the choice of auditors can be. Ch. engchi. partially explained by the ties between board interlocking firms.. Chin and Chan. (2012) further find that, by using the unique 14 data in Taiwan, firms are more likely to retain both auditing firms and partners that are industry specialists if one or more of its directors serve on the boards of other firms that also retain specialists at both levels. Moreover, they find a firm is likely to have higher audit quality if it shares common directors with another firm that uses both a firm and a lead partner with industry expertise, suggesting that audit quality is associated with board interlock.. Yang et al.. (2012) use the data in China and point out that firms that have interlocking directors 14. Chin and Chan (2012) indicate that audit report is issued in the name of two signing auditors as well as the audit firm. 16.

(23) are more likely to hire brand-name auditors, more likely to receive qualified opinions, and less likely to smooth their earnings.. These firms thus have better earning quality,. implying that interlocking directorates can be considered as an effective internal governance mechanism.. These results supports the idea that board interlock serve as. an information network that lead to the diffusion of corporate strategies, practices and even the business structure.. 立. 政 治 大. ‧. ‧ 國. 學. n. er. io. sit. y. Nat. al. Ch. engchi. 17. i n U. v.

(24) 3. Research design 3.1 Hypothesis development This study attempts to test the relationship between conference calls and board interlocks and further examines whether the interlocking ties affect the likelihood of holding conference calls. Board interlock ties serve as a network that facilitates the dissemination of corporate practices.. For decision makers, interlocking network is a familiar. 政 治 大. information resource so that they trust the spread information and further mimic other. 立. Firm. 學. ‧ 國. firms’ practices (Galaskiewicz and Wasserman, 1989; Haunschild, 1993).. strategies and structures are thus influenced though the communication of these interlocking directors.. Prior studies argue that board interlocking is associated with. ‧. the spread of poison pill and golden parachute during the take-over wave in U.S in. y. Nat. io. sit. 1980s (Davis, 1991; Davis and Greve, 1997), option grants backdating (Bizjak et al.,. n. al. er. 2009), synchronous returns (Khanna and Thomas, 2009), private equity offers (Stuart. i n U. v. and Yim, 2010), tax shelter (Brown, 2011), earning contagious (Chiu et al., 2010), and. Ch. engchi. selection of auditors (Davison et al., 1984; Chin and Chan, 2012; Yang et al., 2012). Conference call is a voluntary disclosure medium for companies to communicate firm-specific information to the public effectively and increase the information content in the market (Tasker, 1998; Frankel et al., 1999).. By increasing the. information content in the capital market, the information asymmetry between managers and investors are thus mitigated through conference calls (e.g., Tasker, 1998; Bowen et al., 2002; Brown et al., 2004; Kimbrough, 2005).. Reducing the. information asymmetry between firms and investors lead to economic consequences such as decreases in analysts’ forecast error (Bowen et al., 2002), increases in the 18.

(25) liquidity of shares (Diamond and Verrecchia, 1991), lowering costs of capital (Brown et al., 2004), and higher merger announcement returns (Kimbrough et al., 2011).. For. listed companies, increasing the liquidity of shares and lowering the cost of capital are two major consequences that increase managers’ incentives to voluntarily disclose information (Diamond and Verrecchia, 1991; Healy and Palepu, 1993; Frankel et al., 1995; Healy and Palepu, 2000). Voluntary disclosure policies regarding conference calls can be transferred from firm to firm.. To be more specific, a firm’s disclosure policy of holding conference. Director 政 治 大 interlock serves as a reliable 立 information source that may influence the corporate. calls can be spread through the interlocking director network among firms.. In the perspective of interorganization connection, corporate behavior can. ‧ 國. 學. strategies.. be learned by observing other firms through board interlocking.. When the focal firm. ‧. has directors sit on other boards, these directors have better chances to observe other. sit. y. Nat. firms’ decision making processes of holding conference calls and to better understand. n. al. Thus, directors who. er. io. the potential benefits of this voluntary disclosure mechanism.. i n U. v. sit on other boards that hold conference calls are very likely to facilitate the decision. Ch. e n g c h Ini. to hold conference calls in the focal firms.. other words, the benefits and. importance of conference calls would be transferred from firm to firm through these interlocking directors.. Therefore, I hypothesize that firms connected to other firms. that hold conference calls are more likely to hold conference calls. Hypothesis 1: Firms with interlocked directors connected to other call firms are more likely to hold conference calls Information asymmetry between managers and investors create agency problems that arise from the separation of management and ownership.. According to the. theory of corporate governance and agency problems, independent board of directors 19.

(26) and better disclosure mechanism could alleviate information asymmetry. directors monitor and give advices to the operation of the firm.. Board of. Particularly,. independent directors are directors with professional knowledge and thus, are considered to be more willing to protect shareholders’ interests.. Ajinkya et al. (2005). argue that independent directors not only monitor the quality of financial information but also play a role in determining and monitoring a firm’s voluntary disclosure policy. They find that firms with more outside directors are more likely to issue a forecast and are inclined to forecast more frequently, suggesting that director independence are By using the data in Hong Kong, 政 治 大 Ho and Wang (2001) indicate that audit committee, which is organized by all 立 positively associated with voluntary disclosure.. independent directors in a firm, is positively related to voluntary disclosure.. Cheng. ‧ 國. 學. and Courtenay (2006) provide evident that firms with a higher proportion of. Consistent with this finding, Donnelly and Mulcahy (2008) posit that. sit. y. Nat. disclosures.. ‧. independent directors on the board are associated with higher levels of voluntary. io. voluntary disclosure than other firms.. al. voluntary disclosure.. These studies support the idea that. v i n alleviateCinformation asymmetry h e n g c h i U by increasing n. independent directors. er. firms that have more independent directors or nonexecutive directors make greater. the level of. Since independent directors increase firms’ voluntary disclosure and conference calls is an important voluntary disclosure medium that helps reduce information asymmetry between management and outside investors, an interesting question is addressed: When independent directors sit on board of other call firms, will they spread the information about the benefits of holding conference calls and facilitate the decision to hold conference calls in the focal firm? Chiu et al. (2010) argue that. 20.

(27) board interlocks with different board positions 15 have different influences over financial statements.. Following their argument and prior studies on the relationship. between independent directors and voluntary disclosure, I hypothesize that when the focal firm has independent directors sit on the boards of other firms that hold conference calls, it is more likely to hold conference calls. Hypothesis 2: Firms linked to other call firms through interlocked independent directors are more likely to hold conference calls.. 3.2 Data collection. 政 治 大 I obtain the data of conference call from the website ‘Market Observation Post 立. System’ and databases ‘Knowledge Management Winner (KMW) 16’ and ‘Udndata17’.. ‧ 國. 學. Companies listed on TWSE and GTSM companies (hereafter, listed companies, in. Data of conference calls before 2004 is. sit. y. Nat. Observation Post System since 2004.. ‧. general) are required to post information about conference calls to the Market. Board links,. io. er. obtained by searching the news in both KMW and Udndata databases.. company characteristics, and corporate governance variables are obtained from. n. al. C h (hereafter TEJ). U n i database ‘Taiwan Economic Journal’ engchi. v. The sample includes listed companies during 2000-2009.. After deleting missing. values and industries that did not hold conference calls (e.g. financial industry, food industry and etc.) during the test period, the final sample is 8,669 firm-year observations. 15. Chiu et al. (2010) find that firms are even more likely to manage earnings when their interlocking directors serve as the member or the chairman of the audit committee because audit committees generally exert a greater influence over a firm’s financial reporting decision, relative to other board positions. 16 Knowledge Management Winner (KMW) is a database constructed by China Times and contains news published by China Time, Commercial Times and China Times Express starting from 1994. 17 Udndata is a database constructed by United Daily News and contains news publish by United Daily News, Economic Daily News, United Evening News, Min Sheng Bao, Upaper, World Journal, Global Views Monthly, Business Week, Common Wealth and etc. from 1990. 21.

(28) 3.3 Variable descriptions Dependent variable This study focuses on the effect of the board links on conference calls and tests whether firms with board interlocks are more likely to hold conference calls. Following prior literature that either distinguish firms that hold conference calls and those that do not (e.g., Frankel, 1999) or measure the frequency of calls (e.g., Bowen, 2002), I use two measurements to capture the firms decision to hold conference calls: (1) a dummy variable that equals to 1 if a firm holds conference call in a year, and 0. 政 治 大. otherwise (CALL); and (2) the frequency of conference calls (NCALL).. 立. I include. calls listed on the Market Observation Post System but exclude invited and overseas. ‧ 國. 學. calls.. io. sit. y. Nat. (1) Board links. ‧. Independent Variable. n. al. er. I include two variables to measure the board links between the focal firms and. i n U. v. other call firms: (1) a dummy variable that equals to 1 if the focal firm is connected to. Ch. engchi. other call firms through interlocked directors, and 0 otherwise (DLINK); and (2) the number of other call firms that are tied to the focal firm through interlocking directors (LINK).. For example, if a focal firm has three directors that are tied to other call. firms, one of which sits on board of three other call firms simultaneously, another sits on board of four other call firms, and the other sits on board of five other call firms, the number of other call firms tied to the focal firm is five (DLINK=1; LINK=5). (2) Independent board links To test hypothesis 2, I further distinguish the board positions of interlocked 22.

(29) directors into independent directors and non-independent directors. I use a dummy variable that equals to 1 if the focal firm connected to other call firms through independent directors and 0 otherwise (INDLINK). Control Variables (1) Firm characteristics I control firm characteristic including firm size (SIZE), profitability (ROA), leverage (LEV) and market-to-book value (MB).. Donnelly and Mulcahy (2008). 政 治 大 First, it is less costly for large firms to disclose detail information 立. document three reasons why larger firms tend to have higher level of voluntary disclosure.. because they are assumed to produce more information for internal purpose.. Second,. ‧ 國. 學. as larger firms are more closely watched by various government and regulatory. Third, larger firms need more funds from external capital markets.. y. Nat. government.. ‧. authorities, better financial reporting may lessen undesired pressure from the. er. io. sit. Increasing disclosure may increase investors’ confidence and facilitate the liquidity of a company’s shares, which make external financing easier.. n. al. Ch. n U engchi. iv. Many studies also. identify that company size is positively associated with holding conference calls (e.g., Land and Lundholm, 1993; Frankel et al., 1999; Tasker, 1998). Thus, I measure size (SIZE) by using the natural log of total sales and predict that firm size has a positive effect on the likelihood of holding conference calls.. Frankel et al. (1999) show that. firms that hold conference calls have higher return on assets than firms that do not, suggesting that firms that hold conference calls have better profitability.. The. measurement of profitability (ROA) is net income divided by total assets at the end of that year and it is expected to be positively associated with holding conference calls. Eng and Mak (2003) indicate that debt is a mechanism for controlling the free cash flow and find that firms with lower debts tend to disclose more information. 23. I.

(30) measure a firm’s leverage (LEV) using total liabilities divided by total asset at the end of year and expect that leverage is negatively associated with conference calls. Tasker (1998) uses a composite measure based on market-to-book ration to measure financial statement informativeness.. Frankel et al. (1999) find that firms with higher. market-to-book ratios are more likely to hold conference calls, suggesting that “growth” firms are more likely to voluntary disclose firm-specific information.. I. also control for the market-to-book ratio (MB) and expect that firms with higher MB are more likely to hold conference calls. (2) Corporate governance. 立. 政 治 大. I include directors’ shareholdings (DSHARE), institutional shareholdings. ‧ 國. 學. (ISHARE) and the shareholdings of the largest ten shareholders (LSHARE) to control for corporate governance mechanism.. Empirical evidence from Ruland et al. (1990),. ‧. Eng and Mak (2003) and Chin et al. (2007) indicate that higher directors’. y. Nat. io. sit. shareholdings are associated with a lower level of voluntary disclosure.. Eng and. n. al. er. Mak (2003) argue that when the managerial ownership is low, there is a greater. i n U. v. agency problem and outside shareholders will increase their monitoring in managers’. Ch. i managers have incentives to e n g c hHence,. behaviors in order to reduce agency problems.. voluntary disclose information to reduce agency costs caused by information asymmetry.. I expect that firms with higher directors’ shareholdings (DSHARE) are. less likely to hold conference calls.. Diamond and Verrecchia (1991) find that. institutional investors encourage more disclosures to reduce information asymmetry, which could further increase the liquidity of firms’ securities.. Tasker (1998) argues. that firms with little or no institutional ownership are less likely to hold conference calls since firms use calls to communicate with all the institutional investors and analysts simultaneously.. Therefore, I expect that institutional shareholdings 24.

(31) (ISHARE) would increase the probability that a firm decide to hold conference calls. Eng and Mak (2003) argue that more monitoring is required when share ownership is diffused.. Bushee et al. (2003) argue that firms with more dispersed investor base are. likely to experience greater pressure from shareholders to broaden their disclosure practices and are more likely to provide open conference calls.. Consistent with this. conjecture, they find a negative association between the number of investors and a firm’s probability to open conference calls.. Thus, I expect that firms with higher. dominant shareholdings are less likely to hold conference calls.. I measure the level. 政 治 大 shareholders (LSHARE). Table 1 summarizes the definitions and expected direction 立. of dominant shareholdings by using the total shareholding of the largest ten. of all variables.. ‧. ‧ 國. 學. n. er. io. sit. y. Nat. al. Ch. engchi. 25. i n U. v.

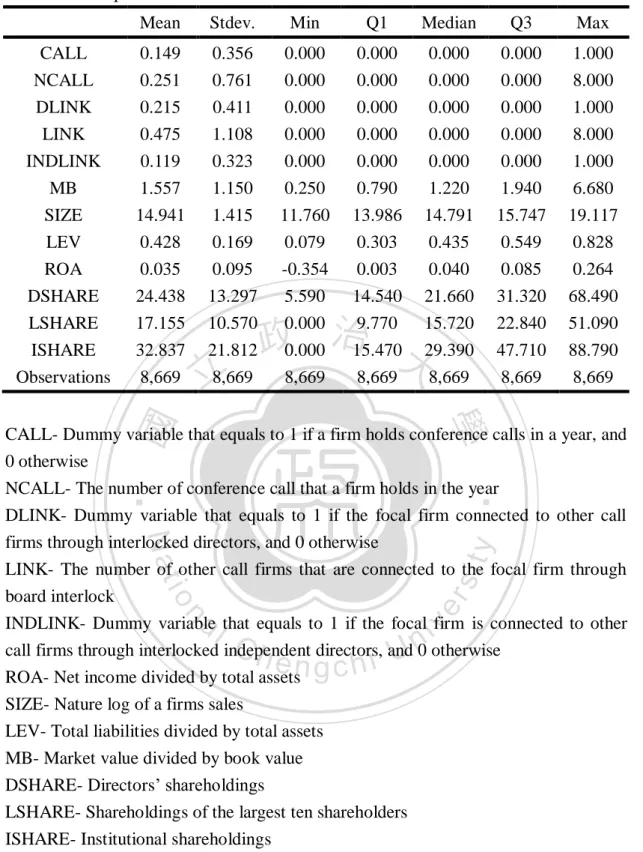

(32) Table 1. Variable descriptions Variables. Expected Direction. Description Independent variables. Dummy variable that equals to 1 if a firm hold conference calls in a year, and 0 otherwise NCALL The number of conference call that a firm hold in the year CALL. Dependent variables DLINK LINK. Dummy variable that equals to 1 if the focal firm connected to other call firms through interlocked directors, and 0 otherwise The number of other call firms that are connected to the focal firm through board interlocks Dummy variable that equals to 1 if the focal firm connected to. 政 治 大. INDLINK other call firms through interlocked independent directors, and. 立. 0 otherwise. + +. +. ROA. Net income in year t divided by total assets. SIZE LEV MB. Nature log of a firms sales Total liabilities divided by total assets Market value divided by book value. ‧. ‧ 國. 學. Control variables: Firm characteristics. +. Nat. y. + +. sit. Control variables: Corporate governance. io. LSHARE Shareholdings of the largest ten shareholders ISHARE Institutional shareholdings. n. al. Ch. er. DSHARE Directors’ shareholdings. n U engchi. 26. iv. +.

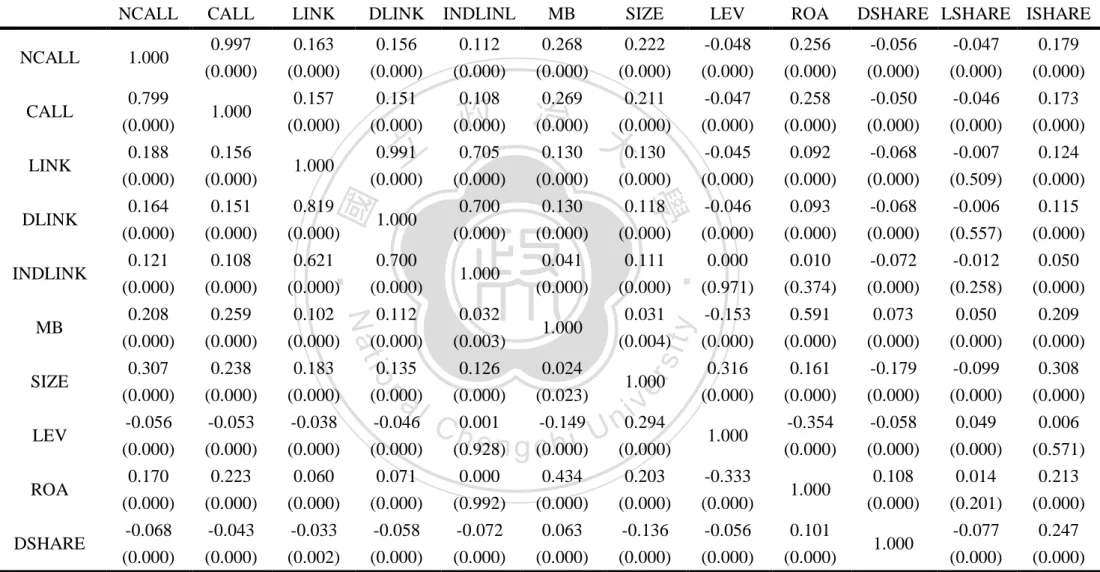

(33) 3.4 Research Method 3.4.1 Research Method To understand the distribution and the trend of conference calls and director link, I first analyze the descriptive analysis of these variables.. I would provide. distribution of dependent variable and independent variables, and the mean, standard error, first quartile, third quartile, minimum and maximum value of each variable. Second, I provide the correlation table to understand the relation between independent The bottom-left corner of 政 治 大 correlation table reports the Pearson correlation and the top-right corner reports the 立 variable, dependent variables and control variables.. Spearman correlations.. Third, this study investigates the relationship between. ‧ 國. 學. conference calls and board interlock and uses Logistic regression and Zero-Inflated I use Logistic regression for equations. ‧. Poisson regression to test the hypotheses.. sit. y. Nat. with CALL as dependent variable and Zero-Inflated Poisson regression for equations. io. n. al. er. with NCALL as dependent variable. 3.4.2 Model Construction. Ch. engchi. i n U. v. This study investigates whether the information about conference calls is transferred through the director network ties between firms and further influences a firm’s disclosure policy on conference calls.. Specifically, I examine whether the. decisions to hold conference calls in the focal firms are affected when the focal firms have interlocked director ties with other call firms.. To test Hypothesis 1, I perform. the following models: CALL = α + 𝛽1 𝐷𝐿𝐼𝑁𝐾 + 𝛽2 𝑅𝑂𝐴 + 𝛽3 𝑆𝐼𝑍𝐸 + 𝛽4 𝐿𝐸𝑉 + 𝛽5 𝑀𝐵 + 𝛽6 𝐷𝑆𝐻𝐴𝑅𝐸 + 𝛽7 𝐿𝑆𝐻𝐴𝑅𝐸 + 𝛽8 𝐼𝑆𝐻𝐴𝑅𝐸 + 𝛽9 𝑌𝐸𝐴𝑅 + 𝛽10 𝐼𝑁𝐷 + 𝜀. 27. (1A).

(34) CALL = α + 𝛽1 𝐿𝐼𝑁𝐾 + 𝛽2 𝑅𝑂𝐴 + 𝛽3 𝑆𝐼𝑍𝐸 + 𝛽4 𝐿𝐸𝑉 + 𝛽5 𝑀𝐵 + 𝛽6 𝐷𝑆𝐻𝐴𝑅𝐸 + 𝛽7 𝐿𝑆𝐻𝐴𝑅𝐸 + 𝛽8 𝐼𝑆𝐻𝐴𝑅𝐸 + 𝛽9 𝑌𝐸𝐴𝑅 + 𝛽10 𝐼𝑁𝐷 + 𝜀. (1B). NCALL = α + 𝛽1 𝐷𝐿𝐼𝑁𝐾 + 𝛽2 𝑅𝑂𝐴 + 𝛽3 𝑆𝐼𝑍𝐸 + 𝛽4 𝐿𝐸𝑉 + 𝛽5 𝑀𝐵 + 𝛽6 𝐷𝑆𝐻𝐴𝑅𝐸 + 𝛽7 𝐿𝑆𝐻𝐴𝑅𝐸 + 𝛽8 𝐼𝑆𝐻𝐴𝑅𝐸 + 𝛽9 𝑌𝐸𝐴𝑅 + 𝛽10 𝐼𝑁𝐷 + 𝜀. (1C). NCALL = α + 𝛽1 𝐿𝐼𝑁𝐾 + 𝛽2 𝑅𝑂𝐴 + 𝛽3 𝑆𝐼𝑍𝐸 + 𝛽4 𝐿𝐸𝑉 + 𝛽5 𝑀𝐵 + 𝛽6 𝐷𝑆𝐻𝐴𝑅𝐸 + 𝛽7 𝐿𝑆𝐻𝐴𝑅𝐸 + 𝛽8 𝐼𝑆𝐻𝐴𝑅𝐸 + 𝛽9 𝑌𝐸𝐴𝑅 + 𝛽10 𝐼𝑁𝐷 + 𝜀. (1D). where CALL is a dummy variable that equals to 1 if the firm holds conference calls in a year and 0 otherwise. firm holds within the year.. NCALL is the frequency of conference call that a. 政 治 大. DLINK in equation (1A) and (1C) is the dummy variable. 立. that equals to 1 if the focal firm is connected to other call firms through interlocked. ‧ 國. 學. directors and 0 otherwise.. LINK in equation (1B) and (1D) is the number of other. call firms connected to the focal firms through interlocked directors.. ‧. When a firm has independent directors tied to. er. io. sit. Nat. disclosure than other board positions.. y. I further argue that independent directors have a greater influence on voluntary. other call firms, they are more likely to facilitate the holding of conference calls in the. al. n. focal firm.. Ch. i n U. v. Thus, I expect the positive association between board interlocks and. engchi. conference calls exists mainly among those interlocking directorates who are also independent directors.. Thus, I predict the coefficient 𝛽1 in both equations (2A) and. (2B) to be positive. CALL = α + 𝛽1 𝐼𝑁𝐷𝐿𝐼𝑁𝐾 + 𝛽2 𝑅𝑂𝐴 + 𝛽3 𝑆𝐼𝑍𝐸 + 𝛽4 𝐿𝐸𝑉 + 𝛽5 𝑀𝐵 + 𝛽6 𝐷𝑆𝐻𝐴𝑅𝐸 + 𝛽7 𝐿𝑆𝐻𝐴𝑅𝐸 + 𝛽8 𝐼𝑆𝐻𝐴𝑅𝐸 + 𝛽9 𝑌𝐸𝐴𝑅 + 𝛽10 𝐼𝑁𝐷 + 𝜀. (2A). NCALL = α + 𝛽1 𝐼𝑁𝐷𝐿𝐼𝑁𝐾 + 𝛽2 𝑅𝑂𝐴 + 𝛽3 𝑆𝐼𝑍𝐸 + 𝛽4 𝐿𝐸𝑉 + 𝛽5 𝑀𝐵 + 𝛽6 𝐷𝑆𝐻𝐴𝑅𝐸 + 𝛽7 𝐿𝑆𝐻𝐴𝑅𝐸 + 𝛽8 𝐼𝑆𝐻𝐴𝑅𝐸 + 𝛽9 𝑌𝐸𝐴𝑅 + 𝛽10 𝐼𝑁𝐷 + 𝜀. (2B). where INDLINK in equation (2A) and (2B) is a dummy variable that equals to 1 if 28.

(35) the focal firm is connected to other call firms through independent directors and 0 otherwise.. 立. 政 治 大. ‧. ‧ 國. 學. n. er. io. sit. y. Nat. al. Ch. engchi. 29. i n U. v.

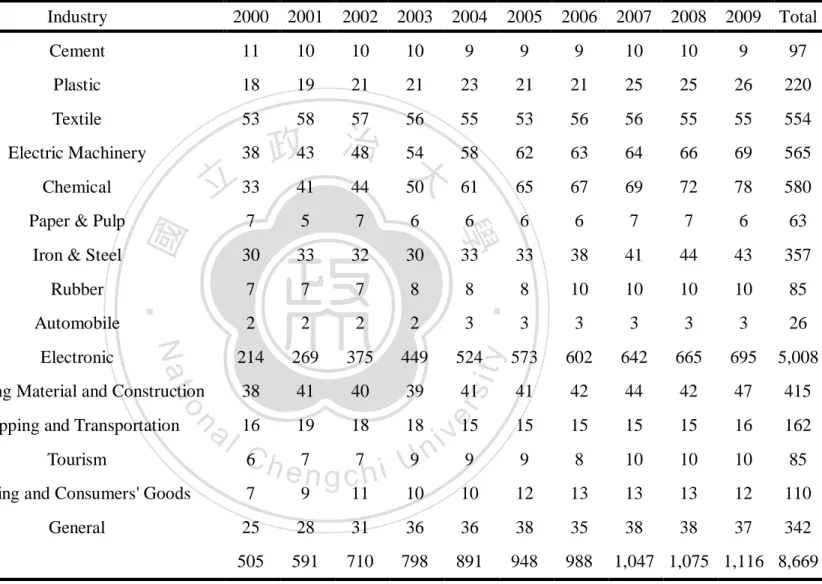

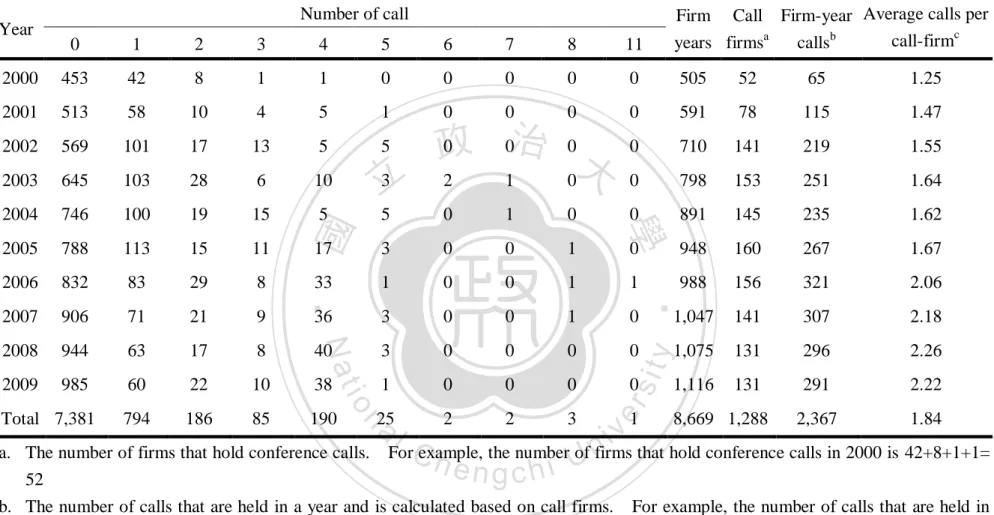

(36) 4. Research Results 4.1 Descriptive Analyses Table 2 provides the distribution of firms in my sample set.. These sample firms. distribute across fifteen industries and for the period 2000- 2009. TWSE and GTSM is increasing yearly.. Firms listed in. More than a half (about 57.77% or 5,008. firm-year observations) of the sample comes from electronics industry, consistent with the fact that electronic industry is the most important part of manufactures.. 政 治 大 my sample. 立 The third and fourth largest. 580. observations (about 6.69%) are from chemical industry, which is the second largest industry in. industry is the electric. ‧ 國. 學. machinery (about 6.52%) and textile (about 6.39%) industry.. Four smallest. percentages of sample firms comes from tourism, rubber, paper & pulp and. ‧. automobile, each of which is less than 1%.. y. Nat. io. sit. Table 3 presents the yearly distribution of conference calls.. From the call firm. n. al. er. column, there is an increasing trend from 2000 to 2005 and reaches the highest in year 2005.. i n U. v. Although the number of firms that hold conference calls slightly decreases. Ch. engchi. after 2005, the number of firms that hold conference calls is still stable.. One. possible explanation for the slightly decrease is that the foreign investors has increased from 18.51% of total stock market value in 2000 to 30.05% in 2009, according to the report on the website of Financial Supervisory Commission in Taiwan. 18. In order to effectively communicate firm value to foreign investors,. Taiwanese firms would hold conference calls overseas or attend calls that are invited by foreign security brokers, either of which are excluded from our sample.. While. year 2005 has the largest number of firms that hold conference calls, year 2006 18. http://www.fsc.gov.tw/ch/ 30.

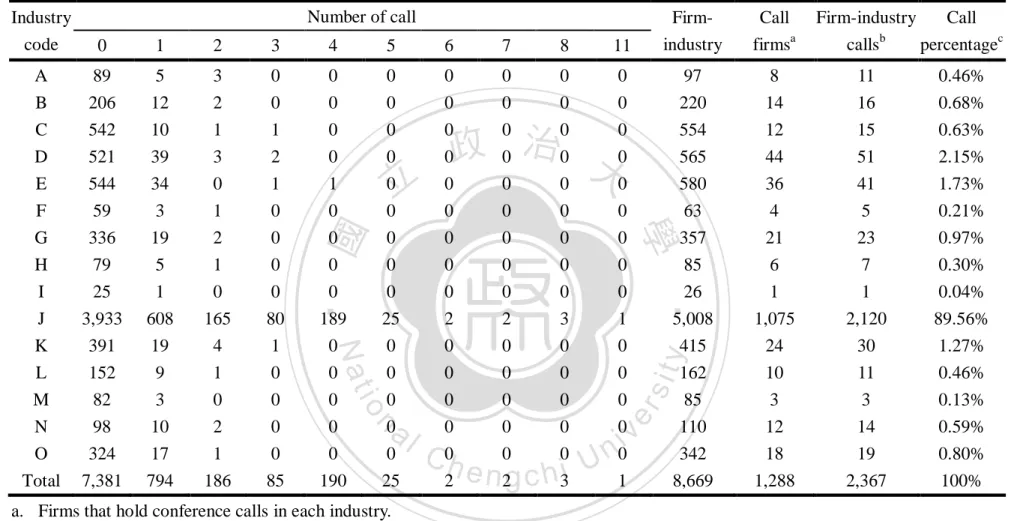

(37) represents the highest frequency of conference calls, i.e. 321 calls within a year.. A. stable trend of conference calls lasts after 2006. For firms that hold conference calls, the average call per year is around 2 during the last four years in my sample period. The relative stability of these numbers implies that the frequency of hold conference calls by listed firms in Taiwan has been relatively constant in recent years. Table 4 illustrates the distribution of conference calls in different industries. Around 89.56% of the calls are held by firms in the electronic industry.. The second. and third largest number of conference calls are in the electric machinery (2.15%) and. 政 治 大 This distribution 立 matches the sample firm distribution in Table 2.. the chemical (1.73%) industry. industries.. Less than 8% of conference calls come from other. ‧ 國. 學. Conference calls held by firms in the electronic industry is up to around 90% in our samples, a situation consistent with the argument held in Chin et al. (2008).. They. ‧. indicate that firms in the electronics sector communicate corporate information. n. al. In Tables 3 and 4, there are 1,288. er. io. statements are unable to reflect their operation.. sit. y. Nat. through conference calls more often than other industries since their financial. v ni. firms that hold conference calls and 7,381 firms that do not.. Ch. engchi U. In percentage terms,. 14.86% of the sample firms hold conference calls while 85.14% do not.. 31.

(38) Table 2. Sample distribution Industry code. Industry. 2000. 2001. 2002. 2003. 2004. 2005. 2006. 2007. 2008. A. Cement. 11. 10. 10. 10. 9. 9. 9. 10. 10. 9. 97. B. Plastic. 18. 19. 21. 21. 23. 21. 21. 25. 25. 26. 220. C. Textile. 53. 58. 57. 56. 55. 53. 56. 56. 55. 55. 554. D. Electric Machinery. 38. 58. 62. 63. 64. 66. 69. 565. E. Chemical. F. Paper & Pulp. G. Iron & Steel. H. Rubber. I. Automobile. J. Electronic. K. Building Material and Construction. L. Shipping and Transportation. M. Tourism. N. Trading and Consumers' Goods. 7. O. General. 50. 61. 65. 67. 69. 72. 78. 580. 7. 5. 7. 6. 6. 6. 6. 7. 7. 6. 63. 30. 33. 32. 30. 33. 33. 38. 41. 44. 43. 357. 7. 7. 7. 8. 8. 8. 10. 10. 10. 10. 85. 2. 2. 2. 2. 3. 3. 3. 3. 3. 3. 26. 214. 269. 375. 449. 524. 573. 602. 642. 665. 695. 5,008. 38. 41. 40. 39. 41. 41. 42. 44. 42. 47. 415. 16. 19. 18. 18. er 15. 15. 15. 15. 15. 16. 162. 9. 9. 8. 10. 10. 10. 85. C 6 h. e7n g c7h i U9. y. sit. ‧ 國 n. 44. ‧. io. al. 41. 學. Nat. TOTAL. 立 33. 48 54 政43 治 大. 2009 Total. v ni. 9. 11. 10. 10. 12. 13. 13. 13. 12. 110. 25. 28. 31. 36. 36. 38. 35. 38. 38. 37. 342. 505. 591. 710. 798. 891. 948. 988. 32. 1,047 1,075 1,116 8,669.

(39) Table 3. Yearly distribution of conference calls 2. 3. 4. 5. 6. 7. 8. 11. 2000. 453. 42. 8. 1. 1. 0. 0. 0. 0. 0. 505. 52. 65. 1.25. 2001. 513. 58. 10. 4. 5. 1. 0. 0. 0. 0. 591. 78. 115. 1.47. 2002. 569. 101. 17. 13. 5. 5. 0. 710. 141. 219. 1.55. 2003. 645. 103. 28. 6. 10. 3 立. 0. 798. 153. 251. 1.64. 2004. 746. 100. 19. 15. 5. 5. 0. 1. 0. 0. 891. 145. 235. 1.62. 2005. 788. 113. 15. 11. 17. 3. 0. 0. 1. 0. 948. 160. 267. 1.67. 2006. 832. 83. 29. 8. 33. 1. 0. 0. 1. 1. 988. 156. 321. 2.06. 2007. 906. 71. 21. 9. 36. 3. 0. 0. 1. 0. 1,047. 141. 307. 2.18. 2008. 944. 63. 17. 8. 40. 3. 0. 0. 0. 0. 1,075. y. 131. 296. 2.26. 2009. 985. 60. 22. 10. 38. 1. 0. 0. 0. sit. 1,116. 131. 291. 2.22. 794. 186. 85. 190. al. 2. 2. 3. 2,367. 1.84. a. The number of firms that hold conference calls.. Ch. 0. er. 25. n. Total 7,381. 0 0治 0 政 大 2 1 0. ‧. 1. io. 0. 學. Firm Call Firm-year Average calls per call-firmc years firmsa callsb. ‧ 國. Number of call. Nat. Year. n engchi U. 1 v i. 8,669 1,288. For example, the number of firms that hold conference calls in 2000 is 42+8+1+1=. 52 b. The number of calls that are held in a year and is calculated based on call firms. For example, the number of calls that are held in 2000 is 42*1+8*2+1*3+1*4= 65 c. The average calls that is held by the conference call firm. In other words, for firms that hold conference calls, average calls is calculated by firm-year calls divided by call firms.. 33.

(40) Table 4. Industrial distribution of conference calls Number of call 11. Firmindustry. Call firmsa. 4. 5. 6. 7. 8. A. 89. 5. 3. 0. 0. 0. 0. 0. 0. 0. 97. 8. 11. 0.46%. B C D E. 206 542 521 544. 12 10 39 34. 2 1 3 0. 0 1 2 1. 0 0 0 1. 0 0 0 0. 0 0 0 0. 0 0 0 0. 0 0 0 0. 0 0 0 0. 政 治 大. 220 554 565 580. 14 12 44 36. 16 15 51 41. 0.68% 0.63% 2.15% 1.73%. F G H. 59 336 79. 3 19 5. 1 2 1. 0 0 0. 0 0 0. 0 0 0. 0 0 0. 0 0 0. 0 0 0. 0 0 0. 63 357 85. 4 21 6. 5 23 7. 0.21% 0.97% 0.30%. I J K L. 25 3,933 391 152. 1 608 19 9. 0 165 4 1. 0 80 1 0. 0 189 0 0. 0 25 0 0. 0 2 0 0. 0 2 0 0. 0 3 0 0. 0 1 0 0. 26 5,008 415 162. 1 1,075 24 10. 1 2,120 30 11. 0.04% 89.56% 1.27% 0.46%. M N O. 82 98 324. 3 10 17. 0 2 1. 0 0 0. 0 0 0. 0 0 0. 0 0 0. 0 0 0. 0 0 0. 0 0 0. 85 110 342. 3 12 18. 3 14 19. 0.13% 0.59% 0.80%. Total. 7,381. 794. 186. 85. 190. 8,669. 1,288. 2,367. 100%. ‧ 國. 立. Nat. io. n. al. 25. Ch 2. e n 2g c h 3i. a. Firms that hold conference calls in each industry. b. The number of calls that firms held in each industry during 2000-2009. (Cement Industry) during 2000-2009. c. The percentage of calls attributed to each industry.. y. 3. sit. 2. er. 1. ‧. 0. 學. Industry code. i n U. 1. v. Firm-industry Call b calls percentagec. For example, there are 11(=1*5+2*3) calls in industry A. For example, 0.46% (=11/2367) of calls come from industry A (Cement. Industry). 34.

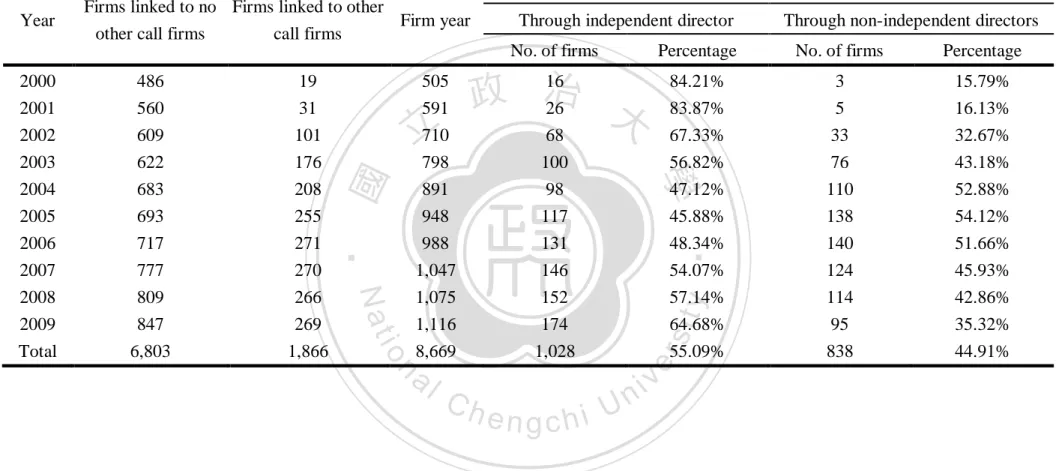

(41) Tables 5 and 6 report the yearly and industrial distribution of the number of other call firms linked to the focal firm.. From table 5, there is an increasing trend in the number of. firms connected to other call firms during the sample period and reaches the highest in year 2006 (271 firms, 27.43%). The number of firms connected to other call firms slightly decrease after year 2006 but the trend remains stable.. While year 2006 has the most firms. connected to other call firms (271 focal firms), year 2007 has the most call firms (720 call firms) connected to the focal firms.. A slightly decrease but stable trend is also maintained. 政 治 大 2007, the highest during the 10-year sample period. Overall, the average number of call 立 after year 2007.. The average number call firms connected to each focal firm is 2.67 in year. firms linked to the focal firm during the sample period is 2.21.. In other words, 2.21 call. ‧ 國. 學. firms are connected to each focal firm during 2000- 2009. Table 6 shows that electronic. ‧. industry has the most number of firms linked to other call firms and most number of call On the. sit. y. Nat. firms connected to focal firms, consistent with the industrial environment in Taiwan.. io. the fewest number of call firms connected to the focal firm.. al. er. contrary, paper & pulp industry has the fewest number of firms linked to other call firms and In percentage, 29.43% of firms. n. v i n Ctoh other call firms U in electronic industry are connected through interlocked directors— the engchi highest among 15 industries, while 3.17% of firms in paper & pulp industry are connected to other call firms— the lowest among 15 industries.. Automobile industry has the highest. average number of call firms connected to each focal firm (3.83 call firms), while the rubber industry has the lowest. average number (1.25 call firms).. Tables 7 and 8 further indicate the yearly and industrial distribution of board interlocking ties through two different board positions.. In table 7, the percentage that firms linked to. other call firms through independent directors is decreasing from year 2000 and reaches the lowest in year 2005 (45.88%).. After year 2005, the trend goes up in the last three years in 35.

(42) the sample period.. Table 8 shows that, all the firms connected to other call firms are. through independent directors in cement and trading and consumers’ goods industry.. None. of the firm is connected to other call firms through independent directors in automobile industry.. Overall, for firms connected to other call firms, 55.09% are connected through. independent directors.. 立. 政 治 大. ‧. ‧ 國. 學. n. er. io. sit. y. Nat. al. Ch. engchi. 36. i n U. v.

(43) Table 5. Yearly distribution of the number of other call firms linked to the focal firm Number of call firms. Firms linked Firms linked Linked call Average linked a to call firms to call firms (%) firmsb call firmsc. 1. 2. 3. 4. 5. 6. 7. 8. 2000. 486. 11. 6. 2. 0. 0. 0. 0. 0. 505. 19. 3.76%. 29. 1.53. 2001 2002 2003 2004. 560 609 622 683. 23 67 104 121. 5 20 38 41. 0 8 11 30. 1 4 15 4. 2 2 7 10. 0 0 0 2. 0 0 1 0. 0 0 0 0. 591 710 798 891. 31 101 176 208. 政 治 大. 5.25% 14.23% 22.06% 23.34%. 47 157 315 371. 1.52 1.55 1.79 1.78. 2005 2006 2007. 693 717 777. 153 116 92. 19 54 43. 36 18 27. 41 81 97. 6 0 5. 0 0 0. 0 0 0. 0 2 6. 948 988 1,047. 255 271 270. 26.90% 27.43% 25.79%. 493 618 720. 1.93 2.28 2.67. 2008 809 96 2009 847 91 Total 6,803 874. 47 42 315. 20 26 178. 93 104 440. 10 6 48. 0 0 2. 0 0 1. 0 0 8. 1,075 1,116 8,669. 266 269 1,866. 24.74% 24.10% 21.52%. 672 699 4,121. 2.53 2.60 2.21. sit. Nat. y. ‧. ‧ 國. 立. 學. 0. Firm Year. Year. a. The number of firms that are linked to other call firms through board interlocks during the year.. For example, 19 (= 11+6+2) firms. io. n. al. er. are connected to at least 1 other firm that holds conference calls in year 2000. b. The total number of other call firms linked to the focal firm through board interlock. For example, in year 2000, 11 firms connected to 1 other call firm, 6 firms connected to 2 others and 2 firms connected to 3 others. 29= 11*1+6*2+2*3. Ch. engchi. i n U. v. c. The average number of other firms that hold conference calls and are tied to the focal firms. For example, for each firm that is linked to other call firms, 1.53 (=29/19) other call firms on average are connected to the focal firm in year 2000.. 37.

(44) Table 6. Industrial distribution of the number of other call firms linked to the focal firm Number of call firms. Firms linked Linked call Average linked Firm Firms linked a Industry to call firm to call firm (%) firmsb call firmsc. 0. 1. 2. 3. 4. 5. 6. 7. 8. A. 83. 8. 3. 1. 2. 0. 0. 0. 0. 97. 14. 14.43%. 25. 1.79. B C D E. 185 531 477 496. 20 16 54 44. 3 3 14 17. 1 3 6 7. 7 1 14 15. 1 0 0 1. 0 0 0 0. 0 0 0 0. 3 0 0 0. 220 554 565 580. 35 23 88 84. 15.91% 4.15% 15.58% 14.48%. 86 35 156 164. 2.46 1.52 1.77 1.95. F G H. 61 331 73. 1 19 9. 1 3 3. 0 2 0. 0 2 0. 0 0 0. 0 0 0. 0 0 0. 0 0 0. 63 357 85. 2 26 12. 3.17% 7.28% 14.12%. 3 39 15. 1.50 1.50 1.25. 1 259 5. 0 146 3. 4 373 12. 1 39 3. 0 2 0. 0 1 0. 0 5 0. 26 5,008 415. 6 1474 44. 23.08% 29.43% 10.60%. 23 3,351 103. 3.83 2.27 2.34. 9.88%. 40. 2.50. 4.71% 14.55% 6.43%. 11 42 28. 2.75 2.63 1.27. 21.52%. 4,121. 2.21. 2. 2. 0. 0. 0. 162. 16. M N O. 81 94 320. 2 4 20. 0 3 0. 0 4 0. 1 5 2. 1 0 0. 0 0 0. 0 0 0. 0 0 0. 85 110 342. 4 16 22. 315. 178. 440. 48. 2. n. Total 6,803 874. al. 1. Ch. e n8,669 gchi. 8. y. 5. sit. 0. er. 7. ‧. 146. 學. L. io. 20 0 3,534 649 371 21. 立. 政 治 大. Nat. I J K. ‧ 國. Industry code. i n U 1,866. v. a. The number of firms that are linked to other call firms through board interlocks in each industry during 2000-2009. For example, 14 (= 8+3+1+2) firms are linked to at least 1 other firm that holds conference calls in industry A (Cement Industry) during 2000-2009. b. The total number of other call firms linked to the focal firm through board interlocks. For example, in industry A (Cement Industry), 8 firms link to 1 other call firm, 3 firms link to 2 others, 1 firm link to 3 others and 2 firms link to 4 others. 29= 11*1+6*2+2*3 c. The average number of other call firms tied to the focal firms. 38. For example, for each firm that is linked to other call firms in.

(45) industry A (Cement Industry), 1.79 (=25/14) other call firms on average are connected to the focal firm.. 立. 政 治 大. ‧. ‧ 國. 學. n. er. io. sit. y. Nat. al. Ch. engchi. 39. i n U. v.

數據

+7

相關文件

5.1.1) 法團校 董會以 受託人 身 分擁 有及 處 理由政 府發放 給學校 的經費 及資 產。法 團校董 會亦以 同樣的身分擁 有及處理由學生繳交的堂費 及由 公眾人士給予學校的捐贈。.

Adolescents who conducted doxing had greater odds of disclosing others’ personal information, students who had conducted doxing had also experienced information disclosure as

捐贈財產清冊及證明文 件、董事名冊、戶籍謄本 及印鑑;設有監察人 者,其名冊、戶籍謄本 及印鑑、法人登記書影 本及法人印鑑、董事會 議紀錄、直接監機關同

It is important to use a variety of text types, including information texts, with content-area links, as reading materials, to increase students’ exposure to texts that they

An information literate person is able to recognise that information processing skills and freedom of information access are pivotal to sustaining the development of a

Zarowin (2010), “Accrual-based and real earnings management activities around seasoned equity offerings,” Journal of Accounting and Economics, Vol. Larcker (1999),

Disclosure and Transparency: The corporate governance framework should ensure that timely and accurate disclosure is made on all material matters regarding the corporation,

校董會組成的規定 校董會各類成員的人數包括校監 社會人士 營辦機構 其他持份 者 家長、 出任獨立 提名 教師或校 校董