於德語系國家提供3D列印積層製造技術之可行性分析 - 政大學術集成

104

0

0

全文

(2) 於德語系國家提供3D列印積層製造技術之可行性分析 Analysis on the feasibility of providing additive manufacturing services in German speaking countries 研究生:史雅倫. Student: Arnold Roland Steinbrecher. 指導教授:蔡政憲. Advisor: Jason Tsai. 國立政治大學. 學. ‧ 國. 立. 政 治 大. ‧. 商學院國際經營管理英語碩士學位學程. er. io. A Thesis. sit. y. Nat. 碩士論文. n. a l to International MBA Program Submitted iv n U i National Chengchi e n g c hUniversity. Ch. in partial fulfillment of the Requirements for the degree of Master in Business Administration. 中華民國一〇三年六月 June 2014.

(3) Abstract Analysis on The Feasibility of Providing Additive Manufacturing Services in German Speaking Countries By Arnold Roland Steinbrecher ‘People can have the Ford Model T in any color – as long as it‘s black‘ (Henry Ford). 治 政 大side of the globe. Product life cycles advantages solely on cheap mass production on the other 立 become shorter, customers more demanding, cost advantages of producing large amounts far In today’s competitive business environment, more is needed than building competitive. ‧ 國. 學. from the distribution channels are eroding and flexibility in production is an essential parameter to meet customer’s demands.. ‧. The purpose of this business plan is to show small and medium sized enterprises (SMEs) a. sit. y. Nat. possibility to conquer constrains of mass production by using one of the few real disruptive technologies of our times. 3D printing or additive manufacturing indeed has the potential to. io. er. change the paradigm for manufacturing.. al. n. v i n C h solid three-dimensional In short, it is the process of building e n g c h i U objects from any digital model data by applying materials usually layer upon layer. This method of building parts of virtually every shape is the reason for the name as opposed to subtractive or traditional manufacturing, where material is being removed by drilling, cutting, and milling. Additive manufacturing technologies can be used anywhere in the product life cycle from preproduction prototypes to full-scale production: On the entry level, small and medium sized enterprises could increase their performance through cost reduction by accelerating the business cycle. This is an implication of reduced time to market and improved product quality.. i.

(4) The next level not only involves speed but also cost savings arising out of supply chain improvements. Additive manufacturing is able to significantly reduce required inventory and therefore is reducing working capital requirements. The third level takes full advantage of this new technology, exploiting the complexity for free phenomenon, which demonstrates that geometrically complex shapes can be produced at virtually no additional costs. Last but not least, while putting all the advantages of additive manufacturing, masscustomization of products becomes an available option even for smaller companies.. 治 政 大the industry is still small in absolute The described paradigm shift already started, and although 立 terms, growth rates have been impressive for the last few years. The global additive ‧ 國. 學. manufacturing market grew by 34.9% (CAGR) to US$ 3.07 billion in 2013, which is a continuation of the remarkable growth rates of 2010, 2011, and 2012. Even more exciting are. ‧. the forecasts, which indicate that additive manufacturing could easily exceed US$ 21 billion by 2020. (cf. McKinsey Global Institute, 2013; Wohlers Associates Inc., 2014). The german. y. Nat. sit. speaking market is about 15% of the global additive manufacturing market with players being. al. er. io. more educated in terms of additive manufacturing. Thus, it seems to be the right time to enter. n. this market eager for innovation.. Ch. engchi. i n U. v. This business plan proposes to set-up an additive manufacturing service provider in Austria, targeting the German speaking countries, and offering its services to mainly but not exclusively small and medium sized enterprises. Since the competition is existent but very segmented, the declared goal of 5% market share should be manageable in the first three years of operation. The main target clients are SME’s in the following fields: Manufacture of fabricated metal products and machinery and equipment Manufacture of motor vehicles, trailers, and semi-trailers Manufacture of furniture. ii.

(5) Manufacture of jewelry, bijouterie, and related articles Manufacture of medical and dental instruments and supplies 3magination, which is the proposed name for the company, shall provide the following services: Additive manufacturing education Design consultancy Material consultancy. 政 治 大 Small series production and prototyping 立. ‧ 國. 學. However, the business model classifies the first three services as trust and relationship building investments and the company only charges for the production itself. 3magination disposes of. ‧. metal and polymer processing printers and is able to produce a very large spectrum of objects. Design, material selection, and the flexible production itself are 3maginations’s declared. y. sit. io. er. performed.. Nat. competitive advantages. To ensure this path, a detailed analysis of key talents has been. al. n. v i n loan facility from banks of EUR C 1.92 generate a NPV of EUR 25.5 million. Due hmillion e n gwould chi U Considering the conservative forecasts, initial investment of EUR 1.1 million in equity and a. to the large investments in fixed assets and the low sales volume at the beginning, a loss is. anticipated in the first year. However, the company breaks even in the second year of operation and makes a small profit of EUR 286,394. From there on, the net income and sales ratio starts accelerating up to 34% in 2019.. Keywords: (3D printing) (additive manufaturing) (service provider) (German speaking countries). iii.

(6) TABLE OF CONTENTS 1. Introduction to Additive Manufacturing ........................................................................... 1 1.1 Definition of Additive Manufacturing and 3D Printing .......................................................... 1 1.2 Advantages of Additive Manufacturing.................................................................................... 2 1.3 Disadvantages of Additive Manufacturing ............................................................................... 4 1.4 Additive Manufacturing Process Technologies ........................................................................ 6. 治 政 大 1.5 Additive Manufacturing System Manufacturers ................................................................... 11 立 ‧ 國. 學. 1.6 Current Status of Additive Manufacturing ............................................................................ 12. 2. Market Analysis .................................................................................................................. 14. ‧. 2.1 Overview .................................................................................................................................... 14. y. Nat. al. er. io. sit. 2.2 Additive Manufacturing Industry Structure.......................................................................... 15. n. 2.3 Additive Manufacturing in Figures ......................................................................................... 16. Ch. engchi. i n U. v. 2.3.1 Laser-Sintered Polymers Market ......................................................................................... 17 2.3.2 Laser-Sintered Metals Market ............................................................................................. 18 2.4 The Austrian Manufacturing Landscape ............................................................................... 18 2.4.1 Potential Clients................................................................................................................... 19 2.4.2 Market Study ....................................................................................................................... 21 2.5 Additive Manufacturing Market Size in German Speaking Countries ............................... 24. 3. Competitor Analysis ........................................................................................................... 26 iv.

(7) 3.1 Additive Manufacturing Service Provider ............................................................................. 26 3.2 Austria........................................................................................................................................ 27 3.3 Germany .................................................................................................................................... 29 3.4 Switzerland ................................................................................................................................ 31 3.5 International Competitors........................................................................................................ 32 3.6 Five Forces Analysis ................................................................................................................. 34. 政 治 大. 3.6.1 Suppliers .............................................................................................................................. 34. 立. 3.6.2 Customers ............................................................................................................................ 35. ‧ 國. 學. 3.6.3 Substitutes............................................................................................................................ 35. ‧. 3.6.4 New Market Entrants ........................................................................................................... 36. Nat. io. sit. y. 3.6.5 Direct Competitors .............................................................................................................. 37. er. 4. Company Profile ................................................................................................................. 38. al. n. v i n 4.1 Legal Background ..................................................................................................................... 38 Ch engchi U 4.2 Human Assets ............................................................................................................................ 39 4.3 Fixed Assets: 3D Printers ......................................................................................................... 46 4.3.1 Metal Laser-Sintering Printer .............................................................................................. 46 4.3.2 Polymer Laser-Sintering Printer .......................................................................................... 51 4.3.3 Stereolithography Printer..................................................................................................... 54 4.3.4 Investment Schedule ............................................................................................................ 57. v.

(8) 5. Services ................................................................................................................................ 59 5.1 Additive Manufacturing Education ........................................................................................ 59 5.2 Design Consultancy................................................................................................................... 60 5.3 Material Consultancy ............................................................................................................... 61 5.4 Small Series Production and Prototyping............................................................................... 61 5.5 SWOT Analysis ......................................................................................................................... 62. 政 治 大. 5.5.1 Strengths .............................................................................................................................. 62. 立. 5.5.2 Weaknesses.......................................................................................................................... 62. ‧ 國. 學. 5.5.3 Opportunities ....................................................................................................................... 63. ‧. 5.5.4 Threats ................................................................................................................................. 63. y. Nat. io. sit. 6. Marketing and Sales ........................................................................................................... 64. er. 6.1 Marketing Strategy ................................................................................................................... 64. al. n. v i n Ch 6.1.1 Promotion ............................................................................................................................ 64 engchi U 6.1.2 Price ..................................................................................................................................... 64 6.1.3 Place (Distribution) ............................................................................................................. 67. 6.2 Market Segmentation ............................................................................................................... 68 6.3 Sales Strategy ............................................................................................................................ 68 6.4 Sales Forecast ............................................................................................................................ 69. 7. Financial Information ........................................................................................................ 71. vi.

(9) 7.1 Funding ...................................................................................................................................... 71 7.1.1 Equity Investors ................................................................................................................... 71 7.1.2 Bank Loans .......................................................................................................................... 71 7.2 General Assumptions ................................................................................................................ 72 7.3 Profit and Loss Statement ........................................................................................................ 72 7.4 Cash Flow Statement ................................................................................................................ 74. 政 治 大. 7.5 NPV and Sensitivity Analysis ................................................................................................... 75. 立. 7.6 Balance Sheet............................................................................................................................. 77. ‧ 國. 學. 8. Conclusion ........................................................................................................................... 79. ‧. Reference ................................................................................................................................. 80. y. Nat. io. sit. Books:............................................................................................................................................... 80. er. Documents from Webpages: .......................................................................................................... 80. al. n. v i n Ch Interviews: ....................................................................................................................................... 80 engchi U Journals: .......................................................................................................................................... 81 Statistics: .......................................................................................................................................... 81 Internet References: ....................................................................................................................... 81. Appendix A: Companies and Interviewee in Sample-Size ................................................. 84 Appendix B: Market Size Calculation Data ......................................................................... 86 Appendix C: Competition ...................................................................................................... 87 vii.

(10) Competition in Austria:.................................................................................................................. 87 Competition in Germany: .............................................................................................................. 88 Competition in Switzerland: .......................................................................................................... 90 Competition Worldwide: ................................................................................................................ 91. 立. 政 治 大. ‧. ‧ 國. 學. n. er. io. sit. y. Nat. al. Ch. engchi. viii. i n U. v.

(11) List of Figures and Table Figure 1: Process of layer-by-layer production. (Source: Direct Manufacturing Research Center (DMRC), 2013). ............................................................................................. 2 Figure 2: Complexity for free. (Source: Merkt at al., 2012). ..................................................... 3 Figure 3: Breakeven analysis comparing conventional and additive manufacturing processes. (Source: Deloitte University Press, 2014) ................................................................. 5 Figure 4: Material extrusion. (Source: Additively Ltd., 2014). .................................................. 7 Figure 5: Material jetting. (Source: Additively Ltd., 2014). ...................................................... 8. 治 政 大 Figure 7: Sheet lamination. (Source: Thre3D, 2014). ................................................................ 9 立 Figure 8:Vat photopolymerization. (Source: Additively Ltd., 2014). ........................................ 9 Figure 6: Binder jetting. (Source: Additively Ltd., 2014). ......................................................... 8. ‧ 國. 學. Figure 9: Power bed fusion. (Source: Additively Ltd., 2014). ................................................. 10 Figure 10: Directed energy deposition. (Source: Additively Ltd., 2014). ................................ 11. ‧. Figure 11: Leading AM system manufacturer in 2013. (Source: Wohlers Associates Inc., 2014). ..................................................................................................................... 12. y. Nat. sit. Figure 12: Industries applying additive manufacturing. (Source: cf. Wohlers Associates Inc.,. al. er. io. 2014.) ..................................................................................................................... 14. n. Figure 13: How AM parts are being used? (Source: cf. Wohlers Associates Inc., 2014). ....... 15. Ch. i n U. v. Figure 14: Service provider revenue estimates (in millions of US$) (Source: cf. Wohlers. engchi. Associates Inc., 2014). ........................................................................................... 17 Figure 15: Revenue from metals powder for laser-sintering in US$ million Source: (Wohlers Associates Inc., 2014). ........................................................................................... 18 Figure 16: Number and total sales of potential Austrian companies in 2011. (Source: cf. Statistik Austria, 2014). ......................................................................................... 20 Figure 17: Probability of additive manufacturing application in production. (Source: cf. Jukic, 2014)............................................................................................................ 22 Figure 18: General application of 3D printer in companies other than production. (Source: cf. Jukic, 2014)............................................................................................................ 23 Figure 19: Current applications of 3D printed parts in sample-size. (Source: cf. Jukic, 2014). ............................................................................................................................... 24 ix.

(12) Figure 20: Selected AM metals service manufacturer. (Source: Roland Berger, 2013). ......... 27 Figure 21: EOS M400 (Source: EOS GmbH, 2014). ............................................................... 47 Figure 22: EOS M290 (Source: EOS GmbH, 2014). ............................................................... 49 Figure 23: EOS P396 (Source: EOS GmbH, 2014).................................................................. 51 Figure 24: EOSINT P760 (Source: EOS GmbH, 2014). .......................................................... 53 Figure 25: 3D Systems ProX 950 (Source: 3D Systems Inc., 2014). ....................................... 55 Figure 26: Different print qualities of 3D printer (Source: cf. RedEye, 2014). ....................... 66 Figure 27: Results of three different building orientations in a medium quality print (Source: RedEye, 2014). ...................................................................................................... 67. 治 政 Table 1: Fictional scenario analysis with improvements 大 to multiple AM variables. (Source: 立 Wohlers Associates Inc., 2014). ................................................................................... 6 ‧ 國. 學. Table 2: Current commercial or near to market applications of AM relative to sectors. (Source: AM SIG, 2012). ......................................................................................... 13. ‧. Table 3: Potential target industry categories. (Source: own compilation). .............................. 21 Table 4: AM market size in Austria, Germany and Switzerland in EUR. (Source: own. y. Nat. sit. compilation). ............................................................................................................. 25. al. er. io. Table 5: Summarized financial payroll. (Source: own compilation): ...................................... 45. n. Table 6: Technical data EOS M400 (Source: EOS GmbH, 2014). .......................................... 48. Ch. i n U. v. Table 7: Technical data EOS M290 (Source: EOS GmbH, 2014). .......................................... 50. engchi. Table 8: Technical data EOS P396 (Source: EOS GmbH, 2014). ........................................... 52 Table 9: Technical data EOSINT P760 (Source: EOS GmbH, 2014). ..................................... 54 Table 10: Technical data 3D Systems ProX 950 (Source: 3D Systems Inc., 2014). ............... 56 Table 11: 3magination’s 3D printer machine park (Source: own compilation). ...................... 57 Table 12: 3D printer prices and depreciation costs (Source: own compilation). ..................... 57 Table 13: 3D printer electricity consumption incl. other utilities. (Source: own compilation with data from Tu, 2014). ......................................................................................... 58 Table 14: Market segmentation and forecasted amount of orders. (Source: own compilation). .................................................................................................................................. 68 Table 15: Sales forecast in EUR. (Source: own compilation). ................................................. 70 Table 16: Pro forma income statement in EUR (Source: own compilation). ........................... 72 x.

(13) Table 17: Pro forma cash flow statement in EUR. (Source: own compilation). ...................... 75 Table 18: Computation of WACC. (Source: own compilation with Data from Bloomberg, 2014 and anonymous M&A boutique). .................................................................... 76 Table 19: Sensitivity analysis. (Source: own compilation). ..................................................... 77 Table 20: Pro forma balance sheet. (Source: own compilation)............................................... 78 Table 21: Additive manufacturing service provider market size in EUR. (Source: cf. Wohlers Associates Inc., 2014)............................................................................................... 86 Table 22: GDP breakdown of manufacturing at current US$ prices. (Source: own compilation with data from United Nations, 2013). ..................................................................... 86. 立. 政 治 大. ‧. ‧ 國. 學. n. er. io. sit. y. Nat. al. Ch. engchi. xi. i n U. v.

(14) 1. Introduction to Additive Manufacturing 3D printing or additive manufacturing (AM) has experienced a huge medial hype in recent years, mostly due to the steep price decrease for consumer desktop printers, which are available for prices as low as US$4991. Other headlines, like human prosthesis or bio-printing of living organs, are certainly other reasons for the actual public interest to the topic.. 1.1 Definition of Additive Manufacturing and 3D Printing Nowadays, the term additive manufacturing is used interchangeably with the term 3D printing. 政 治 大 solid three-dimensional objects 立from any digital model data by applying materials usually layer and rapid prototyping, referring to a group of technologies2. It describes the process of building. ‧ 國. 學. upon layer. This method of building parts of virtually every shape is the reason for the name as opposed to subtractive or traditional manufacturing, where material is being removed by drilling, cutting and milling. (cf. Roland Berger, 2013).. ‧. n. er. io. sit. y. Nat. al. 1 2. Ch. engchi. i n U. v. Taiwan’s XYZprinting company sells its cheapest “da Vinci” 3D printer for US$499. In this business plan, additive manufacturing and 3D printing are also used interchangeably.. 1.

(15) 政 治 大. 立. ‧ 國. 學. Figure 1: Process of layer-by-layer production.. (Source: Direct Manufacturing Research Center (DMRC), 2013).. ‧. Surprisingly, the technology itself is already more than 26 years old and was actually invented by the founder of one of today’s largest 3D printer manufacturer: 3D Systems Inc. This. y. Nat. sit. company commercialized its stereolithography printer in 1989. The first metal additive. al. er. io. manufacturing system was introduced in 1995. (cf. 3D Systems Inc., 2014). In general, this. n. truly disruptive technology is most commonly used to build physical models, prototypes,. Ch. i n U. v. patterns, tooling components, and production parts in plastic, metal, ceramic, glass, and. engchi. composite materials. (cf. Wohlers Associates Inc., 2014).. 1.2 Advantages of Additive Manufacturing The advantages of 3D printing are vast compared to traditional manufacturing. In the following, a few advantages will be listed: . Wide freedom of design: One of the best things about additive manufacturing is that it enables to print objects that simply cannot be produced with traditional manufacturing methods (i.e.: a ball inside a ball). Due to this high degree of flexibility, even internal cavities or structures can be produced, which are interesting for cooling systems amongst others. All 2.

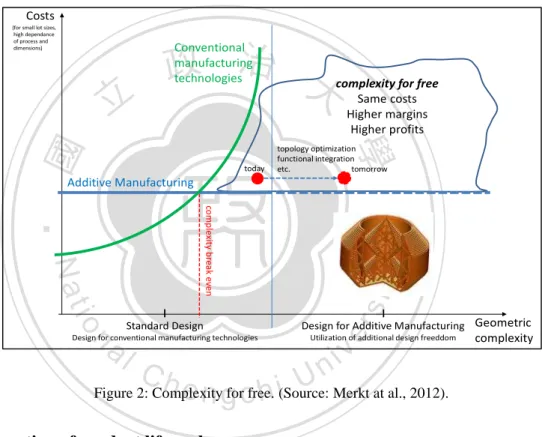

(16) constraints on tooling and machining are eliminated, which also gives a push to http://sajie.journals.ac.za. lightweight parts production especially in the aerospace industry. . Complexity for free: Due to the layer-by-layer building of any given object, it actually doesn’t make a. technologies, manufacturing costs for additive manufacturing (AM) technologies like SLM do. not normally increase with higher geometric complexity. difference whether the printer produces a simple ball or a very complex part. Therefore, In some cases, higher shapes geometric complexity leads to higherperformance preprocessingcan costs SLM (e.g. geometrically complex with increased functional beofproduced platform assembly, backing, scanning strategy, etc.). At the same time, high geometric. at virtually no often additional Below figure brings complexity coststime intofor relation. complexity meanscost. lower build volumes: this decreases theand process SLM and equalises the additional preprocessing costs. Costs (for small lot sizes, high dependance of process and dimensions). today. complexity for free Same costs Higher margins Higher profits. 學. ‧ 國. 立. 政 治 大 Conventional manufacturing technologies. topology optimization functional integration etc. tomorrow. Additive Manufacturing. Design for Additive Manufacturing Geometric. er. io. sit. y. ‧. complexity break even. Nat Standard Design. complexity a v i Figurel 2: The idea of ‘Complexity for Free’ according to [9] n C ha standard design, U For products that exceed SLM can beat economically superior due to e n gforcfree. Figure 2: Complexity al., 2012). h i(Source: Merkt. n. Design for conventional manufacturing technologies. . . Utilization of additional design freeddom. apparent cost drivers of conventional technologies. Functionally-optimised designs (‘design for AM’) can improve product performance at the same cost. This idea of ‘complexity for free’, usingofthe additional Acceleration product life design cycle: freedom of SLM, is shown in Figure 2. Today several applications exceed a certain amount of economical standard design (‘complexity breakare manufactured more economically SLM.can Thebe additional design reduced freedom Dueeven’) to theand flexibility 3D printing offers, time towith market significantly through SLM could be used for future applications that use geometric complexity to improve while enhancing productatquality. This efficiency reduces costs. innovative product performance the same costs (see Fig. consequently 2). Furthermore, SLM enables business models through product individualisation because costs are independent of lot size Supply chain improvements: – in contrast with conventional manufacturing processes.. Since it is possible to produce small series at no additional costs with additive 2.. INTEGRATED TECHNOLOGY EVALUATION MODEL (ITEM). manufacturing, are evaluating able to significantly required inventory The general companies objective when technologies lower is to determine the impactand of technology decisions on a given valuation standard [9]. Technology evaluation is an therefore decreasing working capital requirements. important tool for technology management; it supports the selection, planning, controlling, . andcustomization: positioning of technology. Without targeted technology management, it is difficult for Mass companies to succeed when their surroundings change, and to fulfil increasing market/product requirements. Adaptation to these changes needs to be performed at the technological level. Long-term strategic technology decisions can lead to significant competitive advantages, and build a key point for the future viability of companies.. There are several approaches to general technology evaluation in production that focus on different evaluation criteria. None of3 them can integrate all the criteria relevant to supporting a comprehensive decision-making process. None of the decision methods listed by [10] can support the decision-making process if highly innovative manufacturing methods are evaluated because of their focus either on product or process. Highly innovative manufacturing technologies such as SLM have an.

(17) This could also be referred to more individualization of customers. Due to additive manufacturing even small and medium sized companies are able to offer variation of mass-produced goods or even offer a product on demand for a single customer. . Use of new materials: Although not all materials are available for additive manufacturing, a range of new composite materials with new properties was developed. Among them are biocompatible metals that can be used for implants as well as polymers supporting high temperatures and reaching stiffness of metals.. . 政 治 大. Practically no waste:. 立. Since the printers apply the necessary materials layer by layer, practically no waste is. ‧ 國. 學. being produced. All leftovers can be reused after having been filtered. Some restrictions apply to this rule, where polymer powder gets unusable after more than 12 times. (cf.. ‧. Tu, 2014). As a result, the manufacturing footprint is much smaller than for traditional production.. y. Nat. Less pollution:. sit. . al. n. is safer for humans and the environment. . Ch. Minimal overhead costs:. engchi. er. io. Since additive manufacturing doesn’t use any toxic chemicals of measurable amount it. i n U. v. 3D printer work 24 hours practically unattended, once the printing job is set up. This and the fact that no assembling is necessary imply that labor costs can be kept down and additive manufacturing also pays off in high-income countries.. 1.3 Disadvantages of Additive Manufacturing Of course, 3D printing also comes with certain restrictions. . Speed: Considering the net production time of one single piece, additive manufacturing is much slower. However, the ability to consolidate several machining steps into a single manufacturing step relativizes the argument as well as the time savings because. 4.

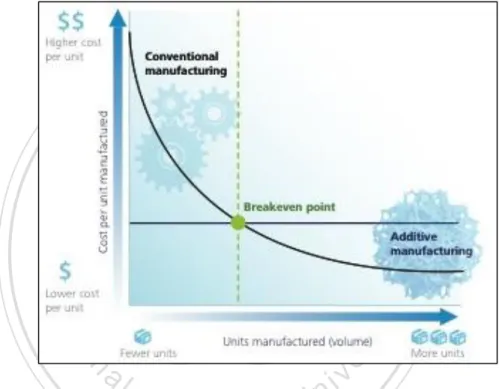

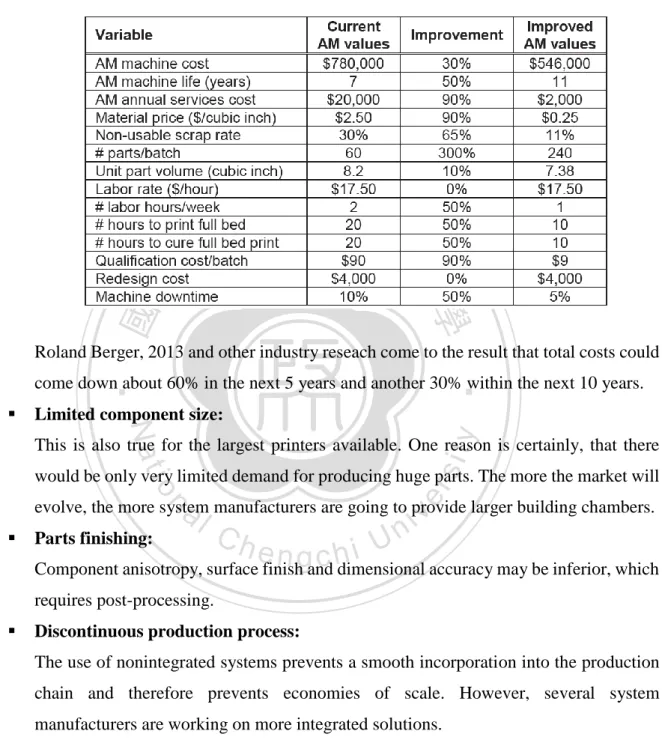

(18) assembling is not necessity. Furthermore, the overall time to market is being increased. Yet, according to industry’s experts, the production time will quadruple by 2018. High production cost: In accordance with the low building rates and relatively high costs for the materials, production costs per item are much higher than for traditional manufacturing. In figure 3, the breakeven point of the two manufacturing technologies is made visible.. 立. 政 治 大. 學 ‧. ‧ 國 io. sit. y. Nat. er. . al. n. v i n C hcomparing conventional Figure 3: Breakeven analysis i U and additive manufacturing processes. e h n c g (Source: Deloitte University Press, 2014). As a result, for the time being, additive manufacturing only pays off for small series production. The table bellows shows that additive manufacturing actually could become cost-effective compared to injection molding if the stated improvements would occur:. 5.

(19) Table 1: Fictional scenario analysis with improvements to multiple AM variables. (Source: Wohlers Associates Inc., 2014).. 政 治 大. 立. ‧ 國. 學. Roland Berger, 2013 and other industry reseach come to the result that total costs could. ‧. come down about 60% in the next 5 years and another 30% within the next 10 years. Limited component size:. y. Nat. . sit. This is also true for the largest printers available. One reason is certainly, that there. al. er. io. would be only very limited demand for producing huge parts. The more the market will. v. n. evolve, the more system manufacturers are going to provide larger building chambers. . Parts finishing:. Ch. engchi. i n U. Component anisotropy, surface finish and dimensional accuracy may be inferior, which requires post-processing. . Discontinuous production process: The use of nonintegrated systems prevents a smooth incorporation into the production chain and therefore prevents economies of scale. However, several system manufacturers are working on more integrated solutions.. 1.4 Additive Manufacturing Process Technologies Over the years, many different technologies evolved that all belong to the group of additive manufacturing. Moreover, every system manufacturer started to name the technologies. 6.

(20) differently, so that the result is a vast soup of terminology. The ASTM 3 International Committee F42 on Additive Manufacturing Technology approved the following names and definitions: (cf. ASTM, 2014) . Material extrusion: is an additive manufacturing process in which material is selectively dispensed through a nozzle or orifice. Most common synonym is fused deposition modeling. This is the technology used for all cheap desktop prosumer printers that entered the market recently.. 立. 政 治 大. ‧. ‧ 國. 學. n. er. io. sit. y. Nat. al. Ch. engchi. i n U. v. Figure 4: Material extrusion. (Source: Additively Ltd., 2014).. . Material jetting: is an additive manufacturing process in which droplets of build material is selectively deposited.. 3. ASTM stands for American Society for Testing and Materials.. 7.

(21) 政 治 大. 立. Figure 5: Material jetting. (Source: Additively Ltd., 2014).. ‧ 國. 學. . Binder jetting: is an additive manufacturing process in which a liquid bonding agent is. ‧. selectively deposited to join powder materials.. n. er. io. sit. y. Nat. al. Ch. engchi. i n U. v. Figure 6: Binder jetting. (Source: Additively Ltd., 2014).. . Sheet lamination: is an additive manufacturing process in which sheets of material are bonded to form an object. 8.

(22) 立. Figure 7: Sheet lamination. (Source: Thre3D, 2014).. ‧ 國. 學. Vat photopolymerization: is an additive manufacturing process in which liquid. ‧. photopolymer in a vat is selectively cured by light activated polymerization. This. io. sit. y. Nat. technology is normally and also in this work referred to as stereolithography.. n. al. er. . 政 治 大. Ch. engchi. i n U. v. Figure 8:Vat photopolymerization. (Source: Additively Ltd., 2014).. 9.

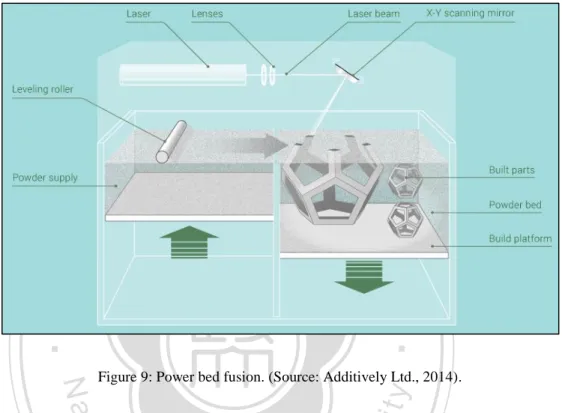

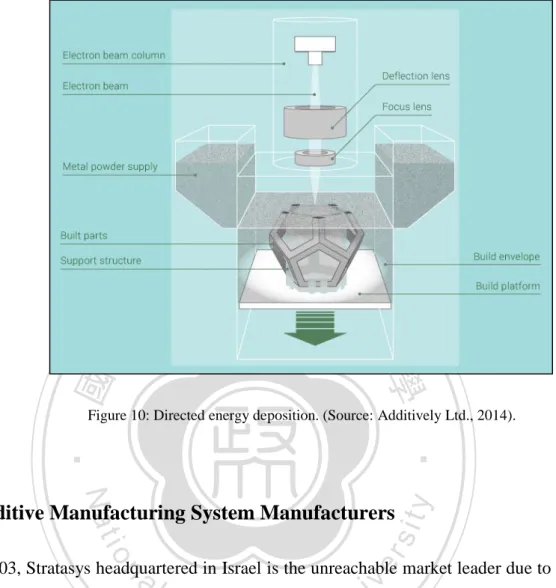

(23) . Powder bed fusion: is an additive manufacturing process in which thermal energy selectively fuses regions of a powder bed. Most common synonym, which is also used in this work, is laser-sintering.. 立. 政 治 大. ‧. ‧ 國. 學 y. sit. al. er. Directed energy deposition: is an additive manufacturing process in which focused. io. . Nat. Figure 9: Power bed fusion. (Source: Additively Ltd., 2014).. n. thermal energy is used to fuse materials by melting as the material is being deposited.. Ch. engchi. 10. i n U. v.

(24) 立. 政 治 大. ‧ 國. 學. Figure 10: Directed energy deposition. (Source: Additively Ltd., 2014).. al. er. io. sit. y. ‧. Nat. 1.5 Additive Manufacturing System Manufacturers. n. Since 2003, Stratasys headquartered in Israel is the unreachable market leader due to a merge. Ch. i n U. v. with Objet. Stratasys only offers material extrusion and material jetting systems.. engchi. 3D systems, who claims to be the inventor of 3D printing and headquartered in the US offers a vast rage of technologies: vat photopolymerization, material jetting, binder jetting, and power bed fusion. EOS and Envisiontec are two German players, who distinguished themselves through specializing in their fields and offering high quality and services. EOS offers power bed fusion systems for both metals and polymers and Envisiontec does vat photopolymerization. The following table demonstrates the distribution of market shares among the leading manufacturer.. 11.

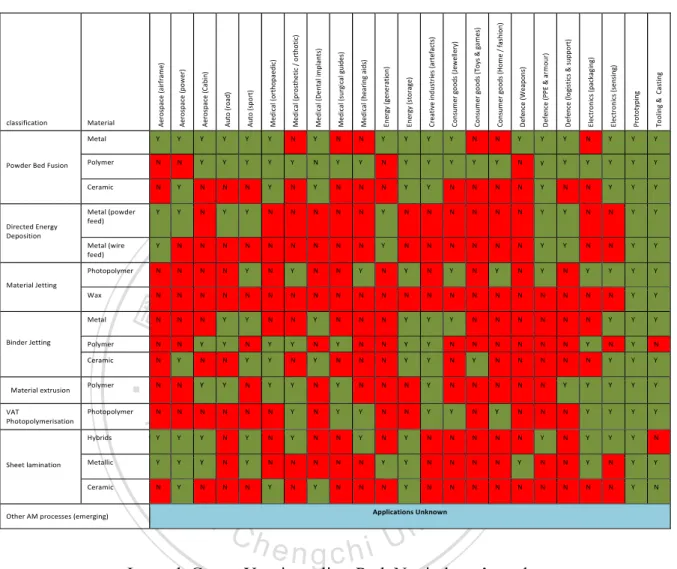

(25) EOS Envisiontec 11.2% 2.0%. Mcor 3.1% Others 9.0%. 3D Systems 18.0%. Beijing Tiertime 2.1%. Stratasys 54.7%. 立. 政 治 大. Figure 11: Leading AM system manufacturer in 2013. (Source: Wohlers Associates Inc., 2014).. ‧ 國. 學. 1.6 Current Status of Additive Manufacturing. ‧. The additive manufacturing industry is divided into professional users and so called prosumers, which mostly are interested in the new cheap material extrusion printers that invaded the. y. Nat. sit. markets recently. The end consumer 3D printing market is not a topic of this work and therefore. al. n. applications of 3D printing and additive manufacturing.. Ch. engchi. er. io. left out. All information and forecasts in this business plan are only based on industrial. i n U. v. Applications in the professional additive manufacturing environment are vast and will be described further in the next chapters. As a foretaste the following table shows how the different technologies can be applied to current or near to market applications for relevant sectors:. 12.

(26) Table 2: Current commercial or near to market applications of AM relative to sectors. (Source: AM SIG, 2012).. 立. 政 治 大. ‧. ‧ 國. 學. n. er. io. sit. y. Nat. al. Ch. engchi. i n U. v. Legend: Green: Yes, it applies; Red: No, it doesn’t apply. As indicated in table 2, different technologies can be applied in different industries. Additive manufacturing only makes sense in areas where it is more cost effective, increases customer satisfaction, or results in improved product functionality compared to conventional manufacturing processes. (cf. Wohlers Associates Inc., 2014). To summarize, additive manufacturing is not going to take over traditional manufacturing. Both technologies have their justifications and the ideal production strategy should involve a mix of both in order to be able to compete successfully.. 13.

(27) 2. Market Analysis 2.1 Overview The technology of additive manufacturing is improving on a weekly basis, the variety of processable materials is rising, and therefore the quality of the products is starting to be comparable with traditional mass manufacturing. Consequently, the amount of applications increases in different industries where it can be applied. A survey processed by Wohlers Associates, 2014 shows the industries applying additive manufacturing as of 2013:. 立. 政 治 大. ‧. ‧ 國. 學. n. er. io. sit. y. Nat. al. Ch. engchi. i n U. v. Figure 12: Industries applying additive manufacturing. (Source: cf. Wohlers Associates Inc., 2014.). The range of usage of these additive manufactured parts is broad. Not all industries use the objects produced with the new technology in production right away. The following chart gives an overview on how companies actually employ parts built on additive manufacturing systems.. 14.

(28) 立. 政 治 大. ‧ 國. 學. Figure 13: How AM parts are being used? (Source: cf. Wohlers Associates Inc., 2014).. ‧. It is clearly visible, that companies use additive manufacturing for functional parts in the first. sit. y. Nat. place and prototypes for fit and assembly in the second place. The third largest category comprises of molds or inserts for production. Therefore it would make sense to position a new. io. n. al. er. company in one or all of those fields. Mr. Tu, president of an additive manufacturing service. i n U. v. provider in Taiwan, estimated that 70% of printed parts are for prototyping and 30% for small. Ch. engchi. series production in his company. (cf. Tu, 2014). However, this trend is about to change and according to Wohler Associates, 2014, the demand for production parts are expected to drive annual revenues to much higher levels in the years to come.. 2.2 Additive Manufacturing Industry Structure The needs of the above mentioned industries for parts produced through additive manufacturing are solved in two ways. The first possibility is, that companies purchase the systems from a range of 3D printer system suppliers themselves and develop the necessary knowledge within the company. This requires a lot of bound capital and the companies normally need to have a certain size in order to economically justify the investment. Large companies, especially in the. 15.

(29) aerospace industry like Boeing, Airbus, Rolls Royce and GE Aviation are heavily investing in R&D for this new technology. The second, being more appropriate for the small and medium sized companies due to their size, is to outsource the process and use service manufacturers who are specialized in this field. This is exactly where a new company should position itself as long as the market is in its premature phase and continues to grow at a fast pace.. 2.3 Additive Manufacturing in Figures. 政 治 大 34.9% (CAGR) to US$ 3.07 billion in 2013. This is a continuation of the impressive growth 立 rates of 2010, 2011, and 2012, having been 24.1%, 29.4%, and 32.7%, respectively. (Wohlers. The primary additive manufacturing market, consisting of all products and services, grew by. ‧ 國. 學. Associates Inc., 2014).. ‧. Out of these, additive manufacturing service providers generated around US$967 million from the sale of parts in 2013 worldwide. Compared to 2012, this signifies a jump of 21.1% from. n. al. er. io. sit. y. Nat. US$ 798.4 million.. Ch. engchi. 16. i n U. v.

(30) 立. 政 治 大. ‧ 國. 學. Figure 14: Service provider revenue estimates (in millions of US$). ‧. (Source: cf. Wohlers Associates Inc., 2014).. io. sit. y. Nat. n. al. er. Regarding the future potential of additive manufacturing, the market consensus agrees that this. i n U. v. technology could easily tap 2% of the total manufacturing economy, which accounts for US$. Ch. engchi. 210 billion out of US$ 10.5 trillion. When forecasting the nearer future, Wohlers Associates as well as big consulting firms like McKinsey, acknowledge that this industry could easily exceed US$ 21 billion by 2020. (cf. McKinsey Global Institute, 2013; Wohlers Associates Inc., 2014).. 2.3.1 Laser-Sintered Polymers Market The shipments of laser-sintered polymers in 2013 showed a steep increase of 30% compared to 2012. The revenues grew by 28% from US$ 105 million to US $135 million from 2012 to 2013, respectively. (cf. Wohlers Associates Inc., 2014). 17.

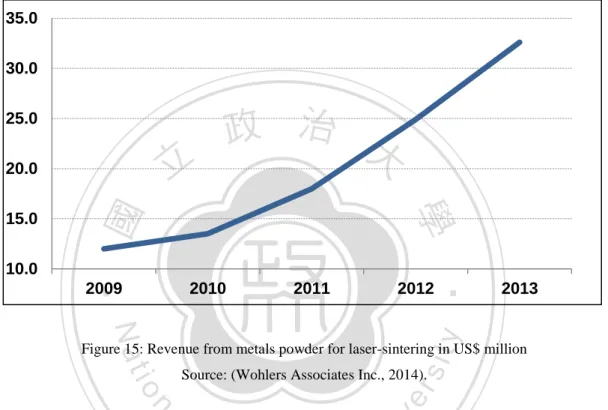

(31) 2.3.2 Laser-Sintered Metals Market As for the laser-sintered metals, revenue climbed by 31% to US$ 32.6 million in 2013 compared to US$ 24.9 million in 2012. The upward trend from 2009 onwards is demonstrated in the following graph: 35.0 30.0 25.0. 立. 20.0. ‧ 國. 2009. 2010. ‧. 10.0. 學. 15.0. 政 治 大. 2012. 2013. Nat. y. 2011. Source: (Wohlers Associates Inc., 2014).. n. al. er. io. sit. Figure 15: Revenue from metals powder for laser-sintering in US$ million. i n U. v. According to Roland Berger as well as Wohlers Associates, additive manufacturing of metals. Ch. engchi. has only started to show its capabilities in the past years. The growth in this field will outperform by far the polymers market. Only by looking at the market potential, the metals market would definitely be a good choice to position a new player in the 3D printer service provider industry. (cf. Wohlers Associates Inc., 2014; Roland Berger, 2013).. 2.4 The Austrian Manufacturing Landscape Looking at Austria’s GDP decomposition, it is observed that with 28.6% being generated through this industry, this small European country has one of the largest secondary sectors in the EU. The service sector is responsible for the majority with 69.8% and the agricultural sector makes up for 1.6% of the total GDP in 2013. (cf. Central Intelligence Agency, 2014).. 18.

(32) The industrial sector is primarily made up of small and medium-sized enterprises, which makes up nearly 98.29% of the companies. In terms of gross value added, nearly 40% is provided by these small and medium sized enterprises as of 2014 in Austria. (cf. European Commission, 2014).4 The most important industries as of 2013 are comprised of construction, machinery, vehicles and parts, food, metals, chemicals, lumber and wood processing, paper and paperboard, communications equipment, and tourism. Austria largest export partners are Germany (29.31%), Italy (6.25%), Switzerland (5.08%), United States (5%), and France (4.27%) as of 2013. (cf. Central Intelligence Agency, 2014).. 政 治 大. These statistics show that Austria is a good place to introduce such a new manufacturing technology, since it is indeed a true manufacturing hub with high concentration on metals,. 立. partly due to the number of automotive supplier.. ‧ 國. 學. 2.4.1 Potential Clients. ‧. Considering that the new business idea proposes a cutting-edge technology in manufacturing, the B2B business model would target manufacturing companies in the first place. Furthermore,. y. Nat. sit. in terms of size the focus lies primarily in small and medium sized enterprises, since large. er. io. corporations are able to invest by themselves in 3D printers. However, this doesn’t exclude. al. larger firms by definition, since even companies that own printers themselves, may lack know-. n. v i n how or simply could have capacity times, which they need to overcome. C bottlenecks h e n g cinhpeak i U. Another really interested potential client would be the medical industry. Due to new biocompatible materials and the possibility to print customized parts, like implants, casts, and any dental appliances, additive manufacturing is the technology of choice to not only ease surgical doctors’ and dentists’ lives, but mostly patients who profit the most out of it. Only a very small part will involve sales to final consumers, and this is even truer at the beginning. Such end-consumers could be designers, eager to produce art and functional parts that are impossible to manufacture otherwise. In addition, entrepreneurs of all kinds, wanting. 4. The query included NACE B-F (Categorization system of the economy in the EU).. 19.

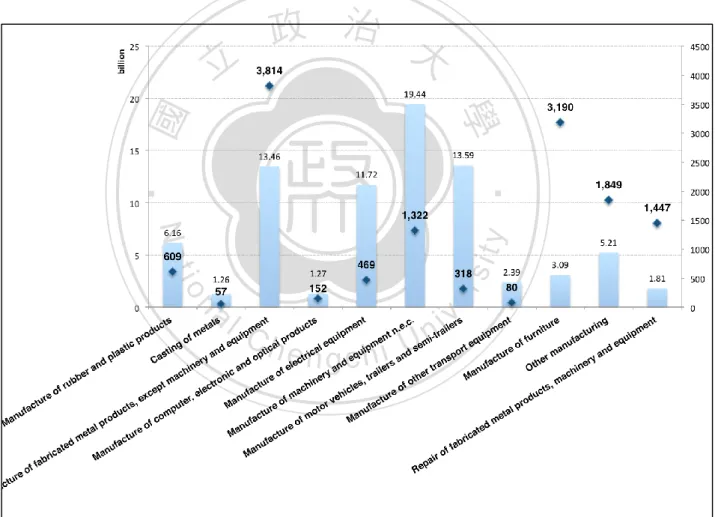

(33) to see and test products that they developed, would also be very likely to use the service. This group was one of the first to take advantage of the additive manufacturing technology, since rapid prototyping can be done easily and very cost effectively. Profound research using the categorization system of the European Union – NACE – could detect a total of 13,307 enterprises in Austria as potential clients. The figure below offers a closer look of which fields they operate and also puts their total turnover into perspective. A sector with less companies and comparable high turnover indicates a high concentration and therefore most probably has higher entry barriers than others.. 立. 政 治 大. ‧. ‧ 國. 學. n. er. io. sit. y. Nat. al. Ch. engchi. i n U. v. Figure 16: Number and total sales of potential Austrian companies in 2011. (Source: cf. Statistik Austria, 2014).. On the other hand, sectors with numerous companies and comparably lower sales indicate many players and lower barriers. The categories called manufacturing of fabricated metal together. 20.

(34) with manufacturing of furniture and other manufacturing are the most promising for new market entry on a first glance. Other manufacturing consists of manufacture of jewelry, bijouterie, musical instruments, sports goods, games, toys, and medical, and dental instruments and supplies manufacturing, whereas the latter group makes up for the highest amount of companies and sales. 5 The following table summarizes the different industry categories, in which it would be ideally to position a new entrant: Table 3: Potential target industry categories. (Source: own compilation).. 政 治 大 Manufacture of fabricated metal products, except machinery and equipment 立 Manufacture of machinery and equipment. ‧ 國. 學. Manufacture of motor vehicles, trailers and semi-trailers Manufacture of furniture. ‧. Manufacture of jewelry, bijouterie and related articles. Manufacture of medical and dental instruments and supplies. y. Nat. er. io. Casting of metals. sit. Manufacture of rubber and plastic products. n. of consumer electronics aManufacture iv l C n hengchi U. These categories make up 35.4% of the total production industry in Austria. Similar numbers can be obtained from Germany and Switzerland. (cf. Statistik Austria, 2014; European Commission, 2014).. 2.4.2 Market Study A small market study, interviewing 10 Austrian companies in the consumer goods industry on the topic of additive manufacturing within their companies, shows insights of the current stage. 5. Manufacture of medical and dental instruments and supplies: no. of enterprises: 893 and total sales: EUR 860 million.. 21.

(35) of development regarding attitude and usability of this cutting-edge technology. These sample companies operate in the following segments (cf. Jukic, 2014): . Furniture. . Home entertainment. . Toys. . Plastics technology. . Lightning. 立. . Prefabricated house. . White goods. . Technical services. . Garden appliances. 政 治 大. ‧ 國. 學. Small excerpts of the interview are summarized in the following chart. The next chart aggregates the results of how probable, 3D printers may be used in the production process. ‧. within the surveyed companies.. n. er. io. sit. y. Nat. al. Ch. engchi. i n U. v. Figure 17: Probability of additive manufacturing application in production. (Source: cf. Jukic, 2014).. This pie chart shows that for production, only 40% of the interviewed SMEs are thinking of, or are already applying 3D printing. The reasons for the 40% definite denial regarding usage were not inquired. The causes could be either because of lacking knowledge, or the general 22.

(36) inappropriateness in the specific industry field. However, when the companies of the samplesize where asked if apart from production they could think of using additive manufactured parts in their company, the results look very different:. 立. 政 治 大. ‧ 國. 學. Figure 18: General application of 3D printer in companies other than production.. ‧. (Source: cf. Jukic, 2014).. Nat. sit. y. Apparently the vast majority within the sample size is using 3D printed parts for other purposes. io. er. but production. The range of these applications is comparable to the ones Wohlers Associates, 2014 figured out in figure 13.. n. al. Ch. engchi. 23. i n U. v.

(37) 政 治 大. 立. Figure 19: Current applications of 3D printed parts in sample-size.. ‧ 國. 學. (Source: cf. Jukic, 2014).. Considering the exact additive manufacturing technology used in the companies of the sample. ‧. size, laser-sintering was named in the first place and fused filament fabrication6 in second.. Nat. sit. y. This small market survey shows that a basic knowledge on 3D printing exists within a few. io. the forecasts presented by Wohler Associates, 2014.. n. al. C. er. companies, but the full potential is far from being exploited. This observation goes in hand with. i n U. v. h e n gSize 2.5 Additive Manufacturing Market c hini German Speaking Countries In this section, the additive manufacturing market size of the targeted German speaking countries for service providers will be estimated since no exact figures exist for this market. The hereby-used methodology will be described in the following: (a) According to Wohlers Associates, 2014 and as already demonstrated in figure 14, the worldwide additive manufacturing market for service provider in 2013 was worth US$ 976 million, which is about EUR 744 million.7 Since Europe. 6 7. Fused filament fabrication belongs to the material extrusion technologies. An exchange rate for EUR/USD of 1.3 is applied throughout this work.. 24.

(38) accounts for one third of the cumulative sold systems, it is assumed that also on third of the service providers’ revenues are generated in Europe. This amounts to EUR 245,469,230. (b) The total manufacturing output of all European countries that have a track record in offering additive manufacturing services totaled US$ 1.98 trillion in 2013. The calculation is in appendix B. (cf. United Nations, 2013). (c) The German speaking countries, Austria, Germany and Switzerland are responsible for about 43.61% of the above figure (b). (United Nations, 2013). (d) Therefore, the total market share of additive manufacturing in German speaking. 治 政 their manufacturing output (c) and of大 the total market value of additive 立 manufacturing in Europe (a). Hence, the total market value of additive. countries is a function of the percentage of German speaking countries’ share of. ‧ 國. 學. manufacturing services in German speaking countries sums up to EUR 107 million in 2013.. ‧. (e) However, since the defined target market in Table 3 only accounts for 35.4% of the total producing industry, only this percentage of (e) has to be taken into. y. Nat. sit. consideration for a company eager to penetrate this market. This market size. al. er. io. would be EUR 37.9 million in 2013.. n. The service provider industry has on average seen a steady growth over the past 10 years,. Ch. i n U. v. peaking in 2011 with more than 26%, and leveling off in the past two years at about 21%.. engchi. Considering the strong forecasts made by Wohlers Associate, 2014, which are based on surveys undertaken by industry participants, the anticipated growth rate in the next years to come will be hitting at least 30%. Regarding this promising outlook, the following table takes a more conservative approach and shows the market size of the German speaking countries in the targeted industries over the next years with an assumed growth rate of 20%: Table 4: AM market size in Austria, Germany and Switzerland in EUR. (Source: own compilation). 2013 37,894,712. 2014 46,345,233. 2015 56,662,609. 2016 69,298,371. 25. 2017 84,751,580. 2018 103,651,182. 2019 126,765,396.

(39) 3. Competitor Analysis 3.1 Additive Manufacturing Service Provider In recent years several additive manufacturing service provider entered the market, most of them in the US and Europe. All service manufacturers have in common to be able to do socalled “rapid-manufacturing”. However, this alone does not necessarily imply, that only 3D printing technology is applied. All below listed service manufacturer are classified as direct competitors and use additive manufacturing at least in part for their services. Most providers. 治 政 polymer processing. Considering those who have the大 capabilities to process metals, they 立metal additive manufacturing systems. Roland Berger estimated normally only have two to four are small and independent with few exceptions. Basically all service manufacturers offer. ‧ 國. 學. in 2013 around 90 companies, offering metal AM manufacturing services worldwide. However, only 10% of those also have advanced capabilities for designing difficult applications. The. io. sit. y. Nat. n. al. er. Berger.. ‧. following figure shows an overview of metal service provider worldwide, compiled by Roland. Ch. engchi. 26. i n U. v.

(40) 學 Figure 20: Selected AM metals service manufacturer.. ‧. ‧ 國. 立. 政 治 大. (Source: Roland Berger, 2013).. y. Nat. io. sit. Since the target market consists of Austria, Germany and Switzerland, a closer analysis on the. n. al. er. competition is following. A complete list of all direct competitors is attached in appendix C.. 3.2 Austria. Ch. engchi. i n U. v. When taking a closer look at the Austrian market six companies are offering services using additive manufacturing technologies. However, most of those companies only offer it as a supplementary service and more importantly none of them has any capabilities in providing metal additive manufacturing. Furthermore only 10% of the existing service providers are able to deliver advanced capabilities for designing complex applications. (cf. Roland Berger, 2013). . 1zu1 Prototypen GmbH & Co KG: This is the largest amongst all Austrian competitors with 130 employees and sales volume of EUR 11.3 million in 2012, which represents an increase of 20% compared to 2011. The company is located at the Swiss border in the western border of Austria. 27.

(41) Basically, 1zu1 Prototypen employs traditional manufacturing like CNC turning, injection molding, machining and vacuum casting in addition to 3D printing. Regarding additive manufacturing they work with four different technologies for polymer processing: stereolithography, photopolymer jetting, selective laser sintering and fused deposition modeling. The company is also able to do molds out of wax. In addition, they have a range of post processing capabilities. (cf. 1zu1 Prototypen GmbH & Co KG; Oesterr. Firmenbuch, 2014; Additively Ltd., 2014) . Robotmech Stössl GmbH:. 政 治 大 western part of the country, towards the Swiss border. The company is specialized on 立. This company is the second strongest competitor in Austria and is also located at the. large size stereolithography but also acquired selective laser sintering systems for. ‧ 國. 學. polymers production. They also do vacuum casting and a little post processing. On their webpage they emphasize the 3D scanning possibility. However, Robotmech Stössel. ‧. doesn’t have any capabilities additive manufacturing for processing metals. (cf.. y. sit. n. al. er. Other competitors:. io. . Nat. Robotmech Stoessl GmbH, 2014; Oesterr. Firmenbuch, 2014; Additively Ltd., 2014). i n U. v. All other competitors in Austria are less successful and not solely focused on additive. Ch. engchi. manufacturing compared to the previously mentioned. Three of the companies are located in the middle of Austria, i.e. Styria and Salzburg. Only one company is based in Vienna. They all use stereolithography and selective laser sintering of polymers and three out of four also do fused deposition modeling. Each of these competitors are stronger in traditional manufacturing and employ all kinds of castings like vacuum, sand, precision and die as well as CNC milling. (cf. Hintsteiner Group GmbH, 2014; RTCAD Tiefenboeck GmbH, 2014; RPD - Rapid Product Development GmbH, 2014; bsmodelshop GmbH, 2014; Oesterr. Firmenbuch, 2014; Additively Ltd., 2014) Overall the major clients for Austria’s additive manufacturing service providers are in the following sectors: automobile industry, machinery, equipment construction technology, electro. 28.

(42) technology, medical and dental technology, white goods, and consumer goods. This is consistent with the findings described in chapter 2.. 3.3 Germany Obviously, the competitive landscape in Germany is much broader. This is not only due to the larger size of Germany’s economy, but also due to the fact that leading AM system manufacturers are located here. Germany’s 3D printer system manufacturers account for 10% of the global cumulative sales and make even up 69% of the sales when it comes to metal additive manufacturing systems. (cf. Wohlers Associates Inc., 2014; Roland Berger, 2013).. 政 治 大 Generally, direct competition in Germany could be put down to eleven companies. However, 立 the differences in size are large with six being bigger companies. Overall, only five have. ‧ 國. 學. capabilities in 3D printing of metal. FKM Sintertechnik GmbH:. ‧. . sit. y. Nat. This company is located in the middle of Germany and states on its webpage to have a sales volume of approximately 5000 orders per year. Their asset size is about EUR 9. io. er. million, which makes it one of the major players in the industry. Furthermore, FKM. al. n. v i n C h laser-sintering 1994. They concentrate on selective e n g c h i U technology only and have orders for. Sintertechnik produces both, polymer and metals through additive manufacturing since. prototyping as well as small series production. According to the webpage they operate. 24 SLS printers, and also offer a range of light post-production services like polishing, coloring, and coating. (cf. FKM Sintertechnik, 2014; Additively Ltd., 2014). . Citim GmbH: Citim is headquartered in the north of Germany with a branch office in the US. Total staff accounts for more than 50 employees and they basically offer laser-sintering for plastic and polymer on eight printers as well as photopolymer jetting when it comes to additive manufacturing. They have a strong emphasis on metals and produce on EOS and SLM printers. Their US branch in Georgia is exclusively offering metal processing.. 29.

(43) On the traditional side, they apply all kinds of castings and molding technologies and CNC machining. (cf. CITIM GmbH, 2014; Additively Ltd., 2014). . PTZ-Prototypenzentrum GmbH: This company, with 17 employees is located in the eastern part of Germany and is also offering a broad range of services. In terms of additive manufacturing, they offer the usual suspects: stereolithography and selective laser-sintering, the latter for both polymers and metals. On the other hand they are also engaged in traditional manufacturing and can do all sorts of casting and CNC machining. The company has. 政 治 大 of EUR 2.3 million. In addition to the German production site, the company also 立. been in business since 1996 and according to the German company register an asset size. operates a branch office in Italy. (cf. PTZ-Prototypenzentrum GmbH, 2014; Additively. . FIT Production GmbH and FIT Prototyping GmbH:. ‧. ‧ 國. 學. Ltd., 2014; Company Register, 2014).. sit. y. Nat. Located in Southern Germany, FIT is one of the largest providers of metal laser-sintered parts, owning two EOS and two SLM printers. One specialty is that they also offer. io. n. al. er. electron beam melting, which is unique amongst all described companies. Needless to. i n U. v. say, FIT also offers polymer processing and uses EOS laser-sintering printers. In addition. to. additive. Ch. i e n g c htechnologies,. manufacturing. FIT. provides. traditional. manufacturing with different ways of casting and CNC machining. Even though the total asset or staff size couldn’t be evaluated, this company undeniably is one of the major players in Germany. (cf. FIT Production GmbH, 2014; Additively Ltd., 2014). . Other competitors: Out of the remaining seven competitors, five offer “fused deposition modeling” or “binder jetting” 3D printing technologies, whose parts are less used in industrial or production processes, but more for presentation purposes as needed in marketing departments and for architectural models, as well as for end consumers. However, the majority still offers laser-sintering and some also do stereolithography. Only two. 30.

(44) companies within these other competitors provide processing of metals, Blue Production GmbH and Jell Werkzeugelemente GmbH. However, the capacity of both is estimated to be very small. In general, all companies are mostly located in the middle and the southern regions of the country. (cf. Additively Ltd., 2014; 3D-Schilling GmbH, 2014; 3D-Labs GmbH, 2014; Blue Production GmbH, 2014; 3D Fab, 2014; 4D Solution, 2014; Werkzeugelemente, 2014; bkl-lasertechnik, 2014). 3.4 Switzerland The Swiss additive manufacturing scene is not to be underestimated and is very comparable to. 政 治 大 laser-sintering, which is totally 立missing in Austria. Five companies could be identified as direct. the Austrian one in terms of size. The major difference is that there is more focus on metal. ‧ 國. 學. competitors, wherein three offer metal processing services and one does this exclusively. Most companies are located in the east of the country.. ‧. . Von Allmen AG:. Nat. sit. y. This company has been in business for 40 years and constantly adapted to the new. io. er. technologies. The company is located in the east of Switzerland and has a staff size of above 20 employees. Regarding additive manufacturing the company offers. n. al. Ch. i n U. v. stereolithography and polymer laser-sintering. Even though the company is one of the. engchi. largest, they don’t offer metal processing. On the traditional manufacturing side, the company does vacuum casting, injection molding, and has a few CNC machines. (cf. Von Allmen AG, 2014; Additively Ltd., 2014). . Ecoparts AG Ecoparts is one of the youngest players in the market and is also located in the east of Switzerland, concentrating on laser-sintering for both, metals and polymers. They also employ CNC turning for postproduction purposes. According to the webpage, the company works with two metal EOS printers. (cf. Ecoparts AG, 2014; Additively Ltd., 2014).. 31.

(45) . Other competitors: One out of the 3 remaining competitors is actually attached to the technical university of Zurich (ETH) and does R&D in cooperation with the industry. However, they have polymer and metal laser-sintering printers and act like a service provider. The two other companies are located in the north of Switzerland, whereas one is also offering metal processing with a printer from SLM. The other, as well as a few more not mentioned, are in the appendix and are rather small players offering either fused deposition modeling or binder jetting services, which are targeted at different customers. (cf.. 政 治 大. Additively Ltd., 2014; Max Horlacher AG Protoshape GmbH , 2014; IRPD, 2014; 3D iam AG, 2014).. 立. ‧ 國. 學. 3.5 International Competitors. In addition to the local smaller competitors described until now, a few international players. ‧. could position themselves successfully. The most prominent service provider is actually a division of the AM system world market leader Stratasys Inc., called Red Eye. However, even. y. Nat. sit. though the company has plans to increase its presence in Europe, other international additive. er. io. manufacturer service providers are predominant in Europe for the moment. Furthermore, the. al. v i n photopolymer jetting and cannotC be seen as direct competitors. h e n g c h i U (cf. RedEye, 2014). n. company only offers printing on Stratasys printers, which use fused deposition modeling and. . Materialise NV: Materialise NV is probably the biggest player in the industry in Europe with over 900 employees and sales of about EUR 50 million. Headquartered in Belgium, it has offices all around the world i.e. China, Malaysia, Japan, USA, Venezuela, Ukraine, and most European countries including Austria and Germany. They basically offer all technologies additive manufacturing has to offer, with the exception of metal processing. Thus, their focus is on all sorts of polymers. In addition to the vast amount of different printers, they also offer vacuum casting and reaction injection molding in a much smaller scale. Furthermore, they offer a self-developed software for AM and they focus. 32.

(46) on biomedical engineering solutions. Obviously for a company of this size, they also do research and development, and offering consulting services for their clients. (cf. Materialise NV, 2014; Additively Ltd., 2014; Nationalbank of Belgium, 2014). . Schneider International Holding GmbH: Below Schneider International Holding are two entities, one focusing on prototyping and the other one on small series production. Compared to the total size of the company, additive manufacturing only accounts for a small part of the sales volume. The major part is produced with conventional machining, which can be derived from the proportion. 政 治 大 International Holding employs a staff of 200 employees worldwide, whereas 60 operate 立 of AM printers to total operating machines published on their webpage. Schneider. in the western part of Germany. Other locations include UK, Hungary, India, and China.. ‧ 國. 學. When it comes to additive manufacturing, the company uses six stereolithography printers, mostly from 3D Systems and 3 selective laser-sinter printers form EOS, all. ‧. exclusively for polymer processing. Consequently, Schneider International Holding is. y. Nat. not producing metal parts with additive manufacturing in any of their branches. (cf.. sit. Schneider International Holding GmbH, 2014; Additively Ltd., 2014; Company. n. al. er. io. Register, 2014).. Ch. i n U. v. To sum up, the competitors’ analysis shows that less than one third of the companies are able. engchi. to process metals with no presence of this service in Austria. Regarding polymer processing, the stereolithigraphy technology is the preferred one, since it is also the oldest. Laser-sintering is the second most widely used and the newcomer is fused depostion modeling, however the latter is less used in production or prototyping but rather for presentation models. The same is true for photopolymer- and binder- jetting which are only used by a handful of professional service providers that normally are more focused on end consumers. Estimating that the biggest 16 companies in the German speaking countries have a total market share of 75% to 80% and the remaining part is divided by many smaller providers, a target of 5% market share for a new entrant with focus on metal processing within three years from now should be feasible.. 33.

(47) 3.6 Five Forces Analysis The Porter Five Forces analysis will not only show the potential threats from existing competition and new entrants into the market, but will also be informative regarding the power of suppliers and buyers as well as the possibilities for substitutes of the new technology.. 3.6.1 Suppliers As a service manufacturer two major things are needed to be supplied: the 3D printers themselves, and the materials to produce the parts.. 治 政 大 power for machines is quite low. Although the printers are not exactly cheap, the bargaining 立 are getting into the market and competition is already More and more system manufacturers ‧ 國. 學. quite intense. According to Roland Berger, 2013 and Wohlers Associates, 2014, prices are estimated to decrease, especially considering the constant capacity increase. This is regardless. ‧. of the exact technology and whether the printer processes polymers or metals.. sit. y. Nat. When it comes to material prices and availability, the picture is very similar. At the moment, many system developers try to force the customers to only use their materials through warranty. io. n. al. er. clauses for the machines. System manufacturers are trying to apply the shaver-blade model and. i n U. v. sell the materials above commodity exchange prices. Nevertheless, this is also going to change. Ch. engchi. with more special material suppliers coming into the market and offering polymer and metal powder as well as VAT photopolymer liquids and so on for different brands. Again Wohlers Associates 2014 and Roland Berger, 2013, forecast a very severe drop in price over the next 5 to 10 years. Summing up, the power of suppliers is medium and will drop further in the future.. 34.

(48) 3.6.2 Customers As described in previous sections, the purpose customers use the products or parts produced with additive manufacturing vary quite strongly. Therefore, it is hard to make a clear statement. Not only are customers coming from different industries, but they also apply the parts for different purposes. In either case, the situation is completely different, than for instance, in the traditional OEM 8 – contract manufacturer relationship, where the strong customer tells the producer how much margin they are allowed to earn on which product. Due to the novelty of the technology, the exact cost structure is difficult to be estimated from the outside. It simply. 政 治 大. depends on too many variables. Nonetheless, it is obvious that realizable margins also depend on the specific client. Margins in the medical, design, and jewelry industry will be higher than. 立. in the automotive supply chain. Manufacturing of parts for machinery and equipment would be. ‧ 國. 學. somewhere in the middle.. However, with competition getting stronger, as well as the awareness of the technology’s. ‧. potential and therefore higher demand in volume from customers, the bargaining power of. y. sit. n. al. er. io. 3.6.3 Substitutes. Nat. customers is medium and will probably become stronger in the long term.. Ch. i n U. v. Substitutes for additive manufacturing would be traditional subtractive manufacturing.. engchi. However, many restrictions apply as already described in the introduction. First of all, complex structures that cannot be manufactured in one piece in any other way than by 3D printing simply exist. The most famous example is the ball in the ball model. Of course, some of these complex structures could be manufactured in several parts and assembled later on, but this has obvious disadvantages, as it is much slower and requires more man-hours. Secondly, speed is generally unbeatable by subtractive manufacturing, whether it is for prototyping or producing small series, which goes in hand with costs.. 8. OEM = Original Equipment Manufacturer.. 35.

數據

+7

相關文件

The case where all the ρ s are equal to identity shows that this is not true in general (in this case the irreducible representations are lines, and we have an infinity of ways

Menou, M.著(2002)。《在國家資訊通訊技術政策中的資訊素養:遺漏的層 面,資訊文化》 (Information Literacy in National Information and Communications Technology (ICT)

Warrants are an instrument which gives investors the right – but not the obligation – to buy or sell the underlying assets at a pre- set price on or before a specified date.

The IEC endeavours to ensure that the information contained in this presentation is accurate as of the date of its presentation, but the information is provided on an

德霖技術學院 德霖技術學院 德霖技術學院..

張庭瑄 華夏技術學院 數位媒體設計系 廖怡安 華夏技術學院 化妝品應用系 胡智發 華夏技術學院 資訊工程系 李志明 華夏技術學院 電子工程系 李柏叡 德霖技術學院

In response to the variance in manufacturing execution systems and comprehensive customized business logic, this study develops an integrated, extensible, and sustainable

Customers now prefer fast and easy online business transactions as well as delivery services, therefore the businesses need to... look into the possibilities of offering