109 (16%)

The Department raises revenue through taxes, duties and fees in accordance with the relevant legislation. In 2000-01, the Earnings and Profits Tax assessed increased by $10.9 billion (16%), as compared with the previous year. On the other hand, the total of duties and fees collected during the year was much the same as the previous year.

Profits Tax

Profits Tax is levied on individuals, corporations, bodies of persons and partnerships, in respect of assessable profits arising in or derived from Hong Kong. In 2000-01, the Profits Tax rates for corporations and non-corporate persons remained unchanged at 16% and 15% respectively..

A ssessing Functions

3

ASSESSING FUNCTIONS

12

2000 01

16% 15%

13

3

ASSESSING FUNCTIONS

5

Figure 5 Profits Tax assessed

Unincorporated Businesses

Corporations 80

60

40

20

0

44.7

36.1 4.2

40.5

1997-98 1998-99 1999-2000 2000-01 ($b)

57.0 6.1 46.2

7.0

5.2

50.9 39.2

30.9

2000 01

447 5

86 (24%)

37.6% 6

3 4

Reflecting an improvement in the state of the economy, Profits Tax of $44.7 billion was assessed during the year, representing an increase of $8.6 billion (24%) over the figure for the previous

year (Figure 5). Of the total tax assessed, the property and banking sectors together contributed 37.6% (Figure 6).

Further statistics relating to the tax assessed in respect of different business sectors are shown in Schedules 3 and 4.

Salaries Tax

Salaries Tax is charged on all income arising

in or derived from Hong Kong from any office (e.g. a directorship), employment or pension. The total tax payable is restricted to an amount not exceeding 15% (i.e. the standard rate of Salaries Tax) of the total income of the individual concerned.

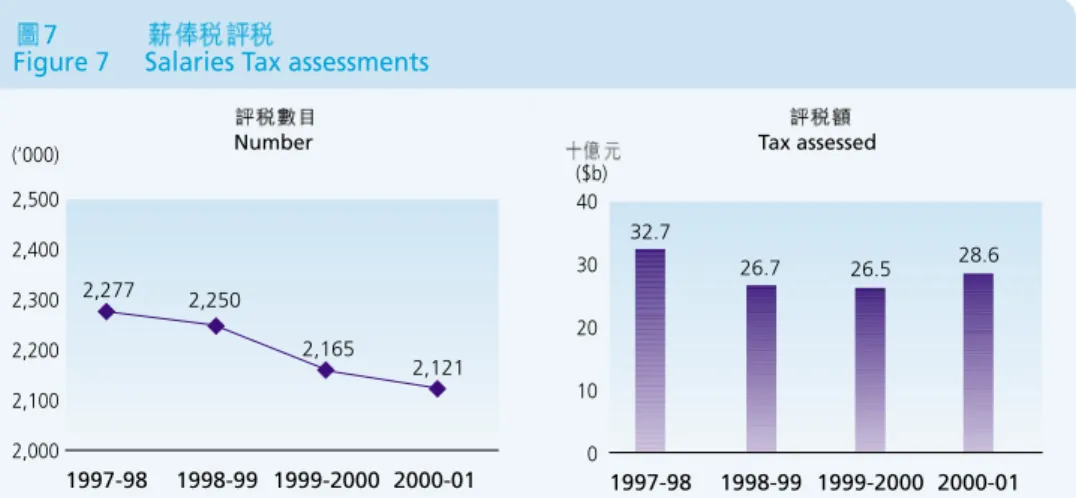

As compared with the previous year, the number of assessments made decreased slightly. However, as a result of an increase in the average level of income 7.9% more tax was assessed than in the previous year (Figure 7). Analyses of tax assessed and allowances granted in respect of taxpayers at various income levels are provided in Schedules 5 and 6.

15%

7.9% 7

5 6

6

Figure 6 Profits Tax assessed ratio by business sectors

Property (22.5%) Public Utilities (11.9%)

Others ( 17.6%) Manufacturing

( 11.6%)

Distribution (21.3%)

Banking (15.1%)

2000-01

7

Figure 7 Salaries Tax assessments

1997-98 1998-99 1999-2000 2000-01 2,500

2,400 2,300 2,200 2,100 2,000

2,121

(’000) Number Tax assessed

28.6 32.7

26.7 26.5

($b)

1997-98 1998-99 1999-2000 2000-01 40

30

20

10

0 2,277 2,250

2,165

10,316

11,602 12.5%

21.6%( 8)

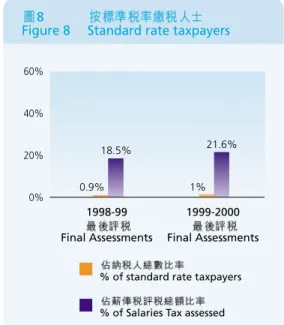

With the increase in the level of salaries, there was an increase of 12.5% in the number of standard rate taxpayers, from 10,316 last year to 11,602 this year. These taxpayers contributed 21.6% of the Salaries Tax assessed (Figure 8).

Notification Requirements of Employers

Apart from reporting commencements and cessations of employments, employers are required to prepare annual retur ns to report the emoluments of each of their employees. In 2000-01, 206,833 employers filed employer’s retur ns with the Department. During the year, the Department continued its past practice of conducting seminars to assist new employers in completing the returns.

In February 2001, letters were sent to 37,405 new employers inviting them to attend seminars which were held at the Concert Hall of the City Hall on 11 April 2001.

Property Tax

Property owners are subject to Property Tax which is charged at the standard rate of 15% in respect of the net assessable value of the property. Unincorporated businesses that pay Property Tax in respect of their business premises can have such payments set off against their Profits Tax liabilities.

Income arising from properties owned by corporations is subject to Profits Tax at the corporate rate in lieu of Property Tax. Statistics on the classification and ownership of properties, based on the records of the Department, are provided in Schedule 7. The number of assessments made during the year increased by 3%, as compared with the previous year. Reflecting reduction in rental income, the amount of Property Tax assessed dropped by 6.2%

(Figure 9).

% of standard rate taxpayers

% of Salaries Tax assessed

8

Figure 8 Standard rate taxpayers

1998-99 1999-2000

Final Assessments Final Assessments 60%

40%

20%

0% 1%

21.6%

0.9%

18.5%

3

ASSESSING FUNCTIONS

14

206,833

2001 2 37,405

4 11

15%

7

2 0 0 0 0 1 3%

6 . 2 % 9

550

500 450 400 350 300

474 (’000)

9

Figure 9 Property Tax assessments

494 488

471 Number

1.36 1.87

1.55 1.45

($b)

1997-98 1998-99 1999-2000 2000-01 3

2

1

0

Tax assessed

15

3

ASSESSING FUNCTIONS

1997-98 1998-99 1999-2000 2000-01

10

Figure 10 Assessments made under Personal Assessment

400

350

300

355 384

367

341

(’000) Number

3.53

4.31 4.00

3.27 ($b)

5 4 3 2 1

0

Tax assessed

1997-98 1998-99 1999-2000 2000-01

1997-98 1998-99 1999-2000 2000-01

4.1%

8% 10

Personal Assessment

An individual may elect for Personal Assessment in respect of his or her total income. Under Personal Assessment, all of the income of the taxpayer and his or her spouse is aggregated into a single sum and, after the deduction of all allowances, is assessed at the marginal tax rates.

In appropriate circumstances, this reduces the total tax liability of the individual (e.g. an individual who would otherwise be chargeable at the standard rate on each separate income source). As a result of an increase in the number of elections, the number of assessments made in 2000-01 was 4.1% more than the previous year.

The amount of tax assessed increased by 8% (Figure 10).

30,000 10,000

6

92 11

Advance Ruling

The advance ruling service allows a person to apply for a ruling on the way in which a provision of the Inland Revenue Ordinance applies in relation to a particular arrangement.

A fee is charged for the service on a “cost recovery” basis.

Initially, the applicant is required to pay an application fee of

$30,000, for a ruling concerning the “Territorial Source Principle”, or $10,000 for a ruling on any other matter.

The Department endeavours to provide a ruling within 6 weeks of the date of application, provided that all relevant information is furnished with the application and further consultation with the applicant is not required.

During the year, 92 advance ruling applications were processed (Figure 11). Most of the applications were for rulings on Profits Tax matters.

3

ASSESSING FUNCTIONS

16

11

Figure 11 Advance Ruling

1999-2000 2000-01

Number Number

5 17

Awaiting decision at the beginning of the year

69 81

Add: Applications received during the year

74 98

– Less: Disposed of –

Ruling made 44 79

Application withdrawn 7 6

Ruling declined 6 57 7 92

17 6

Awaiting decision at the end of the year

2000 01

6 9 12

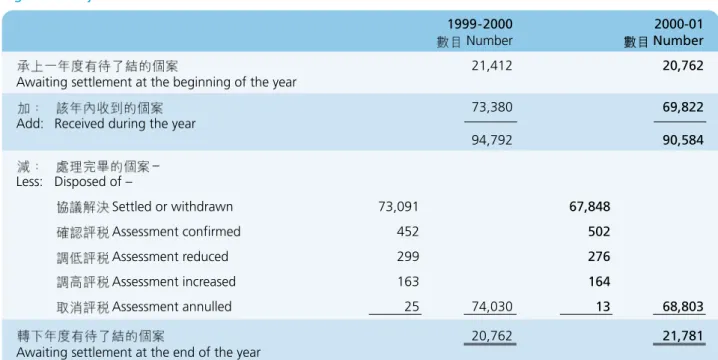

Objections

A taxpayer who is aggrieved by an assessment made under the Inland Revenue Ordinance may lodge an objection to the Commissioner. A significant proportion of the objections received each year arise from estimated assessments issued to taxpayers who have failed to lodge their tax returns in time. An objection of this nature must be supported by a completed return and, where applicable, by supporting accounts. Most of these objections are settled promptly by reference to the returns submitted.

Other objections are also generally settled by agreement between the taxpayers and assessors concerned. Relatively few objections are ultimately referred to the Commissioner for determination. During the year, the Department processed some 69,000 objections (Figure 12).

12

Figure 12 Objection statistics

1999-2000 2000-01

Number Number

21,412 20,762

Awaiting settlement at the beginning of the year

73,380 69,822

Add: Received during the year

94,792 90,584

– Less: Disposed of –

Settled or withdrawn 73,091 67,848

Assessment confirmed 452 502

Assessment reduced 299 276

Assessment increased 163 164

Assessment annulled 25 74,030 13 68,803

20,762 21,781

Awaiting settlement at the end of the year

17

3

ASSESSING FUNCTIONS

2001 3 31

1 9 127

2000

0 1 2 7 7

13

Appeals to the Board of Review

A taxpayer who is dissatisfied with the Commissioner’s determination of his objection may appeal to the Board of Review (Inland Revenue Ordinance) to have the determination reviewed. As at 31 March 2001, the Board consisted of a chairman and 9 deputy chairmen (who have legal training and experience) and 127 other members. During the year, the Board processed 277 appeals (Figure 13).

13

Figure 13 Appeals to the Board of Review

Number

2000 4 1 157

Awaiting hearing or decision as at 1 April 2000

265 Add: Lodged during the year

422 –

Less: Disposed of –

Withdrawn 89

Assessment confirmed 106

Assessment reduced in full 17

Assessment reduced in part 32

Assessment increased 27

Assessment annulled 4

Others 2 277

2001 3 31 145

Awaiting hearing or decision as at 31 March 2001

3

ASSESSING FUNCTIONS

18

2 0 0 0 0 1 3

14 2000 01

Appeals to the Courts

An appellant or the Commissioner may appeal to the Courts against a decision of the Board of Review. During the year, the Court of First Instance ruled on 3 appeal cases. The issues considered included the taxability of profits on the sale of certain properties; the Board’s jurisdiction to substitute its own valuation on a property, rather than use that of the Appellant or the Commissioner; and whether certain receipt was capital in nature.

The Court of Final Appeal decided in favour of the Commissioner in relation to 2 cases which were concerned with the deductibility of interest expenses which had been capitalised as part of the cost of trading stock.

Figure 14 sets out statistics concerning appeals to the Courts for 2000-01.

14

Figure 14 Appeals to the Courts

Court of Court of Total

First Final

Instance Appeal

2000 4 1 8 2 10

Awaiting hearing or decision as at 1 April 2000

15 – 15

Add: Lodged during the year

23 2 25

– Less: Disposed of –

Decided 3 2 5

Discontinued 8 11 – 2 8 13

2001 3 31 12 0 12

Awaiting hearing or decision as at 31 March 2001

19

3

ASSESSING FUNCTIONS

2,000 250

5,200 750

2001 3 31 7,098

5,631 2 , 0 8 6 8

1.5% ( 15)

Business Registration

The Department aims to maintain an efficient business registration system. Every person carrying on business in Hong Kong must register the business and pay the required fee. Registered businesses may renew their registration certificates either annually or once every 3 years. The registration fee and levy for the Protection of Wages on Insolvency Fund are respectively $2,000 and $250 if paid annually, or $5,200 and $750 if paid every three years. Up to 31 March 2001, 7,098 businesses had taken the 3-year certificates.

Reflecting improvement in the economy, the total of new and re-opened registrations in the year was 5,631 higher than that of the previous year. Moreover, the number of cancelled business registrations fell by 2,086 (Schedule 8).

The total number of active registrations recorded a growth of 1.5% for the year (Figure 15).

15

Figure 15 Active Business Registration

Unincorporated Businesses

Corporations 800

600

400

200

0

624,987 615,958

249,663 252,943

375,324 363,015

31.3.2000 31.3.2001 (’000)

3

ASSESSING FUNCTIONS

20

2,450 16

10,000 30,000

9,039 17%

2000

01 5 4

17

There was a corresponding increase in the number of certificates issued, resulting in an increase of $24.5 million in the amount of business registration fees collected (Figure 16).

A small business with sales or receipts below a specified limit ($10,000 for a business mainly deriving profits from the sale of services or $30,000 for other businesses) may apply for exemption from payment of the fee and levy.

The number of exemptions granted during the year was 9,039. This represents an increase of 17% over the previous year.

Where an application for exemption is not allowed, the business operator may appeal to the Administrative Appeals Board. During the year, 5 appeals were received by the Board, 4 of which were subsequently withdrawn by the appellants concerned (Figure 17).

16

Figure 16 Certificates issued and Fees collected

1999-2000 2000-01

Increase

( ) 687,150 703,075 2.3%

Number of certificates issued (Main and Branch)

( ) 1,276.2 1,300.7 1.9%

Fees (inclusive of penalties) ($m)

17

Figure 17 Appeals to the Administrative Appeal Board

Number

2000 4 1 0

Awaiting hearing as at 1 April 2000

5 Add : Lodged during the year

5 4 Less: Appeal withdrawn

2001 3 31 1

Awaiting hearing as at 31 March 2001

21

3

ASSESSING FUNCTIONS

18

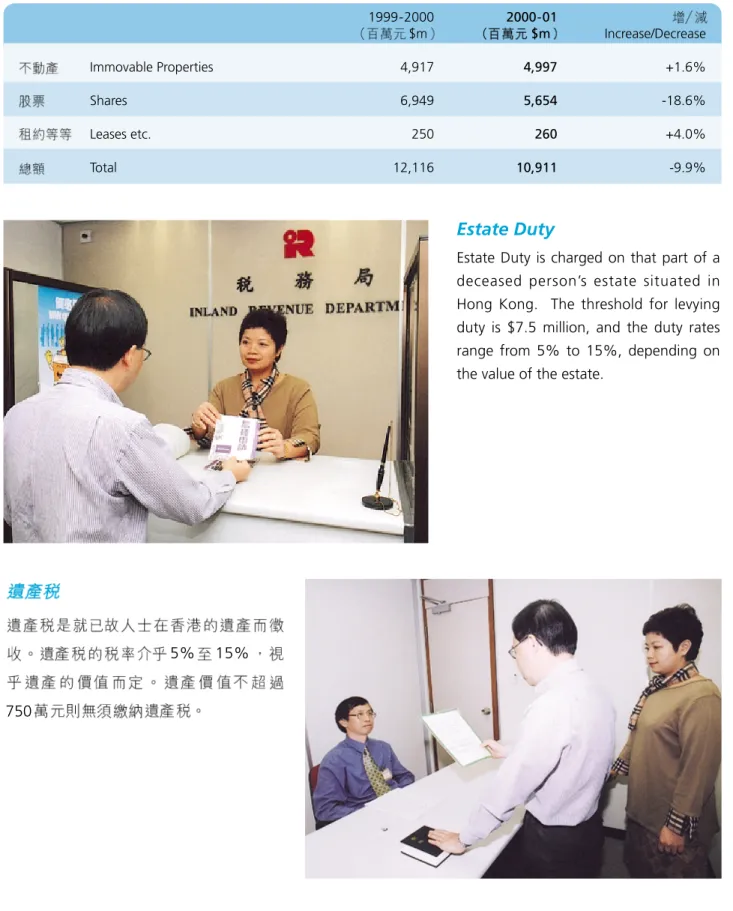

Stamp Duty

CollectionsStamp Duty is charged on instruments effecting property and stock transactions and leasing of property (Figure 18).

18

Figure 18 Composition of Stamp Duty collections

Immovable Properties (45.8%) Leases etc.

(2.4%)

Shares (51.8%)

2000-01

3

ASSESSING FUNCTIONS

22 2000 01

1.6%

10%

18.6%

10% 19 9

4.7% 10

During the year, the property market was relatively stable and the duty collected from property transactions increased slightly by 1.6%. The stock market was less active than the preceding year. This, coupled with a 10% reduction in the stamp duty rate on stock transactions, resulted in a reduction of 18.6% in duty collected from stock transactions. Overall, stamp duty collected during the year decreased by 10%, as compared with the previous year (Figure 19 and Schedule 9). However, there was an increase of 4.7% in the number of documents stamped (Schedule 10).

5% 15%

750

Estate Duty

Estate Duty is charged on that part of a deceased person’s estate situated in Hong Kong. The threshold for levying duty is $7.5 million, and the duty rates range from 5% to 15%, depending on the value of the estate.

19

Figure 19 Stamp Duty collections

1999-2000 2000-01

$m $m Increase/Decrease

Immovable Properties 4,917 4,997 +1.6%

Shares 6,949 5,654 -18.6%

Leases etc. 250 260 +4.0%

Total 12,116 10,911 -9.9%

23

3

ASSESSING FUNCTIONS

20

Figure 20 Composition of Estates

20 21

1 5

11 2.31 (18%)

6

12.58 12

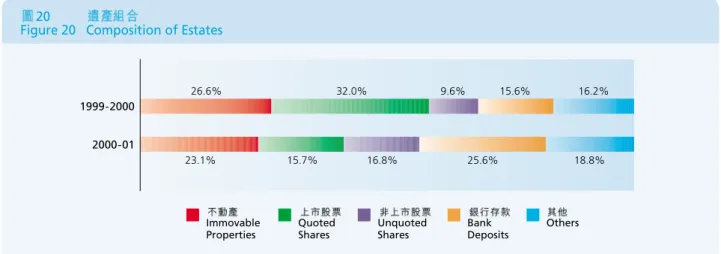

Figures 20 and 21 show the composition of estates and cases processed for the past two years.

Estate Duty of $1.5 billion was collected during the year (Schedule 11), an increase of $231 million (18%) over that of the previous year.

As Estate Duty is payable on delivery of an estate duty affidavit or account (or within 6 months from the date of the deceased’s death, whichever is the earlier), $1,258 million was received during the year in advance of the issue of formal assessments (Schedule 12).

21

Figure 21 Estate Duty cases

1999-2000 2000-01

New cases 14,157 13,880

Cases finalised

Dutiable 354 318

Exempt 13,889 13,246

14,243 13,564

3

ASSESSING FUNCTIONS

24

1999-2000

2000-01

Immovable Properties

Quoted Shares

Bank Deposits

Others Unquoted

Shares

26.6% 32.0% 9.6% 15.6% 16.2%

23.1% 15.7% 16.8% 25.6% 18.8%

1999

3

2 0 0 0 0 1 22

13

5.8% 23

In respect of an appeal case lodged by a dutypayer in 1999, the Court of Final Appeal handed down a decision in favour of the dutypayer. The case concerned the issue of whether certain property disposed of by the deceased within 3 years prior to his death was liable to Estate Duty.

Betting Duty

Betting Duty is charged on bets made on totalisators at race meetings conducted by the Hong Kong Jockey Club and on the proceeds of lotteries conducted by the Hong Kong Lotteries Board.

The rates of duty for 2000-01 are shown below (Figure 22).

Compared to last year, there were increases in respect of both the amounts placed on racing bets and lottery ticket sales (Schedule 13). As a result, the total betting duty collected in 2000-01 was 5.8% more than that of the previous year (Figure 23).

22 2000 01

Figure 22 Rates of Betting Duty in 2000-01

Rate 12%

Standard Bets win, place, double, quinella and quinella place

T T T 19%

Exotic Bets six up, treble, tierce, trio, double trio and triple trio

25%

Lotteries

25

3

ASSESSING FUNCTIONS

23

Figure 23 Betting Duty collections

1999-2000 2000-01

$m $m Increase

10,748.1 11,382.5 +5.9%

Horse Racing

1,189.7 1,247.6 +4.9%

Lotteries

11,937.8 12,630.1 +5.8%

Total

3%

2000 01

4.7% 24

4.4% 25

14

22% 26

Hotel Accommodation Tax

Hotel Accommodation Tax is imposed on hotel and guest house accommodation at the rate of 3% of the accommodation charges paid by guests. The tax is collected quarterly in arrears.

In 2000-01, there was a drop in the number of hotels and boarding houses operating in Hong Kong. However, due to a rise in room occupancy rate of 4.7% (Figure 24), the number of taxable rooms increased by 4.4% (Figure 25).

This factor, together with a slight increase in hotel room charges (Schedule 14), resulted in an increase of 22% in the tax collected, as compared with the previous year (Figure 26).

26

Figure 26 Hotel Accommodation Tax collections

700 600 500 400 300 200 100

222.5 511.3

219.0

182.4

1997-98 1998-99 1999-2000 2000-01 ($m)

24

Figure 24 Room occupancy rates

1999-2000 2000-01

Increase

9,779,071 11,141,928 +13.9%

Room Days

79.4% 84.1% +4.7%

Occupancy Rate

25

Figure 25 Hotels, boarding houses, taxable rooms and exempted rooms

1999-2000 2000-01 Increase/Decrease

168 156 -7.1%

Hotels and Boarding Houses

36,339 37,932 +4.4%

Taxable Rooms

5,475 5,483 +0.1%

Exempted Rooms

3

ASSESSING FUNCTIONS

26

36 2000 01

15 27

Tax Reserve Certificates

There are two sets of circumstances under which Tax Reserve Certificates are purchased.

The first applies to taxpayers who wish to save for the payment of their future tax liabilities. Two service schemes are offered to these taxpayers: the ‘Electronic Tax Reserve Certificates Scheme’ for all taxpayers and the ‘Save-As-You- Earn’ (SAYE) Scheme for civil servants and civil service pensioners. Under the Electronic Tax Reserve Certificates Scheme, certificates can be purchased using various electronic means, i.e. by bank autopay, telephone, the Internet, public information kiosk or bank ATM. Under the SAYE Scheme, certificates are purchased by civil servants and civil service pensioners through monthly deductions from their salaries / pensions. Interest is payable on the certificates when they are redeemed for settlement of tax liabilities, based on the interest rate prevailing at the time of purchase, for a maximum period of 36 months from the date of purchase.

In 2000-01, there was an increase in the number of certificates sold under both the Electronic Tax Reserve Certificates Scheme and the SAYE Scheme (Schedule 15).

However, reflecting the reduction in interest rate during the year, the amount of certificates sold dropped (Figure 27).

The second situation applies to taxpayers who object to tax assessments and are required to purchase Tax Reserve Certificates in respect of the tax in dispute. Such certificates are used to settle any tax found payable upon finalization of the objection or appeal. Interest is only payable on the amount, if any, subsequently required to be repaid to the taxpayer, and is computed at floating rates ruling over the tenure of the certificate.

27

3

ASSESSING FUNCTIONS

27

Figure 27 Certificates sold

1999-2000 2000-01 100

90 80 70 60 50 40 30 20 10 0

799 87,300

1,048 77,695 (’000)

Number

($m)

1999-2000 2000-01 3,000

2,000

1,000

0

Amount

1,218.2

352.4 1,901.1

471.7

Certificates relating to Objections and Appeals

Certificates other than for Objections and Appeals

SCHEDULES

66

3

SCHEDULE 3 CORPORATIONS

PROFITS TAX CONTRIBUTIONS FROM VARIOUS BUSINESS SECTORS

Business Sectors Final Tax Assessed for Year of Assessment

1997-98 1998 -99 1999-2000

/$’000 (%) /$’000 (%) /$’000 (%)

– Distribution : –

777,250 1.8 454,555 1.2 607,426 1.7

Retail

6,805,946 15.4 5,568,802 14.9 6,805,640 19.3 Wholesale, Import and Export

129,765 0.3 91,687 0.2 96,187 0.3

Foreign Corporations carrying on Import and Export

2,789,153 6.3 3,948,746 10.6 4,208,967 11.9 Public Utilities

14,024,954 31.7 12,125,076 32.6 7,935,717 22.5 Estate Development, Investment and Finance

(other than Banking)

8,913,920 20.2 5,754,688 15.5 5,336,349 15.1 Banking

– Manufacturing : –

672,065 1.5 634,331 1.7 904,825 2.6

Clothing and Textiles

246,034 0.6 188,666 0.5 218,725 0.6

Food and Beverage Products

205,288 0.5 222,701 0.6 264,295 0.7

Steel and Other Metals

440,731 1.0 320,752 0.9 327,767 0.9

Printing and Publishing

2,467,264 5.6 2,098,263 5.6 2,399,590 6.8

Others

496,570 1.1 432,966 1.2 505,218 1.4

Shipping (including Shipping Agents, Shipbuilding, Docking, Travel Agents, Air Forwarding Agents and Airline Booking Agents)

944,740 2.1 603,709 1.6 606,310 1.7

Hotels, Restaurants and Amusement Centres

782,613 1.8 876,696 2.4 974,714 2.8

Stevedoring, Wharfing and Godowns

457,346 1.0 475,455 1.3 399,443 1.1

Clubs and Associations

263,409 0.6 237,800 0.6 197,551 0.6

Insurance Companies and Insurance Agents

176,732 0.4 202,024 0.5 221,505 0.6

Non-resident Corporations Trading through Agents (including Consignment Tax)

1,166,994 2.6 1,072,469 2.9 1,139,245 3.2

Building Contractors and Engineering Works

59,558 0.1 49,833 0.1 58,902 0.2

Aircraft Owners and Operators

29,478 0.1 29,402 0.1 36,357 0.1

Taxis, Hire Cars, Public Light Buses and Motor Boats

2,350,971 5.3 1,857,298 5.0 2,085,687 5.9

Miscellaneous

44,200,781 100.0 37,245,919 100.0 35,330,420 100.0 Total

67

SCHEDULES

4

SCHEDULE 4 UNINCORPORATED BUSINESSES

PROFITS TAX CONTRIBUTIONS FROM VARIOUS BUSINESS SECTORS

Business Sectors Final Tax Assessed for Year of Assessment

1997-98 1998 -99 1999-2000

/$’000 (%) /$’000 (%) /$’000 (%)

160,725 5.9 22,346 1.0 33,893 1.7

Estate Developers, Property Dealers, Estate Agents and Subletting Businesses

256,345 9.5 130,099 6.1 149,426 7.4

Finance and Securities including Brokers, Dealers and Insurance Agents

67,388 2.5 64,186 3.0 49,069 2.4

Builders, Decorators and Civil Engineering Works –

Distribution : –

152,928 5.6 118,877 5.6 126,074 6.2

Import and Export

82,172 3.0 56,543 2.7 49,639 2.4

Wholesale

140,034 5.2 101,228 4.8 110,418 5.4

Retail – Manufacturing : –

4,265 0.2 3,029 0.1 3,180 0.2

Agricultural Trades and Food & Beverage Products Manufacturers

33,311 1.2 23,505 1.1 20,272 1.0

Cloth and Clothing

46,820 1.7 35,632 1.7 36,636 1.8

Chemical Products and Mechanical Engineering

22,107 0.8 14,203 0.7 14,353 0.7

Printing and Publishing

62,565 2.3 49,081 2.3 47,399 2.3

Others

68,121 2.5 60,070 2.8 36,453 1.8

Hotels, Restaurants and Amusement Centres

38,004 1.4 29,443 1.4 27,589 1.4

Transport (including Wharfing and Godowns) –

Professions : –

234,668 8.7 251,930 11.8 230,211 11.4

Accountants

28,032 1.0 27,314 1.3 18,614 0.9

Architects, Engineers, Surveyors etc.

615,077 22.7 584,736 27.5 535,701 26.4

Doctors and Dentists

609,015 22.4 476,129 22.4 459,673 22.7

Solicitors and Barristers

79,496 2.9 68,250 3.2 67,723 3.3

Other Professions

12,357 0.5 10,732 0.5 11,171 0.6

Miscellaneous

155 – 49 – 48 –

Non-resident Businesses (Note)

2,713,585 100.0 2,127,382 100.0 2,027,542 100.0 Total

20A(3)

Note : Consignment Tax under Section 20A(3) of the Ordinance

SCHEDULES

685 1999-2000

SCHEDULE 5 ANALYSIS OF SALARIES TAX ASSESSMENTS FOR THE YEAR OF ASSESSMENT 1999-2000 BY INCOME GROUP

Concessionary Deductions

6

Annual Income No. of Percentage No. of Total Income Total Self Total Home Elderly Total Final Percentage Average

Taxpayers of Elections (After Deductions Allowances Education Donations Loan Residential Net Tax of Tax per

Taxpayers for Joint other than (See analysis Expenses to Interest Care Chargeable Total Taxpayer

Assessment Self Education per Charities Expenses Income Final Tax

Expenses and Schedule 6) Concessionary

Deductions)

(%) (%)

($) ($’000) ($’000) ($’000) ($’000) ($’000) ($’000) ($’000) ($’000) ($)

108,001 – 110,000 9,721 0.83 0 1,060,594 1,049,868 49 67 1 0 10,609 209 0.00 21

110,001 – 120,000 56,513 4.84 0 6,515,815 6,103,515 8,369 3,816 824 4 399,287 7,966 0.03 140

120,001 – 130,000 57,545 4.93 0 7,200,684 6,214,890 23,269 13,922 7,095 104 941,404 18,808 0.07 326

130,001 – 140,000 50,494 4.33 0 6,814,302 5,475,777 34,196 15,900 20,284 319 1,267,826 25,338 0.09 501

140,001 – 150,000 49,862 4.27 0 7,222,200 5,517,591 46,775 16,917 42,089 388 1,598,440 36,301 0.14 728

150,001 – 180,000 127,278 10.91 0 20,988,616 14,686,186 153,893 60,832 346,546 2,504 5,738,655 206,892 0.77 1,625

180,001 – 210,000 108,351 9.28 0 21,021,565 13,568,719 159,218 79,376 523,257 4,830 6,686,165 336,822 1.25 3,108

210,001 – 240,000 96,101 8.23 4,958 21,605,470 13,642,037 154,396 88,672 635,026 5,641 7,079,698 456,154 1.70 4,746

240,001 – 270,000 94,486 8.09 9,624 23,979,520 15,223,055 166,372 104,577 735,722 7,918 7,741,876 578,695 2.16 6,124

270,001 – 300,000 82,381 7.06 12,437 23,433,459 14,972,362 158,808 103,925 700,438 8,091 7,489,835 623,737 2.32 7,571

300,001 – 400,000 176,836 15.15 29,861 60,890,506 34,867,731 362,436 303,383 2,502,160 32,945 22,821,851 2,284,948 8.51 12,921 400,001 – 500,000 86,663 7.42 12,676 38,550,822 17,815,579 203,040 216,821 1,988,148 23,809 18,303,425 2,237,693 8.34 25,820 500,001 – 600,000 48,516 4.16 5,354 26,458,881 9,937,419 108,414 148,627 1,286,938 15,830 14,961,653 2,035,941 7.58 41,964

600,001 – 700,000 29,048 2.49 2,592 18,771,601 5,855,546 63,933 102,782 783,154 9,395 11,956,791 1,726,212 6.43 59,426

700,001 – 800,000 20,304 1.74 1,480 15,095,459 4,044,297 38,434 82,335 531,447 6,597 10,392,349 1,552,342 5.78 76,455

800,001 – 900,000 14,239 1.22 989 12,064,309 2,815,178 25,584 59,477 417,628 4,262 8,742,180 1,335,989 4.98 93,826

900,001 – 1,000,000 11,398 0.98 749 10,771,821 2,227,790 20,042 51,917 349,160 2,822 8,120,090 1,260,145 4.69 110,558

1,000,001 – 1,500,000 28,667 2.46 1,985 34,398,038 5,539,956 38,800 159,898 856,992 7,752 27,794,640 4,414,210 16.45 153,982

1,500,001 – 2,000,000 9,153 0.78 641 15,655,346 1,325,937 9,365 75,997 241,817 2,295 13,999,935 2,194,073 8.17 239,710

2,000,001 – 3,000,000 5,875 0.50 169 14,036,427 599,541 3,548 58,081 106,514 1,052 13,267,691 2,055,926 7.66 349,944

3,000,001 – 5,000,000 2,434 0.21 6 9,099,078 15,408 549 37,941 26,233 195 9,018,752 1,354,675 5.05 556,563

5,000,001 – 7,500,000 797 0.07 1 4,742,258 936 199 16,097 4,438 0 4,720,588 708,086 2.64 888,439

7,500,001 – 10,000,000 268 0.02 1 2,263,916 567 99 6,054 1,569 60 2,255,567 338,323 1.26 1,262,397

10,000,001 & /over 361 0.03 0 7,070,667 0 7 39,613 1,393 0 7,029,654 1,054,448 3.93 2,920,908

/ Total 1,167,291 100.00 83,523 409,711,354 181,499,885 1,779,795 1,847,027 12,108,873 136,813 212,338,961 26,843,933 100.00 22,996

69

SCHEDULES

6 1999-2000

SCHEDULE 6 ANALYSIS OF ALLOWANCES FOR THE YEAR OF ASSESSMENT 1999-2000 BY INCOME GROUP

Annual Basic Married Child Dependent Single Dependent Additional Dependent Additional Disabled Disabled Disabled Disabled Disabled Total Income Allowance Person’s Allowance Brother/ Parent Parent Dependent Grandparent Dependent Spouse Parent Grandparent Child Brother/ Allowances

Allowance Sister Allowance Allowance Parent Allowance Grandparent Allowance Allowance Allowance Allowance Sister

Allowance Allowance Allowance Allowance

($) ($’000) ($’000) ($’000) ($’000) ($’000) ($’000) ($’000) ($’000) ($’000) ($’000) ($’000) ($’000) ($’000) ($’000) ($’000)

108,001 – 110,000 1,049,868 0 0 0 0 0 0 0 0 0 0 0 0 0 1,049,868

110,001 – 120,000 6,103,404 0 111 0 0 0 0 0 0 0 0 0 0 0 6,103,515

120,001 – 130,000 6,214,860 0 0 30 0 0 0 0 0 0 0 0 0 0 6,214,890

130,001 – 140,000 5,453,352 0 10,695 4,830 0 6,120 0 780 0 0 0 0 0 0 5,475,777

140,001 – 150,000 5,385,096 0 59,235 29,760 0 37,650 30 5,820 0 0 0 0 0 0 5,517,591

150,001 – 180,000 13,746,024 0 281,872 111,330 0 329,940 168,390 37,620 10,830 0 120 60 0 0 14,686,186

180,001 – 210,000 11,701,908 0 457,537 128,220 54 711,090 469,680 62,130 29,340 0 3,540 840 420 3,960 13,568,719

210,001 – 240,000 9,175,032 2,407,752 473,849 131,280 54 793,740 525,780 70,200 31,830 0 19,080 3,300 1,680 8,460 13,642,037

240,001 – 270,000 7,987,032 4,434,912 809,105 104,220 55,296 999,780 670,560 69,510 33,000 0 42,420 4,260 2,760 10,200 15,223,055

270,001 – 300,000 5,961,708 5,870,880 1,261,006 91,440 85,008 956,130 597,630 61,050 27,390 480 41,100 3,660 3,360 11,520 14,972,362

300,001 – 400,000 11,893,824 14,408,928 3,386,486 159,360 218,023 2,782,830 1,594,980 138,750 58,410 5,880 141,120 13,740 27,300 38,100 34,867,731 400,001 – 500,000 5,926,392 6,866,424 1,771,765 72,660 119,988 1,786,470 991,770 75,480 32,730 4,260 109,260 9,960 20,760 27,660 17,815,579 500,001 – 600,000 3,419,496 3,640,464 1,047,699 32,100 66,150 1,032,810 540,090 36,510 15,180 1,740 70,740 4,560 13,860 16,020 9,937,419

600,001 – 700,000 2,053,836 2,166,696 632,000 16,770 39,744 573,420 286,350 20,580 8,310 960 36,540 3,180 7,500 9,660 5,855,546

700,001 – 800,000 1,403,892 1,577,880 455,996 8,730 25,969 355,890 164,520 10,920 4,260 780 24,360 1,200 5,460 4,440 4,044,297

800,001 – 900,000 963,684 1,148,256 317,960 6,030 20,358 224,160 102,180 7,410 2,400 240 14,460 960 3,540 3,540 2,815,178

900,001 – 1,000,000 771,876 918,216 253,766 4,290 13,932 169,380 73,950 5,040 1,860 240 9,420 900 2,460 2,460 2,227,790

1,000,001 – 1,500,000 1,776,600 2,554,632 655,950 7,410 37,584 332,640 132,420 8,820 2,880 660 19,920 1,200 4,260 4,980 5,539,956

1,500,001 – 2,000,000 126,144 906,768 195,735 810 10,260 58,050 21,660 990 300 0 3,000 240 1,200 780 1,325,937

2,000,001 – 3,000,000 13,500 460,728 93,525 120 4,968 17,610 6,810 480 120 120 780 120 600 60 599,541

3,000,001 – 5,000,000 108 9,720 2,340 60 0 1,620 1,020 90 90 0 240 0 0 120 15,408

5,000,001 – 7,500,000 108 648 180 0 0 0 0 0 0 0 0 0 0 0 936

7,500,001 – 10,000,000 0 432 135 0 0 0 0 0 0 0 0 0 0 0 567

10,000,001 & /over 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

/ Total 101,127,744 47,373,336 12,166,947 909,450 697,388 11,169,330 6,347,820 612,180 258,930 15,360 536,100 48,180 95,160 141,960 181,499,885

SCHEDULES

70

7 2001 3 31

SCHEDULE 7 PROPERTY STATISTICS (as at 31 March 2001)

Classification of Properties No. of Properties %

627,984 32.99 Solely owned by individuals (with rental income, if any, reported in Composite tax returns)

–

Jointly owned, owned by tenants-in-common, or solely owned other than by individuals –

98,438 Letting

33,250 Business use and/or rent free

456,403 Wholly occupied by owners for residential use

21,824 Vacant

72 609,987 32.04

Letting but no liability under Personal Assessment

339,350 17.83 Owned by corporations and exempt from Property Tax under the Inland Revenue Ordinance

207,137 10.88 Home Ownership Scheme or Private Sector Participation Scheme

897 0.05

Government owned

– 118,309 6.21

New Ownership – awaiting classification

1,903,664 100.00 Total

Classification of Ownership No. of Properties %

1 1,108,693 58.24

Properties owned by : 1 owner

2 747,810 39.28

2 owners

3 33,256 1.75

3 owners

4 8,114 0.42

4 owners

5 2,667 0.14

5 owners

6 10 2,641 0.14

6 to 10 owners

11 20 329 0.02

11 to 20 owners

20 154 0.01

Over 20 owners

1,903,664 100.00 Total

71

SCHEDULES

8

SCHEDULE 8 BUSINESS REGISTRATION STATISTICS

1997-98 1998-99 1999-2000 2000-01

Fiscal Year

85,544 73,164 81,689 87,553

New registrations

13,436 3,749 7,337 7,104

Re-opened registrations

104,158 95,338 87,714 85,628

Cancelled registrations

3 31

633,071 614,646 615,958 624,987

Current registrations as at 31 March

725,187 685,841 687,150 703,075

Certificates issued

4,084 5,501 7,704 9,039

Businesses exempted from payment of fees

199,711 228,521 238,831 256,851

Certified extracts issued

($’000) ($’000) ($’000) ($’000)

1,341,070 1,275,703 1,276,238 1,300,714

Fees and penalties collected (excluding levy)

15,481 14,703 10,697 10,320

Court fines 3 31

60,127 56,215 45,309 41,192

Fees and penalties in arrears as at 31 March (excluding levy)

SCHEDULES

72

9

SCHEDULE 9 STAMP DUTY COLLECTIONS

1997-98 1998-99 1999-2000 2000-01

Fiscal Year

($m) ($m) ($m) ($m)

– Duties on –

• 17,278.3 6,335.8 4,917.4 4,996.9

Assignments and Chargeable Agreements

• 11,485.5 3,588.1 6,948.7 5,653.7

Contract notes

• 299.7 246.9 228.1 237.2

Leases

• 4.2 1.5 3.4 6.4

Transfer deeds

• 2.4 1.7 2.4 2.1

Other documents

25.7 13.9 15.1 14.2

Penalties

1.1 0.8 0.8 0.7

Additional duties for delays in payment

29,096.9 10,188.7 12,115.9 10,911.2

Total duty collections

73

SCHEDULES

10

SCHEDULE 10 STAMP OFFICE ACTIVITIES AND COLLECTIONS

1997-98 1998-99 1999-2000 2000-01

Fiscal Year

Average number of callers per day

• 1,834 1,455 1,371 1,448

Stamp Office

• 195 211 185 205

Kowloon Sub-Office

• 123 141 131 130

Tsuen Wan Sub-Office

Number of documents stamped

• 1,140,721 903,334 891,259 929,456

Stamp Office

• 104,383 112,916 100,686 109,249

Kowloon Sub-Office

• 44,365 51,728 47,923 50,312

Tsuen Wan Sub-Office

1,289,469 1,067,978 1,039,868 1,089,017 Total

Contract note duty ($m) ($m) ($m) ($m)

• 11,005.3 3,374.3 6,547.3 5,224.4

Collected through Stock Exchange of Hong Kong Limited

• 480.2 213.8 401.4 429.3

Collected by Stamp Office & Sub-Offices

11,485.5 3,588.1 6,948.7 5,653.7

Total

Duty collections ($m) ($m) ($m) ($m)

• *

28,908.3 10,078.0 12,035.8 10,827.1

Stamp Office*

• 174.8 97.7 68.7 72.2

Kowloon Sub-Office

• 11.8 12.8 11.0 11.9

Tsuen Wan Sub-Office

• 2.0 0.2 0.4 0.0

Lands Department

29,096.9 10,188.7 12,115.9 10,911.2

Total

*

Including contract note duty collected through Stock Exchange of Hong Kong Limited 2000 4 1

Lands Department ceased to collect duty on 1.4.2000

SCHEDULES

7411 2001 3 31

SCHEDULE 11 ESTATE DUTY DUTY ASSESSED AND COLLECTIONS FOR THE YEAR ENDED 31 MARCH 2001

2000 4 1 2000 01

Assessments issued in 2000 -01 Total

Assessments issued before

Original Assessments Additional

1 April 2000 Assessments

200 200 400 400 1,000 1,000 2,000 2,000

Estates valued Estates valued Estates valued Estates valued Estates valued under $2m $2m to $4m $4m to $10m $10m to $20m over $20m

($’000) ($’000) ($’000) ($’000) ($’000) ($’000) ($’000) ($’000)

1999 2000 Outstanding charges brought

261,031 – – – – – – 261,031

forward from 1999-2000

Less: Amount discharged 17,427 – – – – – – 17,427

1999 2000 Net outstanding charges brought

243,604 – – – – – – 243,604

forward from 1999-2000

Net duty assessed – 503 241 48,459 213,614 814,588 3,979 1,081,384

Penalties charged – 55 0 789 4,589 5,781 – 11,214

Interest charged 8,298 547 253 8,641 21,827 70,331 7,371 117,268

Total amount payable 251,902 1,105 494 57,889 240,030 890,700 11,350 1,453,470

2000 4 1 Less: Amount paid on account before

1 April 2000 – – 471 27,141 171,321 725,436 1,306 925,675

2000 01 Net duty, penalties and interest payable

in 2000-01 251,902 1,105 23 30,748 68,709 165,264 10,044 527,795

Less: Outstanding charges carried

2001 02 forward to 2001-02 177,689 745 0 12,490 21,973 70,497 168 283,562

2000 01 Net duty, penalties and interest paid

in 2000-01 74,213 360 23 18,258 46,736 94,767 9,876 244,233

Add: Duty and interest paid on account

in respect of assessments to be – – 968 26,591 173,651 1,057,008 125 1,258,343

issued in subsequent years

2000 01 Total collections in 2000-01 74,213 360 991 44,849 220,387 1,151,775 10,001 1,502,576

75

SCHEDULES

12

SCHEDULE 12 ESTATE DUTY STATISTICS

1997-98 1998-99 1999-2000 2000-01

Fiscal Year

($’000) ($’000) ($’000) ($’000)

Assessment

1,124,063 1,167,991 1,358,871 1,081,384

Duty assessed

191,778 212,960 185,722 128,482

Penalties and interest

1,315,841 1,380,951 1,544,593 1,209,866

Total

Collection

1,087,058 866,162 893,776 1,258,343

Payment before assessment

501,006 370,504 377,854 244,233

Payment after assessment

1,588,064 1,236,666 1,271,630 1,502,576

Total

Arrears

3 31

198,406 238,998 261,031 283,562

Arrears as at 31 March