績效管理平衡計分卡之分析 - 政大學術集成

40

0

0

全文

(2) 績效管理平衡計分卡之分析 An Analysis of the Balanced Scorecard for Performance Management 研究生:金里安. Student: Julio Quinteros. 指導教授:吳文傑. Advisor: Jack Wu. 國立政治大學. 學. ‧ 國. 立. 政 治 大. ‧. 商學院國際經營管理英語碩士學位學程. A Thesis. n. al. er. io. sit. y. Nat. 碩士論文. v. i Submitted to CInternational MBAnProgram. hengchi U. National Chengchi University in partial fulfillment of the Requirements for the degree of Master in Business Administration. 中華民國一百年一月 January 2011.

(3) Acknowledgements First and foremost, I would like to thank my family for all their support during these two years away from home. They have been an incredible source of strength and confidence. I would also like to thank my advisor, Professor Jack Wu, for his time and guidelines, and of course all my teachers at the IMBA for taking the time to show me something valuable in each class. My deepest gratitude goes to my friends at the IMBA, and in general, the people I have met in Taiwan. You have made these two years here truly feel like a second home. I hope to see you again in the future.. 立. 政 治 大. ‧. ‧ 國. 學. n. er. io. sit. y. Nat. al. Ch. engchi. i. i Un. v.

(4) ABSTRACT Business literature is full of management techniques aimed at improving a company’s performance, strategy design and employee engagement. The Balanced Scorecard (BSC) is one of those techniques, and one that has considerably gained most of the attention since it was first introduced in 1992 by Dr. Robert S Kaplan and David P. Norton after a joint research. In the document, they suggested that a business should be studied using four perspectives: customer’s perspective, internal business perspective, innovation and learning perspective, and of course, the financial perspective, which is any company’s ultimate goal. The purpose is that managers should manage, ideally, three to five goals in each perspective and then have. 政 治 大 organization’s vision and translate that vision into measurable actions that employees can 立 understand and follow accordingly. specific measures for those goals. The scorecard could then help managers simplify the. ‧ 國. 學. The Balanced Scorecard is basically a performance analysis technique, designed for the ultimate purpose of translating an organization’s overall business strategy into specific,. ‧. quantifiable goals and to monitor the organization’s performance with respect to achieving. sit. measures that focus on both short and long term performance.. y. Nat. those goals. It provides, like the name states, a balance of financial and non-financial. n. al. er. io. This document seeks to explain the BSC methodology and provide some evidence of its use in. i Un. v. companies worldwide. It is also complemented with personal experience with the tool at a corporation in El Salvador.. Ch. engchi. Research shows that companies that have implemented the BSC have seen significant improvements in their results. These results are not due solely to the BSC implementation, but they are evidence that the BSC can be an effective tool to help organizations achieve their strategic goals more easily if implemented correctly.. ii.

(5) TABLE OF CONTENTS Acknowledgements………………………………………………………..……i Abstract……………………………………………………………………..….ii Table of Contents…………………………………………………………..….iii Figures………………………………………………………………………....iv 1. Introduction……………………………………………………………..….1 1.1 What is a Balanced Scorecard……………………………………..….1 1.2 Origins and Evolution……………………………………………..…..1. 2. 政 治 大. Dissecting the Balanced Scorecard………………………………….......….8. 立. 2.1 The 4 Perspectives of the Balanced Scorecard……………………..…8. ‧ 國. 學. 2.1.1Financial Perspective…………………………………………..….8 2.1.2Customer Perspective…………………………………………..…9. ‧. 2.1.3Internal Processes Perspective…………………………………..10. y. sit. Practical examples of the Balanced Scorecard in action……………….…12. io. er. 3. Nat. 2.1.4Learning and Growth Perspective…………………………….....10. 3.1 ENERCO………………………………………………………….….13. n. al. iv. 3.2 Unum Corporation……………………………………………….…..16 n C. hengchi U. 3.3 Executive BSC in a United Nations Agency………………………....20 3.4 BSC at MTETC…………………………………………………….....23 3.5 More examples of the BSC…………………………………………..26 4. Personal Experience with the BSC………………………………………...27. 5. Conclusions………………………………………………………………..32. References……………………………………………………………………..34. iii.

(6) FIGURES 1. Figure 1: BSC General Model……….……………………………..……….3. 2. Figure 2: Linkage Model…………………….…………………………..….5. 3. Figure 3: BSC Third Generation………………………………………..…..7. 4. Figure 4: BSC Perspectives………………………………………………..12. 5. ENERCO’s BSC Development Process…………………………….……..14. 立. 政 治 大. ‧. ‧ 國. 學. n. er. io. sit. y. Nat. al. Ch. engchi. iv. i Un. v.

(7) 1. INTRODUCTION 1.1 What is a Balanced Scorecard? The Balanced Scorecard is basically a performance analysis technique, designed for the ultimate purpose of translating an organization’s overall business strategy into specific, quantifiable goals and to monitor the organization’s performance with respect to achieving those goals. It provides, like the name states, a balance of financial and non-financial measures that focus on both short and long term performance. Perhaps one of the most important qualities is that it gives an insight into areas of the company that are not looked at traditionally by upper management, but that reflect on the company’s financial performance. 政 治 大 Making a profit is every company’s ultimate goal, so it’s no surprise that the Balanced 立 Scorecard (BSC) focuses on the financial perspective as well, but it also includes other areas nonetheless.. ‧ 國. 學. of the company that reflect on the bottom line: customer, internal processes and people. The ultimate purpose of this management technique is to integrate the areas that make a. ‧. business model and serve as a tool to optimize that business model in order to achieve. y. Nat. financial results, while at the same time keeping customers and employees satisfied. In recent. sit. years, the BSC has evolved to include more areas related to a business, but these 4 areas. n. al. er. io. remain the most commonly used to evaluate a company’s success using this technique.. 1.2 Origins and Evolution. Ch. engchi. i Un. v. One way or another, every company measures their performance following the same basic financial indicators, and other indicators that management considers important for their success. From this perspective, it is clearly difficult to establish which company started using a management technique such as the BSC. Performance management as a business activity also has a long history in management literature and practice, and management historians suggest that the origins of performance management can be dated back to the nineteen fifties. The first formal BSC was developed by Art Schneiderman during the mid eighties, while he was the process owner for non-financial performance measures at Analog Devices, a semiconductor company. Schneidermann started with Analog’s five-year strategic plan and its Total Quality Management initiatives, and generated the BSC from there. Using Japanese continuous improvement techniques, having profound knowledge of the company’s business 1.

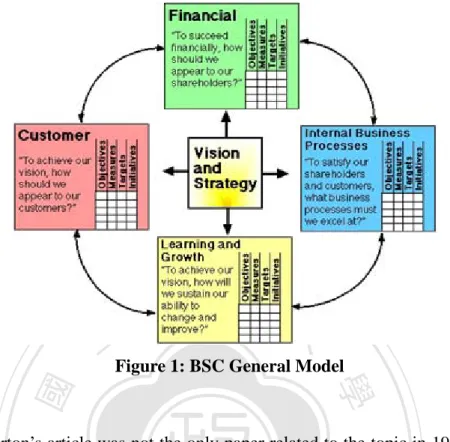

(8) model, and after obtaining support from Ray Stata, CEO at the time, he started developing the key indicators that would define the company’s strategy during those 5 years. It’s interesting to see that after all these years, implementing a BSC still follows this basic roadmap for almost any company, and trial and error are still a part of this process. In 1992, Harvard Business School Professor Robert S. Kaplan and management consultant David P. Norton published research project that took them almost a year, and it involved 12 companies. In their paper, they concluded that the traditional financial measures that most businesses use could not provide an accurate or at least complete picture of a company’s performance during the fast paced business environment of the nineties. It would also be. 政 治 大. foolish to force managers to choose between “hard” financial measures and “soft” operational and customer centric measures, which led them to develop a method that would include both. 立. measures to help managers handle both measures in a balanced way. “The BSC includes. ‧ 國. 學. financial measures that tell the results of actions already taken”, the paper explains, and “it complements the financial measures with operational measures on customer satisfaction,. ‧. internal processes, and the organization’s innovation and improvement activities”. These “lagging” indicators are used as part of the feedback process in those actions taken.. y. Nat. sit. Kaplan and Norton suggested that a business should be studied using four perspectives:. al. er. io. customer’s perspective, internal business perspective, innovation and learning perspective,. n. and of course, the financial perspective. The purpose is that managers should manage, ideally,. Ch. i Un. v. three to five goals in each perspective and then have specific measures for those goals. The. engchi. scorecard could then help managers simplify the organization’s vision and translate that vision into measurable actions that employees can understand and follow accordingly.. 2.

(9) 政 治 大. 立Figure 1: BSC General Model. ‧ 國. 學 ‧. Kaplan and Norton’s article was not the only paper related to the topic in 1992, but it gained almost immediate popularity, and is thus, one of the most quoted papers on the BSC. It was. Nat. sit. y. followed by a second paper in 1993 and a book in 1996. All this popularity has created the. al. er. io. impression that Kaplan and Norton created the BSC concept, despite the fact that others may. n. have been already using it and the fact that a similar management process has existed in. Ch. i Un. v. business literature for a long time. Nonetheless, their paper coined most of the ideas that are. engchi. still prevalent in today’s business environment and made the name popular in the business world. The BSC has come a long way since its introduction during the early nineties. Something that started as a concept has evolved into a framework used by many businesses to manage their vision and strategy, supported by software to make it faster and easier to deploy past results and new initiatives to employees. The changing natures of this model and the changing business environment have led to new perspectives and approaches being used, depending on the business model and/or industry in which it being applied. One of the most notable changes is the refinement of the Learning and Growth Perspective, which seems to be the most difficult for companies to define. Historically, companies have struggled with this perspective and renamed it to Human Perspective, which. 3.

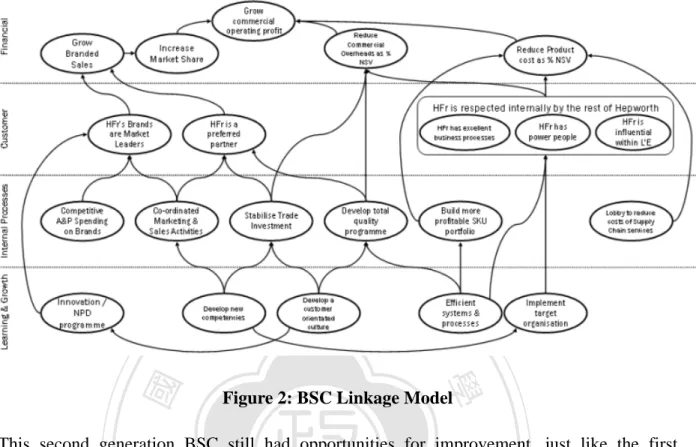

(10) has led them to focus only on personnel satisfaction, turnover, etc. While not entirely wrong, there is more to the original concept than these simple measures, which is why Kaplan and Norton have refined what they consider to be the main components of the Learning and Growth Perspective: •. Human Capital (Employees' skills, talent, and knowledge). •. Information Capital (Databases, information systems, networks, and technology infrastructure). •. Organization Capital (Culture, leadership, employee alignment, teamwork, and knowledge management). 政 治 大 The original 4 perspectives are broad, but they are not comprehensive, which has led to many 立 organizations extend the framework or add new perspectives that suit their needs. Businesses. ‧ 國. 學. now include a “green” perspective, innovation, society, or ethics, among others. Measuring these perspectives and the resulting metrics may not be visible in the monthly or annual. ‧. reports, but these behavior-based metrics may provide a better overall view of the level of. y. Nat. corporate culture, for example, that a company is interested in achieving. The BSC can also. sit. be used in other areas, such as non-profit organizations, health organizations, public. er. io. organizations, health care, etc. As long as the organization that is implementing this technique. n. al. iv n C an evolution h e n gsince c h iits Uinception,. is aware of who are the stake holders in their business model. The BSC has gone through. mostly to fit the different. businesses and their stake holder’s needs. In fact, the most important changes have not been just due to the need of new perspectives, but rather because of changes in the strategic information needs of managers, mainly, the causality between measures. Measure-based linkages provide a richer model of causality than the early versions of the BSC (for example, determining numerical correlation between indicators), despite the fact that they may be difficult to determine. This evolution is illustrated in two papers also by Kaplan and Norton from 1996, which describe linkage as occurring between measures and also between strategic objectives. These changes, according to Kaplan and Norton, made the BSC evolve from “an improved measurement system to a core management system.. 4.

(11) 立. 政 治 大. ‧ 國. 學. Figure 2: BSC Linkage Model. ‧. This second generation BSC still had opportunities for improvement, just like the first generation did. Whereas the focus of concern during the first generation was related primarily. y. Nat. sit. to measure selection (filtering), the focus of the second generation are related more to how to. al. er. io. group this measures (clustering). Companies implementing the BSC found problems selecting. n. measures, grouping them, setting the targets and cascading the indicators to lower levels of. Ch. i Un. v. the organization. Part of the problem was the design process of the BSC, which assumes. engchi. interpretation and understanding of the vision and mission of an organization is shared by the team implementing the BSC, but doesn’t ensure that this is the case. Kaplan and Norton’s original design suggested that the organization’s strategy should be analyzed by a small group composed of key personnel supported by consultants. This analysis would then be used to select priorities and strategic objectives for the organization’s management team. This approach may weaken the value of the strategy and the efficacy of the implementation, since it lacks support from the people who will actually be executing it. The third generation BSC is built upon refinement of the second generation design, with some new features in order to make it more strategically relevant for the company. The evolution was mainly due to the need for validation of strategic objective selection and target setting, which originated the development of another design element, known as the “Destination. 5.

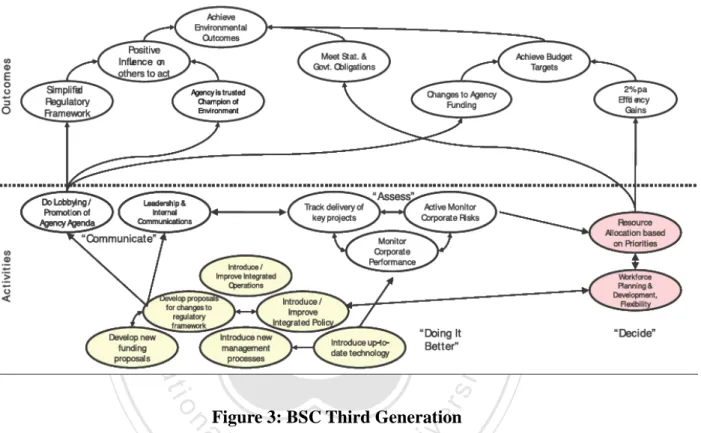

(12) Statement”. Originally, these statements were created towards the end of the design process by challenging the team involved in the BSC design to imagine the impact on the organization of the achievement of the strategic objectives chosen earlier during the design process. This helped identify inconsistencies in the objectives chosen caused by the potential limitation inherent in the use of only four perspectives. The final document was useful to validate the targets chosen for the selected measures. The innovation consisted in realizing that such a statement could be a useful reference point for the target setting process, not just as a feedback at the end of such process. Because of its intended role as a target setting device, effort was made to guarantee that the statement quantified “how much” of key things would. 政 治 大. be achieved at a specific date in time, which made the strategy easier to conceptualize. It was found that management teams were able to discuss, create, and relate to these. 立. “Destinations Statements” easily, and without referencing the selected objectives. After that,. ‧ 國. 學. the design process was reversed, leading to the creation of the “Destination Statement” being the first design activity, rather than the final one. It was also found that by working from. ‧. “Destination Statements”, the selection of strategic objectives, and articulation of hypotheses of causality was also much easier, and consensus could be achieved in the team designing the. y. Nat. n. al. er. io. two things:. sit. BSC more easily. Basically the third generation of BSC enhanced the second generation with. •. Ch. i Un. v. Destination Statement: a description of what the organization is likely to look like at. engchi. an agreed future date. The destination statement is sub-divided into descriptive categories that serve a similar purpose to the “perspectives” in the first and second generation BSC’s. •. Strategic Linkage Model with “Activity” and “Outcome” perspectives: A simplification of a 2nd Generation Balanced Scorecard strategic linkage model – with a single ‘outcome’ perspective replacing the Financial and Customer perspectives, and a single ‘activity’ perspective replacing the Learning and Growth and Internal Business Process perspectives.. 6.

(13) The two-perspective linkage model is an important departure from the original concept of Kaplan and Norton’s four perspective model, but the main difference between the second and third generation BSC is found mainly in how the strategic linkage model is designed, not the way it looks.. 立. 政 治 大. ‧. ‧ 國. 學 er. io. sit. y. Nat. n. 3: BSC Third Generation aFigure i v being a strategic control tool for l n Kaplan and Norton stated that theCmain focus of the BSC was hengchi U. managers, not just a management control tool. In practice, however, academic research and practical application has focused on the application of the BSC for management control purposes, which may be linked to the prevalence of the first generation BSC model in many companies. The transition from the first to second generation of the BSC coincided with the positioning of the BSC as a tool to support strategic control. The practical design of the BSC focused on forming a consensus within the team managing the BSC, which is consistent with the thinking on leadership over many years. The transition from second to third generation represents a significant change in the approach when designing a BSC. Adoptions of third generation designs have been helpful in supporting the development of multiple BSC’s within complex organizations, and it has also helped to solve issues of information asymmetry, in which objectives and goals are not clearly transmitted from one party to other in an. 7.

(14) organization. The projection of a centrally developed strategy into components of an organization can be problematic, in part because the evaluator knows more about the common objective than the rest of the organization. “Destination Statements” help address this communication problem by incorporating more of the local context and issues that cause strategic objectives to be selected. It has been a long road for the balanced scorecard since its inception (assuming Kaplan and Norton as the first to adopt this model) and as we can see, the original concept has been through many changes, not just conceptually but mainly in terms of the design process. First generation BSC’s are still being developed and they are probably still the large majority of. 政 治 大. BSC designs introduced into organizations today. In fact, companies are still trying to figure out how to make this concept work, despite the fact that it has been refined over the years.. 立. Nonetheless, even if new perspectives are added or even if the design process is changed, the. ‧ 國. 學. four basic perspectives remain a core element of this design process, since these perspectives can help describe most current business models. The objectives are also still the same:. ‧. Translating the vision into operational goals. •. Communication the vision and link it to individual performance. •. Business planning and index setting. •. Feedback, learning and adjusting the strategy accordingly. n. er. io. al. sit. y. Nat. •. Ch. engchi. i Un. v. 2. DISSECTING THE BALANCED SCORECARD. 2.1 The 4 Perspectives of the Balanced Scorecard As stated before, 4 perspectives comprise the original concept of the BSC, and those 4 perspectives are still prevalent today when companies try to implement this management methodology. Regardless of what indicators are assigned to each perspective and how they link to each other in order to reflect a company’s strategy, the concepts are basically the same. Each perspective is oriented to satisfy each stakeholder.. 8.

(15) 1. Financial Perspective This perspective answers the question “How do we look to our shareholders?” Making money and staying financially solvent is any company’s ultimate goal. This is why this perspective remains so important in the BSC. Kaplan and Norton developed the BSC during a period of time in which financial measures were coming under attack from management experts. They claimed that if you measure a company’s performance solely by the financial results would encourage companies to focus on short-term results, and thus, avoid actions that would create value in the long term. It was also argued that financial measures looked at past actions taken, rather than look forward at future possibilities.. 政 治 大. Kaplan and Norton do not ignore the traditional need for financial data. In fact, they found that they are an important piece of the management puzzle, but managers need to know if the. 立. operational or customer oriented improvements are reflected in the bottom line. This. ‧ 國. 學. perspective includes traditional measures, such as the return on assets, net profit, operational costs, economic value added, etc. Financial measurements will point out the need to make. ‧. further changes.. y. Nat. sit. 2. Customer Perspective. al. er. io. This perspective answers the question “How do the customers see us?” It is a measure of how. n. the company provides value to the customer. In a very broad sense, satisfying financial. Ch. i Un. v. statements should be a result of satisfied customers, and this perspective ensures that there is. engchi. at least a link between both elements in the business model. Customer satisfaction should be a leading indicator: if they are not satisfied, they will eventually find other companies that will meet their needs. When developing metrics for customer satisfaction, the analysis should focus on the different types of customers, their degree of satisfaction and the processes used to deliver products and services to the market. It is very common to hear of companies making customer service a priority, and the balanced scorecard helps managers to translate this vague goal into specific measures that truly reflect the issues that are most important to their customers. Kaplan and Norton recommend four main areas of customer concern: time, quality, cost and performance. Companies should establish a goal for each of these areas and turn those goals into at least one specific measurement, such as customer satisfaction, new products, customer retention, on-time-. 9.

(16) delivery, reliability, market share, etc. Some of these measurements can be acquired with internal data, but for others to be incorporated into the BSC, managers will need to acquire outside information through customer evaluations and benchmarks, and this will be a valuable exercise because it will force managers to view their company from the customer’s perspective.. 3. Internal Processes Perspective This perspective is closely related to the customer perspective, and it answers the question “What must we excel at?” or in other words, what should the company excel at to be. 治 政 established previously into measures that reflect the 大 company’s internal operations. These 立 measures help managers to know how their business is running, and if the products and competitive? Thus, the focus of this perspective is to translate the customer-centric measures. ‧ 國. 學. services being delivered meet the customer’s expectations. More importantly, these measurements need to be translated into indicators that can be influenced by employee actions,. ‧. which means that internal goals and performance indicators need to be broken down at the local level to provide a link between top management goals and individual goals, such as. y. Nat. sit. reduction in unit costs, reduced waste, defect rate, time per transaction, etc.. er. io. Kaplan and Norton wrote that “this linkage ensures that employees at lower levels in the. al. n. iv n C contribute to the company’s overallhmission”. They also e n g c h i U recommend that managers need to focus on those critical internal operations that enable them to satisfy customer needs.. organization have clear targets for actions, decisions and improvement activities that will. 4. Learning and Growth Perspective In a broad sense, this perspective seeks to answer the question “Can we continue to improve and create value?” It includes goals and indicators related to continuous improvement in the company’s ability to innovate, improve and learn. Historically, this has been a very misunderstood perspective, and as mentioned before, in some cases it has even seen its name changed to “people” in order to simplify its implementation. It has also been the only perspective that has had to be refined by the original authors, due to its complexity and has now been dissected in three subsections:. 10.

(17) •. Human Capital (Employees' skills, talent, and knowledge). •. Information Capital (Databases, information systems, networks, and technology infrastructure). •. Organization Capital (Culture, leadership, employee alignment, teamwork, and knowledge management). Implementing this perspective as “People Perspective” can be effective in knowledge-worker organizations, in which people are the main repository of knowledge, and thus, focusing on goals such as “training” is a good thing. Kaplan and Norton, however, emphasize that. 政 治 大. “learning” is more than just “training”; in also includes other elements, such as mentors and. 立. tutors within an organization. It also includes technological tools (related to learning and. ‧ 國. 學. growth), and any other indicator that measures a company’s ability to innovate, improve and learn, because these elements are tied directly to the company’s value.. ‧. The financial perspective is important because it deals with results from past actions and it deals with the financial value of the company. The innovation and learning perspective, on the. sit. y. Nat. other hand sets measures that help a company compete in a changing business environment,. io. er. and it includes indicators such as the number of new products offered, amount of training, employee retention, employee empowerment, etc. Again, the key approach of this perspective. n. al. Ch. i Un. v. is in the ability to create value; not just in developing employee centric measures.. engchi. 11.

(18) 政 治 大 Ideally, these four perspectives 立should align as shown above. It all starts with a company that Figure 4: BSC Perspectives. ‧ 國. 學. has a clear vision of its growth opportunities, and also makes sure it has the right people in place. A company that does this should be able to optimize its operations and processes in order to keep customers satisfied, by delivering the products and services that clients are. ‧. expecting. Satisfied customers will become a strategic advantage that should be reflected in. sit. y. Nat. the financial results. These results will be the main source of feedback for the effectiveness of. io. Balanced Scorecard.. n. al. er. the overall strategy, thus completing the management cycle. This is the essence of the. Ch. engchi. i Un. v. 3. PRACTICAL EXAMPLES OF THE BSC IN ACTION The BSC helps managers balance strategic focuses on four perspectives, cause and effect relationships and developing a more systemic strategy. However, complex dynamics within companies, misunderstandings of the BSC implementation method and of course, limitations of this technique have led to both success and failure stories. This chapter focuses on both sides of the spectrum and highlights some of the best practices based on selected examples of its implementation.. 12.

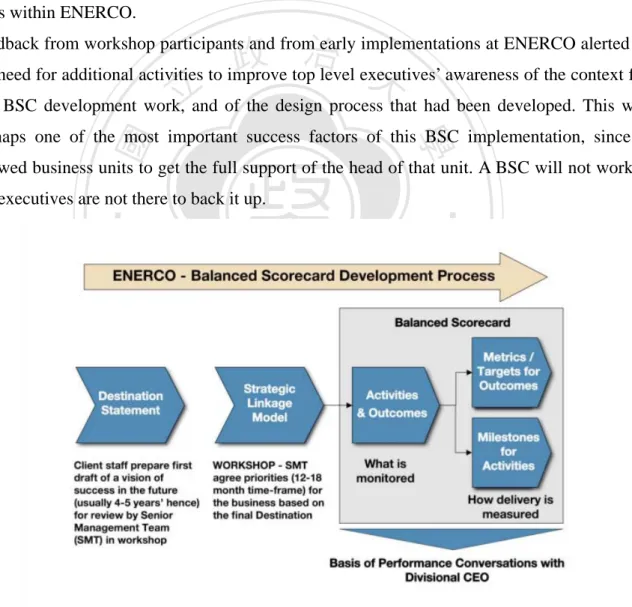

(19) 3.1 ENERCO The global energy company ENERCO implemented the BSC method for its Business Unit and Functional Senior Management Teams worldwide over a 12 month period in 2007-2008. The goals were to improve the alignment of business units behind the division’s strategic goals, and to provide a mechanism to better track the execution of this strategy. The task presented several challenges, mainly due to the complexity of ENERCO’s organizational design. The organization also has an inclination towards deep customization of standard management tools and they also needed the BSC to integrate neatly with other ongoing projects.. 政 治 大. Previously, ENERCO had struggled with the general challenges of performance management, and its own internal analysis had already highlighted the need for improvement in some. 立. processes and systems:. Strategies were not clearly formulated, communicated or linked to the vision. •. Accountabilities were not clearly defined. •. Consequences of failing to deliver against the plan were unclear. •. Performance monitoring relied heavily on detailed financial metrics alone. •. Financial targets were set at easily achievable levels. sit. io. er. Nat. y. ‧. ‧ 國. 學. •. al. n. iv n C a third generation BSC approach h was selected. ENERCO’s already existing 5 year plans engchi U. ENERCO selected 2GC to help support the development of this management tool in 2006 and. offered a good starting point for the design, but the challenge was developing a process that. would help managers translate ENERCO’s strategic goals to present priorities, and for these priorities to actually be “balanced”. Additionally, the complex organizational design at ENERCO meant that in many cases, the senior management team for the business being addressed was scattered across at least two continents. This was particularly troublesome, since the third generation method aims to build consensus among senior management members, which is most easily achieved through whole-team meetings.. Work was split in four stages: 1. Design and test a customized BSC design method 2. Roll-out of the reference design process with further business units and functions 13.

(20) 3. Training on the deployment of the reference design process to internal facilitators 4. Awareness sessions for key financial managers. In order to accelerate the roll-out of the third generation BSC, ENERCO asked 2GC to develop and deliver a series of training courses to transfer skills and knowledge to in-house project teams. The result was a two day training course that reflected the essence of the methodology used and included examples of material produced (such as Destination Statements, Strategic Linkage Models and Metrics/Targets), derived from the early adopting units within ENERCO.. 政 治 大. Feedback from workshop participants and from early implementations at ENERCO alerted of the need for additional activities to improve top level executives’ awareness of the context for. 立. this BSC development work, and of the design process that had been developed. This was. ‧ 國. 學. perhaps one of the most important success factors of this BSC implementation, since it allowed business units to get the full support of the head of that unit. A BSC will not work if. ‧. top executives are not there to back it up.. n. er. io. sit. y. Nat. al. Ch. engchi. i Un. v. Figure 5: ENERCO's BSC Development Process. The size, scope and organization structure at ENERCO created some resistance to the 14.

(21) implementation of the BSC. Some senior managers felt that they already had all they needed with their existing approach to performance management: •. A five year Strategy derived from the 2020 vision. •. A roadmap of implementation. •. Year to year performance metrics allied to an incentive pay scheme. •. Financial, Operational and Health & Safety metrics. ENERCO’s internal analysis had already revealed that in some business units and functions, the Road Map had little influence with the teams, and in some cases it wasn’t even used at all.. 治 政 大 the businesses from making management. All these elements had the effect of discouraging 立 the needed changes, which made it harder for ENERCO to deliver on its strategic agenda. The study also highlighted a disconnection between strategy and year to year performance. ‧ 國. 學. The approach adopted to deal with this engagement issue had three components:. ‧. •. Senior sponsors of the program were encouraged to make clear and visible their. y. Nat. support for the BSC process. •. Project facilitators were encouraged to be highly flexible in their implementation of. n. al. er. sit. Participants in the BSC design work were strongly supportive of it.. io. •. i Un. v. the design process, rather than blindly insisting on compliance with a process.. Ch. engchi. ENERCO and 2GC completed the BSC design within 19 Business Units; each resulting in BSC’s showing 12-18 months priorities, metrics and targets. 16 of the workshops were in major Business Units and 3 within functions in the UK, continental Europe, USA and Africa. This third generation approach was able to address ENERCO’s Performance Management issues listed before, and thanks to this, performance conversations within the company are now based on a broader range of strategic and operational information than previously, with more clearly defined accountabilities in place to ensure priorities are achieved. Comments and feedback from the people involved support the implementation of the BSC:. “The Balanced Scorecard Process provides some much needed structure and standardization 15.

(22) for how we set out, monitor, and track our strategy delivery. It facilitates a discussion for a Senior Management Team to: Articulate and agree what needs to be done to deliver the strategy •. Work out what the overall business milestones and activities should be. •. What success looks like and how we should measure it. •. What really is business critical and requires more effort. •. What resource and skills & capabilities we need.. We intended to do this anyway…..the Balanced Scorecard provides us with the process and tools to do it better”. 立. 政 治 大. ‧ 國. 學. 3.2 Unum Corporation. A Fortune 500 company, Unum is a market leader in disability, group life, long term care and. ‧. voluntary benefits, with operation in the US, Canada, the UK, Continental Europe, Bermuda and Latin America.. y. Nat. sit. Unum had become a complex organization through growth and acquisitions, and the chairman. er. io. recognized that a single focus on a financial result would be difficult to communicate. al. n. iv n C BSC came when the organization required set of goals that everyone could relate to and h e nagnew hi U c that would focus the employees’ energies on improving customer-facing performance while effectively, and would not reflect the diverse challenges of the corporation. The need for a. improving further shareholder returns. In essence, he wanted a balanced set of measures that would reflect the interests of all Unum’s stakeholder groups. James Orr III, chairman and chief executive at the time, created a team of 13 senior managers to develop this new set of “balanced” goals and measures. Although some outside experts were used to facilitate the early meetings, it was the team itself which owned the process and chose the final set of interlocking goals and measures. It is worth pointing out that that Unum’s strategic goals and measures are to support a clearly defined and meaningful corporate vision. This helped facilitate a specific vision statement for each of its four scorecard perspectives. Unum’s vision was “We will achieve leadership in our business”. This may sound like a 16.

(23) generic statement that could be applied to any company in any industry, but this vision was supported with a description of what the vision meant: •. “Leadership does not necessarily mean a dominant market share. Rather, we will achieve leadership in areas that are meaningful and important to our business and market”.. •. “We will focus our business on special risk-relieving products for which we can establish and sustain profitable positions. Development of these products will be driven by the needs of the customer, in both domestic and international markets”.. 治 政 大 These values are: motivated towards achieving breakthrough business performance. 立 • We take pride in ourselves and the organization’s leadership position. Furthermore, corporate values play a key part in creating a culture where employees are. •. We value customers. •. We value communication. ‧. ‧ 國. We value and respect people. 學. •. y. Nat. •. Operating effectiveness. •. Customer satisfaction. •. Shareholder value. n. al. er. UNUM people. io. •. sit. Unum’s BSC consists of four perspectives:. Ch. engchi. i Un. v. During the implementation, Eileen Farrar, vice president of human resources noted that one of the main challenges, but also a key element for achieving corporate goals and for making the scorecard meaningful to all employees is investing time and energy into employee communication. Farrar found that implementing a scorecard is a process of relentless communication and education that must be explained in a way that makes sense within the context of the employee’s own working environment. Just like ENERCO’s case, it was important to obtain senior manager’s participation, but it was just as important to be able to “cascade” the decisions made at that level to all levels in the. 17.

(24) organization. Otherwise, the results will be unsatisfactory without a doubt. At a corporate level, Unum has clearly defined what it means by each of its scorecard perspective visions. In this case, starting with “We will have the mind of a customer and the pride of an owner” as the vision for the people perspective, the company has communicated throughout the organization that Unum’s employees should think like a customer, be interested in results, discover better ways, live by our word, continuously grow and learn, strive together towards our goals, feel accomplished and recognized, value differences, master change, share and listen.. •. 治 政 A benchmark survey measuring employees’ perception 大 of whether this behaviors are actually being “lived”立 within the organization. •. Employees within Unum America developed a trust workshop focusing on the barriers. Unum is making sure that this happens in 3 main ways:. ‧ 國. 學. that exist in the company to stop employees trusting managers. Findings are shared •. ‧. throughout the organization. 360 degree appraisal system. sit. y. Nat. er. io. Also, to contribute to all the perspectives, the chairman constantly charges teams to focus on. al. iv n C sharing that information throughouth the organization.UHe also holds an annual chairman’s engchi review, in which he meets with a group of selected employees from each operating company n. developing some area of best practice, in order to look at how that area can be improved and. or function and discuss how they perceive the progress towards the company’s goals. The chairman’s belief in the scorecard was shown in UNUM’s Annual Report 1997, where, in his letter to shareholders, he outlined the progress against each of the scorecard perspectives. Having the chairman’s support in this initiative was one of the key success factors at Unum, and it is definitely an element that must be considered when implementing a BSC anywhere. No matter how articulated the process is, or how sophisticated the BSC to be implemented, the deployment will not be effective without having set this milestone first. In Unum’s case, for the deployment of the corporate scorecard, each operating unit was charged with finding its own way to achieve the strategic goals. Again, it was important to obtain the full support of the director of each unit, since that person would be handling the. 18.

(25) rest of the deployment process. All initial efforts would’ve stopped at the operating unit’s level otherwise.. Farrar said: “It is up to the management of each company to decide on the most effective way to move that company towards strategic goals. At unit level, it is the responsibility of the manager to roll the unit’s goals back to company and corporate goals. However, annual business goals will not be accepted unless they represent progress towards our corporate goals.”. 政 治 大. Alignment was also ensured with Unum’s performance contracts, in which individual objectives support the scorecard goals. This way, you can clearly see the line of sight from. 立. employee performance through unit, company and ultimately to corporate performance.. ‧ 國. 學. In conclusion, Unum’s BSC is still evolving, but we have to admit that it was a success in its initial implementation. This was the result of getting some fundamental things right, such as:. ‧. 1. The original BSC was built on the success of Unum’s corporate goal, but it was designed to reflect the changes to the organization and a new set of business. sit. y. Nat. challenges. al. er. io. 2. The chairman was totally committed to creating the BSC, and he has been involved in. n. the creation and communication to stakeholder groups.. Ch. i Un. v. 3. Senior managers at Unum owned the process of building the BSC, and used external. engchi. help only as facilitators in early meetings.. 4. Unum already had a clearly defined and meaningful corporate vision 5. The BSC was designed to meet specific time-sensitive goals 6. The reason behind the BSC’s goals and measures were clearly explained to all employees at all levels of the organization 7. The company focused on internal communications 8. All individual performance contracts reflect the scorecard’s four perspectives. With the help of the BSC, the company improved its operating cost structure by 22 per cent over a 1992 base year, and was on its way to achieve the 1998 of 33 per cent. Unum also exceeded its People perspective’s goals, winning a top employer award from several. 19.

(26) magazines including Fortune, Working Mother, Business Week and Equal Opportunity. And although UNUM did not reach their aggressive goal of reaching top-quartile performance of the Standard & Poor’s 500 at 1997 year-end, the company did make the second quartile, and delivered annualized returns of 30.2 per cent. This excellent performance helped rank the company 39th of the 457 current Standard & Poor 500 companies with 10-year stock histories.. 3.3 Executive BSC in a United Nations Agency In February 2008, and during a period of 18 months a United Nations (UN) Agency in their New York City HQ decided to implement a new corporate management system, integrating a. 政 治 大. third generation BSC with the UN’s already existing Results Based Management system. Initially, the Strategic Planning Office (SPO) and the Executive Committee, working with a. 立. consultant group produced two different versions of the BSC. These would be used in areas. ‧ 國. 學. where collaboration between SPO and the EC was essential, and to ensure alignment in the results targeted by each group. After a 12 month pilot, the project was completed with a. ‧. redesign of the Agency BSC to reflect evolving strategic goals and priorities. The UN agency had already tried to implement a BSC during 2004-05, and significant work. y. Nat. sit. was done to develop and promote the BSC in-house. However, this initiative failed because. al. er. io. the methodology was perceived to be too complex and there was a failure to actually sell its. n. value at the most senior level, two of the most common pitfalls when attempting to implement. Ch. i Un. v. a BSC. In 2006, the Executive Committee decided to adopt this methodology again and link it to the 2008-2011 Strategic Plan.. engchi. An internal analysis revealed that: 1. The agency was good at planning for the medium term. Office Management plans and personal development plans were already in place thanks in part to a very capable strategic planning team 2. Perceived difficulties often came up when trying to consistently translate these planning documents into planned-for results, in particular for the team in New York. 3. While field-level results and improvements were impressive, HQ-generated management improvements were less obvious. 20.

(27) 4. Accountability at the Executive Committee level was not strongly established, with little discussion of the objectives to be pursued jointly. One conclusion was that these weaknesses were due in part to the fact that current plans contained more ambition than central management resources could deliver.. Implementation would initially follow the same basic framework: Establish the Destination Statement, design a Strategic Linkage Model and then define the metrics and targets to meet the objectives. Problems appeared, however, when due to cultural norms of the UN, it became. 政 治 大. unfeasible for the Executive Committee members themselves to participate in the BSC development. Instead, a group was established comprised of Regional Representatives, staff. 立. functions (via video conference) and four Country Offfice managers.. ‧ 國. 學. Mixed management levels in the room affected the workshop, since it reduced the amount of open contributions of all attendees. The process was also affected by the limitations of video. ‧. conferencing technology in a workshop such as this, a problem which unfortunately could not be circumvented due to the nature of the organization structure. At the end of the workshop, a. y. Nat. sit. Strategic Linkage Model (SLM) was produced. The SPO continued leading the work under. al. er. io. direct guidance of the Executive Office and several meetings took place with the Chief. n. Executive, which allowed the project team to explain the accountability-related benefits of the. Ch. i Un. v. design process. The meetings also secured the Chief Executive’s support for completing and deploying a full EC level BSC.. engchi. The EC decided that a “management” results perspective would be the top current priority, which allowed them to limit the development issues on the BSC. A final retreat session also took place with the consulting group to agree how the review process would operate and to ensure that cross-functional working could take place in an environment where “silo” working was already strongly established. The UN Agency decided to pilot the BSC at a regional level before considering any use in Country Offices. The pilot included: •. Development by the Regional Director, along with the consulting group of a draft Destination Statement for 2001. •. A workshop with the Regional management team in HQ to create an SLM. 21.

(28) •. Work on metrics and targets by the Regional management team. •. Usage of the BSC tool by the regional management team to set and manage their performance agenda during 2007. After nine months of starting the pilot, the EC decided to review the BSC to focus the Director’s attention solely on the results, and delegate all activities to the deputy directors. This would also help to bring the BSC into line with the already existing departmental planning processes. This reset process had the goal to use agreed priority results to drive activities (due to the need for more coherence with the UN Results-based approach and to. 治 政 大 Results (efficient running of Results would also be divided into two categories: Management 立results (linked to the Agency’s core mandate). This would help the Agency) and Development reflect the Director’s decision to delegate activities to produce those results to their deputies).. ‧ 國. 學. give the BSC more influence with the rest of the organization, according to the implementation team.. ‧. In early 2008, the Executive Committee met again to revise their BSC, as explained above. The results differed from the consulting group’s SLM in having a more simplistic linking of. y. Nat. sit. results and activities, and being developed from results down to the required activities to. al. er. io. achieve those results, rather than bottom up.. v. n. The third generation BSC implementation has helped to bring transparency of performance. Ch. i Un. and it is also helping to strengthen accountability for performance at the top levels of the. engchi. Agency. It has also promoted open discussion and consensus across the EC and has also started to eliminate the “silo” working mentality that existed in the organization. Directors have also been able to adopt a performance review process that reinforces accountability for results, and it has also enabled improved performance at the centre, which translates in improved delivery at the country level. Indications are that this time, the Agency has implemented a management tool that the Executive Committee believes in, and will help to support improved Agency results as it continues to evolve. It has become evident that the BSC has been beneficial for this organization, but the implementation faced several challenges from which we can learn, just like the SPO did. Among some of the most important ones:. 22.

(29) •. Explaining to the Executive Committee the need for a top level BSC to drive the execution of the Agency’s strategic priorities. •. Influencing the CEO’s office to replace their CEO-centered process with one owned by the whole Executive Committee. •. Engaging new Directors in the process who had not been part of the initial design. •. Managing continued attack on the project from other Directors. •. Clarifying users of the differences between priorities and the metrics used to monitor progress against those priorities. Also, persuading users to manage the objectives, not the numbers. 3.4 BSC at MTETC. 立. 政 治 大. The MT Education and Training Center (MTETC) in Malaysia launched the BSC initiative in. ‧ 國. 學. 2000, but rather than implementing it because the unit wanted it, the division was selected to be involved in this pilot initiative. MTETC is an outfit that, at the time of the BSC initiative. ‧. was operating as a cost center, and once the initiative was started there was a debate whether. y. Nat. the division should continue to operate as a cost center or become a profit center. Mr. Ahmad,. al. er. io. it was felt that the BSC could help MTETC with this.. sit. CEO of the Malaysian Telco group at the time needed to reexamine MTETC’s direction, and. n. iv n C that all divisions and subsidiaries should a performance-oriented culture. A similar h e ndevelop gchi U. The BSC was also seen as a key element in carrying the directive from the parent company. BSC initiative had been put previously on hold at MTETC during a change of the General Manager, who did not share his predecessor’s interest in the BSC. In 2001, and under a new General Manager, Mr. Yunus, the BSC initiative was brought back. Mr Yunus was committed towards making MTETC a profit center, and he was confident that MTETC could generate more business and revenue instead of serving as a training center. The BSC was seen as a useful tool to track performance at MTETC and help the division become a profit center. MTETC’s corporate planners presented the BSC initiative in 2002, and in order to cascade MTETC’s goals, each manager was called to discuss with the CEO their Key Performance Indicators (KPI). Slight modifications were also done to the original four perspectives of the BSC in order to meet MTETC’s needs.. 23.

(30) The MTETC BSC team worked closely with the Corporate Strategic Planning department at the group level, but as expected, a number of issues arose once implementation started, especially when trying to develop indicators that would help the division migrate from being a cost center to a profit center. Given its history, units within MTETC never developed the habit or the information system to keep track of their expenses and income. A proper transfer pricing formula for inter-unit activities had not been developed, and at times, the data available at the units and the MTETC’s finance department did not match. This became an issue when trying to link individual performance with outcome, since it was almost impossible to attribute outcomes to individuals.. 政 治 大. The team leading the BSC focused in developing KPI’s for financial issues, and the main reason was because the team found it necessary to orientate MTETC’s managers towards. 立. more accountability for bottom-line measures, something that historically had never been an. ‧ 國. the team.. 學. issue for managers. Developing non-financial measures was even more difficult, according to. ‧. Interviews with tier 2 managers took place in 2002 to examine their views on the BSC initiative being rolled out. They needed to measure the level of involvement and commitment. y. Nat. sit. of these managers since they were the ones heading the main functional units and they would. al. n. BSC targets had not been cascaded to tier 3 managers yet.. Ch. er. io. be responsible for the implementation at those units. When the interviews were conducted, the. i Un. v. The interviews helped to make some important observations that even today are still a. engchi. problem when trying to implement a BSC.. 1. The BSC was seen as something good. However, when asked about their views on the specific “good” things of the BSC, it became obvious that most managers did not have a clear understanding of what the BSC was about, and the majority of managers only understood that it was a mechanism to develop KPI’s. 2. The majority of managers saw the BSC as another fad that MTETC was trying without actually being serious about its implementation. One of the managers mentioned that MT had a habit of launching all kinds of new management initiatives, but never went beyond the launching ceremony. 3. The BSC initiative was seen as an arbitrary and top-down process. It was perceived that managers were just given a set of targets with little discussion related to the. 24.

(31) viability or where those targets came from. 4. A common concern was a misalignment between the performance appraisal system that was under the group’s Human Resources function and the BSC performance measures being handled by MTETC’s Corporate Planning Unit. The HRM department assessed performance based on behaviors related to a set of competencies. Performance outcome was not included in the appraisal. Employees recognized that ultimately, their salaries and bonuses depended on how they do in the performance appraisal and not so much in the goals that were being introduced. This lack of linkage between the performance appraisal system and the BSC initiative resulted in lower. 政 治 大. level employees not feeling accountable for the performance measures included in the BSC. Thus, the expected result of making employees more profit oriented and. 立. accountable to the BSC targets was not achieved. ‧ 國. 學. MTETC’s case highlights some important pitfalls when implementing a BSC. In this case the. ‧. BSC was used arbitrarily and in a top-down manner, which led to skepticism and even passive resistance to the initiative. This was due to a lack of buy-in and commitment and also a lack. y. Nat. sit. of understanding of the initiative itself, which is something Kaplan and Norton warned in. al. er. io. their original paper. They put a lot of emphasis on cascading the BSC through an iterative. n. process that focuses on participation and commitment of all the areas that are going to be. Ch. i Un. v. affected by it. The lack of participation from managers in MTETC BSC initiative is an. engchi. indication that this was not done effectively.. Additionally, something else that in retrospective was missing in the implementation was a strategy map for MTETC. Even though the goal of making MTETC a profit center was clear to all managers interviewed, there was no consensus on how MTETC was planning to achieve this goal. MTETC’s case also shows that measuring performance was difficult without the proper information systems in place. Lastly, MTETC’s case shows what happens when an organization seeks to adopt the management fad of the day without really assessing the needs of the organization. The managers interviewed were evidence that MTETC was suffering from this problem. They simply got tired of trying new management techniques, and this was also true for the BSC, especially when they were excluded in the decision to adopt it in the first place.. 25.

(32) 3.5 More examples of the BSC The BSC is currently one of the most widely used management techniques for measurement and management of enterprise business performance, and it is used by more than70% of the Fortune 500 companies. Additionally, despite its difficulties of implementation, there are numerous examples of implementation worldwide that have proven its effectiveness: •. Mobil Oil (North America) increased its cash flow by $1.2 billion and return on investment increased from 6% to 16% in three years after effectively implementing the BSC. Within 2 years of its implementation, Mobil moved from last place in industry profitability to first place, and it held that place for 5 years before it was. •. 治 政 UPS also increased revenues by 9% and net 大 income by 33% within two years of 立 implementing the BSC.. •. Three years after implementing the BSC, Wells Fargo Bank increased its customer. acquired by Exxon.. ‧ 國. 學. base by 450% and was rated the Best Online Bank. Also, as a result of the BSC. and decreased its costs per customer by 22%. y. Nat. Saatchi and Saatchi, the world famous advertising firm achieved a five-fold increase in. sit. •. ‧. implementation, the company added 750,000 online customers over a 2-year period. er. io. market capitalization to $2.5 billion within 3 years of implementing the BSC and iIt. al. n. iv n C that the BSC helped the company manage human capital and helped transform the heng hi U c agency into being action-oriented and client-focused. was ranked as the #1 creative agency 2 years in a row. The CEO was quoted as saying. •. Siemens IC Mobile increased sales 76% to 9 billion Euros within 1 year of BSC implementation.. Clearly these results are not due solely to the adoption of the BSC. The success of these stories is also associated to the proper systems in place to facilitate its implementation, clear visions and goals, engaged management team and more importantly, the proper implementation of the BSC following the right guidelines and based on what the company really needs. The BSC can be a powerful tool, as some of these examples have shown, but it can also be destined to failure if the inherent difficulties are not identified and overcome, as with the MTETC case. 26.

(33) Despite its limitations and difficulties, the BSC remains a popular management tool in business. Increasingly, the BSC is also being used by non-profit, government and state-owned enterprises to improve performance and achieve strategic alignment and focus. In 1997, Dubai began designing an automated BSC system to monitor the performance of its government departments. The PRC, Thailand, Malaysia and Fiji are also some governments using the BSC to monitor and improve performance. It is also a popular management tool for public sector enterprises in the US, Australia and the United Kingdom. •. The US Postal Service (USPS) first implemented the BSC around 1996. Since then, USPS has increased on time delivery of mail by 20% and productivity by almost 3%. 治 政 大(DFAS) of the US Department of The Defense Accounting and Finance Service 立the first BSC in 2001. Since that year, DFAS has been able to Defense implemented per year, while at the same time increasing employee and customer satisfaction.. 學. ‧ 國. •. increase customer satisfaction by 2% per year, increase employee satisfaction by 14%, cut its federal budget allocation by half, and more importantly, align and clarify its. ‧. mission to its customer, employees and managers.. y. Nat. sit. As stated before, these results are not due solely to the BSC implementation, but they are. al. er. io. evidence that the BSC can be an effective tool to help organizations achieve their strategic. n. goals more easily if implemented correctly.. Ch. engchi. i Un. v. 4. PERSONAL EXPERIENCE WITH THE BSC 4.1 The Case of HSBC Latin America. Design and Implementation HSBC Holdings plc is a global financial services company with headquarters in London, UK. It is currently the sixth largest banking and financial services group and it has around 8,000 offices worldwide in territories across Africa, Asia, Europe, North and Latin America. In 2006, HSBC acquired Grupo Banistmo, a Panamanian banking group that owned Panama’s leading bank, and 106 other branches in Costa Rica, Honduras, Colombia and Nicaragua, as well as 56.2% of the holding company that owned Bancosal, the third largest bank in El Salvador at the time. The next year, HSBC extended two tender offers to acquire the remaining shares in that bank. In 2007, the bank changed its name to HSBC El Salvador. 27.

(34) HSBC El Salvador became part of HSBC Latam (Latin America), and thus, became involved in all the initiatives of this unit. One of those initiatives was the implementation of a Balanced Scorecard to manage performance, and this initiative would include all countries in HSBC Latam. It would be the first time that many units hear of the Balanced Scorecard and many banks didn’t have the necessary systems in place for reporting according to the BSC methodology. All these elements posed a challenge for the project teams. This chapter chronicles some of the main difficulties faced during the implementation of the BSC in El Salvador, the successes and the opportunities for improvements. The first BSC was launched in 2007 with support from Mexico, and the aim was to start using. 政 治 大. the BSC methodology in all local branches as the main input for the employees’ performance evaluation by next year. In retrospective, and after performing extensive research for this. 立. document, it is evident that some of the first steps taken during the implementation could be. ‧ 國. Norton.. 學. improved in order to follow the original design concept of the BSC posed by Kaplan and. ‧. The process suffered from many of the drawbacks that have already been highlighted in the previous chapter, and this made the process even more difficult, considering HSBC Latam. y. Nat. sit. was already dealing with project teams that were miles away and they couldn’t meet face to. al. er. io. face for discussion of the goals and objectives, as suggested by the BSC methodology. The. n. first BSC included the original four perspectives proposed by Kaplan and Norton.. Ch. i Un. v. The team in El Salvador worked closely with HSBC Latam to implement the BSC, but most. engchi. of the work involved defining the way to calculate the indicators, rather than defining a strategy or a strategic linkage model, as suggested by modern best practices. Other difficulties faced by the team were: •. Imposing versus choosing. Just like MTETC’s case, this real life experience showed what happens when a BSC is imposed in an organization without showing first the real need for this management technique. The KPI’s assigned to the bank were indeed consistent with what a generic bank would expect, but at the time it was not clear how those measures aligned with a greater vision and strategy. Thus, the audio-conferences focused more on how to calculate the KPI’s, without actually addressing the issue of “why?”. The teams were motivated, but without a clear destination.. 28.

(35) •. Lack of buy-in of top management. As noticed with the cases in the previous chapter, and effective BSC implementation is not possible without support from top management for the important decisions that this methodology requires. The BSC was initially seen as a system to collect metrics and measure performance, rather than a strategic management tool. Thus, it did not have the impact it intended to. The fact that top management was not the main promoter of this idea also made second and third level managers unaware of the initiative, which made it difficult for the team to sell the idea and benefits of its implementation. This difficult was overcome later during the implementation process.. 治 政 the first BSC’s indicators included measures 大 that were not associated to the HR 立 review. This added to the fact that third and fourth level Department’s performance Not aligned to the bank’s performance review. Again, just like with MTETC’s case,. 學. ‧ 國. •. managers did not see the BSC as something that would reflect their efforts and their department’s performance.. Too many indicators. The original methodology proposed by Kaplan and Norton. ‧. •. suggests 3 or 4 indicators for every perspective, but in this case, the first BSC had. y. Nat. sit. around 48 KPI’s , with most of them focused in the financial perspective. Focusing on. er. io. the financial perspective is not wrong in itself, especially when the BSC was meant for. al. iv n C the KPI’s were redundant, and could have h ethey i Ueasily been simplified by identifying h n c g the key common drivers behind those KPI’s. Nonetheless, the initial 48 indicators n. a bank, but the KPI’s were too many for them to be meaningful. Additionally, some of. remained as part of that BSC version for several months. •. Learning and Growth perspective was misunderstood. The first BSC named this perspective “People Perspective” and focused on KPI’s that ended up becoming sole responsibility of the HR department (average pay, rotation, training, etc), rather than being indicators of the actual growth expectations of the bank.. •. Lack of systems in place to make the BSC implementation effective and easily deployable. The reporting systems and the reports obtained had been effective historically for the bank’s every-day activities, but some of the KPI’s required long calculations and a lot of time to obtain, which made the BSC a cumbersome task in some cases. Additionally, there wasn’t a system in place to communicate the 29.

(36) information from the BSC to all managers in a timely manner, with the results lagging two months when they were presented. This made the BSC even less reliable. •. New concept for everyone. The BSC was a new concept to almost every manager, which is not a problem in itself, since it is the team’s responsibility to explain the methodology. The difficulties arose when explaining the concept and its importance while being affected by all the other problems explained above. Lack of initial support, lack of a clear strategy, lagging indicators, the fact that it had too many indicators, and more importantly, the fact that it wasn’t aligned with the already existing performance review made it difficult to actually “sell” the idea at the business units, which made. 政 治 大. the initial BSC look like a temporary fad that only affected the daily operations due to its complexity.. 立. Constant changes. The BSC went through several revisions, which is a good thing,. 學. ‧ 國. •. considering that iterations and trial and error are all part of the ideal implementation methodology. However, this, when added to all the previous difficulties made it harder. ‧. to establish consensus among managers about what was being measured and why.. sit. y. Nat. al. er. io. These difficulties have already been highlighted in the selected cases in chapter three.. v. n. However, it is interesting to explore them in retrospective and after researching the BSC. Ch. i Un. methodology for this document. Some of them could have been avoided, had the right. engchi. procedure been taken, while others were simply part of the regular “adaptation” process. The implementation had some positive aspects also, some of which were only evident after a second version of the BSC. Other positive aspects were found during the initial implementation as well. •. The BSC became a popular concept with managers. Despite the initial lack of interest, the team made the BSC concept known within the organization through training sessions and meetings with managers. Eventually, it would become part of the bank’s culture and performance management strategy, and managers would already be familiar with the concept, methodology and its goals.. •. Gained support from upper management. This was without a doubt the change that had the biggest influence in the implementation. HSBC headquarters required local 30.

(37) branches to follow a BSC approach to management and set the goals for the region based on this philosophy, which made the heads of each region pay more attention to the BSC. Even if it was still an imposed methodology, and the indicators had already been set for the region, the CEO started getting involved in the process and made sure that the BSC became a priority for second level managers as well. The change in attitude became evident. •. Developed new systems and methodologies. The trial and error experienced during the initial months with the information systems made it evident that new reporting tools were required, and these tools were developed in order to cascade the indicators to the business branches.. 立. 政 治 大. Implementing a BSC is not an easy task, and the case with HSBC El Salvador shows this.. ‧ 國. 學. After all this research, it is interesting to see the stories from the previous chapter and compare it to a real life experience with this tool to identify the successes and the. ‧. opportunities for improvement. Perhaps the most important common denominator found is the importance of having the support of upper management from the beginning to guarantee. y. Nat. sit. effectiveness of the implementation and efficiency while doing so. Most organizations will. al. er. io. not adopt anything new unless upper management wants it to. Furthermore, the BSC is a. v. n. methodology that needs to be “sold” to all the parties involved, and in most cases, this can. Ch. i Un. only be achieved when the BSC is actually associated in some way to a person’s performance.. engchi. This starts with having a clear vision, mission and strategy at the top, and a management team that is engaged with these elements before cascading them throughout an organization. It’s important to remember that the BSC is a management tool, and not a substitute for actual management practices.. 31.

數據

相關文件

Effectiveness of robot-assisted upper limb training on spasticity, function and muscle activity in chronic stroke patients treated with botulinum toxin: A randomized single-

Predicting Successful Employment in the Community for People with a History of Chronic Mental Illness.Occupational Therapy Mental Health,6,31-49. Predictors of employment outcome

With the proposed model equations, accurate results can be obtained on a mapped grid using a standard method, such as the high-resolution wave- propagation algorithm for a

We have presented a numerical model for multiphase com- pressible flows involving the liquid and vapor phases of one species and one or more inert gaseous phases, extending the

Keywords: Adaptive Lasso; Cross-validation; Curse of dimensionality; Multi-stage adaptive Lasso; Naive bootstrap; Oracle properties; Single-index; Pseudo least integrated

This study represents the concept of balanced scorecard (BSC) with four perspectives (financial, customer, internal business processes, and learning and growth) to build the

A., and Revang, O., “A Strategic Framework for Analying Professional Service Firms — Developing Strategies for Sustained Performance”, Strategic Management Society

This research proposes a Model Used for the Generation of Innovative Construction Alternatives (MUGICA) for innovation of construction technologies, which contains two models: