SME LOAN DECISION MAKING PROCESS: A DECLINING ROLE OF

HUMAN CAPITAL

Ottavia, Shao-Chi, Chang Ph.D., Ding-Bang, Luh Ph.D. National Cheng Kung University

Institute of Creative Industry Design 1 University Road, Tainan 70101 Taiwan

This study is intended to draw the relationships among borrower’s attributes, lender’s human capital in SME loan granting process. Conjoint analysis has been used as the main analytical tool. The results showed that: 1) borrower’s attributes are all positively related to the likelihood of loan approval in different levels; 2) officers put different weights over borrower’s attributes; 3) human capital has lost its significant role in SME loan granting process with the existence of a new credit scoring system.

Keywords: SME Loan Granting, Conjoint Analysis, Lender’s Human Capital, Borrower’s Attributes, Likelihood of Loan Approval.

1.0 INTRODUCTION

In banking industry, loan department have been the biggest contributor to banks’ income. The income, in form of loan interest and provision, has taken a significant amount of percentage in the banks’ asset (Golin, 2001). Therefore, loan quality is an important criterion in establishing the creditworthiness of a bank (Golin, 2001). It is a guarantee to ensure that the loans released will continue to ‘work’ to generate profit for the bank (Booth & Booth, 2006; Rosman & Bedard, 1999).

A lot of aspects have to be put into consideration before a bank decides to invest into companies in a form of loan. For any single bad loan, bank will suffer not only financial loss, but also significant damage in its reputation (Coleshaw, 1989). That is why before any loan decision is made; applications must undergo a long analysis procedure to screen bad loans from the beginning. In this decision making process, bank officers will take into account a lot of different kind of attributes related to the borrower’s background and experience, the business and conditions surrounding it (Bruns, Holland, Shepherd, & Wiklund, 2008).

The loan decision making process itself is also affected by factors within the bank (Forbes, 2005). One of them is human capital (Dimov & Shepherd, 2005; Kochetkova, 2006); partly because human judgment plays important portion in loan decision (Coleshaw, 1989). An interesting study held recently in Sweden, which involved 114 loan officers from various banks, gave a slight illustration that loan officers’ human capital influences loan decision (Bruns et al., 2008).

Up to this moment, there are not many studies which can give clear explanations on the relationship between borrower’s attributes, lender’s human capital, and the likelihood of loan approval. This study is exploring the relationship of borrower’s attributes and the likelihood of loan approval; and how human capital factors of loan officers affect the judgment. The

loan approval is not only a matter of technical issue, but it also strongly reflects the subjective factors of loan officers who make judgment on loan applications. Since loan officers play the decisive role in loan approval, it is a vital issue to know how they carry out decision making procedure in banking. In this procedure, mutual interplay among borrower’s attributes and lender’s human capital determines the likelihood of loan approval. By understanding the interactions, it will help to improve the common practice of loan granting in banks.

2.0 LITERATURE BACKGROUND 2.1 Loan Approval: 5Cs

Loans are given based on the belief that the borrower can be trusted to repay the debt (Golin, 2001). In banking industry, loan evaluation procedure is standardized for the sake of systematic evaluation. The most common practice is Five Cs, which accommodate all factors mentioned above.

The first C is Character. It is related to reputation and apparent quality, which are determined by face-to-face meeting with borrowers, information from others (Golin, 2001). Character represents management’s integrity, stability, and overall willingness to repay the loan (Riding, Haines, & Thomas, 1994; Saunders & Allen, 2002). The next C stands for Capacity. It is related to analysis over borrower’s financial condition, financial statements, and future prospects. Capacity emphasizes on firm’s ability, in term of financial status and management experience (Riding et al., 1994).

Capital, or equity, corresponds to owner’s residual claims to a firm’s assets (Golin, 2001), the amount of owner’s money contributed to the business (Barrett, 1990), the proportion of loan borrowed to support the firm’s operation (Coleshaw, 1989), and the fund available to operate the firm (Riding et al., 1994). Capital can be a measurement of firm’s survival prospects. Collateral is any form of assets pledged by the firm in exchange of loan from the bank. It can also be in a form of guarantee from a third party. Loan risk can be mitigated through the pledge of collateral (Golin, 2001). In the worst condition, if the loan goes default, collateral will be the alternative source of repayment for bank to liquidate (Riding et al., 1994).

The last C is Condition. Condition relates to both macro and micro economics conditions surrounding the firm’s business operation. All environmental conditions which can affect the ability of the borrower to repay the debt can be categorized into this area (Riding et al., 1994).

All loan applications received by banks will undergo the comprehensive and careful analyses using Five Cs as the principle of loan decision-making (Riding et al., 1994). This Five Cs principle provides the framework of loan evaluation for loan officers. It is expected for loan officers to have the same perspective and finally reach the same conclusion over loan applications using this principle (Bruns et al., 2008). To eliminate the biases caused by different sizes of loans, for this study, the loan will be limited only to SME loans.

2.2 Borrower’s Attributes

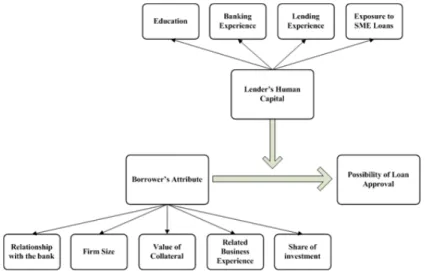

Since there are too many borrower’s attributes to be considered in loan decision process, the study is going to focus only on five elements; which are relationship with the bank, firm size, value of collateral, related business experience, and share of investment. In this study, these factors will represent 5Cs.

2.2.1 Relationship with the Bank.

Bank can get more information through relationship; both lending and other bank services; such as deposit accounts, treasury, and daily transactions (Allen, Saunders, & Udell, 1991). These other forms of bank relationships can be used as reference for future credit relation and creditworthiness (Berger & Udell, 1995; Elyasiani & Goldberg, 2004). According to Rajan (1992), banks that hold more information about the borrower will have more control over credit disbursement only to profitable projects. By doing this, it will push the borrower to put more effort (Rajan, 1992). On the other hand, the more information banks have, the more accurate the analysis would be; resulting in higher risk mitigation (Rajan, 1992).

A more comprehensive study by Bharath, Dahiya, Saunders, and Srinivasan (2007) shows the benefit of building relationship with customers. Relationship banks will have higher probability of securing future loan contract (42%) than non-relationship banks (3%) (Bharath et al., 2007).

Therefore, it can be concluded that a stronger relationship with the bank will lower loan officers’ screening level, resulting the increment of bank’s willingness to take more risks (Jiménez & Saurina, 2004; La Porta, Lopez-De-Silanes, & Zamarripa, 2003). Therefore, the following hypothesis is proposed:

Hypothesis 1: Relationship with the bank positively affect the likelihood of loan approval. 2.2.2 Value of Collateral.

A study by Menkhoff, Neuberger, and Suwanaporn (2006) on 560 credit data set in Thai commercial banks show that Thai banks use collateral to reduce credit risks. By having collateral mortgaged to the bank, it will push the borrowers to place more effort because they have their asset ‘in hostage’. It will also reduce the moral hazard when banks lend money (Jiménez & Saurina, 2004).

Banks will expect higher collateral from borrowers who have higher default risks. By having collateral as the safety net, it may change the willingness of banks to take risks. According to Jiménez and Saurina (2004), collateral reduces bank’s risk exposure, provides incentive to be less careful and take more risks.

Collateral can also be seen as an instrument to ensure good behavior from borrowers’ side (La Porta et al., 2003). Borrowers are obliged to perform in a certain level that complies with bank’s regulation, or otherwise there is a risk that they will lose the asset once the loans fail to perform. A recent case study done in Portugal by Dermine and de Carvalho (2006) also supported this argument. The study employed 10,000 short-term SME loans disbursed during the period of June 1995–December 2000 in Banco Comercial Português (the largest private bank in Portugal). It has found a significant positive relationship between collateral and loan default recovery (Dermine & de Carvalho, 2006).

So it can be concluded that the more valuable the collateral pledged to cover the loan, the more pressure for borrowers to perform according to the bank’s requirement. Consequently, it will reduce possible moral hazard and risk for the bank. Therefore, the following hypothesis is proposed:

2.2.3 Firm Size.

Firm size is related to business scale and business scope. Both represent the organizational capital which offers survival benefits (Bercovitz & Mitchell, 2007). A study by Mitchell (1994) proved that larger firms and businesses tend to survive longer in the business than smaller companies. Size, which is related to sales levels, affects directly to profitability, which therefore affects the sustainability of the business (Bercovitz & Mitchell, 2007; Silverman, Nickerson, & Freeman, 1997).

In practice, banks give different treatment based on the size of the firms. Smaller companies face relatively more difficulties to acquire loan compared to their larger counterparts (Harhoff & Körting, 1998). There is higher likelihood for smaller companies to be rejected when they are applying for loan.

Therefore, it can be concluded that larger firm will have higher sustainability and will be more likely to survive in the business, resulting in lower risk for the bank. In addition to that, they will also have higher bargaining power. Therefore it is easier for them to get loan approval.

Hypothesis 3: Firm size positively affects the likelihood of loan approval. 2.2.3 Related Business Experience.

Knowledge is cumulative (Arthur, 1989). From these accumulated knowledge and experience, entrepreneurs gain a self-reinforcing capacity (Minniti & Bygrave 1999. 2000). These industry-specific know-how contributed to both business survival and growth (Cooper, Gimeno-Gascon, & Woo, 1994).

Entrepreneurs also base their decisions on specific knowledge about the market (related to technical aspects, products, or industry) and general knowledge about business (how to be entrepreneurial). Both of them are accumulated through experience, learning-by-doing or direct observation (Minniti & Bygrave, 2001). Either way, it will increase their capabilities and form routines. These routines of problem solving are patterns constructed of accumulated successful solutions to particular problem happened in the past (Nelson & Winter, 1982). In the case of default loan, the more experience gained in line with the increasing age of the firm, the higher the probability for the firm to recover from default (Dermine & de Carvalho, 2006). A more experienced firm will be able to revive from default status. Therefore, with the skills obtained over time, firms will have a greater chance to achieve success in business and sustain in the business. Thus, when they apply for loan to the bank, it will create a more favorable condition for the bank. Therefore, this following hypothesis is proposed:

Hypothesis 4: Related business experience positively affects the likelihood of loan approval. 2.2.5 Share of Investment.

Share of investment relates to how much capital is invested by the owner for the operation of the firm. Financial capital is an important source to support business against random shocks and make it possible to make more strategies. And it also contributes to both business survival and growth (Cooper et al., 1994). The more capital injected to the firms, the more

sustainable they are to face all the challenges in the business and the higher possibility for the firms to grow.

Financial capital has high influence on firm’s survival (Bates, 1990). Insufficient financial resources leads to business failure (Chandler & Hanks, 1998). Owner’s share of investment is one of the big considerations in loan assessment because it will affect ratio analyses which is the base loan decisions (Vaughn, 1997). If the owner invests more capital into the firms’ operation, it will share more business risk with the lender, leaving banks with relatively lower risk.

Hypothesis 5: Share of investment positively affects the likelihood of loan approval. 2.3 Lender’s Human Capital

Previous studies have shown that human capital can affect decision. There have been studies in various fields which pointed out differences of decisions taken by the experienced and inexperienced, from chess players to auditors (Chase & Simon, 1973; Choo & Trotman, 1991). The same goes to new ventures (Chandler & Hanks, 1998) and multinational enterprises (Carpenter, Sanders, & Gregersen, 2001). A study by Dimov and Shepherd (2005) found that there is a positive relationship between venture capitalists’ human capital and the performance of portfolio firms.

If applied in banks’ loan department setting, loan officers with a higher level of human capital would provide better performance to the bank by giving more accurate analysis on the repayment intention and capacity of potential borrowers for the banks’ interest (Dimov & Shepherd, 2005). Loan officers with higher level of human capital will be more likely to use different kinds approach and effective ways to better define the risks of applicants in the decision process. They will have the knowledge, experience, and skill needed to give more accurate assessment of the business risk; and at the same time take into account all aspects of the customers; collateral, capacity, character, capital, and conditions (Bruns et al., 2008). Even though a lot of attempts have been tried to make the loan decision-making process uniform across loan officers, the human capital factors which are carried by each loan officer have retained their influential stand to the decision making process; causing decisions over loan applications varied depending on loan officers’ experience and knowledge (Andersson, 2001). Different knowledge, familiarity, and self-efficacy related to different levels of human capital will influence the perception of risk, give different judgment, and affect the determination of successful loan project completion through the bank’s loan application processing tools (Bruns et al., 2008). Therefore, the next hypotheses are proposed to measure how human capital can affect the loan decision making process.

Hypothesis 6: Loan officer’s human capital affects the likelihood of loan approval.

In order to operationalize loan officers’ human capital, this study has adapted four human capital factors which have been used in previous study by Bruns, et al. (2008).

2.3.1 Education

Education is broad-based skills that can be applied to a variety of responsibilities and is generally used as a benchmark for general human capital (Gimeno, Folta, Cooper, & Woo, 1997). Loan officers with higher level of education are considered to have a broader

knowledge, information processing, and problem-solving skill to make a more effective and faster decision; and also higher learning capacity (Cohen & Cohen, 1983; Forbes, 2005). 2.3.2 Banking Experience

Banking experience will increase general human capital and provide an opportunity to develop more specific knowledge and skills specific to the banking industry than education (Bruns et al., 2008). Bank training and experience gained related to banking will increase the specific human capital (Gimeno et al., 1997). Even it is not considered as formal training, on-the-job training in bank will give better understanding of products, processes, and services available in the bank. Formal training in class, on-the-job training, discovery, and experience build the tacit knowledge of bankers on how to perform the assigned job more effectively (Berman, Down, & Hill, 2002).

2.3.3 Lending Experience

Lending experience is defined as specific human capital which can be measured by the expertise gained from experiences related to lending activities (Bruns et al., 2008). Loan officers’ expertise and subjective judgment are the key factors in loan decision making (Saunders & Allen, 2002). Along with lending experience obtained, self efficacy will be higher (Wood & Bandura, 1989). In other words, experts are typically efficient in their decision making by focusing on the significant attributes which affect outcomes of decisions the most (Chase & Simon, 1973; Choo & Trotman, 1991). Loan officers with higher lending experience will have higher self-efficacy, different viewpoints, and solutions over loan applications compared to those with less experience (Gavetti & Levinthal, 2000).

2.3.4 Recent Exposure to SME Loans

Recent exposure to SME loans will give more specific tacit knowledge related to small business loans (Bruns et al., 2008). Loan officers can draw on personal experience from similar SME loans proceeded in the past (Inderst & Mueller, 2008). Frequent exposure to SME will thus increase familiarity and thus reduce the risk perception (Lipshitz & Strauss, 1997). Another study by Hitt, Bierman, Shimizu, and Kochhar (2001) on service firms showed that human capital has both direct and moderating effects on the firm performance. 3.0 METHODOLOGY

The study was conducted using metric conjoint experiment which collects first-hand information from respondents. Respondents were given series of pre-specified scenarios with different combinations of five attributes (2 levels, High & Low) to evaluate and approve (Hair, Anderson, Tatham, & Black, 1998). Since employing full scenarios of 25 will

overburden the respondents, fractional factorial design was used, producing a minimum 8 scenarios with 2 hold-out cases.

Conjoint analysis is suitable for analyzing decision making process (Hair et al., 1998); the result will show how each borrower’s attribute’s influence in loan decision process. This research method has been used in many different studies in other fields (Green & Srinivasan, 1978; Green & Wind, 1975; Greening & Turban, 2000). The benefit of conjoint analysis is the placement of the least demand to respondents (Hair et al., 1998). They will be asked for only one response for each scenario given.

Figure 1. Conceptual Model

In total there were 10 scenarios of hypothetical companies which apply for SME loan in the questionnaire. All respondents were loan officers in Indonesian banks. In order to eliminate misinterpretation, all questionnaire items were translated into Indonesian. In total, 350 questionnaires were distributed to officers who were visited by the researcher in person in their branches. From 350 sets, 255 were directly collected on the spot, 36 were sent later by email, and 59 were not returned. In total 291 sets were successfully collected.

4.0 RESULTS

In total there were 291 responses collected from 18 offices. The demography of the respondents is illustrated in Table 1.

Table 1

Result of Descriptive Analysis

No .

Category N % No

.

Category N %

1. Age 5. Bank Experience

1. 20 – 30 74 25.40 1. < 5 years 91 31.30 2. 31 – 40 176 60.50 2. 6 - 10 years 65 22.30 3. 41 – 50 41 14.10 3. 11 - 15 years 104 35.70

2. Gender 4. > 15 years 31 10.70

1. Male 138 47.40 6. Credit Experience

2. Female 153 52.60 1. < 5 years 90 30.90

3. Department 2. 6 - 10 years 65 22.30

1. Risk 103 35.40 3. 11 - 15 years 81 27.80 2. Marketing 188 64.60 4. > 15 years 55 18.90

4. Education 7. SME Experience

1. Up to college 70 24.10 0. None 44 15.10 2. Bachelor 162 55.70 1. 1 – 10 50 17.20 3. Master degree + 59 20.30 2. 11 – 20 46 15.80 3. 21 – 30 76 26.10 4. > 30 75 25.80

Conjoint analysis was then applied to check the relationships between borrower’s attributes to the likelihood of loan approval. The results in Table 2 show that there are positive correlations between the attributes to loan approval. In other words, the higher the value of each attributes, it is more likely for the loan to be approved. Therefore, hypotheses 1 to 5 are proven.

Table 2

Result of Conjoint Analysis

No. Item Code Utility

1 Relationship with the bank Rel Low -0.403 Rel High 0.403 2 Value of collateral Col Low -0.616

Col High 0.616

3 Firm size Size Low -0.140

Size High 0.140 4 Related business experience Exp Low -0.729

Exp High 0.729 5 Share of investment Share Low -0.346

Share High 0.346

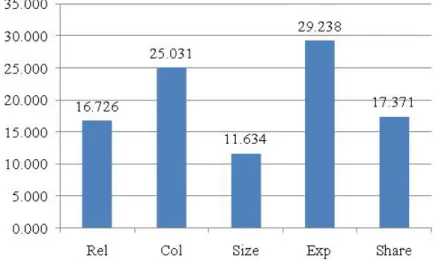

Figure 1. The Value of Importance among Borrower’s Attributes

The result above was found significant because Pearson’s R and Kendall’s tau are both significant, with Pvalue = .000 and .001 respectively. Based on the importance value, it can be concluded that loan officers have their assessment priority in loan decision process. Among these five attributes, the ranks are as follow: 1) Related business experience; 2) Value of collateral; 3) Share of investment; 4) Relationship with the bank; 5) Firm size.

Table 4

Difference of Responses based on Human Capital Factors

Human Capital Factors+

Relationship with the bank

Value of Collateral Firm Size Related Business

Experience

Share of Investment

Low High Fvalue Low High Fvalue Low High Fvalue Low High Fvalue Low High Fvalue

Mean Mean Mean Mean Mean Mean Mean Mean Mean Mean

General Education Up to college/ academy -0.402 0.402 0.529 -0.666 0.666 0.954 -0.173 0.173 0.560 -0.802 0.802 1.657 -0.423 0.423 4.073** Bachelor degree -0.418 0.418 -0.585 0.585 -0.120 0.120 -0.701 0.701 -0.375 0.375 Master degree and more -0.364 0.364 -0.644 0.644 -0.153 0.153 -0.720 0.720 -0.174 0.174 Banking Experience

less than 5 years -0.431 0.431 0.571 -0.552 0.552 2.045 -0.074 0.074 1.458 -0.684 0.684 2.461 -0.431 0.431 1.202 6 - 10 years -0.415 0.415 -0.723 0.723 -0.173 0.173 -0.673 0.673 -0.281 0.281 11 - 15 years -0.388 0.388 -0.595 0.595 -0.172 0.172 -0.811 0.811 -0.316 0.316 16 years and more -0.347 0.347 -0.653 0.653 -0.153 0.153 -0.702 0.702 -0.331 0.331 Lending experience

less than 5 years -0.457 0.457 1.321 -0.568 0.568 0.908 -0.054 0.054 2.633* -0.693 0.693 1.107 -0.576 0.576 14.473*** 6 - 10 years -0.406 0.406 -0.640 0.640 -0.206 0.206 -0.717 0.717 -0.375 0.375

11 - 15 years -0.378 0.378 -0.671 0.671 -0.168 0.168 -0.795 0.795 -0.289 0.289 16 years and

more

Table 4 (continued)

Human Capital Factors+

Relationship with the bank

Value of Collateral Firm Size Related Business

Experience

Share of Investment

Low High Fvalue Low High Fvalue Low High Fvalue Low High Fvalue Low High Fvalue

Mean Mean Mean Mean Mean Mean Mean Mean Mean Mean

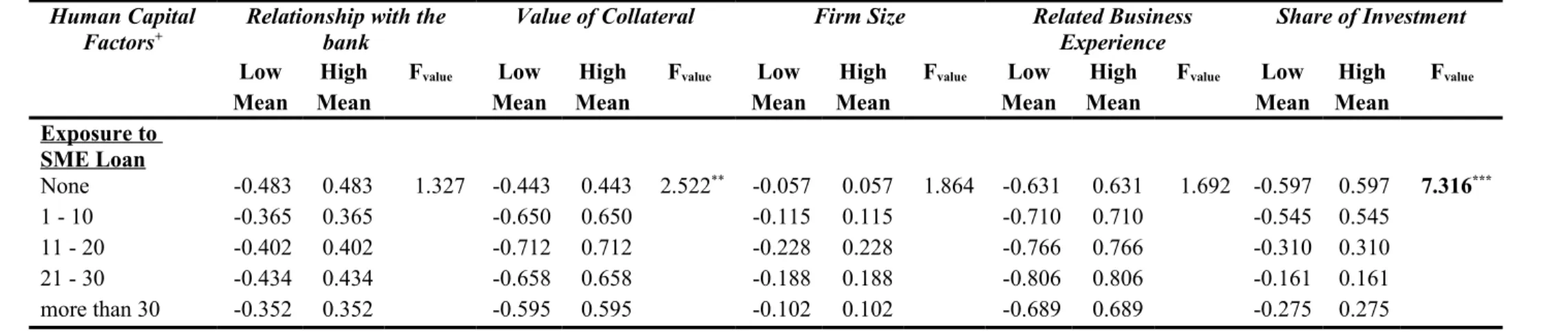

Exposure to SME Loan None -0.483 0.483 1.327 -0.443 0.443 2.522** -0.057 0.057 1.864 -0.631 0.631 1.692 -0.597 0.597 7.316*** 1 - 10 -0.365 0.365 -0.650 0.650 -0.115 0.115 -0.710 0.710 -0.545 0.545 11 - 20 -0.402 0.402 -0.712 0.712 -0.228 0.228 -0.766 0.766 -0.310 0.310 21 - 30 -0.434 0.434 -0.658 0.658 -0.188 0.188 -0.806 0.806 -0.161 0.161 more than 30 -0.352 0.352 -0.595 0.595 -0.102 0.102 -0.689 0.689 -0.275 0.275

Note: * for Pvalue ≤ 0.1

** for Pvalue between 0.05 and 0.01 *** for Pvalue ≤ 0.001

The influence of all human capital factors only exist in the judgment over share of investment, except for banking experience. Since banking experience represent the length of employment in the banking industry, not necessarily in credit setting; the result was found insignificant.

As for the other human capital factors, it was found that loan officers with different education background weighed share of investment differently. The higher the general education level, the less they think that share of investment is important in loan assessment. This can be seen from the decreasing mean value that is followed with the increment in education level. Overall, the Fvalue is 4.073** which is moderately significant.

The same tendency was also found when the more specific human capital factors were analyzed. Lending experience has a highly significant Fvalue of 14.473***. The mean value has

a descending trend as the lending experience increases. More lending experience was proved to lessen the influence of share of investment in the loan decision making process. As for exposure to SME loan, the Fvalue is 14.473*** and highly significant. The decreasing trend in

mean value shows that as loan officers are more exposed to SME loans, they value put less importance in share of investment. Ownership is not considered as a much of a vital issue in loan granting process as the level of exposure increases.

So it can be concluded that among all attributes, only judgment over share of investment is affected by the human capital factors. Therefore, hypothesis 6 is only partially proven, specifically to share of investment attribute in general education, lending experience, and exposure to SME loan context.

5. CONCLUSIONS

5.1 Discussions and Implications

Overall results show that borrower’s attributes have a positive relationship toward the likelihood of loan approval in different degrees. This research found that the most influential attribute among the five is related business experience (importance value of 29.238%), followed by value of collateral factor with only a slight difference (importance value of 25.031%). Share of investment and relationship with the bank was found moderately influential in the loan assessment process (importance value are 17.371% and 16.726% respectively). The factor found was least important is firm size. From the interviews, loan officers indicated this factor as secondary in decision making process. They were more concerned on how much profitable the business is and whether it has enough capital to repay the obligation (bank interest) and keep the business going. These findings have to be reevaluated, whether they are in line with the bank’s initial criteria in credit analysis. If it is found contradicting with the rules, regulations, and the risk weighting in credit scoring system; then more credit trainings and standard regulation socializing need to be done in order to correct the mistake. If it complies with the standard credit rules as intended by the bank, then more analytical tools have to be made to support the credit analysis process. Human capital factors were proven to be less influential toward the judgment of borrower’s attributes in SME loan decision making process. This might be caused by the more standardized rules applied in the new credit scoring system compared to the expert system which relies heavily on loan officer’s judgment. Since what are measured and the weights of each item are clear, this more rigid system produces more standardized decisions in SME applications, leaving only a small room for subjective judgment. Regardless the education

level or experience level of loan officers, using this system, all decisions will be more uniform. Therefore, the existence of a standard credit system could replace the employees’ human capital; the company can replace employees with high level of human capital with a lower one in a novice level. Those highly educated and experienced staffs can then be transferred to commercial or corporate credit department where their valuable human capitals can be utilized in a more optimal level.

5.2 Research Limitations and Suggestions

Even though the experiment has been carefully designed to illustrate credit cases generally processed by loan officers, the credit schemes could not fully represent loan applications in the actual settings. Respondents were also “forced” to plainly accept and make decisions based on the simplified and limited information presented in the loan scenarios. In the real practice, loan officers have access to more information and can make a more interactive communication with their clients when making a due-diligence assessment. They can obtain, clarify, and ask more questions from the clients and other sources.

There was also possibility of Hawthorne effect, the occasion where individuals’ behaviors alter when they are aware that their responses are being studied (Robbins & Judge, 2007). Loan officers might put importance and weighing on certain factors only in the experiment setting but will do otherwise in the real loan assessment process.

Future study might consider employing more factors and conducting it in a larger scale, across countries. It will be interesting to study whether these attributes keep its importance in other working capital loan with bigger and more significant amount; commercial or corporate credit. Future studies can be aimed to discover whether there are differences among these three types of business loan. Comparative study can also be made between working capital loan and consumption loan (housing loan, car loan, and credit card).

REFERENCES

Allen, L., Saunders, A., & Udell, G. F. (1991). The pricing of retail deposits: Concentration and information. Journal of Financial Intermediation, 1(4), 335-361.

Andersson, P. (2001). Expertise in credit granting: Studies on judgment and decision-making

behavior. Stockholm School of Economics, Stockholm.

Arthur, W. B. (1989). Competing technologies, increasing returns, and lock-in by historical events. The Economic Journal, 99, 31.

Barrett, G. R. (1990). What bankers want to know before granting a small business loan.

Journal of Accountancy, 169(4), 47-54.

Bates, T. (1990). Entrepreneur human capital inputs and small business longevity. Review of

Bercovitz, J., & Mitchell, W. (2007). When is more better? The impact of business scale and scope on long-term business survival, while controlling for profitability. Strategic

Management Journal, 28, 61-79.

Berger, A. N., & Udell, G. F. (1995). Relationship lending and lines of credit in small firm finance. Journal of Business, 68, 351.

Berman, S. L., Down, J., & Hill, C. W. L. (2002). Tacit knowledge as a source of competitive advantage in the National Basketball Association. Academy of Management Journal, 45, 13-31.

Bharath, S., Dahiya, S., Saunders, A., & Srinivasan, A. (2007). So what do I get? The bank's view of lending relationships. Journal of Financial Economics, 85, 368-419.

Booth, J. R., & Booth, L. C. (2006). Loan collateral decisions and corporate borrowing costs.

Journal of Money, Credit & Banking, 38, 67-90.

Bruns, V., Holland, D. V., Shepherd, D. A., & Wiklund, J. (2008). The role of human capital in loan officers decision policies. Entrepreneurship Theory and Practice, 23.

Carpenter, M. A., Sanders, W. G., & Gregersen, H. B. (2001). Bundling human capital with organization context: The impact of international assignment experience on multinational firm performance and CEO pay. Academy of Management Journal, 44, 493-511.

Chandler, G. N., & Hanks, S. H. (1998). An examination of the substitutability of founders human and financial capital in emerging business ventures. Journal of Business

Venturing, 13(5), 353-369.

Chase, W. G., & Simon, H. A. (1973). Perception in chess. Cognitive Psychology, 4(1), 55-81.

Choo, F., & Trotman, K. T. (1991). The relationship between knowledge structure and judgments for experienced and inexperienced. Accounting Review, 66(3), 464.

Cohen, J., & Cohen, P. (1983). Applied multiple regression/correlation analysis for the

behavioral sciences. Hillsdale, NJ: Lawrence Erlbaum Associates.

Coleshaw, J. (1989). Credit analysis: How to measure and manage credit risk. Cambridge: Woodhead-Faulkner Limited.

Cooper, A. C., Gimeno-Gascon, F. J., & Woo, C. Y. (1994). Initial human and financial capital as predictors of new venture performance. Journal of Business Venturing, 9(5), 371-395.

Dermine, J., & de Carvalho, C. N. (2006). Bank loan losses-given-default: A case study.

Journal of Banking & Finance, 30(4), 1219-1243.

Dimov, D. P., & Shepherd, D. A. (2005). Human capital theory and venture capital firms: Exploring "home runs" and "strike outs". Journal of Business Venturing, 20(1), 1-21.

Elyasiani, E., & Goldberg, L. G. (2004). Relationship lending: a survey of the literature.

Journal of Economics and Business, 56(4), 315-330.

Forbes, D. P. (2005). Managerial determinants of decision speed in new ventures. Strategic

Management Journal, 26, 355-366.

Gavetti, G., & Levinthal, D. (2000). Looking forward and looking Backward: Cognitive and experiential search. Administrative Science Quarterly, 45, 113-137.

Gimeno, J., Folta, T. B., Cooper, A. C., & Woo, C. Y. (1997). Survival of the fittest? Entrepreneurial human capital and the persistence of underperforming firms.

Administrative Science Quarterly, 42, 750-783.

Golin, J. L. (2001). The bank credit analysis handbook: a guide for analysts, bankers and

investors. Singapore: John Wiley & Sons (Asia) Pte Ltd.

Green, P. E., & Srinivasan, V. (1978). Conjoint analysis in consumer research. Journal of

Consumer Research, 5(2), 103-123.

Green, P. E., & Wind, Y. (1975). New way to measure consumers' judgments. Harvard

Business Review, 107-117.

Greening, D. W., & Turban, D. B. (2000). Corporate social performance as a competitive advantage in attracting a quality workforce. Business and Society, 39(3), 254-280. Hair, J. F., Anderson, R. E., Tatham, R. L., & Black, W. C. (1998). Multivariate data

analysis (5th ed.): Prentice Hall.

Harhoff, D., & Körting, T. (1998). Lending relationships in Germany – Empirical evidence from survey data. Journal of Banking & Finance, 10-11, 22.

Hitt, M. A., Biermant, L., Shimizu, K., & Kochhar, R. (2001). Direct and moderating effects of human capital on strategy and performance in professional service firms: A resource-based perspective. Academy of Management Journal, 44, 13-28.

Inderst, R., & Mueller, H. M. (2008). Bank capital structure and credit decisions. Journal of

Financial Intermediation, 17, 20.

Jiménez, G., & Saurina, J. (2004). Collateral, type of lender and relationship banking as determinants of credit risk. Journal of Banking & Finance, 28(9), 2191-2212.

Kochetkova, A. (2006). The formation of human capital: The systemic conceptual approach).

Russian Education & Society, 48(2), 5-16.

La Porta, R., Lopez-De-Silanes, F., & Zamarripa, G. (2003). Related lending. Quarterly

Journal of Economics, 118, 231.

Lipshitz, R., & Strauss, O. (1997). Coping with uncertainty: A naturalistic decision-making analysis. Organizational Behavior and Human Decision Processes, 69(2), 149-163. Menkhoff, L., Neuberger, D., & Suwanaporn, C. (2006). Collateral-based lending in

Minniti, M., & Bygrave, W. (2001). A dynamic model of entrepreneurial learning.

Entrepreneurship: Theory & Practice, 25, 5.

Mitchell, W. (1994). The dynamics of evolving markets: The effects of business sales and age on dissolutions and divestitures. Administrative Science Quarterly, 39, 575-602. Nelson, R., & Winter, S. (1982). An evolutionary of economic change. Cambridge, MA:

Harvard University Press.

Rajan, R. G. (1992). Insiders and outsiders: The choice between informed and arm's-length debt. Journal of Finance, 47, 1367-1400.

Riding, A., Haines, G. H., & Thomas, R. (1994). The Canadian small business-bank interface: A recursive model. Entrepreneurship: Theory & Practice, 18(4), 5-24.

Robbins, S. P., & Judge, T. A. (2007). Organizational behavior (12th ed.): Prentice-Hall. Rosman, A. J., & Bedard, J. C. (1999). Lenders' decision strategies and loan structure

decisions. Journal of Business Research 1, 12.

Saunders, A., & Allen, L. (2002). Credit risk measurement. New York: Wiley.

Silverman, B. S., Nickerson, J. A., & Freeman, J. (1997). Profitability, transactional alignment, and organizational mortality in the U.S. trucking industry. Strategic

Management Journal, 18, 31-52.

Vaughn, D. E. (1997). Financial planning for the entrepreneur. New Jersey: Prentice Hall, Upper Saddle River.

Wood, R., & Bandura, A. (1989). Social cognitive theory of organizational management.