行政院國家科學委員會專題研究計畫 成果報告

匯率不確定性與海外直接投資時機之選擇: 實質選擇權賽

局理論之應用與台灣廠商之實證

研究成果報告(精簡版)

計 畫 類 別 : 個別型 計 畫 編 號 : NSC 99-2410-H-004-047- 執 行 期 間 : 99 年 08 月 01 日至 100 年 07 月 31 日 執 行 單 位 : 國立政治大學國際貿易學系 計 畫 主 持 人 : 陳坤銘 報 告 附 件 : 出席國際會議研究心得報告及發表論文 公 開 資 訊 : 本計畫可公開查詢中 華 民 國 100 年 11 月 01 日

中文摘要: 本研究應用實質選擇權賽局理論探討匯率不確定性與海外直接 投資時機之關係。本研究理論分析顯示,在面臨匯率不確定情 況下,若國外市場愈競爭,市場導向型廠商愈可能延遲進入該 市場。相反的,對依成本導向型廠商而言,若其本國市場愈競 爭,該廠商愈可能提早將生產活動移往低工資國家。本研究利 用台商至中國大陸投資的調查資料進行實證研究,以檢驗本文 理論架構之解釋能力。本研究採用事件歷史分析法(event history analysis)。本研究實證結果大致支持本研究之理論預 期。

英文摘要: This study applies a real option game approach to examine the relationship between exchange rate uncertainty and the timing of foreign direct investment. In the theoretical part, we show that a more competitive foreign market will deter a market-seeking firm to enter the market earlier if it faces exchange rate uncertainty. In contrast, a more competitive home market will induce a cost-oriented firm to shift its production to a low-wage foreign country earlier. In the empirical part, a recent survey dataset for Taiwanese firms’ investment into China is employed to check the validity of our theoretic framework. With event history modeling, our empirical results are generally consistent with our theoretical prediction.

行政院國家科學委員會補助專題研究計畫

成果報告

□期中進度報告

(計畫名稱)匯率不確定性與海外直接投資時機之選擇: 實質選擇

權賽局理論之應用與台灣廠商之實證

計畫類別:個別型計畫 □整合型計畫

計畫編號:NSC 99-2410-H-004-047

-

執行期間: 99 年 08 月 01 日至 100 年 07 月 31 日

執行機構及系所:國立政治大學國際經營與貿易學系

計畫主持人:陳坤銘

共同主持人:林家慶、溫偉任

計畫參與人員:黃士真

成果報告類型(依經費核定清單規定繳交):精簡報告 □完整報告

本計畫除繳交成果報告外,另須繳交以下出國心得報告:

□赴國外出差或研習心得報告

□赴大陸地區出差或研習心得報告

出席國際學術會議心得報告

□國際合作研究計畫國外研究報告

處理方式:

除列管計畫及下列情形者外,得立即公開查詢

□涉及專利或其他智慧財產權,□一年□二年後可公開查詢

中 華 民 國 100 年 10 月 31 日

摘要

本研究應用實質選擇權賽局理論探討匯率不確定性與海外直接投資時機之關係。本研究 理論分析顯示,在面臨匯率不確定情況下,若國外市場愈競爭,市場導向型廠商愈可能延遲 進入該市場。相反的,對依成本導向型廠商而言,若其本國市場愈競爭,該廠商愈可能提早 將生產活動移往低工資國家。本研究利用台商至中國大陸投資的調查資料進行實證研究,以 檢驗本文理論架構之解釋能力。本研究採用事件歷史分析法(event history analysis)。本研究實 證結果大致支持本研究之理論預期。

關鍵詞: 匯率不確定性,海外直接投資,實質選擇權,賽局理論,事件歷史分 析研究法

Abstract

This study applies a real option game approach to examine the relationship between exchange rate uncertainty and the timing of foreign direct investment. In the theoretical part, we show that a more competitive foreign market will deter a market-seeking firm to enter the market earlier if it faces exchange rate uncertainty. In contrast, a more competitive home market will induce a cost-oriented firm to shift its production to a low-wage foreign country earlier. In the empirical part, a recent survey dataset for Taiwanese firms‟ investment into China is employed to check the validity of our theoretic framework. With event history modeling, our empirical results are generally consistent with our theoretical prediction.

Keywords: Exchange rate uncertainty, foreign direct investment, real options, game theory, event history modeling

一〃 前言

近三十年來,各國對外直接投資(foreign direct investment,簡稱 FDI)之流量不僅成長快速,而且波

動幅度相當劇烈。1

對於 FDI 短期間大幅波動之現象,傳統的 FDI 理論並無法提供合理的解釋 (Blonigen

(1997, p.447))。由於廠商對外直接投資所產生之成本或效益往往涉及不同貨幣之轉換,而 1970 年代以 來,因為各國紛紛採行浮動或機動匯率制度,以致許多國家匯率波動幅度日劇,因此陸續出現許多文 獻探討匯率波動與 FDI 短期波動的關聯性。

綜合過去相關理論與實證文獻,雖然匯率波動對 FDI 可能產生影響已受到肯定,然而,其影響方 向在文獻上的意見卻仍十分歧異。Chen et al. (2006)及 Lin et al. (2006)指出,文獻上的歧異可能是由於 未區分廠商投資動機所致。若匯率水準與匯率波動對 FDI 之影響視廠商投資動機而定,使用總體資料 來分析這個問題可能會造成加總偏誤(aggregation bias)。他們建立一個實質選擇權模型,並討論了三種 投資動機的 FDI:回銷導向、尋求新市場導向及替代出口導向。研究結果顯示,匯率不確定性對 FDI 的影響會依不同投資動機及不同風險態度而異。此外,他們以台商至中國大陸投資為研究對象,發現 投資動機的確是造成匯率及匯率波動對 FDI 時點影響不同的重要因素。可惜的是,不管是 Chen et al. (2006)及 Lin et al. (2006)或過去其他文獻,皆未考慮不完全競爭市場的情況。由於廠商的策略互動可能 影響選擇權之價值, 而多國籍公司在國際上一般往往有一定的定價能力,因此似有必要將廠商的策略 互動的可能影響納入模型之中。

二〃研究目的

本研究的目的,就是延續申請人過去之相關研究 (Chen et al. (2006), Lin et al. (2006), Lin and Chen (2008)),應用實質選擇權理論架構,探討寡占市場下匯率波動與海外直接投資之關係,並以台商至大 陸的投資資料驗證本文理論架構之解釋能力。雖然申請人過去之實證結果大多符合其理論預期,顯示 實質選擇權理論具有相當之解釋能力,惟申請人過去之相關研究均未將市場結構以及廠商策略互動關 係納入。基於近年有關實質選擇權賽局理論之發展,實有必要在理論架構以及實證模型中考慮市場結 構以及廠商策略互動等因素,以進一步探索實質選擇權賽局理論在不同市場結構與競爭條件下之適用 性。 在理論分析方面,本研究探討的主要議題為:匯率波動性與海外直接投資的關係是否可能受到市 場結構以及廠商策略互動等因素之影響?若是,則對於不同投資動機下之廠商所產生之影響可能有何不 同?實證分析分面,本研究將根據理論分析之結果建構實證模型,採用個體廠商資料並應用事件歷史 研究法進行經濟計量分析

三、 文獻回顧

有關匯率波動與 FDI 短期波動的關聯性的文獻,主要包括二大類:(1) 匯率水準值與 FDI;(2) 匯 率不確定性與 FDI。然而,這些文獻對於匯率水準值及其波動影響 FDI 的方式及方向,目前皆尚未有 一定論。以下簡要分別介紹此二大類文獻。匯率水準值與 FDI

關於匯率水準值與 FDI 關聯性的文獻,大致上可分為兩類。第一類文獻聚焦於匯率的波動如何影響廠商收購國外資產時之成本(例如,Froot and Stein (1991)與 Blonigen (1997)),第二類文獻則指出匯

Froot and Stein (1991) 建立一個不完全資本市場模型(imperfect capital market)。該文指出,本國貨 幣貶值會使本國人民財富相對縮水,因此會促使外國人民前來併購本國資產或廠商。Blonigen (1997) 則指出,匯率波動可能會影響併購型 FDI 的行為,因為本國廠商併購之外國資產通常包含了專屬於該 廠商的特定優勢(如技術與管理技能),而該優勢可創造新的利潤且轉移過程不必經由貨幣轉換,可降 低併購國外資產的價格,所以會刺激 FDI 之進行。 在匯率波動對 FDI 之利潤影響方面,Cushman (1985)建立了一個非常完整的模型,其中考慮了多 國籍廠商在何處生產、何處購買生產要素、何處融資與何處銷售產品等因素。該研究指出,外國貨幣 貶值可降低以本國貨幣表示之外國生產成本,因此對 FDI 有利。2上述本國貨幣升值(或外國貨幣貶值)

可促進本國廠商進行 FDI 活動的結論得到非常多實證文章的支持,例如,Kohlhagen (1977)、Cushman (1985)、Froot and Stein (1991)、Klein and Rosengren (1994)、Campa (1994)、Dewenter (1995)、Kogut and Chang (1996)、Blonigen (1997)、Bell and Campa (1997)、Xing (2002)、Iannizzotto and Miller (2002)與 Kiyota and Urata (2004)。

另一方面,Campa (1993)使用 Dixit (1989b)的實質選擇權架構探討匯率波動對 FDI 之影響。與其他 文獻不同的地方就是該文討論的是以銷售為目的之 FDI。當地主國貨幣升值,以本國貨幣表示之銷售 收入會較高,故應有刺激 FDI 的效果。Campa (1993)與 Tomlin (2000)以美國零售業為樣本之實證結果 支持這個論點。

另外,有些文獻則發現匯率水準值對 FDI 的影響會依不同產業或不同國家而異,例如 Goldberg (1993)、Kosteletou and Liargovas (2000)、Gorg and Wakelin (2002)、Kyrkilis and Pantelidis (2003)與 Pain and Van Welsum (2003)等。

匯率不確定性與 FDI

有關匯率不確定性與 FDI 關係之文獻,我們亦可依影響管道之不同將文獻概略分成兩類:廠商風 險態度與保持投資彈性之選擇權價值。較早之文獻認為對風險袪避(risk-averse)廠商而言,較高的匯率 波動會提高利潤之風險程度,以致降低廠商對該利潤之確定等值(certainty equivalent value),因此匯率

波動提高將不利於廠商進行 FDI。3

相反的, Itagaki (1981)則強調利潤暴露在匯率風險下部位(the exposure to exchange rate risk)的重要性。該篇文章指出匯率波動對多國公司生產與貿易之影響,需視該 公司之利潤暴露在匯率風險下的部位是正或是負而定。Cushman (1985)與 Goldberg and Kolstad (1995) 亦強調必須考慮廠商投資後其利潤暴露在匯率風險下的部位有何改變。例如,如果廠商是以 FDI 替代 出口,則 FDI 行為可能降低利潤暴露在匯率風險下的部位,以致匯率波動提高反而有利於 FDI 活動。

另一方面,傳統文獻大多忽略了國際投資之的一項重要特性,就是 FDI 之執行時機通常是有些彈 性,而非本期決定不投資後即失去該投資機會。由 1980 年代開始,實質選擇權理論(real options theory) 開始被應用在分析投資行為上。在不確定性與投資不可回復性(irreversible investment)的假設之下,實 質選擇權理論認為不確定性提高時,廠商可能為了得到未來更多市場資訊而決定多等待一期,因而延 遲投資。Dixit (1989a,b)指出,即使對於風險中立的廠商而言,不確定性提高會使廠商等待的價值(waiting value)提高。因此,由此可以推論匯率波動提高對 FDI 應是不利的。另外,Darby et al. (1999)使用 Dixit-Pindyck (1994)的模型,發現考慮廠商風險袪避行為後,匯率波動對 FDI 時點的影響就會變成不確 定。

在實證文章方面,過去的文章亦指出匯率不確定性對 FDI 的影響仍會依不同國家、不同投資型態 與不同時間而異。例如,Amuedo-Dorantes and Pozo (2001)、 Bell and Campa (1997)、Campa (1993, 1994)、Darby et al. (1999)、Crowley and Lee (2002)與 Kiyota and Urata (2004)發現匯率不確定性和 FDI 是負向關係,但 Cushman (1985)、Goldberg and Kolstad (1995)與 Pain and Van Welsum (2003) 則發現匯 率不確定性和 FDI 是正向關係。

不確定性情況下廠商策略互動與 FDI

目前已有相當多文獻詴圖將實質選擇權理論以及賽局理論結合起來,以分析實質選擇權理論在不 同市場結構下之適用性。主要原因在於許多產業的廠商同時面臨不確定性以及彼此存在策略互動關 係。由於廠商的策略互動可能影響選擇權之價值,而多國籍公司在國際上一般往往有一定的定價能力, 因此在探討匯率不確定性對 FDI 的影響時似有必要將廠商的策略互動的可能影響納入模型之中。這方 面的文獻包括 Kester (1984),Trigeorgis (1991),Smit and Ankum (1993),Grenadier (1996, 2000, 2002), Kutatilaka and Perotti (1998),Baldursson (1998) , Weeds (2002),Nielson (2002),Lambrecht and Perraudin(2003),Huisman and Kort (2004),Smit and Trigeorgis (2004, 2006), Pawlina and Kort (2006),Thijssen et al.

(2006)等。4 有些文獻指出,市場競爭或廠商策略互動會減弱不確性對廠商延遲投資的影響力,亦即當

市場存在兩家以上的廠商彼此競爭時,等待的價值(option value to wait)會隨著競爭程度的提高而減少;

例如 Grenadier (1996, 2000, 2002), Lambrecht and Perraudin (2003), Huisman and Kort (2004), Smit and

Trigeorgis (2004) and Thijssen et al. (2006)。Bulan et. al.(2009) 對加拿大溫哥華公寓建案以及 Bontempi et.al.(2010) 對義大利製造商投資案之實證均支持市場競爭會減弱不確性對廠商延遲投資的影響力。惟 有關實質選擇權理論賽局之實證研究仍然極為少見(Azevedo and Paxson (2010, p.42)。特別是,有關匯率 波動與 FDI 關係之實證研究,似尚未有考慮市場競爭程度之文獻出現。

四、理論架構

本研究首先建立理論架構,探討不同投資動機下匯率波動與海外直接投資之關係。本文研究聚焦 在成本導向之海外直接投資 (cost-oriented FDI) 以及市場導向之海外直接投資 (market-oriented FDI), 因為在過去台商對外投資之動機中,這兩類型之海外直接投資佔了絕大部分。

(一) 市場導向之海外直接投資

假設廠商面對不確定之匯率水準( )R ,而在決定產量時假設匯率水準已知。假設廠商基於尋找新市 場之考量,考慮在適當時機進入國外市場。匯率係以一單位外幣可以兌換多少本國貨幣表示。假設廠 商為風險中立。假設國外設廠生產均必須花費一固定的沉沒成本(sunk costs) , I 。為了簡化分析,假 設變動生產成本為零。假設廠商只在國外市場銷售,面對一線性的逆需求函數 ( ) :P Q ( ) P Q a bQ (1) 1. 獨占情況 首先,假設廠商在進入國外市場前該市場不存在其他廠商,且進入後變成為獨占廠商。則廠商在 進入該市場後每期得到之利潤流量如下:

2 1 1 1 1 4 M M a q q R a R (2) 進入該市場投資帶來之累積利潤折現值可以表為

2

4 M M a R R (3) 其中, 。 該獨占廠商選擇適當時點進入國外市場之決策問題可以寫為:

0 0 1 max , 1 M V R R I V R R t (4) 該獨占廠商只有在匯率水準夠高時(亦即本國幣值夠低時)才會進入國外市場,其門檻值如下:

2 4 1 M M I R a (5) 其中, 2 2 2 2 2 [ ( 0.5 ) ( 0.5 ) 2 ] 1 (Dixit, 1989b, p.626.)。 比較靜態分析結果如下: 0 M dR dI , 0 M dR d , 0 M dR d (6) 由(6)式可知,沈沒成本提高、匯率波動提高或預期本國貨幣升值都會促使尋找新市場之廠商延後進入 國外市場。此結果之經濟直覺參見 Chen et al. (2006)。 2. 雙占情況 接著,假設廠商在進入國外市場前該市場已經存在一家廠商,且進入後該市場變成為雙占局面, 且兩廠商彼此進行數量競爭。則廠商在進入該市場後每期得到之利潤流量如下:

2 1 1 1 9 D M a Q q R a R (7) 其中,Qq1q2。 進入該市場之投資帶來之折現值可以表為

2

9 D M a R R (8) 同理,該廠商只有在匯率水準夠高時(亦即本國幣值夠低時)才會進入國外市場。雙占情況下之門 檻值如下:

2 9 1 D M I R a (9) 3. 獨占與雙占情況之比較 為了瞭解市場競爭對廠商在面對匯率波動時進入國外市場之時點的影響,我們比較在此兩種情況下 之匯率門檻值如下:

2 5 0 1 D M M M I R R a (10) 由(10)式可知,獨占情況下之匯率門檻值較低,此表示市場競爭將促使尋求新市場之廠商延後進入國外 市場。此結果之經濟直覺如下: 進入國外市場之機會可視為一項買權(call option)。是否進入一個市場或 是繼續等待,必須衡量其成本與效益。延遲進入之成本為犧牲一期之利潤流量,但其效益為繼續保有 選擇更適當時點進入市場之機會(及該選擇權)。在雙占情況下利潤流量較低,且選擇權價值較高,故會 等待較久。 由(10)式對 微分可得,

0 1 D M D M M M M M d R R R R d (11)其中, 2 2 2 2 2 2 2 ( 0 . 5 )

[ 1

]

0

。由(11)式可知, 匯率波動愈大,市場競爭促使尋求新 市場之廠商進入國外市場的時點更為延後。此結果之經濟直覺為: 匯率波動變大,選擇權價值提升, 但由於雙佔下的選擇權價值較高,故提升的幅度也就變大。(二) 成本節省型之海外直接投資

本小節接著探討在匯率不確定情況下成本節省型之廠商海外直接投資時機與市場競爭之關係。假 設廠商基於國內生產成本過高,考慮將生產活動移往海外,但生產後將產品回銷回母國。廠商在決定 設廠地點時面對不確定之匯率水準 ( )R ,而在決定產量時假設匯率水準已知。匯率係以一單位外幣可以 兌換多少本國貨幣表示。假設廠商為風險中立。假設國外設廠生產均必須花費一固定的沉沒成本(sunk costs) ,I。假設投資前單位成本為k2,投資後單位成本為R k 1,且R k 1<k2,亦即在國外生產具有成 本優勢。假設廠商只在國內市場銷售,面對一線性的逆需求函數 ( ) :P Q ( ) P Q a bQ 1. 獨占情況 首先,假設廠商在進入國外生產前國內市場不存在其他廠商。則廠商在進入該市場前與進入後每 期得到之利潤流量分別如下: FDI 前利潤:10

aq q1

1k q2 1 (12) FDI 後利潤:11

aq q1

1k Rq1 1 (13) 進入國外生產帶來之每期利潤流量可以表為

2

2 1 0 1 1 1 2 1 1 4 4 M C a R k a k (14) 因此,進入國外生產帶來之累積利潤的折現值可以表為

2

2

1

12

2 2 2 4 2 4 2 M C k a k ak k R R R (15)其中, 2 2 。該獨占廠商選擇適當時點進入國外市場之決策問題可以寫為:

0 0 1 max , 1 C V R R I V R R t (16) 該獨占廠商只有在匯率水準夠低時(亦即本國幣值夠高時)才會進入國外生產。假設其門檻值為 M C R 。 當 M C RR 時的選擇權價值為 1 1 2 2 2 k R a k R , 其中, 2 2 2 2 2 [( 0.5 ) ( 0.5 ) 2 ] 0 。若進入國外生產帶來之累積利潤的折現值

M C R 較選擇權價值高,該廠商即會進入國外生產。反之,若進入國外生產帶來之累積利潤的折現值

M C R 較選擇權價值低,該廠商就會選擇繼續等待。由於非線性關係不易看出門檻值,故以下將使用 數值模擬方式。 本文假設:0,0.05,k11,a100, 2 2 , k R1 k2 。若 M C RR 則投資。R 的模擬結CM 果如表 1 所示。由表 1 可知,匯率波動愈高, M C R 愈小,因此廠商愈會延後投資;策略優勢愈大(投資 前後成本差異愈大), M C R 愈大,因此廠商愈會提前投資。 2. 雙占情況 接著,假設廠商在進入國外生產前本國市場已經存在另一家相同生產成本之廠商,且兩廠商彼此 進行數量競爭。則第 1 家廠商(以下標 2 表示)在進入該市場後每期得到之利潤流量如下: FDI 前利潤:10

aQ q

1k q2 1 (17) FDI 後利潤:11

aQ q

1k Rq1 1 (18) 假設競爭廠商(以下標 2 表示)不管如何都未前往海外設廠,故其利潤函數如下:

2 a Q q2 k q2 2 (19) 第 1 家廠商進入國外生產帶來之每期利潤流量可以表為

2

2 1 0 1 1 2 1 2 1 1 2 9 9 D C a k R k a k (20) 因此,第 1 家進入國外生產帶來之累積利潤的折現值可以表為

2

1

2

12

2 2 4 4 4 9 9 9 2 D C k a k ak k R R R (21) 其中, 2 2 。 D C RR 時的選擇權價值為 1 2 1 2 4 2 9 2 k R a k k R 。由於非線性關係不易看出 門檻值,故以下將使用數值模擬方式。本文假設:0,0.05,k11,a100, 2 2 , 1 2 k Rk 。若 D C RR 則投資。R 的模擬結果如表 2 所示。表 2 結果與表 1 類似。匯率波動愈高,CD D C R 愈小,因此廠商愈會延後投資;策略優勢愈大(投資前後成本差異愈大), D C R 愈大,因此廠商愈會提 前投資。 為了瞭解市場競爭對成本節省型廠商在面對匯率波動時進入國外生產之時點的影響,我們模擬分 析兩種情況下之匯率門檻值大小。本文假設:0,0.05,k11,a100, 2 2, k R1 k2。 D M C C R R 的模擬結果如表 3 所示。表 3 結果顯示RCDRCM 0,亦即市場競爭將促使成本節省型廠商在 面對匯率波動時提早進入國外生產。此外,表 3 結果顯示,匯率波動愈大, D M C C R R 愈大,因此市場 競爭對 FDI 的正面效果愈顯著。再者,策略優勢愈大,亦即k 愈大,市場競爭對 FDI 的正面效果也愈2 顯著。此結果與尋找新市場之 FDI 剛好相反。其經濟直覺如下:與尋找新市場之 FDI 一個重要差異就是, 在雙占情況下,先進入國外生產之廠商將會享有生產成本優勢,而在獨占情況下卻無此種可能。然而, 成本節省型廠商延遲進入國外生產時仍有營收,因此也沒有犧牲當期利潤之問題。因此,最後之結果 端視此兩種力量何者較大而定。五、 實證分析

實證模型 有關實證分析方面,由於本研究目的在於探討匯率波動性與廠商海外直接投資時機之關聯性,我 們採用事件歷史研究法(event history analysis )。事件歷史研究法探討某個事件發生前一段時間可能出現的事情。就本研究而言,廠商進入國際市場的時機可視為此事件發生的時機。 實證模型方面,本研究

採用 Cox (1972, 1975)的比例風險模型( proportional hazard model)。假設樣本的風險率(hazard rate, ( )h t )

的函數如下:

| x , x ( )i1 2i

0

exp

x1i x ( )2i

h t t h t t

式中下標 t 代表時間,i代表廠商; 與 為參數向量; x1i 為與時間無關之解釋變數向量而x ( )2i t

則是與時間有關之解釋變數向量;h t0( ) 為基準風險函數(baseline hazard function)。假設h t0( )不受x1i以

及x ( )2i t 之影響。 假設我們有n個觀察值以及K個不同的進入市場時間點 。如果我們將樣本按照進入市場時間先後排 序,則其概似函數, L ,可以表示為 p 1 2 1j 2j x x ( ) x x ( ) 1 ( ) i i i i t n p t i j t e L e

(22)式中( )ti 代表風險集合(risk set),亦為所有可能進入市場之廠商所形成之集合(詳見 Lawless (2003) or

Box-Steffensmeier and Jones (2004));i為一指標(indicator),i 0表示該樣本為右截斷(right-censored)。

本研究將根據前述理論架構建立廠商進入國際市場時機的實證模型如下:

0

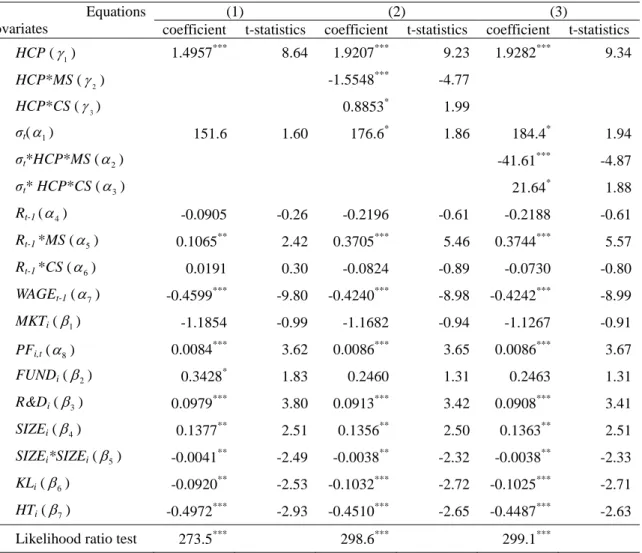

1 2 3 1 2 3 4 1 5 1 6 1 7 1 8 l o g ( ) ( ) i i i i i t t i i t i i t t i t i it it h t h t HCP HCP MS HCP CS HCP MS HCP CS R R MS R CS WAGE PF 1 2 3 4 5 6 7 + + & i i i i i i i i itMKT FUND R D SIZE SIZE SIZE KL HT (23) 各符號說明如下: MS:虛擬變數。尋求新市場 FDI 廠商為 1,其餘為 0。如果在中國子公司當地銷售比率超過 80%, 則定義為尋求新市場 FDI 廠商,符合該定義的廠商共有 70 家。 CS:虛擬變數。尋求降低成本 FDI 廠商為 1,其餘為 0。若廠商屬傳統勞力密集型產業,則定義 為降低成本 FDI 廠商,符合該定義的廠商共有 23 家。傳統勞力密集型產業包括食品飲料製造業、非金

屬製造業、紡織業、成衣服飾業、造紙及印刷業、皮革製品製造業、木竹籐柳製造業等。 HCP:虛擬變數。該廠商所處產業競爭激烈為 1,其餘為 0。依前述理論模型推論,競爭程度對 FDI 時點影響,依投資動機不同而異。本研究預期對尋求新市場廠商而言,競爭程度提高,FDI 時點會 延後;但對降低成本廠商而言,競爭程度提高,FDI 時點將會提前。也就是說,本研究預期符號2為 負,3為正。 1 t R :人民幣相對於新台幣實質匯率水準,以台灣與中國大陸之消費者物價指數平減,因為 FDI 決策需較長時間,故採用落後一期之匯率。本研究預期新台幣貶值對尋求新市場的 FDI 廠商有利,但 對降低成本 FDI 廠商較不利。資料來源為中央銀行與台灣經濟新報資料庫(TEJ)。依前述理論模型推論, 本研究預期5符號為正,6為負。 t :匯率波動度。本研究預期當匯率波動提高,對廠商 FDI 時點有負面影響。然而,對於尋求新 市場的廠商而言,當競爭程度提高,匯率波動提高對 FDI 時點的影響是負面的。反之,對於降低成本 FDI 廠商而言,競爭程度提高,匯率波動提高,對 FDI 時點影響則是正面的。因此,本研究預期符號2 為負,3為正。 1 t WAGE :落後一期之中國與台灣實質工資水準比率。資料來源為 TEJ 資料庫。 其他控制變數:母公司利潤率(PF)、母公司行銷密集度(MKT)、母公司研發密集度(R&D)、母公司 銷貨收入(SIZE)、母公司資本勞動比(KL)。這些變數為 1987-1991 年之平均值,若該公司於 1987 年後 設立,則為設立後 5 年之平均值,資料來源為 TEJ 資料庫。另外,資金來源(FUND)為虛擬變數,若主 要資金來自母公司則設為 1,其餘為 0,資料來源為問卷資料。產業虛擬變數(HT)方面,若該廠商屬高 科技產業則設為 1,其餘為 0,資料來源為經濟部發行之科技產業白皮書。 實證資料 本研究使用經濟部投資審議委員會 2003 年與 2004 年「大陸投資事業營運調查分析報告」之問卷 資料為研究對象。該問卷的調查對象為在台灣地區經投資審議委員會核准之中國大陸地區投資事業, 營運日期滿一年以上之全體廠商。該問卷調查的是台商大陸子公司前一年度之營運狀況,例如,2003 年之問卷調查乃是調查廠商 2002 年之營運狀況。2003 年問卷回收 877 家,回收率為 30.2%,2004 年 問卷回收 872 家,回收率為 34.2%。本研究挑選回收問卷之中上市上櫃廠商共 198 家。進一步,根據 台灣經濟新報資料庫統計,截至 2002 年底,全體上市上櫃公司共 1,145 家,其中在 2002 年之前赴中 國大陸投資者有 672 家,也就是說,本研究樣本占已赴中國大陸投資之上市上櫃公司 29.5%,為避免

樣本偏誤的問題產生,因此再從未赴中國大陸投資廠商中隨機抽取得 139 家,故總樣本廠商數共計 337 家。 由於台灣政府 1987 年開放台灣民眾至中國大陸探親,故本研究設定由 1987 年起為廠商可至中國 投資的起點。但若廠商於 1987 年後才設立,則改以其設立時間為起點,這樣的廠商共有 36 家。接下 來,在問卷中填寫同業競爭激烈的廠商共有 111 家,占至中國大陸投資樣本的 56%。各變數之基本統 計量請見表 4。 進一步,本研究使用條件變異數-GARCH 來估計匯率波動,估計期間為 1985:01~ 2002:12,在這段

期間,我們使用 Augmented Dickey Fuller (ADF) 檢定,一階差分之lnRt數列均拒絕單根(unit root)之

虛無假設,GARCH 模型估計如下: 1 ( 1.24) lnRt lnRt lnRt 0.0031 ut , (25) 2 1 1 (18.00) (9.54) ( 4.22) 0.0012 0.3389 0.1049 t t t h u h , 其中,ht為條件變異數;ut為誤差項;括弧內為 t 統計量。因此,σ 為: 1 2 1 1 1 T t t j j h T

實證結果 本研究實證結果列於表 5-2。(1)欄未考慮投資動機,(2)欄與(3)欄則考慮投資動機扮演的角色。由(1) 欄中可看出,競爭程度提高使台商至中國大陸進行 FDI 的時點提前,且估計係數在 1%顯著水準下,顯 著異於零。其次,匯率波動程度提高,對 FDI 時點影響為正,但未達統計上之顯著水準。在匯率水準 值方面,對尋求新市場廠商而言,新台幣貶值使 FDI 時點提前;但對降低成本廠商而言,則為新台幣 升值使 FDI 時點提前。然而,後者之估計係數未達統計上之顯著水準。 在控制變數方面,多數控制變數均和過去文獻之實證結果相似。例如,台灣工資水準相對於中國大 陸提高對 FDI 時點有正面影響;獲利率較高、母公司提供資金、研發密集度較高對 FDI 時點有正面影 響;規模愈大對 FDI 時點有正面影響,但當規模大到某個程度,規模提高對 FDI 時點則為負面影響; 資本勞動比愈高,對 FDI 時點有負面影響;高科技廠商相對其他廠商,FDI 時點較晚。 第(2)欄與第(3)欄加入了投資動機的虛擬變數,實證結果均是顯著的。其中,對尋求新市場廠商而言,競爭程度提高,FDI 時點相對其他廠商是延後的(2估計係數為-1.5548);反之,對於降低成本廠 商而言,競爭程度提高,FDI 時點相對其他廠商是提前的(3估計係數為 0.8853)。最後,對於競爭激 烈之尋求新市場廠商,匯率波動提高會使其 FDI 時點延後(2估計係數為-41.61)。但對競爭激烈之降 低成本廠商,匯率波動提高會使其 FDI 時點提前(3估計係數為 21.64)。這些實證結果和前節之理論 推理是一致的。

六、 結論

國際間 FDI 流量短期間大幅波動之現象,傳統的 FDI 理論並無法提供合理的解釋。對於此現象, 過去雖已出現許多理論與實證文獻探討匯率波動與 FDI 流量短期間出現大幅波動的關係,然而,其影 響方向在文獻上的意見卻仍十分紛歧。本研究延續申請人過去之相關研究 (Chen et al. (2006), Lin et al. (2006), Lin and Chen (2008)),應用實質選擇權理論架構,進一步探討寡占市場下匯率波動與海外直接 投資之關係,並以台商至大陸的投資資料驗證本文理論架構之解釋能力。本研究理論分析顯示,在面臨匯率不確定情況下,若國外市場愈競爭,市場導向型廠商愈可能延 遲進入該市場。相反的,對於成本導向型廠商而言,若其本國市場愈競爭,該廠商愈可能提早將生產 活動移往低工資國家。本研究利用台商至中國大陸投資的調查資料進行實證研究,以檢驗本文理論架 構之解釋能力。本研究採用事件歷史分析法(event history analysis)。本研究實證結果大致支持本研究之 理論預期。

參考文獻

陳坤銘、林家慶、溫偉任, 2010, 匯率波動性、廠商策略互動與海外直接投資:台灣製造業廠商之實證,

中華國際經貿研究學會 2010 學術研討會論文,台北:國立政治大學,2010 年 12 月 4 日。

Amuedo-Dorantes, Catalina and Susan Pozo, 2001. “Foreign exchange rates and foreign direct investment in the United States,” The International Trade Journal, 15, 323-343.

Azevedo, Alcino and Dean A. Paxson, 2010. “Real options game models: a review.” Working paper.

Baldursson, Fridrik M. 1998. “Irreversible investment under uncertainty in oligopoly,” Journal of Economic

Dynamics & Control, 22, 627-644.

Bell, Gregory K. and Joes M. Campa. 1997. “Irreversible investments and volatile markets: a study of chemical processing industry,” Review of Economics and Statistics, 79, 79-87.

Blonigen, Bruce A. 1997. “Firm-specific assets and the link between exchange rates and foreign direct investment,” American Economic Review, 87, 447-465.

Bontempi, E., R. Golinelli, and G. Parigi ,2010. “ Why demand uncertainty curbs investment: Evidence from a panel of Italian manufacturing firms,” Journal of Macroeconomics, 32, 218–238.

Box-Steffensmeier, Janet M. and Bradford S. Jones, 2004. Event History Modeling: A Guide for Social

Scientists, Cambridge: Cambridge University Press.

Bulan, Laarni T., 2009. “Irreversible investment, real options, and competition-Evidence from real estate,”

Journal of Urban Economics, 65, 237–251.

Campa, Joes M. 1993. “Entry by foreign firms in the United States under exchange rate uncertainty,” Review

of Economics and Statistics, 75, 614-622.

Campa, Joes M. 1994. “Multinational investment under uncertainty in the chemical processing industries,”

Journal of International Business Studies, 25, 557-578.

Chen, Kun-Ming, Hsiu-Hua Rau, and Chia-Ching Lin, 2006. “The impact of exchange rate movements on foreign direct investment: market-oriented versus cost-oriented,” The Developing Economies, 44(3), 269-287.

Chen, Kun-Ming, Chia-Ching Lin, and Wei-jen Wen, 2011. “Exchange Rate Uncertainty, Strategic Interaction and the Timing of Foreign Direct Investment,” presented at Western Economic Association International, The 9th Biennial Pacific Rim Conference, April 26-29, 2011, Brisbane, Aus Australia. Cottrell, T. and G. Sick, 2001. “ First-mover (dis)advantage and real options, ” Journal of Applied

Corporate Finance, 14, 41–51

Cottrell, T. and G. Sick, 2002. “Real options and follower strategies: The loss of real option value to first-mover advantage,” The Engineering Economist, 47, 232–263

Cox David R. 1972. “Regression Models and Life Tables,” Journal of the Royal Statistical Society, B34, 187-220.

Cox David R., 1975. “Partial likelihood,” Biometrika, 62, 269-76.

Crowley, Patrick and Jim Lee, 2002. “Exchange rate volatility and foreign investment: international evidence,” Western Hemispheric Trade conference, Texas A&M International University. Texas.

Cushman, David O. 1985. “Real exchange rate risk, expectations, and the level of direct investment,” Review

of Economics and Statistics, 67, 297-308.

Darby, Julia, Andrew H. Hallett, Jonathan Ireland, and Laura Piscitelli, 1999. “The impact of exchange rate uncertainty on the level of investment,” The Economic Journal, 109, 55-67.

Dewenter, Kathryn L., 1995. “Do exchange rate changes drive foreign direct investment,” The Journal of

Business, 68, 405-433.

Dixit, Avinash K. 1989a. “Hysteresis, import penetration, and exchange rate pass-through,” Quarterly Journal

of Economics, 104, 205-228.

Dixit, Avinash K. 1989b. “Entry and exit decisions under uncertainty,” Journal of Political Economy, 97, 620-638.

Dixit, Avinash K. and Robert S. Pindyck. 1994. Investment under Uncertainty, Princeton: Princeton University Press.

Froot, Kenneth A. and Jeremy C. Stein. 1991. “Exchanges rates and foreign direct investment: an imperfect capital markets approach,” Quarterly Journal of Economics, 106, 1191-1217.

Goldberg, Linda S., 1993. “Exchange rates and investment in United States industry,” Review of Economics

and Statistics, 75, 575-588.

Goldberg, Linda S. and Charles D. Kolstad, 1995. “Foreign direct investment, exchange rate variability and demand uncertainty,” International Economic Review, 36, 855-873.

Gorg, Holger and Katharine Wakelin. 2002. “The impact of exchange rate variability on US direct investment,” Manchester School, 70, 380-397.

Grenadier, Steven R., 2000. “The interaction of real options and game theory,” Journal of Applied Corporate

Finance, 13, 99-107.

Grenadier, Steven R., 2002. Option exercise games: An application to the equilibrium investment strategies of firms. Review of Financial Studies, 15 (3), 691-721.

Huisman, K., Kort, P., 2004. “Strategic technology adoption taking into account future technological improvements,” European Journal of Operations Research, 159 (3), 705–728.

Iannizzotto, Matteo and Nigel J. Miller, 2002, “The effect of exchange rate uncertainty on foreign direct investment in the United Kingdom,” Working paper, IEA World Congress.

Itagaki, Takao, 1981. “The theory of the multinational firm under exchange rate uncertainty,” Canadian

Journal of Economics, 14, 276-297.

Jeanneret, Alexandre, 2009. “Foreign direct investment and exchange rate uncertainty,” mimeo., University of Lausanne-Swiss Finance Institue.

Kester, W. Carl, 1984. “Today‟s options for tomorrow‟s growth,” Harvard Business Review, 153-160.

Kiyota, Kozo and Shujiro Urata, 2004. “Exchange rate, exchange rate volatility and foreign direct investment,” World Economy, 27, 1501-1536.

Klein, Michael W. and Eric S. Rosengren. 1994. “The real exchange rate and foreign direct investment in the United States: relative wealth vs. relative wage effects,” Journal of International Economics, 36, 373-389.

Kogut, Bruce and Sea Jin Chang, 1996. “Platform investments and volatile exchange rates: direct investment in the U.S. by Japanese electronic companies,” Review of Economics and Statistics, 78, 221-231.

Kogut, B., and N. Kulatilaka, 1994, „„Operating flexibility, global manufacturing, and the option value of a multinational network,‟‟ Management Science, 40, 123-39.

Kohlhagen, Steven W. 1977. “Exchange rate changes, profitability, and direct foreign investment,” Southern

Economic Journal, 44, 376-383.

Kosteletou, Nikolina and Panagiotis Liargovas, 2000. “Foreign direct investment and real exchange rate interlinkages,” Open Economies Reviews, 11: 135-148.

Kulatilaka, Nalin and Enrico C. Perott, 1998,” Strategic growth options,” Management Science, 44, 1021-1031.

Kyrkilis, Dimitrios and Pantelis Pantelidis, 2003. “Macroeconomic determinants of outward foreign direct investment,” International Journal of Social Economics, 30, 827-836.

Lambrecht, B., and Perraudin, W., 2003. “Real options and preemption under incomplete Information,”

Journal of Economic Dynamics and Control, 27, 619-643.

Lawless, Jerald F., 2003. Statistical Models and Methods for Lifetime Data, second edition, New Jersey: John Wiley & Sons, Inc.

Lin, Chia-Ching and Kun-Ming Chen, 2008. “The impact of exchange rate movements on foreign direct investment: are there third country effects?” paper presented at the 11th International Convention of the East Asian Economic Association, East Asian Economic Association, Manila, Philippines, November 15-16, 2008.

Lin, Chia-Ching, Kun-Ming Chen, and Hsiu-Hua Rau, 2006. “Exchange rate volatility and the timing of foreign direct investment: market-seeking versus export- substituting,” paper presented at the Conference of WTO, China, and the Asian Economies IV, University of International Business and Economics, Beijing, China, June 24-25, 2006.

Nielsen, Martin J., 2002. “Competition and irreversible investments,” International Journal of Industrial

Organization, 20, 731–743.

Pain, Nigel and Desiree Van Welsum, 2003. “Unitying the Gordian knot: the multiple links between exchange rates and foreign direct investment,” Journal of Common Market Studies, 41: 823-846.

Pawlina, Grzegorz, And Perter M. Kort, 2006. “Real options in an asymmetric duopoly: who benefits from your competitive disadvantage?” Journal of Economics & Management Strategy, 15(1), 1-35.

Smit, Han T.J., and Lenos Trigeorgis, 2004. Strategic Investment, Princeton, N.J.: Princeton University Press.

Smit, Han T.J., and Lenos Trigeorgis, 2006. “ Real options and games: Competition, alliances and other

applications of valuation and strategy,” Review of Financial Economics 15 (2006) 95–112.

Smit, Han T.J., and L.A. Ankum, 1993. “A real options and game-theoretic approach to corporate

investment strategy under competition,” Financial Management, 22(3): 241-250.

Sun, Hongmo, Harvey E. Lapan, 2000. “Strategic foreign direct investment and exchange rate uncertainty,” International Economic Review, 41, 411-423.

Tan, Dan chi, Shih-Chang Hung, and Nienchi Liu, 2007. “The timing of entry into a new market: an empirical study of Taiwanese firms in China,” Management and Organization Review 3(2): 227-254.

Thijssen, J. J. J., Huisman, K. J. M., Kort, P. M., 2006. “The effects of information on strategic investment and welfare,” Economic Theory, 28 (2), 399-424.

Trigeorgis, Lenos, 1991. “Anticipated competitive entry and early preemptive investment in deferrable projects,” Journal of Economics and Business, 43: 143-156.

Tomlin, KaSaundra M. 2000. “The effects of model specification on foreign direct investment models: an application of count data models,” Southern Economic Journal, 67, 460-468.

Weeds, H., 2002. “Strategic delay in a real options model of R&D competition,” Review of Economic Studies, 69 (3), 729-747.

Wihlborg, Clas, 1978. “Currency risks in international financial markets,” Princeton Studies in International

Finance No. 44, Princeton University.

Xing, Yuqing, 2002. “The impact of real exchange rates on Japanese direct investment in China‟s

manufacturing: an empirical assessment,” working paper,International Development Series, The research

表 1 獨占情況下成本節省型 FDI 匯率門檻值( M C R )模擬結果 k2 σ 1 1.25 1.50 1.75 2.0 0.05 0.8540 1.0676 1.2811 1.4947 1.7083 0.10 0.7304 0.9132 1.0961 1.2790 1.4621 0.15 0.6268 0.7841 0.9416 1.0993 1.2573 0.20 0.5449 0.6838 0.8238 0.9650 1.1075 表 2 雙占情況下成本節省型 FDI 匯率門檻值(R )模擬結果 CD k2 σ σ 1 1.25 1.50 1.75 2.0 0.05 0.8542 1.0678 1.2814 1.4951 1.7088 0.10 0.7310 0.9141 1.0974 1.2809 1.4645 0.15 0.6286 0.7869 0.9457 1.1049 1.2647 0.20 0.5536 0.6977 0.8445 0.9941 1.1466 表 3 雙占與獨占情況下成本節省型 FDI 匯率門檻值差異( D M C C R R )之模擬結果 k2 σ σ 1 1.25 1.50 1.75 2.0 0.05 0.0002 0.0002 0.0003 0.0004 0.0005 0.10 0.0006 0.0009 0.0013 0.0019 0.0024 0.15 0.0018 0.0028 0.0041 0.0056 0.0074 0.20 0.0087 0.0139 0.0207 0.0291 0.0391 表 4 基礎統計量 變數名稱 平均值 最小值 最大值 標準差 實質匯率(R) 3.6895 2.6263 4.5714 0.5576 實質相對工資率(WAGE) 0.0648 0.0454 0.1198 0.0218 行銷密集度(MKT, %) 6.6% 0.0% 67.8% 8.4% 廠商規模(SIZE, 十億新台幣) 1.9198 0.0069 138.29 8.5817 利潤率(PF, %) 5.1% -178.0% 61.8% 19.2% 研發密集度(R&D, %) 0.8% 0.0% 33.1% 2.7% 資本勞動比(KL, 百萬新台幣/人) 2.5517 0.0545 49.00 3.8554

表 5 台商至中國大陸投資時點決定因素實證結果 Equations

Covariates

(1) (2) (3)

coefficient t-statistics coefficient t-statistics coefficient t-statistics

HCP (1) 1.4957*** 8.64 1.9207*** 9.23 1.9282*** 9.34 HCP*MS (2) -1.5548*** -4.77 HCP*CS (3) 0.8853* 1.99 σt(1) 151.6 1.60 176.6* 1.86 184.4* 1.94 σt*HCP*MS (2) -41.61 *** -4.87 σt* HCP*CS (3) 21.64 * 1.88 Rt-1 (4) -0.0905 -0.26 -0.2196 -0.61 -0.2188 -0.61 Rt-1 *MS (5) 0.1065 ** 2.42 0.3705*** 5.46 0.3744*** 5.57 Rt-1 *CS (6) 0.0191 0.30 -0.0824 -0.89 -0.0730 -0.80 WAGEt-1 (7) -0.4599 *** -9.80 -0.4240*** -8.98 -0.4242*** -8.99 MKTi (1) -1.1854 -0.99 -1.1682 -0.94 -1.1267 -0.91 PFi,t (8) 0.0084 *** 3.62 0.0086*** 3.65 0.0086*** 3.67 FUNDi (2) 0.3428* 1.83 0.2460 1.31 0.2463 1.31 R&Di (3) 0.0979*** 3.80 0.0913*** 3.42 0.0908*** 3.41 SIZEi (4) 0.1377** 2.51 0.1356** 2.50 0.1363** 2.51 SIZEi*SIZEi (5) -0.0041** -2.49 -0.0038** -2.32 -0.0038** -2.33 KLi (6) -0.0920** -2.53 -0.1032*** -2.72 -0.1025*** -2.71 HTi (7) -0.4972*** -2.93 -0.4510*** -2.65 -0.4487*** -2.63

Likelihood ratio test 273.5*** 298.6*** 299.1***

行政院國家科學委員會補助國內專家學者出席國際學術會議報告

100 年 5 月 11 日 報告人姓名 陳坤銘 服務機構 及職稱 國立政治大學國際經營與貿易學系 教授 時間 會議 地點 100 年 4 月 26 日~4 月 29 日 澳洲,布里斯班 本會核定 補助文號 臺會綜二字第 0990041047 號 會議名稱 Western Economic Association International 9th Biennial Pacific Rim Conference

發表 論文 題目

Exchange Rate Uncertainty, Strategic Interaction and the Timing of Foreign Direct Investment

一、參加會議經過

報告人於 100 年 4 月 23 日晚間搭機前往澳洲,4 月 24 日中午抵達布里斯班。4 月 25 日前往開會地點 Queensland University of Technology 了解當地交通路線以及校園環 境,並在附近地區參觀。4 月 26 日至 29 日參加研討會。4 月 29 日晚間搭機回國,4 月 30 日早上抵達台北。會議期間,報告人於 4 月 26 日早上參加開幕式,接者在當天第一 場會議發表論文。此外,除了參加 4 月 27 日下午第一場會議評論一篇文章之外,也參 加了許多場次的論文發表會。 二、與會心得 此次會議吸引世界各國許多經濟學家參加。有相當多學者來自澳洲、紐西蘭與美 國。亞太地區的中國、日本、韓國與台灣等地出席的學者也相當多。研討會主題雖涵蓋 經濟學各個領域,但以貿易、經濟發展以及環境議題居多。此一方面反映這些議題在亞 太地區之重要性,另一方面,在此次會議議程中,有多個場次的論文發表,係為了向國 際貿易領域之著名經濟學家 Murray Kemp 教授致敬的論文。在這些場次的會議中, Murray Kemp 以及 Ronald Jones 兩位高齡的著名經濟學家大都沒缺席,而且專心聆聽演 講,其敬業精神令人欽佩。 此次會議的另一項特色就是有多場有關水資源問題的研討論文。最近全球各地許多 城市飽受洪水侵襲,但同時卻有許多城市(包括臺灣)鬧水荒。水資源的管理看來是當前 各國面臨的一項重要經濟課題。 三、考察參觀活動(無是項活動者省略) 無。 四、建議 無。 五、攜回資料名稱及內容 本次會議議程。 六、其他

2 無。

Exchange Rate Uncertainty, Strategic Interaction and the Timing of

Foreign Direct Investment

*Kun-Ming Chen

Department of International Business, National Chengchi University Chia-Ching Lin

Department of International Trade, National Taichung Institute of Technology Wei-jen Wen

Department of International Business, National Chengchi University

Abstract

This paper examines the relationship between exchange rate uncertainty and the timing of foreign direct investment empirically. The focus of this paper is on exploring if the relationship between exchange rate movements and the timing of foreign direct investment is related to the market structure and strategic interaction of investing firms. A recent survey dataset for Taiwanese firms’ investment into China is employed. Based on event history modeling, our empirical results reveal that the more competitive a market is, the earlier a firm will enter the market. This result supports the previous theoretical and empirical findings that market competition might diminish the option value of entering a new market, thus reducing the delay in the timing of foreign entry. Our results also demonstrate that there is weak evidence about the possible nonlinear relation between exchange rate volatility and the timing of foreign direct investment, which hinges on market structure.

Keywords: Exchange rate uncertainty, foreign direct investment, real options, game

theory, event history modeling

JEL: F21, F31, G13, C41

*

Corresponding author: Kun-Ming Chen, Professor, Department of International Business, National Chengchi University, Taipei 11623, Taiwan. Tel.: 886-2-29387515. E-mail: [email protected]. Chia-Ching Lin, Department of International Trade, National Taichung Institute of Technology, E-mail: [email protected] Wei-jen

4

1. Introduction

The flows of foreign direct investment (FDI) have been increasing dramatically in many countries since the 1970s. However, the levels of FDI flows in those countries tend to fluctuate sharply over time - a phenomenon that cannot be explained satisfactorily by traditional theories. For instance, the rise in FDI is regarded by OLI paradigm proposed by Dunning (1977) as being motivated by ownership, location or internalization advantages. While those advantages may account for the increase on FDI levels in the long run, they offer little explanation for their substantial short-run movements (Blonigen (1977)).

Ever since the breakdown of the Bretton Woods system in 1973, the exchange rates of many countries have also been fluctuating considerably during the same period. A large body of recent research deals with the possible linkages between exchange rate movements and foreign direct investment. While many theoretical and empirical studies indicate that exchange rate movements have had a significant effect on FDI movements, their impact is found to be heterogeneous across countries and types of investment, and varies over time.

Regarding the relationship between exchange rate level and FDI, some studies focus on the impact of exchange rate movements on acquisition costs of foreign assets. For instance, Froot and Stein (1991) and Blonigen (1997) indicate that, in an imperfect capital market, the depreciation of a country’s currency might induce foreign firm to take over its domestic firms. Some other studies emphasize the impact of exchange rate movements on the profitability of foreign production. Cushman (1985) develops a general model to show that the depreciation of a foreign country’s currency might reduce the costs of foreign production in terms of the currency of the home country. In other words, the depreciation of a country’s currency might induce international capital inflows, which is supported by many empirical studies, such as Kohlhagen (1977)、Cushman (1985)、Froot and Stein (1991)、Campa (1993)、Klein and Rosengren (1994)、Campa (1994)、Dewenter (1995)、Kogut and Chang (1996)、Blonigen (1997)、Bell and Campa (1997)、Tomlin (2000) andKiyota and Urata (2004).

In contrast, Campa (1993) demonstrates that the appreciation of a host country’s currency might increase the revenue of foreign sales in terms of the currency of the home country and thus the appreciation of a host country’s currency might attract international capital inflows. Therefore, the relationship between exchange rate movements and FDI tends to hinge on the investing motives of the firms. Specifically, for a cost-oriented firm, the depreciation of a host country’s currency will stimulate FDI, while for a market-oriented firm the depreciation of a host country’s currency will deter FDI. These relationships are developed in a real-options model by Chen et al. (2006), and the empirical results from their study on the determinants of Taiwanese firms into mainland China are consistent with the perdition of the theory.

Regarding the relationship between exchange rate volatility and FDI, Previous theoretical studies demonstrate that exchange rate volatility affects FDI activity through two main channels: firms’ attitude towards risk and the option value of investment flexibility. It has been suggested that, for a risk-averse firm, higher volatility lowers the certainty equivalent value of the investing firm (Wihlborg (1978)). Hence, FDI decreases as exchange rate volatility increases. By contrast, Itagaki (1981), Cushman (1985), and Goldberg and Kolstad (1995) illustrate the importance of considering the post-FDI changes in the exposure of a firm’s profits to exchange rate risk. If the investing firm can choose to serve foreign markets via exports or FDI, then an increase in exchange rate volatility might lead the firm to substitute FDI for exports, since FDI activity reduces the exposure of its profits to exchange rate risk.

The studies mentioned above are based on the traditional investment theory which assumes that an investment decision is to be taken now or never. They neglect the option of delaying an investment. Beginning in the 1980s a real options theory has been developed to analyze investment behavior. Under the assumptions of uncertainty and irreversible investment, the real options theory emphasizes the option value of the flexibility that a firm has in possibly delaying an investment decision in order to obtain more information about the

6

future. Dixit (1989a,b) indicates that the waiting value increases as the uncertainty rises even for a risk-neutral firm. Hence, an increase in exchange rate uncertainty will defer the FDI activity of the firm. Using Dixit-Pindyck’s (1994) model, however, Darby et al. (1999) illustrate that, for a risk-averse firm, the impact of exchange rate uncertainty on the timing of FDI is ambiguous.

A limitation of Dixit-Pindyck (1994) and Darby et al. (1999) is their treatment of firms’ risk aversion. The risk aversion is incorporated into their model through a risk premium added to the private discount rate. This approach does not consider an important feature in the traditional theory that allows the exposure of the investing firm’s profits to exchange rate risk

to vary with different types of FDI.1

One limitation in Chen et al. (2010) is that they do not consider strategic interaction among investing firms in their theoretical models. Since multinational firms tend to operate under an imperfect competition environment, those firms usually have strategic interactions with their competitors. The strategic interaction among investing firms might diminish the option values of those firms and this affect their invest decision. Several recent studies has tried to incorporate game theory into real option models to investigate investment decision in imperfect competitive markets, such as Grenadier (1996, 2002), Kutatilaka and Perotti (1998), Lambrecht and Perraudin (2003), Huisman and Kort (2004), Smit and Trigeorgis (2004) and Thijssen et al. (2006).

Lin et al. (2010) develop an integrated framework of FDI under uncertainty in which a firm’s attitude towards risk and the option value of investment flexibility are incorporated simultaneously. It is shown that the relationship between exchange rate uncertainty and FDI varies with the extent of the exposure to exchange rate risk which is determined by investing motives. They find that exchange rate volatility tends to delay the FDI activity of a market-seeking firm, but it may accelerate the FDI activity of an export-substituting firm.

1 Although Chen et al. (2006) consider different motives of firms, the risk neutrality assumption in their model

makes their results same as Dixit’s analysis. The “exposure problem” also has not been discussed in their framework.

The purpose of this paper is to extend the empirical study of Lin et al. (2010) by incorporating market structure into their model in order to test the validity of the aforementioned game-theoretical option models. Firm-level data on Taiwanese investment into China will be used. The remainder of the paper proceeds as follows. Section 2 discusses our empirical methodology and model. Section 3 presents the data and empirical results. Brief concluding remarks are given in the final section.

2. Empirical methodology and model 2.1 Empirical methodology

This paper focuses on the analysis of how exchange rate volatility affects the timing of foreign entry. One widely applied method to examine the issue about timing is to conduct event history analysis. Event history analysis investigates what may happen over a time span before a certain event occurs. In our case, the event is a firm’s entry into a foreign market. The waiting time for a firm to enter a foreign market can be treated as the survival time of the firm, and the timing of entry can be treated as the timing of event occurrence.

We adopts Cox’s proportional hazard model (Cox (1972, 1975)), which imposes the condition of “hazard proportionality” and thus makes the analysis of covariates possible

without specifying a hazard function itself. The model treats each sample’s hazard rate h t i( )

as a function of a number of covariates and conceptually defines the baseline hazard h t 0( )

that is not influenced by any covariate. We define the hazard rate as the rate at which a firm invests in a foreign country by time t given that the firm has stayed in the home country until t.

Thus, the hazard function ( | x )h t i can be expressed as

(

| x , x ( )i1 2i)

0( )

ex p x(

1i x ( )2i)

h t t =h t β +α t (1)

where h t is the baseline hazard function; 0( ) β and α are coefficients; x1i and

2

8

represents i firm; subscript t represents time. th

Suppose that we have a dataset with n observations and K distinct entry times. If we sort

the sample by the order of entry times, then the partial likelihood functionLpbecomes

1 2 1j 2j x x ( ) x x ( ) 1 ( ) i i i i t n p t i j t e L e δ β α β α ′ + ′ ′ + ′ = ∈Ω =

∏ ∑

(2)where Ω( )ti is the “risk set”, which represents the number of firms that are at risk of

experiencing an entry at time ti; δ is an indicator, whose value is 0 if the sample is i

right-censored, and 1 if the sample is uncensored.2 The positive (negative) estimators βˆ

and ˆα represent the variables have positive (negative) impact on the occurrence of the

event. 3

2.2 Empirical model

Based on the theoretical framework of Lin et al. (2010) and Kulatilaka and Perotti (1998), the following empirical model is established:

[

0]

1 2 1 2 3 4 1 5 1 6 1 7 8 9 10 1 11 , 1 2 3 lo g ( ) ( ) + & i i t t t t t t t t t t t i t i i h t h t HCP HCP MS ES R R MS R ES MS ES WAGE PF MKT FUND R D γ γ σ α σ α σ α σ α α α α µ α µ α µ α α β β β − − − − = + × + + × + × + × + × + + × + × + + ++ + i +β4SIZEi+β5SIZEi*SIZEi+β6KLi +β7HTi

(3)

Here, subscript i represents th

i firm. Since Taiwanese firms were not permitted to invest in

China until 1987, the dependent variable is defined as the duration from 1987 to the year when the firm invested there. As for independent variables, in addition to the exchange rate variables and industry dummies to take into account investing motives and market competition condition, some are added as explanatory variables in order to control for some important factors that are not considered in the theoretical framework of Lin et al. (2010). The definition of these variables and their expected signs are discussed as follows (see also Table

2 If firms do not invest in the sample period but may invest in the future, then the sample is referred to as a

right-censored sample.

1) 4

t

σ :

: exchange rate volatility. According to Lin et al. (2010), while exchange rate uncertainty tends to deter the FDI activity of market-seeking firms, its impact on export-substituting firms is ambiguous. To test the validity of the theory, we define two dummy variables: 1. MS, whose value is 1 for market-seeking firms; and 0 otherwise; 2. ES, whose value is 1 for export-substituting firms; and 0 otherwise. Therefore, the expected sign

of (α α1+ 2) is negative, and that of (α α1+ 3)is positive (negative) for those export-

substituting firms with high (low) risk-aversion.

i

HCP : market competition condition. According to Kulatilaka and Perotti (1996), in a

highly competitive market, strategic interaction among investing firms might diminish the option values of foreign market entry and thus induce earlier entry. We define a dummy

variable, HCP , whose value is 1 highly competitive industries,; and 0 otherwise. Therefore, i

the expected sign ofHCP is positive. However, Kulatilaka and Perotti (1996) also indicate that i

strategic investment under uncertainty might cause strong preemptive effects due to the deterrence or commitment effect. If these effects outweigh its downside risks under certain market conditions, uncertainty may favorable to investment. In order to test the possible

non-linearity between uncertainty and FDI, we include a multiplicative term, HCPi× in the σt

regression equation.

Rt-1: one-period lagged real exchange rate of NTD versus RMB, in which nominal

exchange rates are deflated with prices of the respective countries to control for the possible movements in prices following the change in nominal exchange rates. Since it is time-consuming to make an FDI decision, the final decision might be more related to the previous exchange rate level, and thus the one-period lagged values are used. According to Lin et al. (2010), an appreciation of the host country’s currency increases market-seeking

4

10

firms’ profits in terms of the home currency and decreases those of export-substituting firms.

Therefore, the expected sign of (α α4+ 5) is positive, and that of (α α4+ 6)is negative.

t

µ : trend of exchange rate. According to Lin et al. (2010), for firms with very low

risk-aversion, an increase in µ accelerates the FDI activity of market-seeking firms and t

delays the FDI activity of export-substituting firms. By contrast, for firms with very high

risk-aversion, an increase in µ delays the FDI activity of market-seeking firms and t

accelerates the FDI activity of export-substituting firms. Therefore, if the risk-aversion of the

firms is very low, then the expected sign of (α α7+ 8)is positive and that of (α α7+ 9)is

negative. If the risk-aversion of the firms is very high, then the expected sign of (α α7+ 8) is

negative and that of (α α7+ 9)is positive.

WAGEt-1: wage rate of the foreign country relative to that of the home country. The ratio

of China’s one-period lagged real wage rate over Taiwan’s one-period lagged real wage rate is used. According to Lin et al. (2010), the expected sign of the coefficient for export-substituting firms is negative, and that for market-seeking firms is ambiguous.

MKTi: marketing intensity, a proxy variable of the sunk costs. According to Lin et al.

(2010), the expected sign of its coefficient is negative.

As for the control variables, based on the previous studies,5 the following variables are

used: profits (PF), source of funds (FUND), R&D intensity (R&D), firm’s size (SIZE), capital-labor ratio (KL), and high-tech industry dummy (HT). According to the liquidity hypothesis, since the cost of internal funds is viewed by investors to be lower than the costs of

external funds,6

5

See, for instance, Agarwal (1980), and Blonigen (2005) for literature surveys.

there is a positive relation between a firm’s internal cash flows and its

investment abroad. The profit rate (PFi,t) is used as a proxy of a firm’s internal capital, the

expected sign of its coefficient is positive. In addition, if the parent company of an investing firm can provide necessary funds, the firm is more unlikely to face financial constraint, and