行政院國家科學委員會專題研究計畫 成果報告

全球資訊網智慧型決策支援系統在個人化財務管理服務之

應用研究

計畫類別: 個別型計畫

計畫編號: NSC91-2416-H-004-014-

執行期間: 91 年 08 月 01 日至 92 年 07 月 31 日

執行單位: 國立政治大學資訊管理學系

計畫主持人: 余千智

計畫參與人員: 王行一 ,陳儷月, 林玫儀, 龔怡寧

報告類型: 精簡報告

處理方式: 本計畫可公開查詢

中 華 民 國 92 年 11 月 1 日

行政院國家科學委員會專題研究計畫成果報告

全球資訊網智慧型決策支援系統在個人化財務管理服務之應用研

究

On the Application of Web-based Intelligent Decision Support

Systems in Personalized Financial Management Services

計畫編號:NSC 91-2416-H-004-014

執行期限:91 年 8 月 1 日至 92 年 7 月 31 日

主持人:余千智 國立政治大學資訊管理學系

計畫參與人員:王行一 陳儷月 林玫儀 龔怡寧 國立政治大學資訊管理系

一、中文摘要

近年來全球資訊網、電子商務及電子

化服務等技術與應用的快速進展,對包括

金融服務業在內的各種產業帶來衝擊及機

會,如何提供線上即時、個人化、全功能

的全球資訊網個人投資理財決策支援服

務,不只是迫切的市場需求,且是一個關

鍵性的學術及實務應用課題。本研究的目

的即在提出一套全球資訊網智慧型決策支

援系統的架構及作業流程,並將此一架構

及流程應用於個人化的財務管理服務,同

時也將建置原型系統,以驗證所提架構、

流程及方法的可行性與績效。

關鍵詞:全球資訊網,個人財務規劃,投資組合管

理,智慧型決策支援系統

Abstract

The rapid advancement of the

World-Wide-Web, electronic commerce, and

electronic services technologies in recent

years has exerted impacts on and brought

opportunities to almost all industries

including financial services business. How to

provide online, real-time, personalized, and

full-function decision support services on the

web environment to facilitate personal

financial planning and investment is not only

a fast emerging market demand, but also a

critical academic as well as professional

issue. The goal of this research is to propose

a system architecture and operational process

of web-based intelligent decision support

systems for personalized financial

management services. A prototype system

will also be developed to validate the

feasibility and performance effectiveness of

the proposed architecture, process and

methodologies.

Keywords: World Wide Web, Personal Financial

Planning, Investment Portfolio

Management, Intelligent Decision Support

System

二、緣由與目的

數位經濟、電子商務及企業電子化等

的快速發展,對各種產業及企業都帶來企

業轉型、組織及流程改造的衝擊,以因應

創新、即時、客製化、全功能服務的市場

需求,金融服務業亦不例外。其中,個人

投資理財服務,包括投資規劃、建議及操

作等,是一個重點發展及競爭方向。舉凡

銀行、保險、證券、投顧等行業,甚或入

口網站、軟體及應用服務業等,都極力發

展個人財務規劃的相關產品與服務,以爭

取及維持客戶,並創造更佳的獲利機會。

然而,現有個人投資理財工具及服務系統

的功能仍屬片面且相當有限,網路服務則

大都只是提供市場上投資工具及商品的資

訊與評價指標等內容服務而已,或需要另

約時間再由專人提供直接會面的諮詢服務

等,缺乏線上、即時、個人化的投資理財

決策支援及組合方案建議功能,無法針對

每個個人財務狀況、理財習性與投資需求

等的差異,提供適合於個人需要的資產配

置建議、保險規劃及投資組合管理等整合

性財務管理服務,以致同質性過高、競爭

激烈且獲利不易。因此,如何引進相關的

資訊及管理技術以創造個人投資理財服務

的價值並掌握競爭優勢,不只是迫切的市

場需求,且是一個關鍵性的學術及實務應

用課題。

Konana et al. (2000) 等學者即指出

對發展投資理財決策支援系統的需求,以

便能有效支援自主性投資人(Do-it-yourself

investors) 選 擇 適 當 的 電 子 化 經 紀 人

(e-Brokerage)[59]。Wells and Wolfers (2000)

同樣也提出對研發能滿足個人化財務服務

需 求 的 電 腦 資 訊 系 統 的 期 待

[97] 。 而

Saatcioglu et al. (2001) 等學者則提出一個

投資理財入口網站的設計模式,以期能支

援客製化的股票選擇權投資組合決策[78]。

大體而言,一般個人投資理財服務的

內容及功能需求包括:金融商品基本及評

等資訊、投資理財知識及教學、投資資訊

資源連結及社群管理、個人投資習性及類

型分析、個人風險忍受程度評估、個人財

務資料管理、個人投資需求及條件設定與

修改、保險需求分析、保險商品搜尋評比、

保險組合方案建議、資產配置建議、投資

標的物商品搜尋及篩選、各類投資標的物

投資組合建議、投資報酬率分析、投資組

合方案確定及執行、投資組合方案績效評

估及調整維護等等。要提供能滿足上述需

求的全功能線上個人投資理財服務於一個

單一且具親和性介面的全球資訊網系統環

境,需要整合超媒體使用者介面技術、網

路資訊檢索及資料庫管理技術、財務模式

運算相關之模式庫管理技術、以及財務評

估規則推論相關之知識庫管理技術等。現

有應用軟體及實務系統所能具備或提供的

功能與服務距離此一個人化投資理財服務

的需求仍有一大段距離,而學術研究文獻

也同樣未能充分涵蓋相關的技術與管理應

用課題,或提供一套完整、適用的系統架

構及建構方法。

以現有線上實務系統而言,國內外有

關個人投資理財服務的網站雖有很多,但

能提供決策支援層次服務的則非常少,且

服務內容及功能多限於特定類型投資工具

或金融商品的市場資訊服務,舉幾個主要

的應用實例如下:

Yahoo!.Finance 網站 -- 提供美國各主要

上市公司的沿革及財務資訊、股票行情

及投資評價、第三者財務分析報告資源

連結等。(biz.yahoo.com)

PreferredCarlson 網站 -- 以房地產為搜

尋標的,可依上網者對房屋屬性(如種

類、區域、價位等)的需求及偏好,列出

可能的房屋清單,供尋屋者瀏覽及評

估。(www.preferredcarlson.com)

Prudential 網站 -- 提供結合人壽保險、

退休計劃、教育基金、醫療保險、房地

產計劃等的組合產品資訊查詢功能,稱

為個人投資及保險(Personal investments

and insurance)。(www.prudential.com)

State Farms InsWeb 網站 -- 提供三家承

保人壽保險、十家承保汽車保險、及其

他承保醫療、殘障、財產保險等保險公

司的保險商品資訊,可供消費者自行瀏

覽及比較選擇。(www.insweb. com)

DBC Online、Quote.com、Wall Street City

等網站 -- 提供各投資工具詢價服務或

技 術 指 標 追 蹤 。

(www.dbc.com,

www.quote.com, www.wallstreetcity.com)

Stock Smart、Quicken.com 等網站 -- 以

股利率、盈餘成長率及其他評價指標做

為股票評估模式輸入變數,提供股票投

資 評 等 及 排 名 結 果 的 資 訊 。

(www.stocksmart.com,www.quicken.com)

Fidelity 、 Barron’s 、 FinanCenter 、 DT

Online、CPA/PFS、Financial Planning、

MSN Money 等網站 -- 提供投資理財相

關 知 識 及 交 易 市 場 資 訊 連 結 服 務 。

(www.fid.inv.com, www.barrons.com,

www.financenter.com, www.dtonline.com,

www.cpapfs.org, financialplan.about.com,

moneycentral.msn.com)

Ernst & Young LLP

、

BerkyInfoTek.com!、Reuters、MECA 等

公 司

-- 提供個人財務規劃軟體工具

Personal Financial Counseling 、 Money

Matter$、WealthBuilder、Managing Your

Money

等

。

(www.ey.com,

www.berkyinfotek.com, moneynet.com,

www.mymnet.com)

國內外證券經紀商,如

E*Trade、寶來等

-- 提供股市行情、趨勢分析等市場相關

資訊及網路下單服務。(www.etrade.com,

www.polaris.com.tw)

Quicken InsureMarket 網站 -- 提供保險

規劃功能單元

Insurance Planner,應用簡

易的計算模式,可讓消費者就年齡、所

得、家庭狀況、健康情形、資產、現有

保險等項目填答基本問卷,並由程式導

出消費者保險需求的優先順序。另外,

限期人壽保險部份,可根據消費者的郵

遞區號、期望保額等,搜尋七家保險公

司的保險商品並列出四家保險經紀公司

的地區接觸點。消費者可自行比較保費

差異、選擇保險商品及經紀公司,並執

行線上投保。(www.insuremarket.com)

Macro*World Asset-Allocation Plan 網站

-- 可讓投資人填寫基本資料及持有資產

內容後,推估並展示有關:目前該投資

人的預期報酬與風險、未來現有投資組

合的模擬表現、及模擬表現結果與理財

目標的比較等資訊。如果預期結果與理

財目標不相符,則該網站提供投資建議

方案。投資人也可更改某些變數如退休

年齡、理財目標等,並執行 What-if 分

析。(www.wallstreetcity.com)

Vanguard 網站 -- 理財規劃系統中提供

退 休 儲 蓄 計 算 器

(Retirement Savings

Calculator)功能,可根據投資人所輸入的

目前年齡、擬退休年齡、婚姻狀況、家

庭所得、現有資產、退休目標、投資性

格、及期望壽命等資料,以模式計算出

退休時為滿足目標應備有的金額及目前

不足的金額。同時也提供包括証券、銀

行存款等應占資產百分比的資產配置建

議。(www.vanguard.com)

至於與本研究計畫相關之研究文獻則

大致包括下列層面及主題:

全球資訊網、電子商務、智慧型決策支

援系統等技術及應用層面:

(1) 電子商務的影響及企業管理決策應用

[1,24,73,103,104],

(2) 全球資訊網應用及資訊系統發展方法

[20,29,38,40,52,53,79,99],

(3) 知識庫系統及決策支援系統的整合應

用

[10,13,21,22,36,45,51,55,61,65,68,71,

80,94,101],

(4) 網際網路全球資訊網資料、知識及決策

運 算 資 源 的 整 合 應 用

[2,9,30,39,50,54,76,105],

(5) 智慧型代理人技術與電子商務的整合

及管理決策應用[8,28,32,43,70],

(6) 智慧型代理人基底的決策支援系統建

構與應用[15,18],

(7) 全球資訊網特定領域資訊系統、決策支

援 系 統 及 知 識 庫 系 統 的 發 展 與 應 用

[11,33,37,56,67,69,75,77,81,90,91,98],

(8) 網際網路開放性決策支援系統架構及

協定的建立[7,46,74,92],

(9) 超媒體技術在管理資訊系統、決策支援

系 統 及 專 家 系 統 的 整 合 應 用 等

[12,93,101]。

財務規劃及投資理財層面:

(1) 公 司 財 務 管 理 政 策 及 決 策 支 援 技 術

[3,34],

(2) 財務市場分析技術[4,58,100],

(3) 企業或個人投資組合規劃、分析及管理

模式與方法[5,6,16,47,57,64,83,86],

(4) 資產配置策略、計畫及管理模式與方法

[14,17,23,41,42,48,49,62, 84,87,96,106],

(5) 特定投資工具及商品如股票、外匯等之

篩 選 及 最 佳 化 組 合 方 法

[26,27,44,60,88],

(6) 保 險 規 劃 及 風 險 評 估 與 管 理 方 法

[31,49,85],

(7) 知識庫系統及決策支援系統在財務規

劃 與 投 資 理 財 的 應 用 方 法

[35,72,95,107],

(8) 網際網路對線上投資理財業務的影響

與應用方法[19,59,63,89],

(9) 全球資訊網財務資訊系統之建構與應

用方法等[25,63]。

由上列參考文獻之分類說明可知,針

對本計畫的整合性研究主題:個人化財務

管理服務之全球資訊網智慧型決策支援系

統,文獻中仍缺乏完整及顯著的研究成

果。綜合而言,以個人化財務管理服務為

對象的線上、全功能之智慧型決策支援系

統研究,包括系統架構、流程、發展及應

用方法等不同層面的整合性應用研究等仍

極為缺乏。因此,本研究的目的即在提出

一套全球資訊網智慧型決策支援系統的架

構及作業流程,並討論應用此一架構及流

程在個人化財務管理服務的相關課題與方

法,同時也將整合相關系統技術與方法並

建置原型系統,以驗證所提架構、流程及

方法的可行性與績效。

三、結果與討論

一個理想的消費者導向智慧型決策支

援 系 統 除 強 調 資 訊 密 集

(Information-intensive) 的 資 訊 搜 尋 功 能

外,也應能充分支援消費者決策制定流程

中的其他決策導向(Decision-oriented)及知

識導向(Knowledge-oriented)步驟,包括輔

助消費者確定需求規格,以及提供決策方

案設計及評估選擇的模式與知識運算功

能,同時也能提供決策方案執行及回饋控

制功能等。再者,電子商務環境中新興商

業交易流程的各主要階段,包括產品搜尋

及發現、條件評比及選擇、協商議價及競

標、交易確認及付款、售後服務及爭議處

理等,也需整合於消費者決策制定流程及

智慧型決策支援系統的功能結構中,且強

調 消 費 者 個 人 化 的 決 策 支 援 服 務

[75,105]。而一個個人化財務管理服務系統

應能提供的投資理財決策支援功能包括:

(1) 客戶個人基本資料管理、個人財務資料

管理,

(2) 財務市場及金融商品資訊、投資理財教

學及資訊資源連結,

(3) 投資標的物商品搜尋及篩選、交易執行

等,

(4) 個人投資習性及類型分析、個人風險忍

受程度評估、個人投資需求及條件設定

與修改,

(5) 保險需求分析、保險商品搜尋評比、保

險組合方案建議及調整、確定、執行

等,

(6) 資產配置方案建議及調整、確定、執

行、修改等,

(7) 各類投資標的物包括股票、基金、債

券、外匯等的投資組合方案建議及調

整、確定、交易執行等,

(8) 投資報酬率分析、投資組合方案確定及

交易執行、績效評估及調整維護等,

(9) 投資社群管理及通訊服務,

(10) 與保險及投資理財服務業者之間的協

商、議價、競標服務等。

基於上述系統功能特性及需求,本研

究所提出能充分提供個人化財務管理服務

之智慧型決策支援系統,其架構中包含下

列幾項應用功能結構單元:

1. 理財資訊瀏覽功能

可透過主題分類目錄瀏覽各類財務決策相

關資訊,如投資工具及商品資訊、及最適

投資產品評估說明等,也可瀏覽資產配置

方案、保險組合方案、投資組合方案及投

資報酬率分析等。

2. 理財資訊查詢功能

可使用基本資料查詢、關鍵字查詢、內容

特徵查詢等多元化查詢方法,查詢並取得

與財務決策有關之資訊、文件、個案及決

策程序等。

3. 理財決策模式及知識運算功能

可執行特定決策程序之運算過程,如最適

資產配置、個人化保單規劃、最適投資組

合等決策程序中之相關資產配置決策模式

及保額計算模式等模式運算功能,以及股

票篩選法則推論功能等。

4. 個人化財務管理功能

可透過親和性的圖形使用者介面,編輯個

人化的決策及資訊目錄畫面,建立個人的

財務及偏好資料檔案、個人理財決策需求

規格及條件檔案,也可對決策、文件、個

案等加入個人註解或設定資訊資源鏈結。

5. 投資社群管理功能

可建立具共同消費偏好的投資社群,設立

公共論壇及通訊管道,可展示個人投資需

求規格、並經由線上交談、提案討論及網

路投票等機制,形成並確定全社群或部分

群體共通的投資理財商品需求規格,以提

高團體共同投資或商品購買的議價能力。

6. 協商競標功能

可透過協商機制與特定金融商品供應商議

價,也可經由拍賣競標功能,針對社群共

通的金融商品團體購買需求規格,如團體

保單、共同基金等,邀集金融服務供應業

者參與報價及競標。

7. 交易支付功能

在投資理財決策形成後,可透過交易功能

執行決策,如進行線上保單訂購、網路證

券下單等。並可透過支付功能進行授權、

請款、轉帳付款等作業。

8. 資訊傳輸功能

可傳遞商品及交易資訊、決策運算及結果

資訊等,包括金融商品型錄、新聞消息、

訂單、合約、發票、交易及授權憑證等。

至於整體個人化財務管理智慧型決策

支援系統之組成架構,除上述特定決策應

用功能結構單元外,尚包括使用者介面及

決策程序庫、資料庫、模式庫、知識庫、

程式及軟體庫、其他決策相關文件庫及個

案庫等之基礎系統管理功能結構單元。整

體系統架構如圖

1 所示。各系統組成結構

單元的功能內容說明如下:

1. 使用者介面

使用者介面可供使用者提出查詢及決策需

求,瀏覽相關資訊及決策運算結果,可提

供回饋意見,也可選擇持續執行其他系統

功能或離開系統。

2. 特定決策支援系統應用功能

特定決策支援系統應用功能提供特定應用

領域如股票、基金、債券投資組合等相關

決策程序、資料、模式及知識之啟動、展

現與處理功能,包括上述瀏覽、查詢、決

策運算、個人化管理、社群管理、協商競

標、交易支付、資訊傳輸等各項系統應用

功能。

3. 決策程序庫

決策程序庫儲存並管理應用領域決策所需

之各個決策程序,包括決策程序說明資

料、決策程序目錄,以及執行決策程序之

應用及控制程式。投資理財相關之特定決

策程序如個人風險忍受程度評估程序、資

產配置建議程序、股票投資組合建議程序

等。

4. 資料庫

資料庫儲存並管理投資理財應用領域決策

所需之各類關聯式資料檔案、多媒體資料

檔案等,以及分散式網際網路資訊資源。

另外也可包括線上分析處理(OLAP)及資料

採掘所需之資料倉儲。同時也包括地區及

分散式資料目錄。

5. 模式庫

模式庫儲存並管理投資理財應用領域決策

所需之各類決策模式,包括最佳化規劃、

統計分析等通用決策運算模式,以及如資

產配置模式、外匯投資評估模式等之特定

決策運算模式。同時也包括模式目錄,以

及模式運算所需之模式輸入及輸出檔案。

6. 知識庫

模式庫儲存並管理投資理財應用領域決策

所需之各類知識及規則,如金融商品特徵

萃取法則、個人風險忍受程度評估及投資

偏好分類法則、股票篩選法則等。另外也

包括知識目錄,以及知識推論及運算所需

之知識輸入及輸出檔案。

7. 程式及軟體庫

程式及軟體庫儲存並管理決策支援系統功

能執行所需之各類程式及軟體,包含應用

程式目錄、軟體目錄及軟體使用說明,以

及軟體執行的驅動程式、外部程式及巨集

程式等。

8. 其他決策相關的文件庫、個案庫

文件庫儲存並管理決策相關之超媒體文件

檔案,包括預建及動態產生之

XML、HTML

檔案等。個案庫則儲存並管理決策相關之

實務個案,可供決策參考並可支援個案基

底推論(Case-based reasoning, CBR)處理,

以利消費者取得並參考相似投資者既有之

經驗及知識,設計出合適的個人投資理財

決策方案。

消費者個人的投資理財服務決策支

援流程大致包括下列步驟:

(1) 消費者輸入個人基本資料及資產負債

與收入支出等個人財務資料,

(2) 系統推估並提出投資總金額建議供消

費者調整及確定,

(3) 消費者進行線上個人偏好及習性問卷

填答,

(4) 系統進行個人投資類型分析及個人風

險忍受程度評估,

(5) 消費者輸入保險需求,

(6) 系統進行保險需求分析,搜尋評比保險

商品、並提出保險組合方案建議,

(7) 消費者調整及確定保險組合方案,

(8) 消費者設定個人投資需求、目標及條

件,

(9) 系統提出資產配置方案建議及投資報

酬率分析,

(10) 消費者調整並確定資產配置方案,

(11) 消費者進入各類投資標的物包括股

票、基金、債券、外匯等之子系統,分

別瀏覽投資標的物商品搜尋及篩選結

果,以及系統所建議之投資組合方案,

(12) 消費者調整並確認各類投資標的物的

投資組合方案,

(13) 系統執行各類投資標的物的投資組合

方案,即進行線上交易及支付程序,

(14) 消費者持續瀏覽投資組合方案績效追

蹤評估及調整建議,並修改確認,

(15) 系統持續執行各類投資標的物的投資

組合方案調整結果,以及來自消費者的

其他查詢、瀏覽、交易、調整、確認等

需求。

細部及進階的個人化財務管理智慧型

決策支援應用以下列二例說明,而大體之

投資理財服務作業流程如圖

2 所示:

1. 保險規劃決策支援部分

除保險商品搜尋功能外,尚能支援保

險消費者對風險管理程序的一般需求,包

括風險辨識、風險控制、保險需求分析(針

對個人或家庭目前及未來之財務狀況,預

估保險需求額度、並列舉適合的保險商品

種類)、保險選擇(評估及選擇滿足保險需求

且保費最低、保障最大的保險商品組合)。

以人身風險管理程序為例,消費者可透過

資料庫查詢瀏覽功能瞭解及辨識風險及財

務損失種類,並透過模式庫及知識庫決策

運算功能執行風險機率分析及保險需求金

額估計。進而可進入風險管理措施選擇階

段,透過查詢瀏覽功能瞭解損失預防措

施,並使用決策運算功能選擇適當的保險

商品組合等,以達到避險理財的目的。其

中之保險商品選擇程式,所使用到之相關

資料含消費者的身份證字號、姓名、年齡、

婚姻狀況、工作類別、薪資所得、其他所

得、所得歷史、家族病史、退休安排、投

保動機、群族類別、可支付保費金額..等,

決策模式則含保險需求模式及保費計算模

式等,決策相關知識則含保額等級評估法

則。決策運算過程先以保險需求模式(如財

務需求法模式、生命價值法模式、家計勞

務法模式等)算出保險需求,再以保額等級

評估法則推出各類險種及保額,即可用保

費計算模式計算保險費並推論出最適合的

保險商品組合建議方案,供消費者瀏覽、

評估、確認或更改需求資料重試。最後部

分則是保險執行與評估階段的支援,包括

風險管理措施的履行(如繳納保費、申請理

賠)及保險契約的變更等。而由個人化風險

管理決策支援再進一步則是團體保險社群

形成、保單協商競標等功能與程序的執

行。亦即可根據消費者的個人基本資料及

就業、生活、癖好等相關資料,連同對如

健康保險等產品險種的需求資料,透過群

組技術(Clustering techniques)依相似性分

群。接著透過消費者偏好及保險商品資料

庫的搜尋及社群服務的提案協商機制,協

助需求相似的同一消費群組獲得一個最佳

產品屬性值的理想保險需求規格方案。然

後將消費群組的健康保險需求及條件資訊

公開,由各保險公司估價並參與投標,再

選出最適合的得標保險公司議定最終保險

契約。

2. 投資組合決策支援部分

個人化投資理財決策支援服務,應能

支援消費者的資產配置決策及投資組合決

策程序等。資產配置決策考慮在各種財務

資產上的財富配置比重,不同的資產類別

如股票、債券、基金、外匯、銀行存款、

海外投資、期貨、不動產等投資標的。投

資組合決策則指對各類金融商品(如証券)

的投資選擇及組合方案。好的投資理財決

策應能考量含投資人本身條件與需求

(含

持有及預期資產、期望報酬、風險忍受程

度、投資期限、流動性限制等)及各種投資

工具的特性(含獲利性、安全性、流動性、

價格波動性等)等不同因素,同時也能因應

目標及環境的改變而動態調整投資組合。

資產配置決策及投資組合決策屬隨機最佳

化規劃及控制問題,所需使用的相關模式

及知識眾多,如一般資產配置及投資組合

之

MVP 模 式 (Mean-variance portfolio

model) 、 MLPM 模 式 (Mean-lower partial

moment model),外匯投資組合之 ARCH 模

式

(Autoregressive conditional

heteroskedasticity model)、RC 模式(Random

coefficient model),股票篩選之 CMH 模式

(Coherent market hypothesis model)及相關

啟發式法則等。

為有效建立及應用個人理財消費者決

策支援系統,本研究所採用之系統發展方

法包括[102]:

(1) 採用整合性系統發展層次結構(Layered

Structure)方法,將系統結構分為應用層

(Application Layer)、概念層(Conceptual

Layer)及實體層(Physical Layer)三層,以

作為技術類別區分及系統發展階段工作

分解的依據。

(2)

採用客戶-代理人-伺服器的多層次主-中-從(Client-Broker-Server)網路架構,規

範整體決策支援系統的分散式作業環

境,以界定全球資訊網伺服器、應用伺

服器、資料庫伺服器、決策模式庫伺服

器、知識庫伺服器、社群及通訊伺服器、

協商拍賣伺服器、以及使用者工作站等

交互運作間的功能分割與作業協定。

(3) 採用整合性超媒體物件導向方法,以節

點

-鏈結(Node-Link)模式方法,建立介

面、畫面、資訊內容、決策程序等之非

線性資源鏈結及作業流程結構;以物件

導向模式方法,界定個人化財務管理智

慧型決策支援系統之類別結構關係,賦

予消費者、決策、資料、模式、知識、

文件、資源、服務、功能、介面、畫面、

程式等一個一致性的模式表現方法。

(4) 採用智慧型代理人方法,建立網路搜尋

引擎、分類目錄、社群管理、協商、拍

賣競標、模式運算、知識運算、個人化

管理等分散式智慧型輔助及服務功能。

(5) 採用程序庫、模式庫及知識庫方法,建

立個人化投資決策程序以整合執行決策

所需之財務相關模式、知識及資料,使

決策程序之啟動到結果方案之產生得以

自動執行。

(6) 採用網際軟體資源整合方法,設定開放

性的決策支援系統軟體資源傳輸協定。

建立實體系統發展及運算資源交互作業

環境,並據以建置全球資訊網個人理財

服務原型系統。

圖

3 至圖 8 分別顯示原型系統中消費

者個人風險忍受程度評估結果、保險組合

方案建議及調整執行結果、資產配置方案

調整結果、債券投資組合方案查詢結果、

團體保險方案社群提案設定、共同基金金

融服務業者競標及出價記錄查看等之系統

輸出畫面。表

1 則顯示本原型系統與包括

Prudential、Wallstreet City、怡富理財網

(www.jfrich.com.tw) 、 聯 合 理 財 網

(money.udn.com)等網站之個人理財服務功

能比較。

四、計畫成果自評

本研究所提出個人理財服務的消費者

決策支援系統概念架構、作業流程、作業

環境及系統發展方法等,透過實體原型系

統的開發及資產配置、保險規劃及投資組

合等應用功能的執行,得以驗證其可行性

與績效。相較於現有理財網站如怡富理財

網、智富網(www.smartnet.com.tw)等的線上

理財目標試算及固定族群投資建議等,更

能滿足個人化及全功能的資產配置與投資

組合理財決策服務需求。綜合而言,本研

究計畫完成之工作項目及成果如下:

(1) 確定智慧型個人化財務管理服務決策

支援系統的整合性系統架構及全球資訊

網建置環境,系統應用服務功能含:客

戶個人基本資料管理、個人財務資料管

理,財務市場及金融商品資訊、投資理

財教學及資訊資源連結,投資社群管理

及通訊服務,個人投資習性及類型分

析、個人風險忍受程度評估、個人投資

需求及條件設定與修改,保險需求分

析、保險商品搜尋評比、保險組合方案

建議及調整、確定、執行等,資產配置

方案建議及調整、確定、修改等,投資

標的物商品搜尋及篩選、各類投資標的

物包括股票、基金、債券、外匯等的投

資組合方案建議及調整、確定、交易執

行等,投資報酬率分析、投資組合方案

績效評估及調整維護等。

(2) 建立線上即時、全功能的智慧型個人化

財務管理服務決策支援系統作業流程,

以及視覺化、交談式之使用者介面,可

大輻提升消費者在個人投資理財流程中

決策制定的效率與效益。系統作業功能

包括瀏覽、查詢、決策模式及知識運算、

個人化管理、社群管理、協商競標、交

易支付、資訊傳輸等。

(3) 建立資料庫、模式庫、知識庫之整合性

概念模式,使全球資訊網智慧型決策支

援系統之投資理財領域應用及交易決策

流程、資料庫、模式庫、知識庫等之間

具有一致性的模式表現方法。

(4) 建立個人化資產配置、風險規劃、投資

組合等不同階段的決策程序、模式與推

論法則,並建立連貫性之作業流程。

(5) 建立開放性軟體整合之實體系統網路

作業環境,並據以建置個人化財務管理

原型系統,驗證系統架構及作業流程之

可行性並顯示其實用價值。

本研究之成果整合並推展以往研究文

獻的架構與結果,為全球資訊網智慧型決

策支援系統在個人化財務管理服務之應用

提供了具體可行的架構、模式、發展方法

及作業流程,具有學術研究的深度及意

義,並具有實務應用的價值,對國家數位

經濟、電子商務、企業電子化的推展亦能

有所助益。計畫參與人員,亦獲得各項技

術發展與應用的深入及整合作業經驗。

五、參考文獻

[1] Aaron, R., Decina, M., and Skillen, R., “Electronic Commerce: Enablers and Implications,” IEEE Communications Magazine, 37(9), Sept. 1999, pp. 47-52.

[2] Abernethy, N. F. et. al., “Sophia: A Flexible, Web-Based Knowledge Server,” IEEE Intelligent Systems, 14(4), July/August 1999, pp. 79-85.

[3] Agarwal, A., Davis, J. T., and Ward, T., “Supporting Ordinal Four-State Classification Decisions Using Neural Networks,”

Information Technology and Management, 2(1), Jan. 2001, pp.

5-26.

[4] Alpar, P. and Dilger, W., “Market Share Analysis and Prognosis Using Qualitative Reasoning,” Decision Support

Systems, 15(2), October 1995, pp. 133-146.

[5] Anderson, M. H. and Prezas, A. P., “Intangible Investment, Debt Financing and Managerial Incentives,” Journal of

Economics and Business, 51(1), January 1999, pp. 3-19.

[6] Angelis, D. I. And Lee, C.-K., “Strategic Investment Analysis Using Activity Based Costing Concepts and Analytical Hierarchy Process Techniques,” International Journal of

Production Research, 34(5), 1996, pp. 1331-1345.

[7] Ba, S., Kalakota, R., and Whinston, A. B., “Using Client-Broker-Server Architecture for Intranet Decision Support,” Decision Support Systems, 19, 1997, pp.171-192. [8] Baker, A. D., Parunak, H. V. D., and Erol, K., “Agents and the

Internet: Infrastructure for Mass Customization,” IEEE

Internet Computing, 3(5), Sept.-Oct. 1999, pp. 62-69.

[9] Baker, J. H., Sircar, S., and Schkade, L. L., “Complex Document Search for Decision Making,” Information &

Management, 34(4), November 1998, pp. 243-250.

[10] Belz, R. and Mertens, P., “Combining Knowledge-Based Systems and Simulation to Solve Rescheduling Problems,”

Decision Support Systems, 17(2), May 1996, pp. 141-157.

[11] Bhargava, H., Krishnan, R., and Mueller, R., “Decision Support on Demand: On Emerging Electronic Markets for Decision Technologies,” Decision Support Systems, 19(3), 1997, pp.193-214.

[12] Bieber, M.,”On Integrating Hypermedia into Decision Support and Other Information Systems,” Decision Support Systems, 14, 1995, pp. 251-267.

[13] Bidgoli, H., “Integration of Technologies: An Ultimate Decision-Making Aid,” Industrial Management & Data

Systems, 93(1), 1993, pp. 10-17.

[14] Blake, D., “Pension Schemes as Options on Pension Fund Assets: Implications for Pension Fund Management,”

Insurance: Mathematics and Economics, 23(3), December

1998, pp. 263-286.

[15] Bose, R., “Intelligent Agents Framework for Developing Knowledge-Based Decision Support Systems for Collaborative Organizational Processes,” Expert Systems with

Applications, 11(3), 1996 pp. 247-261.

[16] Breitler, M. Hegi, S., Reymond, J. D., and Tuchschmid, N. S., ”Application of HPC to a Portfolio Choice Problem,”

Future Generation Computer Systems, 13(4-5), March 1998,

pp. 269-278.

[17] Brennan, M. J., Schwartz, E. S., and Lagnado, R., “Strategic Asset Allocation,” Journal of Economic Dynamics and

Control, 21(8-9), June 1997, pp. 1377-1403.

[18] Bui, T. and Lee, J., “An Agent-Based Framework for Building Decision Support Systems,” Decision Support Systems, 25(3),

April 1999, pp. 225-237.

[19] Carter, R. B., Strader, T. J., and Nilakanta, S., “Online Investment Banking Phase I: Distribution via the Internet and Its Impact on IPO Performance,” Journal of the Association

for Information Systems, 1-6, August 2000, pp. 1-24..

[20] Ceri, S., Fraternali, P. and Paraboschi, S., “Design Principles for Data-Intensive Web Sites,” ACM SIGMOD Record, 28(1), 1999, pp. 84-89.

[21] Chang, A. M., Holsapple, C. W., and Whinston, A. B., “A Hyperknowledge Framework of Decision Support Systems,”

Information Porcessing & Management, 30(4), 1994, pp.

473-298.

[22] Changchit, C., Holsapple, C. W., and Madden, D. L., “Supporting Managers' Internal Control Evaluations: an Expert System and Experimental Results,” Decision Support

Systems, 30(4), March 2001, pp. 437-449.

[23] Chevallier, E. and Muller, H. H., “Risk Allocation in Capital Markets: Portfolio Insurance, Tactical Asset Allocation and Collar Strategies,” Insurance: Mathematics and Economics, 16(3), July 1995, pp. 287.

[24] Cho, S., “Customer-Focused Internet Commerce at Cisco Systems,” IEEE Communications Magazine, 37(9), Sept. 1999, pp. 61-63.

[25] Chou, S. T., “Migrating to the Web: A Web Financial Information System Server,” Decision Support Systems, 23(1), May 1998, pp. 29-40.

[26] Chunhachinda, P., Dandapani, K., Hamid, S., and Prakash, A., “Portfolio Selection and Skewness: Evidence From International Stock Markets,” Journal of Banking & Finance, 21(2), February 1997, pp. 143-167.

[27] Christou, C., Swamy, P. A. V. B., and Tavlas, G. S., “Modelling Optimal Strategies for The Allocation of Wealth in Multicurrency Investments,” International Journal of

Forecasting, 12(4), December 1996, pp. 483-493.

[28] Ciancarini, P. et. al., “Coordinating Multiagent Applications on the WWW: A Reference Architecture,” IEEE Transactions

on Software Engineering, 24(5), May 1998, pp. 362-375.

[29] Cobb, M. A. et. al., “An OO Database Migrates to the Web,”

IEEE Software, 15(3), May/June 1998, pp.22-30.

[30] Corby, O. and Dieng, R., “The Webcokace Knowledge Server,” IEEE Internet Computing, 3(6), Nov.-Dec. 1999, pp. 38-43.

[31] Correnti, S., Nealon, P. A. and Sonlin, S. M., “Total Integrative Risk Management: A Practical Application for Making Strategic Decisions,” Insurance: Mathematics and

Economics, 22(3), July 1998, pp. 302.

[32] Dasgupta, P. et. Al., “MAgNET:Mobil Agents for Networked Electronic Trading,” IEEE Transactions on Knowledge and

Data Engineering, 11(4), July/August, 1999, pp. 509-525.

[33] Davis, J. G. and Sundaram, D., “PETAPS: A Prototype Decision Support System for Consumer Product Marketing and Promotion,” European Journal of Operational Research, 87(2), December 1995, pp. 247-256.

[34] Detemple, J., Gottardi, P., and Polemarchakis, H. M., “The Relevance of Financial Policy,” European Economic Review, 39(6), June 1995, pp. 1133-1154.

[35] Dirks, S., Kingston, J. K. C., and Haggith, M., “Development of a KBS for Personal Financial Planning Guided by Pragmatic KADS,” Expert Systems with Applications, 9(2), 1995, pp. 91-101.

[36] El-Najdawi, M. K. and Stylianou, A. C., “Expert Support Systems: Integrating AI Technologies,” Communications of

the ACM, 36(12), December 1993, pp. 55-65.

[37] Elofson, G. and Robinson, W. N., “Creating a Custom Mass-Production on the Internet,” Communications of the

ACM, 41(3), March 1998, pp. 56-62.

[38] Gellersen, H.-W. and Gaedke, M., “Object-Oriented Web Application Development,” IEEE Internet Computing, 3(1), 1999, pp. 60-68.

[39] Gaines, B. R. and Shaw, M. L. G., “Embedding Formal Knowledge Models in Active Documents,” Communications

of the ACM, 42(1), January 1999, pp. 57-63.

[40] Garzotto, F., Paolini, P., and Schwabe, D., "HDM--A Model-Based Approach to Hypertext Application Design,"

pp. 1-26.

[41] Gerchak, Y. and Shaun, W., “Liquid Asset Allocation Using Newsvendor Models With Convex Shortage Costs,” Insurance:

Mathematics and Economics, 20(1), June 1997, pp. 17-21.

[42] Glassman, D. A. and Riddick, L. A., “What Causes Home Asset Bias and How Should It Be Measured?” Journal of

Empirical Finance, 8(1), March 2001, pp. 35-54.

[43] Glushko, R. J., Tenenbaum, J. M., and Meltzer, B., “An XML Framework for Agent-Based E-Commerce,” Communications

of the ACM, 42(3), March 1999, pp. 106-114.

[44] Gold, S. C. and Lebowitz, P., “Computerized Stock Screening Rules for Portfolio Selection,” Financial Services Review, 8(2), 1999, pp. 61-70.

[45] Gottinger, H. W. and Weimann, P., “Intelligent Decision Support Systems, “Decision Support Systems, 8, 1992, pp. 317-332.

[46] Gregg, D. G. and Goul, M., “A Proposal for an Open DSS Protocol,” Communications of the ACM, 42(11), November 1999, pp. 91-96.

[47] Grootveld, H. and Hallerbach, W., “Variance vs Downside Risk: Is There Really That Much Difference?” European

Journal of Operational Research, 114(2), April 1999, pp.

304-319.

[48] Hobart, B. A., “Computerized Fixed Asset Management: A Guide to Implementation,” Management Accounting, 75(4), Oct. 1993, pp. 20-25.

[49] van der Hoek, J. and Sherris, M., “A Class of Non-eEpected Utility Risk Measures and Implications for Asset Allocations,”

Insurance: Mathematics and Economics, 28(1), February 2001,

pp. 69-82.

[50] Horowitz, E., “Migrating Software to the World Wide Web,”

IEEE Software, 15(3), May/June 1998, pp.18-21.

[51] Houben, G., Lenie, K., and Vanhoof, K., “A Knowledge-Based SWOT-Analysis System as an Instrument for Strategic Planning in Small and Medium Sized Enterprises,” Decision Support Systems, 26(2), August 1999, pp. 125-135.

[52] Isakowitz, T., Bieber, M., and Vitali, F., “Web Information Systems,” Communications of the ACM, 41(7), July. 1998, pp. 78-80

[53] Isakowitz, T., Stohr, E. A., and Balasubramanian, F., “RMM: A Methodology for Structured Hypermedia Design,"

Communications of the ACM, 38(8), Aug. 1995, pp. 34-44

[54] Joshi, A., Ramakrishnan, N, and Houstis, E. N., ”Multiagent System Support of Networked Scientific Computing,” IEEE

Internet Computing, 2(3), May-June 1998, pp. 69-83.

[55] Kaneda, S., Ishii, M., Hattori, F., and Kawaoka, T., “INTERFACER: A User Interface Tool for Interactive Expert-Systems,“ Decision Support Systems, 18(1), September 1996, pp. 107-115.

[56] Kannan, P. K., Chang, A.-M., and Whinston, A. B., “Marketing Information on the I-Way,” Communications of

the ACM, 41(3), March 1998, pp. 35-43.

[57] King, M. A. and Leape, J. I., “Wealth and Portfolio Composition: Theory and Evidence,” Journal of Public

Economics, 69(2), June 1998, pp. 155-193.

[58] Kocherlakota, N. R., “The Effects of Moral Hazard on Asset Prices When Financial Markets are Complete,” Journal of Monetary Economics, 41(1), February 1998, pp. 39-56. [59] Konana, P., Menon, N. M., and Balasubramanian, S., “The

Implications of Online Investing,” Communications of the

ACM, 43(1), Jan. 2000, pp. 35-41.

[60] Konno, H. and Kobayashi, K., “An Integrated Stock-Bond Portfolio Optimization Model,” Journal of Economic

Dynamics and Control, 21(8-9), June 1997, pp. 1427-1444.

[61] Kuhlmann, T.; Lamping, R.; Massow, C., “Intelligent Decision Support,“ Journal of Materials Processing Technology, 76(1-3), April 1998, pp. 257-260.

[62] Kusakabe, T., “Asset Allocation Model for Japanese Corporate Pension Fund from Liability Aspects,” Insurance:

Mathematics and Economics, 17(1), August 1995, pp. 80.

[63] Lee, E.-J. and Lee, J. K., “Haven't Adopted Electronic Financial Services Yet? The Acceptance and Diffusion of Electronic Banking Technologies,” Financial Counseling and

Planning, 11(1), 2000, pp. 49-60.

[64] Lee, H. and Hanna, S., “Investment Portfolios and Human

Wealth,” Financial Counseling and Planning, 5, 1995, pp. 147-152.

[65] Levin, N.; Zahavi, J.; and Olitsky, M., “AMOS - A Probability-Driven, Customer-Oriented Decision Support System for Target Marketing of Solo Mailings,” European

Journal of Operational Research, 87(3), December 1995, pp.

708-721.

[66] Li, E. Y., McLeod Jr, R., and Rogers, J. C., “Marketing Information Systems in Fortune 500 Companies: A Longitudinal Analysis of 1980, 1990, and 2000,” Information

& Management, 38(5), April 2001, pp. 307-322.

[67] Liao, S. H., “A Knowledge-Based Architecture for Implementing Military Geographical Intelligence System on Intranet,” Expert Systems with Applications, 20(4), May 2001, pp. 313-324.

[68] Liberatore, M. J. and Stylianou, A. C., “Toward a Framework for Developing Knowledge-Based Decision Support Systems for Customer Satisfaction Assessment: An Application in New Product Development,” Expert Systems with Applications, 8(1), January 1995, pp. 213-228.

[69] Loban, S. R., “A Framework for Computer-Assisted Travel Counseling,” Annals of Tourism Research, 24(4), October 1997, pp. 813-834.

[70] Maes, P., Guttman, R. H., and Moukas, A. G., “ Agent That Buy and Sell,” Communications of the ACM, 42(3), March 1999, pp. 81-91.

[71] Matsatsinis, N. F. and Siskos, Y., “MARKEX: An Intelligent Decision Support System for Product Development Decisions,” European Journal of Operational Research, 113(2), March 1999, pp. 336-354.

[72] Matsatsinis, N. F., Doumpos, M., and Zopounidis, C., “Knowledge Acquisition and Representation for Expert Systems in the Field of Financial Analysis,” Expert Systems

with Applications, 12(2), 1997, pp. 247-262.

[73] Messerschnitt, D. and Hubaux, J.-P., “Opportunities for Electronic Commerce in Networking,” IEEE Communications

Magazine, 37(9), Sept. 1999, pp. 95-98.

[74] Mirchandani, D. and Pakath, R., “Four Models for a Decision Support System,” Information & Management, 35(1), January 1999, pp. 31-42.

[75] O’Keefe, R. M. and Mceachern, T., “Web-Based Customer Decision Support Systems,” Communications of the ACM, 41(3), March 1998, pp. 71-78.

[76] O’Leary, D. E., “The Internet, Intranets, and the AI Renaissance,” IEEE Computer, 30(1), January 1997, pp. 71-78.

[77] Resnick, P. and Varian, H. R., “Recommender Systems,”

Communications of the ACM, 40(3), March 1997, pp. 56-58.

[78] Saatcioglu, K., Stallaert, J., and Whinston, A. B., “Design of a Financial Portal,” Communications of the ACM, 44(6), June 2001, pp. 33-38.

[79] Schwabe, D. and Rossi, G., "The Object-Oriented Hypermedia Design Model," Communications of the ACM, 38(8), Aug. 1995, pp. 45-46.

[80] Silverman, B. G., “Unifying Expert Systems and the Decision Sciences,” Operations Research, 42(3), May-June 1994, pp. 393-413.

[81] Simpson, J. Kingston, J. and Molony, N., “Internet-Based Decision Support for Evidence-Based Medicine,”

Knowledge-Based Systems, 12(5-6), October 1999, pp.

247-255.

[82] Sprague, R. H. and Carlson, E. D., Building Effective Decision

Support Systems, Prentice-Hall, 1982.

[83] Steiner, M. and Wittkemper, H. G., “Portfolio Optimization With a Neural Network Implementation of the Coherent Market Hypothesis,” European Journal of Operational

Research, 100(1), July 1997, pp. 27-40.

[84] Stevenson, S., “Emerging Markets, Downside Risk and the Asset Allocation Decision,“ Emerging Markets Review, 2(1), March 2001, pp. 50-66.

[85] Stone, M., Foss, B., and Machtynger, L., “The UK Consumer Direct Insurance Industry: A Role Model for Relationship Management?” Long Range Planning, 30(3), 1997, pp. 353-363.

[86] della Tallia, C. P., Judd, M. T., and Pattison, D. D. “GAPV: A New Approach to Joint Venture Investments,” Management

[87] Talmain, G., “On the Number of Currencies Needed to Implement the Complete Asset Market Allocation,” Journal of

Mathematical Economics, 31(2), March 1999, pp. 251-263.

[88] Tam, K. Y., Kiang, M. Y., and Chi, R. T. H., “Inducing Stock Screening Rules for Portfolio Construction,” Journal of

Operational Research Society, 42(9), 1991, pp. 747-757.

[89] Tan, M. and Teo, T. S. H., “Factors Influencing the Adoption of Internet Banking,” Journal of the Association for

Information Systems, 1-5, July 2000, pp. 1-44.

[90] Tang, H.-L., Lee, S., and Yen, D. C., “An Investigation on Developing Web-Based Executive Information Systems,”

Journal of Computer Information Systems, 18(2), Winter

1997-1998, pp. 49-54.

[91] Teich, J.; Wallenius, H.; and Wallenius, J., “Multiple-Issue Auction and Market Algorithms for the World Wide Web,”

Decision Support Systems, 26(1), July 1999, pp. 49-66.

[92] Thornett, A. M., “Computer Decision Support Systems in General Practice,” International Journal of Information

Management, 21(1), February 2001, pp. 39-47.

[93] Tung, Y. A.; Gopal, R. D., Marsden, J. R., “HypEs: An Architecture for Hypermedia-Enabled Expert Systems,”

Decision Support Systems, 26(4), October 1999, pp. 307-321.

[94] Turban, E. and Watkins, P.R., “Integrating Expert Systems and Decision Support Systems,” MIS Quarterly, June 1986, pp. 121-136.

[95] Vranes, S., Stanojevic, M., Stevanovic, V., and Lucin, M., “ INVEX: Investment Advisory Expert System,” Expert

Systems, 13(2), May 1996, pp. 105-120.

[96] Walker, D. A., “A Behavioral Model of Bank Asset Management,” Journal of Economic Behavior & Organization, 32(3), March 1997, pp. 413-431.

[97] Wells, N. and Wolfers, J.: “Finance with a Personalized Touch,” Communications of the ACM, 43(8), 2000, pp. 31-34 [98] Wierenga, B., Oude Ophuis, P. A. M., “Marketing Decision

Support Systems: Adoption, Use, and Satisfaction,”

International Journal of Research in Marketing, 14(3), July

1997, pp. 275-290.

[99] Will, U. K. and Leggett, J. J., “Hyperform: A Hypermedia System Development Environment,” ACM Transactions.on

Information Systems, 15(1), 1997, pp. 1-31.

[100] Wood, D. and Dasgupta, B., “Classifying Trend Movements in the MSCI U.S.A. Capital Market Index--A Comparison of Regression, ARIMA and Neural Network Methods,”

Computers & Operations Research, 23(6), June 1996, pp.

611-622.

[101] Yu, C. C., “HESS: a Hypermedia Expert Support System for Intelligent Decision Making,” Proceedings of the First Asia

Pacific Decision Sciences Institute Conference, June 21-22,

1996, Hong Kong, Vol. 3, pp.1201-1210.

[102] Yu, C. C., “A Hypermedia Development Process for Web Information Systems,” Proceedings of the International

Conference on Electronic Commerce 2000, August 21-24,

2000, Seoul, Korea, pp. 331-337.

[103] Yu, C. C., Yu, H. C. and Chou, C. C., “The Impacts of Electronic Commerce on Auditing Practices: An Auditing Process Model for Evidence Collection and Validation,”

International Journal of Intelligent Systems in Accounting, Finance, and Management, 9(3), Sept. 2000, pp. 195-216.

[104] Yu, C. C., “An Integrated Framework of Business Models for Guiding Electronic Commerce Applications and Case Studies,” Lecture Notes in Computer Science, Vol. 2115, 2001, pp. 111-120.

[105] Yu, C. C., ““Designing a Web-Based Consumer Decision Support Systems for Tourism Services,” Proceedings of the

4th International Conference on Electronic Commerce,

October 23-25, 2002, Hong Kong, (in CD), 14ps.

[106] Zhou, C., “Dynamic Portfolio Choice and Asset Pricing With Differential Information,” Journal of Economic Dynamics and

Control, 22(7), May 1998, pp. 1027-1051.

[107] Zopounidis, C., Doumpos, M., and Matsatsinis, N. F., “On The Use of Knowledge-Based Decision Support Systems in Financial Management: A Survey,” Decision Support Systems, 20(3), July 1997, pp. 259-277. 消費者瀏覽器 使用者介面

圖 1 消費者導向智慧型決策支援系統架構

特定決策支援系統應用功能 瀏 覽 查詢 決 策 運 算 個 人 化 管 理 社 群 管 理 協 商 競 標 交 易 支 付 資 訊 傳 遞 伺服器系統 程序庫 資料庫 模式庫 知識庫 軟體庫 資料倉儲 文件庫 個案庫圖 3 消費者個人風險忍受程度評估結果畫面

費者導向決策支援系統架構

投資金額建議及風險忍 度評估 受 填寫個人財務資料及投資 偏好,個人投資需求分析偏 個人保險需求分析及 保額建議 社群提案及討論、投票, 形成共同方案 啟動競標機制並評選 務供應商簽約執行 服 個人資產配置方案 建議、調整、執行 個人投資組合方案建議、報 酬率分析,方案調整、執行 個人資產配置、保險組合、投資組合方案等之交 追蹤管理、調整維護及執行 易 確定可運用總金額 個人保險組合方案 建議、調整、執行圖

2 個人化投資理財服務作業流程

圖 4 個人保險組合方案顯示畫面

圖 7 團體保險方案社群提案設定畫面

圖 5 個人資產配置方案調整結果顯示畫面

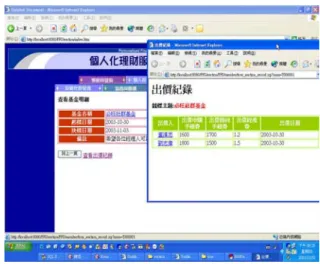

圖 8 共同基金競標及出價記錄畫面

表

1 原型系統與理財網站理財服務功能比較

系統、網站名稱╲

提供功能 原 型 系統 Prudential 網站 Wallstreet city 怡富理 財網 聯合理財網 保險組合方案 ˇ △ × × △ 風險承受度評估 ˇ ˇ × ˇ ˇ 資產配置建議方案 ˇ × △ × △ 股票投資建議方案 ˇ × ˇ × △ 債券投資建議方案 ˇ × × × × 基金投資建議方案 ˇ × ˇ ˇ ˇ 外匯投資建議方案 ˇ × × × × 完整個人理財流程 ˇ × △ × △ 完整個人理財方案 ˇ × △ △ △