Editorial: some measurement methods are applied

to business performance management

Kuen-Horng Lu*

Department of Asia-Pacific Industrial and Business Management,

National University of Kaohsiung, No. 700, Kaohsiung University Road,

Nan Tzu District, Kaohsiung 811, Taiwan, ROC E-mail: [email protected]

*Corresponding author

Chin-Tsai Lin

Graduate Institute of Business and Management, Yuanpei University of Science and Technology, Taiwan, No. 306, Yuanpei Street,

Hsin-Chu 30015, Taiwan, ROC E-mail: [email protected]

Ing-Chung Huang

Department of Asia-Pacific Industrial and Business Management,

National University of Kaohsiung, No. 700, Kaohsiung University Road,

Nan-Tzu District, Kaohsiung 811, Taiwan, ROC E-mail: [email protected]

Abstract: In today’s competitive environment, business being operationally

good is not enough. Business needs to improve their work activities and promotes their performance continuously. Therefore, business’s performance must be managed and measured. Performance measurement is the process of measuring the implementation of business’s goals. It could intensify the visibility of quantified outputs (results) that present how plans are translated into results. Performance measures that are related to the business objectives defined in the goals map are usually referred to as business strategic measures. Performance measures are gathered in what has become popularly known as Data Envelopment Analysis (DEA), Analytic Hierarchy Process (AHP), Strengths, Weaknesses, Opportunities and Threats (SWOT) and Delphi method, etc. This special issue focuses on qualitative and quantitative methods aimed at business performance management. In this Special Issue, six papers reporting recent research results are preceded by a review of literature on the main topics of performance management.

Keywords: business performance management; performance measures; Data

Envelopment Analysis; DEA; Analytic Hierarchy Process; AHP; Strengths, Weaknesses, Opportunities and Threats, SWOT; Delphi method.

Reference to this paper should be made as follows: Lu, K-H., Lin, C-T. and

Huang, I-C. (2007) ‘Editorial: some measurement methods are applied to business performance management’, Int. J. Business Performance

Management, Vol. 9, No. 1, pp.1–6.

Biographical notes: Dr. Kuen-Horng Lu is a Professor in the Department of

Asia-Pacific Industrial and Business Management. He received his PhD from the Institute of Management Science, National Chiao Tung University. His current research interests are performance management, collaborative planning, forecasting and replenishment. He has published several papers in International

Journal of Electronic Business Management, Quality Engineering, International Journal of Information and Management Sciences, International Journal of Libraries and Information Services, Journal of Management and System, Quality World Technical Supplement, Production and Inventory Management Journal, etc.

Dr. Chin-Tsai Lin is a Professor and the President of Yuanpei University of Science and Technology. He received a BS in Mathematics from Tamkang University, an MA in Mathematics from Northeast Missouri State University, and a PhD in the Institute of Management Science, National Chiao-Tung University. He is the Member of the Operations Research Society of Taiwan. His current research interests are in the areas of decision analysis, grey system and optimisation theory and applications.

Dr. Ing-Chung Huang is the President and a Professor in the Department of Asia-Pacific Industrial and Business Management. He received his PhD from the Department of Business Management, Sungkyunkwan University, Korea. His current research interests are retention, mobility, human capital and signalling model. He has published several papers in International Journal of

Manpower, International Journal of Management, Public Personnel Management, Tourism Management, Journal of Advanced Nursing, etc.

1 Introduction

When a manager declared that ‘we did well’, how can anyone detect whether the entire organisation is benefited overall from whatever that department did when it should supposedly ‘did well’? How does the manager know how much of that department’s work and outcomes advanced their organisation towards realising their target and how much was errant work on less relevant pursuits? One way to answer these questions is to improve the organisation’s measurement system itself. Performance measures that are related to the business objectives (targets) defined in the strategy map are usually referred to as business performance measures (Catherine and Joe, 2003). Performance measurement could bring objectivity and balance to the process of making spending/investment and input/output decisions. It provides explicit linkages between strategic, operational and financial objectives. Through performance measurement, it could communicate these linkages to managers and employee teams in a way they can comprehend. Thereby managers could empower employees to act rather than cautiously hesitate or employees do not need to wait for instructions from their managers. It becomes an automatic and spontaneous mechanism rather than an accounting policy control weapon (Gary, 2004).

How do you know if your organisation’s measures are driving the right way/action? What you measure you can likely control and what you control you can improve.

Thus, accurately developed business performance measurement methods/systems will increase the likelihood that they are. With the measurement methods/systems, performance will be monitored based on the results of measurement. Hence, business needs more financial and non-financial measurement reports during the management period, not at the end of the period.

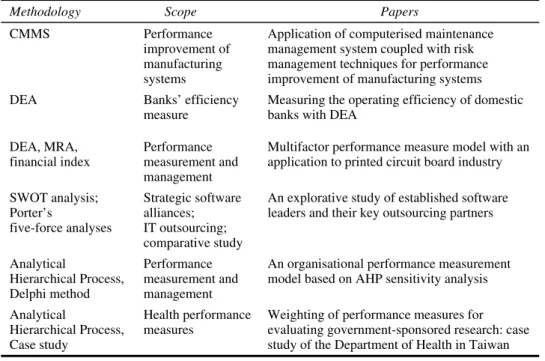

The special issue focuses on ‘Some measurement methods are applied to business performance management’, and six papers reporting recent research results are preceded by a review of literature on the main topics of business performance management. This review is intended as an introduction to the issue. According to the topics of interest, we marshal the six papers and list on the Table 1. The scope of these papers are, apply a Computerised Maintenance Management System (CMMS) coupled with risk management, measure the operating efficiency, construct a multifactor performance measure model, establish outsourcing partners, performance measurement and management, weighting of performance measures. The methodologies of these papers are CMMS, case study, Data Envelopment Analysis (DEA), Statistics Analysis, Analytical Hierarchical Process (AHP), Strengths, Weaknesses, Opportunities and Threats (SWOT) Analysis and Delphi method.

Table 1 Scope and methodology among the seven papers

Methodology Scope Papers

CMMS Performance improvement of

manufacturing systems

Application of computerised maintenance management system coupled with risk management techniques for performance improvement of manufacturing systems

DEA Banks’ efficiency

measure

Measuring the operating efficiency of domestic banks with DEA

DEA, MRA, financial index

Performance measurement and management

Multifactor performance measure model with an application to printed circuit board industry SWOT analysis; Porter’s five-force analyses Strategic software alliances; IT outsourcing; comparative study

An explorative study of established software leaders and their key outsourcing partners

Analytical Hierarchical Process, Delphi method Performance measurement and management

An organisational performance measurement model based on AHP sensitivity analysis Analytical

Hierarchical Process, Case study

Health performance measures

Weighting of performance measures for evaluating government-sponsored research: case study of the Department of Health in Taiwan

2 The methodologies

CMMS is an effective tool for practicing company wide maintenance functions that provides necessary maintenance related data to assess the current performance level of production machines. Based on the computer generated customised reports, causes of machine failures and maintenance delays are analysed using the risk management techniques after which necessary corrective actions are taken to reduce cost.

The DEA is a technical efficiency measure of the multiple-output/multiple-input developed by Farrell (1957). It is a non-parametric linear programming technique that computes a comparative ratio of outputs to inputs for each unit (bank), which is reported as the relative efficiency score. DEA optimises each individual observation with the objective of calculating a discrete piecewise linear frontier determined by the set of Pareto-efficient DMUs. Using this frontier, DEA computes a maximal performance measure for each DMU in relation to all other DMUs. Each DMU lies on the efficient (external) frontier or can be enveloped within the frontier. The DMUs that lie on the frontier are the best practice institutions and retain a value of 1. Those enveloped by the external surface are scaled against a convex combination of the DMUs on the frontier facet closest to it and have values somewhere between 0 and 1.

The SWOT analysis is an important tool in understanding both internal and external strengths and weaknesses of a business organisation. The analysis enables learning about a company’s competencies and areas that can be improved including becoming familiar with its objectives, business plans and decision-making capabilities. It also makes us look at the positives and negatives of the industry and the company itself. The reason to present their SWOT side-by-side was to provide an overall perspective of how these companies, working together as global partners, are leveraging their competencies and overcoming their weaknesses and also dealing with challenges and opportunities they are facing in the marketplace.

The Delphi method accumulates and analyses the results of anonymous experts that communicate in written, discussion and feedback formats on a particular topic. Anonymous experts share knowledge skills, expertise and opinions until a mutual consensus is achieved (Sung, 2001). The Delphi method consists of five procedures (a) select the anonymous experts

(b) conduct the first round of a survey

(c) conduct the second round of a questionnaire survey (d) conduct the third round of a questionnaire survey and (e) integrate expert opinions and to reach a consensus.

Steps (c) and (d) are normally repeated until a consensus is reached on a particular topic (Sung, 2001). Results of the literature review and expert interviews can be used to identify all common views expressed in the survey. Moreover, step (b) is simplified to replace the conventionally adopted open style survey; doing so is commonly referred to as the modified Delphi method (Sung, 2001).

The Analytic Hierarchy Process (AHP) is also a measurement theory that prioritises the hierarchy and consistency of judgemental data provided by a group of decision makers. AHP incorporates the evaluations of all decision makers into a final decision, without having to elicit their utility functions on subjective and objective criteria, by pairwise comparisons of the alternatives (Saaty, 1980, 1996). Conceptually, AHP is only applicable to a hierarchy that assumes a unidirectional relation between decision levels. The top level of the hierarchy is the overall goal for the decision model, which decomposes to a more specific level of elements until a level of manageable decision criteria met (Meade and Sarkis, 1999). Yet, the strict hierarchical structure may need to be relaxed when modelling a more complicated decision problem that involves interdependencies between elements of the same cluster or different clusters.

3 Summary of the papers

In the first paper, ‘Application of computerised maintenance management system coupled with risk management techniques for performance improvement of manufacturing systems’, Karuppuswamy et al. study performance level of machines, software development, implementation of CMMS and effects of implementation in an automotive radiator manufacturing organisation located in Tamilnadu, India.

In the second paper, ‘Measuring the operating efficiency of domestic banks with DEA’, Lu et al. employed the CCR model of DEA and the slack variable analysis to evaluate the operating efficiency of the domestic banks in Taiwan from 1998 to 2004. The operating efficiency of domestic banks was measured using interest expenses, fixed assets, deposits and number of employees as input variables. Interest income, non-interest income, investments and loans were used as the output variable. The results revealed significant differences in the average of fixed assets, deposits and loans between the high and low efficiency groups. This study found that the Non-Performing Loans/Gross Loans (NPL/GL) ratio of the high efficiency group is significantly lower than that of the low efficiency group. This study also found room for improvement in non-interest income and investments in each year and made suggestions for banks to adjust all the variables in order to enhance their overall operating efficiency.

In the third paper, ‘Multifactor performance measure model with an application to printed circuit board industry’, Wu presents an empirical investigation where financial index is considered to measure the printed circuit board performance and the DEA was utilised to derive the efficiency and multiple regression analysis to disclose the effects. The inputs as the independent factors are current assets, the number of employees, inventory investment and operating expenses used in the analysis while the outputs as the dependent factors are sales and gross margin.

In the fourth paper, ‘An explorative study of established software leaders and their key outsourcing partners’, Kumar uses SWOT, financial performance data and Porter’s five-forces analyses show how Indian IT and Software companies (Infosys, Wipro and Satyam) have been able to maintain dual role of competitors and IT outsourcing partners of Microsoft and Oracle.

In the fifth paper, ‘An organisational performance measurement model based on AHP sensitivity analysis’, Wu et al. propose an AHP sensitivity analysis based to evaluate organisation performance of hospitals. The relative weights of evaluative criteria are determined using the AHP sensitivity analysis, followed by ranking of the hospitals for decision makers to evaluate in related medical sectors to evaluate. The AHP sensitivity analysis-based decision-making method to construct an evaluation method can provide decision makers or administrators of hospital with a valuable reference for either evaluating the organisational performance.

In the sixth paper, ‘Weighting of performance measures for evaluating government-sponsored research: case study of the Department of Health in Taiwan’, Lin et al. use AHP to calculate the weighting of performance measures and a case study involving the Taiwanese Department of Health was used to explain the process.

Acknowledgements

Thanks to the reviewers for their candid and strict but friendly comments to improve the quality of the contributions. Most of all, we appreciate all the authors’ efforts in making

this Special Issue a precious publication. Finally, we would like to thank Dr. Dorgham and Inderscience Publishers, for inviting us to guest edit this special issue and for creating the opportunity to publish a journal.

References

Catherine, S. and Joe, S. (2003) Form Cost to Performance Management, John Wiley & Sons, Inc. Farrell, M.J. (1957) ‘The measurement of productive efficiency’, Journal of the Royal Statistical

Society, Vol. 120, pp.253–281.

Gary, C. (2004) Performance Management – Finding the Missing Pieces (to Close the Intelligence

Gap), John Wiley & Sons, Inc.

Meade, L.M. and Sarkis, J. (1999) ‘Analyzing organizational project alternatives for agile manufacturing processes – an analytical network approach’, International Journal of

Production Research, Vol. 37, No. 2, pp.241–261.

Saaty, T.L. (1980) The Analytic Hierarchy Process, McGraw Hill Publications.

Saaty, T.L. (1996) Decision Making with Dependence and Feedback: The Analytic Network

Process, Pittsburgh: RWS Publications.

Sung, W.C. (2001) ‘Application of Delphi method, a qualitative and quantitative analysis, to the healthcare management’, Journal of Healthcare Management, Vol. 2, No. 2, pp.11–19.