行政院國家科學委員會補助專題研究計畫成果報告

※※※※※※※※※※※※※※※※※※※※※※※※※

※ ※

※ BOT 計畫風險分析之研究 ※

※ ※

※※※※※※※※※※※※※※※※※※※※※※※※※

計畫類別:þ個別型計畫 □整合型計畫

計畫編號:NSC 89-2211-E-009-024-

執行期間: 88 年 8 月 1 日至 89 年 7 月 31 日

計畫主持人:馮正民教授

共同主持人:

本成果報告包括以下應繳交之附件:

□赴國外出差或研習心得報告一份

□赴大陸地區出差或研習心得報告一份

□出席國際學術會議心得報告及發表之論文各一份

□國際合作研究計畫國外研究報告書一份

執行單位:國立交通大學交通運輸研究所

中 華 民 國 89 年 10 月 5 日

行政院國家科學委員會專題研究計畫成果報告

BOT 計畫風險分析之研究

計畫編號:NSC 89-2211-E-009-024

執行期限:88 年 8 月 1 日至 89 年 7 月 31 日

主 持 人:馮正民 國立交通大學交通運輸研究所

計畫參與人員:康照宗

國立交通大學交通運輸研究所博士候選人 一、中文摘要 本研究目的係以 BOT 特許公司群體決 策觀點,探討 BOT 特許契約之風險特性。 在考量群體內部談判者有無討論情形下, 對不確定性因素進行風險衡量,以確認風 險事件、主要風險事件及次要風險事件。 本研究以風險及效用理論為基礎,以數學 解析方法構建談判者效用及談判群體效用 模式,並研擬求解方法,同時以範例分析 方式進行模式之測試。經測試結果顯示, 在無討論情形下,若事件之群體總計效用 值小於效用期望值時,此事件即屬風險事 件;反之,事件為非風險事件。由範例分 析結果顯示,特許期限為 BOT 特許公司進 行談判時之主要風險事件,匯率為次要風 險事件。因此,特許期限應為 BOT 特許公 司與政府進行特許契約談判時之首要議 題。而在有討論情形下,本研究採動態多 目標規劃方式進行事件之風險衡量,就所 舉範例之 6 個事件而言,談判者彼此之間 經過討論後,特許期限與匯率不再成為風 險事件。經由本研究範例分析顯示,本研 究所發展之效用衡量模式具有可用性。 關鍵詞:BOT、風險衡量、風險確認、談 判群體、討論、效用相依 Abstr actThe purpose of the study is to explore the characters of risk of the BOT concession contract from the viewpoint of group decision-making. Considering the discussion behavior among the negotiators, this study develops the utility function of negotiators, group aggregation utility function, dynamic multi-objective programming, and iterative algorithm to evaluate the uncertain factors of BOT concession contract, which based on the

utility, risk, and BOT theory. The numerical example shows that the concession period is main risk event, the money exchange rate is secondary risk event, and other events are non-risk event under the independent utility condition among the negotiators. The concession period and money exchange rate could become non-risk events after the discussion among negotiators, which shows that the models of this study developed would be applied to measure the risk of BOT projects in transportation field.

Keywords: BOT, Risk measurement, Risk identification, Negotiation team, Discussion, Dependent utility.

二、緣由與目的

BOT (build, operate and transfer)係交 通基礎建設民營化方式之一。由於 BOT 計 畫具備特許期限長、不確定性因素多、特 許企業聯盟參與廠商多、投入資本龐大以 及融資風險高等特色,所以政府採用 BOT 方式之理由,除兼具考量減輕財政困窘, 藉用民間技術與管理效率之外,更重要的 是在尋找風險分擔對象。對 BOT 特許公司 而言,特許契約談判成為風險分擔重要手 段之一,藉由契約談判來達到風險移轉, 但是欲達特許契約之風險移轉,前題有賴 風險衡量與風險確認之分析工作。按 BOT 理論〔7〕,特許契約內所存在之不確定性 因素可藉由風險衡量方法,達到尋找風險 與非風險因素以及判斷主要風險與次要風 險,完成風險移轉與規避管理措施。此風 險衡量方法,按文獻可分定性分析與量化 分析兩種,BOT 計畫之風險定性分析主要 論述 BOT 計畫之風險種類,如政治風險、 商業風險、法規變動風險、興建完工風險 及營運風險等〔5,7〕,但是此種定性風險

分析並無法有效說明風險水準,風險如何 產生以及如何確認主要風險及次要風險。 定量風險分析方法如統計分析、財務分 析、經濟效用及專家權重方法[4],這些方 法已廣泛運用於交通運輸、管理與投資領 域。效用理論[1,3]除可衡量風險與不確定 性因素外,亦可反應決策者風險偏好行 為,同時該值介於 0 與 1 之間,具備方便 判斷之優點。 由文獻可知,風險定性分析欠缺數據 佐證,無法得知風險水準;定量分析雖具 彌補定性分析的缺點,但仍有許多限制, 如財務風險分析[2]無法放寬資金流量假設 條件,專家權重法[4]無法知道決策者風險 偏好且評估體系不可以一體適用。 由文獻顯示[5,6,7],BOT 計畫之風險 衡量主要是由談判群體內之談判者或專家 們,針對不確定性因素進行衡量,此風險 衡量過程涉及專家(或決策者)風險偏好態 度[3]及不確定性因素之間獨立與否有關, 在此兩個因素下可以構成四種情境:1.風 險因素及決策偏好皆獨立,2.風險因素不 獨立,但決策偏好獨立,3.風險因素獨立 但決策偏好不獨立,4.風險因素及決策偏 好皆不獨立,第一種情境即所謂確定性風 險分析,其餘則為非確定性風險分析。 本研究目的即是考量風險偏好態度與 風險因素獨立與否之架構下,以數學解析 方法來構建 BOT 計畫之風險衡量模式,藉 以求解風險、主要風險事件、次要風險事 件,同時兼考慮談判者風險偏好態度。 三、研究內容與成果 (一)、研究內容項目 本研究內容主要共分七個步驟,包含 研究問題定義、文獻回顧與評析、風險定 義、構建談判者風險衡量模式、構建談判 群體風險衡量模式、簡例測試及結論與建 議。本研究方法以 BOT 理論為架構,效用 及風險理論為分析工具基礎,利用數學解 析方式推導談判者效用函數及談判群體效 用函數,以及研擬求解方法,並分別利用 SAS 統計軟體與 Turbo Pascal,撰寫程式, 進行效用函數與風險衡量之求解。 在簡例分析方面,本研究係假設 BOT 特許公司談判群體有 6 位談判者,並考量 談判者彼此之間有討論與無討論兩種情 形;同時假設該公司於特許期限內面臨用 地取得、銀行融資信款利率、銀行折扣率、 特許期限、費率管制及外匯之 6 個事件(或 不確定性因素),由此 6 位談判者對此 6 個 不確定性因素進行風險衡量。 (二)、研究成果 經由本研究所發展之談判者效用衡量 模式、談判群體效用相依模式及求解法, 所得到結果如下: (1).在假設事件獨立、談判者效用獨立及談 判群體追求風險最小化之情境下,推得 關鍵風險水準為所有風險事件之效用 期望值。另由範例分析得知,特許期限 與匯率屬於風險事件;銀行融資信用貸 款利率、費率管制、用地徵收與折扣率 屬非風險事件。其中,特許期限屬主要 風險事件,匯率屬次要風險事件。 (2).在假設事件獨立,談判者效用不獨立情 境下,談判群體對此 6 個事件之風險衡 量結果,呈現特許期限、匯率、銀行融 資信用貸款利率、費率管制、用地徵收 與折扣率之事件皆屬非風險事件。 (三)、討論 本研究除獲得上述研究成果,並歸納 以下課題可供後續研究。 (1).在效用獨立狀態下,個別談判者之效用 風 險 偏 好 態 度 對 談 判 者 之 風 險 有 影 響,但是當談判者彼此之間存有互動關 係,個別談判者風險偏好態度對群體效 用影響程度是否會展現出來? (2).影響談判者彼此之間的互動因素,除內 部互動外,尚有諸如談判者自我學習能 力、資訊充足與否等因素。此外,外部 環境因素變動對內部談判者之影響,這 些因素改變對模式發展有何改變是值 得思考? (3).迴歸模式雖可構建談判者偏好函數,但 只能反應談判者之效用線性函數或多 元線性函數。惟在實際狀態下,談判者 效用函數可能存在非線性函數形態,此 非線性效用函數如何引入談判者彼此 之間討論模式中,可為後續發展議題。 (四)、研究成果發表 本研究成果部份已發表或投稿於國內

外相關學術期刊,茲臚列如下。

1. Cheng-Min Feng and Chao-Chung Kang (1999), "Risk Identification and Measurement of BOT Projects," Journal of

the Eastern Asia Society for

Transportation Studies, No. 4, Vol. 4, pp. 331-350.

2. Cheng-Min Feng, Chao-Chung Kang and Gwo-Hshiung Tzeng, "Applications of Group Negotiation to Risk Assessment of BOT Projects," submited to Transportation Planning and Technology, 2000.

3. 馮正民、康照宗,「BOT計畫談判群體之 風險衡量」,運輸 計畫 季刊(29卷第四 期,即將刊登),民國89年。 4. 馮正民、康照宗,「在談判者效用互動下 之風險衡量-以BOT計畫之用地取得事 件為例」,運輸計畫季刊(已接受),民國 89年。

5. Cheng-Min Feng and Chao-Chung Kang, "The risk assessment for the BOT Negotiation team: The dynamic utility model," submited to 9th The World Conference on Transportation Research (2001).

五、參考文獻

[1].Bose, U., Davey, A. M., and Olson, D. L., "Multiattrinute Utility Methods in Group Decision-Making: Past Applications and Potential for Inclusion in GDSS", Omega, International Journal of Management Science, Vol. 25, No. 6, 1997, pp.691-706. [2]Buhlmann, H., Mathematical Methods in

Risk Theory, Springer-Verlag, 1996. [3]Keeney, R. L. and Raiffa, H., Decisions

with Multiple Objectives Preferences and Value Tradeoffs, Cambridge University Press, 1993.

[4]Mustafa, M. A. and Al-Bahar, J. F., "Project Risk Assessment Using the Analytic Hierarchy Process", IEEE Transactions on Engineering Management, Vol. 38, No.1, 1991, pp. 46-52.

[5]Philip, N., "Allocation of Risks in BOT Projects", The High Speed Rail BOT Workshop, Taipei, Taiwan, 1995.

[6]Tiong, L. K., "BOT Projects: Risks and Securities", Construction Management

315-328.

[7]Walker, C. and Smith, A. J., Privatized Infrastructure: the Build Operate Transfer, Thomas Telford Publications, 1996.

Journal of the Eastern Asia Society for Transportation Studies, No. 4. Vol. 1, pp.331-350

RISK IDENTIFICATION AND MEASUREMENT OF BOT PROJ ECTS

By

Cheng-Min Feng

&

Chao-Chung Kang

Institute of Traffic and Transportation

National Chiao Tung University

114, 4F, Sec.1, Chung Hsiao W. Rd. Taipei 100, Taiwan

Fax: 886-2-23120082, E-Mail:[email protected]

RISK IDENTIFICATION AND MEASUREMENT OF BOT PROJ ECTS Cheng-Min Feng Chao-Chung Kang

Professor and Chairman Ph, D. Student

Institute of Traffic and Transportation Institute of Traffic and Transportation National Chiao Tung University National Chiao Tung University 114, 4F, Sec.1, Chung Hsiao W. Rd. 114, 4F, Sec.1, Chung Hsiao W. Rd 100, Taipei, Taiwan 100, Taipei, Taiwan

Fax: 886-2-23120082 Fax: 886-2-23120082 E-Mail:[email protected] E-Mail:[email protected]

Abstr act: The purpose of this paper is to analytically measure and rank risk of BOT projects for decision making under an uncertain environment. The individual and group multi-attribute risk utility functions in the risk measurement model are developed based on multiattribute decision making and utility theorems. The preference of the negotiator is considered in the multiattribute risk utility function. The risk event is obtained by the model when the group risk utility value is smaller than the expected risk utility value. Futhermore, the critical risk event is obtained when the group multiattribute risk utility value is not less than the expected utility. In addition the risk measurement model provides an approach to quantify, identify and find critical risk, and to incorporate the preference of the decision-maker in order to share risk under BOT negotiation.

Key Words: BOT; risk identification; critical risk; risk measurement; uncertainty

1. INTRODUCTION

Transportation infrastructure development projects have the following characteristics: large civil works budget, substantial land acquisition over a large area, long construction time frame, large labor force, complex internal government coordination, and multi-national construction/design teams. Few transportation development projects are profitable or self-financing on the basis of user fees only, because of complicating factors such as high capital cost, lengthy construction period with no revenues, and low to moderate fare level favored by government. BOT (Build, Operate and Transfer), one method of privatization, is an approach where the private sector is given a concession to design, construct, finance, manage and operate a project that would normally be built and operated by the government, and transfers ownership of the project back to the government at the end of the concession period. Some important reasons for governments to use the approach are to reduce the government’s financial burden, to use the private sector’s technological know-how, management skills and capital, and to transfer most of the project risks to the private sector.

Since both the government and private sector will take part in a BOT project, the complex contractual negotiation requires considerable cost and time and becomes an important subject of BOT projects. Identification and measurement of risk is fundamental to risk allocation and sharing, which is the basis of contractual negotiation between the government and concession company (Tiong, 1992, 1995, 1996, 1997; Sidney, 1996; Walker and Smith, 1996). Normally, the government wants to transfer most of risk to private sector while the concession company expects to reduce its exposure to risk (Levitt, et al. 1980). Philip (1995), Nicole (1995), Tiong (1990, 1995), and Walker and Smith (1996) have discussed different types of risks BOT projects are exposed to, but risk measurement and risk identification are not explored.

commercial risks, legal risks, construction/completion risks, operation risks, etc. How to measure the degree of risk? and how to distinguish between major and minor risk? are the issues this paper will explore. Tiong (1990, 1995) and Tiong and Yeo (1992) have shown that risk analysis is an important issue for BOT projects particularly during the period of bidding, contract negotiation and risk management. Hwang (1995) has employed the notion of property rights to elucidate the essence of BOT projects, and to illustrate their optimal risk level by means of transaction cost and probability distribution. The results show that the optimal risk of the investment is in positive, indeterminable, or negative relationship to the investment rate of return and that the BOT contract is a non-zero-sum game which is completely different from the zero-sum game. They also show the different relationship between risk and investment return but do not show what level of risk is critical. William and Crandall (1982) considered the attributes of risks, suggesting that the risk measurement of infrastructure projects must consider the attributes of risk events. The risk negotiation was affected by risk attributes and the negotiator’s preference (Seo and Sakawa, 1985, 1990). Following the concepts of Seo and Sakawa, this paper will focus on risk measurement and risk identification.

Quantitative and qualitative methods have been used to discuss or measure risk, in past research. Financial risk analysis (Cuthbertson, 1996), utility analysis (Jia and Dyer, 1996; Seo and Sakawa, 1984, 1985, 1990), statistical analysis (Louis, 1990; Jaselskis and Russell, 1992; Ronald, 1990), and expert investigation (Mustafa and Al-Bahar, 1991) were used to analyze risk in the quantitative analysis field. The indices in financial risk analyses, such as the NPV, B/C ratio and IRR, have been widely used for measurement of financial conditions, but they have difficulty estimating future cash flow. Therefore, financial risk analysis is properly applied to evaluate only short-term projects with a certain environment. As for the BOT project with high uncertainty and with a long concession time, it is difficult to accurately estimate cash flow (Sidney, 1996). In addition, the major problem is to determine what level the risk of loss is? Is it 1 million dollars or 1 billion dollars? This problem is hard to answer by NPV. Although the B/C and IRR ratio have an index value from 0 to 1, the index value cannot reflect the different levels of risk for different events. Buhlman (1996), Ronald (1990), Louis (1990), Jia and Dyer (1996), and Hwang (1995) use the statistical approach to measure risk. The expected value is obtained where the risk probability distribution has a supposed specific distribution. We think the problem lies in what kind of distribution can fit the probability for BOT projects with thirty years concession time, as well as what type of independent or dependent relationships among the risks will lead to measurement error in expected value of loss. As for the utility approach, it is liable to be applied on certainty or uncertainty, and it cannot estimate future cash flow. The approach is especially suited to considering the negotiator’s preference in order to reflect the risk preference during contract negotiation (William and Keith, 1982; Seo and Sakawa, 1984, 1985). Also, the utility approach easily judges with the value between 0 and 1. In addition, Seo and Sakawa have constructed a risk utility function and introduced the fuzzy concept into risk analysis so as to render it more fitting to uncertain negotiation behavior. Seo and Sakawa (1985, 1990) have focused on the preference change for the decision maker’s behavior, but they have not defined the risk by using the utility theorem. Jia and Dyer (1996) have developed risk measurement as R(X)=−E[u(X−X)], and this study provides the concept of a negative expected utility in preference. The u(X−X) is a normalization value in mean, where X is a probability distribution and R(X) is a risk measure, but the equations do not consider the stability in measuring risk for factors deriving from different risks, events, attribute samples, etc. In addition, the normalization value inX−X results in a positive or negative value, and thus, R(X) value will not hold to

only one value.

Expert investigation is a method to measure risk and the AHP method has been used to evaluate risk in criteria construction (Mustafa and Al-Bahar, 1991). The AHP approach captures the weight value from project experts, engineers or project managers and then, based on the weight of experts and performance value, measures risk value. Nonetheless, the weight and performance value obtained from AHP can hardly demonstrate genuine risk. Moreover, there are different risks for each construction project, the criteria and goals have different importance and hence, the hierarchical structure alone can't indicate the unique conditions of the event.

The purpose of this paper is to analytically identify and measure risk, and to determine the critical risk for the government or BOT concession company. In order to take preference and risk attributes into account, this paper uses multiattribute decision making and utility theorem to construct a multiple attribute utility function to illustrate the measurement of risk, identification of risks and critical risk events

The remainder of this paper is organized as follows: section 2 describes the problem, defines the risk and uncertainty, and develops the multiattribute risk utility function; section 3 develops the group utility function; section 4 analyzes the risk of the BOT contract; and conclusions are made in the final section.

2. MODEL DEVELOPMENT

In this section, we will describe the problem of this study, define the risk and uncertainty, and develop the individual risk utility function in order to establish a group negotiation risk utility function.

2.1 The Problem Descr iption

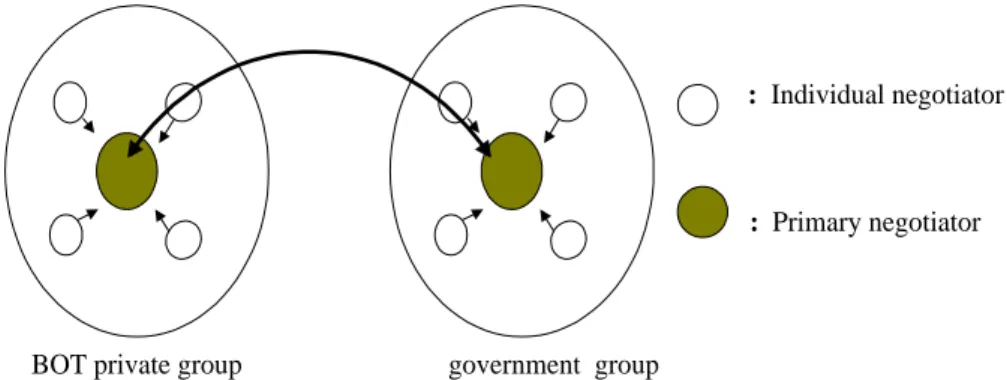

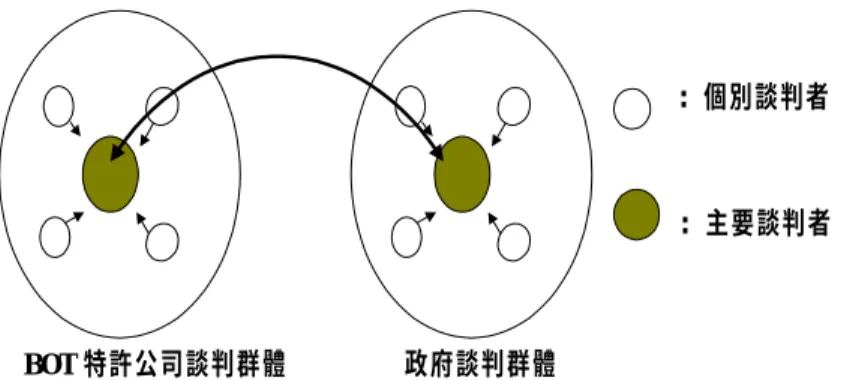

An Airport-Link Rapid Transit project between CKS Airport and Taipei city will be undertaken by BOT approach in Taiwan. The BOT concession company and government are in contract negotiation for this BOT project as bidding for this transportation infrastructure project recently finished. There are two groups taking part in negotiations, one is the government group and the other is the BOT private group. The government group includes some individual negotiators from other government departments, such as the MOTC (Ministry of Transportation and Communications), EPA (Environment Protection Administration), city government, etc. Also the BOT private group has some individual negotiators including lawyers, financial consultants, participators, participant companies, etc. It must be clarified here, that the two primary negotiators of this contract are groups rather than individuals (see Figure 1). The conditions of contract must be acceptable to both parties, otherwise, the BOT project will be terminated.

In the past, most researches qualitatively identify risks from events, however, risk and uncertainty should be strictly treated different. In addition, what are the critical or important risk items should also be a main issue for negotiators during the period of bidding, negotiation and risk mitigation. This paper aims at developing an approach to decompose the set of event into the set of uncertainty and risk, and furthermore to decompose the set of risk items to critical risks and general risks (see Figure 2).

Figure 1. Primary Negotiators and Individuals

: Individual negotiator

: Primary negotiator

BOT private group government group

N E E E Μ 2 1 Event Uncertainty Risk Critical Risk General Risk Figure 2. Event, Uncerrtainty, Risk and Critical Risk

2.2 Basic Assumptions

In this paper, some assumptions for model development are as follows:

(1).The asymmetric information does not exist between the negotiation group and individual negotiator.

(2).The decision-making behavior of individual negotiators within the negotiation group is reasonable.

(3).The probability of event occurrence is assumed to be a Bernoulli experiment and the probability of occurrence is the probability of success.

2.3 Model Development

(1). Risk and uncertainty definition

Based on the literature mentioned above, where variance is greater, the risk is higher and where there is a greater difference between actual occurrence and expectation, there will be greater loss. Considering the stability of risk, the risk and uncertainty definition will be expressed as the following:

(a). Risk definition

Since the dislike events will result in lower utility for decision maker, the risk will be defined as a specific event which will result in lower preference for the decision maker. This interprets the occurrence of risk, the loss of preference and the tolerance of choice. Risk R is defined as Eq. (1):E

) ( ) (x u x u RE ≡ j j < (1)

where uj(xj) is the utility function of outcome x for specific event E ,j 1

) (

0≤uj xj ≤ , u(x) is the expected utility value for specific event E ,

∑ = j j j ju x p x

u( ) ( ),p is the probability of outcome j x ; Eq. (1) implies that the event Ej

has risk when the utility function of outcome x for the decision maker is less thanj expected utility value for event E .

(b). Uncertainty definition

In contrast to risk, uncertainty will be defined as a specific event which will not result in lower preference for the decision maker. The equation can be expressed as Eq. (2).

) ( )) ( (u x u x URE ≡ j j ≥ (2)

where the variables uj(xj) and u(x) are defined as above. The uj(xj) value will be 1

) (

0≤uj xj ≤ .

(2). The risk utility function of the individual decision maker

The risk utility function proposed in this study was based on the multiattribute theory and utility function. The single attribute and multiattribute of a specific event are considered in the risk utility function.

(a). Transformation of the variable

Based on the utility theorem of Keeney and Raiffa (1993), the utility or preference for an event or alternative should be a positive value, that is 0≤uj(xj)≤1. This paper proposes the utility transformation variable to satisfy the condition of a utility value between 0 and 1. The utility normalization is defined as Eq. (3).

)} ( min{ )} ( max{ )} ( min{ ) ( ) ( * ij ij ij ij ij ij ij ij ij x u p x u p x u p x u p x u × − × × − × = (3)

where u*(xij) is the normalized utility value, pij is the probability of the utility of outcome i and state j , for all j=1,2,...,n,i =1,2,...,m; u(xij)is the utility value of outcome x . Since ij 0≤u(xij)≤1 and 0≤pij≤1, the u*(xij) value will be located between 0 and 1, 0≤u*(xij)≤1. Eq. (3) considers a multiattribute case. When i=1, then Eq. (3) becomes a single attribute case.

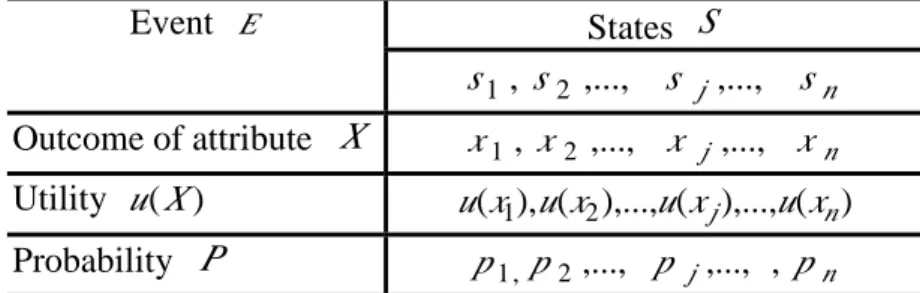

(b) Single attribute risk utility

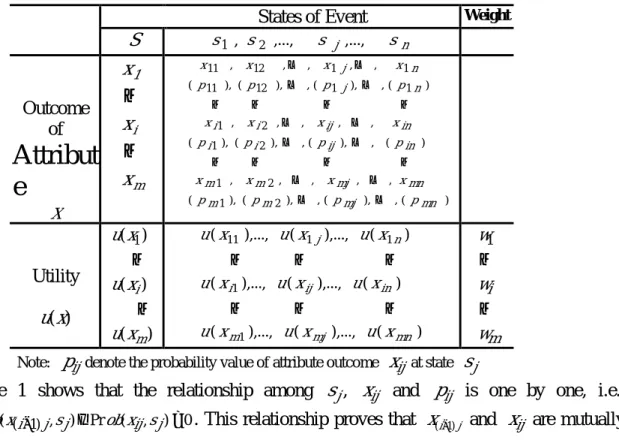

Considering a single attribute of a specific event, let E denote the specific event, S has n states for event E , S={s1,s2,...,sj,...,sn}, for j=1,2,...,n; X has outcomes x under n sn states for event E , X={x1,x2,...,xj,...,xn}; u(X) is the utility value of the individual negotiator of outcome x for event E ; n p is the set of probability corresponding to the

utility, p={p1,p2,...,pj,...,pn}, pj =prob(xj,sj), 0≤pj≤1. The structure of state, probability and outcome of the attribute for event E are shown in Table 1.

Table 1 The Structure of State, Probability and Attribute

Event E States S n j s s s s1, 2 ,..., ,..., Outcome of attribute X x1, x2 ,..., x j ,..., xn Utility u(X) u(x1),u(x2),...,u(xj),...,u(xn) Probability P p1, p2,..., p j,..., , pn

For event E , pj =Prob(xj,sj) is the probability of the utility under the outcome xj and sj states, pj−1=Prob(xj−1,sj−1) is the probability of the outcome under the outcome x and state j−1 sj−1. Because there exists a one-to-one relationship among s ,j xj and p , the states j s and j sj−1 are mutually independent and the outcome x and j x arej−1 also mutually independent, then Prob(xj−1,sj−1)Ι Prob(xj,sj)=0. Based on Table 1, the probability of the utility value is p1,p2,Λ ,pj,Λ ,pn, respectively; the utility mean value is obtained from u(x), ( ) ( )

1 j n j j x u p x u = ∑

= ; the standard deviation of utility value is

) ) ( ( )) ( (u xj = Var u xj

σ , for all j=1,2,..,n. Based on the concept from Eq. (1), the risk utility function of event E for the g individual negotiator can be shown as Eq. (4).

)) ( (( / ) ( )) ( (( ) (R u* x u x u x ug E ≡ j < σ (4)

where ug(RE)is the risk utility function for the g individual negotiator, the risk utility is normalized by u*(xj). If ((u*(xj))<u(x)/σ((u(x)) then event E is a risk event, since

1 ) (

0≤u* xj ≤ , then 0≤ug(RE)≤1. Eq. (4) implies that the event E is a risk event for g individual negotiator when the normalized utility value is smaller than the expected utility value. Otherwise, the event E is an uncertain event.

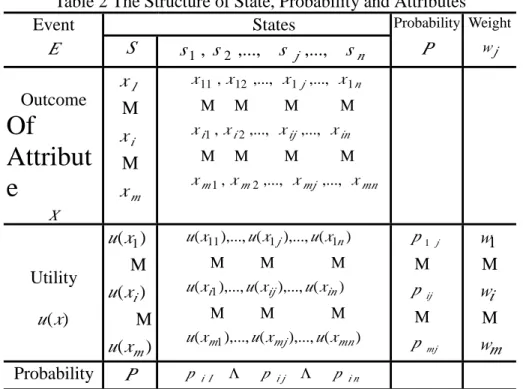

(c). Multiattribute risk utility

This paper, based on the fundamental single attribute risk utility, will develop the multiattribute risk utility function. Suppose event E has m outcomes and n states, let S be the set of state of event E , S={s1,s2,...,sj,...,sn}; X is the set of outcomes

} ,..., ,..., ,

{x1 x2 xi xm

X= , for i=1,2,...,m; the probability P is the set of probability corresponding to the utility, P={p1j,p2j,...,pij,...,pmj}, pij =Prob(xij,sj), 0≤pij≤1, for

n

j=1,2,.., , i=1,2,...,m. The relationship between state, probability and attributes is shown in Table 2.

Table 2 The Structure of State, Probability and Attributes

Event States Probability Weight

E S s1, s2 ,..., s j ,..., sn P wj Outcome

Of

Attribut

e

X x x x i m 1 Μ Μ mn mj m m in ij i i n j x x x x x x x x x x x x ,..., ,..., , ,..., ,..., , ,..., ,..., , 2 1 2 1 1 1 12 11 Μ Μ Μ Μ Μ Μ Μ Μ Utility ) (x u ) ( ) ( ) ( 1 m i x u x u x u Μ Μ ) ( ),..., ( ),..., ( ) ( ),..., ( ),..., ( ) ( ),..., ( ),..., ( 1 1 1 1 11 mn mj m in ij i n j x u x u x u x u x u x u x u x u x u Μ Μ Μ Μ Μ Μ mj ij j p p p Μ Μ 1 m i w w w Μ Μ 1 Probability P p i1 Λ p i j Λ p i nLet pij =Prob(xij,sj) be probability of utility corresponding to the outcome x and stateij j

s , and pi−1,j =Prob(xi−1j,sj) is the probability of utility corresponding to the outcome

j i

x−1 and states ; because there exists a one-to-one relationship between j s ,j x , and ij p ,ij thus Prob(xi−1j,sj)Ι Prob(xij,sj)=0. This shows that pi−1,j and pi,j are mutually

independent. Let = ∑ = n j j j x u p x u 1 1 1 1) ( )

( be the expected utility value of outcome x ,1

∑ = = n j ij ij i p u x x u 1 ) ( )

( be the expected utility value of outcome x , and leti

∑ = ∑= = m i ij n j ij i p u x w x u 1 1 ) ( )

( be the total expected utility value, where wi is the weight value of utility. σ2 =Var(u(x))=E(((u(xij)−u(x))2) is the total variance utility for all j=1,2,..,n,

m

i=1,2,..., . Then, the multiattribute risk utility function of event E for the g individual negotiator can be shown as Eq. (5).

)) ( (( / ) ( )) ( (( ) (R u* x u x u x ug ME ≡ ij < σ (5)

where ug(RME) is the multiattribute risk utility function for the g individual negotiator, the multiattribute risk utility is a normalized value, then the multiattribute risk utility will be between 0 and 1, 0≤ug(RME)≤1.

3. THE GROUP RISK UTILITY MODEL

In this section, the concession negotiator multiattribute risk utility function will be established for the BOT concession company and government sector respectively, and the

function provided will measure risk, identify risk and find out the critical risk event.

The concepts in Eqs. (4) and (5) provided an individual negotiator for risk measurement and results in a constant value, linear, additive, multiplicative or other function form. Although the individual negotiator’s preference can be taken into account in risk utility function, the risk measurement is different between the group and individual negotiators. In addition, the notion must be proposed that event E is a risk event by means of individual risk utility if the risk utility function satisfies Eq. (4). This does not ensure event E is a risk event for the concession group. In other words, this implies that the risk event for the group was determined by group risk utility, not by individual negotiators. The concept of group decision making has previously been discussed by Keeney and Raiffa (1993). Their theory infers that the group utility will be adopted instead of an individual utility when group negotiators are making decisions.

3.1 The Concept of Multiattr ibute Utility Function

Keeney and Raiffa (1993) proposed the multiattribute utility function (MAU). Based on their concept, the additive and multiplicative methods are appropriate for constructing the group decision-maker’s multiattribute utility function. The conditions of this function are: (1) total number of attributes is not less than three, (2) the preference structure of decision-maker is preference independent, and (3) the utility of the decision-decision-maker is preference independent. The fundamental mathematical equation for the multiattribute utility function can be expressed as Eq. (6).

∑ = = n i i i i x U k X U 1 ) ( ) ( (6)

where Ui(xi) is a single attribute utility function, 0≤Ui(xi)≤1; U is a multiattribute utility function; ki is a scaling constant, and 0≤ki ≤1. In Seo’s (1990) study, which constructed the fuzzy multiattribute risk function for group decision making based on the concepts of Keneey and Raiffa, the assumptions were event independent, aversion independent and trade-off attribute independent because of his modified MAU theorem. The reason he made the assumptions was to consider the hazard for decision-makers when the event occurs under an uncertain environment.

3.2 The Group Negotiation Risk Utility Function

(1). Multiattribute risk utility function for the government sector

Suppose the government group has g negotiators, risk utility function ug(RE) exists for each g individual negotiator, for g=1,2,...,h. Assume the negotiators’ utility, trade-off attribute, and events are independent. Following the concept of MAU and risk function constructed by Seo (1990), the group risk utility function for government was employed by this study, and is expressed as Eq. (7).

) ( ) ( ) ( ) ( ) ( ) ( ) ( ) ( ) ( ) ) ( ),..., ( ), ( ( 2 2 1 1 123 1 1 1 2 2 1 1 E h h E E h E b b E a a E g h g g g a b a gab E a a E g h g a gag g h g E g g g E g g E E E g E g R u R u R u k R u R u R u k k R u R u k k R u k R u R u R u U U Λ Λ + Λ + + + = = ∑ ∑ ∑ ∑ ∑ ∑ = > > = > = (7) where E g

is a multiattribute risk utility function for risk event E for g individual negotiator; kg is a scaling constant, and 0≤kg ≤1. If UgE <ug(RgE), the event E is a risk event for group

decision-makers, otherwise, event E is an uncertain event. That means the risk event E is decided by group decision-makers and ug(RgE) is defined as expected value risk utility of event E .

(2). Multiattribute risk utility function of BOT concession company

As for the BOT concession company, the group multiattribute risk utility was established by the same concept described above. Suppose the BOT company group has q negotiators, for q=1,2,...,l, the risk utility function of event F is uq(RF) for q individual negotiator. Also, we assume for the BOT group risk utility function that the negotiators’ utility is independent, trade-off attributes are independent, and events are independent. The group risk utility function for the BOT company was employed and is expressed as Eq. (8).

) ( ) ( ) ( ) ( ) ( ) ( ) ( ) ( ) ( ) ) ( ),..., ( ), ( ( 2 2 1 1 123 1 1 1 1 1 2 2 1 1 F l l F F l F b b F a a F q l q q g a b a qab F a a F q l q q q a aq l q F q q q F F F F F q R u R u R u k R u R u R u k k R u R u k k R u k R u R u R u U U Λ Λ + Λ + + + = = ∑ ∑ ∑ ∑ ∑ ∑ = > > = > = (8) where F q

U is a group multiattribute risk utility function for event E ; uq(RqF) is a multiattribute risk utility function of g individual negotiator for risk event E ; kq is a

scaling constant, and 0≤kq ≤1. Because 0≤uq(RqF)≤1 and 0≤kq ≤1, the F q

U value will be between 0 and 1. If UqF <uq(RqF), where uq(RqF) is expected value risk utility of

event F , then event F is a risk event for q negotiators, q=1,2,...,l; otherwise, event F is an uncertain event.

4. RISK ANALYSIS

In this section, the risk event and uncertainty event will be defined, and the risks of the contract will be explored.

4.1 Risk Event and Uncer tain Event Definition

The concepts in Eqs. (7) and (8) have illustrated one event becoming a risk event for group negotiators instead for an individual negotiator. Because the risks are independent, the risk and uncertain event can be obtained from Eq. (7) or (8). As for the risk to the government, we can get the risk event and uncertain event one-by-one from Eq. (7). The risk event and uncertain event are defined in Eqs. (9) and (10), respectively.

(1). Risk event definition

If event E exists and UgE <ug(RgE), then event E is a risk event, as defined by Eq. (9).

)} ( { gE g gE E g U u R R = < , for g=1,2,...,h (9)

(2). Uncertain event definition

Based on Eq. (7), if event E exists and UgE ≥ug(RgE), then event E is an uncertain event.

4.2. Risk Choice and Ranking Risk (1.) Risk Choice

For the government agency, suppose the group negotiation has g individual negotiators and G events for G=1,2,...t, g=1,2,...,h, and suppose these G events are independent. The risk can be measured per event by Eq. (7), then the risk event and uncertain event can be obtained in order to collect risk and uncertainty for the G events.

Let ΩG denote the set of G events. Based on Eq. (7) and event independence, the events

G

Ω can be separated from risk and uncertainty. The set of events ΩG is defined in Eq. (10). Also, the risk event set and the uncertainty event set can be defined in Eqs. (11) and (12), respectively. } ,..., 2 , 1 ; ,... 2 , 1 ), ( | { } ,..., 2 , 1 ; ,... 2 , 1 ), ( | {RgG UgG u RgG G t g h URGg UGg u RgG G t g h G NR G R G = = ∀ ≥ + = = ∀ < = Ω + Ω = Ω (10) } ,..., 2 , 1 ; ,... 2 , 1 ), ( | {RGg UGg u RGg G t g h G R= < ∀ = = Ω (11) } ,..., 2 , 1 ; ,... 2 , 1 ), ( | {URGg UGg u RGg G t g h G NR= ≥ ∀ = = Ω (12)

As for the BOT concession company, let ΠQ denote the set of Q events for Q=1,2,...r and suppose the event is independent. Based on Eq. (8), the risk event and uncertain event can be obtained for the BOT concession company and expressed by Eq. (12). In addition, the risk event set and the uncertain event set can be defined in Eqs. (14) and (15), respectively, for the BOT concession company.

} ,..., 2 , 1 ; ,..., 2 , 1 ), ( { } ,..., 2 , 1 ; ,..., 2 , 1 ), ( {RqQ u RqQ Q r q l RqQ u RqQ Q r q l Q NR Q R Q = = ∀ ≥ + = = ∀ < = Π + Π = Π (13) } ,..., 2 , 1 ; ,..., 2 , 1 ), ( {RqQ u RqQ Q r q l Q R= < ∀ = = Π (14) } ,..., 2 , 1 ; ,..., 2 , 1 ), ( {RqQ u RqQ Q r q l Q NR= ≥ ∀ = = Π (15) (2). Rank risk and critical risk

(a) Rank risk

Based on Eqs. (8) and (9), the multiattribute risk utility function of group negotiation can be used to measure risk, and we can find the risk event set ΩGR and R

Q

Π of the government and BOT concession company, respectively. Suppose there are O,P,Q,R, and S risk events O,P,Q,R,S∈ΩGR, and the risk utilityU , gO U , gP U , gQ U and gR U can be obtainedgS by means of equation, Based on the preference utility theorem, if the degree of risk utility is UgS πUgOπUgP πUQg πUgR, then the degree of these risks can be ranked by risk utility value, the sequence being RφQφPφOφS. Thus, the concept of ranking can provide

negotiators knowledge about the risk factor.

(b) Critical risk and the general risk event

Based on the ranking mentioned above, the negotiators can know the maximum and minimum degree risk utility of O,P,Q,R, and S risk events. It can be easily found that risk event R is the most critical and risk event S is least critical in this case. The problem is that it is hard to find the critical risk events when there exist many risk events. We use the expected value to deal with the problem and find the critical risk event.

Suppose for the group negotiation with g negotiators of government g=1,2,...,h, there are G− N risk events and N uncertain events. Let fg(w)

G denote the weight value of g

negotiators. The weight value represents the different influence among the g negotiators. Since the g negotiators’ utility is assumed to be dependent, the weight value will be 1,

1 ) (w =

fgG . Assume the government pursues the maximum utility, that is said, the

government party pursues more uncertainty events. The level of optimal risk utility can be obtained by differentiation in UGg , the result is expressed as Eq. (16).

) ) ( ( )) ( ( 1 G g N G G g G g G g Max f w U U E Max ∑− = = G g G g G g G g G g G g G g G g G g G g G g G g G g G g G g G g G g G g N G G g G g G g G g U U E U U E U U U E Let U U E U U U E U U U U E U U w f U U E = ∴ = − ⇒ = ∂ − ∂ ∂ ∂ + ∂ − ∂ = ∂ + − ∂ = ∂ ∑ ∂ = ∂ ∂ − = ) ( 0 ) ( , 0 ) ( ( ] )) ( ( )) ( ( [ ) ( ( ) ) ( ( )) ( ( 1 (16) where G g

U is the total risk utility of the risk events for the government.

The result implies that the optimal risk level is the expected utility value of all risk

events, G

g G g U U

E( )= . Then, the critical risk event and general risk event can be found, the

risk event is a critical event if UGg >E(UgG). It is a general risk event if UGg ≤E(UgG),

N G R G g U ∈Ω −

∃ , for all G =1,2,...,t. Therefore, the critical risk event and general risk event can be defined in Eqs. (17) and (18), respectively.

(i). Critical risk event definition

Let C.R. denote the set of critical risk events. For a specific r risk event, ∀r∈G−N, if the r risk utility is greater than UgG−N, then the r risk event becomes a critical risk event. It can be expressed as Eq. (17).

} 2 1 , { . . ,st CR U U G N , ,...t UGg N∈ΩGR N ≡ gG N> gG N ∀ − = ∃ − − − − (17)

(ii). General risk event definition

Based on the concept in Eq. (17), the general risk event can be expressed as Eq. (18).

} 2 1 , { . . ,st CR U U G N , ,...t UGg N∈ΩGR N ≡ gG N≤ gG N ∀ − = ∃ − − − − (18)

The result of the critical risk event can be found by using Eq. (17) and the critical risk events should become critical bargaining chips during negotiation between the BOT concession company and government. Because the utility of general risk is not greater than the utility of critical risk events, these will be secondary in negotiation.

5. CONCLUSION

This paper has constructed a risk measurement model and risk analysis framework based on the multi-attribute decision making and utility theorems The risk utility function has considered a single attribute and multiattribute event, preference of individual negotiators, and the preference of group negotiators. This model can be used to measure risk, rank risk, and to find the critical risk event for the BOT concession company and government agency. Also, we have modified Jia and Dyer’s (1996) definition of risk, which did not consider the factors of stability in risk.

Suppose the negotiator utility and events are both independent, the optimal risk level will then be the expected risk utility value of all events and be able to distinguish the critical risk events and general risk events. Accordingly, preference of utility, the critical risk event and general risk event can be obtained from the risk sets’ optimal risk level, and it can be interpreted that critical risk events are the primary bargaining chips and general risk events are the secondary target of bargaining.

This study was conducted under the assumption that events, event attributes and utility functions of the negotiators are independent. In practical situations, however, events are not entirely independent and other negotiators will affect utility preference and cognition of the negotiators. The results will change when the assumptions are changed and we believe that this can be investigated in the future. Also, the game model of the negotiation contract can be explored.

REFERENCES

Buhlmann, H. (1996) Mathematical Methods in Risk Theor y. Springer-Verlag.

Cuthbertson, M. (1996) Quantitative Financial Economics Stock, Bonds and Foreign Exchange. Published by John Wiley and Sons, Inc.

Hwang, Y. L. (1995) Pr oject and Policy Analysis of Build-Oper ate-Tr ansfer Infr astr ucture Development, Ph.D. Dissertation, Department of Civil Engineering, University of California at Berkeley.

Jaselskis, E. J. and Russell, J. S. (1992) Risk analysis approach to selection of contractor evaluation method. J our nal of Constr uction Engineer ing and Management 118, 4, 805-812.

Jia, J. and Dyer, J. S. (1996) A standard measure of risk and risk-value models. Management Science 42, 12, 1691-1705.

Keeney, R. L. and Raiffa, H. (1993) Decisions with Multiple Objectives Prefer ences and Value Tr adeoffs. Cambridge University Press.

Levitt, R. E.; Ashley, D. B. and Logcher, R. D. (1980) Allocating risk and incentive in construction. J our nal of the Constr uction Division 106, 297-305.

Louis, A. Cox, Jr. (1990) A probabilistic risk assessment program for analyzing security risks. In Louis, A. Cox Jr. and Paqlo F. R (eds.), New Risks Issues and Management. Plenum Press, New York and London.

Mustafa, M. A. and Al-Bahar, J. F. (1991) Project risk assessment using the analytic hierarchy process. IEEE Tr ansaction on Engineer ing Management 38, 1, 46-52.

Nicole, K. (1995) Risks and risk management in project finance. The High Speed Rail BOT Wor kshop. Taipei, Taiwan, December 1995.

Paek, J. H.; Lee Y. W. and Ock, J. H. (1993) Pricing construction risk: fuzzy set application. J our nal of Constr uction Engineer ing and Management 119, 4, 743-755. Philip, N. (1995) Allocation of risks in BOT projects. The High Speed Rail BOT Wor kshop, Taipei, Taiwan, December 1995.

Ronald, L. I. (1990) Methods used in probabilistic risk assessment for uncertainty and sensitivity analysis. In Louis, A. Cox Jr. and Paqlo, F. R (eds.), New Risks Issues and Management. Plenum Press, New York and London.

Seo, F. and Sakawa, M. (1990) A game theoretic approach with risk assessment for international conflict solving. IEEE Tr ansactions on Systems, Man, and Cyber netics 20, 1, 141-148.

Seo, F. and Sakawa, M. (1984) An experimental method for diversified evaluation and risk assessment with conflicting objectives. IEEE Tr ansactions on Systems, Man, and Cyber netics 14, 2, 213-223.

Seo, F. and Sakawa, M. (1985) Fuzzy multiattribute utility analysis for collective choice. IEEE Tr ansactions on Systems, Man, and Cyber netics 15, 1, 45-53.

Seo, F. (1990) On a Construction Fuzzy Multiattribute Risk Function for Group Decision Making Kacprzyk, A. and Fedrizzi, M., Multiper son Decision Making Models Using Fuzzy Sets and Possibility Theor y, Kluwer Academic Publishers, 98-218.

Sidney, M. L. (1996) Build, Oper ate, Tr ansfer Paving the Way for Tomor r ow' s Infr astr ucture, John Wiley and Sons, Inc.

Tiong, L. K. (1990) Comparative Study of BOT Projects. J our nal of Management in Engineer ing 6, 1, 107-122.

Tiong, L. K. (1990) BOT Projects: Risks and Securities. Constr uction Management and Economics 8, 3, 315-328.

Tiong, L. K. and Yeo, K. T. (1992) Critical Success Factors in Winning BOT Contracts. J our nal Engineer ing and Management 118, 2, 217-228.

Tiong, L. K. (1995) Risks and Guarantees in BOT Tender. J our nal of Constr uction Engineer ing and Management, 121, 2, 183-187.

Tiong, L. K. (1995) Impact of Financial Package versus Technical Solution in a BOT Tender. J our nal of Constr uction Engineer ing and Management 121, 3, 304-311.

Tiong, L. K. and Alum, J. (1997) Final Negotiation in Competitive BOT Tender. J our nal of Constr uction Engineer ing and Management 123, 1, 6-10.

Tiong, L. K. (1996) CSFs in Competitive Tender and Negotiation Model for BOT Projects. J our nal of Constr uction Engineer ing and Management 122, 3, 205-211.

Walker, C. and Smith, A. J. (1996) Pr ivatized Infr astr uctur e: The Build Oper ate Tr ansfer . Thomas Telford Publications.

William, I. C. J. and Crandall, K. C. (1982) Construction Risk: Multiattribute Approach. J our nal of the Constr uction Division 108, 2,187-200.

Submitted to

Transportation Planning and Technologyfor r eview

(paper Number 695)Please do not quote without per mission Comments ar e welcome.

Applications of Group Negotiation to Risk Assessment of BOT Projects

By

Cheng-Min Feng

Chao-Chung Kang &

Gwo-Hshing Tzeng

Institute of Traffic and Transportation

National Chiao Tung University

114, 4F, Sec.1, Chung Hsiao W. Rd. Taipei 100, Taiwan

Fax: 886-2-23120082, E-Mail:[email protected]

Applications of Group Negotiation to Risk Assessment of BOT Projects

Cheng-Min Feng, Chao-Chung Kang and Gwo-Hshing Tzeng Institute of Traffic and Transportation, National Chiao Tung University

114, 4F, Sec.1, Chung Hsiao W. Rd., Taipei 100, Taiwan Fax: 886-2-23120082, E-Mail:[email protected]

Abstract: This study attempts to identify and assess the potential risks of BOT projects. Based on risk analysis and the multi-attribute utility theory, the negotiator’s utility and group utility functions are established via mathematical analysis. The method can evaluate the risk status of event attributes, and can justify whether the event is a risk event or not. This study shows that if the value of group aggregation utility is less than the weight expected utility, the event is regarded as a risk event; otherwise, it is a non-risk event. Numerical examples show that the concession period of the BOT project is the primary risk event; while the foreign exchange ratio is the secondary risk event. The concession period should be the primary consideration in negotiation of the BOT projects. The model developed herein can be applied for use in the contract negotiation of the BOT project. More importantly, this model can find the primary and secondary risk event from among many risk events.

Key Words: BOT; risk assessment; risk identification; uncertainty

1. Introduction

BOT (Build, Operate and Transfer), one type of privatization, is a newly developed approach where the private sector is granted a specific concession to independently plan, design, construct, operate and maintain a project. However, the ownership of the completed project is transferred back to the government at the end of the concession period. Both the public and private sector face great risk in executing a BOT project. The public sector utilizes this approach to alleviate the government’s financial burden, learn technological know-how and management skills from the private sector, and share the potential risks with another party. Meanwhile, for the company seeking the BOT-concession, negotiating the concession contract becomes an important job in trying to share and transfer the possible risk to another party. However, the company must analyze and identify risk events in advance before they can transfer the risk. This study examines risk assessment and risk identification regarding concession contracts for BOT projects.

Risk assessment is the key issue for the Concession Company, involving tendering of the BOT Projects and contractual negotiation (Tiong, 1995; Sidney, 1996). Risk assessment is also the key to successful contract negotiation (Tiong, 1990a; Walker and Smith, 1996). Risk sharing is an important incentive for concluding engineering contracts and is important in both investment and contract negotiation (Levitt, et al., 1980; Walker and Smith, 1996).

The analysis of risk assessment can be classified into qualitative and quantitative analysis. Philip (1995), Tiong (1990b, 1995), and Walker and Smith (1996) investigate different types of risks encountered by BOT projects, like political risk, commercial risk, legislative risk, risk of construction completion, operational risk, and so on. However, qualitative analysis can hardly explain some important measures of effectiveness (MOE) such as the level of risk, how risk is produced, how to identify primary and secondary risk and so on. On the other hand, Quantitative analysis, like statistical analysis (Buhlmann, 1996; Jaselskis and Russell, 1992), financial analysis (Cuthbertson, 1996), engineering

economic analysisc (Cooper and Chapman, 1987), and the weighted method (Mustafa and Al-Bahar, 1991), have been broadly applied to transportation investment projects. Hwang (1995) investigates the relationship between the level of risk and the rate of return of the investment in the BOT Project using the concept of property rights and transaction cost. He applies the statistical approach to measure the project risk, and the expected value of investment benefit was obtained by assuming risk as a specific probability distribution.

The Financial analysis applied to risk includes Net Present Value (NPV), Benefit-Cost (B/C ratio) and Internal Rate of Return (IRR). These analysis methods must make some assumptions and estimate future cash flow. However, effectively estimating future cash flow is very difficult (Sidney, 1996). As for the utility approach, it can assess risk and also reflect risk preference behavior of the decision-maker (Seo and Sakawa, 1984,1985; Keeney and Raffia, 1993).

Owing to different definitions of risk, differences exist among assessment methods. Risk can be measured via probability, expected value, or variance and so on. Rowe (1977) defines risk as "The potential for unwanted negative consequences of an event or activity". Meanwhile, Rescher (1983) explains that "Risk is the chance of a negative outcome", and Lowrance (1976) defines risk as "A measure of the probability and severity of adverse effects". Ansell and Wharton (1992) define risk as "any unintended or unexpected outcome of a decision or course of action"; and Cooper and Chapman (1987) define risk as "Exposure to the possibility of economic or financial loss or gain, physical damage or injury, or delay, as a consequence of the uncertainty associated with pursuing a particular course of action". Keeney and Raiffa (1993) apply the expected utility value for assessing risk shelter. Meanwhile, Jia and Dyer (1996) develop a risk assessment model based on utility theory, and define risk as negative expected utility in preference, which implies the concept of risk loss. The conception of risk includes two basic elements, one is " the possibility of event ", and another is "the potential consequence".

The above mentioned literature review shows that lack of back-up data is a disadvantage of qualitative analysis, because qualitative analysis cannot determine the level of risk. Though quantitative analysis can overcome these disadvantages, certain limitations exist. Financial analysis cannot loose assumptions regarding fixed discount ratio; while statistical analysis faces the assumption of risk probability distribution. Though the weighting method can reflect the risk assessment of the decision-maker, it cannot be applied to all situations. Risk analysis based on utility approach can not only reflect the risk preference of the decision-maker, but also performs assess the risk of the event, and hence meets the characteristics of contract risk assessment.

This study attempts to establish a risk assessment model for BOT projects by using the mathematical analysis method. The remainder of the paper is structured as follows: Section 2 describes the definition of the BOT problem. Section 3 then makes some assumptions, defines the risk-state and develops the analysis model, which presents the group-utility-function. Subsequently, Section 4 presents the solution algorithm for determining primary and secondary risk. After this, Section 5 presents a numerical example. Finally, some discussion is presented and conclusions are drawn.

2. The descr iption of problem

This section describes the BOT problem in detail, as follows.

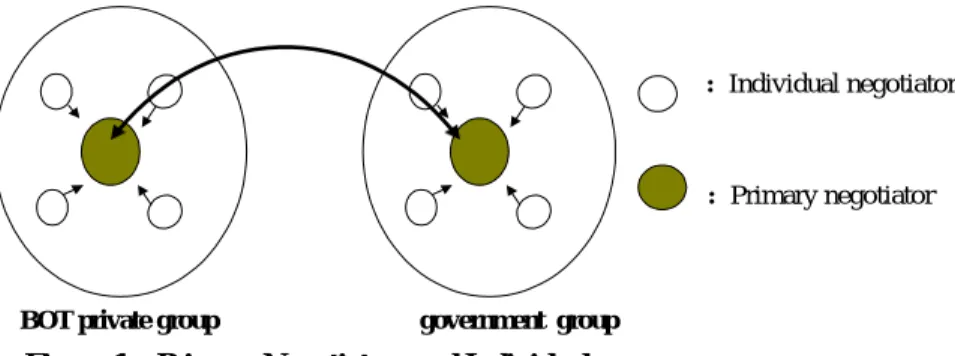

This section assumes a transportation infrastructure project exists which will be carried out via BOT, and that the contract negotiation process will be conducted between the Concession Company and government. Generally, the government negotiation team

includes the members representing transportation, environmental agencies, and local officials. Meanwhile, the Concession Company negotiation team includes lawyers, financial consultants, the initiator, engineering experts and so on. The principal negotiator from each team will be in charge of the negotiation process. Nevertheless, if the negotiation fails, the concession contract will not be valid. The negotiation aims to discuss possible uncertainties in the contract, define the individual rights and obligations of each party and, finally, write all agreements in a concessional format. Figure 1 presents a conceptual diagram of this process.

Figure 1. Primary Negotiators and Individuals

: Individual negotiator

: Primary negotiator

BOT private group government group

Risk analysis is one method widely applied to clarify the uncertainties involved in the BOT contract. Primary and secondary risk events can be identified by assessing the uncertainties, and discussing the primary risk event during negotiation. Restated, both parties will determine the key risk analysis issues requiring discussion during the contract negotiation process. Figure 2 presents a conceptual diagram of risk event, primary event, and secondary risk event.

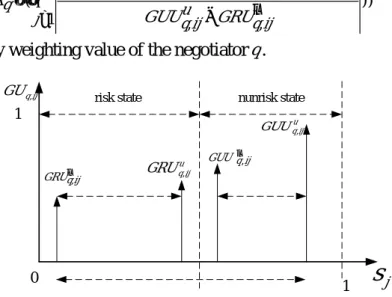

Fiqure. 2 Coneptual of Event, Risk Event, Primary Risk Event, and Secondary Risk Event

Events Risk Event Non-Risk Event Primary Risk Event Secondary Risk Event 3 The Model

This section presents the assumptions made by the proposed model. Furthermore, the definition of risk state and the individual utility functions, as well as the group aggregation utility function developed in this research are described.

3.1 Assumptions

The assumptions made by the proposed model are as follows:

(1) Agential relationships exist between negotiators and the parties they represent; however, we assume that the agent's costs have noting to do with the negotiators’