行政院國家科學委員會專題研究計畫 成果報告

結構資本、人力資本及關係資本之研究─多種研究方法之

應用(3/3)

研究成果報告(完整版)

計 畫 類 別 : 個別型 計 畫 編 號 : NSC 95-2416-H-004-004- 執 行 期 間 : 95 年 08 月 01 日至 96 年 07 月 31 日 執 行 單 位 : 國立政治大學會計學系 計 畫 主 持 人 : 吳安妮 計畫參與人員: 學士級-專任助理:劉景良 報 告 附 件 : 出席國際會議研究心得報告及發表論文 處 理 方 式 : 本計畫涉及專利或其他智慧財產權,1 年後可公開查詢中 華 民 國 96 年 11 月 02 日

The Determinants of Organizational Innovation and Performance:

An Examination of Taiwanese Electronics Industry

The Determinants of Organizational Innovation and Performance:

An Examination of Taiwanese Electronics Industry

Abstract

According to the World Economic Forum, Taiwan ranked fourth and fifth in global growth competitiveness in 2004 and 2005, respectively. These achievements have attracted worldwide attention, and even Time magazine has recognized Taiwan as a strong innovator. Taiwanese Electronics industry has invested a lot of resources in innovation and has become one of the biggest electronic design and production centers in the world. Taiwan is the only country in East Asia that has closed the gap in innovative activities with the leading G7 countries (Breznitz, 2005). For example, from 2003 to 2006, Taiwan ranked second in the rate of international patents per capita, which is one of the most reliable proxies for industrial innovation. Through an increase in patents issued both in the United States and internationally, Taiwan is now a sophisticated player in innovation consortia.

It is important to examine the determinants of organizational innovation. There are many differences in ownership structure and foreign capital between Taiwan and Western countries. Due to Taiwan’s unique situation, the two important determinants in Taiwan are ownership structure and foreign capital. For example, most public firms in Taiwan are owned by families. In recent years, the government has put much effort into attracting foreign capital to Taiwan. In Taiwan’s unique situation, it is relevant to understand whether ownership structure and foreign capital influence organizational innovation and by extension, performance.

We focus on a sample from Taiwanese Electronics industry between 2002 and 2004. The empirical results show that family ownership structure has a negative impact on organizational innovation. By contrast, foreign capital has a positive impact on a firm’s innovation. These two most important components of innovation need to be analyzed together. We find that domestic ownership structure is more important than foreign capital to explain the effect of innovation on organizational performance.

Key words: Organizational innovation, organizational performance, ownership structure, foreign capital, electronics industry.

INTRODUCTION

Ever since Schumpeter (1942) emphasized the importance of innovation, practitioners and academics have looked towards innovation as a significant managerial issue (Litz and Kleysen, 2001). From a resource-based perspective, firms have incentives to invest significant resources to maintain and build capabilities for innovation. Innovation is one of the most important factors in gaining a competitive advantage in global markets. Since the early 1970s, the government of Taiwan has put a lot of effort into developing its electronics industry, resulting in the electronics industry being responsible for the national rapid growth of the past two decades. The semiconductor industry on the island has been a main player in the global market -- for example, the IC design industry went from 51 companies in 1991 to 250 companies in 2003. This quick growth has pushed Taiwan to be the second biggest IC industry in the world.

According to the World Economic Forum (WEF), Taiwan ranked fourth and fifth in global growth competitiveness in 2004 and 2005, respectively. These achievements have attracted worldwide attention, and even Time magazine has recognized Taiwan as a strong innovator. Taiwanese Electronics industry has invested a lot of resources in innovation and has become one of the biggest electronic design and production centers in the world. Taiwan is the only country in East Asia that has closed the gap in innovative activities with the leading G7 countries (Breznitz, 2005). From 2003 to

2006, Taiwan ranked second in the rate of international patents per capita, which is one of the most reliable proxies for industrial innovation. It is important to understand why Taiwan has turned into a key player in innovation consortia, particularly in the electronics industry.

Taiwanese companies are largely controlled by families, rather than by professional managers1. Hempel (2001) pointed out that the primary objective of Chinese corporations is to maintain family control, but not management and innovation. Therefore, it is significant to examine whether ownership structure has any impact on a firm’s innovation in Taiwan. Another distinctive feature of the Taiwanese companies is the inflow of foreign capital. In recent years, the government has expended much effort into attracting foreign capital to Taiwan. For example, the percentage of foreign capital grew from 2% in 1994 to 26.78% in 2005. In order to attract foreign capital, firms focus closely on their innovation for long-term profits and growth purposes. Hence, the central question to be posed concerns how foreign capital influences innovation. As mentioned above, the first objective of this paper is to investigate the determinants of a firm’s innovation.

Facing the intensification of globalization competition, there is a widespread recognition that innovation is a critical force driving economic growth (Huang and

1 La Porta et al. (1998) and Claessens et al. (2000) show that fewer than 50 percent of the firms in the

Liu, 2005). It is generally agreed that firms must be innovative to survive and flourish in a competitive economy. If a firm wants to maintain a competitive advantage, then it must pursue an innovation strategy to create long-term financial performance. The relationship between ownership structure and the performance of a firm has been discussed, using the “agency theory.” The organizational performance of family-controlled firms may be higher, because of the lower monitoring costs. At the country level, there is a positive relationship between foreign capital inflow and economic growth in developing countries. At the company level, foreign capital inflow contributes to a firm’s innovation and then accelerates organizational performance. Although researchers show considerable interest in the impact of innovation on organizational performance, prior studies do not distinguish between the two most important components of innovation, namely, domestic ownership structure and foreign capital. Since the nature of these two different factors is fundamentally different, the results of any study can be determined if they are analyzed together. None of the prior studies has addressed the issue of how innovation might be influenced by domestic and foreign control powers, or how innovation might be a mediator in the relationship between different control powers and organizational performance. Thus, the second objective of this study is to investigate the determinants of organizational performance. We examine the importance of

ownership structure relative to foreign capital for a sample of Taiwanese Electronics industry using Structural Equation Modeling. In particular, we investigate the ability of domestic ownership structure and foreign capital to explain the impact of innovation on a firm’s performance.

There are three special features in this study. First, our model incorporates theory and research in ownership structure, foreign capital, innovation, and organizational performance. Second, we have collected our data from different sources: information on ownership structure is gathered from corporate governance datasets; information on foreign capital is collected from published datasets; innovation measures are from Taiwan and U.S.A. patent datasets; organizational performance measures are collected from financial statement datasets. Third, we consider two main issues together, namely, the determinants of innovation and organizational performance. We explicitly distinguish between the domestic and foreign effects of the explanatory variables on innovation. This distinction has rarely been made in the literature on innovation. There is now a substantial literature that examines the factors determining innovation, with particular emphasis being placed on the role of R&D expenditure2, but with little attempt to investigate these factors in the context of ownership structure or foreign capital. Although researchers show considerable interest in the impact of innovation

2 There are many studies in the literature that examine the relationship between R&D expenditure and

on organizational performance (e.g., Capon, Farley, & Hoenig, 1990; Li, Lam, & Fag, 2000), prior research does not investigate the ability of domestic ownership structure and foreign capital to explain this impact. Using a sample from Taiwanese Electronics industry, we compare the importance of domestic ownership structure relative to foreign capital. We explore the proposition that the divergence of interest between domestic ownership structure and foreign capital has implications for innovation and organizational performance.

The rest of the paper is organized as follows. In the second section, we review the relevant literature and develop testable hypotheses. In the third section, we discuss the sample and variable measures in empirical tests. The fourth section includes the empirical results and sensitivity analyses. The fifth section explains the summary and conclusion of this study.

HYPOTHESES

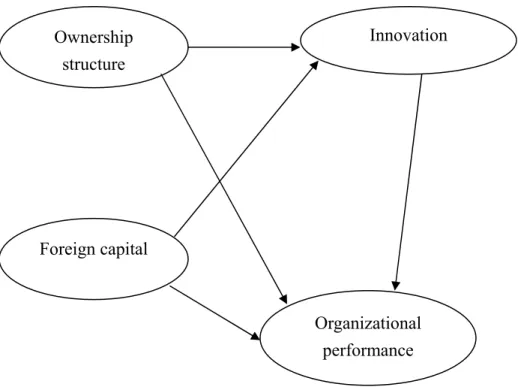

This study discusses the determinants of innovation and organizational performance. The conceptual framework is presented in Figure 1.

[Please insert Figure 1 about here] We organize the hypotheses as follows.

1. Impact of Ownership Structure on Organizational Innovation

and innovation is based on “agency theory” and “New Endogenous Growth Theory.” Based on agency theory, family-controlled firms may face the agency problem by having a lack of specialization and limited portfolio diversification due to lower investment, especially innovation investment (Gorriz & Fumas, 1996). Morck, Wolfenzon and Yeung (2005) pointed out that a family with control rights to a company might cause resource misallocation to affect the innovation of the firm. In general, managers working in family-controlled firms may act for the controlling family, but not for shareholders. In other words, because of the agency problem, firms controlled by families are reluctant to invest in innovation.

Lloyd-Jones et al. (2005) found that family-owned organizations tend to focus organizational culture on loyalty, trust, and social respect, rather than on management and innovation. This means that family-owned firms search for interpersonal relationships and social values, but not for professional management. In this situation, family-controlled firms may spend less effort on developing innovation. According to the New Endogenous Growth Theory, “the larger part of economic growth creates new wealth for entrepreneurs while destroying the old capital value. Families own the old capital, so they are reluctant to invest in innovation” (Morck and Yeung, 2003, p. 369). That study shows that family-owned firms have no “incentive to innovate by internalizing the costs of creative destruction” (p. 379).

Based on the discussion above, we specify the following hypothesis.

H1: The higher the number of family-owned shares, the lower the rate of innovation.

2. Impact of Foreign Capital on Organizational Innovation

In the 1980s and 1990s, developing countries met with world-wide liberalization of foreign investment, and their local firms began to face global competition (Lorentzen & Barnes, 2004).

Inflows of foreign capital create competitive advantages, because foreign firms in a domestic market make efforts to develop technology and innovations. According to the Kannebley et al. (2005) study, one of the major determinants of innovation in Brazilian firms is the origin of foreign capital. Not only do foreign firms focus on innovation, but also foreign institutional investors search for highly innovative firms as investment targets, because innovative firms usually create high economic performance in the future. At the same time, foreign institutional investors always like to push firms to focus on an innovation strategy for long-term competitive advantages. Kor and Mahoney (2005) showed that foreign institutional ownership boosted economic returns by sending positive signals to the market about the firm. Because foreign investors are recognized as a mechanism to upgrade a firm’s innovation, we specify the following hypothesis.

3. Impacts of Ownership Structure, Foreign Capital, or Innovation on

Organizational Performance

3.1 Impact of ownership structure on organizational performance

Fama and Jensen (1983) proposed that family-controlled firms are more efficient than non family-owned firms because of the lower “costs of monitoring.” In general, lower agency costs are related to higher firm values. Family-controlled firms outperform non-family-controlled firms in financial performance because of efficient decision-making and independent management (Adams III, True, & Winsor, 2002). Yeh et al. (2001), using Taiwanese firms as a sample, found that family-controlled firms have operational talent and a cohesive management style, and thus offer good performance. All in all, because of the lower monitoring costs, family-controlled firms have higher organizational performance and efficiency than other firms.

Even in the United States, Kang and Shivdasani (1995) and McConaughy et al. (2001) found that family-controlled firms are operated more efficiently than other kinds of firms. Based on the discussion above, we specify the following hypothesis.

H3a: The higher the number of family-owned shares, the more effective the

organizational performance.

3.2 Impact of foreign capital on organizational performance

strategic decisions (Sundaramurthy, 1996). Thus, institutional investors play a significant role in a firm’s performance (Kor & Mahoney, 2005). In recent years, foreign investors have moved to Taiwan and become the major institutional investors of firms, especially electronics firms. They use many opportunities to check and monitor a firm’s management and strategy and have a positive impact on a firm’s performance. Filatotchev et al. (2005) found that foreign institutional investors are associated with better performance of a firm. We thus specify the following hypothesis.

H3b: The higher the influence of foreign capital, the more effective the organizational

performance.

3.3 Impact of innovation on organizational performance

From a resource-based view, unique organizational resources are valuable to create greater financial performance for a firm. In the new economy era, most firms devote all their efforts and resources to develop innovation, and hence most of the unique resources come from innovation. Based on an in-depth literature review, Capon, Farley, and Hoenig (1990) found that over two-thirds of extant studies show a positive relationship between innovation and organizational performance. Using the data from the 100 largest electronics firms, Li, Lam, and Fag (2000) also found a positive relationship between technology innovation and firm performance in China.

The literature reviewed suggested that researchers show considerable interest in the issue of innovation on organizational performance. However, prior studies do not attempt to differentiate between the two most important components of innovation, namely, domestic ownership structure and foreign capital. Since the nature of these two different factors is fundamentally different, the results of any study can be determined if they are analyzed together. It can be proposed that managers working in family-controlled firms will de-emphasize innovation, preferring the lower risk/lower return of an imitator strategy, rather than the high risk/high return of an innovation strategy. By contrast, with foreign capital, because investors can balance high-risk stocks against low-risk stocks in their portfolio, they are likely to prefer an emphasis upon innovation. Broadly, they indicate that there exists a negative reinforcing effect on organizational innovation and performance if the source of control power is domestic ownership structure. On the other hand, at the opposite end of the spectrum, there is a positive reinforcing effect if the control power is driven by foreign capital. It should be noted that while foreign capital is undoubtedly an important component in determining innovation in many developing countries, it is far from being the largest control power in these countries. For example, the investment percentage of foreign capital in a single Taiwanese firm is legally constrained. Foreign investors, each holding only very small shares, are unlikely to act as a cohesive influence in

enhancing organizational performance. Moreover, if foreign investors are dissatisfied with a firm’s performance, they have the quite easy option to sell their shares. We find that domestic family ownership structure, which constitutes the largest proportion of control power in Taiwanese firms, also performs a significant role. Many Taiwanese firms are belonging to small and medium enterprises (SMEs); these kinds of

companies usually are plagued by a number of governance problems, which significantly reduces their monitoring potential. For instance, family members on the board typically possess only minimal expertise in management and innovation. Managers in family-controlled firms may also pursue non-profit maximizing objectives that increase their private benefits. Therefore, we highlight an interesting dichotomy in these firms’ ability to enhance organizational performance. Our view is that the impact of innovation on organizational performance is conditional on the opposite control powers of domestic ownership structure relative to foreign capital. We explicitly distinguish between the domestic and foreign effects on innovation and by extension, organizational performance. We cannot predict the influence of those two opposite factors on innovation and organizational performance. Consequently, we cannot provide a directional prediction for the impact of innovation on organizational performance. Accordingly, we specify the following hypothesis.

METHODS

Sample and Data Collection

Our sample focuses on Taiwanese Electronics industry from 2002 to 2004. One of the reasons for choosing the electronics industry is the need to limit irrelevant influences from different industries. The other reason is that this industry faces rapid technological advances and highly competitive global markets (Schilling & Hill, 1998; Balkin et al., 2000), such that innovation is a very important competitive advantage for firms. Taiwanese Electronics industry includes the following sectors: electronic systems, motherboard, photoelectronic I/O products, electronic components, network modem, IC production, electronic equipment, communication networks, router, consumer electronics, and software services. Our preliminary sample consists of 635 Taiwanese electronics firms from 2002 to 2004. The related data come from different databases.

We integrate ownership structure, foreign capital, and published financial statements from the Taiwan Economic Journal’s Data Bank. The total number of patents granted in Taiwan is hand-collected directly from the Taiwan Intellectual Property Office (TIPO). The patent information in the United States is purchased from Learningtech Corporation which designs its PatentGuider 2.0 software for searching data in the United States Patent and Trademark Office (USPTO).

Variables Measurement

To test the five hypotheses above, we measure four latent attributes for each firm: (1) ownership structure, (2) foreign capital, (3) organizational innovation, and (4) organizational performance.

Ownership structure: Voting rights controlled by family are widely accepted as a measure of family ownership structure (e.g., Gorriz & Fumas, 1996; La Porta et al., 1998; La Porta et al., 1999; La Porta et al., 2000; Claessens et al., 2000; Yeh et al., 2001; McConaughy et al., 2001; Adams et al., 2002; Ehrhardt & Nowak, 2003; Colli et al, 2003; Filatotchev et al., 2005). In order to analyze the effect of family ownership structure on organizational innovation and performance, we use the family personal shareholding percentage and the percentage of voting rights controlled by family as proxy for family ownership structure. Those two indicators are calculated in a different way from the Taiwan Economic Journal’s Data Bank. Specifically, the percentage of voting rights controlled by family is the shares controlled by the ultimate owner3. To measure the indicator, the Taiwan Economic Journal combines a shareholder’s direct (for example, through shares registered in her name) and indirect (for example, through shares held by entities that, in turn, she controls) voting rights in the firm.

3 La Porta (1999) defined that a firm has a controlling shareholder (ultimate owner) if this shareholder’s

Foreign capital: Foreign capital includes the foreign capital investment percentage and the allowance percentage for foreign capital investment. The allowance percentage for foreign capital investment is the allowance for foreign investors to invest in the future. Those two variables are directly collected from the Taiwan Economic Journal database.

Organizational innovation: There are variations in measuring innovation in organizations (Miller & Friesen, 1982; Subramanian & Nilakanta, 1996; Deng et al., 1999; Hirschey et al., 2001; Prajogo & Sohal, 2006). In this study, we use innovation outputs as the proxy for innovation. We define the innovation outputs – patents as the activities leading to the development of new products, the adoption of products that are new to the market, and the substantial improvement of existing products. For the purpose of capturing different aspects of innovation from different countries, this study builds a construct for measuring the innovation output of the number of patents granted from two countries – the United States and Taiwan.

Organizational performance: Different studies have proposed different viewpoints on the measurement of a firm’s performance. In general, financial measures are regarded as a significant measurement for firms’ performance. After reviewing a number of empirical studies that measure organizational performance (e.g., Hill & Snell, 1988; Holderness & Sheehan, 1988; Kang & Shivdasani, 1995;

Hitt & Brynjolfsson, 1996; Bharadwaj, 2000; Carmeli & Tishler, 2004; Sharma, 2004; BerglöF, 2005; Chen et al., 2005; Habib & Ljungqvist, 2005; Hendricks & Singhal, 2005; Mavridis & Kyrmizoglou, 2005; Muse et al., 2005; Nippani & Washer, 2005; Pugh et al., 2005; Saenz, 2005; Young, 2005; Chang, 2006; Shiu, 2006), we select return on assets (ROA), return on equity (ROE), return on sales (ROS), Tobin’s Q, and market-to-book ratio (M/B) as the proxy for organizational performance. ROA reflects the efficiency of the firm to make use of total assets. ROE represents the returns for shareholders of common stocks and is generally considered an important financial indicator for investors. ROS reflects the profitability of a firm. Both Tobin’s Q and M/B are widely accepted as measures of firm values, or market-related performances.

RESULTS

Descriptive Statistics

Table 1 presents the descriptive statistics for each variable. In two ownership structure indicators, the mean (median) for family personal shareholding percentage and percentage of voting rights controlled by family are 7.89 percent (2.88 percent) and 26.45 percent (23.56 percent), respectively. Of the two foreign capital terms, the mean (standard deviation) for foreign capital investment percentage and allowance percentage for foreign capital investment are 6.77% (10.98%) and 92.75% (12.68%),

respectively. The table shows that the mean for the number of patents granted in Taiwan is 104.50, the minimum is 0 and the maximum is 4429. The average number of patents granted in the United States is 12, with a minimum value of 0 and a maximum value of 613. Comparing the two indicators of financial performance, the mean of ROE (8 percent) is higher than that of ROA (6 percent), and the standard deviations of those two measures are 35 percent and 14 percent, respectively. The mean of ROS is 5 percent, with a wide range from -743 to 74 percent, indicating that there is a wide variation for firms’ profitability4. The average Tobin’s Q is 1.23 and the average M/B is 1.41, implying that the average market value of the firm is above the book value in Taiwanese Electronics industry.

[ Please insert Table 1 about here ]

Hypotheses Tests

We use the Structural Equation Modeling (SEM) for model testing purposes with a mix of exploratory and confirmatory analyses. This methodology is appropriate when studying variables that imperfectly represent latent constructs (Saris and Stronkhorst, 1984). Through the use of multiple indicators, SEM estimates are free from the biases imposed by measurement error or unreliability. Byrne (2001)

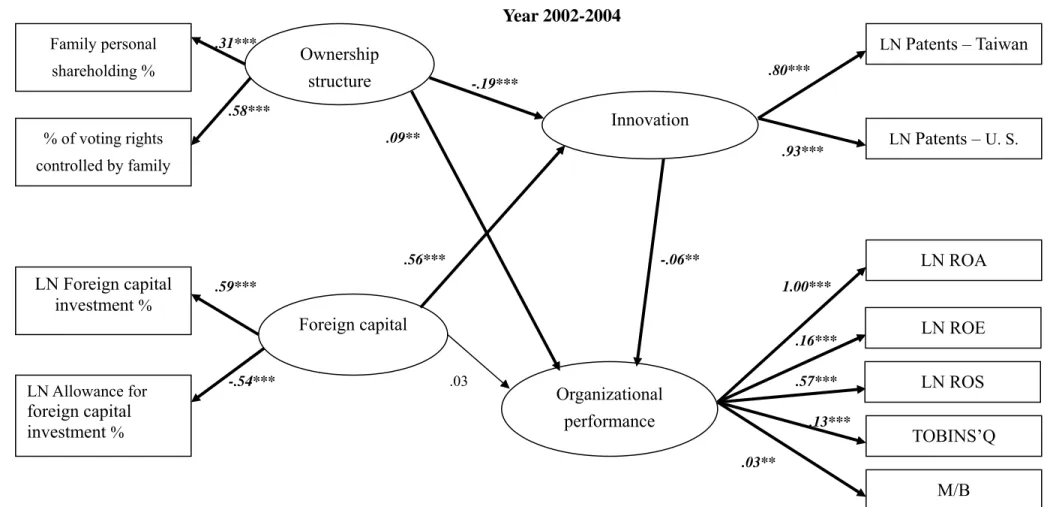

suggested that multiple criteria be used to evaluate the overall fit of a SEM. The overall fit of the hypotheses is assessed through several criteria, such as chi-square, the goodness-of-fit index (GFI), comparative fit index (CFI), root mean square residual (RMR), and the root mean square error of approximation (RMSEA). The basic model in this paper is presented in Figure 2. The model shows adequate fit from 2002 to 2004: the chi-square statistic for the model is 1601.47, with a GFI of 0.81, a CFI of 0.61, an RMR of 0.14, and an RMSEA of 0.27. The result of structure equation analysis confirms the empirical hypotheses. The statistics of models-data fitness is mostly robust (GFI > 0.80, RMR < 0.40), except for the CFI, which is below 0.80. Since SEM can estimate all parameters integrated in the model, we conclude that the model is well specified.

[Please insert Figure 2 about here]

With regard to the relationship between indicators and latent variables, we find that both the family personal shareholding percentage and the percentage of voting rights controlled by family are statistically significant (β = 0.31 and 0.58, respectively, p < 0.01) to the latent variable of the ownership structure. The allowance percentage for foreign capital investment is diametrically opposite (β = -.54, p < 0.01) to the latent variable of the foreign capital. The numbers of patents granted in Taiwan and the United States contribute significantly (β = 0.8 and 0.93, respectively, p < 0.01) to

the latent variable of organizational innovation. In addition, all indicators of organizational performance, including ROE, ROA, ROS, Tobin’s Q, and M/B, also contribute significantly to the latent variable of organizational performance. The convergent validity of all measurement models is confirmed since the coefficients of the indicators of latent variables are all significant.

Figure 2 reveals that there is a negative correlation between the ownership structure and organizational innovation (β = -0.19, p < 0.01), which supports Hypothesis 1: the family ownership structure is negatively related to innovation. We also find that foreign capital is significantly (β = .56, p < 0.01) related to organizational innovation, thereby supporting Hypothesis 2: there is a positive relationship between foreign capital and organizational innovation. Also, we find that ownership structure is significantly (β = 0.09, p < 0.05) related to organizational performance, thereby supporting Hypothesis 3a: there is a positive relationship between family ownership structure and organizational performance. However, foreign capital is not significantly related to organizational performance, as the result Hypothesis 3b is not supported. In addition, organizational innovation is negatively (β = -0.06, p < 0.05) related to firms’ performance which supports Hypothesis 3c: there is a relationship between organizational innovation and organizational performance. We find that the estimated coefficient is significantly negative, indicating that

domestic ownership structure influences are more important in determining the number of innovations than foreign capital. The results suggest that domestic ownership structure is the dominant factor in the overall impact of innovation on organizational performance. On the whole, the results of the structural equation analysis largely confirm our conceptual framework and hypotheses. All in all, the empirical results indicate that family ownership structure has a negative impact on organizational innovation. By contrast, foreign capital has a positive impact on a firm’s innovation. The family ownership structure also has a positive impact on a firm’s performance. Furthermore, we find that domestic ownership structure is more important than foreign capital to explain the effect of innovation on organizational performance.

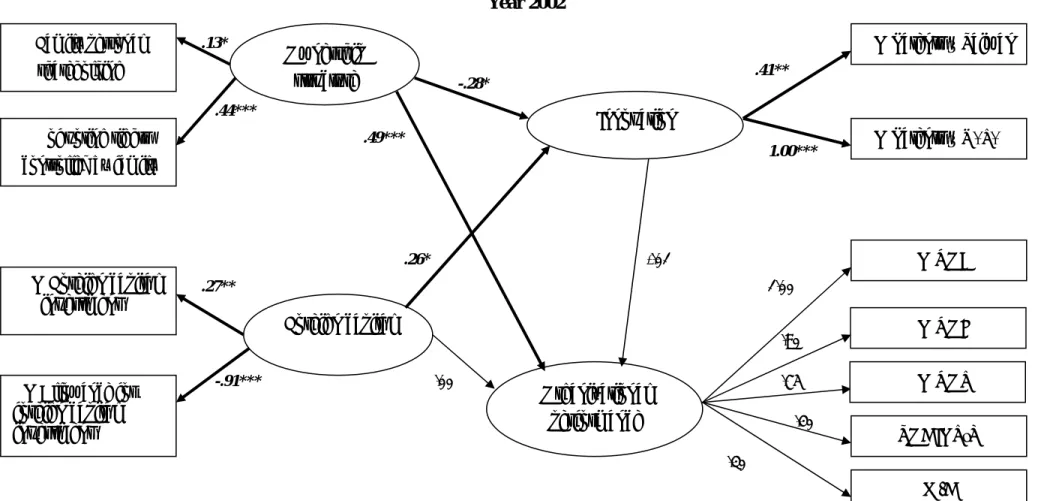

Sensitivity Analyses: For completeness, we additionally ran three structural equation models, each one for 2002, 2003, and 2004. The results are presented in Figures 3, 4, and 5.

The model in Figure 3 provides the empirical results of hypotheses tests for 2002, which show an adequate fit: the χ2 statistics are statistically significant (χ2 = 477.37, df = 35, p < 0.0001). The other results indicate that the GFI is above 0.80 and RMR is below 0.30, revealing that the analytical model is applicable to the 2002 samples. Consistent with Hypothesis 1, we find that the family ownership structure negatively

influences organizational innovation (β = -0.28, p < 0.1). We also see that foreign capital positively influences organizational innovation (β = .26, p < 0.1), and accordingly Hypothesis 2 is supported. In addition, we find that family ownership structure positively influences organizational performance (β = 0.49, p < 0.01), and accordingly Hypothesis 3a is supported. However, we do not find that foreign capital influences firms’ performance, as the result Hypothesis 3b is not supported. We also find that there are no statistically significant links between innovation and performance, and therefore Hypothesis 3c is not supported.

[ Please insert Figure 3 about here ]

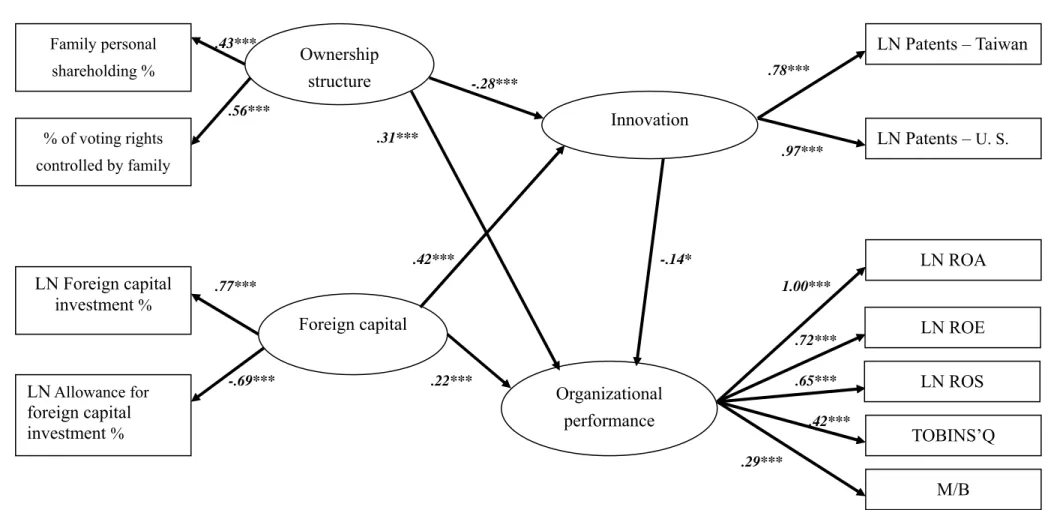

The model in Figure 4 provides the empirical results of hypotheses tests for 2003. The model also shows adequate fit: the majority of the results reflect good fitness (χ2 = 444.73, df = 35, p < 0.0001, GFI = 0.81, and RMR = 0.12). Firms with higher levels of family ownership structure perform worse than those with lower levels in terms of innovation (β = -0.28, p < 0.01), and thus Hypothesis 1 is confirmed. Firms with higher levels of foreign capital perform better than those with lower levels in terms of innovation (β = .42, p < 0.01), and thus Hypothesis 2 is confirmed. Consistent with Hypothesis 3a, the results strongly support that ownership structure is positively related to organizational performance (β = 0.31, p < 0.01). The findings support the reasoning behind Hypothesis 3a that both the family personal

shareholding and voting rights controlled by family have a positive impact on firms’ performance. Consistent with Hypothesis 3b, the results strongly support that foreign capital is positively related to organizational performance (β = .22, p < 0.01). We also find that the organizational innovation is negatively (β = -0.14, p < 0.1) related to organizational performance, as the result Hypothesis 3c is supported. On the whole, the results of the structural equation analysis in Figure 4 confirm all five hypotheses of this study.

[ Please insert Figure 4 about here ]

The model in Figure 5 provides the empirical results of hypotheses tests for 2004. Figure 5 reveals that firms with higher levels of foreign capital perform better than those with lower levels in terms of innovation (β = .35, p < 0.01), and thus Hypothesis 2 is confirmed. Consistent with Hypothesis 3a, we also find that there is a positive (β = 0.05, p < 0.1) relationship between the ownership structure and organizational performance. However, the relationship between foreign capital and organizational performance is unexpectedly negative.

[ Please insert Figure 5 about here ]

All in all, the results of the sensitivity analysis confirm most of the hypotheses of this study. Family ownership structure has a negative impact on organizational innovation. By contrast, foreign capital has a positive impact on a firm’s innovation.

Furthermore, the impact of innovation on organizational performance is dependent upon the different control powers between family ownership structure and foreign capital.

SUMMARY AND DISCUSSION

Our study finds that there is a negative impact of ownership structure on organizational innovation. The result indicates that if a few families control large wealth of a firm but often have little real capital invested, then these ownership structures might quash innovation in that firm. Our study also finds a robust positive and statistically significant relationship between foreign capital and a firm’s innovation. This result suggests that foreign investors favor and emphasize innovation by firms. This result agrees with management thinking, indicating the importance of foreign capital to innovation. Consistent with expectation, this study finds that there is a positive relationship between family ownership structure and organizational performance. This result suggests that the lower agency costs for family-owned firms are related to higher performance. In addition, we find that domestic ownership structure is more important than foreign capital to explain the effect of innovation on organizational performance. This study shows that the domestic effects of family ownership structure greatly outweigh the overseas effects of foreign capital. One

previous literature – innovation is unfavorable to organizational performance. Indeed, there is a positive effect of foreign capital on innovation, but it plays a much less important role in enhancing organizational performance. As a result, the impact of innovation on organizational performance is critically linked to the domestic ownership structure. Family ownership structure is plagued by a number of governance problems, which significantly reduces its monitoring potential. It is clear that family ownership structure is of great importance in diminishing innovation and organizational performance. Since organizational performance results mainly from ownership structure and innovation, it is important to know how to manage effective ownership structure and encourage innovation.

This study is extremely helpful since it advances the research on innovation and performance, especially addressing the impact of family ownership structure and foreign capital. It also can guide and formulate policies for the promotion of Taiwanese technical innovation. Moreover, it allows for future comparisons with international studies that have been under way in different countries.

Given the important role of innovation and its effective implementation, it is important for future research to continue this line of exploration. However, some limitations of this study suggest particular refinements to be undertaken in future research. First, this study assumes that organizational innovation has a linear

relationship with a firm’s performance. There is room for empirical testing of the non-linear relationship between organizational innovation and performance (Ittner & Larcker, 1998; Cañibano et al., 2000). Second, innovative activities can be measured using “inputs” that relate to the process of discovering new products and processes and “outputs” which relate to the outcomes of these “inputs”. This study only uses patents as the proxy for innovation and may not capture all aspects of innovation. Since innovative activities are diverse, so innovation may include input, process, and output measures. Expanding the scope of analyses to include broad measures will offer further insight to innovation. Third, a future study may increase the sample size and focus on the different industries in order to increase the generalizability and external validity of the findings.

Although the study is subject to these caveats, we hope that our findings help clarify the understanding of integrated relationships among ownership structure, foreign capital, innovation, and organizational performance. Overall, the results suggest that family ownership structure has a negative impact on a firm’s innovation, while foreign capital has a positive influence on a firm’s innovation. Those two most important factors of innovation need to be analyzed together. Our study shows the necessity of disaggregating control powers into domestic ownership structure and foreign capital. Our findings highlight the fact that domestic ownership structure is

more important than foreign capital to explain the effect of innovation on organizational performance. Future studies examining the impact of innovation on organizational performance in developing countries should incorporate this distinction.

REFERENCES

Acs, Z. J. and D. B. Audretsch. 1988. Innovation in large and small firms: an empirical analysis. American Economic Review 78 (4): 678-690.

Adams III, A. F., S. L. True, and R. D. Winsor. 2002. Corporate America’s search for the “Right” direction: Outlook and opportunities for family firms. Family Business Review 15 (4): 269-276.

Audretsch, D. B. 1995. Innovation and Industry Evolution. The MIT Press, Cambridge, MA.

Balkin, D., Markman, G. and Gomez-Mejia, L. 2000. Is CEO pay in high-technology firms related to innovation? Academy of Management Journal 43: 1118-1129.

BerglöF, E. 2005. What do Firms Disclose and Why? Enforcing Corporate Governance and Transparency in Central and Eastern Europe. Oxford Review of Economic Policy 21 (2): 178.

Bharadwaj A. S. 2000. A resource-based perspective on information technology capability and firm performance: An empirical investigation. MIS Quarterly 24 (1): 169-196.

Breznitz, D. 2005. Development, flexibility and R&D performance in the Taiwanese IT industry: capability creation and the effects of state-industry coevolution. Industrial and Corporate Change 14 (1): 153–187.

Byrne, B. 2001. Structural Equation Modeling with AMOS. Mahwah: Lawrence Erlbaum Associates, Publishers.

Cañibano, L., M. Garcia-Ayuso and P. Sanchez. 2000. Accounting for intangibles: a literature review. Journal of Accounting Literature 19: 102-130.

Capon, N., J. U. Farley, and S. Hoenig. 1990. Determinants of financial performance: A meta-analysis. Management Science 36(10): 1143-1159.

Carmeli, A., and A. Tishler. 2004. Resources, capabilities, and the performance of industrial firms: A multivariate analysis. Managerial and Decision Economics 25 (6): 299-315.

Chang, C. P. 2006. Establishing a Performance Predication Model for Insurance Companies. Journal of American Academy of Business 8 (1): 73-77.

Chen, M. C., S. J. Cheng, and Y. Hwang. 2005. An empirical investigation of the relationship between intellectual capital and firms’ market value and financial performance. Journal of Intellectual capital 6 (2): 159-176.

Claessens, S., S. Djankov and L. H. P. Lang. 2000. The separation of ownership and control in East Asian corporations. Journal of Financial Economics 58: 81-112. Colli, A., P. F. Perez, and M. B. Rose. 2003. National determinants of family firm

development? Family firms in Britain, Spain, and Italy in the nineteenth and twentieth centuries. Enterprise & Society 4(1): 28-64.

Deng, Z., B. Lev and F. Narin. 1999. Science and technology as predictors of stock performance. Financial Analysts Journal May/June: 20-32.

Ehrhardt, O., and E. Nowak. 2003. The effect of IPOs on German family-owned firms: governance changes, ownership structure, and performance. Journal of Small Business Management 41 (2): 222-232.

Fama, E. F., and M. C. Jensen. 1983. Agency problems and residual claims. Journal of Law and Economics 26: 327-349.

Feldman, M. P. 1994. The Geography of Innovation. Kluwer Academic Publishers, Dordrecht, the Netherlands.

Filatotchev, I., Y. C. Lien, and J. Piesse. 2005. Corporate governance and performance in publicly listed, family-controlled firms: Evidence from Taiwan. Asia Pacific Journal of Management 22 (3): 257.

Freeman, C., and L. Soete. 1997. The Economics of Industrial Innovation, third ed., The MIT Press, Cambridge, MA.

Gorriz, C. G., and V. S. Fumas. 1996. Ownership Structure and Firm Performance: Some Empirical Evidence from Spain. Managerial and Decision Economics 17 (6): 575.

Habib, M. A., and A. Ljungqvist. 2005. Firm Value and Managerial Incentives: A Stochastic Frontier Approach. The Journal of Business 78 (6): 2053-2093.

Glitches and Operating Performance. Management Science 51 (5): 695-711. Hempel, P. S. 2001. Differences between Chinese and Western managerial views of

performance. Personnel Review 30 (2): 203

Hill, C. W. L., and S. A. Snell. 1988. External control, corporate strategy and firm performance in research-intensive industries. Strategic Management Journal 9 (6): 577-590.

Hirschey, M., V. J. Richardson, and S. Scholz. 2001. Value relevance of nonfinancial information: the case of patent data. Review of Quantitative Finance and Accounting 17: 223-235.

Hitt, L., and E. Brynjolfsson. 1996. Productivity, business profitability, and customer surplus: three different measures of information technology value. MIS Quarterly 20 (2): 121-142.

Holderness, C. G., and D. P. Sheehan. 1988. The role of majority shareholders in publicly held corporations. Journal of Financial Economics 20: 317-346.

Huang, C. J., and C. J. Liu. 2005. Exploration for the relationship between innovation, IT and performance. Journal of Intellectual Capital 6 (2): 237-252.

Ittner, C., and D. Larcker. 1998. Are non-financial measures leading indicators of financial performance? An analysis of customer satisfaction. Journal of Accounting Research 36 supplement: 1-35.

Kang, J. K., and A. Shivdasani. 1995. Firm performance, corporate governance, and top executive turnover in Japan. Journal of Financial Economics 38: 29-58. Kannebley, Jr., S., G. S. Porto, and E. T. Pazello. 2005. Characteristics of Brazilian

innovation firms: An empirical analysis based on PINTEC-industrial research on technological innovation. Research Policy 34: 872-893.

Kleinknecht, A. 1996. Determinants of Innovation. Macmillan Press, London.

Kor, Y. Y., and J. T. Mahoney. 2005. How dynamics management, and governance of resource deployments influence firm-level performance. Strategic Management Journal 26: 489-496.

La Porta, R., F. Lopez-de-Silanes, A. Shleifer, and R. Vishny. 1998. Law and finance. Journal of Political Economy 106: 1113-1155.

La Porta, R., F. Lopez-de-Silanes, and A. Shleifer. 1999. Corporate ownership around the world. The Journal Finance 54 (2): 471-517.

La Porta, R., F. Lopez-de-Silanes, A. Shleifer, and R. Vishny. 2000. Investor protection and corporate governance. Journal of Financial Economics 58: 3-28. Li, J., K. Lam, and Y. Fang. 2000. Manufacturing firms’ performance and technology

commitment - the case of the electronics industry in China. Integrated Manufacturing Systems 11(6): 385-392.

Litz, R. A., and R. F. Kleysen. 2001. Your old men shall dream dreams, your young men shall see visions: Toward a theory of family firm innovation with help from the Brubeck family. Family Business Review 14 (4): 335-352.

Lloyd-Jones, R., M. J. Lewis, M. D. Matthews, and J. Maltby. 2005. Control, conflict and concession: Corporate governance, accounting and accountability at Birmingham small firms, 1906-1933. Accounting Historians Journal 32 (1): 149-184.

Lorentzen, J., and J. Barnes. 2004. Learning, upgrading, and innovation in the South African automotive industry. The European Journal of Development Research 16 (3): 465-498.

Mairesse, J., and P. Mohnen. 2004. The importance of R&D for innovation: A reassessment using French survey data. The Journal of Technology Transfer 30 (1-2):183-197.

Mavridis, D. G., and P. Kyrmizoglou. 2005. Intellectual Capital Performance Drivers in the Greek Banking Sector. Management Research News 28 (5): 43-62.

McConaughy, D. L., C. H. Matthews, and A. S. Fialko. 2001. Founding family controlled firms: Performance, risk, and value. Journal of Small Business Management 39 (1): 31-49.

Miller, D., and P. H. Friesen. 1982. Innovation in conservative and entrepreneurial firms: two models of strategic momentum. Strategic Management Journal 3 (1): 1-25.

Morck, R., and B. Yeung. 2003. Agency problems in large family business groups. Entrepreneurship Theory and Practice, Baylor University. (Summer): 367-382. Morck, R., D. Wolfenzon, and B. Yeung. 2005. Corporate governance, economic

entrenchment, and growth. Journal of Economic Literature 43 (3): 655-720. Muse, L. A., M. W. Rutherford, S. L. Oswald, and J. E. Raymond. 2005. Commitment

to Employees: Does It Help or Hinder Small Business Performance? Small Business Economics 24 (2): 97.

Nippani, S., and K. M. Washer. 2005. IBBEA Implementation and the Relative Profitability of Small Business. Mid – American Journal of Business 20 (2): 19-23

Osawa, Y., and Y. Yamasaki. 2005. Proposal of industrial research and development performance indices. R&D Management 35 (4): 455-461.

Prajogo, D. I., and A. S. Sohal. 2006. The integration of TQM and technology/R&D management in determining quality and innovation performance. Omega 34: 296-312.

Pugh, W. N., J. Jr., and S. L. Oswald. 2005. ESOP Adoption and Corporate Performance: Does Motive Really Matter?. Business and Economic Studies 11 (1): 76-94.

Saenz, J. 2005. Human capital indicators, business performance and market-to-book ratio. Journal of Intellectual Capital 6 (3): 374-384.

Saris, W., and H. Stronkhorst. 1984. Casual Modeling in Nonexperimental Research. Amsterdam: Sociometric Research Foundation.

Schilling, M., and Hill, C. 1998. Managing the new product development process. Academy of Management Executive, 12(3): 67-81.

Schumpeter, J. 1942. Capitalism, Socialism, and Democracy. New York: Harper & Row.

Sharma, B. 2004. Marketing strategy, contextual factors and performance: An investigation of their relationship. Marketing Intelligence & Planning 22 (2): 128.

Shiu, H. J. 2006. The Application of the Value Added Intellectual Coefficient to Measure Corporate Performance: Evidence from Technological Firms. International Journal of Management 23 (2): 356-365.

the relationship between organizational determinants of innovation, types of innovations, and measures of organizational performance. Omega 25 (6): 631-647.

Sundaramurthy, C. 1996. Corporate governance within the context of antitakeover provisions. Strategic Management Journal 17 (5): 377-394.

Yeh, Y. H., T. S. Lee, and T. Woidtke. 2001. Family control and corporate governance: Evidence from Taiwan. International Review of Finance 2 (1): 21-48.

Young, C. S. 2005. Top management teams’ social capital in Taiwan: The impact on firm value in an emerging economy. Journal of Intellectual Capital 6 (2): 177-190.

Organizational performance Ownership structure Innovation Foreign capital

Table 1

Descriptive statistics of variables for this study

Variables N Mean Median Standard

deviation

Minimum Maximum

1. Family personal shareholding %

2. % of voting rights controlled by family 3. Foreign capital investment %

4. Allowance for foreign capital investment % 5. Patents – Taiwan 6. Patents – U. S. 7. ROA 8. ROE 9. ROS 10. Tobin’s Q 11. Market-to-book ratio (M/B) 1678 1678 1778 1778 731 635 1891 1891 1891 1703 1703 7.89 26.45 6.77 92.75 104.50 12.00 .06 .08 .05 1.23 1.41 2.88 23.52 2.15 97.84 11.00 1.00 .07 .13 .07 1.12 1.25 10.36 15.93 10.98 12.68 414.80 51.54 .14 .35 .31 .45 .71 0 0 0 0 0 0 -2.47 -7.40 -7.43 .45 -.19 62.93 100 95.78 100 4429 613 .48 2.08 .74 4.56 6.24

Year 2002-2004

LN Patents – Taiwan

Figure 2. Structural Equations Modeling Results of Hypothesis Tests from Year 2002 to 2004.

Notes: 1. N =635;

2. Fit Statistics, χ2 =1601.47, DF =35, P < .0001, GFI =.81, CFI =.61, RMR =.14, and RMSEA =.27; and 3. ***, **, and* indicate significance at the 1, 5, and 10 percent level, respectively.

Family personal shareholding % % of voting rights controlled by family Organizational performance Ownership structure Innovation .31*** .80*** -.19*** .58*** LN Patents – U. S. M/B LN ROS .09** .93*** TOBINS’Q LN ROA .16*** .57*** .13*** .03** 1.00*** -.06** LN ROE .56*** LN Foreign capital investment % .59*** Foreign capital -.54*** .03 LN Allowance for foreign capital investment %

Year 2002

LN Patents – Taiwan

Figure 3. Structural Equations Modeling Results of Hypothesis Tests for Year 2002.

Notes: 1. N = 212;

2. Fit Statistics, χ2 = 477.37, DF =35, P < .0001, GFI =.81, CFI =.68, RMR =.12, and RMSEA =.24; and 3. ***, **, and* indicate significance at the 1, 5, and 10 percent level, respectively.

Family personal shareholding % % of voting rights controlled by family Organizational performance Ownership structure Innovation .13* .41** -.28* M/B LN ROS LN Patents – U. S. TOBINS’Q LN ROA .44*** .49*** .90 .75 .40 .30 1.00 1.00*** .26* -.01 LN ROE Foreign capital LN Foreign capital investment % LN Allowance for foreign capital investment % .27** -.91*** .00

Year 2003

LN Patents – Taiwan

Figure 4. Structural Equations Modeling Results of Hypothesis Tests for Year 2003.

Notes: 1. N = 212;

2. Fit Statistics, χ2 =444.73, DF =35, P < .0001, GFI =.81, CFI =.61, RMR =.12, and RMSEA =.24; and 3. ***, **, and* indicate significance at the 1, 5, and 10 percent level, respectively.

Family personal shareholding % % of voting rights controlled by family Organizational performance Ownership structure Innovation .43*** .78*** -.28*** M/B LN ROS LN Patents – U. S. TOBINS’Q LN ROA .56*** .31*** .72*** .65*** .42*** .29*** 1.00*** .97*** -.14* .42*** LN ROE Foreign capital LN Foreign capital investment % LN Allowance for foreign capital investment % .77*** -.69*** .22***

Year 2004

LN Patents – Taiwan

Figure 5. Structural Equations Modeling Results of Hypothesis Tests for Year 2004.

Notes: 1. N = 211;

2. Fit Statistics, χ2 =697.38, DF =35, P < .0001, GFI =.75, CFI =.60, RMR =.16, and RMSEA =.30; and 3. ***, **, and* indicate significance at the 1, 5, and 10 percent level, respectively.

Family personal shareholding % % of voting rights controlled by family Performance Ownership structure Innovation .71*** .46*** -.05 M/B LN ROS LN Patents – U. S. TOBINS’Q LN ROA .44** .05* .14*** .64** .10*** .08*** 1.00*** 1.00*** .35*** .03 LN ROE Foreign capital LN Foreign capital investment % LN Allowance for foreign capital investment % .33*** -.84*** -.06*