科技部補助專題研究計畫成果報告

期末報告

電子零售業對行動商務之採用:與電子商務績效之依存性

計 畫 類 別 : 個別型計畫 計 畫 編 號 : NSC 102-2410-H-004-235- 執 行 期 間 : 102 年 10 月 01 日至 103 年 09 月 30 日 執 行 單 位 : 國立政治大學資訊管理學系 計 畫 主 持 人 : 周彥君 計畫參與人員: 碩士班研究生-兼任助理人員:施佩吟 處 理 方 式 : 1.公開資訊:本計畫可公開查詢 2.「本研究」是否已有嚴重損及公共利益之發現:否 3.「本報告」是否建議提供政府單位施政參考:否中 華 民 國 103 年 12 月 12 日

中 文 摘 要 : 根據國際 Forrest 研究機構指出,行動商務的產業總值將會 以每年 39%的成長率,於 2016 達到總產值美金 310 億。在 如此快速成長的市場中,企業界紛紛建置多樣性的行動資訊 系統,如行動銀行、行動行銷及行動零售系統,用來滿足消 費者的需求。在既有對行動商務探討的期刊論文中(尤其是實 證研究),大部分的研究者著重在消費者對行動商務的印象及 接受度。反觀在企業供應面來說,實證資料的不足(尤其在早 期行動 商務未成熟時期)導致企業行為在行動商務領域的探討相對缺 乏。早期的學者更指出, 不明確的市場需求,是企業界對行動商務停滯不前之一主要 因素;也因此,供應面的企業行為探討,相對不足。近年 來,由於智慧型手機的崛起,尤其是 iPhone 在 2007 年的發 行,帶動了行動商務的市場,企業也逐漸將行動資訊系統納 入其商業流程。在此背景下,本計畫以行動零售為研究背 景,並以實證資料探討電子零售商採用行動零售服務的決 定。雖然行動商務有許多獨特的特徵,行動零售在本質上仍 是電子零售的延伸服務;本計畫遂採用依存性的角度去探討 電子零售商的特徵以及其行動零售服務採用的關聯性。依據 美國市場的實證資料,本研究探討企業在電子零售市場所累 積的商業資源及客戶偏好如何影響其行動商務的採用決策。 中文關鍵詞: 行動零售服務;行動商務;電子商務;模組性創新;複合性 通路零售

英 文 摘 要 : The rise and ensuing challenges of mobile commerce (or m-commerce) raise a pressing need to examine how firms respond to the emerging mobile sales channel. Early studies on m-commerce have mainly discussed the differences between e-commerce and m-commerce in terms of technical implementation, time differential, and location constraints. The mobility and the

personal nature of mobile devices change the way of service delivery; however, since e-retailing and m-retailing both involve cyber transactions through the Internet, supporting capabilities such as transparent order fulfillment and established customer trust are critical to a firm's e-commerce performance and its initiation of m-commerce as well. Rooted in the theoretical perspective of modular innovation, our empirical investigation shows that the modular innovation from e-retailing to m-retailing, which

changes the core component of service delivery but keeps the operations intact, actually provides more opportunities to well-entrenched firms. Using a cross-sectional dataset of top e-retailers in North America, our analysis reveals that e-retail

characteristics impact firms' migration to the mobile domain. Firms with advantages of operating resources regarding online service competencies, economies of scale, and physical outlets are more inclined to grasp at market opportunities enabled by mobile technologies.

英文關鍵詞: mobile retail services; modular innovation; m-commerce; e-m-commerce; multichannel retailing

1

The Impact of E-Retail Characteristics on Initiating Mobile

Retail Services: A Modular Innovation Perspective

1. Introduction

Ushered in by the advances of mobile devices like smart phones and tablets, mobile commerce (or m-commerce) has experienced tremendous growth over the past few years. In a recent study by Forrester Research (2011), m-commerce generated $6 billion in revenues in 2011 and the sales would continue to rise, on average by 39% a year, to $31 billion by 2016. While forecasts expect mobile spending to increase, firms have been slow to commit to m-commerce. As of 2010, around 80% of U.S. retailers had not developed m-commerce capabilities (eMarketer, 2010). Mobile conversion rate of early adopters is seen as anemic at best (Andrasick, 2011). The challenge of how to develop effective business strategies and generate revenues has kept many firms from exploring m-commerce (Kini and Bandyopadhyay, 2009).

To help firms navigate the transition from e-commerce to m-commerce, early research has mainly focused on distinct features of m-commerce and discussed ways to exploit convenience of mobile commerce or to address limitations of mobile devices. For instance, Clarke (2001) summarizes value propositions for m-commerce in four dimensions: ubiquity, localization, personalization, and convenience. Each dimension is associated with a group of mobile applications that manifest the specified value proposition, such as mobile payments for convenience and mobile advertising for personalization. Similarly, Anckar and D’Incau (2002) identify five distinct value contexts of mobile data services in terms of time-sensitivity, location-based services, spontaneity, entertainment needs, and efficiency. In spite of these opportunities, mobility comes at a price when customers have to endure hardware limitations such as small screen and relatively low connection speed (Tarasewich et al., 2002; Siau and Shen, 2003; Lee and Benbasat, 2003). These hardware constraints of mobile devices not only raise the need for efficient and effective service delivery but also require firms to develop services that are tailored to mobile shopping activities.

In the Internet retailing that demands high-quality service delivery, customers can simply use their smart phones or smart pads to access to retailers’ existing e-commerce websites, but numerous e-retailers still make considerable efforts to initiate mobile retail services. Mobile retail services involve the development of mobile-oriented websites or applications that are specifically designed and optimized for mobile devices. Despite requiring extra efforts and resources, such developmental initiatives are deemed necessary by e-retailers who aim to improve services in on-line retailing (Forrester Research, 2014). In the midst of initializing mobile services on top of existing e-commerce websites, most practitioners and researchers tend to focus on unique features of m-commerce and emphasize on how m-commerce is different from e-commerce. While it may be true that the innovation from PC-based Internet to mobile network could be perceived as different by end-users, e-retailing and m-retailing still share many common business operations. We argue that the emphasis on

2

these differences has constrained the research focus of investigation and left potential dependencies between existing e-retail operations and mobile retail services untapped.

Our analysis of the impact of e-retail characteristics on initializing mobile retail

services is stimulated by the earlier transition from store-based retailing to Internet

retailing at the dawn of the Internet. Since e-retailing could extend sales to previously unreachable areas without physical distribution channels, storbased retailing and e-retailing are widely perceived as two distinct plaforms. Also, the emergence of web-only retailers and potential channel conflicts between distribution channels and manufacturers’ direct virtual channels have led to extensive discussions of how e-retailing differs from, competes with, or even cannibalizes physical e-retailing. Porter (2001), however, points out that these virtual activities are complementary to physical operations as backend processes such as warehousing and logistics are still critical to successful e-retail operations. An important implication from this earlier transition is that both on-line and physical retail stores demand some common and complementary capabilities/resources to sustain their businesses.

Applying the implication from the first transition as noted, we argue that the transition from e-retailing to m-retailing is a modular innovation. Instead of dichotomous categorization of incremental and radical innovations, Henderson and Clark (1990) classify innovations along two dimensions: innovation’s impact on core components of a product and its impact on the interaction between components. In their classification, modular innovation refers to an innovation that changes one or more core design concepts but the relationship between core components remains the same. In this study, we view e-retailing as a service product. The use of mobile devices and wireless networks of m-retail services change the core design concept of the user-interfacing component, which provides the mobility and ubiquity that wired personal computers lack. Nevertheless, e-retailing and m-retailing are both operated through the Internet and share business functions in common. The underlying architecture of e-retailing that links all the other core components – inventory, logistics, and order fulfillment – still remains the same. While m-retailing replaces the core design with mobility, other resources and capabilities of e-retailing can be reapplied to the new context. Although mobility relaxes some constraints of e-commerce, researchers should not overlook how firms can leverage their e-retail resources to facilitate decisions and enhance performance in the mobile market. So far, few empirical studies on m-commerce have looked into how structures in the e-commerce landscape impact initiatives of m-e-commerce (Wei and Ozok, 2005; Lin, 2012; Swilley et al., 2012).

Motivated by the call for studies on the dependency between e-commerce and m-commerce, our study makes an exploratory attempt to answer the following research question: What is the impact of firms’ e-retail characteristics on their initiation of

mobile retail services? Especially, we perform our analysis to address this research

question based on the idea of modular innovation which changes a core design concept of a product but reinforces the remaining core components and the existing linkage of components. Since m-retailing is a modular innovation heavily leveraging inherent resources of e-retailing, we examine the dependency on e-retail characteristics from both operation and customer perspectives. Analyzing a cross-sectional dataset of e-retailers in North America, we find that e-retail characteristics impact firms’ migration to the mobile domain in terms of initiating mobile retail

3

services. Our econometric analysis suggests that firms with advantages of operating resources regarding e-service competencies, economies of scale, and physical outlets are more inclined to grasp at market opportunities enabled by m-commerce and hence are more likely to initiate mobile retail services.

Our paper contributes to the literature of e-commerce and e-services in two aspects. On the theoretical front, earlier studies on m-commerce have mainly focused on its distinct features and new value propositions (Clarke, 2001; Lee and Benbasat, 2003). Despite unique value contexts enabled by mobile devices, both e-retailing and m-retailing involve extensive online transactions facilitated by many capabilities in common. We apply the idea of modular innovation and explore the dependency between e-retail characteristics and m-retail services to elaborate on the inner workings among the associated constructs. We further assess the link between e-commerce and m-e-commerce along two distinct dimensions: resources related to business operations and those related to customer preferences. As firm-level analyses incline to focus on operation-related resources/capabilities, the dimension of customer demand/preferences has been under-studied (Witt, 2001). We incorporate customer-related factors into our research model and test their effects on firms’ initiatives toward m-commerce.

On the empirical front, despite the presence of conceptual frameworks and case studies on m-commerce, empirical evidence that validates the assertions has been lacking. To help firms develop mobile services in response to the emerging commerce, conceptual frameworks on the strategic implications of various m-commerce initiatives have been proposed (e.g., Balasubramanian et al. 2002; Zhang et al. 2002). Few studies, however, have gone beyond conceptual frameworks to empirically assess m-commerce initiation at the organizational level. Dahlberg et al. (2008) conduct a thorough literature review on mobile payment research and comment, “Surprisingly, we identified only four papers focusing exclusively on merchant… Merchant adoption had not been studied with quantitative data and surveys.” In the broader context of m-commerce, only a few studies such as Mallat and Tuunainen (2008) and Guo et al. (2010) examine merchant’s initiation of mobile services. Furthermore, a recent review of 618 articles (Chen and Holsapple, 2013) reports that most quantitative studies on m-commerce use psychometric models (i.e., survey-based instruments) to articulate the behavioral intentions of consumers like their perceptions about unique features of mobile data services and mobile web browsing (e.g., Wu and Wang, 2004). Empirical studies that make novel use of archival data to assess m-commerce initiatives are scant. Therefore, our study is distinct from prior studies in that we shift the focus from customers’ acceptance of m-commerce to firms’ responses to m-m-commerce. Instead of using customer-level survey data, we collect organization-level secondary data to perform an econometric analysis of firms’ initiatives towards m-commerce.

The remainder of this paper is organized as follows. Section 2 articulates the concept of modular innovation and puts forward five hypotheses. Section 3 describes the data and operationalization of variables. Section 4 presents estimation methodology and results of our empirical analysis. Section 5 discusses research implications, limitations, and potential directions for future research. Section 6 concludes the paper.

4

2. Theoretical Foundation and Hypothesis Development

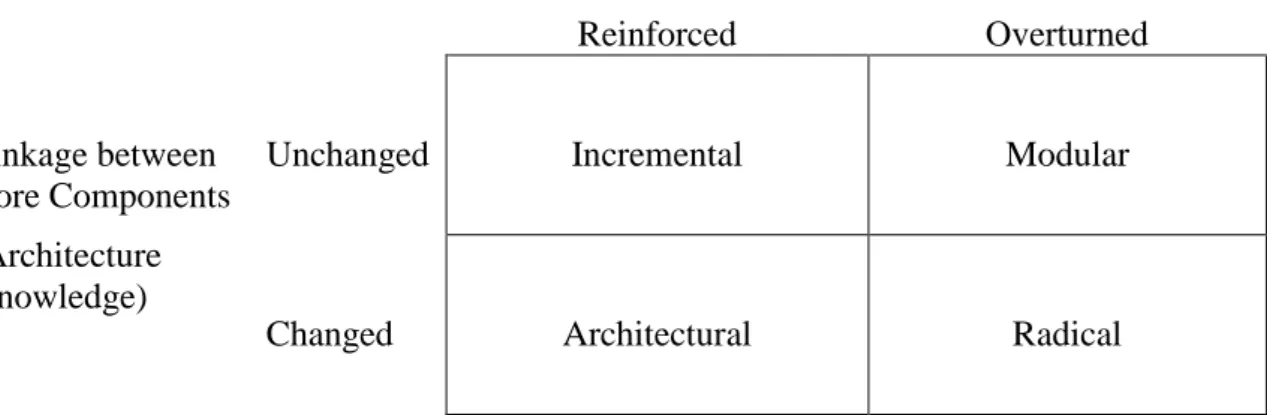

2.1 Modular InnovationIn the literature of technological innovations, researchers (e.g. Tushman and Anderson, 1986) have classified technological innovations as competence-enhancing innovations versus competence-destroying innovations. The former is so-called incremental innovations which introduce relatively minor changes to the existing product and often reinforces the dominance of established firms. Companies usually use incremental innovations to issue different versions of products such as car remodel and software upgrade. The latter is radical innovations that introduce a new dominant design and hence overturn the current product market, illustrated by the example of music format from cassette tapes to compact disk (CD) and then from CD to mp3. Henderson and Clark (1990) argue that this dichotomous distinction, while providing important insights, is incomplete. They point out that some innovations involve modest changes but have dramatic competitive consequences, while others can still exploit established foundation. The implication lies in the two types of knowledge of product development: component knowledge and architecture knowledge. Component knowledge refers to the knowledge of core design concepts and how they are implemented in each core component. Architecture knowledge, on the other hand, indicates the ways in which each component is integrated or linked together coherently to build a product. They then classify technological innovations along these two dimensions. The horizontal dimension captures an innovation’s impact on components and the vertical captures its impact on the linkages between components (See Figure 1).

Core Components (Component Knowledge) Reinforced Overturned Linkage between Core Components (Architecture Knowledge)

Unchanged Incremental Modular

Changed Architectural Radical

Figure 1. The Classification of Innovations by Henderson and Clark (1990)

Radical and incremental innovations are extreme points along both dimensions. The other two types with modest changes are architectural and modular innovations. The essence of architectural innovation is the reconfiguration of an established system to link together existing components in a new way such as the difference between

5

ceiling-mounted room fans and portable fans. While primary components are largely the same, the architecture of the product is different. Modular innovation refers to the innovation that changes only one or more core design concepts of a technology but the other components and the way in which components are linked together remain intact. Because architecture knowledge (e.g., information-processing procedures) is difficult for firms to adjust, Henderson and Clark (1990) argue that this type of innovation poses subtle challenges on well-entrenched firms. In contrast, modular

innovation, such as the replacement of analog telephones with digital telephones,

brings less change to the organization (Afuah and Bahram, 1995). To some extent, firms can simply replace an analog dialing device with a digital one and keep the product of telephone services operate as the way it is (i.e., architecture knowledge remains applicable).

In this study, we view the transition from e-retailing to m-retailing as a modular innovation. The use of mobile devices and wireless networks make mobile retail services different from e-retailing in the way of service delivery. While one core component changes, the back-end operations and even some front-end functionalities of e-retailing are still effective in the m-retail domain. Customers were used to be confined in front of computers. Using the m-retail channel, customers can, for example, make grocery shopping while they are waiting in line at a restaurant. Even though the one core component of service delivery method changes, the order still relies on efficient transaction and reliable fulfillment processes to make customers satisfied.

At the first glance at m-commerce, we tend to put our focus on the proliferation of wireless capability and emerging opportunity beyond the fixed-line personal computer. Nevertheless, the glue that ties together the core retail activities to enable smooth operations of cyber-shopping remains the same. Based on the concept of modular innovation, we expect firms to rely on accumulated e-retail resources and experience to develop their strategies for initiating m-retail services. Especially, well-entrenched e-retailers are expected to utilize their advantages and act actively in the m-retail domain.

2.2 Research Hypotheses

Front-end and back-end functions are technology enablers of a firm’s digitalized services. Zhu and Kraemer (2002) classify e-commerce functions into four digitalized services dimensions: information, transaction, customization, and supplier support. Alternatively, Voss (2003) defines a three-layer model that categorizes digitalized services into foundational, customer-centered, and value-added functions. These website functions are among the critical determinants of a firm’s online competence, service quality, and sales performance (Chuang et al. 2014). Zhu (2004) and Zhu and Kraemer (2005) find a significant correlation between website functions and e-business value in financial and retail industries.

Since m-retailing represents a modular innovation that involves digitalized services through wireless networks, firms with strong development of e-retail functions are expected to utilize their e-retailing experiences and associated architecture knowledge to facilitate the development of the new core component of mobile retail services. Wei and Ozok (2005) compile a list of functions that support online ticketing processes from leading e-commerce websites and they use the list to

6

evaluate 27 major airlines’ mobile ticketing websites. They find a significant level of similarity in functions between e-ticketing and m-ticketing websites of these airlines. According to Cam Fortin, the Director of Business Development at Wine.com, one of the critical success factors that drive the outcome of mobile site implementation is the established website functions the firm has been able to accumulate from its e-commerce website (Minnick, 2012). Besides, firms with comprehensive e-retail functions are generally considered to be more technologically innovative. According to the e-service model by Voss (2003), firms build upon their online foundational functions and further expand to value-added ones. Hence, a technologically competent/innovative firm with established e-retail functions is more likely to extend retail services into the mobile domain, which creates a new channel to serve customers.

Customers also derive their perception about e-service quality based on e-retailer website functions (Heim and Field, 2007). Since perceived service quality can be transferred from one channel to another, customers may use a firm’s m-retail website or application because they have favorable perceptions about the firm’s e-service quality (Lin, 2012). Therefore, firms with well-established e-retail functions may benefit from their accumulated reputation of e-service quality to achieve superior m-retail performance. Taken together, we hypothesize the following:

Hypothesis H1. Firms with more e-retail functions are more likely to initiate mobile retail services.

Among different types of e-retailers, retail chain is the store-based e-retailer with potential cross-channel synergies between virtual and physical channels (Berman and Thelen, 2004; Xia and Zhang, 2010). For example, JCPenney, Walgreens, and Office Depot have increased customer visits to their physical outlets by tightening the cooperation between their websites and physical stores through such convenient features as online inventory data lookup for each store location and online prescription pickup at the chosen physical store (Gulati and Garino, 2000; Porter, 2001; Berner, 2007). In addition, with physical outlets, retail chains can provide online customers with a free option of “shipping to store.” Some retailers even upgrade the option with additional convenience by allowing customers to buy products online, schedule a pickup time, and have employees meet them curbside with their purchased goods (Tuttle, 2012). Product return is another concern in e-retailing because returns occur more frequently in online retailing than in traditional retailing (Xia and Zhang, 2010). The store presence also enables retail chains to provide the “return to store” service, which helps retail chains build advantages in e-retail operations (Vishwanath and Mulvin, 2001).

With a modular innovation like m-retailing that changes the way of service delivery, retail chains can extend foregoing store-based e-retailing synergies and the accumulated architecture knowledge to m-retailing. Both options of in-store pickups and return/exchange are also applicable and critical to mobile retail services, perhaps even so to a greater extent due to the mobility and physical proximity enabled by mobile devices. The new mobile channel also brings extra traffic to physical outlets. Customers can browse and check out products through mobile devices at anytime from anywhere, especially when they receive location-based services (LBS) like real-time promotions and advertisements. Afterwards, they can go to a nearby physical outlet to check out products and to make sure that the products fit their size or taste.

7

Customers can also go to physical outlets and purchase products right away without waiting for deliveries (The Economist, 2012). This combination of location and mobility fulfills the so-called “instant gratification” that is said to characterize the millennial and younger generations.

Overall, when compared with other non-store e-retailers (e.g., web-only retailers, catalog retailers, and consumer brand manufacturers), retail chains with their presence of physical stores are in a better position to create cross-channel synergies when they adopt the mobile platform. This leads to our second hypothesis.

Hypothesis H2. Compared with the other firm types, retail chain firms are more likely to initiate mobile retail services.

E-retail market share reflects a firm’s relative size/scale in the product category. To achieve a significant size/scale in a product market, a firm needs to acquire and deploy corresponding resources and capabilities. For example, Grewal et al. (2004) argue that economic reward alone is not a strong enough incentive to maintain a stable online customer base, given that competition is only a click of mouse or a touch of screen away. Instead, reliable order fulfillment and customer trust are two equally important drivers for determining the success of online transactions. The former increases online customer satisfaction and the latter reduces perceived risks associated with online transactions. Zhu (2004) and Zhu and Kraemer (2005) survey firms in the retail industry and find that firms with tight integration of back-end infrastructures in such supply chain activities as inventory and order fulfillment have better e-retail and overall financial performances. Hulland et al. (2007) find that e-retailers’ brand management and customer service capabilities are positively associated with their e-retail performances. Since m-e-retailing is a modular innovation that changes mainly one core component (i.e. wireless delivery of digitalized services) but maintains the others and the interactions among components, firms with higher e-retail market share and more accumulated resources should be able to leverage their existing e-commerce competencies and bring their e-retail advantages into the m-retail arena. This results in our third hypothesis.

Hypothesis H3. Firms with higher e-retail market shares are more likely to initiate mobile retail services.

Classified as a modular innovation, m-retailing changes the core component of service delivery through wireless networks leading to the benefit of retail services anytime and anywhere. Aside from these operational benefits, the change of service delivery may also introduce new business rules such as security concerns and the profile of frequent users of mobile networks for consideration. The next two hypotheses H4 and H5 are related to how firms’ existing e-retail resources match with the new business rules of m-retailing.

According to a survey of 117 firms with mobile retail services, 56% report that their average dollar amount of orders received through the mobile channel is less than $75 dollars (Brohan, 2011). One possible explanation for the small order value is customers’ security concerns about m-commerce. Customers’ perception of under-developed security has been found to affect their trust in and usage of mobile data services (Siau and Shen, 2003; Yun et al. 2011). In addition, due to hardware constraints of mobile devices and the typically short duration of usage occasion, m-commerce to a great extent is about spontaneous and instant shopping (Anckar and

8

D’Incau, 2002). As a result, when using mobile retail services, customers tend to make purchases that involve instant decisions without significant information search and price comparison (Shankar and Balasubramanian, 2009). Transactions with small order values are perceived to be less risky and satisfy these spontaneous buying criteria.

According to the foregoing discussion about security concerns, hardware constraints, and spontaneous purchasing, a firm with relatively small order value in e-retailing is likely to sell products that better fit with the profile of m-e-retailing. It is reasonable to expect customers’ purchase patterns, such as order quantities for specific products and firms’ product/service offerings, to carry over from e-retailing to m-retailing. This leads to our fourth hypothesis.

Hypothesis H4. Firms with smaller e-retail order values are more likely to initiate mobile retail services.

Demographic characteristics such as age and gender have been identified as key factors that drive technology adoption and usage (Morris and Venkatesh, 2000; Mitchell and Walsh, 2004). In the context of m-commerce, Anckar and D’Incau (2002) conduct a consumer survey in Finland and find that customer willingness to use mobile data services is higher for the younger generation. In a more recent survey conducted by National Retail Federation (2010), 26.8% of American adults with a smart phone report use of these devices to research or make holiday purchases, and that number jumps to 45% among young adults from 18 to 24 years of age. Based on these statistics, the young generation is apparently more likely to opt for mobile retail services. Moreover, the young generation tends to influence their peers’ purchase decisions and hence bring additional customers to a retailer through word-of-mouth and referrals. From the firm’s perspective, offering mobile retail services is a sensible and viable strategy to provide more shopping convenience to and win over young consumers.

Given the evidence that young adults make up a significant proportion of potential m-retail patrons, a firm with a relatively young e-retail consumer base should be more willing to initiate mobile retail services to entice its existing young shoppers to experience the mobile channel. This carryover effect is more likely to take hold in online retailing as customer loyalty is found to be higher online than offline (Shankar et al. 2003). This leads to our final hypothesis.

Hypothesis H5. Firms with younger e-retail shopper ages are more likely to initiate mobile retail services.

3. Data and Measures

As the major focus of the study is to explore the dependency between e-retailer characteristics and mobile retail services, we collect data about online sales, website functions, and other metrics pertaining to leading e-retailers from the Top 500 Guide published by Internet Retailer, a data services company. The Top 500 Guide provides an annual ranking of the largest e-retailers in the United States and Canada based on annual online sales. Several prior studies (e.g., Chuang et al. 2014; Tsai et al. 2013) have used the same data source to investigate online retail services. We analyze the

9

cross-sectional dataset of the top 500 e-retailers in 2010. Yet, due to missing data of some variables, the dataset for our analysis consists of 456 firms.

We define mobile retail services as a binary dependent variable where 1 denotes that a firm has initiated a mobile-oriented website or a mobile application, and 0 otherwise. Independent variables reflect e-retailer characteristics. The variable e-retail

function represents the intensity of a firm’s ability to provide digitalized services

through system functions relative to its peers. We apply the construction method proposed by Tsai et al. (2013) and adopted by recent studies on e-retail services (e.g., Chou et al. 2014; Chuang et al. 2014). Our website functions include 60 service features that cover multiple dimensions, and Appendix A provides the complete list of these e-retail functions. Each feature takes on one of two possible values (0 = not implemented and 1 = implemented) and represents a specific function that facilitates online retail operations. We first take the ratio of 1 (if the firm has implemented one particular feature) over the total number of firms that have the same function, and we sum up such ratios for the 60 binary features. This ratio sum number is then normalized to show a firm’s relative functional strength compared with peers. In other words, a firm’s e-retail function is represented by a Z score with consideration of average and variations of peers. Retail chain is a dummy variable, which takes the value of 1 for retail chains and 0 for other firm types including catalog retailers, consumer brand manufacturers, and web-only retailers. The variable e-retail market

share captures the percentage of a firm’s e-retail sales to total sales of its own product

market. Each firm in our sample belongs to one of the following 15 product markets: apparel/accessories, automotive parts/accessories, books/music/video, computers/electronics, flowers/gifts, food/drug, hardware/home improvement, health/beauty, housewares/home furnishings, jewelry, mass merchant, office supplies, specialty/non-apparel, sporting goods, and toys/hobbies. Finally, e-retail order value and e-retail shopper age are included to reflect the extent to which a firm is susceptible to the customer preferences toward online retailing. The former is operationalized by the average dollar amount of customer orders placed through the e-retail channel. The latter is approximated by the average age of customers who make purchases through the e-retail channel.

Control variables include differences between public and private firms as well as market competition. Public firm is a dummy variable reflecting whether the firm is publicly traded. Public firms are noted to have access to resources such as financial capital more easily (Srinivasan and Moorman, 2005). Market competition reflects the competitive level of a market in which a firm operates. The variable is operationalized by Herfindahl-Hirschman index (HHI) of a firm’s e-retail product market (Krishnan, 2005; Zhu et al. 2003). Generally an increase in HHI indicates a decrese in competition. Table 1 lists the description and summary statistics of variables. Table 2 reports the pair-wise Pearson correlation coefficients of variables.

---Insert Table 1 & Table 2 Here---

4. Analysis and Results

10 0 1 2 3 4 5 6 7 i i i i i i i i i

MobileRetailServices ERetailFunction RetailChain

ERetailMarketShare ERetailOrderValue ERetailShopperAge PublicFirm MarketCompetition

Since the dependent variable – MobileRetailServices – is a dichotomous measure, fitting an ordinary linear regression model is not appropriate (Hoffmann, 2004). We employ the logit and probit models for estimation. The logit function is expressed as:

exp( ) Pr( 1| ) 1 exp( ) i i i i MobileRetailServices X X X

where Xi is the vector for independent variables and γ is the vector of parameters to be

estimated. The probit function, on the other hand, is specified as:

Pr(MobileRetailServicesi 1| i) i ( )z dz

XX

where ( ) z denotes the standard normal density function.

Both logit and probit functions are symmetric around zero and commonly used for regression modeling of binary response variables. However, considering that the distribution of MobileRetailServices is asymmetric (i.e., 152 initiating firms vs. 304 non-initiating firms), we accommodate the skewed distribution by applying the complementary log-log function (Cameron and Trivedi, 2009), which is specified as:

Pr(MobileRetailServicesi 1|Xi) 1 exp exp(Xi)

We perform maximum likelihood estimation of the logit, probit, and complementary log-log models. Table 3 reports the estimation results. The Wald Chi-square test suggests that all three models are significantly better than null models. We perform the Pregibon’s link test and find no evidence of poor model specification. Coefficient estimates of ERetailFunction, RetailChain, and ERetailMarketShare in all three models show support for hypotheses H1-H3. The estimates of

ERetailOrderValue and ERetailShopperAge provide no statistical support for H4 and

H5. The results reveal that a firm with better e-retail functions to provide digitalized services (H1), operating in the form of retail chain (H2), and/or with stronger e-retail performance in terms of market share (H3) is more likely to initiate mobile retail services. Regarding the two control variables, the significant estimates of PublicFirm imply that publically-traded firms are more inclined to initiate mobile retail services while HHI is found not associated with such initiatives.

---Insert Table 3 Here---

For the three models in Table 3, we assess a firm’s status of initiating mobile retail services in 2010 irrespective of the timing. However, it is possible that the propensity of initiation varies with year. To ensure that our findings are reliable, we collect available data on the timing of initiation for 422 out of 456 e-retailers in our sample. Figure 2 illustrates the Kaplan-Meier survival curve (Hoffmann, 2004) of the probability of initiating mobile retail services for the 422 e-retailers from 2007 to 2010. The curve reveals that the initiation rate increases over the four-year period. Less than 10% of firms had initiated m-retail services in 2007, whereas around 25% of firms had started m-retail services in 2010.

11

Figure 2. Kaplan-Meier Survival Curve of the Initiating Probability

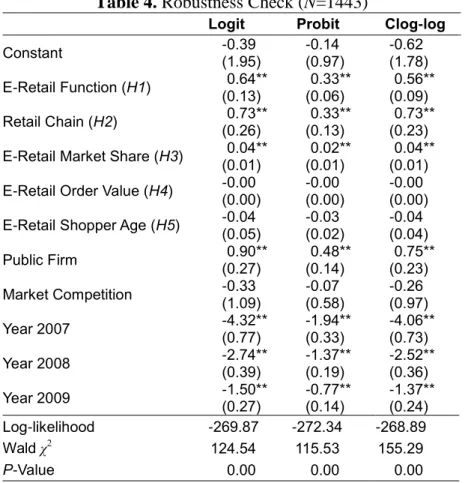

Using the longitudinal data on the timing of initiation, we fit the logit, probit, and cloglog models with year dummies to account for discrete time effects (Rabe-Hesketh and Skrondal, 2008). This exercise serves as a robustness check for results of hypothesis testing. A limitation is that only cross-sectional data in 2010 are available for e-retailer characteristics (i.e, independent variables) that explain a firm’s initiation decision. That being said, since the time period (2007-2010) is short and those independent variables are not highly likely to change dramatically in this relatively short time-span, we assume the same values for e-retail function, firm type, e-retail order value, and e-retail shopper age of a firm across the four years. To reflect the variations of e-retail sales over years, we obtain the e-retail sales of the whole market from 2007 to 2010, and calculate the annual growth rate of the market over the period. We then use a firm’s e-retail sales in 2010 as the baseline, and derive e-retail sales in 2007, 2008, and 2009 by the market’s annual growth rates. Because of the constant values assumption on regressors, this robustness check is deemed not perfect but still informative.

Table 4 reports the results of this robustness check. Consistent with the findings in Table 3, coefficient estimates of ERetailFunction, RetailChain, and

ERetailMarketShare provide support for H1, H2, and H3. Treating the year of 2010 as

the base year, we find the three year dummies to be negative and significant. These negative signs of estimated time parameters indicate that the initiation propensity increased over the years, which is consistent with the non-parametric curve shown in Figure 2.

---Insert Table 4 Here---

5. Discussion

We first provide a discussion of practical and research implications. Then we discuss potential limitations of our study while pointing out directions for future research.

5.1 Implications

According to a survey conducted by Shop.org (2010), 80% of retailers still do not have clearly defined operation strategies for initiating mobile retail services. Being an exploratory attempt, our empirical analysis of e-retailer characteristics from operation

12

and customer dimensions aims to help managers understand the cross-channel initiative taken by other firms in order to expand from e-retailing to m-retailing. Interestingly, we find that the two retailer characteristics related to customers –

e-retail order value and e-e-retail shopper age – are not significantly associated with

firms’ initiatives toward mobile retail services. On the other hand, three e-retail characteristics related to operations – e-retail function, retail chain, and e-retail

market share – do have a significant impact on initiating m-retailing.

A key implication is that, while the immaturity of the mobile market, unclear business value, and lack of apparent customer needs might create barriers for firms in initiating mobile services in the early days (Frolick and Chen, 2004; Wang and Cheung, 2004; Mallat and Tuunainen, 2008), the wide use of mobile devices and the prospering of m-commerce in recent years seemed to leave firms with no choices but to enter the mobile domain. Instead of discounting the influence of customer attributes on a firm’s adoption altogether, a more appropriate interpretation is that due to the recent emergence of m-commerce, firms are inclined to grasp at the additional sales opportunities quickly if they have technological competence (i.e., comprehensive e-Retail functions to provide digitalized services), significant cross-channel synergies (i.e., being a retail chain) or strong market performance in their specialized field (i.e., high market share and economies of scale/scope). In other words, as firms sense that they have operational edge to fuel channel expansion and move ahead of competitors, they are willing to initiate mobile retail services even when their order value or shopper age may not fit best with m-retailing. This point is further supported by the fact that public firms with more resources/funds in our sample are more likely to initiate m-retailing.

The finding that retail chains are more likely to initiate mobile retail services is worth further discussion. Kumar and Venkatesan (2005) suggest that multichannel retailers can outperform single-channel competitors because their customers are more likely to spend money, revisit the store, and repeat product purchases. The emergence of m-commerce creates a unique opportunity for retail chains to exploit multichannel formats and better serve customers by creating synergies between mobile services and physical outlets. For example, despite the wide range of shopper age of their customer bases, retail chains as a group are still more likely to adopt m-Retailing simply because they see chances of creating cross-channel synergies between e-Retailing and m-Retailing in terms of in-store pickups, exchange and return, etc. The nature of mobility also enhances their location advantages as customers can browse mobile sites at anytime from anywhere, choose to go to physical outlets nearby to check out a product to ensure its fit, and purchase the product on the spot without having to wait for delivery.

Firms search actively for innovations that attract new customers and bring in more revenues. While innovations that are obviously classified as radical or incremental are well discussed in the prior studies, modular innovation that is disguised by the changes of core components but dependent on existing operations is rarely discussed in the literature. Our empirical investigation shows that the modular innovation from e-retailing to m-retailing, which changes the core component of service delivery but keeps the operations intact, actually provides more opportunities to well-entrenched firms. Early studies on m-commerce have mainly discussed the differences between e-commerce and m-e-commerce in terms of technical implementation, time differential,

13

and location constraints. The mobility and the personal nature of mobile devices indeed change the way of service delivery. However, as e-retailing and m-retailing both involve cyber transactions through the Internet, supporting capabilities such as transparent order fulfillment and established customer trust are critical to a firm’s e-commerce performance and its initiation of m-e-commerce as well. Rooted in the theoretical perspective of modular innovation, we argue that established firms perceive the advantages of the cross-fertilization between e-retail capabilities and m-retailing, and thus take initiatives to offer mobile retail services when the emerging market gains traction.

Berry et al. (2006) propose a matrix to facilitate strategic thinking about service innovations that can attract new customers and even create a new market. They suggest firms to think from two dimensions: the type of benefit offered and the degree of service separability. In the first dimension, a firm can innovate by offering a new core benefit or a new delivery benefit that makes customers’ access to the service more easily. The second dimension indicates that firms are confined by whether the service must be produced and consumed simultaneously when delivering services. Within the matrix, firms can propose a service innovation that offers a new core benefit and that is built around servicing consumers due to the inseparable nature. Alternatively, firms can invest in a service innovation that provides a new core benefit by making an inseparable service as a separable service such as online care through the Internet. The transition from e-retailing to m-retailing falls into the matrix by innovating the way of service delivery. Due to the separable nature and the new delivery benefit, m-retailing allows customers to enjoy the service at any time and place. The match of the matrix and retailing emphasizes the importance of m-retailing as a service innovation that brings opportunity for growth. More importantly, we intend to inquire which type of firms is more likely to take the initiative and what the associated competitive implications are. Our study answers the key posed research question from the perspectives of the nature of the innovation and the inherent resources a firm possesses.

5.2 Limitations

Given its exploratory nature, our study has several limitations, many of which are due to data unavailability and hence can be addressed by future research when more data become available. First, the cross-sectional research design limits our ability to make causal inference. We address the limitation by performing the robustness check using longitudinal information on the timing of initiating mobile retail services for 422 firms from 2007 to 2010. Yet, the robustness analysis is still confined by the unavailability of longitudinal data for independent variables. A better understanding about antecedents and consequences will require a complete panel data analysis.

Second, the operation and customer dimensions we assess are by no means exhaustive. For instance, learning externalities and bandwagon effects may exist, which can affect other firms’ decisions to initiate mobile retailing. Future research can explore to what extent a firm’s initiation is influenced by its peers. A follow-up study can also address what types of firms are prone to influences of prior initiators, but that will require data on the history of firms’ initiatives toward m-commerce.

Third, our study focuses exclusively on the binary measure of initiating mobile retail services. Subsequent studies on m-commerce could consider going beyond the

14

conventional dichotomy of “adoption versus non-adoption” by incorporating firms’ extent of adoption and business value into research models, since technology/innovation diffusion involves not only initiation but also routinization (Rogers, 2003). For example, researchers may attempt to explore firms’ extent of initiating mobile services in terms of system implementation choices, which provide a more detailed and granular view on the extent of adoption. This level of analysis is more detailed and relevant to firms’ actual decision-making, although doing so would demand more data collection and comprehensive analysis.

Fourth, our sample is composed of the top 500 e-retailers in North America. This limited sample source is often encountered by empirical researchers as firm-level secondary data is usually available for only large and/or public firms. Nonetheless, our sample still has fair generalizability given that these top 500 e-retailers make up 75% of total e-retail sales in the online retail market of North America. Therefore, our findings on firms’ initiatives toward mobile retail services still should be representative of a broad population of e-retailers.

Finally, practitioners have started to recognize and discuss the potential cannibalization between e-retailing and m-retailing as mobile devices such as large-screen tablets make mobile shopping more convenient. However, it is difficult to assess this cannibalization issue under our cross-sectional setting. Alternatively, since e-retail and m-retail markets are both currently still in growing stages (Brohan, 2011), a plausible case is that firms with growing e-retail sales would also enjoy growth of m-retail sales, leading to an increase in overall sales. Future studies can extend the focus to the performance of a firm as a whole, preferably with data across long enough years. Doing so will gain a deeper understanding of the overall impact of the additional m-retail channel and contribute to the literature of multichannel retailing management.

6. Conclusion

Driven by the proliferation of wireless capability, many existing studies stress distinct attributes of m-commerce to contrast it from e-commerce. However, the replacement of the service delivery interface from e-retailing to m-retailing does not change the importance of process from inventory tracking, payment checking, to order fulfilling. We thus adopt the modular innovation concept to empirically assess the association between e-retailer characteristics and mobile retail services. We observe that retail firms’ attributes in e-commerce have substantial impacts on their decisions to activate commerce. The transition or extension from e-retailing to m-retailing is a service innovation that attracts new customers and creates a new market by enhancing the way of service delivery. Our finding suggests that the link between e-commerce and m-commerce can actually be a valuable resource to facilitate the service innovation for both e-retailers and online marketers. We encourage more research to further explore this link and illuminate the tight connection between e-commerce and m-e-commerce, both theoretically and empirically.

15

Afuah, A. N. and N. Bahram, 1995. The hypercube of innovation. Research Policy, 24(1), 51-76.

Anckar, B. and D. D’Incau, 2002. Value creation in mobile commerce: Findings from a consumer survey. Journal of Information Technology Theory and Applications, 4(1), 43-64.

Andrasick, C. Breaking out of the mobile commerce metaphor trap. E-commerce

Times. Available at

http://www.ecommercetimes.com/story/72759.html?wlc=1310399412

Balasubramanian, S., R. A. Peterson, and S. L. Jarvenpaa, 2002. Exploring the implications of m-Commerce for markets and marketing. Journal of the Academy

of Marketing Science, 30(4), 348-361.

Berman, B. and S. Thelen, 2004. A guide to developing and managing a well-integrated multi-channel retail strategy. International Journal of Retail and

Distribution Management, 32(3), 147-156.

Berner, R., May 7th 2007. J.C. Penny gets the net. Business Week.

Berry, L. L., V. Shankar, J. T. Parish, S. Cadwallader, and T. Dotzel, 2006. Creating new markets through service innovation. MIT Sloan Management Review, 47(2), 56-63.

Brohan, M., 2011. Top 500 Brand manufacturers have yet to reach their full e-commerce potential. Internet Retailer.

Cameron, A. C. and P.K. Trivedi, 2009. Microeconometrics Using STATA, Stata Press, College Station, TX.

Chen, L. and C. W. Holsapple, 2013. E-business adoption research: State of the art.

Journal of Electronic Commerce Research, 14(3), 261-286.

Chou, Y. C., H. H. C. Chuang, and B. B. M. Shao, 2014. Information initiatives of mobile retailers: A regression analysis of zero-truncated count data with underdispersion. Applied Stochastic Models in Business & Industry, forthcoming. Chuang, H. H. C., G. Lu, X. D. Peng, and G. R. Heim. 2014. Impact of value-added

service features in e-retailing processes: An econometric analysis of website functions. Decision Sciences, forthcoming.

Clarke, I., 2001. Emerging value propositions for m-commerce. Journal of Business

Strategy, 18(2), 133-148.

Dahlberg, T., N. Mallat, J. Ondrus, and A. Zmijewska, 2008. Past, present and future of mobile payments research: A literature review. Electronic Commerce Research

and Applications, 7(2), 165-181.

eMarketer, 2010. Marketers slow to integrate mobile tactics. Available at

http://www.emarketer.com/Article.aspx?R=1007834

Forrester Research, 2011. Mobile commerce forecast: 2011 to 2016. Forrester Research, Inc.

Forrester Research, 2014. Retailers modify objectives in 2014 as mobile tops priority

16

Frolick, N. M. and L. Chen, 2004. Assessing m-Commerce opportunities. Information

System Management, 21(2), 53-61.

Grewal, D., G. R. Iyer, and M. Levy, 2004. Internet retailing: enablers, limiters and market consequences. Journal of Business Research, 57(7), 703-713.

Gulati, R. and J. Garino, 2000. Get the right mix of bricks and clicks. Harvard

Business Review, 78(3), 107-114.

Guo, X., Y. Zhao, Y. Jin, and N. Zhang, 2010. Theorizing a two-sided adoption model for mobile marketing platforms. International Conference on Information Systems

(ICIS) Proceedings, Paper 128.

Heim, G. R. and J. M. Field, 2007. Process drivers of e-service quality: Analysis of data from an online rating site. Journal of Operations Management, 25(5), 962-984.

Henderson, R. M. and K. B. Clark, 1990. Architectural innovation: The reconfiguration of existing product technologies and the failure of established firms, Administrative Science Quarterly, 35(1), 9-30.

Hoffmann, J. P., 2004. Generalized Linear Models: An Applied Approach. Pearson Education, Inc.

Hulland, J., W. R. Michael, and A. D. Kersi, 2007. The Impact of Capabilities and Prior Investments on Online Channel Commitment and Performance. Journal of

Management Information Systems, 23(4), 109-142.

Kini, R. B. and S. K. Bandyopadhyay, 2009. Adoption and diffusion of m-commerce. In Taniar, D. (ed), Mobile Computing: Concepts, Methodologies, Tools and

Applications (pp. 38- 46). Hershey, PA: Information Science Reference.

Krishnan, R., 2005. The effect of changes in regulation and competition on firms' demand for accounting. The Accounting Review, 80(1), 269-287.

Kumar, V. and R. Venkatesan, 2005. Who are the multichannel shoppers and how do they perform? Correlate of multichannel shopping behavior. Journal of Interactive

Marketing, 19(2), 44-62.

Lee, Y. and I. Benbasat, 2003. Interface design for mobile commerce.

Communications of the ACM, 46(12), 49-52.

Lin, H. H., 2012. The effect of multi-channel service quality on mobile customer loyalty in an online-and-mobile retail context. The Service Industries Journal, 32(11), 1865-1882.

Mallat, N. and V. K. Tuunainen, 2008. Exploring merchant adoption of mobile payment systems: An empirical study. e-Service Journal, 6(2), 24-57.

Minnick, F., March 2012. What app? Wine.com focuses on cross-platform site.

Stores.org. Available at

http://www.stores.org/STORES%20Magazine%20March%202012/what-app?adid=ST_Weekly

Mitchell, V. and G. Walsh, 2004. Gender differences in German consumer decision-making styles. Journal of Consumer Behavior, 3(4), 331-346.

17

Morris, M., and V. Venkatesh, 2000. Age differences in technology adoption decisions: Implications for a changing work force. Personnel Psychology, 53(2), 375-403.

National Retail Federation, 2010 Economy still impacting shoppers, but glimmers of

hope appear in first NRF holiday. Available at

http://nrf.com/modules.php?name=News&op=viewlive&sp_id=1016.

Porter, M., 2001. Strategy and the Internet. Harvard Business Review, 79(3), 63-78. Rabe-Hesketh, S., and A. Skrondal, 2008. Multilevel and Longitudinal Modeling

Using Stata. College Station, TX: Stata Press.

Rogers, E. M., 2003. Diffusion of Innovations, New York, NY: Free Press.

Shankar, V., A. Smith., and A. Rangaswamy, 2003. Customer satisfaction and loyalty in online and offline environments. International Journal of Research in

Marketing, 20(2), 153-175.

Shankar, V. and S. Balasubramanian, 2009. Mobile marketing: A synthesis and prognosis. Journal of Interactive Marketing, 23(2), 118-129.

Shop.org, 2010. Three-quarters of online retailers are dialing up mobile strategies. Available at http://www.mobilepaymentstoday.com/article/112989

Siau, K., and Z. Shen, 2003. Building customer trust in mobile commerce.

Communications of the ACM, 46(4), 91-94.

Srinivasan, R. and C. Moorman, 2005. Strategic firm commitments and rewards for customer relationship management in online retailing. Journal of Marketing, 69(4), 193-200.

Swilley, E., C. F. Hofacker, and B. T. Lamont, 2012. The evolution from e-commerce to m-commerce: Pressures, firm capabilities and competitive advantage in strategic decision making, International Journal of E-Business Research, 8(1), 1-16.

Tarasewich, P., R. C. Nickerson, and M. Warkentin, 2002. Issues in mobile e-Commerce. Communication of the Association for Information Systems, 8(3), 41-64.

The Economist, February 25th 2012. Making it click. The Economist, 75-76.

Tsai, J. Y, T. S. Raghu, B. B. M. Shao, 2013. Information systems and technology sourcing strategies of e-retailers for value chain enablement. Journal of

Operations Management, 31(6), 345-362.

Tushman, M. L. and P. Anderson, 1986. Technological discontinuities and organizational environments. Administrative Science Quarterly, 31(3), 439-465. Tuttle, B., November 26th 2012. Put down the mouse: Retailers try new ways to get

holiday shoppers off the Internet and into stores, Time.

Vishwanath, V. and G. Mulvin, 2001. Multi-channels: The real sinners in the B2C Internet wars. Business Strategy Review, 12(1), 25-33.

Voss, C. A., 2003. Rethinking paradigms of service: Service in a virtual environment.

18

Wang, S. and W. Cheung, 2004. E-Business adoption by travel agencies: Prime candidates for mobile e-Business. International Journal of Electronic Commerce, 8(3), 43-63.

Wei, J. and A. Ozok, 2005. Development of a web-based mobile airline ticketing model with usability features. Industrial Management and Data Systems, 105(9), 1261-1277.

Witt, U. 2001. Economic growth: What happens on the demand side? Introduction.

Journal of Evolutionary Economics, 11(1), 1-5.

Wu, J. H. and S. C. Wang, 2004. What drives mobile commerce? An empirical evaluation of the revised technology acceptance model. Information &

Management, 42(5), 719-729.

Xia, Y. and G. P. Zhang, 2010, The impact of the online channel on retailers’ performances: An empirical evaluation. Decision Sciences, 41(3), 517-546.

Yun, H., C. C. Lee, B. G. Kim, and W. J. Kettinger, 2011. What determines actual use of mobile web browsing services? A contextual study in Korea. Communications

of the Association for Information Systems, 28(1), 313-328.

Zhang, J. J., Y. Yuan, and N. Archer, 2002. Driving forces for m-Commerce success.

Journal of Internet Commerce, 1(3), 81-105.

Zhu, K., 2004. The complementarity of information technology infrastructure and e-commerce capability: A resource-based assessment of their business value.

Journal of Management Information Systems, 21(1), 167-202.

Zhu, K. and K. L. Kraemer, 2002. E-commerce metrics for net-enhanced organizations: Assessing the value of e-commerce to firm performance in the manufacturing sector. Information Systems Research, 13(3), 275-195.

Zhu, K., and K. L. Kraemer, 2005. Post-adoption variations in usage and value of e-Business by organizations: Cross-country evidence from the retail industry.

Information Systems Research, 16(1), 61-84.

Zhu, K., K. L. Kraemer, and S. Xu, 2003. Electronic business adoption by European firms: A cross-country assessment of the facilitators and inhibitors. European

19

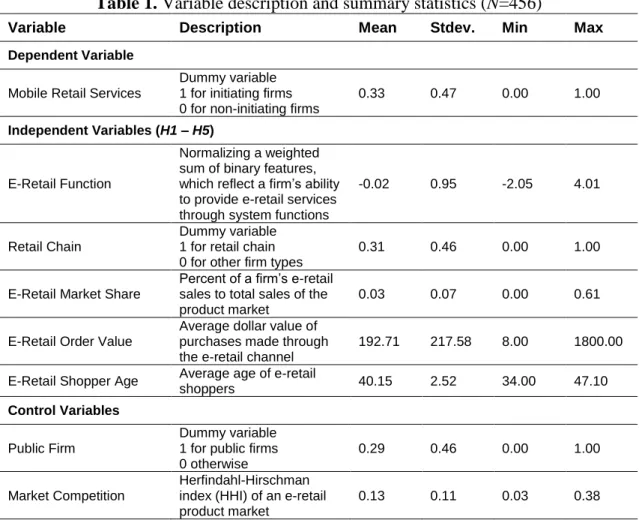

Table 1. Variable description and summary statistics (N=456)

Variable Description Mean Stdev. Min Max

Dependent Variable

Mobile Retail Services

Dummy variable 1 for initiating firms 0 for non-initiating firms

0.33 0.47 0.00 1.00

Independent Variables (H1 – H5)

E-Retail Function

Normalizing a weighted sum of binary features, which reflect a firm’s ability to provide e-retail services through system functions

-0.02 0.95 -2.05 4.01

Retail Chain

Dummy variable 1 for retail chain 0 for other firm types

0.31 0.46 0.00 1.00

E-Retail Market Share

Percent of a firm’s e-retail sales to total sales of the product market

0.03 0.07 0.00 0.61

E-Retail Order Value

Average dollar value of purchases made through the e-retail channel

192.71 217.58 8.00 1800.00 E-Retail Shopper Age Average age of e-retail

shoppers 40.15 2.52 34.00 47.10

Control Variables

Public Firm

Dummy variable 1 for public firms 0 otherwise

0.29 0.46 0.00 1.00

Market Competition

Herfindahl-Hirschman index (HHI) of an e-retail product market

0.13 0.11 0.03 0.38

Table 2. Pair-wise Pearson correlation coefficients (N = 456)

1. 2. 3. 4. 5. 6. 7.

1. Mobile Retail Services

2. E-Retail Function 0.32**

3. Retail Chain 0.22** 0.16**

4. E-Retail Market Share 0.23** 0.16** 0.08*

5. E-Retail Order Value 0.03 -0.03 -0.09** 0.03

6. E-Retail Shopper Age -0.07 0.02 -0.14** 0.08* -0.01

7. Public Firm 0.20 0.06 0.27** 0.23** -0.01 -0.08*

8. Market Competition 0.05 0.11** -0.01 0.22** 0.03 0.25** -0.01 *sig. 0.1 level; **sig. 0.05 level

20

Table 3. Estimation Results (N=456)

Logit Probit Clog-log

Constant (1.81) 1.26 (1.07) 0.77 (1.45) 0.59 E-Retail Function (H1) (0.13) 0.64** (0.07) 0.38** (0.08) 0.48** Retail Chain (H2) (0.23) 0.55** (0.14) 0.32** (0.18) 0.49** E-Retail Market Share (H3) (0.02) 0.04* (0.01) 0.03* (0.01) 0.03** E-Retail Order Value (H4) -0.00 (0.00) -0.00 (0.00) -0.00 (0.00) E-Retail Shopper Age (H5) -0.06 (0.05) -0.04 (0.03) -0.05 (0.04) Public Firm (0.24) 0.73** (0.15) 0.45** (0.19) 0.56** Market Competition (1.06) 0.42 (0.63) 0.25 (0.82) 0.36 Log-likelihood -251.06 -251.36 -250.37 Wald χ2 60.31 66.66 73.43

P-Value 0.00 0.00 0.00

Standard errors are in the parentheses. *sig. 0.1 level; **sig. 0.05 level

Table 4. Robustness Check (N=1443)

Logit Probit Clog-log

Constant -0.39 (1.95) -0.14 (0.97) -0.62 (1.78) E-Retail Function (H1) (0.13) 0.64** (0.06) 0.33** (0.09) 0.56** Retail Chain (H2) (0.26) 0.73** (0.13) 0.33** (0.23) 0.73** E-Retail Market Share (H3) (0.01) 0.04** (0.01) 0.02** (0.01) 0.04** E-Retail Order Value (H4) -0.00 (0.00) -0.00 (0.00) -0.00 (0.00) E-Retail Shopper Age (H5) -0.04 (0.05) -0.03 (0.02) -0.04 (0.04) Public Firm (0.27) 0.90** (0.14) 0.48** (0.23) 0.75** Market Competition -0.33 (1.09) -0.07 (0.58) -0.26 (0.97) Year 2007 -4.32** (0.77) -1.94** (0.33) -4.06** (0.73) Year 2008 -2.74** (0.39) -1.37** (0.19) -2.52** (0.36) Year 2009 -1.50** (0.27) -0.77** (0.14) -1.37** (0.24) Log-likelihood -269.87 -272.34 -268.89 Wald χ2 124.54 115.53 155.29 P-Value 0.00 0.00 0.00

21 APPENDIX A E-Retail Function List

360 degree spin Microsites Widgets Affiliate program Mouseover Wish list Auction Online circular Zoom

Blogs Online gift certificates Account status/History Catalog quick order Outlet center Buy online/Pick up in

store

Color switching Pre-orders Click to call

Coupons/Rebates Product comparisons Currency converter Customer reviews Product customization Estimated shipping date Daily/Seasonal specials Product ratings Express checkout Dynamic imaging Product recommendations Free return shipping E-mail a friend Product wikis Live chat/E-mail Enlarged product view Registry Order confirmation Frequent buyer program RSS feed Order status

Frequently asked questions Site personalization Pre-paid labels Gadgets Social networking Rain checks

Guided navigation Store locator Real-time inventory check Interactive catalog Syndicated content Ship to multiple addresses Interactive kiosks Top sellers Shipping costs calculator Mapping Videocasts Shipment tracking Mash-ups What’s new Toll-free number

科技部補助計畫衍生研發成果推廣資料表

日期:2014/12/11科技部補助計畫

計畫名稱: 電子零售業對行動商務之採用:與電子商務績效之依存性 計畫主持人: 周彥君 計畫編號: 102-2410-H-004-235- 學門領域: 資訊管理無研發成果推廣資料

102 年度專題研究計畫研究成果彙整表

計畫主持人:周彥君 計畫編號: 102-2410-H-004-235-計畫名稱:電子零售業對行動商務之採用:與電子商務績效之依存性 量化 成果項目 實際已達成 數(被接受 或已發表) 預期總達成 數(含實際已 達成數) 本計畫實 際貢獻百 分比 單位 備 註 ( 質 化 說 明:如 數 個 計 畫 共 同 成 果、成 果 列 為 該 期 刊 之 封 面 故 事 ... 等) 期刊論文 0 0 100% 研究報告/技術報告 0 0 100% 研討會論文 0 0 100% 篇 論文著作 專書 0 0 100% 申請中件數 0 0 100% 專利 已獲得件數 0 0 100% 件 件數 0 0 100% 件 技術移轉 權利金 0 0 100% 千元 碩士生 1 1 20% 博士生 0 0 100% 博士後研究員 0 0 100% 國內 參與計畫人力 (本國籍) 專任助理 0 0 100% 人次 期刊論文 0 1 100% 研究報告/技術報告 0 0 100% 研討會論文 0 0 100% 篇 論文著作 專書 0 0 100% 章/本 申請中件數 0 0 100% 專利 已獲得件數 0 0 100% 件 件數 0 0 100% 件 技術移轉 權利金 0 0 100% 千元 碩士生 0 0 100% 博士生 0 0 100% 博士後研究員 0 0 100% 國外 參與計畫人力 (外國籍) 專任助理 0 0 100% 人次其他成果

(

無法以量化表達之成 果如辦理學術活動、獲 得獎項、重要國際合 作、研究成果國際影響 力及其他協助產業技 術發展之具體效益事 項等,請以文字敘述填 列。)本專案計畫所產生之論文,目前已投稿至 Information and Management (SSCI; 國科會資訊管理期刊排序 7)於第一輪審查 成果項目 量化 名稱或內容性質簡述 測驗工具(含質性與量性) 0 課程/模組 0 電腦及網路系統或工具 0 教材 0 舉辦之活動/競賽 0 研討會/工作坊 0 電子報、網站 0 科 教 處 計 畫 加 填 項 目 計畫成果推廣之參與(閱聽)人數 0