行政院國家科學委員會專題研究計畫 成果報告

以土地拍賣樣本測試投標者投標行為

研究成果報告(精簡版)

計 畫 類 別 : 個別型 計 畫 編 號 : NSC 100-2410-H-004-085- 執 行 期 間 : 100 年 08 月 01 日至 101 年 07 月 31 日 執 行 單 位 : 國立政治大學財務管理學系 計 畫 主 持 人 : 姜堯民 計畫參與人員: 學士級-專任助理人員:劉書蓉 報 告 附 件 : 國外研究心得報告 出席國際會議研究心得報告及發表論文 公 開 資 訊 : 本計畫可公開查詢中 文 摘 要 : 我利用台北市及台北縣的國有土地拍賣資料來測試 Sherman(2005)的拍賣資訊蒐集成本模型。結果顯示,台北市 的參與投標人多會於事前收集資訊,再決定是否進入參與投 標,投標行為也不會有亂投標的情況。而相對地,台北縣的 投標人,不會收集資訊就來投標,投標行為也多是亂投標。 所以認為參與台北市土地拍賣者較符合有資訊投標人的行 為,而參與台北縣投標的像是沒有資訊投標人的行為。 中文關鍵詞: 土地拍賣,拍賣人數,資訊蒐集成本

英 文 摘 要 : I use land auction data in Taipei City and in Taipei County to test Sherman’s (2005) information

production theory. Results show that bidders in Taipei City (a core metropolitan area) and those in Taipei County (a suburb) have different bidding behavior. I find that bids in Taipei City’s land auctions are generally consistent with the

predictions of auction theory for informed bidders. They tend to expend resources to collect information and shave their bids optimally. However, bids in Taipei County exhibit uninformed and overbidding behavior.

英文關鍵詞: Land Auction, Endogenous Entry, Number of Entry, Information cost

行政院國家科學委員會補助專題研究計畫 X

成果報告 □ 期中進度報告 以土地拍賣樣本測試投標者投標行為計畫類別:X 個別型計畫 □整合型計畫

計畫編號:NSC 100‐2410‐H‐004‐085

執行期間: 2011/08/01 ~ 2012/07/31

執行機構及系所:政治大學財務管理系

計畫主持人:姜堯民

共同主持人:

計畫參與人員:

成果報告類型(依經費核定清單規定繳交):x 精簡報告 □完

整報告

本計畫除繳交成果報告外,另須繳交以下出國心得報告:

x 赴國外出差或研習心得報告

□赴大陸地區出差或研習心得報告

x 出席國際學術會議心得報告

□國際合作研究計畫國外研究報告

處理方式:

除列管計畫及下列情形者外,得立即公開查詢

□涉及專利或其他智慧財產權,□一年□二年後可

公開查詢

Evidence on the Endogenous Entry of Bidders in Land

Auctions

Yao-Min Chiang

Department of Finance, National Chengchi University

NO.64,Sec.2,ZhiNan Rd.,Wenshan District,Taipei City 11605,Taiwan TEL: +886-29393091 ext. 81140

Email: [email protected]

Abstract

I use land auction data in Taipei City and in Taipei County to test Sherman’s (2005) information production theory. Results show that bidders in Taipei City (a core metropolitan area) and those in Taipei County (a suburb) have different bidding behavior. I find that bids in Taipei City’s land auctions are generally consistent with the predictions of auction theory for informed bidders. They tend to expend resources to collect information and shave their bids optimally. However, bids in Taipei County exhibit uninformed and overbidding behavior.

Keywords: Land Auction, Endogenous Entry, Number of Entry

Evidence on the Endogenous Entry of Bidders in Land Auctions

1. Introduction

Auctions are used by governments for a variety of purpose. Governments use auction to allocate various publically owned natural resources. State-owned land is commonly sold at auctions. Central and/or local governments may auction large amount of undeveloped land, residential housing, and commercial real estate. Auctions provide several purposes. Auctions can raise revenue for the government, and can generate an efficient allocation (Ashenfelter and Genesove, 1992; Lusht, 1996).1 More importantly, an auction can reveal information: how strong the demand is, and how bidders value the asset.

Auctions are transparent and fair. In an auction, the government has no allocation discretion to influence the allocation outcome. In that sense, impropriety, or even corruption can be prevented. Auction outcomes are determined independent of policy makers’ preferences. In summary, land auctions allow governments to obtain maximum pricing through an efficient and transparent bidding process that sets a realistic benchmark for pricing through broader market exposure.

Auctions put power over pricing into the hands of bidders, with little or no role for the government in pricing and allocation. Nonetheless, auctions are challenging for bidders. Whether it is best to place pricing entirely in the hands of investors depends in part on how sophisticated those investors are at evaluating the object. When there are common values, the Vickrey auction is efficient. When a buyer's information is multidimensional, no auction is generally efficient. The auction model of incomplete information predicts ‘winner’s curse’, since the winner of a sealed-bid

1

auction of unknown common value tends to overestimate the true value of the auction object (Giliberto & Varaiya, 1989)

In a model for auction with endogenous entry, rational investors will choose to acquire information and enter an auction if they expect to recover their costs evaluating the object (Sherman, 2005). If they follow the optimal entry and bidding strategies, the entry of these informed bidders and the aggressiveness of their bids will be positively related to returns to winning bidders. I therefore want to test whether the bidders’ entry decisions depend on information costs, and how the aggressiveness of their bids depends on the entry of bids2. Chiang, Qian, and Sherman (2010) use Taiwan’s auction IPO data to empirically test Sherman’s information production model. They find that the unexpected entry of more institutional investors is related to higher expected returns, suggesting that institutional investors bid based on information. The bids of individual investors, in contrast, exhibit evidence of return chasing, and the unexpected entry of more individual investors is related to lower returns, a sign of systematic overbidding perhaps due to inadequate bid shaving. It means that unexpected entry not based on information will lead to a higher clearing price and hence lower returns (Engelbrecht-Wiggans and Katok, 2005). In this paper, I will test the effect of unexpected entry on winning price of land auctions in Taiwan. Other papers discuss land auctions include Ashenfelter and Genesove (1992); and Lusht (1996). These literatures, however, do not examine bidders’ entry decisions and the effects of entry on bid premium.

My sample includes five-hundred-ninety-seven land auctions held by the government in Taiwan during 09/2007–02/2010. Not like many countries that all land virtually owned by the government, land auction by the government in Taiwan is not

2

In a first-price, sealed-bid auction, number of bid is equivalent to the number of bidders, since each bidder may place only one bid.

the only way for developers to obtain new developable land. Developers can obtain land from private sectors. They may decide to enter an auction held by governments based on their own judgment. This gives us less constraint to test whether investors may acquire information and enter an auction held by the government. The dataset, containing land in Taipei City (the core metropolitan area) and in Taipei County (the suburb), allows us to examine potential differences between bidders in different locations. Taipei City is a core area that attracts more attentions. There will be more information on land auction in Taipei City. On the contrast, it is more costly to collect information on land auctions in Taipei County. I want to test whether location will affect how investors collect information, their decisions to enter an auction, and their bidding strategies.

I find that individual bidders’ behavior in Taipei City is very different from those in Taipei County. I first run logistics regressions to test what contribute the success of a land auction. An auction to be successful needs at least one bidder to participate. Empirical results show that previous auction premium (the ratio of winning price over reserve price), building attached to land or not, land use code for residential dummy, and market return are significant factors to induce at least one investor to bid in Taipei City. Evidences show that investors tend to bid in Taipei City’s land auctions when it is a hot market. However, only the dummy of land use code for residential is the significant factor affecting the participation tendency of investors in Taipei County. The number of bid regression shows a similar result that more and more investors tend to bid in hot market in Taipei City, but not in Taipei County.

The bid premium regression shows that in Taipei City, the entry of more investors is not related to higher bids placed by these investors, suggesting that even

contrast, the entry regression of Taipei County auction data tells us that number of bids in Taipei County is hard to predict, making the entry of bids have a significantly impact on winning prices. It indicates that bidders in Taipei County’s auctions tend to be uninformed.

My findings add to the literature regarding investors’ bidding behavior in different locations, a core area and a suburb. I find that bids of investors in Taipei City’s land auctions are largely consistent with the predictions of auction theory regarding informed bidders. Investors in Taipei City’s land auctions place their bids based on information. The bids of investors in Taipei County, in contrast, exhibit evidence of unpredictable, and the entry of investors is related to higher bids placed by these investors, a sign of systematic overbidding.

The article is organized as follows: Section 2 lays out the hypotheses that I will be testing. Section 3 describes the institutional features of land auctions in Taiwan. Section 4 discusses data and methodology used in this paper. Section 5 presents evidence results on entry, while Section 6 presents results on bid premium. Section 7 is the conclusion.

2. Hypotheses

Based on Sherman’s (2005) information production models, investors spend resources on evaluation and choose to enter only if they expect to recover their evaluation and entry costs on average. Sherman’s model predicts that entry decreases with information uncertainty or costs of information production. One important implication of Sherman’s model is that since entry is uncoordinated, there will be ex post fluctuations in entry and in bidders’ bid premium (the ratio of winning price over the reservation price). For an auction to be successful, the auction must at least attract one investor to bid. Therefore, the success of auctions and the number of bids in an

auction will be negatively related to information uncertainty or information cost. Therefore, I have two hypotheses regarding entry of bidders:

Hypothesis 1A. The probability of success in an auction decreases in information

uncertainty or information cost.

Hypothesis 1B. The number of bids decreases in information uncertainty or

information cost.

Sherman’s model also predicts that investors will shave their bids more when they receive more positive information. When there is unexpectedly high entry driven by positive information, the expected value of the shares is higher and thus we expect more bid shaving. Alternatively, there might be naïve bidders who do not follow the optimal entry and bidding strategies. Land in Taiwan is very limited. Developers try to get available land from every possible resource. Potentially, there are many investors decide whether to expend resources producing a more accurate valuation of the land and whether to enter the auction. If participants do not have knowledge of auction theory or experience with auction bidding, they may have difficulty shaving their bids adequately to adjust for the winner’s curse and may therefore overbid systematically. Therefore, I focus on the relationship between the entry of bids and the bid premium. Entry not based on information will lead to a higher winning price.

Giliberto and Varaiya (1989) investigate acquisitions of failed banks. They consider such transaction at first-price, sealed-bid auction. They find evidence that bid premium increases with increased competition, which is consistent with bidder’s failing to adjust for the winner’s curse. Giliberto and Varaiya attempt to distinguish between common value auction and private value auction empirically. The theory of dynamic auctions with private values predicts that more informed bidders should pay

common value auctions. Information asymmetry between participants is shown to influence the premium paid.

I organize the above arguments into two hypotheses regarding bid premium as follows:

Hypothesis 2A. If entry is driven by the entry of informed investors that have

received positive signals, then the number of entry will be negatively related to bid premium.

Hypothesis 2B. If entry is driven by the entry of uninformed investors, then the

number of entry will be positively related to bid premium.

3. Institutional Details of the Taiwan’s Land Auction Market

According to Chapter 6 of National Property Act in Taiwan, selling ways of national property mainly are divided into sale, sale as a special case, sale by tender, sale by tender under current situation, and sale price or listed floor price, unless otherwise specified in other relevant laws, shall base on the stipulations of Article 58 of National Property Act and evaluation methods of the national property to appraise by referring to market price.

Since 2002, the National Property Administration of the Ministry of Finance launched auction method to sell state-owned land for non-public use in three major metropolitan areas in Taiwan. These auctions attract a lot of investors to participate in bidding for state-owned land with large scale. Three regional offices of the National Property Administration, Taipei, Taichung, and Kaohsiung offices conduct public auctions from time to time. In this paper I use data from those auctions conducted by the Taipei branch from 09/2007 to 02/2010.

The public tendering method is the first-price sealed-bid auction. Bidders must submit their bids in a prescribed form and accompanied by a deposit in the form of a

money order or of a bank draft. Under the auction procedure, the administration office will publicly announce the area, location, and other properties of the land, and the reservation price (also known as the floor price), and the dates bidders can submit orders. During the bid-tender period, the administration office is not allowed to open the sealed bids and is explicitly forbidden from revealing bid information in the auction. Bids will be opened in public to determine the winner. The winning price is the maximum bid price among all bids. If there are more than one bid with the same highest bidding price, the winner will be awarded by lottery. When there is no bid for an auction, the auction fails and the public tendering is not completed. In my sample, there were 302 out of 597 auctions failed to induce any bid to participate.

Using data of Taipei City and Taipei County provides an opportunity to further investigate bidders’ behavior in different market segmentation. In Taipei City, the capital city of Taiwan, housing prices are much higher. Hsueh, Li, and Tseng (2002) indicated that house prices in Taipei City are not affected by migration or the labor market, but are exogenously determined. However, on the other hand, for Taipei County, a suburban area of Taipei metropolis, there is a close interaction existing between housing prices and population migration.

The real estate industry in Taipei City was ushered into a new era of luxury housing. The luxury house price in Taipei City skyrocketed 200% from 2006 to 2009. Not only domestic rich investors, but also foreign and Chinese investors are aggressively searching for potential investments. Therefore, housing developers aggressively acquire more land to build luxury mansions. Besides, in terms of better cross-strait relation between Taiwan and China, the demand for commercial building in Taipei City also increases. The sale of state-owned land is a major public issue and

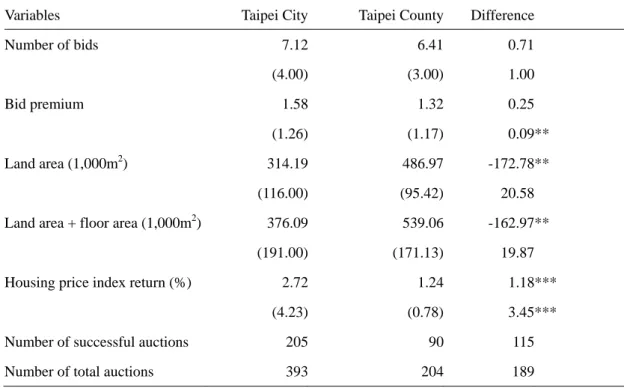

City and immigrate to the neighboring Taipei County, where housing prices are much cheaper. The supply of land in Taipei County is also tight. However, due to new area development plans, land supply in Taipei County is more than that in Taipei City. We can see from Table 2, land area for auction in Taipei County is larger than that in Taipei City.

4. Data and Methodology

My sample includes five-hundred-ninety-seven public tendering of state-owned land in Taipei City and Taipei County during 09/2007–02/2010. I obtain detailed bidding information on each auction from the website of National Property Administration of the Ministry of Finance, number of bids and the bid price of every bid. The dataset also includes information on the land size, the reservation price, land use code, and whether a building is attached or not. Of the five-hundred-ninety-seven land auctions in my sample, two-hundred-ninety-five were successful.

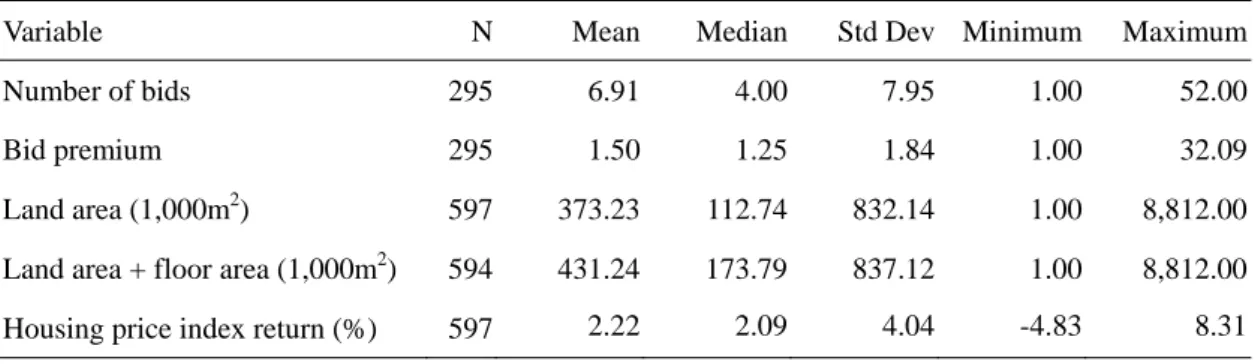

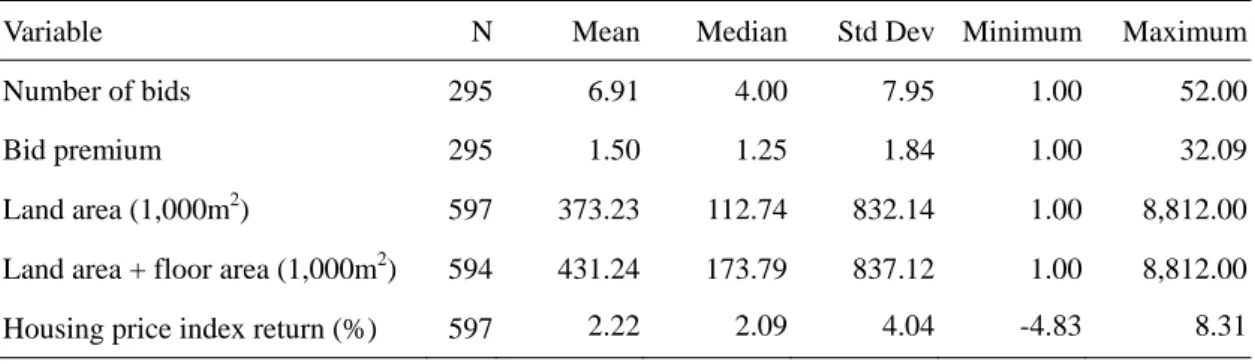

Table 1 presents the descriptive statistics for the land auction sample. Panel A displays the statistics for the entire sample. The average tendering has a land area of 373.23 thousand square meters, a land area plus building area of 431.24 thousand square meters. For a typical successful auction, the average number of bids is 6.91 with a standard deviation of 7.95, and the average bid premium (the ratio of winning price over the reservation price) is 1.50 with a standard deviation of 1.84. Consistent with Sherman’s (2005) model prediction, there are substantial variations in the number of bids and in bid premium.

Panel B of Table 1 displays land auction background information by year. The average number of bid increases from 2007 through 2010, indicating that land auction has become more and more popular as we see market return has also been increased. Another interesting factor, the average bid premium, seems to have a decreasing

trend.

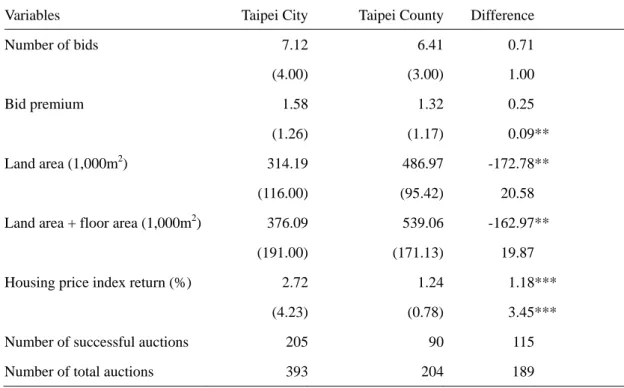

Table 2 presents summary statistics of bidding activities in Taipei City and in Taipei County. We can see the successful ratio in Taipei City (205/393) is higher than that in Taipei County (90/204), and the average number of bids in Taipei City (7.12) is significantly higher than that in Taipei County (6.41). We also see the average land area in Taipei City is smaller than that in Taipei County. Market return calculated based on the housing price index shows that Taipei City had a higher growth rate during the sample period. The competition in Taipei City seems more intensive than that in Taipei County. I predict that bidders in Taipei City’s land auctions will be more likely to expend resources producing a more accurate valuation of the land.

I use bid premium to measure the aggressiveness of bids or the level of optimism of bidders regarding the land value. The bid premium is the ratio of the winning price over the reservation price. The Wilcoxon signed rank test for differences in medians between Taipei City and Taipei County shows that bidders in Taipei City pay higher premium. I have more discussion on this in the bid premium regression analysis.

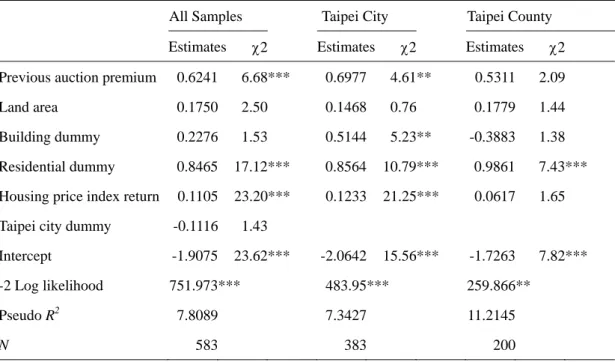

I will examine the factors that influence bidders’ entry decisions. Hypothesis 1 predicts that entry will be higher when information uncertainty or information costs are lower. I have two tests on Hypothesis 1. The first one is a logistic regression to test what factor affecting the success of a land auction:

i i i i i i i i PPM LA BD RD RM CD S =β0 +β1 +β2 +β3 +β4 +β5 +β6 +ε (1) The dependent variable, S, is a dummy variable and equals 1 if the auction is successful and 0 otherwise. I use a set of variables to measure information uncertainty

I therefore include only a dummy variable, BD, to indicate whether there is a building attached to the land. RD is another dummy variable equaling 1 if the land use code is for residential use and 0 otherwise. I include two variables to measure investors’ expectation and market condition: one is the previous auction’s bid premium and the other is the housing index return. To explore how bidders are affected by previous auction result, I include previous auction premium, PPM, into the regression model. Market returns, RM, are calculated based on Housing Price Indexes in Taipei City and in Taipei County. I also include a dummy to distinguish the location in Taipei City and in Taipei County. I run this logistic regression for all sample, and for sample in Taipei City and in Taipei County respectively.

I also test an entry regression using the natural logarithm of the number of bids as the dependent variable:

i i i i i i i i PPM LA BD RD RM CD N) =β0 +β1 +β2 +β3 +β4 +β5 +β6 +ε ln( (2)

According to Sherman’s (2005) information production model, number of bidders will decrease with higher information uncertainty or information cost. I conjecture that the information costs and/or uncertainty about the land decreases with larger land size, building attached to the land, the residential use code, higher previous auction premium, and higher market returns. I run this entry regression for all sample, and for sample in Taipei City and in Taipei County respectively.

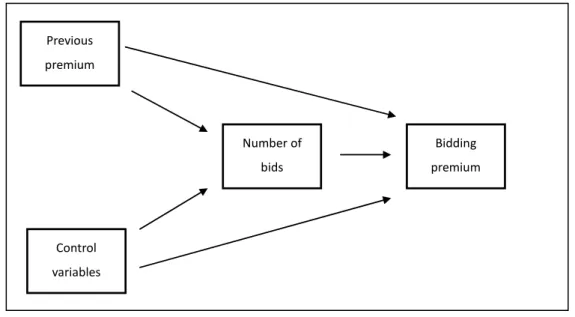

I then examine bidder aggressiveness on land auctions. Especially, I like to know how bid premium is affected by the entry of bids. Since entry and bid premium are both exogenously determined by auction characteristics, I apply structural equation model to estimate how entry can be affectd by different auction characteristics and how bid premium is affected by entry and other auction characteristics. Structural equation modeling (SEM) is a methodology for representing,

estimating, and testing a network of relationships between variables (measured variables and latent constructs).

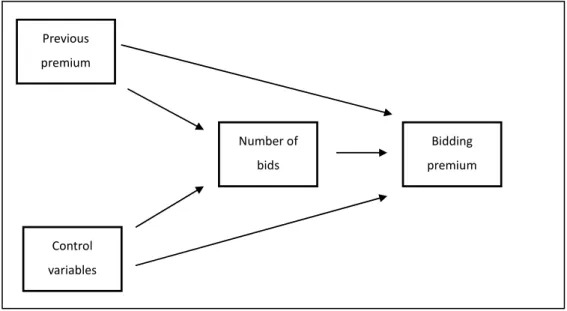

The relation among bid premium, number of entry, and auction characteristics can be describe by Figure 1 as follows:

Figure 1 Path analysis of bid premium, entry and auction characteristics

The structural equation model is as follows:

i i i i i i i i i PPM LA BD RD RM CD N BP =β0 +β1 +β2 +β3 +β4 +β5 +β6 +ln( ) +ε1 i i i i i i i i PPM LA BD RD RM CD N) 0 1 2 3 4 5 6 2 ln( =β +β +β +β +β +β +β +ε (3)

The dependent variable, BP, the bid premium, is the ratio of winning price over the reservation price. .

Hypothesis 2 says that if there are more entry of informed bidders, bid premium will be lower. On the contrast, when there are more uninformed bidders enter the auction, bid premium will be higher. To check which result holds after controlling for other characteristics that are known to influence bid premium, I apply structural

Previous premium Control variables Number of bids Bidding premium

and in Taipei County respectively.

5. Results on Entry into Land Auctions

Logistics Regression on the Success of an Auction

I first run a logistic regression to test what factors attribute to the success of a land auction. For a first-price, sealed-bid land auction to be successful, there must be at least one bidder. Table 2 reports logistic regressions that test whether previous premium and other variables affect the likelihood of auction success. The dependent variable is a dummy equal to one if the land auction was successful. The regressor of interest is the previous premium that bidders observe from the last land auction in the same city area. I control for other variables representing information uncertainty/ information cost. Regression results for all samples show that a land auction is more likely to be successful if the previous auction premium is higher, if the market return is higher, and if the land code is for residential use. When the market is hot, investors tend to participate in a land auction. When the past premium moves from the 25th percentile to the 75th percentile holding the control variable at its mean, the probability of bidding increases from 43.63% to 47.93%. We can also see from Table 3 that a land is coded as residential use is more likely to be acquired. Due to the boom of residential housing market, developers were eager to purchase land for residential projects.

The regression results on success of land auction in Taipei City and in Taipei County are quite different. Investors in Taipei City’s auctions tend to bid in hot market, but it is not true for investor in Taipei County’s auctions. Investors in Taipei County’s auctions care only about whether the land code is for residential use. Office market is not popular in Taipei County. Developers in Taipei County like to

purchase land to develop large scale residential projects.

Regression Results on Number of Bids into Land Auctions

Next, I run regression of number of bids to examine the factors that influence bidders’ entry decisions. Sherman’s (2005) information production model predicts that entry will be higher when information uncertainty or information costs are lower. I use the natural logarithm of the number of bids as the dependent variable to test the effect of a set of variables measuring information uncertainty or information costs. I expect that information costs and/or uncertainty about the land decreases with larger area, the fact that a building is attached to the land, the residential use code for the land, and larger market return. To explore the impact of previous auction result, I also include previous premium as an explanatory variable to explore the impact of this variable on bidder’s entry decision.

Table 4 presents the results of the number of entry regressions. I run three regressions for all samples, samples in Taipei City, and samples in Taipei County respectively. These OLS regression results are different from the logistic regression results. The logistic regression is used to test whether there is at least one bidder to participate in the auction. The OLS regressions here are used to test how many bids will be placed in an auction. For example, the logistic regression results show that with higher previous auction premium, there will be at least one bidder to bid to make the auction to be successful. However, the entry regression shows that larger previous auction premium will not attract more investors to bid. Furthermore, for all samples, larger land area is not critical to the success of an auction, but has a significant power on attracting more bidders to bid.

bids. Larger area also has a significant impact on number of bids. It is interesting to see that market return has a significantly positive relation with the success of an auction, but has no power in explaining how many bidders to bid.

For the auction samples in Taipei County, entry regression results are similar to those of logistic regression. Only the dummy of residential use code is positively significant. What investors in Taipei County’s auctions really care is whether the land can be used for residential purpose or not.

Overall, we see when the information uncertainty or the information cost is lower, number of investors to bid in an land auction are more. Empirical evidences also show that bidders like to bid in Taipei City’s auctions when the previous auction has a larger premium, indicating the competition was intensive.

Previous auction premium affects the entry decision of bidders in Taipei City’s

auctions. In terms of the economic significance of the impact of previous auction

premium on number of bids, if the value of previous auction premium goes from the

twenty-fifth to the seventy-fifth percentile, with other explanatory variables at their mean values, then the expected number of individual bidders increases by 0.09 (6.39-6.30=0.09, 1.26% of the mean number of bids for samples in Taipei City). In contrast, investors’ entry decision in Taipei County is insignificantly related to

previous auction premium.

6. Results on Land Auction Premium

In this section, I examine bid premium, the ratio of the winning price and the reservation price, from land auctions. To see whether bidders optimally shave their bids in different locations, I test Hypotheses 2 by running structural equation models: entry regression on previous premium and measures of information-uncertainty/ information costs, while bid premium regression on previous premium and measures

of information-uncertainty/ information costs, and entry. We see from Table 2 that the average bid premium in Taipei County’s auction samples is smaller than that in Taipei City. However, this phenomenon does not imply that bidders in Taipei County’s land auctions bid more smartly. We must consider how number of bids affect the bid premium in order to make any judgment. I therefore include the number of bids to estimate the bid premium regression.

I also include the previous auction premium in the bid premium regression. If there is a hot market, bidders tend to bid high and one can expect the bid premium on the current land auction to be positively related to the latest auction premium.

Bid premium regression results are reported in Table 5. On Panel A and Panel C, we see bid premiums are positively related to entry for all samples and samples in Taipei County. This result is consistent as predicted in Hypotheses 2B for unsophisticated uninformed bidders. Based on the hypotheses, the positive coefficient for entry suggests that bidders in Taipei County are uninformed and not bidding optimally. On the contrast, the coefficient on entry in Taipei City’s sample is not significant. Bidders in Taipei City’s land auction tend to collect information and bid optimally.

To evaluate the impact of entry on bid premium in Taipei County, I gauge the economic significance of the entry of bids by computing the change in bid premiums when the entry of bids increases by one standard deviation. I find that a one-standard-deviation (0.8698) increase in entry of bids increases the bid premium by 0.2916 (22.09% of the mean bid premium in Taipei County).

The coefficient on previous auction premium is insignificant. Investors did not follow high previous premium to bid high at the current auction. Regarding the

samples in Taipei City. When the land code is for residential use, bidders tend to bid high. It is also interesting to note that for samples in Taipei County, area has a significantly positive relation with bid premium. As I mentioned above, developers in Taipei County like to obtain land for large scale projects.

I also redefine the bid premium as the ratio of AVERAGE bid price over the reservation price. The average bid price include information of those losing bids. As a robustness check, I use this new definition of premium to run the regression. Results are the same.

7. Conclusions

Empirical results indicate that bidders in Taipei City’s land auctions are generally consistent with the predictions for rational informed bidders. Higher previous premium and higher market return may attract more bidders to bid in Taipei City’s auctions. However, these bidders tend to shave their bids optimally. For Taipei City samples, entry of bids is not related to bid premium. Bidders in Taipei City’s auctions did not overbid by paying too high premium. They tend to spend resources to collect information and shave their bids optimally.

On the contrast, bidders in Taipei County’s land auction show a different behavior. For Taipei County samples, bidders’ entry decisions cannot be predicted by previous auction premium or by market return. Entry of bids, therefore, has a significantly positive impact on current auction’s bid premium. Bidders in Taipei County’s land auctions tend to be uninformed and overbid.

Empirical evidences suggest that investors should acquire information in order to avoid overbidding. Sophisticated professional investors can make use of their professional expertise and extensive resources to evaluate a tendered land. Without information, investors tend to participate in a land auction on the spur of the moment.

Entry of these uninformed investors causes investors to overbid, i.e. high winning price.

In a core metropolitan area, like Taipei City, competition for acquiring a land is intensive. Although intensive competition may induce more investors to participate in a land auction, investors tend to expend resource to collect information and to form an optimal bidding strategy. On the contrast, in a suburb area, like Taipei County, competition is not so intensive. Entry of bids becomes less predictable. Shock of bid entry causes overbidding.

References

Ashenfelter, Orley and Genesove, David. (1992). Testing for Price Anomalies in Real-Estate Auctions, American Economic Review, vol. 82(2), 501-05,

Chiang, Yao-Min, Qian, Yiming, and Sherman, Ann. (2010). Endogenous entry and partial adjustment in IPO auctions: Are institutional investors better informed? Review

of Financial Studies, Vol.23, No.3, pp.1200-1230.

Engelbrecht-Wiggans, R., and E. Katok. (2005). Experiments on Auction Valuation and Endogenous Entry. In J. Morgan (ed.), Behavioral and Experimental Economics, pp. 171–96. Stamford, CT: Elsevier Science.

Giliberto M. and Varaiya, N. (1989). The winner’s curse and bidder competition in acquisitions: Evidence from failed bank auctions. Journal of Finance, 44 (1):59–75.

Hsueh, L, Li, C. and Tseng, H. (2002). The Population Migration in Taiwan, and its Causal Relationship with Labor Market and Housing Market, International Real

Estate Review, 2002, vol. 5, issue 1, pages 61-90

Lusht K.M. (1996). A comparison of prices brought by English auctions and private negotiations. Real Estate Economics, 24(4): pp.517-530.

Pagan, A. (1984). Econometric Issues in the Analysis of Regressions with Generated Regressors. International Economic Review 25:221–47.

Sherman, A. (2005). Global Trends in IPO Methods: Bookbuilding versus Auctions with Endogenous Entry. Journal of Financial Economics 78:615–49.

Table 1 Summary statistics of land auctions

The sample includes five-hundred-ninety-seven land auctions in Taiwan during 2007-2010. Land is tendered either in Taipei City (the core area) or in Taipei County (a suburb). Number of bids is the number of bids submitted by investors in an auction. Bid premium is the winning price relative to the reservation price. Housing price index returns are calculated based on Taipei City Housing Index, and Taipei County Housing Index provided by Sinyi Realtor. Panel B shows by year the mean, median (in parentheses), and standard deviation (in square brackets) of each variable.

Panel A,

Variable N Mean Median Std Dev Minimum Maximum

Number of bids 295 6.91 4.00 7.95 1.00 52.00

Bid premium 295 1.50 1.25 1.84 1.00 32.09

Land area (1,000m2) 597 373.23 112.74 832.14 1.00 8,812.00

Land area + floor area (1,000m2) 594 431.24 173.79 837.12 1.00 8,812.00

Housing price index return (%) 597 2.22 2.09 4.04 -4.83 8.31

Panel B,

Year 2007 2008 2009 2010

Mean of number of bids 6.26 6.29 7.19 8.72

(3.00) (4.00) (3.00) (3.00) [7.10] [6.70] [8.75] [9.67]

Mean of bid premium 2.73 1.42 1.35 1.50

(1.28) (1.28) (1.20) (1.27)

[6.42] [0.42] [0.42] [0.61]

Mean of land area (1,000m2) 265.87 499.01 307.55 262.06

Mean of (land area + floor area) (1,000m2) 348.89 537.80 372.87 335.72

Mean of housing index return (%) -0.33 0.22 4.47 2.74

Number of successful auctions 23 119 124 29

Table 2 Summary statistics of bids by locations

The sample includes five-hundred-ninety-seven land auctions in Taiwan during 2007-2010. Land is tendered either in Taipei City (the core area) or in Taipei County (a suburb). Number of bids is the number of bids submitted by investors in an auction. Bid premium is the winning price relative to the reservation price. Housing price index returns are calculated based on Taipei City Housing Index, and Taipei County Housing Index provided by Sinyi Realtor. I use a paired t-test for differences in means, and the Wilcoxon signed rank test for differences in medians between groups. ***, **, and * denote that the difference is significant at the 1%, 5%, and 10% levels, respectively.

Variables Taipei City Taipei County Difference

Number of bids 7.12 6.41 0.71 (4.00) (3.00) 1.00 Bid premium 1.58 1.32 0.25 (1.26) (1.17) 0.09** Land area (1,000m2) 314.19 486.97 -172.78** (116.00) (95.42) 20.58

Land area + floor area (1,000m2) 376.09 539.06 -162.97**

(191.00) (171.13) 19.87

Housing price index return (%) 2.72 1.24 1.18***

(4.23) (0.78) 3.45***

Number of successful auctions 205 90 115

Table 3 Logistics regression of auction success

The dependent variable is a dummy equal to one if a land auction is successful. Previous auction

premium is the premium of last auction in the same location. Land area is measured in one thousand

square meters. Building dummy equals 1 if there is building attached to the land and 0 otherwise.

Residential dummy equals 1 if the land use code is for residential use and 0 otherwise. Housing price index returns are calculated based on Taipei City Housing Index, and Taipei County Housing Index

provided by Sinyi Realtor. Taipei dummy equals 1 if the auctioned land is in Taipei City and 0 otherwise. t-statistics are adjusted using White’s correction for heteroskedasticity. כ, ככ, and כככ denote significance at the 1%, 5%, and 10% levels, respectively.

All Samples Taipei City Taipei County

Estimates χ2 Estimates χ2 Estimates χ2 Previous auction premium 0.6241 6.68*** 0.6977 4.61 ** 0.5311 2.09

Land area 0.1750 2.50 0.1468 0.76 0.1779 1.44

Building dummy 0.2276 1.53 0.5144 5.23 ** -0.3883 1.38

Residential dummy 0.8465 17.12*** 0.8564 10.79 *** 0.9861 7.43 *** Housing price index return 0.1105 23.20*** 0.1233 21.25 *** 0.0617 1.65

Taipei city dummy -0.1116 1.43

Intercept -1.9075 23.62*** -2.0642 15.56 *** -1.7263 7.82 *** -2 Log likelihood 751.973 *** 483.95*** 259.866 **

Pseudo R2 7.8089 7.3427 11.2145

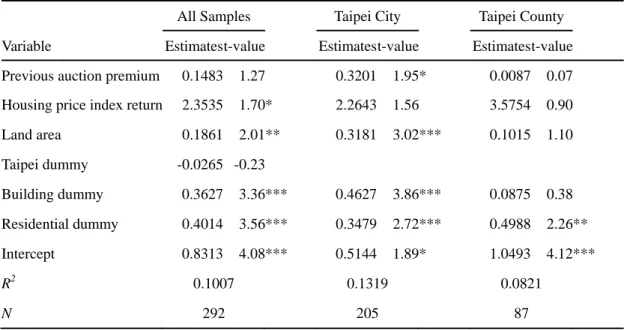

Table 4 Entry regression

The dependent variable is the natural logarithm of the number of bids in an auction. Previous auction

premium is the premium of last auction in the same location. Land area is measured in one thousand

square meters. Building dummy equals 1 if there is building attached to the land and 0 otherwise.

Residential dummy equals 1 if the land use code is for residential use and 0 otherwise. Housing price index returns are calculated based on Taipei City Housing Index, and Taipei County Housing Index

provided by Sinyi Realtor. Taipei dummy equals 1 if the auctioned land is in Taipei City and 0 otherwise. t-statistics are adjusted using White’s correction for heteroskedasticity. כ, ככ, and כככ denote significance at the 1%, 5%, and 10% levels, respectively.

All Samples Taipei City Taipei County

Variable Estimatest-value Estimatest-value Estimatest-value Previous auction premium 0.1483 1.27 0.3201 1.95* 0.0087 0.07 Housing price index return 2.3535 1.70* 2.2643 1.56 3.5754 0.90

Land area 0.1861 2.01** 0.3181 3.02*** 0.1015 1.10 Taipei dummy -0.0265 -0.23 Building dummy 0.3627 3.36*** 0.4627 3.86*** 0.0875 0.38 Residential dummy 0.4014 3.56*** 0.3479 2.72*** 0.4988 2.26** Intercept 0.8313 4.08*** 0.5144 1.89* 1.0493 4.12*** R2 0.1007 0.1319 0.0821 N 292 205 87

Table 5 Premium regression

The dependent variable is the bid premium for each auction, calculated as the winning price divided by the reservation price. Previous auction premium is the premium of last auction in the same location. Entry of bids is the residuals from the entry regressions. Land area is measured in one thousand square meters. Building dummy equals 1 if there is building attached to the land and 0 otherwise. Residential

dummy equals 1 if the land use code is for residential use and 0 otherwise. Housing price index returns

are calculated based on Taipei City Housing Index, and Taipei County Housing Index provided by Sinyi Realtor. Taipei city dummy equals 1 if the auctioned land is in Taipei City and 0 otherwise. כ, ככ, and כככ denote significance at the 1%, 5%, and 10% levels, respectively. Unstandardized parameter estimates retain scaling information of variables and can only be interpreted with reference to the scales of the variables. Standardized parameter estimates are transformations of unstandardized estimates that remove scaling and can be used for informal comparisons of parameters throughout the model. Standardized path coefficients with absolute values less than .10 may indicate a “small” effect. Values around .30 indicate a “medium” effect. Values greater than .50 indicate a “large” effect.

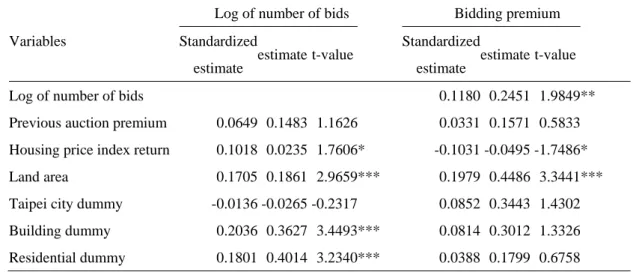

Panel a, all sample

Log of number of bids Bidding premium Variables Standardized

estimate estimate t-value

Standardized

estimate estimate t-value

Log of number of bids 0.1180 0.2451 1.9849 **

Previous auction premium 0.0649 0.1483 1.1626 0.0331 0.1571 0.5833 Housing price index return 0.1018 0.0235 1.7606* -0.1031 -0.0495 -1.7486 * Land area 0.1705 0.1861 2.9659*** 0.1979 0.4486 3.3441 *** Taipei city dummy -0.0136 -0.0265 -0.2317 0.0852 0.3443 1.4302 Building dummy 0.2036 0.3627 3.4493*** 0.0814 0.3012 1.3326 Residential dummy 0.1801 0.4014 3.2340*** 0.0388 0.1799 0.6758

Table 5 Premium regression (continued)

Panel B, Taipei City

Log of number of bids Bidding premium Variables Standardized

estimate estimate t-value

Standardized

estimate estimate t-value

Log of number of bids 0.0480 0.1180 0.6854

Housing price index return 0.1038 0.0226 1.5669 -0.0895 -0.0480 -1.3418 Previous auction premium 0.1122 0.3201 1.7070* -0.0620 0.4348 0.9360

Land area 0.2059 0.3181 3.0784*** 0.3288 1.2485 4.8031***

Building dummy 0.2588 0.4627 3.8636*** 0.1303 0.5727 1.8773* Residential dummy 0.1565 0.3479 2.3825*** 0.0315 0.1719 0.4721

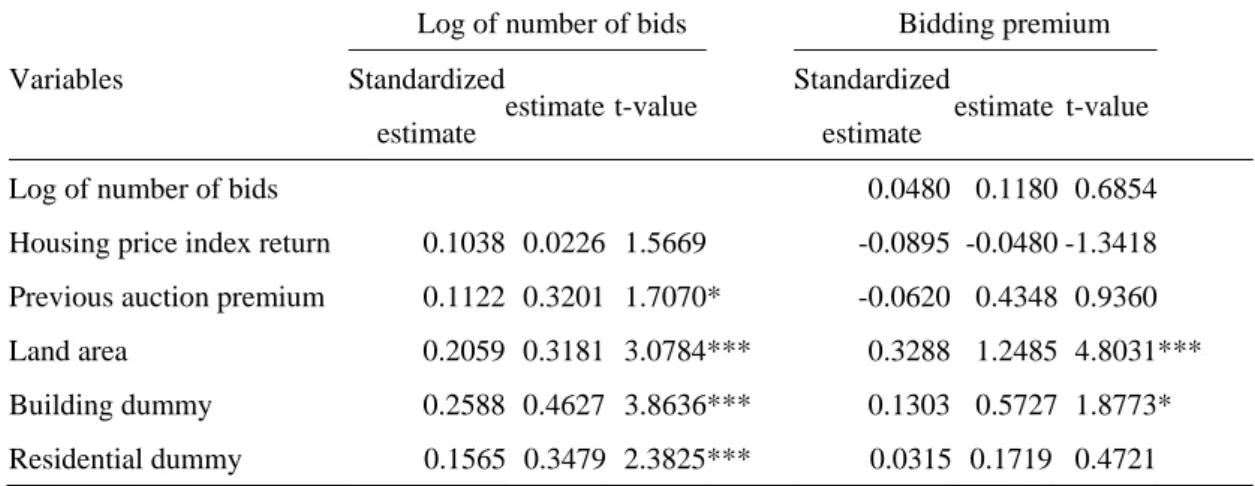

Panel C, Taipei County

Log of number of bids Bidding premium Variables Standardized

estimate estimate t-value

Standardized

estimate estimate t-value

Log of number of bids 0.7607 0.335310.1682***

Housing price index return 0.1107 0.0358 1.0354 -0.0617-0.00878 -0.8267 Previous auction premium 0.0052 0.0087 0.0494 -0.0218 -0.0161 -0.3010

Land area 0.1360 0.1015 1.2522 -0.0482 -0.0159 -0.6339

Building dummy 0.0446 0.0875 0.4112 -0.1733 -0.1498 -2.2994*** Residential dummy 0.2230 0.4988 2.0809** -0.1189 -0.1172 -1.5605

出國報告(出國類別:出國與共同作者討論及參加國際研討會)

目的地:美國芝加哥

時間:101 年 1 月 4 日-101 年 1 月 10 日

討論對象:

J. Sa-Aadu, Professor, the University of Iowa.

YimingQian, Associate Professor, the University of Iowa.

Michelle Lowry, Associate Professor, Penn State University.

Chun Chang, Professor, Shanghai Advanced Institute of Finance

參加會議:2012 Allied Social Science Associations Annual Meeting 中的

American Finance Association Annual Meeting 及 American Real Estate and Urban Economic Association Annual Meeting

服務機關:國立政治大學商學院 姓名職稱:姜堯民教授 派赴國家:美國芝加哥

出國期間:101 年 1 月 4 日-101 年 1 月 10 日 報告日期:101 年 1 月 16 日

出國成果報告書(格式) 計畫編號1 NSC100-2410-H-004-085 執行單位2 政治大學財管系 出國人員 姜堯民 出國日期 101 年 1 月 4 日至 101 年 1 月 10 日,共 7 日 出國地點3 美國芝加哥 出國經費4 國科會補助

前往美國芝加哥參加 2012 Allied Social Science Associations Annual Meeting 中的 American Finance Association Annual Meeting 及 American Real Estate and Urban Economic Association Annual Meeting,以及與共同作者討論研究:J. Sa-Aadu, Professor, the University of Iowa; YimingQian, Associate Professor, the University of Iowa; Michelle Lowry, Associate Professor, Penn State University; 以及 Chun Chang, Professor, Shanghai Advanced Institute of Finance。

主要行程

1/4 出發及抵達美國芝加哥。

1/5 報到,傍晚參加 Shanghai Advanced Institute of Finance, Shanghai Jiao Tong University 的茶會。

1/6 上午與 Yiming Qian 討論,中午與 Chun Chang 討論,下午與 Michelle Lowry 討論。晚上與 DePaul University 的 James Shilling 討論及晚宴

1/7 上午與 J. Sa-Aadu 討論,參加 AFA 及 AREURA 研討會,聆聽報告。中午 與系上老師湛可南討論此次赴會心得。晚上參加 AREURA 的 reception

1/8 參加 AFA 及 AREURA 研討會,聆聽報告。 1/9 離開芝加哥。

1/10 回到台灣。

The Allied Social Science Association (ASSA) 是由 the American Economic Association (AEA) 所主導,聯合許多學術團體所組成的聯合會,其中包括 the American Finance Association 及 AREURA 等。聯合年會每年在 1 月上旬舉行, 每回都有上千人與會,是國際上非常重要的會議。趁著許多學者都會參加這個重 要的會議,我也趁機來參加會議,聆聽新的研究報告,同時跟共同作者一起討論 研究案。

A.與 Yiming Qian 及 Chun Chang 討論 Emerging Stock Market project 討論重點: 研究上市前的交易資料有助於制訂政策,尤其是美國目前才在發展類似台灣的興 櫃市場。這個計畫要盡快做,有時效性。 1.我們要研究興櫃市場交易是否有助於新股上市時的正確定價? a. 興櫃市場的交易較格與新股上市後佳格之間的關連性 b. 討論有哪些因素會影響上述的關聯性 2.如果興櫃市場的交易有助於訂價的正確性,則其可以降低資訊不對稱。那資訊 不對稱因子對新股上市期初報酬得影響就會變小。 1單位出國案如有 1 案以上,計畫編號請以頂大計畫辦公室核給之單位計畫編號 + 「-XX(單位自編 2 位出國案序號)」型式為之。如僅有 1 案,則以頂大計畫單位編號為之即可。 2執行單位係指頂大計畫單位編號對應之單位。 3出國地點請寫前往之國家之大學、機關組織或會議名稱。 4出國經費指的是實際核銷金額,單位以元計。

B.與 Yiming Qian 及 Michelle Lowry 討論自營商交易對新上市股票績效的影響 討論重點 討論新股上市後自營商的交易,尤其是分成與原先承銷有無關聯的自營商來看這 些交易會不會影響新股上上後的股價報酬。初步結果證實主辦承的後續自營交易 確實會影響股票報酬。 1.問題在於它們的交易是出自於價格穩定操作嗎?還是在出清原先的持股? 2. 所測度的交易期間必須做 robustness check 3.盈餘宣告的影響 C.與 J. Sa-Aadu 的討論

Referee 要我們加入 Pay-option ARM 於貸款選擇的模式中。

模型必須調整成 5 期模型。利率必須按比例調整成跟 30 年期貸款相類比。Balloon mortgages 改為 2/3 期模型。

希望檢定 pay-option ARM 不適合長期貸款人選擇這一個假說。及選用 pay-option ARM 會使借款人效用降低的這一個假說。

4.參加 AFA 及 AREURA 研討會

積極聆聽多場報告,尤其是 David Hirshleifer 所主持的 Behavioral Finance 場次, Jay Ritter 所主持的 IPOs and SEOs 的場次。本系湛可南教授的文章在這個場次發 表。也參加 James Shilling 主持的 Pricing and commercial real estate 的場次,以 及其他多場。 採行之建議事項: 1. 每年有許多人來參加這個盛會,可惜的是台灣來的學者並不多。可鼓勵及補 助老師多多參加這個會議。 2. 即使是沒文章發表,也應該來參加這個研討會。可以看到新的研究方向,認 識知名學者,尋求合作機會,趁機與共同作者討論研究。一舉數得。 3. 也趁機參加幾場各個學校所各自舉辦的 reception。誠如本系湛可南教授建 議,未來也可辦一場政大或是以台灣為名義的 reception,與國際學者交流。 4. 許多學校也趁機面試教師。未來我們要聘新的教師也可以利用這個研討會面 試新人。 出國人簽名: 姜堯民 日期:2/01/2012 連絡人: 分機:81140

出國報告審核表 出國報告名稱:出國與共同作者討論及參加國際研討會 出國人姓名 職稱 服務單位 姜堯民 教授 財務管理系 出國類別 考察進修 V 研究實習 V 其他國際會議(例如國際會議、國際比賽、業務接洽等) 出國期間: 101 年 1 月 4 日至 101 年 1 月 10 日 報告繳交日期:101 年 01 月 16 日 計 畫 主 辦 機 關 審 核 意 見 1.依限繳交出國報告 2.格式完整(本文必須具備「目的」、「過程」、「心得及建議事項」) 3.無抄襲相關出國報告 4.內容充實完備 5.建議具參考價值 6.送本機關參考或研辦 7.送上級機關參考 8.退回補正,原因:不符原核定出國計畫以外文撰寫或僅以所蒐集外文資 料為內容內容空洞簡略或未涵蓋規定要項抄襲相關出國報告之全部或 部分內容電子檔案未依格式辦理未於資訊網登錄提要資料及傳送出國 報告電子檔 9.本報告除上傳至出國報告資訊網外,將採行之公開發表: 辦理本機關出國報告座談會(說明會),與同仁進行知識分享。 於本機關業務會報提出報告 其他 10.其他處理意見及方式: 審核 人 一級單位主管 機關首長或其授權人員 說明: 一、 各機關可依需要自行增列審核項目內容,出國報告審核完畢本表請自行保存。 二、 審核作業應儘速完成,以不影響出國人員上傳出國報告至「政府出版資料回應網 公務出國報告專區」為原則。

出國報告(出國類別:出國參加國際研討會及與 Professor James Shilling 討論)

目的地:新加坡

時間:101 年 7 月 7 日-101 年 7 月 10 日

參加會議:The 2012 AsRES - AREUEA Joint International Conference

討論對象:James Shilling, Professor, De Paul University.

服務機關:國立政治大學商學院 姓名職稱:姜堯民教授

派赴國家:新加坡

出國期間:101 年 7 月 7 日-101 年 7 月 10 日 報告日期:101 年 7 月 16 日

出國成果報告書(格式) 計畫編號1 NSC100-2410-H-004-085 執行單位2 政治大學財管系 出國人員 姜堯民 出國日期 101 年 7 月 7 日至 101 年 7 月 10 日,共 4 日 出國地點3 新加坡 出國經費4 國科會補助

前往 The 2012 AsRES - AREUEA Joint International Conference,以及與 Professor James Shilling 討論合作計畫。

主要行程

7/7 出發及抵達新加坡。傍晚報到,參加歡迎茶會,與多位學者見面。 7/8 參加會議,報告文章,及評論文章。參加晚宴。

7/9參加會議,晚宴上認識Penn State University 的Coulson教授。Coulson教 授是國際著名學者,曾來台灣訪問,說很喜歡台灣。宣布明年年會在京都舉行, 是Professor Yuichiro Kawaguchi, Waseda University 負責舉辦,我與

Kawaguchi教授認識多年,明年一定去參加。 7/10 回國。 亞洲房地產學會(AsRES)每年會在 7 月份於亞洲不同城市舉辦年會,高雄剛於 2010 年辦過,今年是在新加坡舉行。通常會與美國的 AREUEA 一起舉行。每回都 會吸引 300 餘人與會,是國際上非常重要的房地產學術會議。這一回我有兩篇文 章被接受發表。同時趁著參加這個重要的會議,也可以認識許多國際上重要的學 者,向他們請教,討論。同時也跟 Professor Shilling 一起討論研究案。 A. 參與會議

此次參加2012 AsRES & AREUEA 聯合年會最重要的工作是要發表兩篇文章 1. Mortgage Contract Choice Decision in the Presence of the Balloon

Mortgages

這篇文章主要是在探討當借款人面臨不同貸款契約時,如何做最適的選擇。借款 人的選擇會受到市場利率高低,借款人收入高低,及借款人提前清償機率大小等 因素的影響。

本文探討在不同條件底下,借款人如何做選擇。

2. Evidence on the Endogenous Entry of Bidders in Land Auctions 這篇文章是我獨力完成,也受到國科會的研究獎勵,這一回到會議上發表是一個 成果驗收。 這篇文章是在探討投標人是否會因為市場不確定性高低,資訊成本高低而影響其 參與投標的意願。另一主題是參與投標者的多寡是否會影響到得標的高低。 結果發現參與台北市土地標售的投標人多會事前蒐集資訊以決定是否參與競 標,新北市的投標人較隨性參與。 1單位出國案如有 1 案以上,計畫編號請以頂大計畫辦公室核給之單位計畫編號 + 「-XX(單位自編 2 位出國案序號)」型式為之。如僅有 1 案,則以頂大計畫單位編號為之即可。 2執行單位係指頂大計畫單位編號對應之單位。 3出國地點請寫前往之國家之大學、機關組織或會議名稱。 4出國經費指的是實際核銷金額,單位以元計。

台北市的參與人數增加並不會顯著造成得標價格的上升,但在新北市則明顯為正 向關係,顯示新北市投標人較不會蒐集資訊就來參與投標。

同時,這個研討會中,我有幫忙評論了兩篇文章。

1. The Study on the Relationships among the Housing Price, the Regulation of Mortgage Finance Market, and the Performance of Banking Industry: The International Evidence

這篇文章討論房價偏離程度如何影響到銀行放款績效,而上述關係的強弱會受到 政府對銀行放款管制政策的影響。

2. Pricing of PreSale Contracts with Macroeconomic Factors and Stochastic Basis Risk 這篇文章以遠期契約模型來討論預售屋房價的訂定。 B.與 Professor Shilling 討論可能的合作計畫 Professor Shilling 發表許多重要文章與國際頂級期刊,著作等身,最重要的 是他的研究中心有許多重要的房地產資料可以供研究使用。 C.積極聆聽多場報告

有許多的報告非常有趣,尤其是Professor Riddiough, University of Wisconsin 提到早在100年前,Wisconsin就發生過2008年的金融風暴,原因都 出在房屋抵押貸款的違約上。他探討該事件的原因及與2008年金融風暴相似之 處及可供借鏡之處。 金沙集團總經理介紹了該集團在新加坡發展情形及對新加坡經濟的影響,馬祖 剛通過要設賭場,新加坡的經驗正可做參考。 美國Ginnie Mae總裁介紹美國房地產市場現況,復甦很慢,金融風暴受創很重。 採行之建議事項: 1. 臺灣每年都有許多人來參加這個盛會,表現都很不錯是該標線不錯。 2. 房地產領域的學者多會來參加這個會議,應多鼓勵年輕學者來參加,認識這 些學者,像我一樣,尋求合作機會。 出國人簽名: 姜堯民 日期:7/16/2012 連絡人: 分機:81140

出國報告審核表 出國報告名稱:出國與共同作者討論及參加國際研討會 出國人姓名 職稱 服務單位 姜堯民 教授 財務管理系 出國類別 考察進修 V 研究實習 V 其他國際會議(例如國際會議、國際比賽、業務接洽等) 出國期間: 101 年 7 月 7 日至 101 年 7 月 10 日 報告繳交日期:101 年 7 月 16 日 計 畫 主 辦 機 關 審 核 意 見 1.依限繳交出國報告 2.格式完整(本文必須具備「目的」、「過程」、「心得及建議事項」) 3.無抄襲相關出國報告 4.內容充實完備 5.建議具參考價值 6.送本機關參考或研辦 7.送上級機關參考 8.退回補正,原因:不符原核定出國計畫以外文撰寫或僅以所蒐集外文 資料為內容內容空洞簡略或未涵蓋規定要項抄襲相關出國報告之全部 或部分內容電子檔案未依格式辦理未於資訊網登錄提要資料及傳送出 國報告電子檔 9.本報告除上傳至出國報告資訊網外,將採行之公開發表: 辦理本機關出國報告座談會(說明會),與同仁進行知識分享。 於本機關業務會報提出報告 其他 10.其他處理意見及方式: 審核 人 一級單位主管 機關首長或其授權人員 說明: 一、 各機關可依需要自行增列審核項目內容,出國報告審核完畢本表請自行保存。 二、 審核作業應儘速完成,以不影響出國人員上傳出國報告至「政府出版資料回應網 公務出國報告專區」為原則。

AsRES & AREUEA Joint International Conference 2012, Singapore (update till 22nd June 2012) PRE-CONFERENCE SESSION PS 1 Regional / Urbanization 7 July 2012, Saturday 09:00 - 11:00 Chair: Seow Eng Ong, National University of Singapore Begonia 3011

No. Author (s) Affiliation Title

045 Zhigang Nie Kwok Chun Wong

The University of Hong Kong Paradox or Corollary: Social Cost Analysis in Urban Village Renewals

062 Chamna Yoon University of Pennsylvania The Decline of the Rust Belt: A Dynamic Spatial Equilibrium Analysis

228 Fang-Ni Chu Chin-Oh Chang Ngai-Ming Yip

National Chengchi University Performance Evaluation of Condominiums among Taipei, Hong Kong and Shanghai: From a Perspective of Institutional and Communitarian Approaches to Collective Action

184 Hsiao Jung Teng Chin-Oh Chang

National Chengchi University Contagious Housing Bubbles Force Housing Price Diffusion

PS 2

Housing Choice

7 July 2012, Saturday 09:00 - 11:00 Chair: Kim Hiang Liow, National University of Singapore Begonia 3012

No. Author (s) Affiliation Title

196 Ha Na Im Chang Gyu Choi

Hanyang University Study on the Historical Origins of the Chonsei System in South Korea

089 Moosang Cho Sogang University A Study on the Effect of Baby Boomers' Retirements on Housing Market in Korea

064 Pei-Syuan Lin Chin-Oh Chang

National Chengchi University Which Do You Want, House or Children? The Connection between Household’s Fertility Decision and First-Time House Buying

156 Yi-Hsuan Lin Chien-Wen Peng

National Taipei University Housing Affordability and Homeownership Rate in Taipei

AsRES & AREUEA Joint International Conference 2012, Singapore (update till 22nd June 2012)

National University of Singapore | Department of Real Estate | Institute of Real Estate Studies 16

PS 3

House Price Dynamics

7 July 2012, Saturday 11:00 - 13:00 Chair: Yong Tu, National University of Singapore Begonia 3011

No. Author (s) Affiliation Title

214 Zhongyu He Asami Yasushi

University of Tokyo A Conjoint Analysis of the Revealed and Stated Preference Methods for Housing Valuation in Beijing

072 Ning Chai Seoul National University Research on the Effectiveness of the Macro-control Policies Aiming for Curbing the Rapidly Rising Housing Prices in China

105 Bin Li Suodi Zhang

Taiyuan University of Science and Technology

Real Estate Return Evaluation: A Cross-City Analysis of China

046 Jian Chen Gao Bo

Nanjing University Can Real Estate Provide a Hedge against Inflation? Evidence from China

024 Daisy Huang Charles Leung Baozhi Qu

City University of Hong Kong Can Credit and Location Choice explain the House Price Inflation in China?

019 Fang Zhang University of Bath Modelling Housing Market in China: a Dynamic Panel Data Model

PS 4

Spatial Development & Transportation

7 July 2012, Saturday 11:00 - 13:00 Chair: Seow Eng Ong, National University of Singapore Begonia 3012

No. Author (s) Affiliation Title

066 Hajime Seya Yoshiki Yamagata Morito Tsutsumi

National Institute for Environmental Studies

Automatic Selection of a Spatial Weight Matrix in Spatial Econometrics: Application to a Spatial Hedonic Approach

212 Daisuke Murakami Morito Tsutsumi

University of Tsukuba Geostatistical Model that Considers Spatial Autocorrelation Affected by a Transportation Network

069 Jianfu Shen University of Hong Kong Binomial Option Models for Practical Real Estate Development

216 Doo Hwan Go Choi Chang Gyu

Hanyang University The Commuting Behaviors in the Suburban New Towns in the Seoul Metropolitan Area (SMA)

AsRES & AREUEA Joint International Conference 2012, Singapore (update till 22nd June 2012)

PhD panel on “Publishing in RE journals” 7 July 2012, Saturday 13:00 - 14:00

Begonia 3011

Chaired by Associate Professor Joseph Ooi, National University of Singapore Panels Members:

Professor Edward Coulson, Penn State University Professor Ko Wang, Baruch College/CUNY

ARGUS Technology Session 7 July 2012, Saturday 13:00 - 14:00

Begonia 3012

ARGUS Technology Session by

Jeffrey Fisher, President, Homer Hoyt Institute and Global Consultant to ARGUS and Real Capital Analytics

PS 5 Land

7 July 2012, Saturday 14:00 - 16:00 Chair: Grace Wong, National University of Singapore Begonia 3011

No. Author (s) Affiliation Title

163 Xiao Hu Renmin University of China Study on Collective Land Transfer and Theory of Economic Organization Property Right in China: Referring to the Reforming Experience of State-Owned Enterprises Property Right

114 Dapeng Xiu Ping Lv Shuang Li

Renmin University of China Study on Effects of Land Supply System on Old-Age Care Institutions Developing Institutions Developing in China

085 Wen-lu Li Ping Lv Mei-ling Luo

Renmin University of China Study on the System of Section Land Price Index Real-Time Measuring Method Based on GIS

099 Nestor Garza Colin Lizieri Danilo Igliori

AsRES & AREUEA Joint International Conference 2012, Singapore (update till 22nd June 2012)

National University of Singapore | Department of Real Estate | Institute of Real Estate Studies 18

PS 6 REITs

7 July 2012, Saturday 14:00 - 16:00 Chair: Kim Hiang Liow, National University of Singapore Begonia 3012

No. Author (s) Affiliation Title

197 Annisa Dian Prima Simon Stevenson Peter Wyatt

University of Reading Asian REITs Investment Decision in the Presence of Free Cash Flow

160 Ranajit Bairagi William Dimovski

Deakin University The Underwriting Syndicate Structure and the Indirect Costs of REIT SEOs

067 Jianfu Shen University of Hong Kong Ownership Structure, Corporate Governance and Firm Performance: Evidences from Real Estate Development in China

052 Eva Steiner Jamie Alcock

University of Cambridge Capital Structure Choices and The Management of Exposure to Inflation

162 Bo Xiong Kunhui Ye

Chongqing University, China A Preliminary Study on Corporate Social Responsibility of Large Real Estate Companies in China

PS7 Others

7 July 2012, Saturday 16:00 - 18:00 Chair: Lawrence Chin, National University of Singapore Begonia 3012

No. Author (s) Affiliation Title

048 Wenjie Ding University of Pennsylvania Policy Intervention, Ownership Structure and China's Housing Market

044 Pil-Won Huh Yong-Hoon Choi Hyo-Mook Lim Gyo-Eon Shim

Konkuk University A Study of Comovement and Factors Causing Volatility in REIT Returns Before and After the Global Financial Crisis - Centered on the U.S., Japan, Singapore, and Hong Kong Markets-

217 Yilan Xu University of Pittsburgh Does Mortgage Deregulation Increase Foreclosures? Evidence from Cleveland

131 Hassan Gholipour Fereidouni

Universiti Sains Malaysia Foreign Real Estate Investments and House Prices: Evidence from Emerging Economies

51 Kazuki Tamesue Morito Tsutsumi

University of Tsukuba Interdependence Between Land Prices and Population Migration in Tokyo Metropolitan Area

7 July 2012 (Saturday) – Pre-Conference Session

08:00 - 17:00 Registration

09:00 – 18:00

Sessions: PS (1) , PS (2) , PS (3) , PS (4) , PS (5) , PS (6) , PS (7) PhD Panel on “Publishing in RE Journals”

ARGUS Technology Session Board Meeting (I) 18:00 - 19:30 Welcome Reception

Lotus Ballroom (4D & 4E)

19:00 - 21:00 Board Dinner (by invitation only) 8 July 2012 (Sunday)

08:00 - 15:00 Registration

08:45 - 09:15

Opening:

Associate Professor Yu Shi Ming, President, Asian Real Estate Society

Professor Timothy Riddiough, President, American Real Estate and Urban Economics Association Guest of Honour, Mr Lee Yi Shyan, Minister of State (National Development & Trade and Industry)

Cassia Jnr Ballroom

09:15 - 09:45 1st Keynote Speech by Professor William Strange

Cassia Jnr Ballroom

09:45 - 10:00 Tea Break Parallel Session A

10:00 - 12:15

Session A1

Commercial Real Estate

Cassia Jnr Ballroom

Session A2

Real Estate Investment I

Begonia 3011

Session A3

Housing Economics / Econometrics I

Begonia 3012 Session A4 Green / Sustainability Begonia 3111 Session A5 Housing Studies I Begonia 3112 Session A6 Housing Market I Hellconia 3413 12:15 - 13:15

Lunch Talk by Mr Theodore W. Tozer President, Ginnie Mae

Heliconia Jnr Ballroom

Parallel Session B

13:15 - 15:30

Session B1

Real Estate / Financial Markets

Cassia Jnr Ballroom

Session B2

China Real Estate

Begonia 3011

Session B3

Urban / Social Planning

Begonia 3012

Session B4

House Price / Index I

Begonia 3111 Session B5 Housing Studies II Begonia 3112 Session B6 Housing Market II Hellconia 3413 15:30 - 15:45 Tea Break Parallel Session C 15:45 - 18:00 Session C1 REIT - Finance Cassia Jnr Ballroom Session C2

Real Estate Investment II

Begonia 3011

Session C3

Housing Economics / Econometrics II

Begonia 3012

Session C4

Housing Studies III

Begonia 3111

Session C5

Valuation / Transaction - Based Studies

Session C6

Real Estate Development and Pricing