治稅以法 服務以誠

Tax by the Law Service from the Heart

Vision, Mission and Values

VISION

We aim to be an excellent tax administration that plays an important part in promoting Hong Kong’s prosperity and stability.

MISSION

We are committed to –

• collecting revenue efficiently and cost-effectively;

• providing courteous and effective service to the taxpaying public;

• promoting compliance through rigorous enforcement of law, education and publicity programmes; and

• enabling staff to acquire the necessary knowledge, skills and attitude so that they can contribute their best to the achievement of our vision.

VALUES

Our core values are –

• Professionalism

• Efficiency

• Responsiveness

• Fairness

• Effectiveness

• Courtesy

• Teamwork

1

Contents

Chapter 1 Commissioner’s Foreword Chapter 2 Revenue

Chapter 3 Assessing Functions Profits Tax

Salaries Tax Property Tax

Personal Assessment Tax Treaty Network

Advance Pricing Arrangement Automatic Exchange of Financial

Account Information Automatic Exchange of

Country-by-Country Reports Advance Rulings

Objections

Appeals to the Board of Review Appeals to the Courts

Business Registration Stamp Duty

Estate Duty Betting Duty

Tax Reserve Certificates

Chapter 4 Collection Collection of Tax Refund of Tax

Recovery of Tax in Default

Chapter 5 Field Audit and Investigation Field Audit

Investigation

Property Tax Compliance Check

Chapter 6 Taxpayer Services IRD Website

Electronic Enquiry Service Enquiry Service Centre

Tax-help Services for Completion of Tax Returns

Complaints and Compliments

Chapter 7 Information Technology IT Environment

Electronic Services

Chapter 8 Human Resources Organisation Chart Establishment

Staff Promotions and Turnover Training and Development Staff Relations and Welfare The IRD Sports Association

Chapter 9 Legislative Amendments Chapter 10 Environmental Report

Green Management Policy Green Management and

Promotion of Green Awareness Environmental Protection

Performance in 2019-20 New Initiatives and Targets

Chapter 11 Miscellaneous Charitable Institutions General Inspection Internal Audit

Approval for Tax Return Forms and the Manner of Furnishing Tax Returns

Schedules

2

1 Commissioner’s Foreword

I am pleased to present the 2019-20 Annual Report of the Inland Revenue Department.

The year 2019-20 was full of challenges and uncertainties. Badly hit by the combined effects of local social incidents, global economic slowdown and escalated US-China trade tensions, the Hong Kong economy entered recession in the third quarter of 2019. Stepping into 2020, the Hong Kong economy turned even worse as a result of the threat of the COVID-19 epidemic on global trade and local consumption-related activities. Overall, the Department’s total revenue collection fell by 11.1% ($37.9 billion) to $303.6 billion in 2019-20. The two main tax types, namely profits tax and salaries tax, together dropped over $20 billion in total.

Tax collections in 2019-20 mainly came from tax demand notes for the year of assessment 2018-19. The decrease in profits tax collection was partly attributable to the implementation of the two-tiered profits tax rates regime effective from the year of assessment 2018-19. The profits tax rate for the first $2 million of assessable profits is reduced to half of the standard rate. Besides, in the relief measure announced in August 2019, the Government further increased the tax reduction for salaries tax, tax under personal assessment and profits tax for the year of assessment 2018-19 from 75% to 100%, while retaining the ceiling of $20,000.

Consequently, over a million taxpayers had left the tax net, leading to a drop in tax revenue.

Hong Kong adopts a provisional tax system. Provisional tax for the year of assessment 2019-20 was also charged in the 2018-19 tax demand notes. As affected by the worsened economic condition, some taxpayers

3 encountered financial difficulties. Besides, the Government announced on 4 December 2019 conditional waiver of surcharges for instalment settlement of demand notes for the year of assessment 2018-19. Hence, the number of applications from taxpayers for holding over of 2019-20 provisional tax and instalment payment surged, leading to a reduction of tax collection in 2019-20.

Further, two factors had affected the progress of the Department’s assessment work, which in turn had impacted the 2019-20 tax revenue. Firstly, the Inland Revenue (Amendment) (Tax Concessions) Bill 2019, the object of which was to give effect to the tax concessions for the year of assessment 2018-19, was only passed by the Legislative Council in November 2019. The Department started issuing tax demand notes from December 2019 onwards, a delay of 4 months as compared to past years.

Secondly, in order to reduce the risk of the spread of COVID-19 in the community, the Department implemented special work arrangement in February and March 2020, which to a certain extent affected the issue of assessments. Some tax demand notes were issued later than as planned, resulting in the deferral of tax payment due dates to the financial year 2020-21.

For stamp duty, decreases both in the total number of property transactions in 2019-20 and in the number of residential property transactions chargeable with buyer’s stamp duty had caused a drop of $12.8 billion in the total stamp duty collection for the year 2019-20. With the waiver of business registration fees for 2019- 20, the amount of business registration fees and penalties collected in 2019-20 was reduced to $189 million, representing a huge drop of 93.3%.

On the front of international tax cooperation, steady progress was attained in 2019-20. As at 31 March 2020, Hong Kong has signed comprehensive avoidance of double taxation agreements or arrangements covering various types of income with 43 jurisdictions, and signed tax information exchange agreements with 7 jurisdictions. In addition, Hong Kong smoothly completed the first and second rounds of automatic exchange of financial account information in tax matters with other jurisdictions through the Organisation for Economic Cooperation and Development (OECD) Common Transmission system in 2018 and 2019 respectively. To facilitate Hong Kong entities to comply with their reporting obligations and implementation of automatic exchange of country-by-country (CbC) reports, the Department launched the CbC Reporting Portal for submission of returns and data files in March 2018. Hong Kong has smoothly completed the automatic exchange of CbC reports for 2018 with exchange partners.

4

To address tax challenges arising from the digitalisation of the economy and Base Erosion and Profit Sharing issues, the OECD is developing new rules for the allocation of taxing rights for profits of digitalised businesses and the prevention of shifting of profits by multinational enterprises to no or low tax jurisdictions. Currently, the goal is to deliver a consensus-based long term solution by mid-2021. These proposals will have far- reaching implications for Hong Kong’s existing tax system and tax treaties as well as multinational enterprises.

The Department will continue to work with the relevant bureau to monitor the developments, make assessments and devise corresponding measures.

Under the leadership of my predecessor, Mr WONG Kuen-fai, and support from colleagues, the Department had gone through a difficult year 2019-20. With public health and safety as our foremost concern amid the COVID-19 epidemic, the Department will endeavor to continue providing services to members of the public and taxpayers. Like all Hong Kong citizens, we hope to see the epidemic fade away soon, the economy recover and life return to normal.

TAM Tai-pang

Commissioner of Inland Revenue

5

Revenue 2

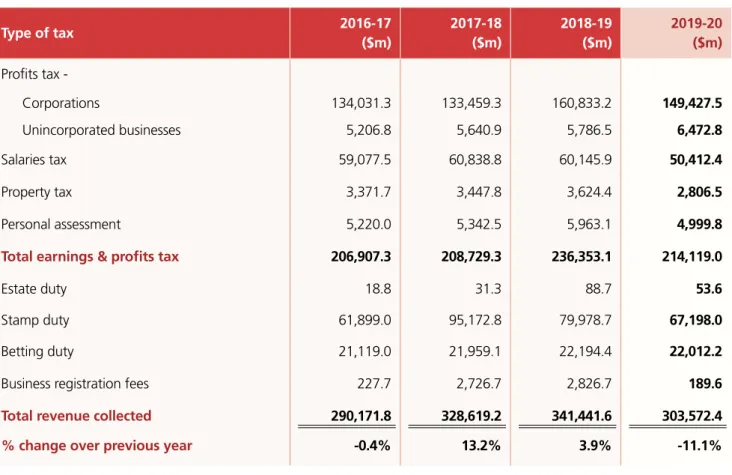

In 2019-20, the Inland Revenue Department collected $303.6 billion which represents a decrease of $37.9 billion or 11.1% as compared with the previous year. The decrease was due to the fall in stamp duty, salaries tax and profits tax (corporations). Stamp duty collections and salaries tax collections both dropped by 16% to

$67.2 billion and $50.4 billion respectively. Profits Tax (corporations) collections dropped by 7.1% to $149.4 billion. Owing to the waiver of business registration fees, collection of business registration fees dropped sharply by 93.3% to $0.2 billion. An analysis of the revenue collected by tax type is provided in Figure 1.

Figure 1 Revenue collected by tax type

Type of tax 2016-17

($m)

2017-18 ($m)

2018-19 ($m)

2019-20 ($m) Profits tax -

Corporations 134,031.3 133,459.3 160,833.2 149,427.5

Unincorporated businesses 5,206.8 5,640.9 5,786.5 6,472.8

Salaries tax 59,077.5 60,838.8 60,145.9 50,412.4

Property tax 3,371.7 3,447.8 3,624.4 2,806.5

Personal assessment 5,220.0 5,342.5 5,963.1 4,999.8

Total earnings & profits tax 206,907.3 208,729.3 236,353.1 214,119.0

Estate duty 18.8 31.3 88.7 53.6

Stamp duty 61,899.0 95,172.8 79,978.7 67,198.0

Betting duty 21,119.0 21,959.1 22,194.4 22,012.2

Business registration fees 227.7 2,726.7 2,826.7 189.6

Total revenue collected 290,171.8 328,619.2 341,441.6 303,572.4

% change over previous year -0.4% 13.2% 3.9% -11.1%

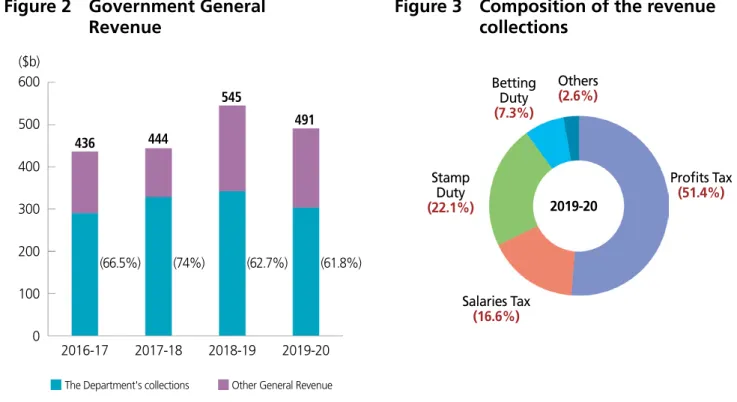

The revenue collected by the Department during 2019-20 accounted for 61.8% of the Government General Revenue (Figure 2). Profits tax and salaries tax contributed 68% of the total revenue collected while stamp duty made up a further 22.1% (Figure 3).

6

Figure 2 Government General Revenue

(66.5%) (74%) (62.7%) (61.8%) 600

500 400

300 200

100 0

436

The Department's collections Other General Revenue

444

545

491

2016-17 2017-18 2018-19 2019-20 ($b)

Figure 3 Composition of the revenue collections

Betting (7.3%)Duty

Others (2.6%)

Profits Tax (51.4%) Stamp

(22.1%)Duty

Salaries Tax (16.6%)

2019-20

In 2019-20, the cost of collection increased from 0.48% to 0.56% (Figure 4).

Figure 4 Cost of collection

1

0.5

0

0.48

0.56

2016-17 0.55

0.48

2017-18 2018-19 2019-20 (%)

7

Assessing Functions 3

The Department raises revenue through taxes, duties and fees in accordance with the relevant legislation.

Earnings and profits tax are assessed by reference to the incomes / profits of the taxpayers in the previous year, whereas duties and fees are charged at the time the relevant activities occur. For 2019-20, earnings and profits tax assessed decreased by $5.8 billion (2.4%) (Schedule 2) as compared with the previous year. The total amount of duties and fees collected decreased by $15.6 billion (14.9%).

Profits Tax

Profits tax is levied on individuals, corporations, bodies of persons and partnerships, in respect of assessable profits arising in or derived from Hong Kong. The two-tiered profits tax rates regime has been implemented since the year of assessment 2018-19. The profits tax rate for the first $2 million of assessable profits is 8.25%

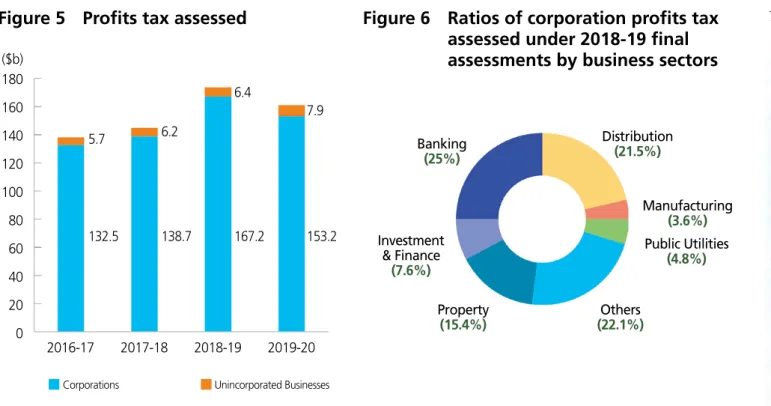

for corporations and 7.5% for unincorporated businesses. Profits above that amount is subject to the tax rate of 16.5% and 15% respectively. For two or more connected entities, only one of them may elect the two- tiered profits tax rates. The amount of profits tax assessed in 2019-20 was $161.1 billion, which was $12.5 billion (7.2%) less than that of the previous year (Figure 5).

The amounts of final tax assessed in respect of different business sectors are shown in Schedules 3 and 4.

Of the total final tax assessed for the year of assessment 2018-19, the property, financial and banking sectors together contributed 48% and the distribution sector generated 21.5% (Figure 6).

Figure 5 Profits tax assessed

132.5 5.7

138.7 167.2 153.2

6.2

6.4

7.9 180

160 140 120 100 80 60 40 20 0 ($b)

Corporations Unincorporated Businesses

2016-17 2017-18 2018-19 2019-20

Figure 6 Ratios of corporation profits tax assessed under 2018-19 final assessments by business sectors

Manufacturing (3.6%) Distribution

(21.5%) Banking

(25%)

Public Utilities (4.8%) Property

(15.4%) Investment

& Finance (7.6%)

Others (22.1%)

8

Salaries Tax

Salaries tax is charged on all incomes from any office (e.g. a directorship) or employment and pension arising in or derived from Hong Kong. The total amount of tax payable is restricted to the standard rate (15%) on the net total income (without deduction of allowances) of the individual concerned.

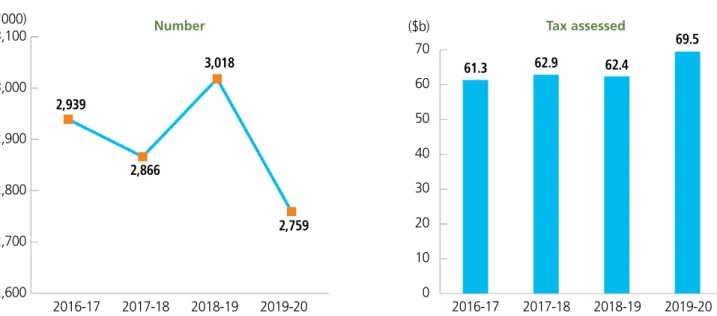

As compared with the previous year, the number of salaries tax assessments made during 2019-20 decreased by 8.6%. However, the growth in wages and earnings has resulted in a 11.4% increase in the amount of tax assessed (Figure 7).

Figure 7 Salaries tax assessments

3,100

3,000

2,900

2,800

2,700

2,600

2,759 2,939

2,866 Number

3,018 ('000)

2019-20 2016-17 2017-18 2018-19

($b) Tax assessed

70 60 50 40 30 20 10 0

61.3 62.9 62.4

69.5

2016-17 2017-18 2018-19 2019-20 Analyses of salaries tax assessments and allowances granted in respect of taxpayers at various income levels for the year of assessment 2018-19 are provided in Schedules 5 and 6.

For the year of assessment 2018-19, the number of standard rate taxpayers decreased by 3,706 to 24,689.

These taxpayers together contributed 37.6% of the final salaries tax assessed, a drop of 2.8% compared with last year (Figure 8).

Figure 8 Salaries Tax - standard rate taxpayers

Percentage of total number of taxpayers

Year of Assessment 2017-18 2018-19

Total number of taxpayers 1,869,593 1,837,824

Standard rate taxpayers 28,395 24,689

Percentage 1.5% 1.3%

9

Figure 8 Salaries Tax - standard rate taxpayers (continued)

Percentage of total final tax assessed

Year of Assessment 2017-18 2018-19

Total final tax assessed ($M) 60,379 63,258

Final tax contributed by standard rate taxpayers ($M) 24,369 23,800

Percentage 40.4% 37.6%

Notification Requirements of Employers

Employers are required to notify the Department of commencements and cessations of employment as well as employees’ impending departure from Hong Kong for more than 1 month. Besides, employers are required to prepare annual employer’s returns to report the emoluments of each of their employees. During the year, 400,693 employers filed employer’s returns with the Department.

The Department provides e-Seminars and disseminates tax information to employers on the IRD website to help them understand the relevant statutory requirements. The contents cover completion of employer’s returns, employer’s obligations and answers to frequently asked questions. Employers can also obtain specimens of completed employer’s returns and notification through the Fax-A-Form service.

Property Tax

Property owners (including corporations) are subject to property tax which is charged at the standard rate (15%) in respect of the net assessable value of the property. Rents received from properties solely owned by individuals should be declared in Tax Returns-Individuals (BIR60); whilst rents received from properties jointly owned or co-owned by individuals or properties held by corporations / bodies of persons should be declared in Property Tax Returns (BIR57 / BIR58). Property owners that pay property tax in respect of premises used for their businesses can have such payments set off against their profits tax liabilities. For corporations, income arising from properties owned by them is also subject to profits tax at the corporation rate. To obviate the need for yearly set-off of property tax against profits tax, a corporation can apply for exemption of property tax on the property concerned.

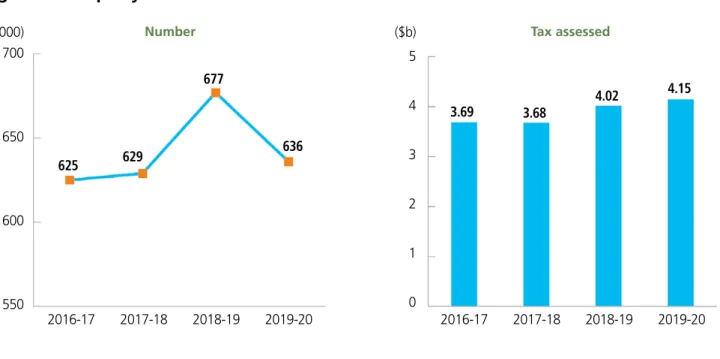

Statistics on the classification of properties and classification by number of owners, based on the records of the Department, are provided in Schedule 7. The number of assessments made in 2019-20 was less than that in the previous year by 6.1%. The amount of property tax assessed increased by 3.2% (Figure 9).

10

Figure 9 Property tax assessments

700

650

600

550

625 629

Number 677

636 ('000)

2016-17 2017-18 2018-19 2019-20

($b) Tax assessed

5

4

3

2

1

0

3.69 3.68 4.02 4.15

2016-17 2017-18 2018-19 2019-20

Personal Assessment

If an individual has income chargeable to profits tax and/or property tax, the individual may elect for personal assessment. Under personal assessment, all the incomes of the taxpayer are aggregated and, after deduction of allowances, are assessed at the progressive tax rates applicable to salaries tax. From the year of assessment 2018-19 onwards, a married person may elect for personal assessment separately from or jointly with the person’s spouse. In appropriate circumstances, this would reduce the tax liability of the taxpayer or the total tax liability of the taxpayer and the taxpayer’s spouse.

As compared with the previous year, the number of personal assessments made in 2019-20 decreased by 6.8%

and the amount of tax assessed was 11.3% lower (Figure 10).

Figure 10 Assessments made under personal assessment

450

400

350

384

373

Number

410

382 ('000)

7 6 5 4 3 2 1

5.28 5.36

6.03

5.35

($b) Tax assessed

11

Tax Treaty Network

Double taxation arises where the same item of income or profit of a taxpayer is subject to tax in Hong Kong as well as in another tax jurisdiction. A wide tax treaty network can help minimise exposure of Hong Kong residents and residents of the tax treaty partners to double taxation. It will also facilitate the flows of trade, investment and talent between Hong Kong and the rest of the world, and enhance Hong Kong’s competitiveness as an international financial, investment and commercial hub.

As at 31 March 2020, Hong Kong has signed comprehensive avoidance of double taxation agreements / arrangements (CDTAs) with 43 jurisdictions, which cover various types of income. They are Austria, Belarus, Belgium, Brunei, Cambodia, Canada, the Mainland of China, the Czech Republic, Estonia, Finland, France, Guernsey, Hungary, India, Indonesia, Ireland, Italy, Japan, Jersey, Korea, Kuwait, Latvia, Liechtenstein, Luxembourg, Macao Special Administrative Region, Malaysia, Malta, Mexico, the Netherlands, New Zealand, Pakistan, Portugal, Qatar, Romania, Russia, Saudi Arabia, South Africa, Spain, Switzerland, Thailand, the United Arab Emirates, the United Kingdom and Vietnam.

To comply with the international standard on exchange of information, Hong Kong entered into tax information exchange agreements (TIEAs) with appropriate partners since 2014. As at 31 March 2020, Hong Kong has signed TIEAs with 7 jurisdictions. They are Denmark, the Faroes, Greenland, Iceland, Norway, Sweden and the United States of America.

Hong Kong is committed to enhancing tax transparency and preventing tax evasion. The Central People’s Government has deposited a declaration to the Organisation for Economic Cooperation and Development (OECD) for extending the application of the Convention on Mutual Administrative Assistance in Tax Matters (the Convention) to Hong Kong. With the entry into force of the Convention in Hong Kong on 1 September 2018, Hong Kong can now ride on a multilateral platform under the Convention to implement various forms of administrative co-operation in the assessment and collection of taxes, including exchange of information on request, automatic exchange of financial account information and automatic exchange of country-by-country reports and spontaneous exchange of information on tax rulings under the base erosion and profit shifting package promulgated by the OECD.

Advance Pricing Arrangement

An Advance Pricing Arrangement (APA) is an arrangement that determines in advance an appropriate set of criteria for the determination of the transfer pricing of cross-border transactions between associated enterprises over a fixed period of time. The APA process gives enterprises the opportunity to reach agreements with tax administrations on the method of applying the arm’s length principle so that transfer pricing issues can be more efficiently dealt with in real time, thus avoiding the risk of transfer pricing audit later. This arrangement enables enterprises to better assess their tax exposure and facilitates their business operation.

12

A unilateral APA is an arrangement between the Commissioner and the enterprise concerning the transfer pricing of its cross-border transactions with an associated enterprise. As the APA process does not involve the agreement with a CDTA partner, it does not guarantee the agreement of the CDTA partner to the arrangement made.

A bilateral APA is an arrangement between the Commissioner and the competent authority of a CDTA partner concerning the transfer pricing of cross-border transactions. It provides certainty to enterprises that double taxation will not arise. The same also applies to a multilateral APA which is a similar arrangement involving the partners of two or more CDTAs.

The Department rolled out the APA programme in April 2012 and introduced a statutory APA regime in July 2018. Up to 31 March 2020, the Department has received quite a number of unilateral and bilateral APA applications which involve CDTA with different partners including the Mainland of China, Italy, Japan, Korea, Malaysia, the Netherlands, Thailand and the United Kingdom. These cases are currently under different stages of the APA programme and a few of them have already been completed.

Automatic Exchange of Financial Account Information

For the purpose of enhancing tax transparency and combating cross-border tax evasion, the OECD released in July 2014 a new international standard for automatic exchange of financial account information in tax matters (AEOI). In September 2014, Hong Kong indicated its support for implementing AEOI on a reciprocal basis with appropriate partners with a view to commencing the first exchanges in 2018. So far, over 100 jurisdictions have committed to implementing this international standard.

Hong Kong put in place a legislative framework for implementing AEOI in 2016. Furthermore, the Department has developed the AEOI Portal to facilitate reporting financial institutions to fulfil their obligations related to AEOI.

Hong Kong will only conduct AEOI with a reportable jurisdiction when an arrangement is in place with the reportable jurisdiction concerned to provide the basis for exchange. Hong Kong first adopted a bilateral basis in implementing AEOI. Later, after the Convention came into force in Hong Kong on 1 September 2018, Hong Kong has been able to take a multilateral approach in implementing AEOI. Hong Kong’s network for tax information exchange has been expanded accordingly.

Hong Kong smoothly completed the first and second rounds of AEOI with other jurisdictions through the OECD Common Transmission system in 2018 and 2019 respectively.

13

Automatic Exchange of Country-by-Country Reports

Hong Kong put in place a legislative framework for implementing the country-by-country reporting in 2018.

The requirements for filing a country-by-country return only apply to a multinational enterprise group whose annual consolidated group revenue reaches the specified threshold amount of HK$6.8 billion. The primary obligation of filing a country-by-country return is on the ultimate parent entity resident in Hong Kong. A Hong Kong entity of a reportable group whose ultimate parent entity is not resident in Hong Kong will be subject to a secondary obligation of filing if certain conditions are met. The mandatory filing of country-by- country return commenced for accounting period beginning on or after 1 January 2018.

To facilitate Hong Kong entities to comply with their reporting obligations and implementation of automatic exchange of country-by-country reports, the Department has launched the CbC Reporting Portal for submission of returns and data files. Hong Kong has smoothly completed the automatic exchange of country- by-country reports for 2018 with exchange partners.

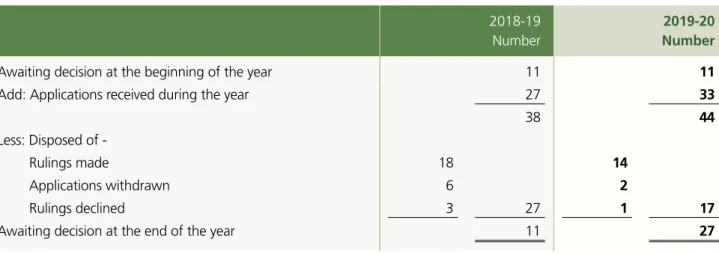

Advance Rulings

Taxpayers may apply for an advance ruling on how a provision of the Inland Revenue Ordinance applies in relation to a particular arrangement. A fee is charged for the service on a “cost recovery” basis. The applicant is required to pay an initial application fee of $45,000 for a ruling concerning the application of the “Territorial Source Principle” in a profits tax case, or $15,000 for a ruling on any other matter. An additional fee is payable if the processing time exceeds the specified limit. The Department endeavours to respond within 6 weeks of the date of application, provided that all relevant information is supplied with the application and further information from the applicant is not required.

During 2019-20, the Department completed the processing of 17 advance ruling applications (Figure 11).

Most of the applications were for rulings on profits tax matters.

Figure 11 Advance rulings

2018-19 Number

2019-20 Number

Awaiting decision at the beginning of the year 11 11

Add: Applications received during the year 27 33

38 44

Less: Disposed of -

Rulings made 18 14

Applications withdrawn 6 2

Rulings declined 3 27 1 17

Awaiting decision at the end of the year 11 27

14

Objections

A taxpayer who is aggrieved by an assessment may lodge a notice of objection to the Commissioner within the prescribed time limit. If the objection is against an estimated assessment raised in the absence of a tax return, a properly completed return, together with the supporting accounts where applicable, must also be accompanied with the notice of objection. A significant proportion of the objections received each year arise from estimated assessments. Most of these objections are settled promptly by reference to the returns subsequently received. Many of the other types of objections are also settled by agreement between the taxpayers and the assessors concerned. Only relatively few objections are ultimately referred to the Commissioner for determination. During 2019-20, the Department completed the processing of 60,737 objections (Figure 12).

Figure 12 Objections

2018-19 Number

2019-20 Number

Being processed at the beginning of the year 41,303 43,233

Add: Received during the year 95,314 55,207

136,617 98,440

Less: Disposed of -

Settled without determination 92,801 60,069

Determinations:

Assessments confirmed 277 353

Assessments reduced 176 169

Assessments increased 124 130

Assessments annulled 6 583 93,384 16 668 60,737

Being processed at the end of the year 43,233 37,703

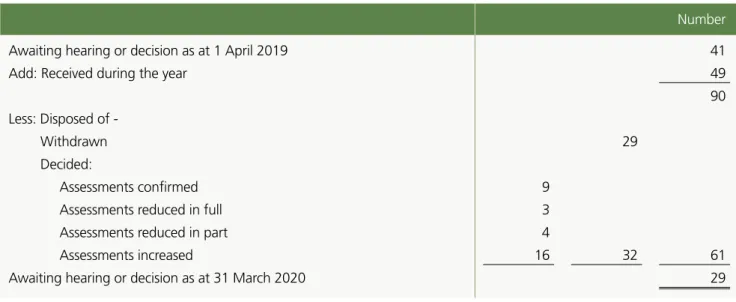

Appeals to the Board of Review

A taxpayer who is dissatisfied with the Commissioner’s determination of his objection may appeal to the Board of Review (Inland Revenue Ordinance) (the Board). The Board is an independent statutory body. As at 31 March 2020, the Board consisted of a chairman and 8 deputy chairmen, who have legal training and experience, as well as 69 members. During 2019-20, the Board settled 61 appeal cases (Figure 13).

15

Figure 13 Appeals to the Board of Review

Number

Awaiting hearing or decision as at 1 April 2019 41

Add: Received during the year 49

90 Less: Disposed of -

Withdrawn 29

Decided:

Assessments confirmed 9

Assessments reduced in full 3

Assessments reduced in part 4

Assessments increased 16 32 61

Awaiting hearing or decision as at 31 March 2020 29

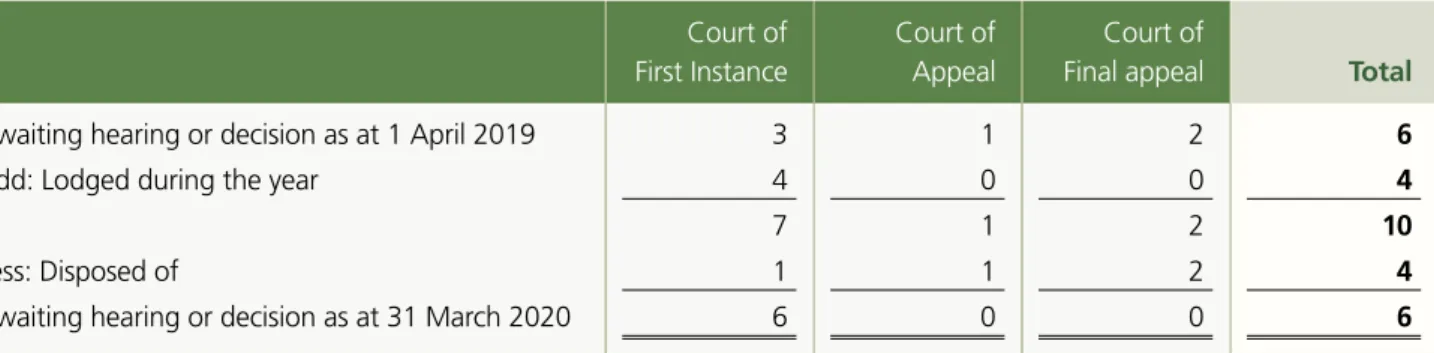

Appeals to the Courts

A decision of the Board is final, provided that either the taxpayer or the Commissioner may, pursuant to section 69 of the Inland Revenue Ordinance, appeal to the Court of First Instance against the Board’s decision on a question of law. Before 1 April 2016, taxpayers or the Commissioner may only appeal to the court by way of case stated from the Board. With effect from that date, the case stated procedure was abolished and no appeal may be made unless leave to appeal has been granted by the court, on the application of the taxpayer or the Commissioner.

During 2019-20, the Court of First Instance ruled that a sum received after termination of employment should not be chargeable to tax. The Court also heard a tax appeal where the deductibility of amortisation of spectrum utilization fees was in dispute.

During the year, the Court of Appeal dismissed an appeal by the Commissioner relating to additional tax assessments. The Commissioner has filed an application for leave to appeal.

The Hong Kong Court of Final Appeal Ordinance provides that, a taxpayer or the Commissioner may, with the leave of the Court of Appeal or the Court of Final Appeal, appeal against the judgment of the Court of Appeal. During 2019-20, the Court of Final Appeal handed down two judgments on appeals lodged by the Commissioner. In one case, the Court ruled that the taxpayer did not change its intention with respect to a piece of land, and the sum received was not chargeable to tax. In another case, certain benefit accrued upon termination of employment was held not chargeable to tax.

Figure 14 sets out the statistics concerning appeals to the Courts during 2019-20.

16

Figure 14 Appeals to the Courts

Court of First Instance

Court of Appeal

Court of

Final appeal Total

Awaiting hearing or decision as at 1 April 2019 3 1 2 6

Add: Lodged during the year 4 0 0 4

7 1 2 10

Less: Disposed of 1 1 2 4

Awaiting hearing or decision as at 31 March 2020 6 0 0 6

Business Registration

The Department aims to maintain an efficient business registration system. A person carrying on a business in Hong Kong must register the business and pay the required fee and levy. The number of business registrations as at 31 March 2020 stood at 1,537,116. It was 19,365 more than that as at 31 March 2019 (Figure 15).

Figure 15 Number of business registrations

1,600 1,400 1,200 1,000 800 600 400 200 0

1,270,982 1,261,002

266,134 256,749

31.3.2020 31.3.2019

('000)

1,537,116 1,517,751

Corporations Unincorporated Businesses

Business registration certificates are generally valid for one year, but businesses may elect for 3-year certificates. As at 31 March 2020, 27,208 businesses held 3-year certificates.

To help business enterprises, the Government waived the business registration fees for 2019- 20. Businesses were still required to pay the levy on their business registration certificates.

For a 1-year certificate, the levy was $250. For

businesses electing for 3-year certificates, they were required to pay $3,200 for the business registration fees and $750 for the levy.

Businesses that were not required to renew their registration certificates in 2019-20 could obtain concessionary refunds if they had paid the registration fees for that year. Up to 31 March 2020, the Department had issued concessionary refunds to 36,889 businesses totaling $46 million.

Due to the waiver of business registration fees for the whole financial year 2019-20, the amount of business registration fees and penalties collected in 2019-20 was reduced to $189 million. It represents a significant decrease of 93.3% compared with last year, notwithstanding that 1.2% more certificates were paid (Figure 16). Business registration statistics are set out in Schedule 8.

17

Figure 16 Business registration statistics

2018-19 2019-20 Increase/Decrease

Number of certificates paid (Main and Branch) 1,517,791 1,536,705 +1.2%

Fees (inclusive of penalties) collected ($m) 2,826 189 -93.3%

Under the Business Registration Ordinance, a small business with average monthly sales or receipts below a specified limit ($10,000 for businesses deriving profits mainly from the sale of services, and $30,000 for other businesses) can apply for exemption from payment of the business registration fee and levy. Where an application for exemption is not allowed, the business operator may appeal to the Administrative Appeals Board. The number of exemptions granted during 2019-20 was 11,403, representing a decrease of 31.5%

from the previous year. No appeal case was received by the Board during 2019-20 (Figure 17).

Figure 17 Appeals to the Administrative Appeals Board

2018-19 Number

2019-20 Number

Awaiting hearing at the beginning of the year 0 1

Add: Lodged during the year 2 0

2 1

Less: Disposed of -

Appeal allowed 0 0

Appeal dismissed 0 1

Appeal withdrawn 1 1 0 1

Awaiting hearing at the end of the year 1 0

Stamp Duty

Stamp duty is charged on instruments effecting property transactions, stock transactions and leasing of property in Hong Kong (Figure 18).

Figure 18 Composition of stamp duty collections

Shares (50%)

Immovable Properties

(49%) Leases etc.

(1%)

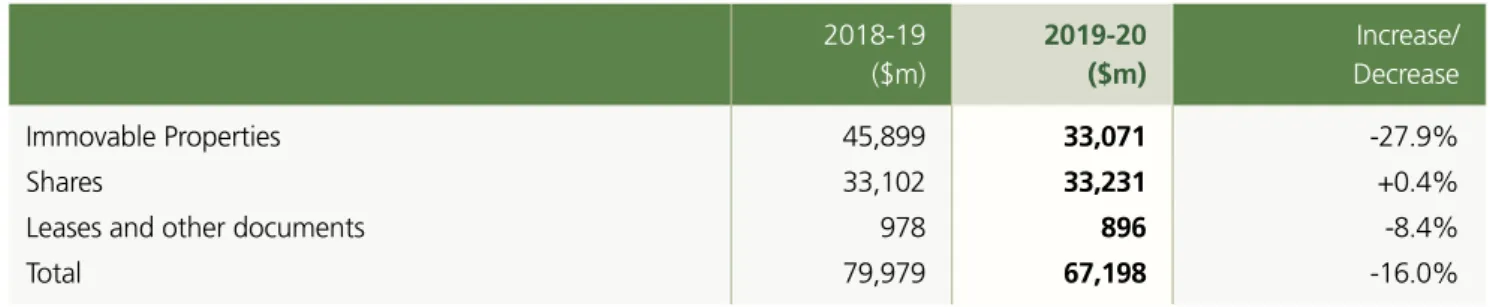

2019-20 Overall, there was a decrease of 16% ($12.8 billion) in the

total stamp duty collection for the year 2019-20 (Figure 19 and Schedule 9). The decrease in the total stamp duty collection is attributable to the following factors:

(1) There was a decrease in the number of property transactions in 2019-20 when compared with that for 2018-19.

18

(2) There was a decrease in the number of residential property transactions in 2019-20 chargeable with buyer’s stamp duty.

Figure 19 Stamp duty collections

2018-19 ($m)

2019-20 ($m)

Increase/

Decrease

Immovable Properties 45,899 33,071 -27.9%

Shares 33,102 33,231 +0.4%

Leases and other documents 978 896 -8.4%

Total 79,979 67,198 -16.0%

Estate Duty

Estate duty is charged on a deceased person’s estate situated in Hong Kong. The threshold for levying duty is $7.5 million and the duty rates range from 5% to 15%, depending on the value of the estate.

The Revenue (Abolition of Estate Duty) Ordinance 2005 came into effect on 11 February 2006 abolishing estate duty in respect of persons who passed away on or after that date. The estate duty chargeable in respect of estates of persons died between the period 15 July 2005 to 10 February 2006, with the principal value exceeding $7.5 million, is reduced to a nominal amount of $100.

The number of new cases stood at 454 in 2019-20, a decrease of 17.6% from the last year (Figure 21).

Figures 20 and 21 show the composition of estates and cases processed for the past two years.

Figure 20 Composition of estates

87%

33% 16%

13%

37%

5%

9%

2018-19

2019-20

Immovable Properties Quoted Shares Unquoted Shares

Bank Deposits Others

Figure 21 Estate duty cases

2018-19 Number

2019-20 Number

New cases 551 454

Cases finalised

- Dutiable 2 7

- Exempt 565 448

567 455

19 Estate duty of $53 million was collected during the year (Schedule 10), a decrease of $35 million (40%) compared with the previous year.

Estate duty is payable on delivery of an estate duty affidavit or account (or within 6 months from the date of the deceased’s death, whichever is the earlier). $3.8 million was received during the year in advance of the issue of formal assessments (Schedule 10).

Betting Duty

Betting duty is charged on the net stake receipts from betting on horse races and football matches and on the proceeds of Mark Six lotteries, all administered by the Hong Kong Jockey Club. In 2019-20, the rates of betting duty on these betting activities remained unchanged (Figure 22).

Figure 22 Rates of betting duty in 2019-20

Rate Horse racing

Local bets on local horse races Net stake receipts

the first $11 billion 72.5%

the next $1 billion 73%

the next $1 billion 73.5%

the next $1 billion 74%

the next $1 billion 74.5%

the remainder 75%

Local bets on non-local horse races Net stake receipts 72.5%

Mark Six lotteries Proceeds 25%

Football betting Net stake receipts 50%

The total betting duty collected in 2019-20 was 0.8% lower than that of the previous year (Figure 23 and Schedule 11).

Figure 23 Betting duty collections

2018-19 2019-20 Increase/

Decrease

($m) ($m)

Horse racing 12,696.7 12,341.1 -2.8%

Mark Six lotteries 1,987.1 1,931.6 -2.8%

Football betting 7,510.6 7,739.5 +3.0%

Total 22,194.4 22,012.2 -0.8%

20

Tax Reserve Certificates

Taxpayers may purchase Tax Reserve Certificates (TRCs) under two situations.

The first situation applies to taxpayers who wish to save for the payment of their future tax liabilities. The Department has set up two schemes, namely the “Electronic Tax Reserve Certificates Scheme” for all taxpayers and the “Save-As-You-Earn” (SAYE) Scheme for civil servants and civil service pensioners. With a Tax Reserve Certificate account, taxpayers may purchase TRCs by various channels, including bank auto-pay, telephone, the Internet and bank ATM. Under the “SAYE Scheme”, civil servants and civil service pensioners can purchase TRCs through monthly deductions from their salaries / pensions. Interest is payable on the TRCs when they are redeemed for settlement of tax liabilities, based on the interest rate prevailing at the time of purchase, for a maximum period of 36 months from the date of purchase.

In 2019-20, there was a decrease of 3% in the number but an increase of 6.9% in the amount of TRCs sold under the “Electronic Tax Reserve Certificates Scheme”. For the “SAYE Scheme”, a decrease of 1.8%

and 0.9% respectively was noted in the number and amount of TRCs sold (Schedule 12). Overall, the total amount of TRCs sold increased by 5.5% (Figure 24).

The second situation applies to taxpayers who object to tax assessments and are required to purchase TRCs in respect of the tax in dispute. Such TRCs are used to settle any tax found payable upon the finalisation of the objection or appeal. Interest is only payable on the amount of the TRC, if any, subsequently required to be repaid to the taxpayer, and is computed at floating rates over the tenure of the TRC.

Figure 24 Certificates sold

100

80

60

40

20

0 1,713 1,196

88,932 86,767

2018-19 2019-20

('000)

Certificates relating to Objections and Appeals Number

442.7 467

2018-19 2019-20

4,500 4,000 3,500 3,000 2,500 2,000 1,500 1,000 500 0

2,514.2 4,177.5

($m)

Certificates other than for Objections and Appeals Amount

21

Collection 4

Revenue collected by the Department includes tax, additional tax, surcharge and fines. Schedules 13 and 14 provide details of additional tax, surcharge and fines imposed by the Department in respect of earnings and profits tax during 2019-20.

Collection of Tax

Taxpayers can conveniently settle their tax liabilities by various payment methods, including electronic payment (by phone, bank ATM or via the Internet), payment in person or payment by post. From November 2019, taxpayers can also pay the bills of the Department via Faster Payment System (FPS). For earnings and profits tax, electronic payment remains the most popular.

Refund of Tax

Tax refunds were made mainly due to two reasons, namely, overpayment of tax by taxpayers and revision of assessments. There were 702,358 refund cases in 2019-20, representing a decrease of 7.3%. The total amount of refunds was $20.49 billion, representing a decrease of $0.52 billion or 2.5% compared with the previous year (Figure 25).

Figure 25 Tax refunds

2018-19 2019-20

Type of tax Number Amount ($m) Number Amount ($m)

Profits tax 60,585 9,303.7 59,643 10,168.4

Salaries tax 616,193 5,472.1 536,758 4,813.0

Property tax 20,650 240.8 15,423 169.3

Personal assessment 36,599 541.0 26,883 469.8

Others 23,689 5,459.5 63,651 4,872.8

Total 757,716 21,017.1 702,358 20,493.3

Recovery of Tax in Default

Taxpayers should pay tax on or before the due date shown on the demand notes issued to them. The vast majority of taxpayers settle their tax liabilities in a timely manner.

A late payment surcharge of 5% will generally be imposed where tax is in default. If tax debts remain outstanding for more than six months after the due date, the Department may impose a further surcharge of 10% on the total unpaid amount. In light of the economic condition in 2019-20 and the financial difficulties that some taxpayers might be facing, the Government announced on 4 December 2019 a relief measure on tax payment. For instalment plans approved by the Department for settlement of Salaries Tax, Profits Tax and Personal Assessment demand notes for the year of assessment 2018-19 issued between December 2019 and December 2020, no surcharge will be imposed for a maximum period of one year counting from the

22

Any tax in default is immediately recoverable. Recovery notices can be issued to employers, bankers, debtors and persons holding money on behalf of the defaulting taxpayers to effect collection. Actions may also be commenced in the District Court. Figure 26 summarises different types of recovery actions taken by the Department. Owing to the deferral of payment deadlines and recovery actions from late January 2020 when Government departments were under special work arrangements during the COVID-19 epidemic, there were significant decreases in the numbers of 5% surcharge notices and recovery notices issued in 2019-20 as compared to those of the previous year.

Figure 26 Recovery action

5% Surcharge Notice Number of notices

250

200

150

100

50

236,274 224,785

242,816

77,294

2016-17 2017-18 2018-19 2019-20

('000) Total amount

2016-17 2017-18 2018-19 2019-20 400

300

200

100

0

333

60

264 273

($m)

10% Surcharge Notice Number of notices

22,000

21,000

20,000

19,000

18,000

21,539 21,501 21,828

20,774

2016-17 2017-18 2018-19 2019-20

Total amount 240

180

120

60

0

137

239

126

146 ($m)

2016-17 2017-18 2018-19 2019-20

23

Figure 26 Recovery action (continued)

Recovery Notice

Number of notices 150

130

110

90

70

142,896 141,004

81,157 140,451

('000)

2016-17 2017-18 2018-19 2019-20

Total amount 15,000

11,250

7,500

3,750

0

12,817 12,426

10,595

11,934 ($m)

2016-17 2017-18 2018-19 2019-20

Upon entry of judgment, a defaulting taxpayer becomes liable to legal costs and interest on judgment debt for the period from the date of commencement of proceedings to the date of full settlement in addition to the outstanding tax. Figure 27 shows the legal costs and judgment interest collected during 2019-20.

Figure 27 Legal costs and judgment interest collected in 2019-20

$ $

Court cost

Court fees 614,027

Execution fees 2,039 616,066

Fixed cost 247,560

Judgment interest

Pre-judgment interest 1,617,953

Post-judgment interest 15,561,544 17,179,497

Total costs and interest collected 18,043,123

Furthermore, the Commissioner may apply to a District Judge to prevent a person with tax in default from leaving Hong Kong. If the District Judge is satisfied that it is in the public interest to ensure that the person does not depart from Hong Kong, or if he returns, does not depart again, without first paying the tax or furnishing security to the satisfaction of the Inland Revenue Department for payment of that tax, he shall issue the “departure prevention direction”. The person concerned has the right to appeal to the Court of First Instance of the High Court against the District Judge’s decision.

24

5 Field Audit and Investigation

The Field Audit and Investigation Unit is responsible for conducting field audits and investigations on businesses and individuals with a view to combating tax evasion and avoidance. Back tax is assessed and penalties are generally imposed where discrepancies are detected.

During 2019-20, the Field Audit and Investigation Unit completed 1,716 cases (including tax avoidance cases) and assessed back tax and penalties of about $2.5 billion (Figure 28). As a result of the Department’s special work arrangement during the COVID-19 epidemic, investigation work was affected, resulting in fewer number of cases completed as compared to past years.

Figure 28 Results of the Field Audit and Investigation Unit

2016-17 2017-18 2018-19 2019-20

Number of cases completed 1,801 1,804 1,802 1,716

Understated earnings and profits ($m) 12,408.8 11,687.7 13,910.0 12,893.4

Average understatement per case ($m) 6.9 6.5 7.7 7.5

Back tax and penalties assessed ($m) 2,528.4 2,526.2 2,826.6 2,548.5

Back tax and penalties collected ($m) 2,386.8 2,231.1 3,352.5 2,799.4

Field Audit

In 2019-20, there were 17 Field Audit sections. Field audit is conducted on both corporations and unincorporated businesses. The work of field auditors entails site visits to business premises and examination of accounting records of taxpayers in order to ascertain whether correct returns of profits have been made.

Anti-tax Avoidance

Two of the 17 Field Audit sections concentrate on tackling tax avoidance schemes, whereas other investigation officers and field auditors handle avoidance cases on an operational need basis. During 2019-20, the Field Audit and Investigation Unit completed 209 tax avoidance cases and assessed back tax and penalties of about

$1.25 billion (Figure 29).

Figure 29 Results of the audit on tax avoidance cases

2016-17 2017-18 2018-19 2019-20

Number of cases completed 214 208 207 209

Understated earnings and profits ($m) 6,201.8 4,613.4 7,891.4 6,979.5

Average understatement per case ($m) 29.0 22.2 38.1 33.4

Back tax and penalties assessed ($m) 1,120.2 948.5 1,426.6 1,246.6

25

Investigation

In 2019-20, there were 5 Investigation sections. Investigation officers are responsible for conducting in- depth investigations into suspected tax evasion, and taking penal action (including prosecution proceedings in appropriate cases) as a deterrent.

Prosecution

One of the 5 Investigation sections is the prosecution section focusing on criminal investigation of tax evasion.

Tax evasion is a serious crime. A person convicted of tax evasion could be sentenced to imprisonment for up to 3 years and fined.

During the year, the Department successfully prosecuted three tax evasion case which involved omission of rental income and making false statements in connection with claims for additional dependent parent allowance. Among these three cases, the defendant of one case was sentenced to 4 weeks’ immediate imprisonment and a fine of $134,398 (200% of the tax evaded). The defendant of another case was sentenced to 9 weeks’ immediate imprisonment and a fine of $288,794 (200% of the tax evaded). The defendant of the last case was sentenced to a community service order of 180 hours.

Property Tax Compliance Check

In addition to conducting audits on businesses, the Department also carries out verification checks on the correctness of rental income reported by property owners. In 2019-20, the Department completed compliance check on 266,998 property tax cases (Figure 30).

Figure 30 Results of the property tax compliance checks

2016-17 2017-18 2018-19 2019-20

Number of cases completed 209,499 234,726 261,181 266,998

Understated rental income ($m) 850.8 951.6 1,111.7 990.8

Back tax and penalties assessed ($m) 102.1 114.2 133.4 118.9

26

6 Taxpayer Services

IRD Website

www.ird.gov.hk

The IRD website is a very effective channel for disseminating tax information and providing electronic services to the public. With continuous enrichment and updates, the website enables taxpayers to obtain the most current information about Hong Kong taxation in a fast and convenient manner.

Through the website, members of the public can:

• obtain information on tax law, tax returns, tax obligations and answers to frequently asked questions;

• use IRD software and download IRD public forms;

• run the interactive program to calculate their liability under salaries tax and personal assessment; and

• access to the personalised on-line tax services provided by the Department under eTAX.

To facilitate all sectors of the community to locate the relevant tax information, there are thematic content pages for individuals, businesses, property owners, employers, tax representatives, etc.

The IRD website has adopted responsive web design, which enables users to have quick and convenient access to tax information.

Electronic Enquiry Service

Electronic enquiry services are provided to eTAX users at <www.gov.hk/etax>. They can view their tax position in relation to their returns, assessments and payments, etc. at any time.

Enquiry Service Centre

The Department’s Enquiry Service Centre handles telephone and counter enquiries. The Centre is equipped with a computer network linked to the Department’s Knowledge Database to enable our staff to provide, as far as possible, an immediate “one-stop” service.

27

Telephone Enquiry Service

The Centre operates an Interactive Telephone Enquiry System (ITES) with 144 telephone lines. Callers can have access on a 24-hour basis to a wide range of tax information by listening to recorded messages. Besides, callers can obtain facsimile copies of information sheets and forms through the system. A “Leave-and-call- back” facility, for recording information requests, and a “Fax-in enquiry” service are also available. The telephones are manned during office hours by staff who would readily serve the callers. The Centre also provides an eTAX help desk hotline to handle enquiries on eTAX services and provide technical support.

The statistics of services provided through ITES during 2019-20 are shown in Figure 31.

Figure 31 Statistics of services provided through ITES

2018-19 Number

2019-20 Number

Increase/

Decrease

Calls answered by staff 712,790 598,368 -16.1%

Calls answered by system 792,473 1,158,198 +46.1%

Leave-and-call-back messages 53,316 64,822 +21.6%

Documents supplied by fax 4,303 7,896 +83.5%

Counter Enquiry Service

Generally, the counter staff of the Centre is able to handle enquiries, collects mail items and issues forms on the spot without the need of referring callers to other sections in the Department for attention. The number of counter enquiries handled and forms issued during 2019-20 was about 0.69 million (Figure 32).

Figure 32 Counter enquiries

251,278 268,299

800

600

400

200

0

686,587 729,827

2018-19 2019-20

('000)

No. of callers No. of enquiries

Information leaflets on topics of general interest are available for collection at the form stand located on the first floor of Revenue Tower. The public may also obtain general tax information and download forms from the IRD website and GovHK <www.gov.hk>.

28

Tax-help Services for Completion of Tax Returns

On the IRD website, e-Seminars are provided for employers, property owners and individual taxpayers.

Information on how to complete tax returns, fulfil tax obligations and overcome difficulties in compliance is uploaded to the website. After reading the information, taxpayers can raise enquiries electronically at the

“Q&A Corner”. The Department will reply the questions on a regular basis.

The Department issued 2.68 million Individuals Tax Returns for the year of assessment 2018-19 on 2 May 2019. To assist the taxpaying public in completing tax returns, the Department extended the service hours of telephone enquiry services in May 2019. Service hours from Monday to Friday were extended by one and a half hours till 7:00 pm and additional service was also provided on Saturday from 9:00 am till 1:00 pm.

During peak periods, the Department also redeployed manpower resources and employed part-time staff to strengthen daytime telephone enquiry services.

Complaints and Compliments

If taxpayers are dissatisfied with the services provided by the Department or their problems cannot be solved satisfactorily through normal channels, the Complaints Officer may be approached for assistance. The complaint channel provides taxpayers with the means of having individual grievances dealt with independently at a senior level. This ensures that such cases are properly handled in a fair and impartial manner.

During 2019-20, 212 complaints cases were received (Figure 33).

Figure 33 Complaint cases

Not substantiated Partially substantiated Substantiated

212 256

300

250 200 150 100

50

0 2018-19 2019-20

134 149

69

85 9

22

If taxpayers are dissatisfied with any administrative action taken by the Department, they may refer the matter to the Ombudsman. During 2019-20, the Ombudsman sought written comments from the Department in respect of 21 cases. In the light of these cases, the Department has reviewed relevant operations with a view to improving them.

Taxpayers may compliment the service of the Department. During the year, 403 Letters of Compliments were received.

29

Performance Pledge

The service standards a taxpayer can expect from the Department are set out in the performance pledges.

The Department has achieved most of the targets of performance pledges and excelled in some of the targeted performance with remarkable results during 2019-20.

30

7 Information Technology

The Department has been making extensive use of information technology to enhance operational efficiency and provide quality services to the public.

IT Environment

The Department has built up a comprehensive and integrated IT infrastructure with different types of computer application systems and platforms. The Department’s network connects the computer system and workstations of staff on different floors. Assessment process is automated by the “Assess-First-Audit-Later”

system. Tax audit and investigation work is facilitated by the use of data mining and advanced analytical tools. The Document Management System and Workflow Management System enhance the control and monitoring of documents, files and workflow, facilitate the tracking of case progress, and thus enable the Department to improve overall service quality. A wide range of information is stored in the Department’s Intranet and General Enquiry Knowledge Database for convenient access by our staff at work. Moreover, e-mail and Internet facilities provide an efficient and environment-friendly communication platform for our staff.

Electronic Services

eTAX

The Department continues to provide a wide range of online tax services to the public, including internet filing of tax returns, e-stamping of property documents, business registration e-services, electronic notices, electronic payments and lodgement of applications, etc.

eTAX services are widely used by the public. As at 31 March 2020, there were some 981,000 registered eTAX users. The take-up rate increased year after year (Figure 34).

31

Figure 34 eTAX Usage Statistics

2018-19 Number

2019-20 Number

Increase/

Decrease Internet filing of tax returns

- Tax Return-Individuals, Property Tax Return and Profits Tax Return

661,587 725,375 +9.6%

- Employer’s Return of Remuneration and Pensions

BIR56A 15,335 23,219 +51.4%

IR56B 145,696 299,009 +105.2%

- Employer’s Notifications of Commencement of Employment, Cessation of Employment and Employee’s Departure from Hong Kong

24,727 32,505 +31.5%

Stamping of Property Document 307,792 294,932 -4.2%

Business Registration Number Enquiry 2,940,302 5,559,018 +89.1%

Application for Supply of Information on the Business Register

- Requisition 181,781 166,101 -8.6%

- Business registrations involved 503,938 487,255 -3.3%

Other Electronic Services

During 2019-20, some 36,200 employers furnished annual returns for 2,757,200 employees in total by diskettes, DVDs or USB storage devices. About 62% of these employers used the free software provided by the Department.

32

8 Human Resources

Organisation Chart of the Inland Revenue Department as at 31.3.2020

Commissioner

Deputy Commissioner

(Technical)

Commissioner's Unit Appeals

Technical Research Tax Treaty

Charitable Donations Complaints

Internal Audit

Special Duties

Forms &

General Support

Unit 1

Assessment and Review (Profits Tax - Corporations and

Partnerships)

Unit 2

Assessment (Salaries Tax, Profits Tax - Sole proprietorships, Property Tax - Sole Owners

and Personal Assessment)

Departmental Administration

Division

Deputy Commissioner

(Operations)

Unit 3

Collection

Inspection Estate Duty

Stamp Duty

Business Registration

Unit 4

Field Audit and Investigation

Headquarters Unit Information

Systems Training

Enquiry Services Document Processing

Output Despatch Tax Records

Assessment (Property Tax - Joint Owners and

Corporations) and Review (Profits Tax - Sole

proprietorships, Property Tax and Personal Assessment) Overall Establishment

No. of Staff

Commissioner's Office 83

Commissioner's Unit 120

Headquarters Unit 703

Unit 1 382

Unit 2 774

Unit 3 624

Unit 4 239

33

Establishment

The Commissioner, the two Deputy Commissioners and the five Assistant Commissioners, together with the Departmental Secretary, form the top management of the Inland Revenue Department.

Members of the Top Management of the Inland Revenue Department (as at 31.3.2020)

Mr WONG Kuen-fai, Commissioner

Mr TAM Tai-pang, Deputy Commissioner (Operations) Mr CHIU Kwok-kit, Deputy Commissioner (Technical)

Mr WONG Kai-cheong, Tony, Assistant Commissioner (Acting) (Headquarters Unit) Ms LEUNG Wing-chi, Assistant Commissioner (Unit 1)

Ms WONG Ki-fong, Jenny, Assistant Commissioner (Acting) (Unit 2) Ms TSE Yuk-yip, Assistant Commissioner (Unit 3)

Mr LEUNG Kin-wa, Assistant Commissioner (Unit 4) Miss MAN Wai-ming, Departmental Secretary (Acting)

As at 31 March 2020, the Department had an establishment of 2,925 permanent posts (including 28 directorate posts) in the Commissioner’s Office and the 6 Units of the Department. Of the total, 2,009 posts were in departmental grades (namely Assessor, Tax Inspector and Taxation Officer grades), performing duties directly concerned with taxation. The remaining 916 posts were in common / general grades, providing administrative, information technology and clerical support services (Figure 35).

Figure 35 Staff establishment

3,000

2,000

1,000

0

2,841 2,852 2,889 2,925

912 911 914 916

1,104 1,110 1,121 1,140

105 105 105 105

720 726 749 764

2018-19 2019-20 2016-17 2017-18

Assessors (Professional)

Tax Inspectors Taxation Officers

Common / general grade officers

34

Most of the professional officers serving in the Department were below the age of 45 (Figure 36). The ratio of male to female professional officers was 1:1.7.

Figure 36 Age and gender profiles of professional staff (on strength basis)

Age Group Male Female Total

Below 25 15 (5%) 29 (6%) 44 (6%)

25 to below 35 98 (35%) 166 (35%) 264 (35%)

35 to below 45 35 (12%) 100 (21%) 135 (18%)

45 to below 55 99 (35%) 137 (29%) 236 (31%)

55 and over 36 (13%) 40 (9%) 76 (10%)

Total 283 (100%) 472 (100%) 755 (100%)

Staff Promotions and Turnover

In 2019-20, a total of 73 departmental grade officers and 18 common / general grade officers were promoted. Among them, 5 were directorate rank. 233 officers joined the Department, of which 198 were new appointees and 35 were officers transferred from other grades / departments. A total of 203 officers (including 56 transferred to other departments) left the Department.

Training and Development

Staff are the Department’s valuable assets. We recognise the importance of providing opportunities of continuous learning to our staff to keep them abreast of the changing environment and to acquire the necessary knowledge to perform their duties. A variety of training courses in taxation, accounting, interpersonal skills, management, languages, computer, etc. are offered to staff members. In 2019-20, our staff received training for a total of 9,892 man-days, which was equivalent to about 3.38 man-days per officer.

The major training activities conducted for our staff during 2019-20 were as below:

Training Courses

• Induction courses for all grades of staff upon joining the Department

• Two-year taxation law and practice course for newly appointed Assistant Assessors

• Briefing sessions on legislative amendments and new services

• Refresher courses on professional knowledge

• Course on International Taxation

• Course on Mainland Taxation

• Updates on Hong Kong Accounting Standards

35

• Written and spoken English courses

• Computer software courses

Workshops

• Leadership and teamwork workshop

• Performance appraisal workshops on English writing and interviewing skills

• Updates on legal and regulatory requirements for foreign enterprises in the Mainland

• Workshop on bringing out the best in people

• Workshop on building resilience

• Workshop on customer service skills on the telephone

• Workshop on effective communication in the workplace

• Workshop on emotional wellness

• Workshop on how to handle taxpayers with special needs

• Workshop on interviewing and negotiation skills

• Workshop on leading innovation and change

• Workshop on problem solving and decision making

Continuing Professional Education

5 seminars were held by the Training Committee under the in-house Continuing Professional Education (CPE) Programme on the following subjects for professional officers:

• Anti-Money Laundering – Court Cases Sharing

• PRC Individual Income Tax Reform

• Know More About Bitcoin, Cryptocurrencies and Token Economy

• New Concessionary Deductions: Health Insurance Premiums; Annuity Premiums and MPF Voluntary Contributions

• Sharing of Customer Service Culture in Towngas

Speakers for 1 of the seminars were staff members and others were experts from various fields. A total of 753 staff members attended these seminars. The video files of the CPE seminars were uploaded onto the Department’s Intranet and a total of 504 staff members had viewed these video files.