國立台灣大學管理學院國際企業學系 博士論文

Department of International Business College of Management

National Taiwan University Ph.D. Dissertation

文化特徵、國家治理與資訊滲透對國外投資之研究 The Role of Culture Characteristics, Governance and Information Penetration in Foreign Portfolio Investment

袁正達 Cheng-Da Yuan

指導教授:陳思寬 博士 Advisor:Shikuan Chen, Ph.D.

中華民國 100 年 11 月

November, 2011

2

謝 辭

隨著博士論文的完成以及口試的進行,彷彿宣告離開校園的腳步近了,學生生活 也即將告一段落,步伐往另一個人生階段邁進。在台大攻讀博士的求學過程能夠 順利圓滿,首先必須由衷地感謝陳思寬老師、林修葳老師、張元晨老師、萬哲鈺 老師以及張銘仁老師對於口試以及論文內容提出許多寶貴的意見,讓論文發表以 及後續的研究方向更為豐富。尤其特別要感謝指導教授陳思寬老師,在台大國企 所博士班攻讀學位期間,提供正達許多的幫助與指導,老師在國際經濟與金融方 面的研究成果豐碩且學養深厚,不僅在論文題目上給予學生最大的彈性,且在論 文寫作與投稿過程也都獲得陳思寬老師的悉心指導,才能在博士的養成過程中獲 得最大的收穫與成長。

攻讀博士學位的契機與推手來自於就讀世新大學碩士期間多位老師的指 導。世新大學郭迺鋒老師、郭敏華老師以及楊浩彥老師的一路提攜與照顧,讓正 達可以在多元的學術領域中探索,接觸資料、學習不同的研究方法並獲得許多實 際應用的機會,是正達研究興趣的啟蒙階段。尤其是郭迺鋒老師從碩士班階段,

近十年時間不間斷地給予學習的機會,並引薦正達進入世新大學與景文科技大學 兼課,才得以累積寶貴的教學經驗。另外,郭敏華老師對於論文寫作邏輯的嚴格 訓練,奠定了我日後研究論文寫作的基礎,並不時提供在每一個求學階段的我可 以有反思的機會,讓我在自我成長方面有很大的助益。

此外,博士班的求學階段少不了一起奮鬥的同窗戰友,感謝國企所博士班的 每一位同學。包含一起修課鑽研市場微結構的瑞文大哥,常一起聊天寫作業的賽 局高手一誠,總是在學校大操場運動不期而遇的碧娟,在北京大學研討會難得遇 到的陽照與瑞容,公司理財模型推得天昏地暗的同組夥伴信夫以及傳授投資組合 理的玄啟,承蒙多位同窗好友的指教,每每在討論賽局、隨機微積分、公司理財 等科目的過程中,累積了抽象的理論基礎與研究的能量,同時學校生活也因有了 大家的參與,留下許多難忘的回憶。另外,研究過程中每當遇到瓶頸或需要靈感 時,政勳學長總能適時地給予珍貴建議,教學與研究過程中也常常受到秀秀學 姐,鼎宇與曉園學長等多位學長姐的鼓勵與照顧,在此也一併深深致謝。

攻讀博士學位期間,並非一帆風順。何其幸運在人生最低潮的時刻,有小翰 哥與小微姐一家人的支持與鼓勵,讓來自嘉義鄉下的我能夠適應台北的生活,重 新找回生活的重心與節奏;在許多無所適從,茫然無頭緒的時刻,多虧小翰哥無 數個伴隨著便當與咖啡的對話,意外地成為求學過程中一段特別值得回味的午茶 時光。感謝一路上陪伴在正達身邊許多人的付出與關愛,因為有了您們,才能在 人生與求學這一條路上不是踽踽獨行,而是途經滿地的盛放。

最後,謹獻給親愛的家人與從小辛苦撫養我長大的爺爺袁炳煌先生、奶奶黃 夜好女士,有您們的教養,正達今日才有機會完成博士學位;也勉勵自己記得這 段最特別的求學時光,在未來的日子裡,樂觀積極並且要能笑得燦爛。

摘 要

本博士論文主要由二篇有關文化特徵與國家治理如何影響海外投資組合的文章 所組成,其中我們也探討了資訊網路在跨國投資行為裡的角色。第一篇文章探討 不同的文化特徵如何影響跨國投資行為?並透過引力模型的建置以了解國家文化 的特性以及文化距離等因素是否會影響海外投資組合的持有。模型的實證結果發 現,不同構面的文化因子不僅對於投資組合有顯著的影響,並且兩國之間的文化 距離愈遠,過度投資在母國的現象就愈形嚴重。另外,資訊距離的落差更會進一 步擴大文化距離,使得資訊不對稱與交易成本的提高,間接導致跨國之間的投資 更形困難。因此,無法達到最佳化的資產配置與分散風險的效果。

第二篇文章主要探討國家治理的概念與資訊滲透的程度對跨國投資的影 響。實證結果發現,擁有較佳治理機制的國家能夠吸引較多的國外投資,能夠降 低過度投資在母國的現象。另外,更發現國家治理穩定且擁有高度通訊網絡的國 家,可更進一步吸引外國投資並使得本國投資者更易於持有海外資產,以分散投 資組合的風險。該結果說明資訊滲透的程度可以加強國家治理的力量,並使得投 資組合更國際化,能降低過度投資在本國的偏誤。因此,國家應該致力於建立更 透明、有效率的國家治理機制,並建設普及化的網路通訊設施來有效地分散資產 投資組合的風險。

關鍵詞: 母國偏誤,文化特徵,引力模型,國家治理,資訊滲透

4

Abstract

The Ph. D. dissertation is a collection of two essays on equity home bias, national culture characteristics and information technology. Chapter 1 addresses the role of national culture played in the cross-border investment. We first investigate the effects of various culture dimensions on foreign portfolio investment constructing gravity model. Our evidence indicates that various culture characteristics exert different impact on foreign portfolio holdings. We also incorporate cultural distance and it’s interaction with information distance to home bias. The empirical result suggests that culture distance have significant positive effect on equity home bias. Moreover, the information gap between originating country and destination country can increase the culture distance that discourages foreign diversification.

In Chapter 2, we examine the addressed issue of governance regime and information penetration on cross-border investment. The estimated result shows that better regulatory has a negative but insignificant effect on reducing home bias.

Nevertheless, we further find that a country with greater governance appears to decrease cross-border investment bias under higher information penetration. This implies that information penetration can moderate the strength of the relationship between governance quality and home bias. The implication is that for a country tries to diversify internationally should devote themselves into developing better governance environment and information infrastructure.

Keywords: home bias, culture characteristics, gravity model, regulatory governance, information penetration

Table of Contents

Chapter 1

Gravity Analysis on Culture and Information Distance in Home Bias

1.1 Introduction ... 10

1.2 The Linkage between International Diversification and Culture Characteristics ... 12

1.3 Data and Methodology ... 16

1.3.1 Home Bias Measure... 16

1.3.2 Model Specification ... 19

1.4 Panel Estimation Results ... 21

1.5 Robustness Checks ... 28

1.6 Concluding Remarks ... 30

Appendix 1.1 ... 31

Chapter 2 Governance Quality, Information Penetration, and Home Bias 2.1 Introduction ... 34

2.2 Literature Review ... 39

2.3 Data and Methodology ... 41

2.3.1 Measuring the Equity Home Bias ... 41

2.3.2 Variable Definitions ... 44

2.3.3 Model Specification ... 46

2.4. Empirical Results ... 48

2.5 Robustness Checks ... 50

2.6 Concluding Remarks ... 52

References ... 56

6

List of Figures

Figure 1.1 Home bias for year 2009 ... 16

Figure 2.1 Evolution of home bias and governance quality ... 36

Figure 2.2 Evolution of home bias and internet penetration ... 38

List of Tables

Table 1.1 Summary statistics ... 21

Table 1.2 Panel data estimation: the effects of culture characteristics ... 23

Table 1.3 Panel data estimation: the effects of culture distance ... 25

Table 1.4 Panel data estimation: the interaction effect... 27

Table 1.5 Hauseman‐Taylor estimation ... 29

Table A1.1 Pooled OLS estimation: the effects of culture characteristics ... 31

Table A1.2 Pooled OLS estimation: the effects of culture distance ... 32

Table A1.3 Pooled OLS estimation: the interaction effect ... 33

Table 2.1 Equity Home Bias 2009 ... 43

Table 2.2 Variables’ Definitions and Descriptive Statistics ... 46

Table 2.3 Panel Estimation with a Fixed Effect for Equity Home Bias ... 50

8

Introduction

The home bias phenomenon is firstly observed by French and Poterba (1991) in equity market. However, the author argue that the national wealth not always move together, investors can diversify their assets in foreign countries. Despite the international diversification can decrease the non-system risk and benefits portfolio holdings, investors merely invest their wealth in their own countries. Moreover, the home bias emerges in various fields such as consumption, debt and equity investment, mutual fund and bank loans. Previous literature provides plenteous theories to explain why investors allocate less proportion of their wealth in foreign market, despite the fact that diversification benefits are recognized for decades. For example, the home bias can be attributed to transaction costs and barriers to international investments (see Errunza and Losq, 1985; Warnock, 2002).

Lewis (1999) and Sercu and Vanpée (2007) summarize that the equity home bias can be explained by hedging for domestic risks, such as inflation risk, real exchange rate risk, domestic consumption risk, and the risk of non-tradable wealth components like human capital (see Baxter and Jermann, 1997; Obstfeld and Rogoff, 1996;

Wheatley, 2001). Cooper and Kaplanis (1994) argue that the departure of purchasing power parity could be another reason to explain home bias, while Brennan et al (2005) suggest that information asymmetry could be a potential explanation for home bias.

The latest study addresses the role of cultural characteristics on foreign investment since country-specified culture can deeply affects investment behavior. We argue culture traits can be factors that influence foreign portfolio investment. Therefore, our first paper related our foreign investment issue to country-specified cultural dimensions.

In particular, this dissertation focuses on the roles of country-specified culture characteristics, governance environment on international diversification. The thesis addresses two parts of survey-based data conducted by Hofsted’s (2001) and Kauffman et al (1999). According to Hofsted’s (2001), the rooted culture is transmitted generation by generation and is a pattern of thinking, feeling and reaction.

In fact, national culture is a traditional value, beliefs that distinguished from another group. Hofstede (2001) identifies the culture traits into the following primary dimensions, power distance, uncertainty avoidance, individualism, masculinity, and long-term orientation. These variables reveal the differences in thinking, values, and social behaviors among people from more than 50 countries. Thus, we argue that national cultural characteristics can exert significant effect on home bias.

The major variables regard to the governance concept of interest are Worldwide

Governance Indicators (WGI) conducted by Kauffman et al (1999). In particular, these variables are obtained from 25 important sources and covering various aspects of governance quality. These indicators include voice and accountability, political stability and absence of violence, government effectiveness, regulatory quality, rule of law, and control of corruption. These indicators are compiled every year and cover more than 245 countries, including most of the developed and emerging markets. This allows us to relate culture and governance dimensions to cross-border investment.

Therefore, we use these two survey-based data to revisit the home bias issue.

In Chapter 1, we find that culture characteristics exert different influences on international diversification while traditional gravity model focuses on country characteristics variables such as GDP, population, and geographic distance. In particular, countries characterized by higher uncertainty avoidance tend to exhibit less diversification in their foreign holdings and display greater home bias. Moreover, portfolios from countries with higher levels of higher power distance and geographic distance display higher home bias. The significant interaction effect of culture distance and information distance implies that information distance increases culture distance and discourages foreign investment. Therefore, culture impacts investor behavior directly and not merely though indirect channels such as legal and regulatory framework. Our findings also suggest that culture distance has significant impacts on international investment behavior after control geographic distance. This result is consistent with the conclusion of Anderson et al. (2011).

In Chapter 2, we argue the legal regime in a country can affect international portfolio holdings. However, previous studies use corporate governance such as investors’ protection to explain home bias, how governance quality in macroeconomic level affects home bias is not investigated. Hence, we adopt Kauffman (1999) governance matter survey data to construct panel data consisting more than 40 countries to explore this issue. Our result shows that better governance has a negative but insignificant effect on reducing home bias. Nevertheless, we further find that a country with greater governance appears to decrease cross-border investment bias under higher information penetration. That is the development of information communication technology can moderate the effect of governance mechanism.

This dissertation is organized as following. In Chapter 1, we use gravity model to analyze the relation between culture characteristics and foreign portfolio allocation. In Chapter 2, we discuss how governance quality and information penetration impact international diversification. Finally, we conclude this thesis and shed the light for further research.

10

Chapter 1

Gravity Analysis on Culture and Information Distance in Home Bias

This study uses the IMF’s Coordinated Portfolio Investment Survey data across 45 countries during 2001-2009 to examine the relationship between national culture characteristics and equity home bias. We find different culture characteristics exert significant influences on international diversification. Despite the fact that geographic distance and language consistently have a significant effect on home bias, distance in the degree of a different culture has a positive effect on home bias, implying that cultural difference discourages foreign investment. Furthermore, we show that information distance increases culture distance, thus leading to more home bias.

1.1 Introduction

The asset allocation theory suggests that a country should diversify its investments internationally, but investment in foreign markets is far from a market portfolio as predicted. This phenomenon is referred to the famous puzzle, “home bias”. The traditional explanation proposes that home bias is affected by trading barriers, transaction cost, information asymmetry and familiarity, foreign exchange rate risk, corporate governance, corruption, and the regulatory system. We argue that national culture characteristics, such as the attitude towards taking risk, a system of values and beliefs, and perception toward the future, affect the preference for international investment. Furthermore, these culture characteristics vary across countries.

Culture is a framework that stands for the foundational institutions of society. It also can be seen as a system of values and beliefs underlying more specific formal institutions and informal ones (North, 1990; Williamson, 2000). Tabellini (2008) describes the national culture as a system of values and core beliefs that provide guidance for behavior and perceptions of the world. We conjecture that the rooted culture and beliefs in a country do affect its preference for foreign portfolio holdings.

Therefore, we address the interesting issue of whether culturally-rooted behavior impacts cross-border investment.

Previous literature has provided abundant explanations for home bias. Tesar and

Werner (1995) suggest that differences in language and legal environment and the cost for obtaining information from the foreign market make investors prefer to invest domestically. Grinblatt and Keloharju (2001) confirm that investors tend to invest in stocks of firms located close to them. Moreover, the Chief Executive Officer’s (CEO) native tongue and culture background exert significant effects on investors’ portfolio holdings. Coval and Moskowitz (1999) use airfares and phone rate to explain home bias. Huberman (2001) finds evidence that investors tend to invest in the company they are familiar with and ignore that their assets should be diversified. In particular, culture is a composite concept locally rooted in the home country, including values, judgment, beliefs, and attitudes.

We propose that culture characteristics such as decisiveness, assertiveness, competitiveness, subject perspective, and attitude toward risk affect foreign investment. Aggarwal, Kearney and Lucey (2011) identify the culture distance on cross-border investment both in debt and equity. The estimated coefficients of distance in masculinity and the degree of individualism are positively significant in both the debt and equity equations, implying that a country with a more aggressive attitude has more foreign investment in equity. They also confirm that culture distance increases the geographic distance, which has a reverse effect on foreign investment.

Anderson et al (2011) address the function of culture in determining the asset allocation in a foreign market by exploring mutual fund data. Huang (2008) and Chui et al. (2010) utilize the culture distance to explain investors’ trading behavior and industrial growth. Thus, the geographic distance, the place where a company’s headquarters is located, and whether two countries share a common language and religion are important determinants that influence international diversification. The culture difference thus can affect the preference for cross-border investment.

To examine the effect of culture characteristics on equity home bias, we apply the quantitative data from the International Monetary Fund’s (IMF) Coordinated Portfolio Investment Survey (CPIS) data across 45 countries during 2001-2009. Our hypothesis is that a country with a greater culture distance implies more divergence in preferences for foreign investment, attitude towards risk, beliefs, and perception.

Nevertheless, the home country will underweight its investments in a foreign country and exhibit more home bias towards the target market, because the culture gap between the home country and the host country is large.

Another part of this study examines how information distance interacts with culture distance. This article uses the number of Internet users per 100 people between the originating and destination countries to proxy for information distance. Since the speed of information transmission is accelerated, information infrastructure development improves the accuracy and efficiency of acquiring and processing

12

information for investors. From this point of view, we argue that two countries with greater information distance incur more information asymmetry and transaction costs that discourage investors to invest in the foreign market. Thus, information distance significantly increases the cultural difference in determining cross-border investment.

Though culture distance significantly influences foreign investment, we conjecture that information distance raises gap and makes investors allocate their assets domestically. Mondria and Wu (2010) apply variables such as the number of people with Internet access, the number of mobile telephone subscribers, and the average circulation of newspapers to proxy information capacity and conclude that home bias increases with information capacity.

This study constructs a gravity model to examine the effect of culture distance on international portfolio allocation and offers the following empirical insights. First, we find each culture dimension has a different effect on home bias. For example, a country with high uncertainty avoidance tends to allocate less proportion of its portfolio in foreign markets and exhibits higher home bias. On the contrary, culture characteristics such as masculinity and long-term orientation are reversely associated to home bias while a country with more individualism displays less home bias.

Second, we confirm that a greater culture distance discourages foreign investment and affects international asset allocation, leading to more home bias. Third, we further investigate how information distance interacts with culture distance. Our empirical evidence shows that a country with higher information distance can significantly increase the culture distance, which results in more home bias in equity investment.

This article is organized as follows. Section 2 reviews the linkage between national culture characteristics and international investment bias. Section 3 describes the data and model specifications. Section 4 presents empirical results and the implication for cross-border investment. Section 5 uses an alternative estimation to check the robustness. Section 6 concludes this study and provides implications for further research.

1.2 The Linkage between International Diversification and Culture Characteristics

Though previous literature proposes various explanations for home bias, the culture dimensional impacts on the decision-making process related to international investment, financial intermediation, and corporate finance have become more and more important. Stulz and Williamson (2003)show that a country’s principal religion predicts the cross-sectional variation in creditor rights better than other variables such as language and trade openness. Chang and Noorbakhsh (2009) suggest that national

culture influences corporate managers’ cash holding behavior, even controlling for governance and financial development. The empirical finding is that corporations hold larger cash and liquid balances in countries where people tend to avoid uncertainty.

Rossi and Volpin (2004) and di Giovanni (2005) use language similarity and geography as proxies to examine the effect of cultural distance on merger and acquisition activity, while Chan, Covrig, and Ng (2005) take variables for common language, geographical proximity, common colonial ties, and bilateral trade to address the role of informational asymmetry in the home bias. Anderson et al. (2011) examine the role of national culture from the view of institutional investors, concluding that culture characteristics indeed influence home bias and foreign diversification. Lin (2009) confirms that culture affects foreign investment where investors perform superior in a foreign market that has a formal regime and culture similar to their own country. The culture distance therefore creates information asymmetry, and thus culture difference and governance mechanism affect cross-border investment.

Aggarwal and Goodell (2010) suggest that a country characterized by society openness, economic inequality, and lower uncertainty avoidance prefers to finance through the equity market while a society engraved by regulatory and ambiguity aversion would rather have more bank-based financing.

Zheng et al. (2011) propose that national culture explains cross-country variations in the maturity structure of corporate debt. They conclude that firms prefer to use short-term debt when a country is characterized with high scores in uncertainty avoidance, power distance, and masculinity. While many studies apply culture variables from Hofstede (2001), Siegel, Licht and Schwartz (2011) use egalitarianism distance to capture the degree of institutional compatibility. They find the larger egalitarianism distance between the home country and host country decreases cross-border bonds, equity investment, syndicated loans, and mergers and acquisitions.

Slangen (2006) finds strong empirical evidence for greater differences in national culture reducing foreign acquisition performance by analyzing 102 cross-border acquisitions by Dutch firms in 30 countries. However, Diyarbakirlioglu (2011) finds culture distance provides a limited explanation for international portfolio holdings.

Cho and Padmanabhan (2005) present that cultural distance is positively associated with full ownership of Japanese foreign manufacturing entities. Aggarwal and Goodell (2009) examine the role of national culture in determining the preferences of financial intermediation (markets versus institutions), showing a country characterized by higher uncertainty avoidance is more bank-based instead of market-based. Beugelsdijk and Frijns (2010) apply a society’s culture and the cultural

14

distance between two markets to explain the foreign bias. In particular, the authors find that an uncertainty-avoiding country allocates less to foreign markets while a country with a higher degree of individualism tends to invest more in foreign markets.

However, though various culture dimensions are related to economic issues, national culture characteristics’ influence on cross-border investment is rarely examined.

This study uses cross-border equity investment data from 45 countries to examine whether culture distance affects foreign portfolio investment by constructing a gravity model. Hofstede’s survey including power distance, uncertainty avoidance, individualism, masculinity, and long-term orientation allows us to relate these culture characteristics to the international investment issue. However, various culture dimensions capture different effects on equity investment, and these concepts can be translated into investment behavior. Following Anderson et al. (2011), we categorize national culture components into corresponding investment behavior and form testable hypotheses as follows.

The concept of power distance is associated with the content of hierarchy. A high power distance society tends to limit the opportunity for education and controls the media and information. In contrast, a country with a lower power distance can freely disseminate information and encourages personal development and access to education. Therefore, we expect a power distant society will allocate less assets to foreign markets, resulting in a higher degree of the home bias measure.

Hypothesis 1. Countries characterized by a high power distance tend to allocate

assets domestically and exhibit more home bias.We conjecture that a country with a higher ranking of uncertainty avoidance prefers to invest its wealth domestically and in a country they are familiar with. We predict that a country with the propensity to avoid uncertainty toward the future will allocate its wealth in the home country instead of oversea markets. Therefore, this leads to higher home bias.

Hypothesis 2. Countries characterized by high uncertainty avoidance tend to

underweight their investment in foreign markets and exhibit more home bias in their investment behavior.A higher score in individualism implies that a country behaves more aggressive and undertakes more risk taking in foreign investment. A country with this property is confident about itself that it can process information efficiently and correctly. Such a country interprets information from foreign markets better to improve its decision

making process. We argue that a country with a high score in this culture dimension of individualism prefers to hold foreign assets and has less home bias.

Hypothesis 3. Countries characterized by high individualism diversify their wealth

in foreign markets and therefore have a lower home bias than countries with low individualism scores.According to the suggestion in the field of behavior finance, gender can affect investment behavior. Barber and Odean (2001) confirm that male investors suffer more investment loss than female investors due to over-trading, which is attributed to psychological bias such as over-confidence and self-attribution. Thus, we expect a more masculine society is more willing to hold or trade securities in foreign markets.

Therefore, we predict that masculinity exerts a negative effect for home bias.

Hypothesis 4. Countries characterized by high masculinity scores have more equity

ownership abroad and therefore a lower home bias than countries with low scores.The characteristic for the dimension of long-term orientation often implies that investors are more patient and forward looking and believe that long-term investment lowers systematic risk, which is consistent with the diversification theory. A country with higher scores on this dimension is more likely to diversify its portfolio internationally. Thus, this type of country exhibits less home bias in equity investment than countries with lower scores.

Hypothesis 5. Countries characterized by high long-term orientation have more

ownership abroad and therefore have a lower home bias than countries with low scores in this dimension.Hypothesis 6. A greater distance in the level of culture dimension discourages

foreign portfolio holdings from the originating country to the destination country and leads to more home bias.We further argue that the information gap between two countries increases the culture distance and hurts international diversification. We use the difference of Internet users per 100 people from two countries as a proxy of information distance.

We predict that the information gap between the home country and host country increases culture distance and raises home bias.

16

Hypothesis 7. Countries with a higher information distance can strengthen the

culture distance between the source and destination countries, and thus the originating country exhibits more home bias toward the destination country.1.3 Data and Methodology 1.3.1 Home Bias Measure

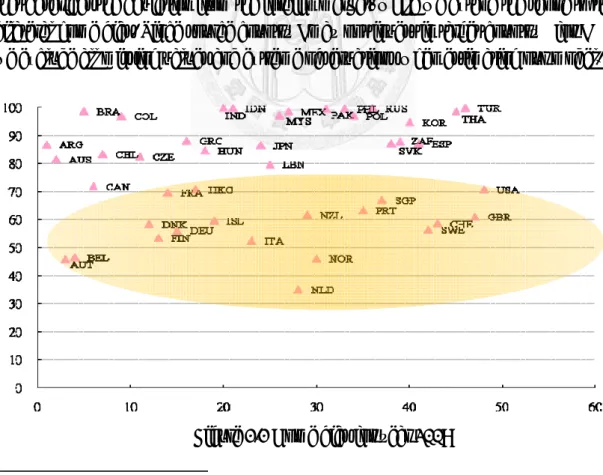

The Coordinated Portfolio Investment Survey (CPIS) conducted by the IMF provides bilateral equity investment data for more than 70 countries. The CPIS breaks down offshore investment into 255 foreign countries for an individual country during the period 2001 to 2009.1 More than 70 countries report their international equity portfolio investments in foreign countries, but CPIS data do not identify domestic securities holdings. Therefore, the aggregate portfolio investment in a selected country, as reported by the remaining countries, serves as an estimate of that country’s liabilities. This allows us to calculate the domestic portfolio holdings by subtracting the foreign liabilities from the local market capitalization. Moreover, we calculate the equity investment across major countries, which is intensively used in home bias related research. Following Chan et al. (2005), we calculate the country home bias that describes the deviation from the foreign market, while we extend the scope to the bilateral home bias. Since source country i may not invest in target country j for i ≠ j, we exclude all missing values and extreme observations when estimating our model.

Figure 1.1 Home bias for year 2009

1

Participation in the Coordinated Portfolio Investment Survey (CPIS) is voluntary and 75 economies

currently participate in the survey. The foreign holding data for each country provided by CPIS are

available annually for the period 2001-2009 and some data are also available for 1997

.In this study the subscript i and j denote the home country and the host country, respectively. The share of i’s equity investment in country j (wij) is the ratio of domestic country i’s holdings of country j equities to country i’s total equity portfolio.

The total equity portfolio for country i is calculated as country i’s market capitalization less equities held by foreign investors plus foreign equities held by domestic investors.

'

ij

'

country i s holdings of country j equities

w country i s total equity portfolio

(1.1)*

'

j

country j s market capitalization

w world market capitalization

(1.2)Here, the optimal portfolio allocation

w is the ratio of target country j’s equity

*j capitalization relative to the world market and is used as the benchmark of optimal portfolio holdings.Following Chan et al. (2005) and Fidora et al. (2007), Equation (1.3) defines the home bias measure of country i toward country j. The under/overweighting of the target countries is calculated as the actual allocation by each target country deviating from the market portfolio as suggested by the Capital Asset Pricing Model (CAPM).

This measures how far the actual portfolio allocation deviates from the market portfolio

w as suggested by CAPM.

*j*

* 1 *

j ij ij

ij

j j

w w w

Home Bias

w w

(1.3)

This paper addresses the issue of how cross-cultural differences affect foreign portfolio holdings. According to the well-known survey conducted by Hofstede (2001), the culture attributes can be identified into the following primary dimensions, including the differences in thinking, values, and social behaviors among people from more than 50 countries. This allows us to relate culture dimensions to international asset allocation. These culture dimensions are power distance index (pdi), uncertainty avoidance index (uai), individualism (idv), masculinity (mas), and long-term orientation (lto).

According to Hofstede’s framework, the cultural dimension of power distance is associated with the content of hierarchy. In a high power distant society, we expect the power imbalance to cause unequal resource distribution, a limited

18

decision-making process, and a lack of social mobility. These will allow a powerful authority to pursue private interest and privilege, which will lead to a corrupt and bureaucratic government that lowers the level of trust and increases opportunistic behaviors. The extent to uncertainty avoidance is related to a society’s tolerance for uncertainty and ambiguity, indicating that people will feel either nervous or anxious in unpredicted situations. A country with a higher degree of uncertainty avoidance will expect its investment to be protected by strict laws and rules, in particular for investors preferring to allocate their assets in a safe and secure market.

Individualism is the degree to which individuals are integrated into groups. A country with a greater degree of individualism focuses on individual motivation, self-interest, and ambitions and one is expected to look after his immediate family. By contrast, a collectivism society refers to the extent that people are strongly connected and prefer group decision-making. Masculinity refers to a society that emphasizes assertiveness, competitiveness, and success instead of femininity, such as nurturance, support, and attentiveness. The last culture dimension of Hofsted (2001) is the long-term orientation, which refers to values associated with thrift and perseverance.

Despite the above-mentioned primary dimensions of national culture, we also utilize a composite measure of cultural distance through Kogut and Singh (1988) as follows:

, ,

1

( ) /

N n I n J

I

n n

C C

CD N

V

, (1.4)where CDI is the cultural distance of domestic country I from target country J. Here,

C

n,I is the index for the nth cultural dimension of country I, Vnis the variance of the nth index, and C

n,J is the index for the nth cultural dimension of country J. A higher culture distance indicates a greater difference between the source and target countries.The data analyzed in this study are collected from various sources. The specific country characteristics such as GDP, total population, the ratio of private sector finance to GDP, telephone lines, the number of mobile phone subscribers, and Internet users per 100 people are from World Development Indicators (WDI), while country governance is from governance matters conducted by Kaufmann (1999). Our addressed cultural dimension measures, including power distance, uncertainty avoidance, individualism, masculinity, and long-term orientation versus short-term orientation, are from Hofsted’s website (www.geert-hofsted.com/). The gravity variables such as geographic distance between two countries and dummy variables indicating whether the two countries share a common language are drawn from CEPII (http://www.cepii.fr/anglaisgraph/news/accueilengl.htm).

1.3.2 Model Specification

We first examine whether national culture characteristics and culture distance between the home and host countries influence foreign investment. We are also interested in the interaction effect of culture distance and information gap on cross-border investment. We argue that information distance significantly increases the culture distance and discourages foreign investment, thus increasing the home bias measure for the originating country. The gravity model is specified as follows:

0 1 2 3 4 5

6 7 8

9 10 11

ln( ) ln( ) ln( ) ln( ) ln( )

ln( ) ln( )

ln( ) ln( ) ln( ) ,

ijt it it jt jt ij

ij it jt

cul cul int

it ij ijt ij

home bias gdp pop gdp pop dist

comlang credit credit

culture dist dist dist

(1.5) Here:

home bias

ijt is the home bias measure of source country i to target market j at time t. ln(gdp)

it andln(gdp)

jtare the GDP levels for source country i and target country j

in year t. ln(pop)

it and ln(pop)jtare the populations for source country i and target country j

in year t. ln(dist)

ij is the geographic distance between the capital cities of countries i and j. comlan is a dummy variable for whether two countries share a common

language. ln(credit)

it and ln(credit) jt are the ratios of private sector debt to GDP for country i and country j in year t. ln(culture)

it are the scores of Hofsted’s culture characteristics. ln(dist

cul)

ijt denotes the cultural distance for Hofsted’s culture characteristics between the source and target countries. ln(dist

cul dist

int)

ijt denotes the cross product term of culture distance and information distance between the source and target countries.

εijt is the normal error term with mean zero and variance σ2.

The dependent variable home biasijt denotes the home bias measure in cross-border equity investment, subscriber i denotes the cross-section country, and the symbol t represents each time period. The term α0 is a constant term, while the estimated coefficients of β1 to β4 capture the economic scale and specific country characteristics that are basic variables in the gravity model. The estimated coefficients for β5 and β6 measure the marginal effect of the gravity variables, geographic distance and whether two countries share common language, on international portfolio

20

holdings. The coefficients for β7 and β8 capture the impact of financial development on bilateral home bias. The estimated coefficients for β9 measure the marginal effects for different national culture characteristics in home bias, while coefficient β10

captures the effects of various distances in the level of culture dimensions on home bias.

Shenkar (2001) suggests that national culture can be modified by corporate culture and addresses the interaction effect between culture distance and other interesting variables. Cho and Padmanabhan (2005)investigate the moderating effects of a firm’s experience levels in the relationship between cultural distance and foreign ownership mode choice. Slangen (2006) hypothesizes that national culture reduces foreign acquisition performance, depending on the level of post-acquisition integration. This study also interacts the cultural distance with information distance to examine whether the information gap increases this culture distance and result in an increasing home bias. Therefore, we expect the coefficient for β11 to be positive for the interaction term. Table 1.1 presents the summary statistics of the related variables used in this paper.

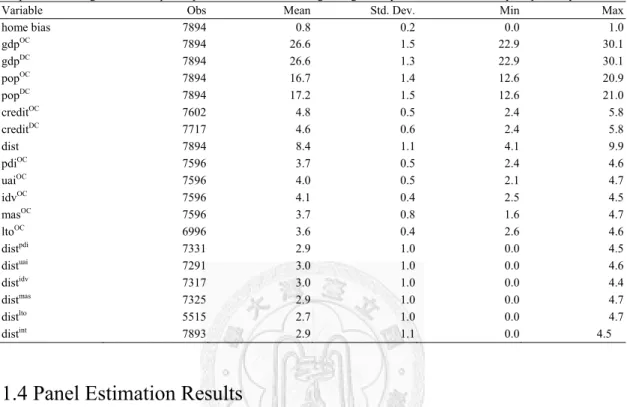

Table 1.1 Summary statistics

Table 1 presents descriptive statistics for the variables used in this study. We constrain our sample by censoring the values of home bias exceeding 0.99 and less than 0, since observations exceeding 0.99 or having a negative value can be seen as extreme values or foreign bias. The control variables include gross domestic product (GDP), total population (pop) for originating and destination countries, geographic distance (dist); a dummy variable indicates whether two countries share a common language (comlan); and the credit to the private sector as a share of GDP is used to proxy financial development (fin) for the originating and destination countries. The culture identifiers are Hofstede’s power distance (pdi), uncertainty avoidance (uai), individualism (idv), masculinity (mas), and long-term orientation (lto). The culture distance dimensions include power distance (distpdi), uncertainty avoidance (distuai), individualism (distidv), masculinity (distmas), and long-term orientation (distlto). All these variables are presented in log form. The superscripts OC and DC denote originating country and destination country, respectively.

Variable Obs Mean Std. Dev. Min Max

home bias 7894 0.8 0.2 0.0 1.0

gdpOC 7894 26.6 1.5 22.9 30.1

gdpDC 7894 26.6 1.3 22.9 30.1

popOC 7894 16.7 1.4 12.6 20.9

popDC 7894 17.2 1.5 12.6 21.0

creditOC 7602 4.8 0.5 2.4 5.8

creditDC 7717 4.6 0.6 2.4 5.8

dist 7894 8.4 1.1 4.1 9.9

pdiOC 7596 3.7 0.5 2.4 4.6

uaiOC 7596 4.0 0.5 2.1 4.7

idvOC 7596 4.1 0.4 2.5 4.5

masOC 7596 3.7 0.8 1.6 4.7

ltoOC 6996 3.6 0.4 2.6 4.6

distpdi 7331 2.9 1.0 0.0 4.5

distuai 7291 3.0 1.0 0.0 4.6

distidv 7317 3.0 1.0 0.0 4.4

distmas 7325 2.9 1.0 0.0 4.7

distlto 5515 2.7 1.0 0.0 4.7

distint 7893 2.9 1.1 0.0 4.5

1.4 Panel Estimation Results

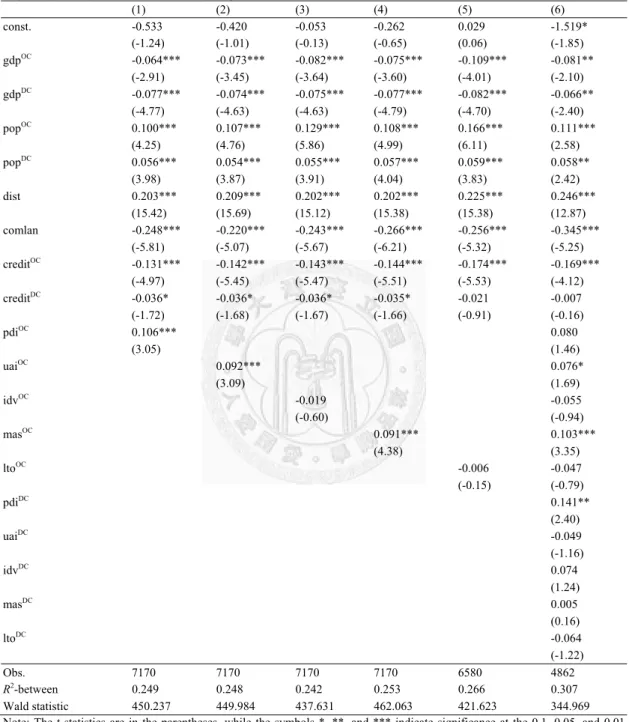

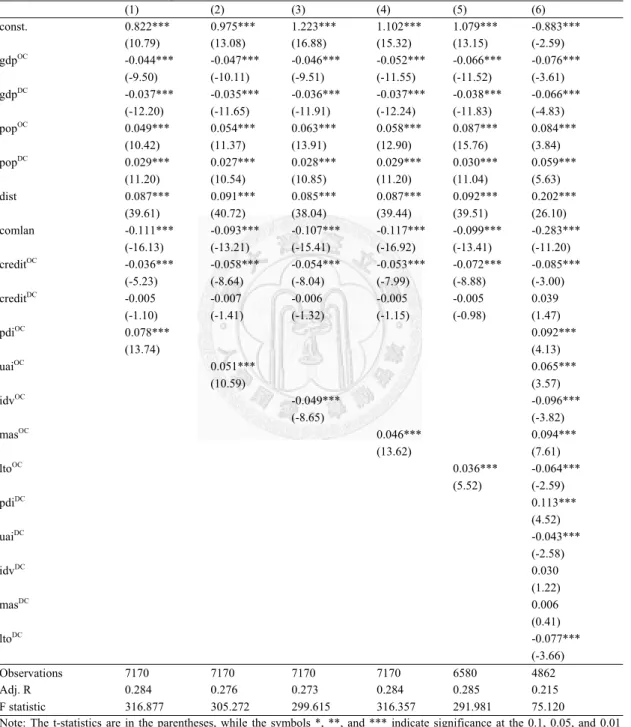

In order to provide insights for the relationship between rooted-cultural difference and equity home bias, we construct a gravity model from CPIS cross-border equity investment data that consist of 45 countries during 2001 to 2009. The following empirical results are estimated by the panel data approach, while the pooled OLS regression is conducted in Appendix.

Our analyses begin by identifying the national culture impacts on home bias by entering the specific culture characteristics into our model separately. Table 1.2 presents panel data estimation for the effects of different cultural dimensions, including power distance, uncertainty avoidance, masculinity, individualism, long-term orientation, and overall cultural distance measure, on international equity holdings. The positive sign of uncertainty avoidance suggests that a home country with a higher score in this cultural dimension exhibits more home bias. In general, a country with higher uncertainty avoidance has a greater risk adverse attitude and is more conservative in investing its wealth in foreign markets. The negative coefficient of individualism (ind) reflects that a country with a higher score in this dimension is confident in the ability to understand and interpret information quickly from the target market. Thus, investors are more willing to allocate their wealth in foreign markets

22

and exhibits less home bias. This result is consistent to Anderson et al. (2011).

A country characterized by high masculinity is associated with the extent of aggressiveness, taking adventure, and highly confident. Barber and Odean (2001) find that male investors suffer from a lower return than female investors since they typically have higher trading volume. The cultural dimension of masculinity can thus be categorized into overconfidence. Hence, we predict a country prefers to have ownership abroad than those countries with lower scores and therefore behaves with less home bias. The negative estimated coefficient for masculinity indicates that a country prefers to hold foreign assets, because the self-attribution bias makes people believe they can process and interpret more information than other countries.

Consequently, our Hypothesis 4 is confirmed.

According to the survey, long-term orientation is related to the value of thrift and perseverance. We predict that a country with a long-term investment view acts patiently and is more willing to diversify its assets internationally, leading to less home bias. However, the estimated coefficient of long-term orientation (lto) is negative, but insignificant. The estimated signs are as expected except for the coefficient of masculinity (mas).

We now turn to the estimated coefficients for the important gravity variables. The expected signs for the gravity variables are consistent with both theoretical predictions and existing findings in the literature. We find that geographic distance consistently enters the model with a positive sign, which implies that geographic distance increases information asymmetry and transaction cost to the target market, thus discouraging foreign investment. On the contrary, the estimated sign for common language is negative as predicted. This confirms that investors prefer to invest in a country with the same language, which makes it easier to extract and interpret information from financial statements. Thus, common language significantly reduces home bias. The negative and significant coefficient for financial development reflects that the originating country with better financial openness exhibits less home bias.

Table 1.2 Panel data estimation: the effects of culture characteristics

Table 2 shows results from panel estimation with random effect. We analyze the relationship between culture identifier and home bias in equity investment after controlling gravity variables. The dependent variable is the home bias measure. We censor the values of home bias exceeding 0.99 and less than 0, since observations exceeding 0.99 or having a negative value can be seen as extreme values or foreign bias. The control variables include gross domestic product (GDP), total population (pop) for originating and destination countries, geographic distance (dist); the dummy variable indicates whether two countries share a common language (comlan); and the credit to the private sector as a share of GDP is used to proxy financial development (fin) for originating and destination country. The culture identifiers added in our model are power distance (pdi), uncertainty avoidance (uai), individualism (idv), masculinity (mas), and long-term orientation (lto). The superscripts OC and DC denote originating country and destination country, respectively.

(1) (2) (3) (4) (5) (6)

const. -0.533 -0.420 -0.053 -0.262 0.029 -1.519*

(-1.24) (-1.01) (-0.13) (-0.65) (0.06) (-1.85) gdpOC -0.064*** -0.073*** -0.082*** -0.075*** -0.109*** -0.081**

(-2.91) (-3.45) (-3.64) (-3.60) (-4.01) (-2.10) gdpDC -0.077*** -0.074*** -0.075*** -0.077*** -0.082*** -0.066**

(-4.77) (-4.63) (-4.63) (-4.79) (-4.70) (-2.40) popOC 0.100*** 0.107*** 0.129*** 0.108*** 0.166*** 0.111***

(4.25) (4.76) (5.86) (4.99) (6.11) (2.58) popDC 0.056*** 0.054*** 0.055*** 0.057*** 0.059*** 0.058**

(3.98) (3.87) (3.91) (4.04) (3.83) (2.42) dist 0.203*** 0.209*** 0.202*** 0.202*** 0.225*** 0.246***

(15.42) (15.69) (15.12) (15.38) (15.38) (12.87) comlan -0.248*** -0.220*** -0.243*** -0.266*** -0.256*** -0.345***

(-5.81) (-5.07) (-5.67) (-6.21) (-5.32) (-5.25) creditOC -0.131*** -0.142*** -0.143*** -0.144*** -0.174*** -0.169***

(-4.97) (-5.45) (-5.47) (-5.51) (-5.53) (-4.12) creditDC -0.036* -0.036* -0.036* -0.035* -0.021 -0.007 (-1.72) (-1.68) (-1.67) (-1.66) (-0.91) (-0.16)

pdiOC 0.106*** 0.080

(3.05) (1.46)

uaiOC 0.092*** 0.076*

(3.09) (1.69)

idvOC -0.019 -0.055

(-0.60) (-0.94)

masOC 0.091*** 0.103***

(4.38) (3.35)

ltoOC -0.006 -0.047

(-0.15) (-0.79)

pdiDC 0.141**

(2.40)

uaiDC -0.049

(-1.16)

idvDC 0.074

(1.24)

masDC 0.005

(0.16)

ltoDC -0.064

(-1.22) Obs. 7170 7170 7170 7170 6580 4862 R2-between 0.249 0.248 0.242 0.253 0.266 0.307 Wald statistic 450.237 449.984 437.631 462.063 421.623 344.969

Note: The t-statistics are in the parentheses, while the symbols *, **, and *** indicate significance at the 0.1, 0.05, and 0.01 levels, respectively. The Wald statistic checks the overall significance of the model against the null that all coefficients are simultaneously zero.

24

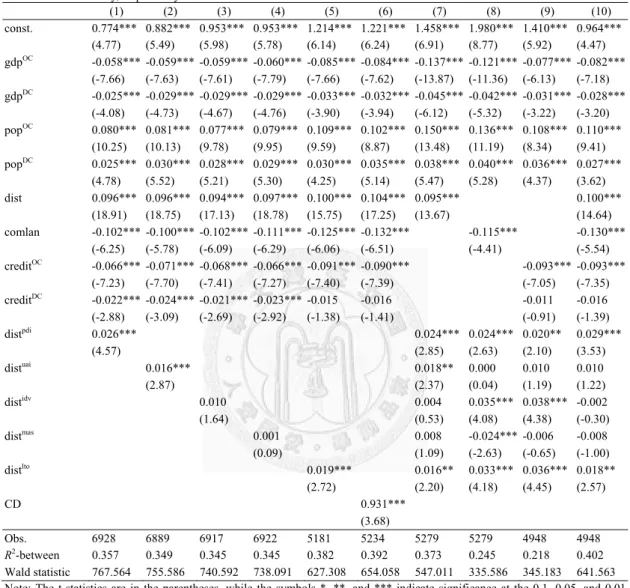

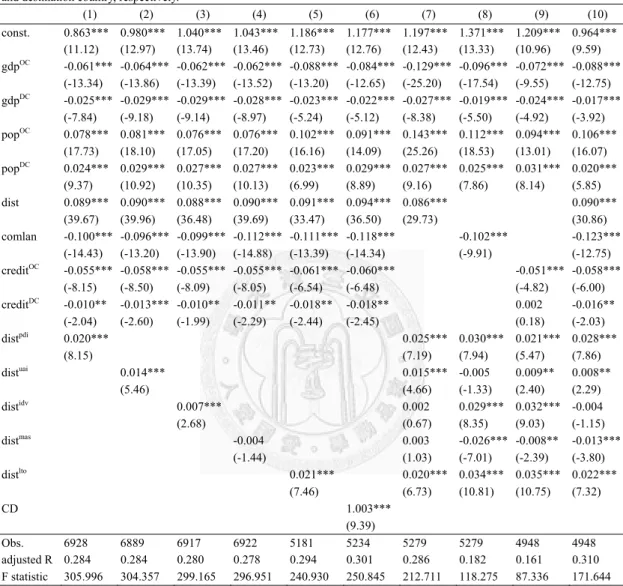

Table 1.3 shows the effects of various culture distances on home bias. The coefficients for culture distance, such as distpdi , distuai , distlto, and composite culture distance (CD), are strongly significant at 0.01. The estimated signs for distidv and distmas are positive, however they are insignificant. This result confirms our hypothesis that not only does geographic distance increase transaction cost which prevents portfolio diversification, but also culture distance discourages foreign investment. For models (7) to (9), we further examine the effect of culture distance on an international portfolio after controlling geographic distance, language, and the level of financial development. By adding geographic distance in the model specification, all the coefficients for culture distance remain positive. Our empirical results suggest that investors prefer to invest in a country with a closer culture background and beliefs. The estimation result is similar to the previous result. The coefficients for geographic distance show a persistent positive sign across models.

The expected negative sign of the coefficient for common language implies that the two countries tend to invest in target markets when they share the same language. A common language is helpful in decreasing home bias since it is critical for acquiring and processing information. This result is in line with Grinblatt and Keloharju (2001) in that investors tend to invest in a firm where the CEO speaks the same language.

Table 1.3 Panel data estimation: the effects of culture distance

Table 3 shows results from panel estimation with random effect. We analyze the relationship between culture distance and home bias in equity investment after controlling the gravity variables. The dependent variable is the home bias measure. We censor the values of home bias exceeding 0.99 and less than 0, since observations exceeding 0.99 or having a negative value can be seen as extreme values or foreign bias. The control variables include gross domestic product (GDP), total population (pop) for originating and destination countries, geographic distance (dist); the dummy variable indicates whether two countries share a common language (comlan); and the credit to the private sector as a share of GDP is used to proxy financial development (fin) for originating and destination countries. The culture distance identifiers added in our model are power distance (distpdi), uncertainty avoidance (distuai), individualism (distidv), masculinity (distmas), and long-term orientation (distlto), while (CD) denotes the aggregate measure of culture distance for various culture dimensions. The superscripts OC and DC denote originating country and destination country, respectively.

(1) (2) (3) (4) (5) (6) (7) (8) (9) (10) const. 0.774*** 0.882*** 0.953*** 0.953*** 1.214*** 1.221*** 1.458*** 1.980*** 1.410*** 0.964***

(4.77) (5.49) (5.98) (5.78) (6.14) (6.24) (6.91) (8.77) (5.92) (4.47) gdpOC -0.058*** -0.059*** -0.059*** -0.060*** -0.085*** -0.084*** -0.137*** -0.121*** -0.077*** -0.082***

(-7.66) (-7.63) (-7.61) (-7.79) (-7.66) (-7.62) (-13.87) (-11.36) (-6.13) (-7.18) gdpDC -0.025*** -0.029*** -0.029*** -0.029*** -0.033*** -0.032*** -0.045*** -0.042*** -0.031*** -0.028***

(-4.08) (-4.73) (-4.67) (-4.76) (-3.90) (-3.94) (-6.12) (-5.32) (-3.22) (-3.20) popOC 0.080*** 0.081*** 0.077*** 0.079*** 0.109*** 0.102*** 0.150*** 0.136*** 0.108*** 0.110***

(10.25) (10.13) (9.78) (9.95) (9.59) (8.87) (13.48) (11.19) (8.34) (9.41) popDC 0.025*** 0.030*** 0.028*** 0.029*** 0.030*** 0.035*** 0.038*** 0.040*** 0.036*** 0.027***

(4.78) (5.52) (5.21) (5.30) (4.25) (5.14) (5.47) (5.28) (4.37) (3.62) dist 0.096*** 0.096*** 0.094*** 0.097*** 0.100*** 0.104*** 0.095*** 0.100***

(18.91) (18.75) (17.13) (18.78) (15.75) (17.25) (13.67) (14.64) comlan -0.102*** -0.100*** -0.102*** -0.111*** -0.125*** -0.132*** -0.115*** -0.130***

(-6.25) (-5.78) (-6.09) (-6.29) (-6.06) (-6.51) (-4.41) (-5.54) creditOC -0.066*** -0.071*** -0.068*** -0.066*** -0.091*** -0.090*** -0.093*** -0.093***

(-7.23) (-7.70) (-7.41) (-7.27) (-7.40) (-7.39) (-7.05) (-7.35) creditDC -0.022*** -0.024*** -0.021*** -0.023*** -0.015 -0.016 -0.011 -0.016

(-2.88) (-3.09) (-2.69) (-2.92) (-1.38) (-1.41) (-0.91) (-1.39) distpdi 0.026*** 0.024*** 0.024*** 0.020** 0.029***

(4.57) (2.85) (2.63) (2.10) (3.53) distuai 0.016*** 0.018** 0.000 0.010 0.010 (2.87) (2.37) (0.04) (1.19) (1.22) distidv 0.010 0.004 0.035*** 0.038*** -0.002 (1.64) (0.53) (4.08) (4.38) (-0.30) distmas 0.001 0.008 -0.024*** -0.006 -0.008 (0.09) (1.09) (-2.63) (-0.65) (-1.00) distlto 0.019*** 0.016** 0.033*** 0.036*** 0.018**

(2.72) (2.20) (4.18) (4.45) (2.57)

CD 0.931***

(3.68)

Obs. 6928 6889 6917 6922 5181 5234 5279 5279 4948 4948 R2-between 0.357 0.349 0.345 0.345 0.382 0.392 0.373 0.245 0.218 0.402 Wald statistic 767.564 755.586 740.592 738.091 627.308 654.058 547.011 335.586 345.183 641.563 Note: The t-statistics are in the parentheses, while the symbols *, **, and *** indicate significance at the 0.1, 0.05, and 0.01 levels, respectively. The Wald statistic checks the overall significance of the model against the null that all coefficients are simultaneously zero.

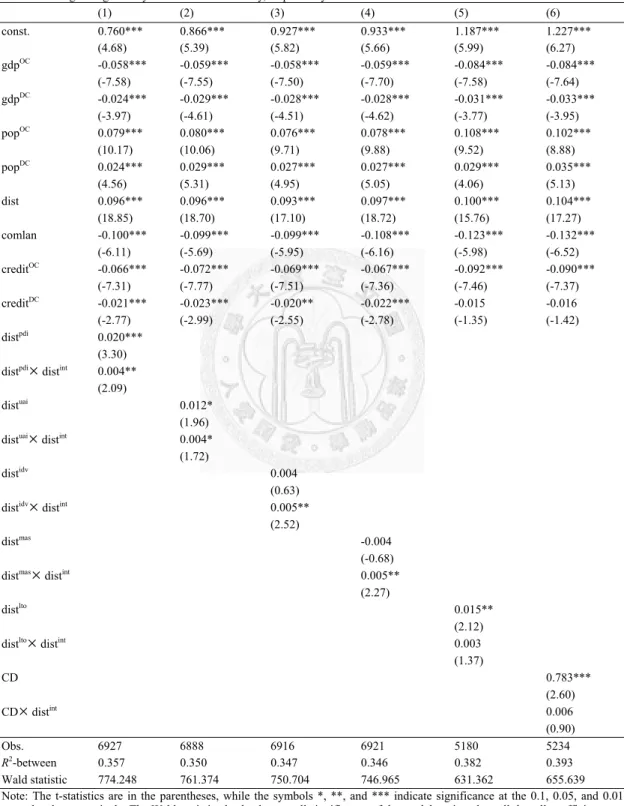

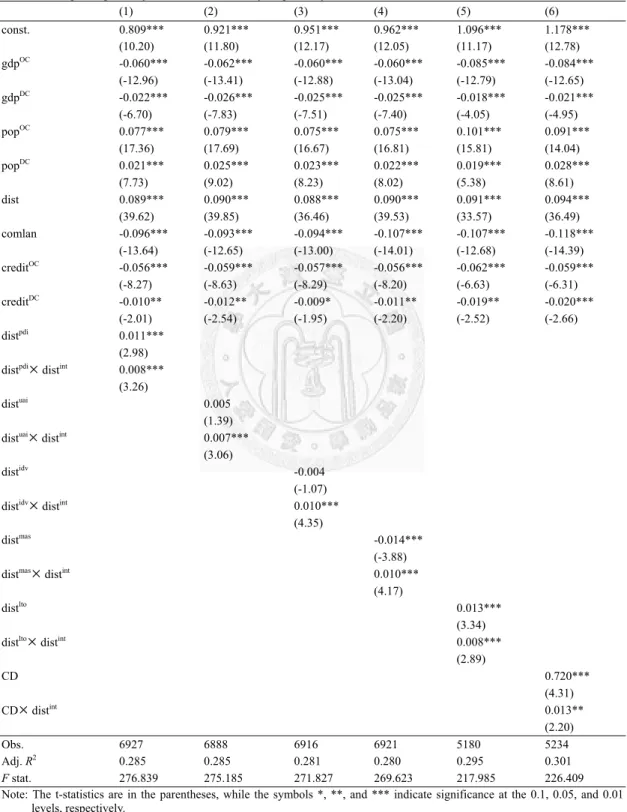

Although culture distance can influence international portfolio holdings, we further hypothesize that the information gap increases this culture distance and discourages foreign investment. Table 1.4 re-estimates the gravity model by considering the interaction effect between culture distance and information distance.

The estimated result for the gravity variables, such as geographic distance and whether two countries share a common language are similar to the previous result.

The adjusted R2 across the models is about 0.28. Overall, the multiplicative distance term is positive and strongly significant in models (1)-(4). This supports our

26

hypothesis that the information gap increases the culture distance, leading to more home bias. The coefficients for distpdi and distpdi

distint are 0.02 and 0.004, respectively. The positive and significant coefficient of the multiplicative term distpdi

distint implies the information distance significantly raises the level of home bias by strengthening the effect of culture distance. Similar results are be found in models (2) to (6). The interaction terms for distpdi

distint, distuai

distint, distmas

distint, and distidv

distint are significant at 0.05 and 0.1 statistically. The statistically significant interaction effect indicates that the effect of national cultural distance on cross-border investment varies with the information distance.In summary, our primary results show that cultural distance influences equity home bias. Moreover, the multiplicative term enters our model specification with a positive sign as predicted. This result confirms our hypothesis that information distance significantly increases culture distance and discourages foreign portfolio holdings.

Table 1.4 Panel data estimation: the interaction effect

Table 4 shows results from panel estimation with random effect. We analyze the effect of the multiplicative term culture distance and information distance on home bias in equity investment after controlling gravity variables. The dependent variable is the home bias measure. We censor the values of home bias exceeding 0.99 and less than 0, since observations exceeding 0.99 or having a negative value can be seen as extreme values or foreign bias. The control variables include gross domestic product (GDP), total population (pop) for originating and destination countries, geographic distance (dist); the dummy variable indicates whether two countries share a common language (comlan); the credit to the private sector as a share of GDP is used to proxy financial development (fin) for originating and destination countries. The culture distance identifiers added in our model are power distance (distpdi), uncertainty avoidance (distuai), individualism (distidv), masculinity (distmas), and long-term orientation (distlto), while (CD) denotes the aggregate measure of culture distance for various culture dimensions. The superscripts OC and DC denote originating country and destination country, respectively.

(1) (2) (3) (4) (5) (6)

const. 0.760*** 0.866*** 0.927*** 0.933*** 1.187*** 1.227***

(4.68) (5.39) (5.82) (5.66) (5.99) (6.27) gdpOC -0.058*** -0.059*** -0.058*** -0.059*** -0.084*** -0.084***

(-7.58) (-7.55) (-7.50) (-7.70) (-7.58) (-7.64) gdpDC -0.024*** -0.029*** -0.028*** -0.028*** -0.031*** -0.033***

(-3.97) (-4.61) (-4.51) (-4.62) (-3.77) (-3.95) popOC 0.079*** 0.080*** 0.076*** 0.078*** 0.108*** 0.102***

(10.17) (10.06) (9.71) (9.88) (9.52) (8.88) popDC 0.024*** 0.029*** 0.027*** 0.027*** 0.029*** 0.035***

(4.56) (5.31) (4.95) (5.05) (4.06) (5.13) dist 0.096*** 0.096*** 0.093*** 0.097*** 0.100*** 0.104***

(18.85) (18.70) (17.10) (18.72) (15.76) (17.27) comlan -0.100*** -0.099*** -0.099*** -0.108*** -0.123*** -0.132***

(-6.11) (-5.69) (-5.95) (-6.16) (-5.98) (-6.52) creditOC -0.066*** -0.072*** -0.069*** -0.067*** -0.092*** -0.090***

(-7.31) (-7.77) (-7.51) (-7.36) (-7.46) (-7.37) creditDC -0.021*** -0.023*** -0.020** -0.022*** -0.015 -0.016 (-2.77) (-2.99) (-2.55) (-2.78) (-1.35) (-1.42) distpdi 0.020***

(3.30)

distpdi

distint 0.004**(2.09)

distuai 0.012*

(1.96)

distuai

distint 0.004*(1.72)

distidv 0.004

(0.63)

distidv

distint 0.005**(2.52)

distmas -0.004

(-0.68)

distmas

distint 0.005**(2.27)

distlto 0.015**

(2.12)

distlto

distint 0.003(1.37)

CD 0.783***

(2.60)

CD

distint 0.006(0.90) Obs. 6927 6888 6916 6921 5180 5234 R2-between 0.357 0.350 0.347 0.346 0.382 0.393 Wald statistic 774.248 761.374 750.704 746.965 631.362 655.639 Note: The t-statistics are in the parentheses, while the symbols *, **, and *** indicate significance at the 0.1, 0.05, and 0.01

levels, respectively. The Wald statistic checks the overall significance of the model against the null that all coefficients are simultaneously zero.

28

1.5 Robustness Checks

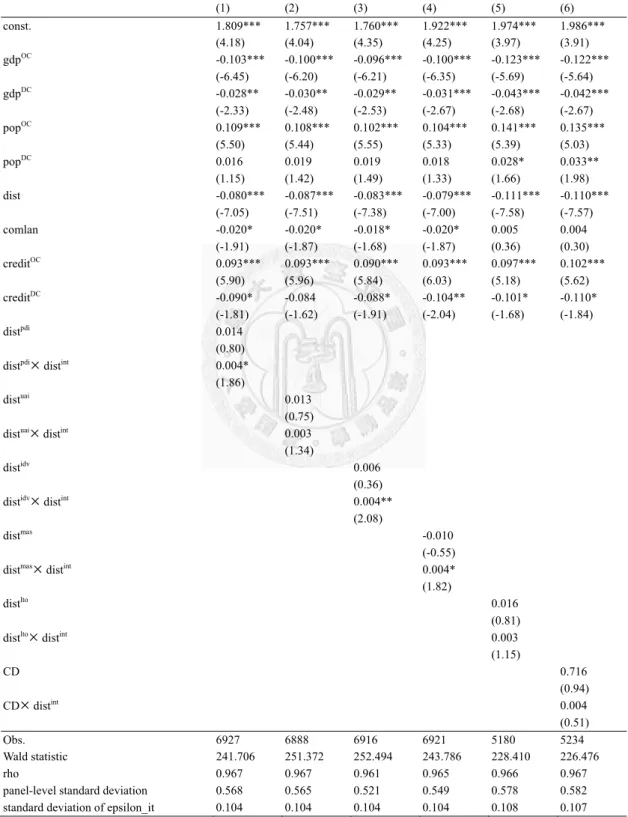

Despite results estimated by the panel data approach and pooled OLS regression, we re-estimate the empirical models applying the Hausman-Taylor model (HTM).

However, panel data approach allows us to capture the individual effects and time effects and controls for the possibility that the unobserved effects may be correlated with the regressors. The problems occur in the fixed effect estimation when time invariant variables, such as geographic distance and common language, are included in the model specification. This study applies the Hausman-Taylor model as suggested by Egger (2005) to examine cultural characteristics on cross-border investment bias. This approach not only allows us to estimate time invariant variables such as distance and cultural dimensions, but also solves the potential problems of correlation between unobservedindividual effects and explanatory variables. The time invariant variables in our model include geographic distance, common language, and different dimensions of culture distance. These variables serve as instrumental variables, which provide additional information from the dataset to eliminate the correlation between the explanatory variables and the unobservedindividual effects.

Table 1.5 presents the estimation results for the relationship between culture distance and cross-border equity investment home bias. The estimated coefficients for the basic gravity variables are similar to previous results. Obviously, common language enters the model with a negative and statistical significance, implying that investors rely on common language to interpret information correctly and share common values between two countries. Therefore, the originating country tends to hold foreign securities from a destination country that shares the same language.

We next turn to the role of geographic distance. Not surprisingly, the sign of distance is positive as predicted and is consistent with previous studies. The culture distance remains positive except for distmas, however it is not significant. The interaction effects of culture distance and information distance are positive for distpdi

distint, distmas

distint, and distidv

distint and significant at the 0.1 and 0.05 statistical levels, respectively. These results support Hypothesis 7 that information distance increases culture distance between the home and source countries and exhibits more home bias.Table 1.5 Hauseman-Taylor estimation

Table 5 shows results by re-estimating our model using the Hauseman-Taylor model. We analyze the effect of the multiplicative term culture distance and information distance on home bias in equity investment after controlling gravity variables. The dependent variable is the home bias measure. We censor the values of home bias exceeding 0.99 and less than 0, since observations exceeding 0.99 or having a negative value can be seen as extreme values or foreign bias. The control variables include gross domestic product (GDP), total population (pop) for originating and destination countries, geographic distance (dist);

the dummy variable indicates whether two countries share a common language (comlan); the credit to the private sector as a share of GDP is used to proxy financial development (fin) for originating and destination countries. The culture distance identifiers added in our model are power distance (distpdi), uncertainty avoidance (distuai), individualism (distidv), masculinity (distmas), and long-term orientation (distlto), while (CD) denotes the aggregate measure of culture distance for various culture dimensions. The superscripts OC and DC denote originating country and destination country, respectively.

(1) (2) (3) (4) (5) (6) const. 1.809*** 1.757*** 1.760*** 1.922*** 1.974*** 1.986***

(4.18) (4.04) (4.35) (4.25) (3.97) (3.91) gdpOC -0.103*** -0.100*** -0.096*** -0.100*** -0.123*** -0.122***

(-6.45) (-6.20) (-6.21) (-6.35) (-5.69) (-5.64) gdpDC -0.028** -0.030** -0.029** -0.031*** -0.043*** -0.042***

(-2.33) (-2.48) (-2.53) (-2.67) (-2.68) (-2.67) popOC 0.109*** 0.108*** 0.102*** 0.104*** 0.141*** 0.135***

(5.50) (5.44) (5.55) (5.33) (5.39) (5.03) popDC 0.016 0.019 0.019 0.018 0.028* 0.033**

(1.15) (1.42) (1.49) (1.33) (1.66) (1.98) dist -0.080*** -0.087*** -0.083*** -0.079*** -0.111*** -0.110***

(-7.05) (-7.51) (-7.38) (-7.00) (-7.58) (-7.57) comlan -0.020* -0.020* -0.018* -0.020* 0.005 0.004

(-1.91) (-1.87) (-1.68) (-1.87) (0.36) (0.30) creditOC 0.093*** 0.093*** 0.090*** 0.093*** 0.097*** 0.102***

(5.90) (5.96) (5.84) (6.03) (5.18) (5.62) creditDC -0.090* -0.084 -0.088* -0.104** -0.101* -0.110*

(-1.81) (-1.62) (-1.91) (-2.04) (-1.68) (-1.84)

distpdi 0.014

(0.80)

distpdi

distint 0.004*(1.86)

distuai 0.013

(0.75)

distuai

distint 0.003(1.34)

distidv 0.006

(0.36)

distidv

distint 0.004**(2.08)

distmas -0.010

(-0.55)

distmas

distint 0.004*(1.82)

distlto 0.016

(0.81)

distlto

distint 0.003(1.15)

CD 0.716

(0.94)

CD

distint 0.004(0.51)

Obs. 6927 6888 6916 6921 5180 5234

Wald statistic 241.706 251.372 252.494 243.786 228.410 226.476 rho 0.967 0.967 0.961 0.965 0.966 0.967 panel-level standard deviation 0.568 0.565 0.521 0.549 0.578 0.582 standard deviation of epsilon_it 0.104 0.104 0.104 0.104 0.108 0.107 Note: The t-statistics are in the parentheses, while the symbols *, **, and *** indicate significance at the 0.1, 0.05, and 0.01 levels, respectively. The Wald statistic checks the overall significance of the model against the null that all coefficients are simultaneously zero.

30

1.6 Concluding Remarks

This study extends previous research in terms of culture characteristics to the international diversification issue. To investigate the effect of culture scores and culture distance on equity home bias, we utilize bilateral equity investment data across 45 countries from CPIS to construct the gravity model. Our empirical findings provide the following insights. First, we find that different national culture characteristics exert different influences on international diversification. A society with a higher power distance tends to allocate assets domestically, resulting in an increasing home bias for the originating country. Moreover, a country with the attitude to avoid uncertainty tends to exhibit more home bias in equity investment. This result is consistent with the conclusion of Anderson et al. (2011). Second, despite the fact that geographic distance consistently has a significant effect on home bias, distance in the degree of a different culture discourages foreign investment and provides additional explanation in determining international portfolio allocation. The positive and significant interaction effect of culture distance and information distance supports our hypothesis that information distance increases culture distance and discourages foreign investment. This implies that a country can set up its portfolio holdings more efficiently by reducing both culture distance and information distance.