人力資本與經營績效

Chiao Da Management Rev;ew Vol. 29 No. 1, 2009

pp.83-130

Human Capital and Operating Performance

林日召伶 1 Chao-Ling Lin長榮大學 會計資訊學系

Department of Accounting and Infonnation System, Chang Jung Christian University

陳燕錫 Y油n-Shir Chen

雲林科技大學 會計系

Dep紅伽lentof Accountin皂, National Yunlin University ofScience and Technology 摘要:由於全球對會計專業規範的日益嚴苛,以及執業環境的惡化,會計師 事務所如何在市場上占有一席之地,是一門值得深思的課題,尤其是事務所 特別依賴著以知識為基礎的人力資本來執行其審計服務,然而,有關於事務 所之經營績效為何,以及人力資本的優劣究竟在事務所之經營績效上扮演何 種角色,卻少見研究探討之 。 因此,本文首先採用資料包絡法 , 分析事務所 效率與規模報酬等經營績效,其次,利用資源基礎觀點,進而探討高品質人 力資本是否會影響事務所之經營績效 。 本文按生產技術水準將樣本分為大型 及小型等兩類事務所,結呆顯示,就效率而言,大型事務所樣本下之四大表 現較俊,且主因千島吉主管理者有較佳的資源運用能力 。 小型事務所則以員工 9 人(含)以上事務所表現較佳,惟與四大情況不同,其原因並非源、自於管理者 能力,而你有較佳的生產規模所致 。 就規模報酬而言,大型事務所中的四大, 多數均處於最適的生產規模中,從年度趨勢來看,非四大事務所有積極調整 規模的現象 。 小型事務所中,員工 9 人以下事務所大多處於規模報酬遞增, 而員工 9 人(含)以上事務所則多數於規模報酬遞減之生產狀態下 。 就高品質

1 Coπesponding au曲。r Departmenl of Accounting and Infonnalion Sys脂m, Chang Jung Chrislian Universi旬,Tainan City, Taiwan. E-mail: chao_lingI4@1抽tmai l. com

甘le au出ors wish 10 acknowledge 由e helpful commenls on 血is paper by the anonymous reVlewers

84 Human Capital and Operaling Pe功rmance 人力資本能否影響事務所績效而言,結呆顯示,無論是大型或小型事務所, 若所內有愈多經驗豐厚之高階專業人力,愈能提昇技術效率,且主主事務所教 育訓練支出愈多者,其技術效率亦愈能有所增加,惟無論是大型或小型事務 所,所內有愈多高學歷的高階專業人力,均無法顯著增加其技術效率 。 關鍵詞:人力資本;會計師事務所 ; 績效

Abstract: Recently, increasingly severe regulation and s甘 ingent market competition deteriorate the operating environment in which auditors practise According旬, it is undoubtedly an impo此ant lesson for auditors to adapt to the practicing situation to survive and to sustain ∞mpetitive advantages in the audit market. As a professional org個ization, audit firm offers various services by knowledge-based human capital. However, few prior studies address the operating performance of audit firm and the role played by human capital in creating the operating performance. To fill the gap, this study estimates the efficiency and retum to scale by Data Envelop Analysis. Th間, this study investigates the effects ofhigh quality human capital upon operating performance in terms of resource-based view. Total observations used in this study are grouped into large and small firms by production technical level. Empirical results indicate that Big 4 intemationaI firms and small firms with number of employee equal to and more than 9 possess higher efficiency. For retum to scale, most of the Big 4 intemational fi口ns are in the optimal scaIe of production. Non-Big 4 firms adapt their scale aggressively in the long-run tendency. Of the small firrr尬, firms with number of employee less than 9 訂e in the increasing retum to scale and firms with number of employee equal to and more than 9 are in the decreasing retum to scale. Finally, audit firms with more 巴xperienced upper-Ievel professionals lmprove 出eir technical efficiency significantly. In addition, audit firms with more expenditure on educational training significantly increase technical efficiency. However, for either large or small firm, more upper-Ievel professionals with high academic degree are unable to improve their technical efficiency

Chiao Da A4ánagemenl Review 均1. 29 No. /. 2009 85

1. Introduction

The environment in which auditors operate has changed drastically during the past few years of this new century. 1 n the demand side of audit service, many audit clients either closed their businesses or moved to Mainland China, southem Asia emerging countries, such as Philippines or Vietnam, for new opportunities due to the faltering regional economy in Taiwan. Traditional audit market is impacted adversely and becomes more competitive as a result of the shrinkage of auditing practices. Further, the Fair Trade Commissi凹, Executive Yu仰,

abolished the long-standing audit fee standard, set up by the Taiwan Certified Public Accountants Association in 1998. This exacerbates traditional audit market competition accordingly. In the supply side of audit service in Taiwan, there 紅E

much more quaIified public practicing accountants after the rise of passing rate of

uniform ∞rtified public accountants (CPA) examination in 1990's (L伐, Shih, and

Tsai, 2003). Besides, in 1998, the establishment oftax agent system impacts small firms adversely due primarily to cheaper fees charged by and easy of access to tax agent. As a result,∞mpetition within and outside of the public accounting profession further deteriorates the practicing environment

More important, today's regulatory environment (巴,皂 , passage of Sarbanes-Oxley Act of 2002) 2 broadens and intensifies pressures on audit firms to enhance the qual 旬, effectiveness, and efficiency of the services offered

2 For example, Sarbanes-OxJey Act of 2002 establishes the Public Company Accounting Oversight Board (PCAOB) to oversee public accounting firms. Annual inspection is conducted with 間spect

to registered public accounting finn 也at reg叫 arly provides audi t reports for more than 100 issuers. Inspection not less frequentJy than once every 3 years is conducted with respect to registered public accounting firm that regularly provides audit reports for 100 or fewer issuers

The PCAOB inspection report issued to 316 smaller public accoun恤g firms (100 or fewer issuer

c1ients) through July 2006 indicates 出 at 189 inspected firms (60 percent) have audit deficiencies (Herrnanson, Houston, and Ri間, 2007) 的 PCAOB, 也e Taiwan Disciplinary Committee of Certified Public Accountant (CPA), Taiwan Disciplin缸y Retrial Committee of CPA, Assessment

Committee ofTaiwan Institute ofCPA, and Accounting Research and Development Foundation in

T曲 wan perform 出e discipline of CPA, peer review 叩d 由e establishment of accounting and auditing principle, respectively. Jn recent year乳白e discipline of CPA has been increasingly

tighter 出an ever due primarily to material audit failures occurring once in a few years in Taiwan Hence, there is a tendency of rigorous regulati叩 over CPA in 出e global public accounting

86 Human Capi的Iand Operatíng Performance

(Vera-Muñon, Joanna, and Chow, 2006). Auditors become risk averse and conservative in accepting audit engagement and other service provlslOn (Fu,

Chang, and Ch凹, 2005). Moreover, many audit clients are proceeding with the strategy of globalization and e-commerce for competitive advantages in the changing market. Complex transactions and global marketing deployment result in auditing process and procedure more difficult than ever. In addition, when providing se何時的, auditors face a huge challenge in their professional judgement under the tendency of using a set of globally accepted accounting principle, the Intemational Financial Reporting Standards. Ac∞rdingly, it is undoubtedly an important lesson for auditor to adapt to the changing and stringent environment to survive and to sustain ∞mpetitive advantages in audit market

From the resource-based view of fírm, performance differences across fírms

cωbe attributed to the variance in the fírm's resources and capabilities (Penro銬,

1959; Wemerfel

t,

1984; Prahalad 個dH剖nel, 1990; Peteraf, 1993). Among the resources owned, which one enables the fírm to outperform others? Barney (1991) notes resources that are valuable, rare, unique, and di飢cult to imitate can providethe basis for fírms' sustained competitive advantages. Under the new e∞nomy landscape, Grant (1996) suggests 曲at knowled阱, existent primarily in human capital, is the critical ingredient for gaining a competitive advantage. Pfeffer (1994) points out that human capital has long been regarded as a critical resource in most fírms. Thus, it is the human capital that constitutes the most consentaneous item in the measurement of intellectual capital by researche時, such as Hubert (1996), Bontis (1998), and Guthrie (2001). ) In addition, prior studi的

document that human capital attributes, such as education, experience, and skills

and characteristics of top managers, a缸ect a firm's outcomes significantly (Huselid, 1995; Wrigl祉, Smart, and McMah側, 1995; Pennings, Lee, and

3 Intellectual capi阻1 refers to the swn of knowledge and competency 由at creates value and gains

competitive advantage for 祖 orgam且包 on (Roos and Roos, 1997; Stewart, 1997). Measurement

dimensions ofintellectual capital differ for different researchers. In addition 抽出em句 or item of hum個 capl祖1, other componen恆。fintellectual capital include organi血tion capital, flow capi凶,

mnovatJOn capl個1. customer capì個1 , and relationship capi個1. F or further det祉, we refer to Edvinsson 個d Malone (1997), R∞s, 泌的, and Dragonetti (1997), Stewart (1997), Bontis

Chiao Da Managemenl Review Vol. 29 No. 1, 2009 87

Witteloostui戶, 1998; Carpenter, Sande時, and Gregersen, 2001; Ling and J aw, 2006).

Audit firm is typically a professional service organization (Morris and

Empson, 1998), primarily providing financial statements audit services, tax

services and management consultation services by CPA and assistants with professional knowledge (Gibbins and Wright, 1999). 4 Accordingly, it is

expected that human capital influences audit quality and in tum operating performance of the audit firm. In particul缸, under the severely regulatory

environment, audit firms need to create, integrate, share and use knowledge about their c1ient's control activities and corporate govemance to improve audit

efficiency and upgrade audit quality (Vera-Muñ凹, Kinney, and Bonner, 2005). In

effectively implementing these knowledge-based activiti郎, human capital plays a critical role (De Carolis, 2003)

To our knowledge, only a few prior studies address the effects of human capl凶 on performance of an audit firm. Bröchel缸, Maijoor, and Witteloostuijn, (2004) examine the relationship between auditor human capital 個d audit firm

survival in the Dutch audit market for 1930-1992. Pennings, Lee and Witteloos仙叭, (1998) investigate the effects of human capital and social capital

on survival of audit firm. In the behavior accounting research, some exploit experimental methodology to examine the performance di宜erence of audit judgement for auditors with and without experience in bankruptcy forecast (Moriari妙, 1979), in payroll control system (Ashton and Brown, 1980), in analytical review process (Libby and Frederi仗, 1990), and in intemal control of sales transaction cycle (Tub悅, 1992). However, these prior studies focus on the performance of some specific auditing task not on the operating performance of

4 Maister (1993) and Gr間nwood 且d Lachm血 (19%) define professional service firms (PSF) as

個 org缸U且.tion that renders services such as law, acco間包ng 四d audit,∞nsul個包帥,

advertisemenl, and softw缸e. Monis and Empson (1998) use the lerm PSF 10 refer to an org缸U血tion that 回desm且 nly on 曲e knowledge ofits h凹nan capl阻1 , that is,也 employees 叩d the producer叫ow悶悶, 10 develop and deliver intangible solulions 10 clienl problems. ln addition to being CJ品sified as a PSF, audit firm is also referred to 晶尬。wledge-based 0嗯血U血tlOn

(Drucker, 1998), knowledge-inlensive organi訕。n (Starbuck, 1997), or human

88 Human Capital and Operaling Pe研ormance

an audit finn. Under the increasingly severe regulation in public accounting

profession, audit finn needs to upgrade audit efficiency and quality to sustain competitive advantage by rich human capital it owns. Accordingly, this study

aims to address the effects of high quality human capital on operating

perfonnance of audit finn. With the results obtained, this study fills the gap left by pnor sωdies and ∞ntributes to the literature in human capital of audit finn

Bröcheler, Maijoor, and Witteloostuijn, (2004) 的te that performance detenninants of audit finn, human capit剖, and smaller audit finn are 出ree areas

left underdeveloped in the audit market research due to data unavailability. 5

Although data about audit finn have been publicly available in Taiwan since 1989,

most prior studies focus on the demand side of auditing. In contrast, topics of supply side of auditing, such as administration of audit finn, are less investigated

(L伐, Shil>, and T:間, 2003; Chen and Lee, 2006; Cheng, Wan皂, and Weng, 2000a;

。隨時, Wang, and Weng, 2000b). In methodology, the most commonly used method to measure perfonnance is regression model. In addition to more restrictions imposed, 6 this method c剖mot identity the best performance unit due

to 1包 mean estimation standard (that is, higher than mean value is defined as the

superior and defined as the inferior if less than mean value) (Cooper, Seiford, and

Tone, 2006). In contras

t,

data envelopment analysis (DEA), a nonpar街ne甘 lC method, subje的 to less restrictions and can identity exactly; 7 among the units5 T 0 present. prior s仙dies exam.ining the topics of supply side of audi恤皂,出at IS operatmg

perfonnance of au曲直 nn, diffc前 from tbls study. For example, L間, Shih, and Tsai (2003), Banker, Chang, 個d Kao (2002), B扭曲缸" Chan皂, andC山mingh由n (2005),個d Chen 曲d Lee

(2006) investigate 出e operation of audit finn from different dimension and 出eir main themes

are different from tbls study. Next, Cher嗯, Wan皂, and Weng (2000a) and B扭曲er, Chan且,個d Cunningham (2003) ad扭扭曲e sc的 economy of audit finn by a parametric m拙。d (∞st

function and revenue function), different from the non-p缸缸netric method (DEA) used in 出JS study. Examining 出eh山n扭曲plt訕。 faudit finn, however, Pen血n斜, Lee, and Witteloostuijn (1998) and Brochel前" M品IJoor,祖d Witteloostuijn (20ω) focus on 血e effect of human capi旭l

on survival oppotturtity. Fi叫Iy, Chen皂, Wan皂,個d Weng (2000b) investigate the detenninants

of operating perfonnance (teclu世臼1 e伍ciency) of audit finn 刊ey do not take into account the

effect ofh山nancapital on perfonnance. Thus,也eirtopic investigated differs from this study

,

As a non-parametric method, DEA needs no priori infonnation about the distribution fonn ofproduction function 個d error tenn. ln contrast, a par.血netric method h且 to aS$Uß1e the

distribution form of production function and error terrn

Chiao Da .Managemenl Rev昭寺v Vol. 29 No. 1, 2009 89

assessed, which one or ones has the best performance. In one topic, this study examines the effect of human capital upon operating performance by the regression analysis. In another topi乳 白的 study employs the DEA to investigate the efficiency and retum to scale to capture which audit firms possess full efficiency and what retum to scale production are for most audit fi口ns. With the results from DEA, this study fills the gap left by prior studies

The remainder of this study proceeds as follows. We describe the research design in Section 2. Section 3 presents empirical results and Section 4 concludes this sωdy.

2.

Research Design 2.1 HypothesesPublic accounting firms, a typical

“

professional services" organization, offer a wide range of services to clients (Morris and Empson, 1998). These firms depend on the knowledge and professional expertise of partners and staff (Gibbins and Wright, 1999). 8 Therefore, knowledge is a key determinant of thesustainable competitive advantage (Stimpson, 1999) and a critical factor determining the performance of audit firm (Morris and Empson, 1998)

Knowledge can be classified as articulable or as tacit (Polanyi, 1967; Lane and Lubatkin, 1998). Articulable or explicit knowledge can be codified and thus can be written and easily transferred (Liebeskind, 1996). Tacit knowledge, however, is

not articulable and therefore cannot be easily transferred (Tee侃, Pisano, and Shuen, 1997). According to Maister (1993), tacit knowledge is integral to professional skills. As a result, tacit knowledge is often unique, difficuIt to imitate,

nonnal distribution of residual tenn, and the perfonn扭曲 me自urement of single output 0叫y 8 Researchers use diverse expressions to de街祖 knowledge. For instance, Goldstein (1993) defines

knowledge 甜甜 adequate understanding of fac阻,∞ncep阻, and 出e叮 relationsh巾, and 扭曲e basic foundation of the infonnation a per叩n needs to perform a task. Bartol and Srivastava

(2∞2,的) consider knowledge to inc1ude infonnati凹. ide品,血d expertise that are relevant for tasks perfonned by individuals, teams, work 阻ts, and the orga血且.tton 由 awhole. As 必C凶mg

。n individual's knowledge, 由JS S'缸.dy defines knowledge as 出e spec:叫ty and expertise needed to P前fonnaudit finn's job e伍 ciently and effectively

90 Human Capilal and Operating Performance

and uncertain (Mowery, Oxl旬, and Silvennan, 1996)

In tenns of 由e 甘ansfer means, explicit knowledge can be shared through verbal or written communication. On the other hand, tacit knowledge is typically

shared 血rough socializati凹, such as highly interactive conversations, apprenticeship (e.g., observation), storytelling, analogies, and shared experiences and activities (Nonak

a,

1994; Nonaka and Takeuchi, 1995; Za仗, 1999; Stenmark, 2000; Smith, 2001). As tacit knowledge cannot be codified and can only be observed through i的 application and acquired through practice, its transfer is slow, costly, and uncertain (Kogut and Zander, 1992). In additi凹, knowledge transfer involves both transmission and receipt. Knowledge receipt must 叫ce into account the absorptive capacity of the recipient or the recipient's ability to integrate new個d outdated infonnation (Cohen and Levinthal, 1990). Some knowled侈, such as financial information, can be transferred and integrated. However, some specific

knowledge or personal-oriented knowledg皂, such as infonnation of leader's character or ch訂m, can neither be transferred nor integrated (Jensen and Meckling, 1992; Gran

t,

1996)In a professional service organization, education, experiences, together with innate personal characteristi俗, are considered to be main elements of expertise (Bonner and Lewis, 1990). D'Aveni (1996) notes that the value of professionals'

education often holds 血roughout their careers. Thus, after completing their advanced educational requirem凹的, most professionals enter their careers as apprentices (for example, 的 residentslinterns in medicine, or as associates in law)

In these roles,由ey continue to learn and th酌, they gain significant tacit knowledge through

‘

learning by doing' (Pisano, 1994). As a result,

professionals gain explicit (articulable) knowledge through fonnal education or professional training and gain tacit knowledge through on-the-job learning and practical experience (Hitt et al., 2001). Most profession祉 service finns, such as audit finn or law finn, a1ways are fonned as a partnership. In such an organization structure, those who learn the rnost and who are highly effective in applying that knowledge are eventually rewarded with partner sta仙5 and thus own stakes in a finn. On their road to partnership, these professionals acquire considerable knowledge, rnuch of which is tacit (Szulanski, 1996). In the public accounting profession,Chiao Da Management Review 均1. 29 No. 1, 2009 91

professionals in an audit finn include partners, managers, senior audit仗, and staff assistants. They gain explicit knowledge, such as accounting, auditing, 個d taxes rules, through formal academic education and ∞ntinuing professional education and accumulate tacit knowledge through practical experience and personal characteristics.

According to the resource-based view of firm, resources that are valuable,

rare, unique, and difficult to imitate can provide a basis for the finns' sustained competitive advantages (Barney, 1991). Apparently, not all audit firms with knowledge-based human capital gain sustained competitive advantages in the market. Partner/practicing public accountant plays dual role as the chief executive officer and owner in an audit finn and manager is a potential partner of the finn Both partner and manager, upper-Ievel professionals, have a greater incentive to use their human capital for finn growth and perfonnance than do other employees (Pennin郎, Lee, and Witteloostuijn, 1998). Accordingly, we assert that human capital from the upper-Ievel professionals is the key factor for audit finn to gain sustained competitive advantages in the marl也t. In addition, knowledge, ∞mpetency, management notl帥, and personal charrn of the upper-Ievel professionals differ due to their varied farnily education, fonnal academic education, and work experiencιHuman capital of the upper-Ievel professionals is unique, difficult to imita筒, and irreplaceable (Stewart, 1997). Whether the upper-Ievel professionals constitutes the key resources, 的 defined in the

resour∞ -based view of firm, to gain sustained competitive advantages depends on their competency to create much more added-values for the finn. In other words,

whether manpower of the upper-Ievel professionals is valuable to the finn is the key resource to audit finn.

As stated previously, professionals gain explicit knowledge through fonnal education 個d tacit knowledge through work experience. Upper-Ievel professionals endowed with a high level of human capi叫, high education level and much experience, are more likely to deliver consistent and high-quality

services (Mincer, 1974). Further, Maister (1993) states that a professional finn's ability to attract and retain clients depends not only on i的∞mpetence to produ∞

92 Human Capital and Operating Performance

upper-Ievel professionals graduating 合om the top institutions often develop and maintain elite social networks that can be valuable-as a source of c1ients (D' Aveni and Kesr間, 1993). Experienced upper-Ievel professionals build relationships with current and potential clients and, over time, develop social capl叫 t尬。ugh their c1ient networks (Nahapiet and Ghosh剖, 1998). Thus, upper-Ievel professionals with high education level and more experien臼 are

expected to create added values for the firm and constitute one of the critical factors gaining sustained competitive advantages. As a result, we expect that an audit firrn with more experienced 個d high education level upper-Ievel professionals improves operating performance and develop the following hypotheses

H1: 1n an audit jir

m,

the more upper-Ievel professionals with high academice伽cation 1,仰el, the higher the operating pe.φrmancι

H2: 1n an audit jir

m,

the mare experienced uppe叫ével pr,可"essionals, the higher the operating performancιShultz (1961) states that human capital is the capital fostered by the knowledge and skill gained from education and training. 9 Psacharopoulos (I985) points out that investment in education and traini月 foster the forrnation ofhuman caplt叫 and it advances the productivity of employees. When the contribution of employees is more importan

t,

company invests more on human capital with which to upgrade their productivity and enhance the company's performance (Youndt et 瓜, 1996; Pames, 1984). From the perspective of human capital, education and training are regarded as a critical path to invest the human capital. For a ∞mpany, training is an important investment in human capital. Training not only advances the productivity of employee but a1so increases the company's performance (Garcí

a,

2005). In addition, literatures of human resources practice state that human9 Both education 個d 訂祖mng 缸'e two main ways to accumulate or invest hurnan capita1. However, Becker (1975) points out that various activiti自由at affect future monetary income or mentality through the enhancement of hurnan 臼p'叫 are regarded 晶 investment of human capital Broadly defined, investment ofhwnan capital includes education, tr阻ning, medical care, health, seeking for employment, and immigration

Chiao f)a Mal1agement Review Vol. 29 No. 1, 2009 93

resources system, including educational 甘amm皂, is unique and inimitable Synergies resulting from the system advance a firm's competency and constitute a critical factor for the firm to gain sustained ∞mpetitive advantages in the market place (Lado and Wils凹, 1994; Snell, Youndt, and Wright, 1996)

For an audit firm, how to provide service of high quality and to gain sustained competitive advantages in the market? As stated previously, probably the key factor resides in profe的 ionals of high quality, that is, abundant human

capital. In addition to gain knowledge through work experien侃, professional

accumulates expertise through on-the-job training. In the ∞urse of 個 audit engagement, knowledge and expertise about client's operating environment,

industry, business model, and operations are typically distributed unevenly among

audit team members. This is because auditors are routinely assigned to different

engagements that v訂y in terms of complexity and industry (Ramsay, 1994; Davidson and Gist, 1996; Rich, Solomon, and Trotmanm, 1997; Harding and Trotman; 1999; Murthy and Kerr, 2004). Hence, when a new professional is recruited, a professional is promoted, or accountinglauditing standard or related law/rule is promulgated or amended, an audit firm communicates related knowledge and professional skills to profession剖 through educational 甘ammg. This makes the professional possess necessary competence to finish audit job and to perform it efficiently and effectively

Hence, it is expected that educational training upgrades the knowledge and competency of the professional and in 仙 m enhance his/her job quality (Huang

and Tze嗯, 2001). Educational training thus is a supporting system to advance

human capital. This system not only advances the human capital level of an audit

firm, especially the firm-specific human capital, but also improves the firm's operating performan∞ Accordingly, we expect that the more the expenditure on educational 甘aining of each professional, the higher the expe口Ise, e宜ectiveness

and efficiency of his/her job. As a result, operating performance of the audit firm is thus enhanced and we hypothesize:

H3: In an audit jir

m,

the more expenditure on educational training,

the higher the operating peφrmancι94 Human Capita/ and Operating Performance

2.2 Data

2.2.1 Sample Selection

Empirical data used in this study are obtained from the 2001-2003 Census Report of Public Accounting Firms in Taiw徊, publ ished by the F inancial Supervisory Commission, Executive Yuan. For consistent comparison criter悶,

observations with audit firm age less than one or with e汀oneous data or with incomplete data are deleted. In addition, following Cher嗨, Wang, and Wer嗯,

(2000b), we exclude audit firms having no revenue either in 由eir financial 甜的t

service (FIN), tax service (TAX), or consulting and co叩orate regis甘ation services

(AD ηFor 2001-2003, the final number of observation is 571, 534,卻 d 539,

respectively. Table 1 displays the annual sample dis甘ibution

Table 1

Sample Distribution

Original number of observations

Observations with firrn age less than 1 Observations with erroneous data.

Observ國lOns wt也 incompletedata b

Observations wi也 no revenues in fmancial attest service (FIN), 恤 service (TAX), or ∞nsulting 個d corporate registration services (AD η

Final number of observations

2001 781 31 45 37 97 571 2002 762 21 62 49 96 534 2003 723 9 58 45 72 539

a For example, audìt firrn with 00 operating ex但nse or audit firm 00 practicing public a血。untant or audit firrn with the number of practicing public accountant fewer 曲an three but with positive attest revenues

from public ∞mpany

b For example, audit finn without any employ目前 withoutfixed assets or 明白outtO旭l ∞st' 2.2.2 Sample Classification

Testing the substitution bÿtween labor input and capital input of audit firms,

Chang and Chen (2005) indicate that technological level between audit firms with and without offering services to public company differs and in 仙rn their patterns of production function vary as well. Sample period of Chang and Chen (2005),

1989 to 2000, is different from this study, 2001 to 2003. In additi凹, Chen and Lee (2006) further divide audit firms without offering services to public company

Chiao Da Management Reνlel.tl 均1. 29 No. 1, 2009 95

into two categories, partnership and proprietorship. To obtain homogeneous

S街npl巴, that 時, observations with the same production techno10gy level, this study replicates Chang and Chen (2005) for the sample period of2001 to 2003. With the results, this 5ωdy verifies whether different audit firms reveal different pattems of production function.

Chang and Chen (2005) exploit the Box-Cox transformation procedure to examine the functional form of audit firm. As known, the function form of

product的n between constant elasticity of substitution (CES) and variable

el的ticity of substitution (VES) differs and the former is a log-Iinear form and the latter a Iinear form. Box and Cox (1964) provides a technique to discriminate between linear and log-linear functional forms

Chang and Chen (2005) define mean capit叫 assets available to each employee (rKlL) as non-Iabor capital expenditure divided by the number of employee. Average salary (w) is estimated by the sum of salary expens郎,甘剖mng

expenses, pension and fringes divided by the number of employee. Then they specify the relation between capital assets available to each employee (r.ι4月創d

average salary (w) as follows

(rK

/

LY

= α。 +αJwY

( 1 )whereλis the parameter of the power transformation on the variable.

By the Box-Cox procedure, equation (1) can be rewritten as follows

[((rKlL)l -1)/ À.] =叮 +α;[((w)Ã -1)/ À.]+u

,

(2)where u

,

is the normally distributed error term.Equation (2) can be assessed by the maximum likelihood techniques. As noted by Lovell (1973), the differential equation of (2) defines a c1ass of

production functions. When λapproximates zero, equation (2) approaches CES

model. If À approximates one, then equation (2) reduces to the VES model

According 的 equation (2) and given λ , the maximum likelihood estimate of the variance of residual is obtained by the regression of (rKlL)λon (w)λ Except for

96 Human Capilal and Operating Performance

the constant term, Box and Cox (1964) derive a maximum logarithmic likelihood

for determining the functional form parameter as folJows.

Lm間(λ) = -(N /2)ln&' (À) + (λ-1 )芝 (rK / L) (3) where N is the sample size.

The maximum logarithmic likelihood over the entire parameter spa臼 can

be found by estimating the λ in equation (3). By the folJowing equation, we have the 95% confidence interval ofλ

2[Lm(i).Lm

x

(λ)]

<

χ~(α)

= 3.84 (4)where

x;

denotes the chi-叫uare statistic w仙 one degree offreedom.Table 2 lists the functional form of audit firm estimated from equation (2)

to equation (4) for 2001 品。3. Total observations are divided into audit firms with

and without public company servi ∞s, which means that the audit firm renders and does not render financial statements audit service to the public company. Further,

audit firms without public company service are portioned into partnership and proprietorship firms.. As shown, confidence intervaJs ofλfor the audit firms

with and without public company services do not overlap, which indicating that their functional forms of production differ materialJy. In contrast, confidence

intervaJs ofλfor the partnership and proprietorship firms overlap. Henc巴, we

cannot identify 飢y significant difference in the functional form of production between partnership and proprietorship firms. Meanwhi峙, we conduct additionaJ tests to examine whether the value ofλdiffer from zero or one for audit firms with public company servic郎, without public company se閃閃的, partnership firms,

。r proprietorship firms. The untabulated results indicate that alJ values ofλare

different from zero or one significantly. Consistent with Chang, Yang, and Chen,

(2004), our results demonstrate that no definite functionaJ form of production

exists in the audit firms. As a result, we decide to utilize a non-par街ne甘ic method that imposes no assumption and least restriction on the functional form of

production, that 峙, DEA. Thus, it is feasible for us to examine the efficiency and retum to scaJe of audit firm by the DEA

Chiao Da Mal1agemel1t-Review Vol. 29 No. 1, 2009 97

As can be seen from the column of audit firms without public company service in Table 2, no sign的cant difference exists in the functiona1 form of production between partnership and proprietorship audit fi口ns. To obtain audit firms with identical technology level for ana1yzing e的 ciency and re仙m to scale,

total observations are partitioned into two categories in terms of providing financial statements audit service to public company. For ease of subsequent exposition, audit firms with public company services are refe叮ed to as large firms and those without public company services are referred to as small firms.

Table 2

Estimating Results of Functional Form of Audit Firms for 2001-2003 Total audit finns Audit company servlce finns without public

Wi出 public W尬。utpublic

P缸tnership Proprietorship

company servlCe company servlce

l 0.479 。 199 。 185 。 206 Confidence interval 。 329-0.629 。 159-0.238 。 113-0.257 。 159-0.253 on N 171 1,473 437 1,036 Log Iikelihood -2459 -21738 -6439 -15286 LRzf 4.34 15.40 11.28 24.12 P吋 〉zf 0.037" 0.000'" 0.001'" 0.000'" I.N = number of observations

2... . ••• denotes signi 日 cant at 5% and 1% level. respectively

2_2.3 Classilication of Groups for Comparison

To compare operating perfoπnance of different sized audit firms, we first conduct DEA to acquire efficiency scores for large and sma11 firms. Then we compare efficiency s∞res by either leading group or total number of employee for large and sma11 firms. As known, Big 4 intemational firms are regarded as a leading group. Hence large firms are divided into Big 4 and non-Big 4 groups to

∞mpare efficiency score. At present, Big 4 include KPM

G,

PricewaterhouseCoopers, Emst & Young, and Deloitte & Touche. Dissolution of the late Arthur Andersen makes its loca1 affiliate firm combine with the loca1

98 Human CapjfQl and Operating Performance

member ofDeloitte & Touche to become the largest firm in Taiwan effective June 1, 2003. Thus, actually Big 4 comprises five intemational firms for 2001-2002. For small firr肘, no generally perceived leading group is available. Small firms are partitioned into two categories in terms of medi缸1 of total number of employee,

that 芯, firms with number of employee less and more than 9.

2.2.4 Detection of Outlicr

Outlier refers to an observation diverting away 企om a cluster of data and is

always incongruent with other dataset (Bamett and Lew時, 1995). Outlier does not have the attribute of general acceptability and thus is excluded from the statistical

research (Davies and Gather, 1993). 10 In DEA, outlier materially affects the

estimation of efficiency score and thus has to be detected 細d excluded. However, Simar (2003) argues that no optimal or magic detection procedure is available in the definition of detection method. Sampaio de Sousa and Stosic (2005) point out

that most detection methods heavily depend on manual data inspection and are

hard to apply in the large sample condition. According旬, to detect outl ier

e宜iciently, this study exploits the Wilson (1995) procedure and designs related program by Matlab. 11

This study defines outl 間的自 a decision making unit (D恥ru) under

assessment that affects other DMUs and 郎 total efficiency score is greater than 5 After detection, no outI ier that materially affects e宜iciency of other firms is found

in the large firm sub-sample. However, a few outliers exist in the small firm

sub-sample. Number of outlier is 2, 1, and 4 for 2001, 2002, and 2003. Table 3

的 Ouùier is synonymous wì出 deviate observation, extreme observation. influential observation, and abnonnal observation

11 [f a DMU under assessment wi出 efficiency 品ore that materially affects other DMU, WiIson

(I995) argues, the DMU is probably an outlier 刷出 materi aI infIuence and 出e detection

procedure is 晶晶Ilows. (I) Compute 出e super e借口ency sωre for aIl DMUs under ∞nstant

retum to scale assumption. That 間, the DMU is excIuded from the constraint set when

e佰臼 ency for 出e DMU is computed. Thus e伍 ciency score is not reslricted to be 1 and DMU

刷出 e伍Clcncy score greater 曲曲 1 is probably the outlier. (2) For every possible outlier, ∞mpu扭曲ee伍 cicncy score Wlder constant retum to scale 品S山nptI on 1D由e sltualIon 血 at the

DMU intended for computing e宙間 ency score and the possible outlier 缸e excIuded from 出e ∞ns甘aint se!. (3) For every possible outlier, compute i個 extent of effect 00 efficiency score of

Chiao Da 比fanagemenl Review Vol. 29 No. 1, 2009 99

displays the annual sample distribution with outlier excluded. As no outl 間

detected in the large firm, the number of observations remains unchanged. Total

number of observations is still 171 and respective number of observations is 59,

58, and 54 for 2001, 2002, and 2003. After outliers are deleted, tot叫 number of observations of small firm is 1,466. For 2001-2003, annual number of observations is 510, 475, and 481 respectively. Thus we have to個1 final number of observations 1,637

Table 3

Sample Distribution with Outliers Dcleted

Large finn Small finn

Year Tota\

Big 4' Non-Big4 Subtota\ NE<9b NE~ 9b Subtota\

200\ 5 54 59 273 237 5\0 569

2002 5 53 58 254 22\ 475 533

2003 4 50 54 258 223 48\ 535

To叫 171 1,466 1,637

a Big 4 inc\ude KPMG, PricewaterhouseCoopers, Emst & Young, and Oe\oitte & Touche

b NE<9 denotes audit finns wi出 nwnber of emp\oyees fewer 曲曲 9 個d NE孟9 denotes audit finns with nwnber of emp\oyees equa\ to and more 曲曲 9

2.3 Model and Variable Definitions

2.3.1 Analysis of Efficiency and Return to Scale

By definition in DEA, efficiency is referred to whether we may produce

equal output with the least input or we may produce more output with equal input

(Cooper, Seiford, and Tone, 2006). Originally, this measurement approach is

established by Farrell (1957). 12 Then Charnes, Cooper, and 肘。des (1978)

甘 ansform the engineering measurement of efficiency into an economic

12 Farrell (1957) constructs a production frontier to enve\op all data and use 出e frontier 品 a benchmark 甘1e efficiency of other observation is measured a10ng a ray from the observed

produc包onpoint to the production frontier. Thus, the production frontier-based approach is also 闊的erred to as a measurement of relative e伍Clency.

100 Human Capilal and Operaling Peiformance

perspective estirnate of efficiency (hereafter the CCR model). 13 Finally, Banker,

Charn郎, and Cooper (1984) extend the CCR model and split the technical efficiency into pure technical efficiency and scale efficiency (hereafter the BCC model). 14 Technical efficiency measures the resources utilization efficiency of

an organization. It identifies the inefficiency resulting from either incorrect decision-making or poor administration of the management and lor from the waste of resources due to scale effects. In other words, we may ascribe the

existence of 臼11 technical efficiency or technical inefficiency to the management's ∞mpetency or/and scale effects

If the efficiency measurement ascribes inefficiency to the management's

competency only, we entitle the technical efficiency as pure technical efficiency

and as scale efficiency if ascribes inefficiency to the scale effects only. In addition, an organization with full scale efficiency is in the optimal scale of production, that is, constant return to scale. While an organization with scale inefficier>cy, It IS

either in the increasing return to scale or in the decreasing return to scale. 15

ln general, we may estimate efficiency score from either input-orientated or

output-orientated measure. 16 When the producer focuses on market demand and

can adjust the amount of production element freely, Lovell (1993) suggests that

efficiency score should be measured from the input-orientated measure. In

contrast to the level of services offered, audit firrn possesses more space to adjust

13ChammC冶oper, and 他odes (1978) employ dual 甘甜的nnaUon 阻d under constant retums to

sc叫e 晶sumption to transform 伽山J.it isoquant model of Farrell (1957) into ordinary linear programming model

14 Using 也e concept of distance function from Shephard (1970) and to derive the same model as

CCR, B扭曲er, Chames, and Cooper (1984) add four ass山nptions: production possibility set

with convex.i妙 me伍ciency postu1ate, ray unboundedness, and minim山n extrapolation. Then,

they relax the restriction of ray unboundedness ass山nption to establish a measurement model

under variable returns to scale

J5 If 個 audit 街mWI由 1 employee produces 1 nliUion outpu阻 but produces 1.5 nlillion outputs

WI出 2 employees, then 吐le finn is in the production condition of decreasing return to scale

Sinlil缸旬,曲。由er audit firm produces 1 nlillion outpu阻刷出 1 employee and produces 2 nlillion outputs W他 2 employees, and then the firm is in the condition of constant return to scale 回d optimal production scale.

16 Con臼ptu叫Iy, the input-orientated measure: given the same output quanti旬'. whether we can

produce it wi曲曲e 1目前 input? However,也e output-onen扭扭dme由自e: given the same intput,

Chiao Da Managemenl Review 均1. 29 No. 1, 2009 101

elements. Accordingly, this study measures the efficiency score from the input-orientated measure. Under this measure, technical efficiency, pure technical efficien句" and scale efficiency Iies between 0 and 1. TaI倚仗chnical efficiency as an ex缸nple , If the technical efficiency score of a DMU equals 1, the DtI,仇J has full technical e位iciency, which means that given the output level the DMU uses the least amount of element. If the technical efficiency score is less than 1, technical inefficier>cy exists in 出e DMU. Given the output level, the DtI,侃) may decrease the amount of input element. In detail, some of the input resources yields no benefit and pertains to resource waste. Likewi銬, both pure technical efficiency and scale efficiency scores apply to the s誼ne exposition above. As stated previousl弘 technical efficiency is further divided into pure technical efficiency and scale efficiency. Hence, their relationship is: technical efficiency score = pure tec加lical efficiency score x scale efficiency score. 17

First, we employ both the Cham郎, Cooper, and Rhodes (CCR) model to estimate technical efficiency (T,的 and Banker, Cham的, and Cooper (BCC) model

m , 目 =

min8-

e

(Ls

;

+

L

S: ) i=1 r=1 (5) " s.tL

XijÀj+

S; = 幟。 i=

1,2,..., m. j=

1,2,...,n " m y = Aυ AV F E eu 、,-E + F J S A A' η 5 , V J' 寸 ι J 間, λ J r = 1,2,..., s. 'if i,j ,r17 For example, audit finn A wi也 1 employce produces 1 million revenues but audit finn B produces I million revenues with 2 employees. In contrast to finn A. 由e tecru甘 cal e伍 clency

score of finn B is 0.5ηlÎs indicates 出at firm B may reduces 50% input of manpower to

produce the same revenues as firm A (悶 , 2 employees x 50% = 1 employee). As stated,

technical effici叩cy score is the product of pure technicaJ e伍ciency score and scaJe e伍 clency

score. lf firm B has 0.5 t郎hnical efficiency score resulting from p叮e technical e伍臼 ency (也副

院 P叮e technical e伍ciency score is equal to 0.5 and scale e伍 ciency score is equal to 1), 出en

lts me伍 ciency is derived from inappropriate utili回tion of human resources by the management. That is, firm B has waste of manpower. However, if finn B has 0.5 technical e伍ciency score resulting from scale e伍ciency (that is, pure technical e伍臼 ency score is equal to I and sc.le e伍ciency score is equal to 0.5), 出en Its me伍ciency is derived from scale size Specifically, firm B increases no revenue after 出eadditional manpower of I employee

102 Human Capìlal and Operaling Performance

to estimate pure technical efficiency (PTE), and as a result obtain scale efficiency

TE denotes technical

(SE) by derivating the preceding two e旺iciencies. Displayed below is the CCR model. e宜IClency. é is a non-Archimedean number and defined as a positive

real number with extremely small value. Xio is the input of element i by a specific DMU. y", is the output of service r by a specifíc DMU 勾 denotes the input of

element i by audit firm j. y" denotes the output of service r by audit firm j λIS

the weight and

s

;

,s

;

denotes the input slacks, and the output slacks, respectively BCC model is as follows. 、' , + edF S YL 叫 + eo mYLM r a ‘ 、 E Aσ nH m E 74 P (6) " s.t ~ xijÅj + s; = 你的 ; = 1,2, 可 m. } = 1,丸 , n ~YoÅj -S; =y",r =

1,2,一,s主毛 =1

j"l 令, 叫, s; 20V

;

,} ,r. PTE denotes the pure technical efficiencyIn theory, retum to scale depicts the changes in output as all production

elements change. Constant retum to scale, for example, indicates that output will

double if all production elements double. That 時, if output changes in proportion to the change in production elements, then the production situation is a constant retum to scale. In con甘a哎, increasing retum to scale denotes that average output

improves increasingly as input elements increase. Decreasing retum to scale

means that average output reduces decreasingly as input elemenl increases (Vari側,

1996). Conceptually, Ihe constanl retum 10 scale, increasing retum 10 scale, and decreasing retum 10 scale are equivalenl 10 the parametric constant economy to

Chiao Da Management Review Vol. 29 No. 1. 2009 103

know the exact return to scale condition in which an organization locates, we need to compare the value of technical efficiency under the three returns to scale assumptions. This includes technical efficiency (T.旬, pure technical efficiency (PTE), and technical efficiency under non-increasing return to sc曲 (TF!'). 18

The estimation model of T

F!'

is defined as follows (Banker, Chang, and Cooper,1996)

.

站N = min8-&(2:

s;

+

2:

s

;)

;:1 7=) (7) " s.t 芝 XijÂj+

S

;

=θx i=1 叉,...,m. j = 1,2γ ,n "2:

Y

,A

-S

;=Yro

r = 1,2,..., s n芝毛 sl

令, s; , 可 =。 \;j i,j ,r.Following Che嗯, Wang,如d Weng (2000b) and Banker, Chang, and Cunningham (2005), we identify the input and output variables needed to estimate the models above, that 時, x and y. Output variables include revenue of financial

泌的tation (Fl川, revenue of tax servi臼s (T AX), and revenue of advisory services

(AD η19 Revenue of audit of financial statements (FIN) is defined as revenue

ls lf TE=PTE' 的 DMU is in the production of constant return to 阻a1e. If PTE=Ti!', 伽 DMUis

m 出e production of decreasing return 阻 scale. However, If PTE* Ti!', 也e DMU 扭曲曲e

production of increasing return to scale (Banker et al., 2004)

的 Bo血 Cheng, Wang, and Weng (2000b) 血d Bank前, Chan耳, and C山mingham (2005) mc。中orate audit revenues, 個x revenu間, and management consulting revenues 晶 output variables. However, the tax revenues do not include revenues 音om audit of an in∞me 個X 問個rn. According to the Survey Report of Public Ac∞unting Firm in T,缸W曲, 由em句or five

so叮'ces of revenue for 扭曲dit firm are from audit of an income tax retum, audit of financ凶

statements of public ∞mpanies, audit of financial statements for granting a bank loan, audit of financial statements of nonpublic ∞mp由ues, and management consultation. To obtain a more appropnate so叮臼 ofrevenues for expos也凹,出1S 到udy reclassifies the revenues from audit of an mcome 旭x return mto 由e 個x revenues 甘1e revenues from audit of financial staternents of public comp由U間, audit of financial statements for granting a bank loan, and audit of fin個cial

104 Human Capilal and Operaling Performance

from audits of financial statements for public company, nonpublic compani郎, and for granting a bank loan. Revenue of tax services (TAX) includes revenue from rendering audit of an income tax return, tax plannin皂, administrative remedy of internal taxation, and other tax operations. We define revenue of advisory services (AD ηas revenue from offering management advisory service, co叩orate regls甘ation, and bookkeeping 飢d accounting service

Table 4 Variable

lnput variable

Definitions of Input and Output Variable De街tition

T otal number of employee (μ B)

Tolal fixed 扭扭扭 (CAP)

Operating cost (OPE) Output variable Revenue of audit of

financial slatements (FIN)

Revenue of tax services

(TAX)

Revenue of advisOly services (AD 內

Sum of the number of partoers, manage時. senior auditors, and staff

asSlst缸3個

Fixed 品sets owned by a firm and 扭扭扭 leased by the firm less fixed

品sets rented out 。

Statione旬, printing, utilities, newspaper and magazine, 個d postage Revenue from audits of financial slatements for public company,

nonpublic ∞mp缸U間, and for granting a bank loan

Revenue from rendering audit of an in∞met缸 retum.阻x planrtin皂, adminis甘甜 veremedy of intemal taxation,曲do出er 旭Xoperanons

Revenue from offering management advisory service, C。巾orate

regls甘ation, and bookkeeping and acco間恤g servl呵。

Next, this 5仙dy modifies 甘le input variables used in Che嗯, Wang, and Wen皂,

(2000b). Input variables used in this study include labor, capital, and operating

cost and defined as tot叫 number of employee (LA8), total fixed assets (CAP), and operating cost (OPl月, respectively. 20 Total number of employee (LA8) is

slatements of nonpublic companies are grouped together 阻d are refeπ.ed to 由 revenue of

financial attestation ins悟ad of as audit revenues

20 lnput variables employed by Cheng, W:阻皂, 阻d Weng (2000b) include ending number of

employees and net fixed 自扭扭 ln addition to 出e input of manpower and fixed assets, audit

finn incurs operating ∞st such as printing, pos旭阱, and stationel)'. Following Ou 個d Lin

(2000) and Hsu et al. (2003) 扭曲urung the knowledge-intensive organization, this study include not onJy labor and capi個I but also operating cost as the third input variable

Chiao Da Management Review Vol. 29 No. 1, 2009 105

defined as sum of the number of partners, managers, senior auditors, and staff

assistants. Total fixed assets (CAP) include fixed assets owned by a firm and

卸的 leased by the firm less fixed assets rented out. Operating cost (OPE) is

measured as expenditure on stationery, printin皂, utilities, newspaper and magazine,

and postage. Table 4 lists the definitions of input and output variable.

2.3.2 Effect ofHuman Capital on Operating Performance

The resource-based view of firm suggests that firm depends on its criti叫 or

core resources to adapt to the changing environment and to create and sustain its

∞mpetitive advantages (Penrose, 1959; Prahalad and Hamel, 1979; Wemerfelt,

1984). As stated previously, we argue that experienced upper-Ievel professionals

with high academic degree represent 曲 e critical resources with which an audit

firm plays an impo此ant role in the market. To render professional service with

quality, audit firm must be backed by a group of professionals with expertise. In

general, professionals gain knowledge through formal education and through

learning on the job. The human capital stock of formal education may be assessed

by the education level acq肌肉 d by the professionals. However, human capital

acquired from learning on the job may be estimated through experience and the

expenditure on educational training by an audit firm. Additionally, Che月 Wang,

and Weng (2000b) state that factors affecting technical efficiency of an audit firm

include firm size, firm age, service concentration, and number of firm branch. In

addition, CCR model (equation 5) comes from the assumption oflong run optimal

production scale (Wang and Lee, 2006). To achieve full technical efficiency

constitutes the long term goal pursued by an ente叩rise. According旬, this study employs the technical efficiency assessed by CCR model to measure operating

performance of an audit firm. Technical efficiency lies between 0 and 1, different

from ordinary least square regression model with unlimited dependent variable Accordingly, we exploit Tobit regression model instead. Taken together, we

develop our empirical model as follows

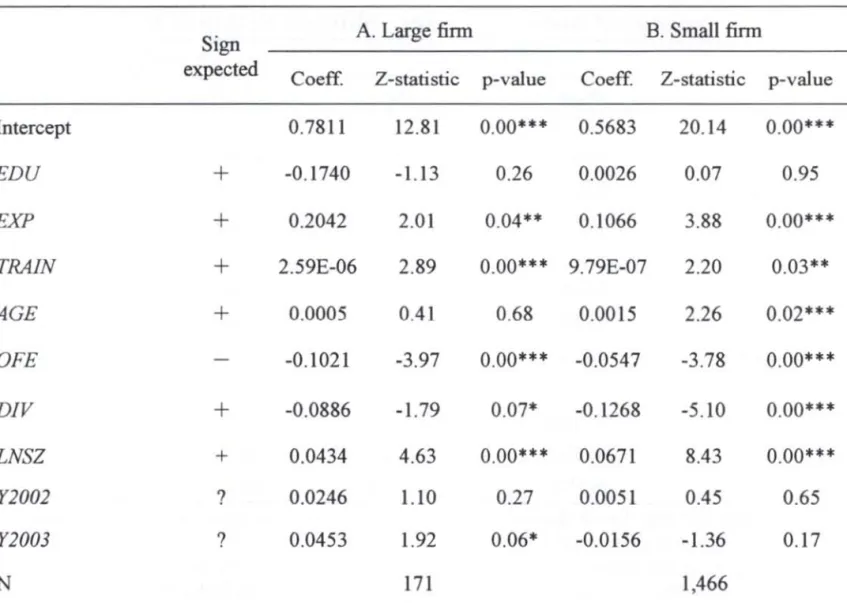

TE =戶。+ß, EDU+ ß

,

EXP+ß,T

RAJN+ß,

AGE+ß,

OFE+仇 DTV+扎 LNSZ

+

ß

.

Y2002 +仇 Y2003+ê106 Human Capilal and Operaling Performance

Dependent variable is the technical efficiency (TE) used to measure the

operating perfonnance of an audit finn. Experimental variables include intensity

of upper-Ievel professionals wi血 high academic educational degree (EDU), intensity of experienced upper-Ievel professionals (EXP), and mean expenditure on educational training (TRAlN). In addition, firm age (AG旬, establishment of

branch (OF.旬, business diversification (DI內, firm s ize (LNS勾, and year dummy

variable (Y2002 and Y2003) are included as control variables. The following

depicts the definitions of independent variables and their expected relationship with technical efficiency. Table 5 displays the definitions of variable used in Tobit

regression model.

(1) Intensity of upper-Ievel professionals wi由 high academic educational degree

(ED的

Upper-Ievel professionals with high academic educational degree possess

quality expertise and competency to direct assistants to complete job assigned Thus, we expect that the association between intensity of upper-Ievel professionals with high academic degree and technical efficiency is positive. EDU

is operational泣ed as the number of upper-Ievel professionals with master or

doctoral degree to the number of professional employees. Upper-Ievel

professionals include public practicing ac∞untants and managers. Professional employees comprise public practicing accountants, managers, and staff assistants (2) Intensity of experienced upper-Ievel professionals (EXP)

Experienced upper-Ievel professionals not only direct assistants to complete assignments efficiently with their rich expertise but a1so expand client base

曲。ugh their abundant social network. As a result, a positive relation between

expen侃侃d upper-Ievel professionals and technical efficiency is expected 互XP is

defined as a ratio of upper-Ievel professionals older than 35 years. 21 (3) Expenditure on educational training (TRAL川

Some audit fmns initiate educational 虹ammg when a professional is promoted or professional standardlrule is amended. This leads himlher to f:街niliar

21 Wi血∞ns叫ting partners in two audit finns, we define experienced upper-Ievel professiona1s as

Chiao Da Management Review 均1. 29 No. 1, 2009 107

with the job assigned quickly and thus enhances his/her competency. Hence, the

relationship between expenditure on educational training and technical efficiency

is positive. We define TRAJN as total expenditure on educational 甘aining divided

by ending number of professional employees

(4) Firm age (AGE)

Cheng, Wan皂, and Weng (2000b) report a significantly positive relationship

between firm age and technical efficiency of audit fmns due in part to the

leaming-curve effects accumulated. The age of a CPA firm (AGE) is defined as

the difference between data survey year and establishment year of audit firm pl的

(5) Establishment ofbranch (OF.劫

Cher嗨, Wang, and Weng (2000b) report 仙 inferior technical e在iciency of

audit firm wi由 a branch, suggesting an ine宜icient management over the branch

We construct a dummy variable and set to 1 when a branch is established and 0,

otherwise.

(6) 8usiness diversification (DJη

8ased on the existence of economies of s∞阱, Cher嗨, Wang, and Weng

(2000b) suggest a significant negative between business diversification and

technical efficiency of an audit firm. DJV is measured by an Entropy index over

three largest business revenue eamed by an audit firm: revenue of audit of

financial statements (FI^巾, revenue oftax services (TAX), and revenue of advisory

services (AD η

(7) Firm size (LNSZ)

Cher嗨, Wang, and Weng (2000b) find a positive relationship between size

and technical efficiency of an audit firm. Presumably, an audit firm is able to

E叮 oy economies of scale when its size expands. In this study, LNSZ is measured

as nature log of total number of employees (SJZE) in an audit firm. Total

employees include public practicing accountants, managers, staff assistants, and

the administrative staff.

(8) Year dummy variable (Y2002 and Y2003)

As technical efficiency is estimated annually, we construct ye訂 dummy

108 Human Capital and Operating Performance

environment in different year. Following Tseng, Kao, and Ho (2005) and Wang

and Lee (2006), we establish dummy variable of

Y2002

andY2003.

IfY2002

=1, itdenotes year 2002 and

Y2003=1

denotes year 2003. IfY2002=Y2003=O

, it denotesye紅 2001

Table 5

Definitions ofVariable in Tobit Regression Model Variable

Oependent variable

Tecbnical e伍 ciency (TE)

Experimenta1 variables

Intensì秒。fupper-Ievel

professionals wi出 high academic educational degree (EDU) Intensity of experienced upper-Ievel professionals (EXP) Expenditure on educational tr血rung (TRA1N) Control variables

Finn age (AGE)

Establishment ofbranch (OF,的

Business diversification

(D1V)

Finn size (LNSZ)

Year dummy variable

(Y2002 甜d Y2003)

Oefinition

ln OEA, t回bnical e伍 ciency score estimated by CCR model

(s凹n of the number of public practicing accountants and

managers Wl也 masteror doctoral degree) ~ (sum ofthe

number of public practicing accountants, managers, and staff

assistants)

(s凹n of the number of public practicing account扭扭曲d

managers older 曲曲 35 years) .;. (sum ofthe number of

public practicing ac∞m阻n阻,manage凹, and s個質品SIS個nts)

Annual expendi個re00 educational trainir啥.;. (sum of 伽

n山nberof public practicing acco叩tan阻,managers, and staff

臨時岫阻)

Oata s叮veyyear - establishment year of audit fi訂n + 1

When a branch is es旭blishedOFE=I and 0,。由erwlse

(ratio of revenues 企om audit of fmanc凶 statements) X log( 1

ratio of revenues from audit of fmancial statemen旭)+ (ratio

of revenues of tax se凹1血。 x log( 1 .;. ratio of revenues of

tax services) + (ratio ofrevenues ofadvi叩ry services) x

10g(1 宇間的 o ofrevenues ofadvisory services)

Nature log oftotal number ofpublic practicing accoun祖n阻,

manage間,s旭ff assistan阻,and 出eadministrative s扭住。

IfY2002 斗, it denotes year 2002 and Y2003= 1 denotes year 2003. If Y2002=Y2003={), it denotes year 2001

3.

Empirical ResultsChiao Da Management Review Vo/. 29 No. 1, 2009 109

Descriptive statistics of input and output variable are displayed in Table 6 and 7 for large and small firm, respectively. As can be seen from Table 6, except

Table 6

Descriptive Statistics of Input and Output Variable for Large Firm

LAB CAP OPE 1刁'N TAX ADV

2001 (N=59) Mean 157 107.028.028 59,394,203 105,610,861 58,996,936 30,069,486 Max 1,651 1,420,741,872 938,147,783 1,405,686,316 715,508,031 627,760,591 Min 13 280,974 1,944,781 232,541 2,862,049 454,802 Median 52 32,642,335 11,121,261 13,479,387 20,469,586 6,388,361 S.D 337 258,912,177 167.33L672 301.348.368 127,622,754 94,423,605 2002 (N=58) Mean 168 108,574,552 65,002,175 117,224,118 55,705,394 32,102,336 Max 1,542 1,124,719,558 1,040,000,000 1,631,239,155 707,898,321 455,003,305 Min. 15 1,200,00 。 1,562,318 170,000 3,861,700 208,500 Median 50 30,490,189 11,911,545 13,495,500 19,256,218 5,353,063 S.D. 353 237,938,577 182,658,841 335,021,381 120A66.181 85.148.757 2003 (N=54) Mean 170 99,857,270 68,670,405 135,812,127 58,240,849 34,814,881 Max 2,001 1,919,303,645 1,212,204,071 2,694,310,845 562,961,475 586,589,875 Min \0 693,083 2,436,646 J 06,506 2,046,030 762,815 Median 50 30,264,871 13,562,306 16,258,338 20,307,099 6,067,686 S.D 393 286,323,0 I 0 203,783,663 451,109,624 124,271,411 104,837,834

1.N = number of 曲servations. LAB = to個1 number of employee. CAP = tota1 fixed 晶sets. OPE = operating CQst. FIN= financial attestation revenue. rAX= tax revenue. ADV= advi叩門 servlce revenue

2.A11 variable are expr自sed in new T創W個 dollarexcept LA8

both total fixed assets (CAP) and tax revenue (TAX), total number of employee (LAB), operating ∞st (OP日, financial attestation revenue (FIN), and advisory

110 Human Capilal and Operating Performance

service revenue (AD 內 ofl紅ge finn, on average, increase year by year. F or the

small finn, shown in Table 7, operating cost (OPE) increases annually. However, total number of employee (LAB), total fixed assets (CAP), financial attestation

revenue (FIN), tax revenue (T AX), and advisory service revenue (AD 內 either remain intact or f1uctuate over time

Table 7

Descriptive Statistics of Input and Output Variable for Small Firm

LAB CAP OPE FIN TAX ADV

2001 (N=510) Me個 11 9,428,046 2,049,575 1.375.350 3,650,960 1,551,527 Max 58 70,302,833 23,105,878 12,380,223 34,457,170 18.459.491 Min 11,976 83,141 21,598 4,990 499 Median B 7,636,017 1,387,138 798,424 2,535,297 688,686 S.D 9 8,062,489 2,095,905 1,723,509 3,865,816 2,243,945 2002 (N=475) Me祖 11 9,999,314 2,066,758 1,439,179 3,727,934 1,505,310 M缸 93 52,754,963 19,127,110 25,000,000 44,007,939 19,496,790 Min 2 420,000 20,000 10,000 30,000 1,00。 Median 8 8,009,970 1,350,367 800,000 2,508,120 610,000 S.D 11 8,091,044 2,294,592 2,312,479 4,403,262 2,377,551 2003 (N斗 81) Mean 11 9,534,635 2,068,803 1,409,333 3,691,514 1,580,123 M缸 72 137,327,218 21,592,465 24,814,334 48,595,744 20,731,860 Min 2 108,807 55,836 14,242 50,148 1,003 Median 8 7,183,120 1,378,192 797,109 2,449,218 608,393 S.D 10 10,103,863 2,279,356 2,049,970 4,372,807 2,624,836

I.N = nwnber of observations, LAB = total nwnber of emp10yee. CAP = to旭1 fixed assets. OPE = operating ∞sl. FIN = fin祖cial attestation revenue. TAX = tax revenue, ADV = advisory 盟rvJCe revenue.

2.All variab1e 缸'e expres阻 d in new Taiwan dollar except LAB

In order to examine the isotonicity required by DEA, that 時, Increase in input accompanied by non-decrease in output, this study estimates the Pearson