創新的金融服務 ~ 保險結合殯葬服務的商業模式設計

123

0

0

全文

(2) 創新的金融服務 ~ 保險結合殯葬服務的『常春』商業模式設計 A New Financial Service Innovation ~ The Design of an Insurance-Funeral Business Model 研 究 生:陳碧玉 指導教授:張力元. Student:Eva Chen Advisor:Charles V. Trappey 國 立 交 通 大 學. 管 理 學 院 (國際經貿學程)碩士班 碩 士 論 文. A Thesis Submitted to Department of Management Science National Chiao Tung University in partial Fulfillment of the Requirements for the Degree of Master Program of International Business Administration and Trade June 2004 Hsinchu, Taiwan, Republic of China. 中華民國九十三年六月.

(3) ABSTRACT. Nothing is certain but death. As the aging population and lower birth rate problems become worse, more and more people are aware of the necessity of pre-planning their future life. At the same time, many companies try to find new business opportunities for this coming trend. Funeral business is one of the great potential markets which have estimated over NT$ 50 billions sales volume per year. This figure is becoming bigger with the inflation rate. Pre-need funeral arrangement is one of the products that are born under this trend, but it is still not popular to the public. The reason is people have to pay money before they get the service. For customers, they feel it is difficult to buy an intangible service especially when they are not familiar with this service.. This research tries to build a new business model for the people who are willing to pre-plan their future risks. The design of this new business model is to extend a whole life insurance service to pay the funeral expenses. Customer could have an easier and cost saving way to buy two services at one time through this new model design. Insurance companies could earn more business opportunities from providing this new financial service to the customers. The findings and results of this new business model also provide an idea for government, insurance companies, and funeral homes some information for the future products development. Key words: Insurance, Funeral Service, Pre-need funeral arrangement, CRM, New financial service. i.

(4) ABSTRACT IN CHINESE 中文摘要. 人的ㄧ生無非生、老、病、死四個階段,每個人都希望自己的人生可以「生前活的 精采,死後不留遺憾」。生前要過怎樣的生活,可以靠自己的努力獲得,然而如何讓人 生的謝幕ㄧ樣精采,漸漸地被現代人所關心。 台灣的社會已邁入老人化的時代,有人甚至說: 「二十一世紀是老年人的世紀」 。再 加上社會結構改變,許多現代人意識到自己的未來生活不能仰賴子女而須自己提早規 劃。所以,許多的產品就在這樣的時代背景下推出市場。其中生前契約便是近來日漸為 民眾所知的ㄧ項產品。它教育客人事先規劃的觀念,除了價格於購買時固定,不用擔心 通貨膨脹問題;減輕家人日後支付喪葬費用的負擔及讓自己有個完美人生的謝幕都是其 銷售的重點。另外,加上這個市場每年有超過 500 億的商機,所以許多財團及殯葬業者 都想跨足此市場。不過,生前契約引進台灣雖近十年,由於需事先支付前金,再加上殯 葬市場的服務品質參差不齊。多數的消費者仍多採身故時請殯葬業者服務的模式。 本研究主要利用人壽保險發展一套新金融服務模式,將保險服務延伸至殯葬服務。 讓客戶在買保險時,除了規劃人生的風險,同時保險公司能真正落實陪客人走完他的最 後一段路。對客戶而言,利用保險來支付喪葬費用,達到減輕家人負擔愛的表現,同時 透過保險公司的篩選包裝,安心一次購足兩項服務。對保險公司而言,透過差異化的商 品服務,可以開拓新市場及商機,同時搭配客戶關係管理增加更多銷售機會。研究中探 討市場概況及其潛在的商機。同時,亦對國內外的相關產品做了一些研究。希望此商業 模式的設計,可以提供業者研發新產品及政府制定相關法令做一些參考。. 關鍵字: 保險、新金融服務、殯葬服務、生前契約、顧客關係管理. ii.

(5) ACKNOWLEDGEMENT. This thesis is in memory of my beloved father. He died in July, 2003. As experiencing the sorrow at my father’s death, I realize that life is unpredictable. How to pre-plan your future is very important. I also see some problems that a family might have when encounter similar experience. It is his spirit that supports me to finish this thesis.. Besides my father, I would like to express my warmest thanks to my professor, my family, my colleagues, and friends that help me during this hard time. I can not complete this thesis without their continuous support.. As a part-time student, working woman and a-mother-to-be, it is really a hard time to me to finish this thesis, especially writing English thesis for a student that her mother language is Chinese. My professor gave me a chance to study harder as possible. Although I study in Taiwan, he makes me feel like I study abroad. This is definitely would be an unforgettable and valuable experience in my life.. I wish one day this thesis could really put into practice and help people in need. Finally, I wish everyone lives a happy and healthy life.. iii.

(6) TABLE OF CONTENTS ABSTRACT .............................................................................................................................................................I ABSTRACT IN CHINESE .................................................................................................................................... II ACKNOWLEDGEMENT..................................................................................................................................... III LIST OF TABLES.................................................................................................................................................VI LIST OF FIGURES..............................................................................................................................................VII CHAPTER 1 INTRODUCTION............................................................................................................................. 1 1.1. RESEARCH MOTIVATION AND BACKGROUND .............................................................................. 1. 1.2. RESEARCH OBJECTIVES ..................................................................................................................... 4. 1.3. RESEARCH PROCESS............................................................................................................................ 5. CHAPTER 2 LITERATURE REVIEW .................................................................................................................. 6 2.1. THE MEANING AND CHARACTERISTICS OF “PRE-NEED FUNERAL ARRANGEMENTS".. 6. 2.2. THE DEVELOPMENT OF AMERICAN “PRE-NEED FUNERAL ARRANGEMENTS".............. 10. 2.3. THE DEVELOPMENT OF TAIWAN “PRE-NEED FUNERAL ARRANGEMENTS".................... 16. 2.4. CUSTOMER RELATIONSHIP MANAGEMENT ................................................................................ 29. 2.5. MARKETING MIX ................................................................................................................................ 32. CHAPTER 3 INSURANCE-FUNERAL BUSINESS MODEL DESIGN ............................................................ 35 3.1. BUSINESS MODEL DESIGN ............................................................................................................... 36. 3.2. HYPOTHESIS ........................................................................................................................................ 38. 3.3. INSURANCE-FUNERAL BUSINESS MODEL STRUCTURE ........................................................... 40. 3.4. 4PS & 4CS OF “INSURANCE-FUNERAL BUSINESS MODEL”....................................................... 47. 3.5. HOW DOES “INSURANCE-FUNERAL BUSINESS MODEL” HELP TO MAINTAIN LONG TERM CRM?. .................................................................................................................................................. 57. CHAPTER 4 METHODOLOGY.......................................................................................................................... 61 4.1. METHODOLOGIES............................................................................................................................... 61. 4.2. METHODOLOGIES OF EACH HYPOTHESIS ................................................................................... 64. CHAPTER 5 DISSUSSION THE RESULTS OF INSURANCE-FUNERAL BUSINESS MODEL ................... 71 5.1. THE METHODOLOGY RESULTS AND DISCUSSION..................................................................... 71 iv.

(7) 5.2. METHODOLOGICAL RESULTS THAT SUPPORT THE BUSINESS MODEL DESIGN ................. 86. CHAPTER 6 MODEL VALIDATION .................................................................................................................. 88 6.1. ASSUMPTIONS OF “INSURANCE-FUNERAL BUSINESS MODEL”............................................. 88. 6.2. THE COST AND PROFIT PREDICTION FOR THE FIRST TEN YEARS ......................................... 92. CHAPTER 7 CONCLUSION AND SUGGESTION............................................................................................ 96 7.1. CONCLUSION ...................................................................................................................................... 96. 7.2. SUGGESTIONS FOR THE FOLLOWING RESEARCH ................................................................... 100. APPENDIXS....................................................................................................................................................... 107 QUESTIONNAIRE 1.......................................................................................................................................... 107 QUESTIONNAIRE 2.......................................................................................................................................... 111. v.

(8) LIST OF TABLES. TABLE 2.1 BREAKDOWN OF TAIWAN FUNERAL SERVICE EXPENSE .................................................... 18 TABLE 2.2 PREDICTION OF FUNERAL EXPENSES GROWTH BY 2% INFLATION RATE PER YEAR . 19 TABLE 2.3 PRE-NEED FUNERAL ARRANGEMENTS IN TAIWAN .............................................................. 21 TABLE 2.4 COMPARISON BETWEEN TRADITIONAL FUNERAL SERVICE AND PRE-NEED FUNERAL SERVICE........................................................................................................................................... 23 TABLE 2.5 COMPARISON OF PRE-NEED FUNERAL MARKET BETWEEN AMERICAN, JAPAN AND TAIWAN............................................................................................................................................ 24 TABLE 4.1 METHODOLOGY SUMMARY OF EACH HYPOTHESIS ............................................................ 64 TABLE 6.1 NEW CUSTOMER PREDICTION FOR THIS MODEL.................................................................. 89 TABLE 6.2 THE PREDICTION NUMBER OF INSURED USING THIS MODEL........................................... 90 TABLE 6.3 OTHER REVENUE COMES FROM THE INSURED BUYING OTHER INSURANCE PRODUCTS THROUGH LONG TERM CUSTOMER RELATIONSHIP MANAGEMENT......... 91 TABLE 6.4 COST PREDICTION OF 「INSURANCE-FUNERAL BUSINESS MODEL」............................ 92 TABLE 6.5 PROFIT PREDICTION OF 「INSURANCE-FUNERAL BUSINESS MODEL」 ........................ 94. vi.

(9) LIST OF FIGURES. FIGURE 2.1 PERCENTAGE OF PEOPLE OVER AGE 65 IN TAIWAN ........................................................... 17 FIGURE 2.2 MARKETING-MIX STRATEGIES ................................................................................................ 33 FIGURE 3.1 TIME LINE OF DEALING A FUNERAL AND INSURANCE CLAIM........................................ 36 FIGURE 3.2 PROCESSES OF BUILDING AN INSURANCE-FUNERAL BUSINESS MODEL..................... 41 FIGURE 3.3 INSURANCE-FUNERAL BUSINESS MODEL ............................................................................ 43 FIGURE 3.4 MARKETING MIX ......................................................................................................................... 48 FIGURE 3.4 LONG TERM CUSTOMER RELATIONSHIP MANAGEMENT OF 「INSURANCE-FUNERAL BUSINESS MODEL」 ................................................................. 59 FIGURE 5.1 THE PERCENTAGE OF OLD AGE POPULATION IN TAIWAN ................................................ 71 FIGURE 5.2 BIRTH RATE IN TAIWAN ............................................................................................................. 72 FIGURE 5.3 OLD AGE POPULATION DEPENDENCY RATIO IN TAIWAN.................................................. 72 FIGURE 5.4 LIFE INSURANCE INSURING RATE........................................................................................... 74 FIGURE 5.5 QUESTIONNAIRE 1- SAMPLE SIZE AND STRUCTURE.......................................................... 76 FIGURE 5.6 QUESTIONNAIRE 2- SAMPLE SIZE AND STRUCTURE.......................................................... 80 FIGURE 5.7 DRAWING OF WHOLE LIFE AND TERM LIFE INSURANCE.................................................. 84 FIGURE 6.1 COST AND PROFIT VALIDATION OF 「INSURANCE-FUNERAL BUSINESS MODEL」.. 94. vii.

(10) CHAPTER 1 INTRODUCTION. 1.1 Research Motivation and Background Nothing is certain but death. Death is a must process that everyone has to face. There is no getting away from the fact that a death in the family causes a great deal of stress and upset. In real life, we tend not to think about funeral planning until after a person has died, and many do not discuss their final wishes with those closest to them. Yet, not doing so places the responsibility to handle such affairs with surviving loved ones who are still trying to accept their loss. According to Ministry of the Interior’s statistic in 2003(Department of Civil Affairs, Ministry of Interior,2003), the population of aged people(above 65) are 9.02% of Taiwan’s total population. Compare to WHO’s definition of advanced age society (7% 0f total population), Taiwan has already been an aging society. As the result of aging society, the Executive Yuan estimate the body count from 2002 to 2050 will be 3 times of 2002’s number, which are 130,000. The funeral expenses per person are around NT$ 376,000 (Department of Social affairs, Government of Taiwan Province, 1998), the total funeral related expenses in. 1.

(11) Taiwan would around NT$ 50 billion per year. This number will increase through the increasing deceased people and inflation rate. As the funeral business market is a huge potential market, many funeral homes and big business are eager to enter this market. Some of them introduce pre-need arrangement product concept from the WEST and Japan in 1993, but it didn’t work very well because of the social value to this concept is not popular. However, people are more open to talk about the dead and will issue in these two years. More and more companies join this market and even have some commercials on TV. On the other hand, the government enacted some policies to the funeral business in 2002, this represents that the government’s concern of the development of this market. Many consumers have considered arranging their future life, not only for themselves but also for their families. Although there seem some products to choose in the market, they still hesitate to buy because of the following reason: 1. They know little about funeral affairs, so that it is hard to choose the right product for them. 2. They don’t trust funeral homes enough because of the small size, credit, consistency of the funeral homes. They are afraid to pay ahead and finally get nothing.. 2.

(12) 3. The funeral service business is still not well organized enough. Products don’t have a standard price, service content. Customers may encounter some losses and disadvantages buying this product. Under this environment, we found that insurance product has similar product concept with the pre-need funeral arrangement, because they both have pre-planning concept and try to minimize some risks in people’s life. As the aging market has been quite concerned by many businesses, some funeral companies try to forge alliance with insurance companies or rest homes to figure out a new integrated product which can link with funeral service to provide a one stop shopping service to the customers in 2003. Even the insurance companies also try to develop more new product related to this booming aging market. This thesis tries to setup a new business model that funeral company ally with insurance product and compare this new product concept with traditional funeral business using 4P model and business process. As the related research is little, this research also gathered some information from either insurers or funeral homes. The research also tries to make a 10 year cost and profit validation for companies or government who are interested in this new financial service development.. 3.

(13) 1.2 Research Objectives Customers know little about funeral service and many families encounter financial problems because of dealing with funeral affairs. New business model concept ally with the funeral home can be a trend to provide a better, safer financial service to the customers. This thesis probed into the development of funeral arrangement and insurance products. Furthermore, try to setup a new integrated product and analyze its possibility of success in the market. From business view, how to maintain long term relationship with customer and earn more business opportunity are key points to a company’s consistency. This thesis tries to analyze how the new business model provides a better way to maintain long term customer’s relationship and profitability. As the pre-need funeral issue has been more popular in the market, this thesis provides some information for the government to enact related policy to protect customers’ rights and for business companies to develop better products and services.. 4.

(14) 1.3 Research Process 1. Through gathering information to understand the development of the products, the background of the market and setup the research structure and methodology. 2. To gather related information from books, periodicals, magazines, newspapers, papers, funeral homes and insurance companies. 3. Setup research structure, hypotheses and new business model design. 4. Analyze the marketing mix of the product by using 4P model. 5. Te probe into the long term customer relationship of this new business model. 6. Identify research object and methodology, and then gather some information for cost & profit validation. 7. Setup some assumptions for analyzing the ten year cost and profit validation. 8. Make conclusions and suggestions.. 5.

(15) CHAPTER 2 LITERATURE REVIEW. The meaning and characteristics of “Pre-need Funeral Arrangements". 2.1. 2.1.1. The meaning of “Pre-need Funeral Arrangements”. 1. Eric Clark (2002): “Pre-need Funeral Plan” is an agreement in which a seller agrees to provide funeral service and merchandise at the time of buyer’s death. 2. William Stalter (2001): A “preneed trust” is a trust which holds, administers and distributes those payments made by a preneed contract purchaser to a funeral home which the applicable state law requires the funeral home to deposit into trust as security for the performance of the preneed contract. A 「preneed contract」is a written agreement between a consumer (a “purchaser”) and a funeral home in which the funeral home agrees to provide the funeral or cemetery merchandise or services described in the contract (a “prearranged funeral”) at the purchaser’s death. Every state preneed law requires the funeral home to deposit some or all of the purchaser’s payments into a preneed trust. 3. Ministry of Interior (2002): According to” Funeral and Interment Management. 6.

(16) Regulation” Article 2, Subsection 12, the definition of “Pre-need funeral arrangement” :The interested parties (Funeral home and purchaser) agree the other party to provide the funeral or cemetery merchandise or services described in the contract after the appointed party’s (Purchaser) death. 4. You zhi, Huang and Wen long, Deng (2001): “Pre-need funeral arrangement” is a contract that the funeral homes should provide any related products, services and information for before customers making a decision and guarantee the enforcement of the contract.. 2.1.2. The characteristics of “Pre-need Funeral Arrangements". You zhi, Huang and Wen long, Deng (2001) stand for that a “Pre-need funeral arrangement” should base on a complete service system. It should provide services with humanity concern and esteem. These services include care at one’s dying breath, medical service, heritage arrangement, funeral service, soothe family, law consultant. The services should be provided with the following characteristics: 1. The seller should prompt clear product information to the customers. As the customers know less about the funeral service, they are intended to be sold the product that might suitable for their demand. So the seller should take the responsibility of providing the most suitable service to meet the customers’. 7.

(17) demand and let them know they have the right to choose the service content. 2. The services or products provided by the seller must be transparent and open. Before signing pre-need contract, the seller should try to explain the details of all the products, including the price, different classes of services and so on. 3. Customers can be their own master to choose the product or service they want. Customers can choose the most suitable product or funeral service depending on his or her own will, economic situation, religion, and family’s suggestion. 4. Customers have the right to change the service content or cancel the contract before they die. As the future is unpredictable, customers’ need may change through time. Without damaging the seller’s legal right, customers could change or cancel the contract with freedom and flexibility. 5. As pre-need funeral arrangement is the people who sign the contract before his death, his own will or decision must be fully respected by everyone. Traditional funeral service, deceased people can not speak or decide his funeral arrangement. The family may have different opinions about the funeral arrangement and waste lots of money on unnecessary products or services. The deceased people signed the pre-need funeral arrangement for themselves; therefore, their will must be fully respected.. 8.

(18) 6. The money for signing a contract collected by the seller must be used in a legal and safe way. In order to guarantee the future execution of the pre-need contract, the sellers must arrange the money they collected from the customers legally and safely. If they charge guarantee money ahead from customers, 75% of the money has to put into a trust account for assuring the future enforcement of the pre-need funeral arrangements. (Funeral and Interment Management Regulation, 2002) 7. The government should make policies to supervise the companies that provide pre-need funeral arrangement service. As the deceased person could not supervise the service quality of the funeral homes, the government should make a supervisory system or assign a department to supervise this business regularly in order to protect customers’ rights.. 9.

(19) 2.2. The development of American「Pre-need Funeral Arrangements」. The preneed concept originated with burial organizations that sold burial certificate plans in the 1930s. During the 1950s, funeral directors began selling prearrangements in the United States. The preneed market slowly evolved over the next 30 years. There are two main reasons that pre-need sales are a booming industry today. 1. According to the 2003 World Population Data Sheet from Population Reference Bureau in U.S, we found that 10% of the U.S populations are over age 65. This phenomenon means that the continuing growth of older population will bring more potential market in pre-need funeral service. 2. Funeral expenses are one of the most purchases that Americans make. According to a survey from AARP (American Associate of Retired Persons), the average cost of funeral per person was US$ 5,160(without any extras). In-ground burial can add another US$ 2,400 to total expenses. In contrast to the purchase of these other expensive products, however, most funeral and burial purchases are made when buyers are vulnerable emotionally and lack the time and information to negotiate prices effectively. This is another main. 10.

(20) reason why increasing numbers of consumers are entering into preneed agreements to purchase funeral and burial goods and services prior to death.. More and more Americans are entering into preneed agreements to purchase funeral and burial goods and services prior to death. Funds in preneed agreements exceed $25 billion, up from $18 billion in 1995. Two in five persons age 50 and older reported that they had been contacted about the advance purchase of funerals (43%) or of burial goods and services (39%). (AARP survey, 1999) Individuals prepay for funerals and burials by entering into a preneed agreement, or contract, to pay in advance for goods or services they will receive upon death. Generally, this agreement is between the individual and the funeral director, and is funded through a funeral trust, annuity, or insurance policy. Upon the individual's death, the funds are used by the representative of the funeral home or cemetery to provide the designated goods and services. In the past, preneed funeral agreements often included only cemetery plots and, therefore, were primarily sold by cemeterians. Preneed agreements are now likely to include a package of both funeral and burial goods and services that may be sold by funeral directors or cemeterians.. 11.

(21) 2.2.1. Funeral Insurance in American. There are plenty of reasons to pre-plan and, if possible, pre-pay your final arrangements long before the need arises. A product called "pre-need" insurance, also known as burial or funeral insurance is intended for just that purpose. “Funeral Insurance” first appeared in 1930 when Los Angeles funeral director became concerned that legal reserve life insurance was the only dependable vehicle through elderly people could pre-fund their future funeral expenses.. According to a 1990 survey of 18 companies conducted by the Life Insurers Conference(LIC), there is US$ 3.8 billion of pre-need funeral insurance in force from two million policies. In 1998, these companies sold 192,923 pre-need contracts totaling US$ 165 million of new premium. There are over 50 life insurance companies in this business, either as a specialty or as part of a broader portfolio and market. Until 2003, most funeral homes work with at least one major insurance company that offer funeral insurance.(Funeral expenses). Unlike some other types of insurance, funeral insurance is a kind of insurance that only covers funeral expenses. (Insure.com)Usually the face amount is smaller than other life insurances; most of them are under US$ 10,000. Under the insurance. 12.

(22) amount, the customers could determine the coverage. For example, the policies could cover these specifics:. •. A casket or urn. •. Cremation. •. Embalming (not legally required unless there will be a public viewing). •. Burial vault or grave liner. •. Grave marker. •. Hearse and other funeral vehicles. •. Flowers. •. Digging and filling the grave. •. The burial plot. In most cases, you must purchase a burial policy in one lump-sum payment. Some policies let you pay your premiums over three, five or 10 years. Payment plans also depend on what options you include in the policy.. If you buy a single-premium policy (and pay one lump sum at the time of application), you immediately have coverage for the full death benefit. People who have a serious health problem may receive a policy with a "graded death benefit," which means the coverage amount increases over time. For example, for a three-payment policy, the death benefit might be 50 percent of the face amount in the first year and 100 percent thereafter. For longer pay plans, say five or 10 years, the. 13.

(23) death benefit is 30 percent of the face amount in the first year, 70 percent in the second year, and 100 percent thereafter.. If you are over 70 and shopping for a funeral policy, companies might offer you only the single-premium option. That’s because the chances are greater you won’t live long enough to pay premiums spread out over several years. Most pre-need companies will let you buy time-pay plans up to age 70 or 75.. According to the information of SHIBA (Senior Health Insurance Benefits Assistance), they gave funeral insurance a good definition and mentioned about traits of funeral insurance. It said, funeral insurance, a form of life insurance that covers funeral expenses and is sold by funeral homes and insurance agents, usually with the following traits:. •. It's sold to people concerned about the expenses of their death for surviving loved ones.. •. Many of those who buy funeral insurance have health conditions that make other life insurance unavailable to them.. •. It may be sold by funeral homes as a "pre-need" funeral plan.. •. It's often sold as a "guaranteed issue" policy, which means it's available to anyone who wants to pay for it.. •. Applicants for funeral insurance don't need to be in good health as they do for other types of life insurance.. 14.

(24) •. The premiums are generally higher than for an equal amount of other types of life insurance.. •. The death benefit is usually smaller than for other types of life insurance. 15.

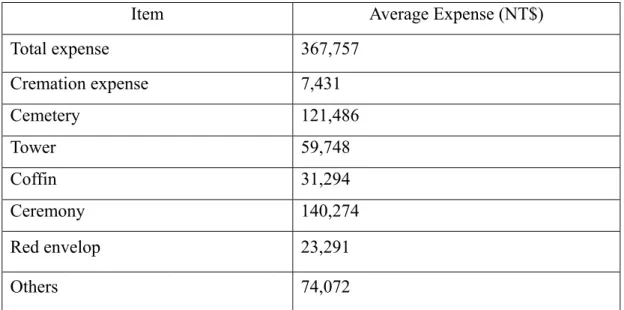

(25) The development of Taiwan “Pre-need Funeral Arrangements". 2.3. The pre-need funeral arrangement concept was introduced to the Taiwan market in 1993. Before that, most funeral homes provide funeral or cemetery service to immediate market. Even though, they also have few pre-planning programs, most of them are selling cemeteries. Although pre-need funeral arrangement was introduced in the Taiwan market in 1993, it has not been popular until these two years. Why it is more popular now? It has some certain social background. This section will probe into more details about Taiwan funeral service market development.. 2.3.1. The aging population, low birth rate. The aging population seems to be a trend in nowadays. According to the statistic of Executive Yuan in 2003, the percentage of people over age 65 is increasing from 8.3% (1998) to 9.2% (2003). The Development of Economic Association even predicted that this number will reach to 21.6% in 2030. This information means that Taiwan is stepping into a population aging society. The rest home issue, long term care issue and funeral arrangement and any issues related to this growing number of. 16.

(26) aging people will be highly concerned by the government, and the public. More and more people agree they should prepare for their funeral arrangement and life planning when they are young. On the other hand, most families in Taiwan have only one child. Some people even think they just want to get married, not having a baby. According to the statistic of Taiwan birth rate from 1980 to 2003, we found that the birth rate in Taiwan has been dramatically declined from 2.3% to 1.06%. This kind of phenomenon indicates that people have to manage their future life well instead of relying upon their children. Figure 2.1 display the percentage of people over age 65 in Taiwan.. Figure 2.1: Percentage of people over age 65 in Taiwan. 9.40% 9.20% 9.00% 8.80% 8.60% 8.40% 8.20% 8.00% 7.80%. 9.20%. 8.60% 8.30%. 1998. 1999. 2000. 2001. 2002. 2003. 2004. year. Source: Directorate-General of Budget, Accounting and Statistics, Executive Yuan (2003). 17.

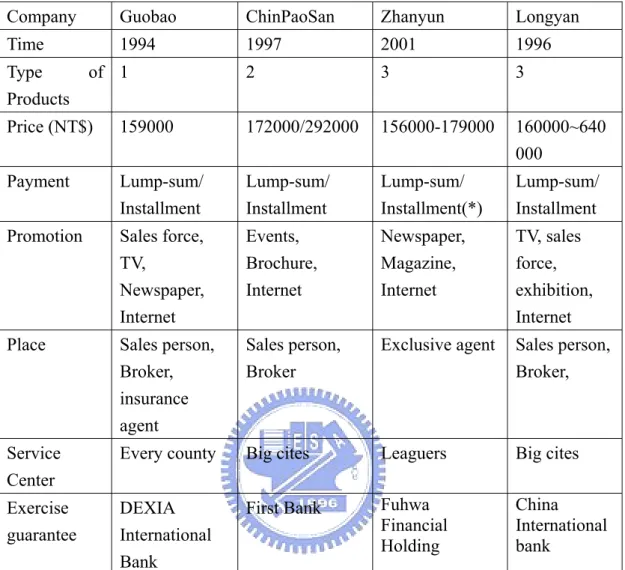

(27) 2.3.2. The expenses of Taiwan Funeral service industry According to the statistic of social department of Taiwan Province (1997), the. average total expense of funeral per person is NT$ 367,757. (Table 2.1) Most of the money spent on the funeral ceremony (NT$ 140,274), the second is cemetery (NT$ 121,486). The details are shown on Table 2.1. If the inflation rate is 2% every year, the total funeral expenses in 2010 would be NT$ 475,733. In 2050, this number would be NT$ 1,050,437. (Table 2.2) That means if you don’t prepare your funeral arrangement now, you might have to pay over one million NT dollar after 50 years. These information also show how important is the pre-need funeral arrangement and the coming trend of pre-planning concept.. Table 2.1 Breakdown of Taiwan funeral service expense Item. Average Expense (NT$). Total expense. 367,757. Cremation expense. 7,431. Cemetery. 121,486. Tower. 59,748. Coffin. 31,294. Ceremony. 140,274. Red envelop. 23,291. Others. 74,072. Source: Social department of Taiwan Province (1997). 18.

(28) Table 2.2 Prediction of funeral expenses growth by 2% inflation rate per year year. 1997. 2010. 2030. 2050. funeral expense(NT$). 367,757. 475,733. 706,914. 1,050,437. 2.3.3. How big is this market? According to the statistic of Ministry of Interior in 2003, we found out that there. are 128,357 people died in 2002. If the total funeral expenses per person in 2002 are around NT$ 400,000 (calculated by the same base as Table2.2), the immediate market volume in Taiwan would over NT$ 51.3 billions per year. Therefore, we can use the same method to predict the pre-need market. If we assume people over age 65 are the target market, the people over age 65 in 2003 are around 2 million in 2003, then the total market volume of the pre-need market would over NT$740 billions. Moreover, the overall potential market is greater than the target market, because not only the target market will buy this service. Many people would be very surprised at the above figure. If the population aging and inflation raise problem get worse, more people will pre-plan their funeral arrangement and retirement life earlier than ever. The pre-need market would be blooming up in the future.. 19.

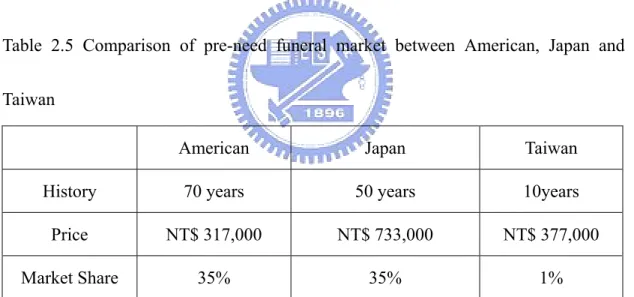

(29) 2.3.4. The development of Taiwan “Pre-need Funeral Arrangements". Before 1993, most funeral homes provide funeral service to immediate market. After they finished their service, they charge money for customers. From 1989~1994, some funeral homes think about exploring the potential market and new business opportunities. They start to sell pre-need funeral tower or cemetery for customers who plan for future demand, so that they can earn more money and get more prospects for future business. Gradually, they expand their service including pre-need funeral arrangement. (Zi qiang, Li, 2002). Pre-need funeral arrangement was introduced to Taiwan in 1993. Most of the products concept is learned from U.S by the funeral homes. The product content and business model has some different characteristics in order to fit into Taiwan’s consumer behavior and culture. Table 2.3 displays 4 main products in Taiwan market. The prices of these four products only focus on the funeral service, excluding cemeteries and towers. If they want to buy a cemetery or tower also, they have to pay additional expenses.. 20.

(30) Table 2.3 Pre-need funeral arrangements in Taiwan Company. Guobao. ChinPaoSan. Zhanyun. Longyan. Time. 1994. 1997. 2001. 1996. 2. 3. 3. Type Products. of 1. Price (NT$). 159000. 172000/292000. 156000-179000. 160000~640 000. Payment. Lump-sum/ Installment. Lump-sum/ Installment. Lump-sum/ Installment(*). Lump-sum/ Installment. Promotion. Sales force, TV, Newspaper, Internet. Events, Brochure, Internet. Newspaper, Magazine, Internet. TV, sales force, exhibition, Internet. Place. Sales person, Broker, insurance agent. Sales person, Broker. Exclusive agent. Sales person, Broker,. Service Center. Every county. Big cites. Leaguers. Big cites. Exercise guarantee. DEXIA International Bank. First Bank. Fuhwa Financial Holding. China International bank. More people are known about pre-need funeral arrangement through TV commercials, newspaper and Internet, but many people still don’t know this product well. The research did a comparison between traditional funeral service and pre-need funeral arrangement to help readers to understand the differences between these two different products.. 21.

(31) 1. Product contents Usually people avoid talking about death, they know little about funeral arrangement. When they have to deal with their family member’s funeral, it is really a hard time to them. They took everything that funeral homes proposed and didn’t know if it is necessary to do. The product contents in this industry are not transparent, and suitable for customers. Pre-need funeral arrangements disclose its product contents and services very clearly, customers can know what they buy when they are still alive. All of the service contents have to be agreed by the mutual parties and signed in a contract. 2. Price As customers know less about funeral arrangement, they also have no idea about funeral expenses. They might pay more to the funeral expenses and waste a lot of money. Pre-need funeral arrangement is pre-planed by customer; customer can know the price when they buy this service. Specially, this price will be fixed from the time customer buy the service. Therefore, compare to the traditional funeral product, pre-need funeral arrangement considers the inflation issue for customers. 3. Funeral expenses will cause a financial problem to a family. 22.

(32) Funeral expense is one of the most expenditure of a family. In a lower income family, funeral expenses will put the family into a worse financial situation if they can not pay but they have to. Compare to the traditional way, the pre-need arrangement usually pay a single amount or installment, so when family encounter this situation, their financial problem will become smaller or even zero.. 4. Follow the deceased’s last will Traditional funeral arrangement can not follow the deceased’s last will, usually the family member make the decision for funeral arrangement. The pre-need funeral arrangement is arranged according to his wish before the deceased die, so it can respect the deceased’ last will.. Table 2.4 Comparison between traditional funeral service and pre-need funeral service Traditional funeral service. Pre-need funeral arrangement. Product Content. Not transparent. Transparent. Price. No standard price. Standard price(fixed). Yes. Lower financial problems. No. Yes. Financial problems Follow the deceased’s will. 23.

(33) 2.3.5. Comparison pre-need funeral arrangement between American, Japan and Taiwan As we learn form American and Japan market experience, we found that people. in U.S are more open and willing to plan their future in advance than Taiwan. However people’s thinking change over time, many funeral homes think Taiwan’s pre-need funeral market is stepping into a booming future. This research did a comparison about pre-need funeral arrangement in American, Japan and Taiwan.. Table 2.5 Comparison of pre-need funeral market between American, Japan and Taiwan American. Japan. Taiwan. History. 70 years. 50 years. 10years. Price. NT$ 317,000. NT$ 733,000. NT$ 377,000. Market Share. 35%. 35%. 1%. Source: http://www.lungyen.com/inside4.htm. 24.

(34) 2.3.6. Insurance linked with funeral service through insurance benefits trust In Taiwan, there is no funeral insurance. One of the reasons is the insurance. companies are not specialized in funeral industry. The other reason is the MOF does not allow the insurance companies to put funeral expenses as a coverage in the insurance policy so far. The only way to link the insurance and funeral service is through insurance benefits trust from bank. Some customers can sign a trust contract with the bank to tell the bank how to deal with their properties if one day they died. These properties include insurance policy. One kind of trust is insurance benefits trust which is a contract that customer signed with the bank. After signing this contract, the bank would use the trust fund to buy insurance, when customer died, the bank would pay insurance benefits to the funeral homes. For customers, they think it is safer to pre-plan their funeral through this way than buying a pre-need contract from funeral homes. Actually, there are some disadvantages of this product. One is customers have to pay a lot of fees to bank for signing and maintain this insurance benefits trust. The other disadvantage is it is not convenient and simple enough for customers. However, this is the only way for insurance companies extending their service to funeral service so far.. 25.

(35) Though the government hasn’t opened the funeral service putting into the insurance policy, the insurance companies like Shinkong Life, Global Life, Fubon Life, and Kuo Hua Life are trying to persuade MOF to open this new coverage or business in order to provide their customers a really whole life service. At the same time, they also can expand their business to a new potential market.. 2.3.7. The profile of Taiwan Funeral and Life insurance industry According to a thesis written by Li-Ching, Tsai in 2003, she mentioned about. that there are around 27,500 funeral homes in Taiwan, and the total working people in this business is around 80,000. Most of the funeral homes are very small companies with no business management and professional training. The total capital of the biggest funeral home is less than NT$ 0.8 billion. This is the main reason that people feel hesitate to buy a pre-need funeral arrangement from these funeral homes. Compare to funeral industry, insurance companies are much bigger. There are 29 life insurance companies in Taiwan, over 260,000 people working in this industry. According to the insurance law, the minimum capital to form an insurance company is NT$ 2 billion. Every new insurance policy including coverage, price, and insurance reserve contribution has to been approved under the MOF’s requirements. Beside that, the insurance companies are required to contribute reserve into Insurance Safety Fund. 26.

(36) in order to guarantee the enforcement of the policy. The capital of the biggest insurance company in Taiwan is over NT$ 83 billions. Furthermore, most of the companies have good business management, professional training. Legal license is required by every sales agent if they want to sell insurance. According to the above information, Insurance companies tend to be more reliable and creditable than funeral homes. Therefore, people might be more willing to buy a pre-need funeral service from insurance companies than from funeral homes.. 2.3.8. Various products and tax issue make insurance more attractive Twain insurance industry has been developed for over 60 years. At the beginning,. people prefer the saving product. So the 3-6 year endowments are the most popular products. As the economic and education level advanced, people concern more about diversifying different risks during their lifetime. Nowadays, insurance products are more consumer-oriented and the government also gives a more open mild to encourage insurance company to develop good and creative insurance products. Therefore, customers could buy various insurance products on the market. For example, MOF allowed insurance company to sell investment-linked insurance products from 2001. Recently they also consider open the insurance companies to sell the foreign currency policy. This policy could enable the customers who hold foreign. 27.

(37) currency away from the exchange rate risk. Moreover, woman could also buy an insurance policy when they are pregnant. The baby could get some protection when he was still in mother’s body. To conclude, people could feel the insurance products innovation from time to time. The government is willing to approve the products that are beneficial to customers. Insurance is attractive to customers not only because of it is a risk management tool, but also it has some tax free benefits. According to Insurance Law, Article 112, the death benefits are tax free. It means if you hold an insurance policy, when you died, the total insurance benefits are exempt from inheritance tax. This is a very good selling point; hence many people would buy insurance as an asset allocation tool.. 28.

(38) 2.4. Customer Relationship Management. Every business recognizes that retaining customers is the top priority for long term business opportunities. Without customers, there is no business. The phrase of “Customer Relationship Management” has been very hot in these recent years. Many businesses recognize that the way of marketing has been changed from market to millions to market to one. Personalized customer communications and special preferences acknowledge that keep a long term relationship between a company and each of their customers. These relationships are the backbone of a profitable business.. 2.4.1. The definition of CRM. 1. Jeffery Peel (2002): Customer relationship management (CRM) is about understanding the nature of the exchange between customer and supplier and managing it appropriately. The exchange contains not only monetary consideration between supplier and customer but also communication. The challenge to all supplier organizations is to optimize communication between parties to insure profitable long-term relationships.. 29.

(39) 2. Meta Group: CRM (customer relationship management)-the automation of horizontally integrated business process involving “front-office” customer touch-points – sales (contact management, product configuration), marketing (campaign management, marketing), and customer service (call-center, field service) –via multiple, interaction). The CRM application architecture must combine both operational (transaction-oriented business process management) technologies as well as analytical (data mart-centered business performance management) technologies. 3. Duane E. Sharp (2003): CRM- A companywide, ongoing process whereby customer information is intelligently used to service customers more efficiently, thus optimizing customer satisfaction and company profits.. 2.4.2. The technology of CRM applied to insurance industry Many insurance companies especially a subsidiary in financial holding group are. benefit from CRM related technologies. These benefits begin with the development and implementation of a data warehouse, data management systems, data mining and business analysis software. Insurance industry unlike the other business, they have a special relationship with their customers. Insurance products are variable and have to meet with customers. 30.

(40) need during lifetime. Therefore, how to maintain a long term relationship with their customers is very important. More and more insurance companies now apply CRM technologies to help them to run marketing campaigns, choose right market segmentation, analyze customers’ information, provide personalized service and develop new products. OLAP (Jeffery Peel) tools are sometimes referred to as decision support tools and are used in insurance companies that allow users or applications to make decisions in real time. Online Analytical Processing technology can help the insurer to look at data from different perspectives and have the ability to examine summarized and detailed data. When an insurance company is developing a new product and campaign for their customers, OLAP technology helps them define the target market and evaluate the performance of the campaign in a short time.. Nowadays, many companies they provide special CRM service for financial industry to run a good customer relationship management. The insurance companies would need this kind of technology to help them dealing with the customer relationship as their customer base become huge. Therefore, some insurance companies in Taiwan they spent a lot of money to implement CRM system. They even buy a lot of training programs to train their employees to use these systems. The only goal is to make more profit in this competitive environment. 31.

(41) 2.5. Marketing Mix. Winning companies will be those who can meet customers’ need economically, conveniently and with efficient communication. Marketing mix is a set of marketing tools that the firm uses to pursue its marketing objectives in the target market. (Philip Kotler). Marketing mix includes four P components, product, price, promotion and place, which is just about everything you need to cover when you sell something. But basically, the ‘mix’ comes down to you offering what your customers really need and want, at just the right price, at a time and place they find most convenient and having heard about you in a way that encourages them to buy. 1. Product: all the product or service characteristics aimed at the target market 2. Price: the real cost to the customer including costs more than solely money. 3. Place: everywhere or every way the product or service is made available. 4. Promotion: all the marketing methods used to communicate with the target customers. Before launching a new product or service, you have to make a good marketing strategy. Figure 2.2 shows a marketing-Mix strategy that company preparing an offering mix of products, services and prices, and utilizing a promotion mix of sales. 32.

(42) promotion, advertising sales force, public relations, direct mail, telemarketing and Internet to reach the trade channels and the target customers.. Figure 2.2 Marketing-Mix Strategies Promotion mix. Offering mix. Compa ny. Product s Service s Prices. Sales promotion. Advertising Sales force. Distribution channels. Target Customers. Public relations. Direct mail, Telemarketi ng, and Internet. Source: Philip Kotler, Marketing Management(2000). When we talk about marketing mix (4Ps), they represent the sellers’ view of marketing tools available for influencing buyers. From a buyer’s point of view, each marketing tool is designed to deliver a customer benefit. When customer relationship. 33.

(43) management is becoming more and more important for a company’s winning position in the market. Robert Lauterborn suggested that the sellers’ four Ps correspond to customers’ four Cs, which are more customer oriented.. Four Ps. Four Cs. Product Price Place Promotion. Customer solution Customer cost Convenience Communication. 34.

(44) Chapter 3 INSURANCE-FUNERAL BUSINESS MODEL DESIGN. After a family finished a funeral ceremony, there comes the bill of total funeral expenses. If they didn’t pre-arrange a funeral service, the whole family could face a financial problem for paying the expenses. As the funeral expenses for a family might be a huge expenditure, they might have to borrow money to pay this bill. The pre-need arrangement could lower this problem, but what if the customer bought the pre-need contract by installment and he died before paying up the installment. The family still has to face the remaining expenses that haven’t paid off. On the other hand, the pre-need funeral contract still has some problems, such as what if the funeral home goes bankrupt before the customer’s death. The customer would lose more and still keep the financial problems for his family. In order to solve this problem, this research tries to build a new business model to lower the existing problems in funeral market and providing the consumers a better service to choose.. 35.

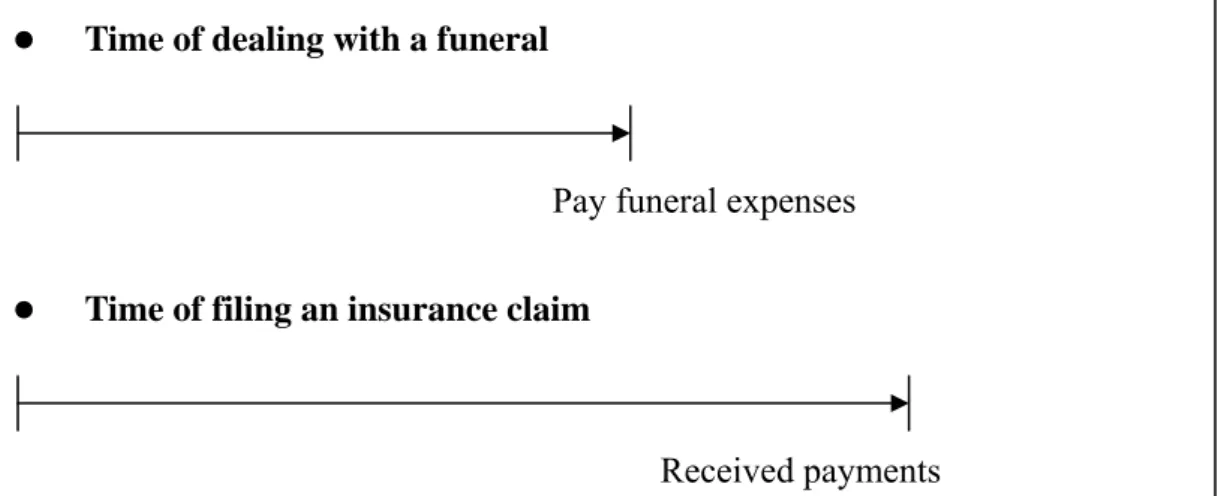

(45) 3.1 Business model design. Everyone has more than one insurance policy in Taiwan. According to the statistics of Life Insurance Association of the Republic of China in 2002, the insuring rate in 2002 is 143.7%. The insurances help people to diversify risks and take care of their family when accident happens. When people deal with the funeral matter, usually they will file an insurance claim at or after finishing the funeral matters. We know insurance can help a family to go on their life. But the insurance payment usually comes after the funeral expenses bill. So most of the time, the family has to pay the funeral expenses first, and then get the insurance indemnity. Figure 3.1 shows a time line of dealing a funeral and filing an insurance claim. Figure 3.1 Time line of dealing a funeral and insurance claim z. Time of dealing with a funeral. Pay funeral expenses z. Time of filing an insurance claim. Received payments. 36.

(46) Therefore, if customers could use the insurance benefits to pay the funeral bills, it might be easier and more convenient to the customers. This research tries to build an insurance-funeral model to combine the funeral and insurance service together in order to give the customer an easier and safer way to pre-plan their future needs. The goal of this business model design not only provides an easier and safer financial service, but also fulfills the goal of taking care of people a whole lifetime. Besides that, companies could find a new potential business opportunity for making profits.. 37.

(47) 3.2 Hypothesis. As there is no related research about insurance covering funeral service in Taiwan, in order to evaluate in a more specific way, this research did some hypotheses from an insurance company’s point of view to design this new model. The following are hypotheses of 「Insurance-Funeral business model」.. H1:As the population is aging, birth rates are falling in Taiwan, customers are more willing to plan their pre-need demands(pre-need funeral arrangement)more than ever. H2:According to the Taiwan Insurance Law and Tax Income Act, insurance benefits to the beneficiary should be exempted. People are willing to buy insurance as one of their asset allocation tools. H3:People think it is more convenient to buy one product including two services at one time instead of buying two. H4:People are interested in a product that can not only take care of themselves but also their family. H5:Customers trust insurance companies’ credibility more than funeral homes. H6:Customers feel insurance products are more familiar than funeral products. They. 38.

(48) also believe insurance regulations are better than funeral regulations. H7:The Government encourages insurance companies to provide new and innovative insurance coverage that are beneficial to customer. H8:More insurance companies are studying funeral related insurance products. H9:Insurance companies believe providing differentiated products in venture with funeral homes will bring more business opportunities. H10:Whole life insurance is more suitable for this business model than term life insurance.. 39.

(49) 3.3 Insurance-Funeral business model structure. Insurance is a very wonderful financial tool to help people diversify many risks that they might encounter in their whole life. For the insurance products in Taiwan, they could take care of a person from his birth, education, marriage, to retirement. But when people died, the only thing insurance company can help is giving his family a check. Many young people even think about not to buy high insurance amount, because they can not use on themselves when they pass away. So this research tries to build a new business model that could extend insurance service with pre-planning funeral service. Customers could buy a really whole life financial service, and save much time to buy one product instead of two. Figure 3.2 display processes how an insurance company set up an 「Insurance-Funeral Business Model」.. 40.

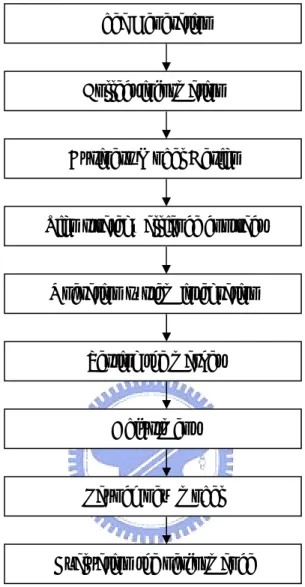

(50) Figure 3.2 Processes of building an Insurance-Funeral Business Model Idea Generation. Collect information. Business Model Design. Sign strategy alliance contract. Operation system integration. Testing the market. Adjustment. Launch new model. Evaluation the performance. 1. Idea generation: Product development department see market trend of future needs, and find out the relationship between insurance and funeral service has chances to link together and explore new market opportunity.. 41.

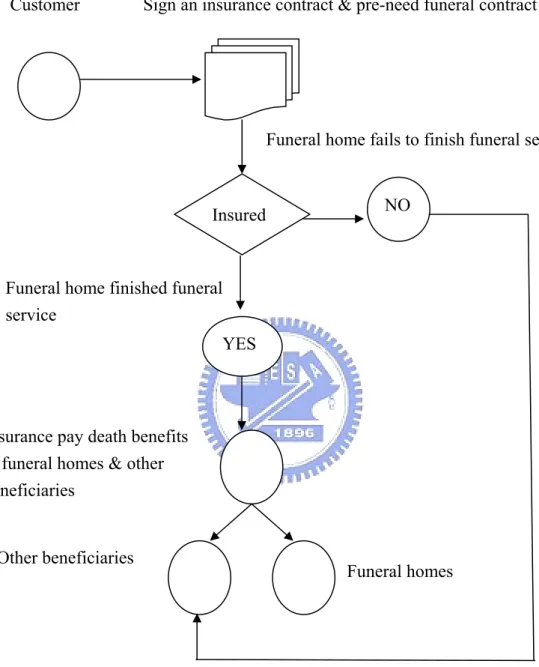

(51) 2. Collect information: Company set up a project team starting to collect any information useful for this idea, including literature review and any experience in other countries. 3. Business Model Design: This business model including funeral service into insurance product, compare to the funeral insurance in American, this model provide an insurance that could cover more customer’s needs instead of only covering funeral service expenses. How to do that? Insurance company adds pre-need funeral service into to the whole life policy. If the insured is interested in this extending service, he can designate a certain insurance amount to the funeral homes as the first beneficiary. When the inured died, insurance company will pay the funeral expenses to funeral home under funeral service finished. Figure 3.3 display whole processes of 「insurance-funeral business model」.. 42.

(52) Figure 3.3 Insurance-Funeral Business Model. Customer. Sign an insurance contract & pre-need funeral contract. Funeral home fails to finish funeral service. Insured. NO. Funeral home finished funeral service YES. Insurance pay death benefits to funeral homes & other beneficiaries. Other beneficiaries. Funeral homes. Through this new business model, the insurance company could provide an extendable and differentiated service to the customer. It combined two industries’ service into one and would be more convenient to customers. But, as the funeral. 43.

(53) industry in Taiwan is not well organized enough, there might be a chance that the funeral homes go bankrupt before the customers die. Therefore, through this model design, it could provide a certain protection to customers. 4.. Sign a strategy alliance contract: As insurance company is not specialized in funeral service, they have to alley. with funeral homes. It is very important to choose a good funeral home with good service quality. Therefore, the insurance company has to spend some time to find a good funeral home in the market. When two companies are willing to sign an alliance contract, the content of this contract is very important. The insurance company should consider the obligations and rights they might have and ask lawyers’ professional suggestions about signing this contract. 5.. Operation system integration: Computer system plays a very important role in this new model. The insurance. company has to build a new system for running this model. In order to provide the right time service, they must have a good integration with the funeral home’s system. So how to deal with the data in two different systems is a critical issue in this model design. With good system integration, the insurance company can do well business model evaluation after product launch and do good data analysis for CRM.. 44.

(54) 6.. Testing the market: When the business model completely set up, the insurance company could try to. choose a target market to test the customer’s attitude of this business model design. Testing market is a good way to know how customer’s feeling about the new financial service. Insurance company can also evaluate if there is anything needed to change of the model design. 7.. Adjust business model and marketing strategy: After testing the market, there might be something needed to adjust. The. insurance company could use this chance to adjust the model or marketing strategy. Try to solve the relate problems that happen during the test. 8.. Launch new model: After adjusting the model, how to well launch a new product is very important.. Company can plan a good launch plan, including advertising and marketing campaign. Having a good product launch could make a new product successful. 9.. Evaluate the performance: Insurance company should make a regular evaluation plan to see the. performance of new product after launch. The evaluation results could be very good references for better improvement of the product design.. 45.

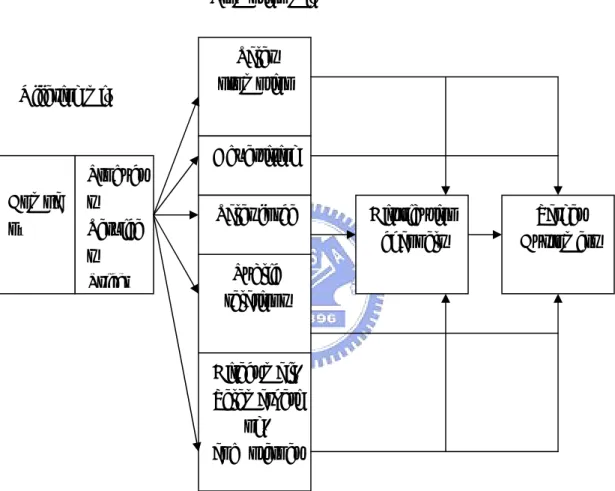

(55) 3.3.1 Protection to funeral home’s failure of execution As we know in the recent way of buying a pre-need funeral arrangement, customers have to pay all of some money ahead of they get the service. What if the funeral home goes bankrupt before customer’s death, customer might get nothing back but lose all the money they paid. In order to solve this problem, the 「Insurance-Funeral Business model」provide a protection mechanism for customers. If the customers do not get the funeral service under some unexpected reason like just mentioned above, the insurance company will pay the death benefit to other beneficiaries that insured designated before instead of paying to the funeral home. This is kind of protection of customers’ money. In the following section, this research will use 4Ps Vs 4Cs strategy to explain more detail about “Insurance-Funeral Business Model”.. 46.

(56) 3.4 4Ps & 4Cs of “Insurance-Funeral Business Model”. In chapter 2, the literature review mentioned about the relationship between 4Ps & 4Cs. 4Ps are the marketing mix from seller’s point of view, they are key elements when a company sets up a marketing strategy. Kotler suggested that marketer should concern more about customer-oriented perspective. 4Cs nowadays are key factors when a company wants to keep a customer for long term relationship. In this section, the research will mention about「Insurance-Funeral Business Model」 from 4Ps(seller’s point of view)to 4Cs(customer’s point of view).. 3.4.1 Marketing Mix of “Insurance-Funeral Business Model” 4Ps refer to product, price, promotion and place. Each P has some components to explain this business model clearly. The particular marketing variables under each P are shown in Figure 3.4.. 47.

(57) Figure 3.4 Marketing Mix. Marketing Mix. Product Design Service Brand. Price. Promotion. Place. List price Payment period. Sales promotion Advertising Direct Marketing Internet. Channels Coverage Locations Transport. Source: Philip Kotler, Marketing Management(2000). In this sector, the research would like to talk about the marketing mix of this model after finishing the basic model design. This is very important for company before they launch a product. The reader will be clear about this model after reading this sector.. 1. Product (1). Design Product design of this model contains a whole life insurance covers with a pre-need funeral service. Why choose whole life insurance? As this. 48.

(58) model’s object is to serve the customers with an extendable funeral service, whole life insurance is the best choice that it covers a person’s whole life upon to the insured’s death. Compare to whole life insurance, term life is not suitable because customer might still alive when the policy expires. The extendable funeral service will be provided by the funeral homes. Because they are more expertise of doing this business than insurance companies, it is better for insurance company and funeral home take good care of their own expertise. Under this model, how to sign a complete alliance contract between funeral home and insurance company is quite important to keep good service quality to the customers. When an insurance company decides to provide new financial service, they have to be care of choosing the funeral homes size, financial ability and service quality. They also have to well regulate the mutual obligation and responsibility.. (2). Service In the past, customer has to buy insurance and funeral service separately. Through this new business model, insurance company provides an integrated service which combines insurance and funeral service. 49.

(59) together to customer and increases its business opportunity through this new differentiated financial service. Moreover, compare to the funeral insurance in U.S, this model not only covers the funeral expenses, but also whole life risk. This model uses whole life insurance as the main structure, funeral expenses would only be paid when insured died. The sum insured can cover the family’s future expenditure and funeral expenses. Therefore, if the inured wants to leave some money to his family, he only has to buy one policy instead of buying funeral insurance and whole life insurance separately.. (3). Brand Brand image is very important for this new business model. As the whole life insurance and pre-need funeral service are intangible service that customers buy for future needs, how to let the customers trust your service is more important than tangible commodities. Good brand image will be a competitive advantage for a new product launch. If an insurance company is already with good reputation and ally with a good funeral home, the possibility of success would be higher than a nameless company.. 50.

(60) 2. Price (1). List price In this new business model, the funeral expense will be paid by insurance benefits. So the total money, customer has to pay first is only insurance premium. But under the existing business model, if customer wants these two services, they have to pay for both of these services. Therefore, this new business model will be more attractive to the customers. Insurance company will get more business opportunity from providing this new service. As this pre-need funeral service now included into insurance policy, funeral homes could save their marketing cost for promotion. Insurance company can ask the funeral home to share some additional operation and marketing cost of insurance company. Then, insurance company could set an attractive price to customer and make their product more competitive. As the mortality rate and interest rate are the same between the insurance companies, the average level whole life insurance premium per year for a 30 year old woman, insurance amount is NT$ 500,000 with a 20 year installment is around NT$ 12,000. With the previous example, if this woman died in the second year after insured, she. 51.

(61) only paid NT$ 24,000 for buying this product. Compare to paying N$ 500,000 funeral expenses, this is a very attractive price and product for customers to buy. (2). Payment period This new business model provides 6 payment period, 6, 10, 15, 20, 25, and 30 year installment. The variable payment period could satisfy different customers with different needs or ability of payment. The more service choices the insurance company can provide, the more attraction of the product to the customers.. 3. Promotion (1) Sales promotion The primary objective of sales promotions is to predict and modify customer purchasing behavior, most often to improve sales. Insurance company could give the customer some premium discount if they buy a new insurance policy with pre-need arrangement service. As the funeral homes can also get potential customers from this new business model, they can also provide some peripheral services with some discounts to attract people buy this product. The other way to make a good sales volume is giving some incentive. 52.

(62) for sales force to encourage them to sell more. Unlike other product, this is an intangible product; to give the sales force a good incentive when they reach the target sales volume definitely will help the sale figure.. (2) Advertising Advertising is a good and fast way to let people know your product in a very short time. As this is a new, fresh financial service to the customer, good advertising will help public to be aware of your service, and indirectly build your company brand image into the public’s mind. How efficiently to advertise your product at the right time, right place is very important. For this new business model, the target market would be people over 45 years old. As they are the people who have ability to buy and stronger motivation to prepare their funeral, choose the financial, health and news channels at peak time in the evening would have a better outcome for this product’s advertising. (3) Direct Marketing Direct marketing is a very common promotion way today; it includes distributing mail, brochure, product sample, promotion leaflet directly into the hands of the target consumers in order to achieve maximum promotion result. In order to achieve a successive marketing goal for this new business model, 53.

(63) direct marketing is also a good way of promotion. (4)Internet Internet is now become a must tool in people’s life. It is efficient, cheap and fast way of promotion. Insurance company could set up a website for this new financial service, and use viral marketing to spread this news to the Internet. If people are interested to know more, they could leave their contact information for further information. Insurance company could get some information from the message and try to close a deal by contacting the potential customers. 4.. Place If a company wants to have an advantageous position in the market, good product and channel are two important factors. There is a good saying says, “If you owns the channels, you win the market.” An insurance company can sell this new financial service by not only their sales force, but also other channels that can sell insurance. The funeral homes could also be a very good channel to sell this product because of their expertise of funeral service. In Taiwan, besides sales agent of the insurance company, insurance broker and banks are allowed to sell insurance products. If the insurance company is one of the subsidiaries of a financial holding group, all companies in the whole financial holding group are. 54.

(64) allowed to cross-sell insurance products too. Therefore, choose the right channels, more channels to sell your products does good for promoting this business model.. 3.4.2 4Cs of “Insurance-Funeral Business Model” 4Cs represents customer solution, customer cost, convenience, communication. This concept is from customer’s point of view to the product. It is more concerned by many companies in order to get a long term business relationship.. 1.. Customer solution The design of Insurance-Funeral Business Model helps the customers to diversify their risk. The extendable funeral service helps a family paying the funeral expenses through insurance death payments. This model helps customers to reduce their financial problems and comfort their mind when unexpected things happen.. 2.. Customer cost If a 30 year old female customer buys a 20 year installment life insurance which insurance amount is NT$400,000. The insurance premium she has to pay NT$7,200 per year. If she dies after 3 years, the insurance company would pay. 55.

(65) NT$ 400,000 to her funeral expenses, but actually she only paid NT$ 21,600 to get this service. This will help her and her family to save a lot of money. 3.. Convenience It is more convenient to buy a one-stop shopping service than two services. This model including two services into one financial service concept could save customers a lot of searching time and cost.. 4.. Communication Insurance-Funeral Business Model is a life time service. Insurance company and funeral home have a lifetime to do customer relationship management. They also provide some services like policy loan, birthday greeting and coverage adjustment service for customers. These are ways to communicate with customers. Beside that, they also have service centers for customers to communicate with insurance company.. With a well planned marketing strategy would help this business model having more chance to success. After having a good start, making new public to become your customers, how to maintain them is also quite important. In next sector, the research would probe how insurance company through this model to begin their long term customer relationship management.. 56.

(66) 3.5 How does “Insurance-Funeral Business Model” help to maintain Long term CRM?. Insurance is a kind of financial services that is never written in stone. People’s needs change over the course of their whole life. Insurance is a special financial tool to help people to diversify their risk during their whole life. Every company now is eager to maintain a long term customer relationship with their customers. But not all kinds of products are easy and suitable for maintaining a long term customer relationship. Insurance is an exception.. There are many kinds of insurances which are designed to diversify many risks during a person’s life. Insurance services can meet different people’s need. People can have a personalized insurance package correspondent with their own demand. People could choose an insurance policy with different kinds of riders to make the whole package complete to indemnify loss when unpredictable situation happens. The most important thing is, insurance is a long term product and can be adjustable with human life cycle. Therefore, it is a very good product for maintaining long term customer relationship. Nowadays, customer relationship has been a very important issue for. 57.

(67) insurance companies. Many insurance companies measure customer satisfaction on a regular basis to get an idea of how well the company is doing at maintaining these important assets~ their customers.(Tom Moormann, 2004). Under “Insurance-Funeral Business Model” design, the research would try to explore how this new business model suitable to maintain long term customer relationship.. Insurance is like a big umbrella that could cove many risks during a person’s life. From a baby’s birth, go to school, start to work, get married to retirement, you can find variable insurance products that cover a person life time risk planning. Under “Insurance-Funeral Business Model”, the research assumed a person has to buy a whole life policy. After he became one of the insurance company’s customers, insurance company can use a lot of CRM technology to analyze this customer’s future needs and provide the best service to the customer. In the meanwhile, insurance company can earn more business opportunities from their existing customers. Figure 3.4 display how new business model help to maintain long term customer relationship management.. 58.

數據

+7

相關文件

The main goal of this research is to identify the characteristics of hyperkalemia ECG by studying the effects of potassium concentrations in blood on the

Therefore, this research paper tries to apply the perspective of knowledge sharing to construct the application model for the decision making method in order to share the

The purpose of this research lies in building the virtual reality learning system for surveying practice of digital terrain model (DTM) based on triangular

Lee's (2007) "Study of Long Stay Destination Evaluation Indicators for Japanese Pensioner Tourists in Taiwan" as research dimension, to analyze the grading

In order to serve the fore-mentioned purpose, this research is based on a related questionnaire that extracts 525 high school students as the object for the study, and carries out

Lee's (2007) "Study of Long Stay Destination Evaluation Indicators for Japanese Pensioner Tourists in Taiwan" as research dimension, to analyze the grading criteria for

The purpose of this research is to study the cross-strait visitor’s tourist experience.With the research background and motives stated as above, the objectives of this research

This research takes the voluntary soldiers in each air base for example to know how the working attitude affects the performance in their work.. Furthermore, this research