Declaration Effect, Stock Returns and Earnings Management:

A Study of Private Placement in Taiwan

†Ruey-Dang Changa, Wen-Hua Shenb,*, Yi-Hsiang Huangc

a

National Chung Hsing University bNational Kaohsiung University of Applied Sciences

c

National Sun Yat-sen University

Abstract

Since its inception in 2002, the private placement system has become one of the import-ant alternatives for the listed and OTC companies in Taiwan to raise needed capitals. The pur-pose of the study is to investigate the declaration effect and one-year stock returns of the pri-vate placement companies and to examine if the companies would engage in earnings man-agement before undertaking the private placement. Empirical results indicate that for the com-panies that decided to undertake the private placement, there was no significant declaration effect; the cumulative abnormal returns after one year of the private placement have been sig-nificantly positive. In addition, the study also found that the more insiders and institutional in-vestors participated in the private placement, the higher the long-term cumulative abnormal returns and company size and market-to-book ratio are both negatively related to long-term cumulative abnormal returns. However, there is no evidence that the companies had conduc-ted earnings management to influence specific investors to participate in the private plac-ement.

Keywords: Private placement, Declaration effect, Stock returns, Earnings management

1. Introduction

Private placement has been applied in America for years, but it was implemented in Ta-iwan since the amendment of the Securities and Exchange Law in 2002. So far, more than 100 listed and OTC companies had employed private placement for capital recruitment. Narrow-ing down to private equity offerNarrow-ings, 3 listed and OTC companies in 2002, 14 in 2003, 18 in 2004, and 25 in 2005 applied equity private placements. And from January to June in 2006, total proceeds collected by all publicly listed and OTC companies amounted to 215.138 bil-lion NT. Among them, public offerings accounted for 149.736 bilbil-lion NT (69.6%), while pri-vate offering accounted for 65.402 billion NT (30.4%). It shows that more and more compan-ies have used the channel of private placement to acquire capital for operation.

Based on the Article 7 of the Securities and Exchange Law, the term "public offer" as used in this Act means the act of offering securities to the general public by the promoters pri-or to the incpri-orppri-oration of the company, pri-or by the issuing company pripri-or to the issuance of the † We appreciate the comments from two anonymous reviewers and participants of the 2007 TAA annual meeting. * Corresponding author. Email: [email protected]

said securities. The term "private placement" as used in this Act means the act of offering securities to specific persons pursuant to paragraphs 1 and 2 of Article 43-6 by a company. Therefore, private placement indicates the capital collection of securities from the specific in-vestors, while public offering is exclusive to the non-specific investors. The primary differ-ence between private and public offering is that the placee of private placement is restricted to some specific investors, who should be searched and contacted by the firms. Because the sys-tem of private placement in Taiwan didn't set out until 2002, there has been comparatively lit-tle research relating to the announcement effect of it. Although Hsu (2003) conducted a study on the private placed firms, there were only thirteen observations in her study. Moreover, the study was conducted in the beginning period of private placement. As private placements have prevailed gradually, whether the result of the above study could be generalized is still a question. By contrast, there is already large amount of literature in other countries discussing the declaration effect of private placement on firms' stock price. For example, Wruck (1989) and Hertzel et al. (2002) discover that the average abnormal return from day -3 to day 0 (an-nouncement date) is significantly positive, showing that private placement delivers a positive declaration effect on firms' stock price. Since the focus of private placement conducted by the listed and OTC firms in Taiwan is common stock, this study also likes to make analysis upon the listed and OTC firms placing common stock privately to see if the same positive declar-ation effect exists in Taiwan.

According to the report by SEC (1971), listed firms mostly privately placed at a dis-count. On average, the discount approximates to 30%. Other literature also indicates that in order to complete private placement, firms will provide the participating investors with a cer-tain discount to compensate them for the problem of cash liquidity (Wruck, 1989; Silber, 1991). However, why are investors willing to accept private equity offerings? Based on the perspective of self-interests, the reason for investors to participate in private placement may arise from the larger discounts offered by the firms. Other than that, investors may identify with the firms' future operating projects, believing that firms will be able to have better opera-tin g performances after receiving private placed funds. They wish to acquire more investment benefits through increasing stock prices. Hertzel et. al. (2002), however, find that firms issuing privately have negative abnormal return of stock price three years after announcem-ent, a n indication that investors are often over-optimistic about the future performance of pri-vate placed firms. In order to explore whether investors participating in pripri-vate placement in Taiwan have the same over-optimistic inclination, this study adopts the listed and OTC firms placing privately as samples to examine whether long-term stock price outperforms after com-pletion of private placement.

Since its inception, more and more listed and OTC firms have conducted private

plac-ement1. Some firms have flourished again because of the infusion of private capital. However,

some firms are hollowed out due to private placement. Therefore, adoption of private plac-ement could be double-faced. Although it could help acquire capital, technique, knowledge, and human resources, it may introduce the evil and put the firm in a great danger. Since the size, market comments, and investors participating in placement may influence firms' stock performance after private placement, this study would like to examine whether the declaration effect and post-placement stock performance will be affected by the variables of firms' size,

1.Take the cases in 2005 as examples, the noted firms placing privately include Power Quotient International,

market-to-book ratio, percentage of insider's participation, and institutional investors' particip-ation. Results could be used by investors to make decision when participating private plac-ement.

Finally, private placement could help those firms with poorer reputation and lower stock price out of the distress, in which they can hardly obtain capital through public offerings, and firms placing privately have the opportunity to collect money with less cost, in a shorter time, and in an easier way. However, information asymmetry exists between mangers and investors. In order to obtain funds through private placement, managers are possibly manipulating earn-ings to window-dress financial statements as to attract funds infusion from specific investors. What's more, earnings management has the "reversing effect" which may negatively affect earnings one year following the private placement. Therefore, this study also examines whether firms conduct earnings management one year before and after, and in the year of pri-vate placement.

The sample firms are publicly listed firms (including OTC) on the Taiwan Stock Ex-change that placed privately from 2002 to 2006 and have data available in the Taiwan econ-omic Journal (TEJ hereafter). Empirical results indicate no significant declaration effect, but stock return one year after placement was significantly positive. Both results are inconsistent with literature in the US. The reason might be that comparatively larger proportion of private placement in Taiwan was participated by insiders. Moreover, this study also finds that when firm size is smaller (bigger) or market-to-book ratio is lower (higher), long-term cumulative average abnormal return after announcement is higher (lower). When higher (lower) propor-tion of insiders or institupropor-tional investors participates in the placement, long-term cumulative average abnormal return after announcement is higher (lower). However, this study doesn't find that managers solicit specific investors to participate in private placement through con-ducting earnings management.

The remainder of the paper contains four sections. Section II reviews relevant literature and develops hypotheses to be tested in the study. Section III discusses the method employed in examining the research questions. Section IV presents results of the study. Section V con-cludes the paper and discusses implications and limitations of the study.

2. Literature Review and Hypothesis Development

2.1 Declaration Effect of Private Placement

Myers and Majluf (1984) demonstrate that equity issues convey management's belief that the firm is overvalued. They indicate that managers of undervalued firms with profitable in-vestment opportunities, but lacking financial slack, will choose not to make inin-vestment. Therefore, they can prevent new shareholders from sharing benefits of existing shareholders when they do not issue new stocks. By not issuing, managers are choosing to forego the in-vestment opportunities. Under the same notion, because mangers possess more information, they will choose to issue equity publicly to collect more capital if they believe the firm is overvalued. Therefore, if a firm chooses public offerings, it delivers a message to investors that the manager believes firm's value is overestimate. Then stock price will be adjusted by market mechanism later, which may lead to the result of stock price decrease. Hertzel and Smith (1993) suggest that private placement can solve the underinvestment problem, which results from that undervalued firms are worried about the initial stockholders' benefits being reduced. Therefore, the fact that managers choose private equity offerings and investors are willing to invest implies that the firm's stock price is undervalued. Spiess and Affleck-Graves

(1995) and Loughran and Ritter (1997) find that when firms announce seasoned equity offer-ing (SEO), they may encounter negative stock return duroffer-ing the announcement period and their five-year stock return is also significantly lower than that of the non-SEO firms. Hertzel and Smith (1993) find out that the cumulative abnormal return (from day -3 to day 0 (announ-cement day)) of the firms implementing private pla(announ-cement is 1.72%, and cumulative abnormal return from day -29 to day 10 approximates to 9%. Under the circumstance of information as-ymmetry, if the firms prefer private equity offerings to public equity offerings and the inves-tors are willing to make private equity investment, both launch a signal that the stock prices of those firms are undervalued. Wruck (1989) finds that 4.5% of average abnormal return exists after announcement of private placement, which is significantly different from the research re-sult of the announcement effect of SEO (negative 3% of average abnormal return). Aside from the information asymmetry hypothesis, Wruck (1989) suggests that the change of ownership structure, such as the increase of blockholders' shares, may be the reason for a positive announcement effect. When blockholders inject more funds into a specific firm's pri-vate equity offerings, the linkage in benefits with the firm will become stronger, which may induce their motivations to strengthen the degree of monitoring on the firm. Therefore, private placement may generate a positive announcement effect.

Adopting firms conducting public offerings and private offerings during 1981 to 1990 as samples, Lee and Kocher (2001) sort out five and three variables based on information as-ymmetry hypothesis and agency cost hypothesis respectively, then combine the same vari-ables. Eventually, six variables such as firm size, dividend policy, growth opportunities, over-valuation, free cash flow, and ownership fraction were used to examine the characteristics of firm equity offerings publicly and privately. The result shows that private placement firms en-tail smaller size, higher growth opportunities, and limited financial slack, which shows that information asymmetry underlies when private placement firms collect funds outward. Also, firms with different characteristics may collect funds with different ways. Wruck (1989) and Hertzel and Smith (1993) suggest that when firms announce private placement, the public will deem the information positive. Kato and Schallheim (1993) find that a positive announcement effect also exists in Japanese firms placing privately, and the average abnormal return can re-ach to 5%. With a sample of 56 private placement firms in Singapore during 1988 to 1996, Ruth et al. (2002) find that the cumulative average abnormal return from day -20 to day 1 is 6.27%, indicating a positive announcement effect in private placement. Hsu (2003) used 13 private placement firms in Taiwan as a sample and also found a positive announcement effect. Abnormal return on the announcement day is 2.2088%, and 4.5272% of average abnormal re-turn is shown on the day 1.

2.2 Long-term Stock Performance of Private Placement

Hertzel et al. (2002) examine stock return of American firms placing privately with method of buy-and-hold abnormal returns and find that three-year buy-and-hold abnormal re-turn is merely 0.21%, which is far lower than firms with public offerings. Furthermore, the stock performance doesn't improve after private placement, which shows that participating in-vestors tend to be over-optimistic about corporate operation. Krishnamurthy et al. (2005) use American firms as samples and discover a positive announcement effect and negative long term abnormal returns in firms placing privately. This result is consistent with that by Hertzel et al. (2002). Krishnamurthy et al. (2005) find that although long-term stock return is not fa-vorable, an average of 20% discounts is provided during private equity offerings. Thus the

participating investors are usually able to gain a positive abnormal return, which is higher than public offerings. They also divide investors as affiliated ones (officers or directors of the firm, and relative institutions) and unaffiliated ones. As the affiliated ones possess lower in-formation cost, having clearer picture of cash flow and intrinsic value of the firms, their capi-tal injection into the firms can be regarded as assurance of firms' value and can also lessen ag-ency cost. Although they find bigger discounts are normally allowed for unaffiliated investors than affiliated ones, long-term abnormal return doesn't differ significantly in between. This also explains that although affiliated investors have lower information cost, they basically have no information advantages compared with unaffiliated investors. Furthermore, given the control of financial distress, private equity with affiliated investors will generate a positive an-nouncement effect and long-term abnormal returns. Chen et al. (2002) examine long-term stock performance of public firms placing privately in Singapore between 1988 and 1993. Their result indicates that cumulative abnormal returns will significantly decrease in two years after placement. Their study adopts four models (size-adjusted, book-to-market adju-sted, market adjuadju-sted, and industry adjusted) for cumulative abnormal returns. Except for the industry-adjusted model, the cumulative abnormal returns of three other ones are approximate 20%. After making comparison between firms placing privately and benchmark firms, the for-mer ones present lower stock performance. Firms with smaller sizes will also tend to have lower stock performance, which is consistent with the information asymmetry hypothesis. That is to say, information asymmetry will be more serious in smaller sized firms. Moreover, Chen et al. (2002) also find that firms with low book-to-market ratio will have better perform-ance in stock price. The reason may be that book-to-market ratio can be seen as a proxy for growth opportunities. Therefore, firms with lower growth opportunities are more likely to issue shares when being overvalued. Finally, Chen et al. (2002) calculated discretionary ac-cruals to examine earnings management behavior before and after private placement and found no significant results for earnings management behavior.

Hertzel et al. (2002) find the characteristics of high capital expenditure, high R&D ex-penditure, and high book value in private placed firms. Although their operating performance is not so favorable, the stock price before private placement is apparently upward, showing that investors may gauge firms' value by growth opportunities. Marciukaityte et al. (2005) take American firms from 1979 to 1996 as samples to conduct research in private placement. Among the samples, at least 37% of firms are young or still developing. Their study finds that 7% of firms were recognized as financially distressed with three standards such as cancella-tion of the dividend payment, inability to fulfill financial duty, or occurrence of other financial problems. But investors may think these firms fell into financial distress only because they were under the product development stage instead of in any financial problems. That is to say, investors tended to be over-optimistic about private placed firms' perspective. Marciukaityte et al. (2005) adopted the prospect theory from Tversky and Kahneman (1974) and thought that investors will inject the successful experience of other firms into private placed firms once those firms possess speculative growth opportunities. And investors are inclined to be-lieve that private placed firms will achieve the growth goals established before placement. Namely, investors will predict private placed firms' performance with other firms' perform-ance. However, investors will not only over-expect firms' operating performance but also overvalue firms if over-trusting other firms' successful experience and ignoring long-term per-formance.

2.3 Hypotheses

Hertzel and Smith (1993) argue that managers are inclined to collect capital by private placement if they believe that firms are undervalued. Managers can also increase shareholding percentage through private placement participation to grab the opportunity for future benefit. Wruck (1989) argues that shareholders' participation in private placement will increase their holding shares and therefore their incentives for monitoring, which is beneficial for firms' op-eration. Because private placement is restricted to specific participants, the main investors will include insiders like managers and directors, institutional investors and financial organ-izations, natural persons, juristic persons and funds conforming to regulation by competent authorities. Those participants are all qualified for the rules rectified by the authorities con-cerned. They all have the opportunities to communicate with managers face-to-face about fir-ms' future perspectives before participation. Therefore, after serious assessment, those inves-tors think of the firms' as highly prospective and participate in placement in hope for larger benefits. The announcement of private placement not only discloses the information of firms being undervalued, but also represents the managers' confidence in firms' future and value for investment. Thus, when firms announce private placement, the market will recognize that firms are being undervalued and new capital will be helpful for firms' operation. Therefore, a positive announcement effect will arise. Accordingly, hypothesis 1 is established as follows:

Hypothesis 1: The declaration effect of private equity offerings will be positive.

Loughran and Ritter (1997) find that public equity issuing firms' will have higher capital expenditure before and after offering, showing that managers and investors are both likely to be overoptimistic about the investment projects. Managers will take advantage of selection of timing to decide when to conduct private placement, which causes that the announcement year of placement usually comes along with high performance. Investors will use firms' per-formance in the placement year as a reference to decide whether to participate or not, and they are also accustomed to predicting firms' future performance by that. Therefore, prior overopti-mistic prediction may lead to slide in long-term stock returns because the predicted goal was not achieved. Hertrzel et al. (2002) and Marciukaityte et al. (2005) also discover that investors tend to be overoptimistic about firms' operation and R&D capability. In addition, they will in-ject success experience from a few firms to the firm they invest, so they believe that particip-ating in private placement will bring in higher benefits. Other studies such as Chen et al. (2002) also find negative long-term stock returns after placement. Therefore, hypothesis 2 is established as follows:

Hypothesis 2: Private placement is negatively correlated with long-term stock returns.

Lee and Kocher (2001) discover that compared with firms with public offerings, private placed firms are usually smaller in size. Brooks and Graham (2005) find that compared with bigger firms placed privately, smaller firms have higher abnormal returns during the announ-cement period. The evidence indicates that firm size can affect not only the behavior of plac-ement but also abnormal return for investors after placplac-ement. Firms in smaller size might not be able to attract investors in public offerings because of less popularity. As for private plac-ement, managers could find the specific investors and explain to them about the firms' growth opportunities, and therefore investors are possibly persuaded to participate easier. The posi-tive declaration effect and higher long-term returns will then easily come about. Therefore,

hypothesis 3a and 3b are established as follows:

Hypothesis 3a: When firms issuing privately are smaller in size, positive declaration effects

on stock return will be greater.

Hypothesis 3b: When firms issuing privately are smaller in size, long-term stock returns will

be higher.

When investors participate in private placement, most of them hope that after infusion of cash, firms' operating performance will boost. And then stock price will reflect firms' perform-ance to provide investors with abnormal returns. Therefore, firms with higher growth opportun-ity will be favored. Chen et al. (2002) find the stock price of firms with low book-to-market will outperform that of firms with high book-to-market ratio. And book-to-market ratio is the proxy for growth opportunity. Therefore, hypothesis 4a and 4b are established as follows:

Hypothesis 4a: Firms issuing private placement with lower book-to-market ratios will have

bigger positive declaration effects.

Hypothesis 4b: Firms issuing private placement with lower book-to-market ratios will have

higher long-term stock returns.

Wruck (1989) thinks that change of ownership structure after private placement may generate more monitoring incentives for new shareholders for newly owned shares or for in-itial shareholders because of increase in share holdings. Because insiders have more informa-tion about the firm than outsiders and have informainforma-tion advantages, their willingness to par-ticipate will reveal their confidence in firm's future perspectives. Moreover, it may also repre-sent that the stock price is undervalued, so rational insiders would participate in the private placement instead of foregoing the potential profits. On the contrary, if insiders have little confidence in firms' operation, or private placement price is overpriced, they may not want to join in the private placement. Therefore, higher percentage of insiders' participation means brighter perspectives for the firms. Krishnamurthy et al.(2005) also find that private plac-ement with the affiliated parties will bring about higher announcplac-ement effect than without, which also shows private placement with the affiliated will be considered by the market with high value. Thus, hypothesis 5a and 5b are established as follows:

Hypothesis 5a: Higher percentage of insiders participating in the private placement will bring

about bigger declaration effects.

Hypothesis 5b: Higher percentage of insiders participating in the private placement will bring

about higher long-term stock returns.

Admati and Pfleiderer (1994) find that internal investors like venture capital will miti-gate the agency problem resulting from financial contracts. Without these kinds of investors, firms will not disclose all internal information. So, the existence of internal investors will help mitigate information asymmetry. In addition to insiders, institutional investors also participate in private placement for quite a large amount of money than insiders or regular investors. Un-like other investors, institutional investors tend to have weaker linkage with the firm. How-ever, because institutional investors possess more resources, they have more ability to assess the firm's value, purpose for private placement, and future perspectives. Therefore, higher per-centage of institutional investors' participation means that they have more confidence in the future perspectives of the firm after private placement. Thus, hypothesis 6a and 6b are estab-lished as follows:

Hypothesis 6a: Higher percentage of institutional investors' participation leads to bigger

posi-tive declaration effects.

Hypothesis 6b: Higher percentage of institutional investors' participation leads to higher

long-term stock returns.

Teoh et al. (1998a, 1998b) find that firms will conduct earnings management before IPO or SEO. When firms collect capital through public offerings with non-specific investors, in-vestors can only get access to the firms' operating performance by financial statements, while managers might be able to use discretionary accruals or other accounting options to manage earnings. Thus, investors may purchase the firm's stock for better earnings performance in the same year. Chen et al. (2002) used firms placing privately in Singapore as samples to examine earnings management behavior, and found no significant results. The reason might be that over 90% of the sample firms were audited by renowned audit firms, and thus managers' ma-nipulation of earnings was restrained. This study postulates that because targets of IPO and SEO firms are mainly regular investors, most of them know little about firms' internal infor-mation. In order to gather up sufficient capital, firms will try their most to present the best financial statements to attract investors. However, the target of private placement firms is fo-cusing on the specific investors, which are fewer in numbers. Also, when firms arrange pri-vate placement, they can directly communicate with the investors, explaining the opportuni-ties to them instead of attracting them with earnings management. Therefore, hypothesis 7 is established as follows:

Hypothesis 7: No significant earnings management is shown before and after private

plac-ement.

3. Research Methodology

Common stock, preferred stock, corporate bonds, and depository receipts are all included in the subjects of private placement. To avoid the difference of the subjects which may disturb the effect, this study only chooses publicly listed and OTC firms placing common stock as samples. To begin with, the information of private placement announced by board of directors of publicly listed and OTC firms from 2002 to 2006 was acquired from the Market Observa-tion and Post System (MOPS). The event date was the announcement date on MOPS. The fraction placed by insiders and institutional investors was calculated with the data of firms' annual reports and message on the private placement section on MOPS. Other financial data were acquired from Taiwan Economic Journal (TEJ) database. A total of 43 private placement firms were eliminated due to incomplete data during the estimate period. Finally, data of 83 firms with private placement event were collected.

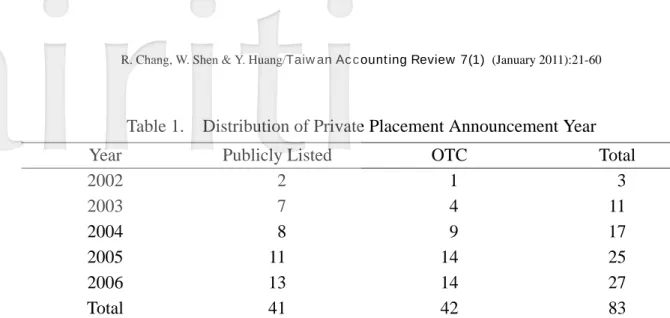

A trend of increasing number of firms placing privately can be seen in Table 1. Among the 83 firms, 41 are publicly listed and 42 are OTC firms. From Table 2, it shows that most firms come from the electronics-related industry, and the highest percentage resides in the in-dustry of computer and peripherals, components, and semi-conductors. From Table 3, firms placed privately in Taiwan are mostly small-sized listed or OTC firms. Average assets of lis-ted samples are well below the average of total lislis-ted firms while average of OCT samples are about the same as the average of all OTC firms.

Table 1. Distribution of Private Placement Announcement Year

Year Publicly Listed OTC Total

2002 2 1 3 2003 7 4 11 2004 8 9 17 2005 11 14 25 2006 13 14 27 Total 41 42 83

Table 2. Distribution of Sample Industry

Industry Listed % of listed OTC % of OTC Total Total %

Food Plastics Textile Ceramics

Machinery and electronics Chemistry and biotech Steel

Rubber

Semi-conductor

Computer and peripheral Optronics Components Telecommunication Online channel Other electronics Information service Construction Transportation

Oil, electricity, and gas Others 1 0 2 1 2 1 1 0 3 9 6 1 3 0 2 0 5 1 1 2 2.439% 0.000% 4.878% 2.439% 4.878% 2.439% 2.439% 0.000% 7.317% 21.951% 14.634% 2.439% 7.317% 0.000% 4.878% 0.000% 12.195% 2.439% 2.439% 4.878% 0 1 0 0 4 1 1 1 6 4 1 8 2 3 2 4 1 1 0 2 0.000% 2.381% 0.000% 0.000% 9.524% 2.381% 2.381% 2.381% 14.286% 9.5247% 2.381% 19.048% 4.762% 7.143% 4.762% 9.524% 2.381% 2.381% 0.000% 4.762% 1 1 2 1 6 2 2 1 9 13 7 9 5 3 4 4 6 2 1 4 1.205% 1.205% 2.410% 1.205% 7.229% 2.410% 2.410% 1.205% 10.843% 15.663% 8.434% 10.843% 6.024% 3.614% 4.819% 4.819% 7.229% 2.410% 1.205% 4.819% Total 41 100% 42 100% 83 100%

Table 3. Total Assetsaof Sample Firms Year Average of Listed Samples Number of Listed Samples Average of Listed Firms Number of Total Listed Firms Average of OTC Samples Number of OTC Samples Average of OTC Firms Number of Total OTC Firms 2002 7,164 41 13,815 669 1,979 42 1,706 538 2003 7,373 41 14,872 672 2,113 42 1,923 538 2004 8,126 41 16,332 675 2,187 42 2,213 539 2005 8,314 41 17,922 677 2,220 42 2,425 539 2006 8,772 41 20,244 677 2,351 42 2,813 540

amillions NT except number of samples and firms

3.1 Measurement of Declaration Effect and Stock Return after Private Placement This study follows the method by Wruck(1989) and takes the publicly listed and OTC firms placing privately from 2002 to 2006 as samples. The event study is adopted to examine the declaration effect of private placement. Event date is defined as the day on which private placement is announced on MOPS. Estimation period is established from day -201 to day -60 on the basis of event date as day 0. Event period starts from day -59 to day 60. The market model method is adopted to calculate the expected return, and the ordinary least square, OLS, is used to establish the regression model for individual stock returns as follows:

Rit= i+ iRmt+ it

Where

Rit: stock return of firm i in day t

Rmt: market return on day t

it: estimation error, it~N(0, )

The daily average abnormal return (AR) and cumulative abnormal return (CAR) of sam-ple firms are calculated as follows:

ARit=Rit-E(Rit)=Rit- ( i+ iRmt)

ARt= 1N N i=1ARit

Where

ARit: abnormal return of firm i in period t

ARt: average abnormal return in period t

Rit: actual return of firm i in period t

E(Rit): expected return of firm i estimated by market model in period t

CAR(t1,t2)= t2 t=t1 ARt= 1N N i=1 t2 t=t1 (ARit),

Where

CAR(t1,t2): cumulative abnormal return from periodt1tot2

The number of sample in the study is large enough to be tested by the t-distribution ac-cording to the central limit theorem. Therefore, the AR and CAR are tested by t-distribution as follows:

1. t-test forAR

t(ARt)= ARt

Var(ARt)

ARt=average of abnormal return in the event period t

VAR(ARt)=standard deviation of average abnormal return in event period t

Var(ARt)= 1N N i=1S 2 i= 1N N i=1 1 (Ti-1) t2 t=t1 ( it -Ti t=1 it Ti) 2

Ti=period T of firm i in estimation period

it=residual error of firm i in estimation period, it=Rit-E(Rit),

S2

i=error term of variance of firm i in estimation perior, S2I=

t2 t=t1

( it- i)2

(Ti-1) ,

it=the average of residual error in estimated period, it=

t2 t=t1

it

Ti

2. t-test of cumulative average abnormal return t(CARt1, t2)= CARt1, t2 Var(CARt1, t2) , Where CARt1, t2= t2 t=t1 ARt, Var(CARt1, t2)=Var( t2 t=t1 ARt),

assuming covariance term=0,then

Var(CARt1, t2)=Var( t2 t=t1 ARt)=Var(ARt1+…+ARt2) =( 1N2 N i=1S 2 i)+…+( 1N2 N i=1S 2 i) =m( 1N2 N i=1S 2 i) which leads to t(CARt1, t2)= 1 N× N i=1 t2 i=t1 (ARit Si ) m ,

percentage of insider participation is higher in Taiwanese private placement firms and insiders have fully understood firms' operation, there is no need for firms to conduct earnings manage-ment behavior by means of DA.

4.5 Sensitivity Analysis

In order to check robustness of the test results, besides adopting the non-standardizedAR and

CAR as presented in the above, we also examines the announcement effect, stock price return,

and earnings management with standardized AR and standardized CAR that are available in

the TEJ database. The results indicate no difference between the two sets of tests. Therefore, the results of the study are robust.

5. Conclusion

At first, the empirical results of the study show that the declaration effect of listed and

OTC firms placed privately in Taiwan is not significant, but positive AR appears more times

than negative AR after placement. Moreover, CAR of day 60 is significantly positive, an

indi-cation that although the placement announcement of listed and OTC firms does not appear positive, it still helps to boost stock price.

Second, this study also finds that CAR one year following placement is significantly

positive, which is inconsistent with foreign literature. The reason might arise from the higher percentage of insider participants in most private placement in Taiwan, who can obtain most information of firms' operation. When insiders are willing to participate in large percentage, it shows their confidence in firms' future prospects, and therefore it is reasonable for positive CAR one year following announcement.

On the other hand, both firm size and market-to-book ratio have significantly negative

correlation with CAR of day 250, suggesting that when placing firms are smaller in size or

lower in market to book ratio, long-termCAR after placement will be comparably higher.

Per-centage of insider participants and institutional investors is also positively correlated with CAR of day 250, which indicates that higher percentage of insiders or institutional investors

will lead to higher long-termCAR after placement. Finally, this study also finds no significant

earnings management behavior in the prior year, in the very year, and in the following year of placement announcement. The reasons might be the limited number of places, a higher per-centage of insider participants, and placing firms can directly collect capital from investors, all of which may make managers lack incentives for conducting earnings management.

This study has searched and selected all information about private placement of listed and OTC firms in Taiwan. Since private issuance started from 2002, samples for study are still not many. Part of information and data of private issued firms have to be collected from annual reports of the firms, which may only contain incomplete information. Therefore, some research samples might be deficient, which is the first limitation of the study. In addition, this study only focuses on the firms which had private placement the first time. Firms issuing more than one time are not included, which is the second limitation of the study.

References

Admati, A.R., and P.Z. Pfleiderer. 1994. Robust financial contracting and the role of venture capitalists. Journal of Finance 49:371-402.

Brooks, L.D., and J.E. Graham. 2005. Equity private placements, liquid assets, and firm valu-e. Journal of Economics and Finance 29: 321-336.

Chen, S.S., K.W. Ho, C.F. Lee, and G.H.H. Yeo. 2002. Long-run stock performance of equity-issuing firms: The case of private placements in Singapore. Review of Pacific Basin

Fi-nancial Markets & Policies 5: 417-438.

Hertzel, M., and R.L. Smith. 1993. Market discounts and shareholder gains for placing equity privately. Journal of Finance 48: 459-485.

Hertzel, M., M. Lemmon, J.S. Linck, and L. Rees. 2002. Long-run performance following pri-vate placements of equity. Journal of Finance 57: 2595-2617.

Hsu, S.F. 2003. A study of private placement on the listed and OTC firms. Master Thesis, Na-tional Sun Yat-sen University (in Chinese).

Jones, J. 1991. Earnings management during import relief investigations. Journal of

Account-ing Research 29:193-228.

Kato, K., and J.S. Schallheim. 1993. Private equity financings in Japan and corporate grou-ping (keiretsu). Pacific-Basin Finance Journal 1: 287-307.

Krishnamurthy, S., P. Spindt, V. Subramaniam, and T. Woidtke. 2005. Does investor identity matter in equity issues? Evidence from private placements. Journal of Financial

Inter-mediation 14: 210-238.

Lee, H.W., and C. Kocher. 2001. Firm characteristics and seasoned equity issuance method: Private placement versus public offering. Journal of Applied Business Research 17: 23-36.

Loughran, T., and J.R. Ritter. 1997. The operating performance of firms conducting seasoned equity offering. Journal of Finance 52: 1823-1850.

Marciukaityte, D., S.H. Szewczyk, and R.Varma. 2005. Investor overoptimism and private equity placements. Journal of Financial Research 28:591-608.

Myers, S.C., and N.S. Majluf. 1984. Corporate financing and investment decisions when fir-ms have information that investors do not have. Journal of Financial Economics 13: 187-221.

Ruth, T.S.K., P.L. Chng, and Y.H., Tong. 2002. Private placements and rights issues in Singa-pore. Pacific-Basin Finance Journal 10: 29-54.

Securities and Exchange Commission. 1971. Institutional Investor Study Report (U.S. Gov-ernment Printing Office, Washington, D.C.)

Silber, W.L. 1991. Discounts on restricted stock: The impact of illiquidity on stock prices.

Fi-nancial Analysts Journal 47: 60-64.

Spiess, D.K., and J. Affleck-Graves. 1995. Underperformance in long-run stock returns fol-lowing seasoned equity offerings. Journal of Financial Economics 38: 243-267.

Teoh, S.H., I. Welch, and T.J. Wong. 1998a. Earnings management and the long-run market performance of initial public offerings. Journal of Finance 53:1935-1974.

Teoh, S.H., I. Welch, and T.J. Wong. 1998b. Earnings management and the underperformance of seasoned equity offerings. Journal of Financial Economics 50: 63-99.

Tversky, A., and D. Kahneman. 1974. Judgment under uncertainty: Heuristics and biases,

Sci-ence 185:1124-1131.

White, H. 1980. A heteroskedasticity-consistent covariance matrix estimator and a direct test for heteroskedasticity. Econometrica 48: 817-838.

Wruck, K.H. 1989. Equity ownership concentration and firm value. Journal of Financial

Ap

pen

d

ix

Dispersion of Event D ates of Private Issuance Firms Code Event date Industry C ode E ve nt date Industry 2449 20021031 Semi-conductor 6186 20050408 Semi-conductor 2601 20021 125 T ransportation 2341 20050413 Compute r and peripheral 5466 20021 125 Semi-conductor 5102 20050415 Rubber 9934 20030324 Others 6195 20050415 Online channel 6150 20030414 Computer and peripheral 2340 20050428 Optronics 1215 20030516 Food 6603 20050518 Machinery and Elec tronics 5309 2003061 1 C omponents 2444 20050525 Communica tion and inte rnet 2505 20030623 Construction 4534 20050525 Machinery and Elec tronics 1464 20030808 T extile 2429 20050610 Components 2331 20031009 Computer and peripheral 6217 20050701 Components 5009 20031024 Ste el 6101 20050823 Components 9905 20031030 Others 6238 20050901 Other electrionics 4502 20031 1 1 1 Machinery and Electronics 2396 20051021 Optronics 2461 20031204 Other electronics 2399 20051025 Compute r and peripheral 1442 20040209 Construction 5310 200601 10 Information service 4503 20040223 Machinery and Electronics 2384 20060213 Optronics 2530 20040304 Construction 1735 20060321 Chemistry and Biote ch 6231 20040308 Information service 6179 20060322 Other electronics 2540 20040325 Construction 1512 20060330 Machinery and Elec tronics 5364 20040330 Components 4304 20060410 Pla stics 5205 20040428 Information service 1526 20060412 Machinery and Elec tronics 1806 2004051 1 C eremics 3017 20060412 Compute r and peripheral 8935 20040514 Others 2543 20060414 Construction6130 20040802 Semi-conductor 6121 20060503 Compute r and peripheral 5386 20040804 Computer and peripheral 8008 20060504 Compute r and peripheral 2465 20040825 Computer and peripheral 9937 20060504 Oil, electricity , and gas 3054 20040901 Computer and peripheral 5523 20060510 Construction 2479 20041202 Optronics 4414 20060525 T extile 41 13 20041203 Chemistry and Biotech 8081 20060713 Semi-conductor 2443 20041207 Optronics 2466 20060724 Optronics 3004 20050103 Other electronics 61 10 20060726 Information service 5345 20050105 Components 8066 20060803 Semi-conductor 6135 20050121 Online channel 6220 20060807 Components 4907 20050215 Communication and internet 6259 20060818 Online channel 2494 20050302 Communication and internet 8299 20061005 Compute r and peripheral 61 14 20050308 Components 2007 20061020 Steel 3041 20050316 Semi-conductor 3046 20061027 Compute r and peripheral 4903 20050318 Communication and internet 5605 20061 128 T ransportation 2442 20050321 Computer and peripheral 8942 20061 128 Others 5321 20050331 Components 6287 20061215 Semi-conductor 6145 20050331 Semi-conductor 2455 20040621 Communication and internet 3051 20060425 Optronics

宣告效果、股價報酬與盈餘管理:

我國企業私募股權之研究

張瑞當

a,沈文華

b,*,黃怡翔

c中文粹要

:私募、宣告效果、股價報酬、盈餘管理一、研究議題

相對於私募制度在國外早已行之多年,國內遲至 2002 年增修訂證券交易法後,才 開始實施私募制度,至今已有越來越多上市上櫃公司透過私募的方式,取得營運所需 資金。根據證券交易法第 7 條:「本法所稱募集,謂發起人於公司成立前或發行公司 於發行前,對非特定人公開招募有價證券之行為。本法所稱私募,謂已依本法發行股 票之公司依第 43 條之 6 第 1 項及第 2 項規定,對特定人招募有價證券之行為。」由於 我國的私募制度較晚實施,對於私募股權宣告效果之研究相對較少,但國外早有文獻 針對私募股權的宣告效果進行研究,並且發現公司私募宣告前 3 天至宣告當日股價的 平均異常報酬顯著為正,顯示私募計劃對於公司股價具有正向宣告效果(Wruck 1989; Hertzel et at. 2002)。而由美國證管會(1971)的報告可發現,發行公司大多以折價方式辦 理股權私募,且平均而言,其折價幅度約 30%。其他文獻也發現,公司為了要順利完 成私募,會提供相當程度之折價給參與私募的投資人(Wruck, 1989; Silber, 1991),以彌 補參與公司私募所產生的資金流動性問題。由於投資人參與私募的原因,除了較大的 折價幅度,也可能是認同公司未來的營運計劃,希望藉由參與公司私募,獲得正的長 期股價異常報酬。但是 Hertzel et al.(2002)卻發現,私募股權公司在私募宣告後三年期 的股價異常報酬為負值,顯示投資人對於私募股權公司未來的營運展望,往往過度樂 觀。因此,本研究同時探討國內上市上櫃公司私募股權之宣告效果及私募股權公司於 私募完成後的長期股價表現。 隨著國內上市上櫃公司私募股權之案例越來越多,私募股權的宣告效果與後續的 股價表現,也越來越受到重視。而私募股權公司是否能享有正的宣告效果與長期股價 * 通訊作者:[email protected]表現,除了受到公司未來成長動能與成長機會之影響,在私募參與者中,內部人及法 人參與私募股權之比率,代表公司內部與公司外部擁有資訊之投資人對公司辦理私募 股權的態度。因此,本研究也探討公司規模、股價淨值比率、內部人參與比率及法人 參與比率等變數對私募股權宣告效果及公司後續股價表現之影響,以作為投資人參加 公司私募股權時之決策參考。 最後,管理者為了能順利經由私募取得資金,有可能會透過盈餘操弄來美化或窗 飾 (window-dressing)財務報表,吸引特定投資人資金之挹注。由於盈餘管理具有迴轉效 果,倘若私募股權公司在私募當年度,曾有盈餘管理行為,此迴轉效果即可能會影響 私募完成後次一年度之盈餘。因此,本研究也針對私募股權公司在私募宣告前一年度、 私募宣告當年度及私募宣告後一年度,是否會有顯著的盈餘管理行為進行探討。

二、研究假說

當管理者認為公司價值遭到低估時,會傾向利用私募進行籌資,並經由參與私募 掌握未來獲利的機會(Hertzel and Smith 1993)。由於私募對象限定於特定人,這些參與 私募股權的投資人,都是在審慎評估之下,參與公司私募。因此當公司宣告要以私募 的方式籌集資金時,市場可能以公司價值受到低估及新資金投入有助於公司發展的角度來解讀,故本研究建立假說 H1如下:

H1:公司私募股權對於股價具有正向的宣告效果。

辦理現金增資之公司,在增資前後的資本支出往往相對較高,顯示管理者與投資 人可能對公司新的投資方案過於樂觀(Loughran and Ritter 1997)。再加上管理者有權決定 何時辦理私募,而造成公司私募宣告年度,往往正逢績效高峰期,因此,投資人對公 司未來過度樂觀的預期,比較容易使私募後之績效不如預期,導致公司長期股價報酬

下滑,故本研究提出假說 H2如下:

H2:公司私募股權與長期股價表現呈現負向關係。

私募股權公司通常具有規模較小之特性(Lee and Kocher 2001),且規模較小之私募 股權公司在私募宣告期間之異常報酬相對較高(Brooks and Graham 2005)。由於規模較小

之公司,具有較大的成長空間,比較容易受投資人青睞,故本研究提出假說 H3a及 H3b 如下: H3a:私募股權公司規模越小時,其正向宣告效果越大。 H3b:私募股權公司規模越小時,其長期股價報酬越高。 Chen et al.(2002)發現低淨值股價比率之私募股權公司的股價表現,會優於高淨值股 價比之私募股權公司。由於淨值股價比反映投資人對公司未來展望看好的程度,也可 作為公司成長機會的代理變數,故本研究建立假說 H4a與 H4b如下: H4a:淨值股價比率越低之私募股權公司,其正向宣告效果越大。 H4b:淨值股價比率越低之私募股權公司,其長期股價報酬越高。

若公司內部人參與公司私募股權比率越高,一方面代表內部人對公司越有信心, 另一方面也可能代表公司私募股權訂定之股價偏低,使內部人不願意放棄參與公司私 募股權的機會。故本研究提出假說 H5a及 H5b如下: H5a:公司內部人參與私募程度越高,其正向宣告效果越大。 H5b:公司內部人參與私募程度越高,其長期股價報酬越高。 外部法人經常成為公司私募股權的應募對象,且應募金額往往高於其他投資人。 當法人參與企業私募股權之程度越高時,也代表法人對公司具有信心,故本研究提出 假說 H6a及 H6b如下: H6a:法人參與私募程度越高,其正向宣告效果越大。 H6b:法人參與私募程度越高,其長期股價報酬越高。 公司為了募集資金,在募集資金的過程中,往往會盡量呈現出較好的盈餘數字, 以提高投資人購買公司股票之意願。不過,因為私募股權之籌資對象為特定人,且人 數較少,管理者可面對面向應募人詳述未來的營運計劃,而不必透過盈餘管理的方式, 來吸引一般的投資人,因此本研究提出假說 H7如下: H7:私募股權公司在私募前後無顯著盈餘管理行為

三、研究方法

私募制度包含私募普通股、特別股、私募公司債及海外存託憑證等,為避免因私 募標的不同,產生效果上之混淆,本研究將樣本鎖定於私募普通股之上市上櫃公司。 首先,利用公開資訊觀測站取得 2002 年至 2006 年上市上櫃公司董事會通過辦理私募 之訊息,並以董事會通過私募案後,於公開資訊觀測站公告之日為事件日,依個別公 司年報所揭露之私募資訊,與公開資訊觀測站私募專區所公布之訊息,計算公司內部 人及法人參與私募之股權比率,然後再由 TEJ 資料庫取得財務資料,經刪除資料不完 整及平均異常報酬估計區間內資料不足之樣本後,共取得 83 家曾辦理私募股權公司之 相關資料。其中,屬於上市公司者共 41 家,餘 42 家皆屬於上櫃公司(詳如表 1),而 其產業分類則以電子相關產業最多(詳如表 2),且大多屬於規模較小的上市上櫃公司 (詳如表 3)。 本研究採用事件研究法探討私募股權之宣告效果,將「事件日」定義為公司董事 會決議辦理私募股權後,於公開資訊觀測站公布訊息之日;「估計期」設為事件日前 201 日至前 60 日;而「事件期」則為事件日前 59 日至事件後 60 日,採用市場模式計 算期望報酬率,以普通最小平方法建立個股股價報酬率之迴歸模型如下: Rit= i+ iRmt+ it 式中:t=t1……tn,代表天數;i=1, 2…N,代表公司;Rit=第 t 天 i 公司之股價報 酬率; i與 i皆為估計參數;Rmt=第 t 天市場報酬率; it=誤差項, it~N(0, )至於樣本公司每日平均異常報酬(average abnormal return, AR)與累計平均異常報酬

(cumulative abnormal return,CAR)之衡量方式如下:

ARit=Rit-E(Rit)=Rit- ( i+ iRmt) ARt= 1N N i=1ARit 式中:ARit=事件期 t 期之異常報酬;ARt=事件期 t 期之平均異常報酬;Rit=i 公 司在事件期 t 期之實際報酬;E(Rit)=以市場模式估計 i 公司在事件期 t 期之預期報酬 而事件期 t1至 t2之累計平均異常報酬(CAR(t1,t2))之計算方式如下: CAR(t1, t2)= t2 t=t1 ARt= 1N N i=1 t2 t=t1 (ARit) 另外,為檢驗公司規模、股價淨值比率、內部人參與比率及法人參與比率是否會 影響公司私募股權後之股價表現,本研究以累計平均異常報酬為因變數,公司規模、 股價淨值比率、內部人參與比率、法人參與比率、產業別及負債比率為自變數進行下 列迴歸分析:

CARit= 0+ 1SIZEit+ 2MBit+ 3INSIDERit+ 4INSTITUTIONit

+ 5INDit+ 6LEVit+ it

式中:CARit=i 公司第 t 期累計平均異常報酬;SIZEit=i 公第 t 期期初資產總額取

對數值;MBit=i 公司第 t 期之股價淨值比率;INSIDERit=i 公司第 t 期公司內部人參與

之比率;INSTITUTIONit=i 公司第 t 期法人參與之比率;INDit=虛擬變數,i 公司第 t

期之產業分類若為電子資訊業設為 1,否則為 0;LEVit=i 公司第 t 期之負債比率; it=

誤差項

最後以 modified Jones model 估算裁決性應計數,衡量私募股權公司的盈餘管理行 為。

四、研究結果

私募宣告當日之平均異常報酬(AR)為-0.4775(p>0.1),且在私募後 10 日內,只有第 3 日(AR=0.8567, p<0.01)與第 5 日(AR=1.0711, p<0.01)之平均異常報酬達到顯著水準, 而私募宣告日當日及宣告日前 10 日之股價平均異常報酬率,均未達到顯著水準(詳如 表 6),顯示並無足夠證據支持私募宣告具有正向的宣告效果,假說 H1並未獲得支持。 不過,由圖 1 可發現,在私募宣告日後,公司股價呈正向平均異常報酬之日數,不僅 明顯多於負向平均異常報酬之日數,也多於私募宣告日前正向平均異常報酬之日數, 且由圖 2 及表 8 可發現私募後 60 日之累計平均異常報酬為正,且達到顯著水準,顯示 國內上市上櫃公司的私募宣告,雖不具正向宣告效果,但對公司股價還是具有較大的 正面意義。 其次,公司自私募宣告後第 40 日起,其累計平均異常報酬開始穩定達到 =0.05 的 顯著水準(第 40 日之累計平均異常報酬=5.0483%),且維持正的累計平均異常報酬,至宣告日後第 250 日止之累計平均異常報酬為 26.2272% (p<0.01),顯示公司於私募宣 告後一年,其股價具有正的累計平均異常報酬(詳如圖 3 與表 10),假說 H2未獲支 持。而其原因可能是,國內公司辦理私募,常有較高的內部人參與比率(詳如表 4), 甚至 100%由內部人認購。當內部人願意大舉參與私募時,也代表內部人對公司深具信 心。由圖 4 與圖 5 可發現,具有高內部人參與比率之公司,其私募宣告後 60 日累計平 均異常報酬率之走勢,明顯優於低內部人參與比率之公司。其中高內部人參與比率之 公司,60 日累計平均異常報酬率為 9.5073%,t 值為 2.6968(p<0.05)。而低內部人參與 比 率 之 私 募 股 權 公 司,其 60 日 累 計 平 均 異 常 報 酬 率 為-14.9133%,t 值 為-1.2973 (p>0.01)。再由圖 6 及圖 7 則可發現,具高內部人參與比率之公司,其私募宣告後 250 日累計平均異常報酬率之走勢,也明顯優於低內部人參與比率之私募股權公司。其中 高內部人參與比率之私募股權公司,其 250 日累計平均異常報酬率為 28.1983%,t 值 為 4.1250(p<0.01)。而低內部人參與比率之私募股權公司,其 250 日累計平均異常報酬 率為-62.3254%,t 值為-2.3692(p<0.1)。此結果顯示內部人參與比率與公司私募後之累 計平均異常報酬有關,也正足以作為國內公司在私募宣告後一年,股價呈現正向累計 平均異常報酬的合理解釋。 另外,若以私募宣告後 60 日累計平均異常報酬率為依變數,對公司資產規模、股 價淨值比率、內部人參與比率、法人參與比率、產業分類及負債比率進行迴歸分析, 可發現法人參與比率與產業分類之係數分別為 0.4637(p<0.05)及 20.6909(p<0.05),顯 示私募宣告後 60 日之股價累計平均異常報酬與法人參與比率有正向關係,而當私募公 司屬於電子相關產業時,私募宣告後 60 日之股價累計平均異常報酬也相對較高(詳如 表 11),顯示短期而言,投資人對於法人參與比率較高或產業分類屬於電子業之私募 股權公司,會給予較佳的評價。至於資產規模、股價淨值比率及內部人參與比率等三 項變數之係數,則未達到顯著水準。故只有假說 H6a獲得支持,假說 H3a、H4a及 H5a皆 未獲得支持。 在長期股價表現方面,法人參與比率之係數為 1.4960(p<0.05),而資產規模、股價 淨值比率及內部人參與比率之係數分別為-39.8720(p<0.1)、-16.0078(p<0.1)及 1.3858 (p<0.05)(詳如表 12)。顯示就長期而言,公司資產規模及股價淨值比率,與公司私 募宣告後 250 日之累計平均異常報酬有負向關係,而與內部人參與比率有正向關係, 代表當公司資產規模較小、股價淨值比率較低或內部人參與比率較高時,在私募宣告 後一年,公司股價的累計平均異常報酬相對較高,因此除了假說 H4b外,H3b、H5b及 H6b皆獲得支持。 最後,由於國內私募股權公司不論在私募宣告當年度、前一年度或後一年度,其 裁決性應計數與對照組公司均無顯著差異,顯示國內私募股權公司於辦理私募時,並 無利用裁決性應計數操弄盈餘之現象,假說 H7獲得支持。