國立臺灣大學管理學院財務金融學系 碩士論文

Department of Finance College of Management National Taiwan University

Master Thesis

相依結構對多資產選擇權定價影響之實證分析 Bivariate Options Pricing with

Copula-Based GARCH Model -Empirical Analysis

許凱雯 Kai-Wen Hsu

指導教授:王耀輝 博士 Advisor: Yaw-Huei Wang, Ph.D.

中華民國 98 年 6 月

June, 2009

i

摘要

本論文係探討相依結構對二元選擇權定價結果影響的實證分析。所謂二元選 擇權,乃指兩個相異標的資產所衍生而得的奇異選擇權,其價格與兩個資產的價 格變動及相依結構具有極大關聯。在此選取四組不同的金融指數作實證分析,其 組成內容包含跨國家和跨資產,以期觀察在不同的相依結構下,對三種市場上較 為廣泛交易的二元選擇權,其選擇權評價結果有何異同。論文中採用 Copula-based GARCH 模型作為定價方法,並利用適合度檢定選取出一最適相依結構,最後以蒙地 卡羅模擬求得選擇權價格後,比較各相依結構下的選擇權評價差異。

研究結果發現,當標的資產相關程度愈強、選擇權到期日愈長、選擇權到期 時的價格在價平附近與選擇權的報酬函數為二元彩虹選擇權時,在不同相依結構 下的評價結果,其價格差異顯著性會愈高。故總結而言,相依結構的設定對二元 選擇權的價格確實存在影響,在評價二元選擇權時是不可被忽略的一環。

關鍵字:二元選擇權、多資產選擇權、相依結構。

ii

Abstract

Multivariate options have experienced significant development in the last decade,

due to their excellent abilities for hedging the risk of multiple assets. The most

important issue in the valuation of multivariate options is the dependence structure

among these underlying assets. In this paper, we use copula-based GARCH model as

pricing device to describe the dependence structures of underlying assets, rather than the

traditional linear correlation and Gaussian assumptions to price multivariate claims.

Particularly, the skewed-t GARCH model is applied to capture the marginal

distributions of underlying financial assets. To compare the impact of difference

dependence structures on option pricing, we perform Monte-Carlo simulation to

simulate the bivariate option prices, and observe the error of option prices caused from

different model dependence structures, time-to-maturities, strike prices and option

payoff functions. We use goodness-of-fit tests to choose one dependence model that fit

the empirical distributions best, and then the paired t-test is also implemented to

determine whether the pricing errors are significant enough.

iii

Contents

摘要 ...i

Abstract ... ii

1. INTRODUCTION ... 1

2. LITERATURE REVIEW ... 3

3. THE COPULA-BASED GARCHMODEL ... 8

3.1 SKEWED-T GARCHMODEL ... 8

3.2 THE COPULA FUNCTIONS ... 9

3.3 IFMMETHOD ... 11

3.4 GOODNESS-OF-FIT TEST... 13

3.5 MONTE CARLO SIMULATION ... 15

4. DATASETS AND OPTION PAYOFF STRUCTURES ... 17

4.1DATA AND DIAGNOSTIC ANALYSIS ... 17

4.2OPTION PAYOFF STRUCTURES ... 19

5. EMPIRICAL RESULTS ... 20

6. CONCLUSION ... 40

7. REFERENCE ... 42

APPENDIX A:The Simulation Results of Pair 2 - MSCI World Energy Index and MSCI World Bank Index ... 47

APPENDIX B:The Simulation Results of Pair 3 - Reuters/Jefferies CRB Index and MSCI Latin America Index... 52

APPENDIX C:The Simulation Results of Pair 4 - S&P 500 Index and DXY currency Index... 57

iv

Tables

Table 1: Bivariate copula families ... 10

Table 2: Quasi-inverse function of copula function 𝒄𝒖(𝒗) ... 16

Table 3: The linear correlation of each pair assets ... 17

Table 4: Summary Statistics ... 18

Table 5: Bivariate options payoff structures ... 19

Table 6: Copula-based GARCH Model Estimations ... 22

Table 7: Goodness-of-fit test to Copula-based GARCH Models ... 24

Table 8: T test for the distance between the ATM (K=1) option prices of different dependence structures with 1 month time-to-maturity - Pair 1- MSCI Pacific Index and MSCI Far East Index ... 31

Table 9: T test for the distance between the ATM (K=1) option prices of different dependence structures with 6 months time-to-maturity - Pair 1- MSCI Pacific Index and MSCI Far East Index... 32

Table 10: T test for the distance between the ITM (K=0.8) option prices of different dependence structures with 6 months time-to-maturity - Pair 1- MSCI Pacific Index and MSCI Far East Index... 34

Table 11: T test for the distance between the OTM (K=1.2) option prices of different dependence structures with 6 months time-to-maturity - Pair 1- MSCI Pacific Index and MSCI Far East Index... 35

Table 12: T test for the distance between the ATM (K=1) option prices of different dependence structures with 6 months time-to-maturity – Pair 1 to 4 ... 37

Table 13: T test for the distance between the ATM option prices of different dependence structures with 6 months time-to-maturity - Pair 2- MSCI World Energy Index and MSCI World Bank Index ... 51

Table 14: T test for the distance between the ATM option prices of different dependence structures with 6 months time-to-maturity - Pair 3- Reuters/Jefferies CRB Index and MSCI Latin America Index ... 56

Table 15: T test for the distance between the ATM option prices of different dependence structures with 6 months time-to-maturity - Pair 4 - S&P 500 Index and DXY currency Index... 61

v

Figures

Figure 1: The Empirical Copula of the Standardized GARCH Innovations…………..20 Figure 2: Digital Option Pricing Result Under Different Copulas vs. Different Strike

Prices - Pair 1- MSCI Pacific Index and MSCI Far East Index………..27 Figure 3: Digital Option Price Result Under Different Copulas vs. Different Time to

Maturities - Pair 1- MSCI Pacific Index and MSCI Far East Index ... 28 Figure 4: Spread Option Pricing Result Under Different Copulas vs. Different Strike

Prices - Pair 1- MSCI Pacific Index and MSCI Far East Index ... 28 Figure 5: Spread Option Price Result Under Different Copulas vs. Different Time to

Maturities - Pair 1- MSCI Pacific Index and MSCI Far East Index ... 29 Figure 6: Rainbow Option Pricing Result Under Different Copulas vs. Different Strike

Prices - Pair 1- MSCI Pacific Index and MSCI Far East Index ... 29 Figure 7: Rainbow Option Price Result Under Different Copulas vs. Different Time to

Maturities - Pair 1- MSCI Pacific Index and MSCI Far East Index ... 30 Figure 8: Digital Option Pricing Result vs. Different Strike Prices - Pair 2- MSCI World

Energy Index and MSCI World Bank Index………....47 Figure 9: Digital Option Price Result vs. Different Time to Maturities - Pair 2- MSCI

World Energy Index and MSCI World Bank Index ... 48 Figure 10: Spread Option Pricing Result vs. Different Strike Prices - Pair 2- MSCI

World Energy Index and MSCI World Bank Index ... 48 Figure 11: Spread Option Price Result vs. Different Time to Maturities - Pair 2- MSCI

World Energy Index and MSCI World Bank Index ... 49 Figure 12: Rainbow Option Pricing Result vs. Different Strike Prices - Pair 2- MSCI

World Energy Index and MSCI World Bank Index ... 49 Figure 13: Rainbow Option Price Result vs. Different Time to Maturities - Pair 2- MSCI

vi

World Energy Index and MSCI World Bank Index ... 50 Figure 14: Digital Option Pricing Result vs. Different Strike Prices - Pair 3-

Reuters/Jefferies CRB Index and MSCI Latin America Index ... 52 Figure 15: Digital Option Price Result vs. Different Time to Maturities - Pair 3-

Reuters/Jefferies CRB Index and MSCI Latin America Index ... 53 Figure 16: Spread Option Pricing Result vs. Different Strike Prices - Pair 3-

Reuters/Jefferies CRB Index and MSCI Latin America Index ... 53 Figure 17: Spread Option Price Result vs. Different Time to Maturities - Pair 3-

Reuters/Jefferies CRB Index and MSCI Latin America Index ... 54 Figure 18: Rainbow Option Pricing Result vs. Different Strike Prices - Pair 3-

Reuters/Jefferies CRB Index and MSCI Latin America Index ... 55 Figure 19: Rainbow Option Price Result vs. Different Time to Maturities - Pair 3-

Reuters/Jefferies CRB Index and MSCI Latin America Index ... 56 Figure 20: Digital Option Pricing Result vs. Different Strike Prices - Pair 4 - S&P 500

Index and DXY currency Index ... 57 Figure 21: Digital Option Price Result vs. Different Time to Maturities - Pair 4 - S&P

500 Index and DXY currency Index ... 58 Figure 22: Spread Option Pricing Result vs. Different Strike Prices - Pair 4 - S&P 500

Index and DXY currency Index ... 59 Figure 23: Spread Option Price Result vs. Different Time to Maturities - Pair 4 - S&P

500 Index and DXY currency Index ... 60 Figure 24: Rainbow Option Pricing Result vs. Different Strike Prices - Pair 4 - S&P 500

Index and DXY currency Index ... 60 Figure 25: Rainbow Option Price Result vs. Different Time to Maturities - Pair 4 - S&P

500 Index and DXY currency Index………...61

1

1. I

NTRODUCTIONMultivariate options have experienced significant development in the last decade,

due to their excellent abilities for hedging the risk of multiple assets. These options are

financial derivatives written on the performance of two or more underlying securities or

indices. They usually take the form of options on the best or worst performance of a

number of underlying assets. Particularly, when there are only two underlying assets on

multivariate options, they are called as bivariate options. Options on the maximum,

minimum, difference between the performance of two assets, or options to exchange

one asset for another are all common types of bivariate claims.

The most important issue in the valuation of multivariate options is the dependence

structure among these underlying assets. The dependence structures firmly affect the

value of multivariate options. For instance, consider a spread option which gives

option holder the right to gain the difference between the performances of two

underlying assets with a pre-determined strike price. If these two underlying assets have

highly positive correlation, the difference between their performances would be smaller

than those are low correlated or tend to move on the opposite direction. This means the

spread option is less valuable when the underlying assets are low correlated, and vice

versa. Hence, how to determine the dependence structure becomes the most critical

issue in the multivariate options pricing.

2

Although there are growing offers of multivariate claims on the OTC markets, and

the pricing problem in the literatures is also far from elementary, the key determinant of

dependence describing issue is still not sophisticated enough. In this paper, we use

copula-based GARCH model as pricing device to describe the dependence structures of

underlying assets, rather than the traditional linear correlation and Gaussian

assumptions to price multivariate claims. Particularly, the skewed-t GARCH model is

applied to capture the marginal distributions of underlying financial assets.

To compare the impact of difference dependence structures on option pricing, we

furthermore perform Monte-Carlo simulation to simulate the bivariate option prices, and

observe the error of option prices caused from different model dependence structures,

time-to-maturities, strike prices and option payoff functions. We use goodness-of-fit

tests to choose one dependence model that fit the empirical distributions best, and then

the paired t-test is also implemented to determine whether the pricing errors are

significant enough.

The paper is structured as follows: section II presents the literature review of

multivariate options pricing models. Section III formally introduces the copula

functions and the GARCH model. In section IV, we present the dataset used to the

empirical test, and illustrate the payoff structures employed in this study. Section V

demonstrates the main empirical results. Section VI concludes.

3

2. L

ITERATURER

EVIEWSince Black and Sholes (1973) introduced the Brownian motion framework in

option pricing, there are various generalizations used to price multivariate claims, or

even some provide analytical expressions for the most common payoff structures, such

as Margrabe (1978), Stulz (1982), Johnson (1987), Reiner (1992), and Shimko (1994).

Empirically, the marginal distribution of the underlying financial asset usually exists

stochastic volatility and jumps, and many models even deal with the heteroscedasticity

including Merton (1976), Rubinstein (1983), Hull and White (1987), and so on.

Nevertheless, these models still encounter the difficulties that the variance rate is

unobservable.

Hence, Duan (1995) introduced the generalized autoregressive conditional

heteroskedastic (GARCH) process that follows Bollerslev (1986) for option pricing.

The GARCH model has three most special characteristic: the risk premium is embedded

in the underlying asset when doing the GARCH option pricing; the GARCH model is

non-Markov; it can explain the systematic biases of Black-Sholes model such as the

implied volatility smile.

Besides, Heston and Nandi (2000) also followed the same framework to develop a

closed-form solution for European options, proving that the out-of-sample valuation

errors from the single lag version of the GARCH model are lower than the

4

Black-Scholes model. The main contribution of the GARCH model is that

successfully implements the discrete time framework on option pricing, which describe

the correlation and the path dependence of volatility between underlying asset returns

both better than the continuous time framework.

Bollerslev, Engle and Wooldridge (1988) first extended the GARCH model to a

basic multivariate framework, VECH GARCH model, that extended GARCH

representation in the univariate case to the vectorized conditional variance matrix.

However, the VECH GARCH model cannot ensure the conditional variance-covariance

matrix to be positive definite. The BEKK model of Engle and Kroner (1995) ensures the

conditional variance-covariance matrix to be positive definite in the process of

optimization, but the parameters are difficultly interpreted. Bollerslev (1990) also

introduced the constant conditional correlation (CCC) GARCH model, which has more

computational advantages than the BEKK model, but the dependence structure between

underlying assets is still quite restricted.

Subsequently, Engle and Sheppard (2001) and Engle (2002) proposed the dynamic

conditional correlation (DCC) GARCH model, which has flexible correlation structure

and simplifies the estimation procedure. Nevertheless, most of DCC GARCH models

are based on the assumption that the underlying assets follow multivariate Gaussian

distribution and it is obviously unrealistic. Most financial asset returns are actually

5

non-Gaussian: skewed, leptokurtic, and asymmetrically dependent. In some recent

studies, such as Sahu et al. (2001) and Bauwens and Laurent (2002), proposed

multivariate skewed distribution or even the skewed Student’s t distribution to allow the

asymmetry and leptokurtic. However, it is impossible to specify a general multivariate

extension to every types of univariate distribution that allow the dependence structure

can be captured completely.

Furthermore, these papers model the dependence structure between underlying

financial assets only by their linear correlation, which may not describe the entire

dependence structure well enough. There are abundant empirical studies emphasizing

the drawbacks of a linear dependence structure and the flexible copula functions can

better represent the joint behavior of underlying financial assets. For instance,

Embrechts et al. (2002) showed that correlation is often not a satisfactory measurement

of dependence unless the asset returns are multivariate Gaussian distribution. In

addition, the correlation between financial assets generally increases within the high

volatility period or bad states of the economy, see Boyer et al. (1999) and Patton (2003,

2004). The correlation structure of asset returns may differ as time goes by.

To overcome these shortcomings, copula-based GARCH model is therefore

introduced to model the dependence structure of multivariate claims. Instead of the

assumption of multivariate Gaussian distribution, copula is a multivariate distribution

6

function that each marginal follows uniform distribution on the unit interval. Sklar

(1959) proved that any continuous multivariate distribution can be uniquely composed

of its marginal distributions and a copula function, and then Nelson (1999) and Joe

(1997) implement it into the financial field.

The advantage of copula-based model is that each marginal can be estimated by

any desired method that better represent the distribution of asset returns, and then linked

these marginals through a chosen copula or copula family that could best describe the

dependence structure. This is particularly useful whenever the multivariate Gaussian

distribution assumption does not hold. The associated dependency parameters can be

also easily conditioned or varying with time to capture the dependence structures.

There are some studies using copula-based approach to model multivariate option

pricing issue. For instance, Rosenberg (1999) employed Plackett copula to obtain a

bivariate risk-neutral distribution from which the bivariate claims can be evaluated, and

Cherubinni and Luciano (2002) extend the work to other copula families. Patton (2003)

further employed dynamic-copula approach in the foreign exchange market and found

time variation of asymmetric dependence between two exchange rates to be significant.

Goorbergh, Genest and Werker (2005) also applied the dynamic-copula model to the

bivariate equity options, and the empirical results showed that the option prices under

dynamic-copula models significantly differ from the static ones, especially in

7

high-volatility periods. Jondeau and Rockinger (2006) extended the empirical test that employed skewed Student’s t distribution to the innovations. These studies developed

the process of bivariate option pricing and parameter estimation and examined the price

differences between static and dynamic copula.

In this paper, our main purpose is to compare the pricing errors between copulas

under different circumstances and see the impact of copula selecting. Therefore, we

apply the static copula-based GARCH model to simplify the whole option pricing issue.

8

3. T

HEC

OPULA-

BASEDGARCH M

ODEL3.1 SKEWED-T GARCHMODEL

Since we could consider the marginal distributions and dependence structures both

simultaneously and separately under the copula functions, the joint distributions of

underlying asset returns are therefore more flexible and realistic. Here we assume that

each of the objective marginal distributions of the underlying asset returns ri,t follows

the skewed-t GARCH(1,1) process specifying by Hansen (1994) with time-varying

volatility. The return process is denoted as follows:

For i ∈ 1,2 ,

ri,t = μi+ εi,t,

hi,t = ωi+ βihi,t−1+ αiεi,t−12 , (3.1)

εi,t|ℱt−1= hi,tzi,t , zi,t~skewed − t zi ηi, ϕi

where ωi > 0, βi> 0, αi > 0, and ℱt−1 is the information set at time t-1. The density

function of the skewed-t distribution is defined as

skewed − t z η, ϕ = bc(1 +η−21 (bz +a1−λ)2)−η+12, z < −ab

bc(1 +η−21 (bz +a1+λ)2)−η+12, z ≥ −ab (3.2)

The constants a, b and c are given by

a ≡ 4λcη−2η−1, b ≡ 1 + 3λ2 − a2 and c ≡ Γ(η+

1 2) π η−2 Γ(η2)

9

where η is the kurtosis parameter restricted to 2 < 𝜂 < ∞, and λ is the asymmetry

parameter restricted to −1 < λ < 1. Therefore, the specified marginal distributions of

underlying asset returns under our assumptions are asymmetric, fat-tailed, and

non-Gaussian. The GARCH parameters are estimated by maximum likelihood with the unconditional variance level 1−βωi

i−αi as initial value hi,0.

3.2 THE COPULA FUNCTIONS

By the Sklar theorem, each multivariate distribution with continuous margins has a

unique copula representation. Hence, we use copula functions to determine the joint

distribution between the objective marginal distributions of the underlying asset returns.

Theorem 1 Sklar (1959): Let F be a joint distribution function with marginal

distributions 𝐹1, … , 𝐹𝑛. Then, for all x1, … , xn ∈ R,

(i) There exists a copula C such that

𝐹 x1, … , xn = 𝐶(𝐹1(x1), … , 𝐹𝑛(xn)) (3.3)

If the margins are continuous, C is unique.

(ii) Conversely, if C is a copula and 𝐹1, … , 𝐹𝑛 are univariate distribution functions,

then the function F defined in Formula (3.3) is a joint distribution function with

marginal distributions 𝐹1, … , 𝐹𝑛.

In Formula (3.3), a multivariate distribution F could be formed by combining

10

marginal distributions with a copula function C. We also could evaluate Formula (3.3) at

the arguments xi = Fi−1 ui , 0 ≤ ui ≤ 1, i = 1, … , n, and then we obtain another

representation

𝐶(u1, … , un) = 𝐹 𝐹1−1 u1 , … , 𝐹𝑛−1 un (3.4)

In this paper, we have five types of bivariate copula functions employed to

combine the marginal distributions of the underlying asset returns into the joint

distribution functions: the Gaussian copula, the Student’s t copula, the Gumbel copula,

the Clayton copula, and the Frank copula. The below Table 1 displays several bivariate

copula families.

Table 1: Bivariate copula families Elliptical Copula

Gaussian CGa u1, u2 = Φρ

XY(Φ−1 u1 , Φ−1 u2 ) Student’s t Ct u1, u2 = Ψρ,ν(tν−1 u1 , tν−1 u2 ) Archimedean Copula

Gumbel CGu u1, u2 = exp{−[ −lnu1 ∝+ (−lnu2)∝]1 ∝} Clayton CC u1, u2 = max[(u1−∝+ u2−∝− 1)1 ∝, 0]

Frank

CF u1, u2 = −∝1ln[1 +(e−∝u1− 1)(e−∝u2− 1)

e−∝− 1 ]

Note: u is a vector of marginal probabilities, Φρxy is the standard bivariate normal distribution function with linear correlation coefficient ρXY, Φ is the standard normal distribution function, Ψρ,ν is the cdf of a bivariate Student’s t distribution with correlation matrix ρ and degrees of freedom parameter υ> 2.

Both Gaussian and Student’s t copula belong to the class of elliptical copula. For

imperfectly correlated variables, the Gaussian copula implies tail independence. When the number of degree of freedom diverges, the Student’s t copula converges to the

11

Gaussian one, but the Student’s t copula still assigns more tail events than the Gaussian copula. Moreover, the Student’s t copula exhibits tail dependence even if the correlation

coefficients equal zero.

Besides the elliptical copula family, we also use some Archimedean copula

functions, in particular to the one-parameter ones. These copula functions could be

distinguished by their own tail dependency. The Gumbel family has upper tail

dependency with λU = 2 − 21α, the Clayton family has lower tail dependency for α > 0,

since λL = −21α, and the Frank family has neither lower nor upper tail dependency.

3.3 IFMMETHOD

In general, people consider using maximum likelihood method to estimate the

copula parameters. Using Formula (3.3) in Sklar theorem, it is obtained that the

log-likelihood function can be represented by

𝑙 𝜃 = Tt=1ln 𝑐(𝐹1(x1t), … , 𝐹𝑛(xnt)) + Tt=1 nj=1ln 𝑓𝑗(xjt) (3.5)

where 𝑐(𝐹1(x1t), … , 𝐹𝑛(xnt)) = ∂𝐶(𝐹∂𝐹1(x1t),…,𝐹𝑛(xnt))

1(x1t)…∂𝐹𝑛(xnt) , and θ is the set of all parameters of both the marginal distributions and copula functions.

As we identify the marginal distributions and the copula, we could obtain the

previous log-likelihood function and the maximum likelihood estimators

θ MLE = Arg max𝜃𝑙(𝜃) (3.6)

12

However, the maximum likelihood estimators could be very computationally

intensive in the case of high dimensions, because we have to estimate the parameters of

the marginal distributions and the dependence structure represented by the copula

simultaneously. We alternatively implement the inference for the margins or IFM

method proposed by Joe and Xu (1996). They suggest that these sets of parameters

should be estimated in two steps:

(i) In the first step, we estimate the parameters of the marginal distributions θ1 by

performing the estimation of each univariate margins:

θ 1 = Arg maxθ1 Tt=1 nj=1ln 𝑓𝑗(xjt; θ1) (3.7)

(ii) In the second step, we then estimate the copula parameter θ2 by given θ 1: θ 2 = Arg maxθ2 Tt=1ln 𝑐(𝐹1(x1t), … , 𝐹𝑛(xnt); θ2, θ 1) (3.8)

The IFM estimator θ IFM = (θ 1, θ 2)′ is different from the MLE θ MLE because the

IFM estimator is the solution of:

∂θ∂𝑙1

11,∂θ∂𝑙2

12, … ,∂θ∂𝑙𝑛

1n,∂θ∂𝑙𝑐

2 = 0′ (3.9) but the MLE comes from the solution of:

∂θ∂𝑙

11,∂θ∂𝑙

12, … ,∂θ∂𝑙

1n,∂θ∂𝑙

2 = 0′ (3.10)

where l is the entire log-likelihood function, lj is the log-likelihood function of the jth

marginal distribution, and lc is the log-likelihood function of the copula itself. In general,

these two estimators are therefore not equivalent.

13

Also, Patton (2006) showed that the IFM estimator verifies the property of

asymptotically efficient and normality, and we have

T(θ IFM − θ0) → N(0, 𝒢−1(θ0)) (3.11)

where θ0 denotes the true value of the parameter vector, and the 𝒢(θ0) denotes the

Godambe information matrix taking the following form:

𝒢 θ0 = D−1V(D−1)′ (3.12)

with

D = E ∂s θ ∂θ , V = E[s(θ)s(θ)′],

and a score function

s θ = ∂𝑙1

∂θ11, ∂𝑙2

∂θ12, … , ∂𝑙𝑛

∂θ1n,∂𝑙𝑐

∂θ2 ′

3.4 GOODNESS-OF-FIT TEST

As we obtain the marginal distributions of the underlying asset returns and

combine them into the joint distribution with copula, next we suppose to test whether

the specific distribution for a random variable accurately fits the corresponding

observations. We propose to use Kolmogorov-Smirnov (K-S) test and Anderson-Darling

(A-D) test as our measurement, which belong to the large class of goodness-of-fit tests.

They test the null hypothesis that the populations drawn from two or more

independent samples of data are identical. This test therefore can be used to decide

14

which dependence structure best fit the empirical data, namely the null hypothesis H

0of

same population distributions cannot be rejected. Then we can compare the P-value

with the desired significance level to facilitate a decision about this null hypothesis.

Let x be a set of sample observations. According to the Glivenko–Cantelli theorem,

the empirical cumulative distribution FE will converge to the hypothetical cumulative

distribution FH almost surely. The test statistics of K-S test and A-D test are described

as follows:

DKS = max

t FE xt − FH(xt) (3.13) DAD = F[FE x −FH x ]2

H x [1−FH x ]

x dFH x (3.14) The empirical cumulative distribution FE is defined as

FE(x) =1T Tt=1 Nj=1I(xj,t≤ xj uj∙T ) (3.15)

where I(∙) is the indicator function, u is a vector of marginal probabilities, and xj uj∙T is the uj∙ T th order statistic.

The K-S test is distribution free in the sense that the critical values do not depend

on the specific distribution being tested, and it is more sensitive to deviations in the

center of the distribution. The A-D test introduced by Anderson and Darling (1952,

1954) is a modification of the K-S test that gives more weight to deviations in the tails

than K-S test. By using these two goodness-of-fit tests simultaneously, we could have

more evidence to prove our model selection.

15 3.5 MONTE CARLO SIMULATION

Here we propose to apply a conditional sampling method to simulate draws from a

specific bivariate copula. Given the parameters of each copula function, our task is to

generate pairs of observations (𝑢, 𝑣) of the random vector (𝑈, 𝑉), where 𝑈, 𝑉 are

both independent uniform distribution and their joint distribution function is C. The

main idea of conditional sampling is based on the conditional distribution 𝑐𝑢 𝑣 = Pr(𝐹2 ≤ 𝑣 𝐹1 = 𝑢) = lim

Δ𝑢→∞

𝐶 𝑢+Δ𝑢,𝑣 −𝐶(𝑢,𝑣)

Δ𝑢 =𝜕𝐶𝜕𝑢 = 𝐶𝑢 𝑣 (3.16) where 𝐶𝑢(𝑣) is the partial derivative of the copula. The conditional distribution 𝑐𝑢 𝑣

is a non-decreasing function and exists for all 𝑣 ∈ [0,1].

The general procedure to simulate the desired return process is stated as follows:

(i) Generate two independent random variables (𝑢, 𝑢′) ∈ Uniform(0,1), where 𝑢

is the first desired draw.

(ii) Compute the quasi-inverse function of 𝑐𝑢 𝑣 , which depend on the parameters

of the selected copula and on 𝑢. Set 𝑣 = 𝑐𝑢−1(𝑢′) to obtain the second desired

draw. The following Table 2 reports the quasi-inverse functions of copulas.

(iii) Let 𝐹𝑖 ∙ be the cumulative density function of the standardized marginal

innovations zi,t ~skewed − t zi ηi, ϕi . We take the inverse functions 𝑆𝑇1,𝑡, 𝑆𝑇2,𝑡 = 𝐹−1 𝑢1 , 𝐹−1 𝑢2 as the observation of innovations at time 𝑡.

16

Then calculate the daily asset returns 𝑟1,𝑡, 𝑟2,𝑡 by the following formula:

𝑟𝑖,𝑡 = 𝑟𝑓 −12ℎ𝑖,𝑡−1+ 𝑆𝑇𝑖,𝑡, for 𝑖 ∈ 1,2 , 𝑡 ∈ 1, … , 𝑇 (3.17)

Table 2: Quasi-inverse function of copula function 𝒄𝑢(𝒗)

Gaussian Φ 1 − 𝜌2Φ−1 𝑣 + 𝜌Φ−1 𝑢

Stud𝑒𝑛𝑡’s t

t𝜈 𝜌 t𝜈−1 𝑢 + 𝜈 + t𝜈−1 𝑢 2 × 1 − 𝜌2

𝜈 − 1 t𝜈 +1−1 (𝑣)

Gumbel No closed-form solution

Clayton 𝑣 = u−∝ u′−∝+1∝ − 1 + 1

−1

∝

Frank 𝑣 = −1

∝ln 1 + u′(1 − e−∝) u′ e−∝u− 1 − e−∝u

Note: The inverse function of 𝑐𝑢(𝑣) for Gumbel copula is calculated by solving an equation by numerical way. The details are discussed in the book Copula Methods in Finance, written by Cherubini, Luciano, and Vecchiato, 2004.

(iv) After we have all daily asset returns (𝑟1,𝑡, 𝑟2,𝑡) for 𝑡 = {1, … , 𝑇}, we obtain the

percentage growth (𝑅1,𝑡, 𝑅2,𝑡) of underlying assets defined as:

𝑅i,𝑡 = exp 𝑡𝑗 =1𝑟𝑖,𝑗 , for 𝑖 ∈ 1,2 , 𝑡 ∈ 1, … , 𝑇 (3.18)

Finally, we can calculate the bivariate option prices under different payoff functions

with underlying asset return (𝑅1,𝑇, 𝑅2,𝑇) and count it in one simulation sample.

17

4. D

ATASETS ANDO

PTIONP

AYOFFS

TRUCTURES4.1DATA AND DIAGNOSTIC ANALYSIS

We use several types of indices as proxy for the equity, commodity and foreign

exchange returns with different regions or industries: MSCI Pacific Index and MSCI Far

East Index (cross regions), MSCI World Energy Index and MSCI World Bank Index

(cross industries), Reuters/Jefferies CRB Index and MSCI Latin America Index (cross

assets), S&P 500 Index and DXY currency Index (cross assets). The linear correlations

of each pair of underlying financial assets are shown in Table 3. We would like to

compare the impact of different types of dependence structure to the bivariate options

pricing.

Table 3: The linear correlation of each pair assets

Linear Correlation Pair Composition

Pair 1 0.9828 MSCI Pacific Index and MSCI Far East Index

Pair 2 0.6330 MSCI World Energy Index and MSCI World Bank Index Pair 3 0.4160 Reuters/Jefferies CRB Index and MSCI Latin America Index Pair 4 0.0317 S&P 500 Index and DXY currency Index

All data are collected from Bloomberg over the period from July 1, 2002 to

December 31, 2008. The analysis is based on the logarithm returns of daily closing

prices which exclude non-trading days to ensure that enough observations of the tail of

18 the distributions are available.

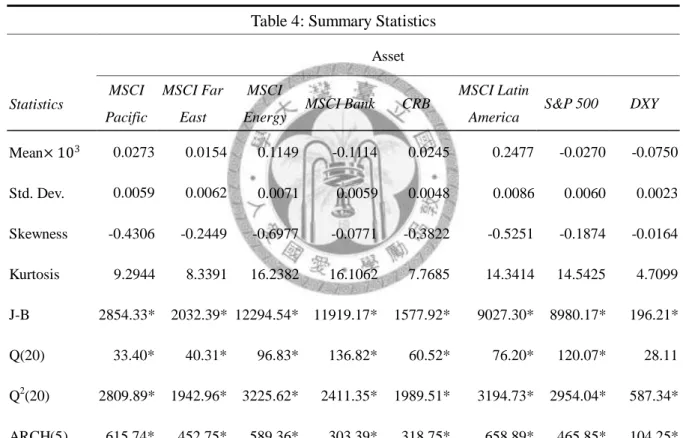

The following Table 4 reports the summary statistics on the returns in the samples.

All of them have apparently skewness and leptokurtotic, which implies the

unconditional distributions of asset returns are asymmetric and fat-tailed. Moreover, the

Jarque-Bera test also shows obviously non-Gaussian characteristic at the 5%

significance level for all underlying assets.

Table 4: Summary Statistics Asset

Statistics MSCI Pacific

MSCI Far East

MSCI

Energy MSCI Bank CRB MSCI Latin

America S&P 500 DXY Mean× 103 0.0273 0.0154 0.1149 -0.1114 0.0245 0.2477 -0.0270 -0.0750 Std. Dev. 0.0059 0.0062 0.0071 0.0059 0.0048 0.0086 0.0060 0.0023 Skewness -0.4306 -0.2449 -0.6977 -0.0771 -0.3822 -0.5251 -0.1874 -0.0164 Kurtosis 9.2944 8.3391 16.2382 16.1062 7.7685 14.3414 14.5425 4.7099 J-B 2854.33* 2032.39* 12294.54* 11919.17* 1577.92* 9027.30* 8980.17* 196.21*

Q(20) 33.40* 40.31* 96.83* 136.82* 60.52* 76.20* 120.07* 28.11 Q2(20) 2809.89* 1942.96* 3225.62* 2411.35* 1989.51* 3194.73* 2954.04* 587.34*

ARCH(5) 615.74* 452.75* 589.36* 303.39* 318.75* 658.89* 465.85* 104.25*

Note: The sample period for the daily logarithm returns runs from July 1, 2002 to December 31, 2008 excluding the holidays. J-B represents the Jarque-Bera test for normality; Q(20) is the Ljung-Box lack-of-fit hypothesis test for up to the 20th order serial correlation in the returns; Q2(20) is the Ljung-Box test for the serial correlation in the squared returns; and ARCH(5) is the LM test for up to the fifth-order ARCH effects. *indicates significance at the 5% level.

19

We also implement the Ljung-Box lack-of-fit hypothesis test, computing the

Q-statistic for autocorrelation lags 20 at the 5% significance level. There are significant

serial correlations in the returns and squared returns for most of samples, but the DXY

Index have no serial correlation in the returns. Moreover, the Engle's ARCH test for up

to the fifth-order shows significant evidence in support of the GARCH effects, or

namely the heteroscedasticity. These statistics support the preliminary hypothesis of

skewed-t GARCH model settings that we discussed before.

4.2OPTION PAYOFF STRUCTURES

We select three types of exotic bivariate options commonly seen in practice, the

digital options, the spread options, and the rainbow options, as our proxy to examine the impact of each dependence structure. Let Xi be the logarithm return at maturity of asset

i ∈ {1,2}, K is the pre-determined strike price, and I ∙ is the indicator function, which

equals 1 if the statement in parentheses holds and zero otherwise. The payoff structures

are shown in Table 5.

Table 5: Bivariate options payoff structures

Option Payoff Structure

Digital Options I(X1> 𝐾 , X2> 𝐾)

Spread Options max(X1− X2− K , 0)

Rainbow Options max max(X1 , X2 − K, 0]

20

5. E

MPIRICALR

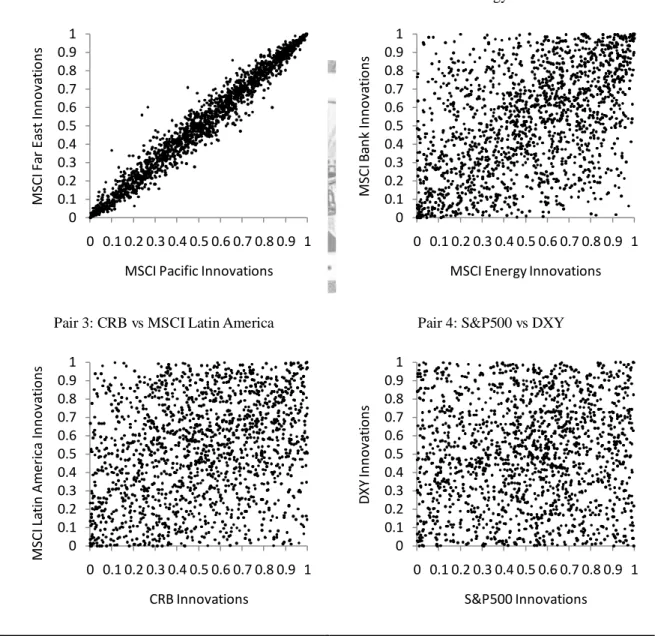

ESULTSWe implement the skewed-t GARCH model to the above dataset and derive the

empirical copula of the standardized GARCH innovations displayed in Figure 1. The

empirical copula would converge to the true copula function under the regularity

condition; for instance, Gaenssler and Stute (1987) or van der Vaart and Wallner (1996).

Figure 1: The empirical copula of the standardized GARCH innovations Pair 1: MSCI Pacific vs MSCI Far East Pair 2: MSCI Energy vs MSCI Bank

Pair 3: CRB vs MSCI Latin America Pair 4: S&P500 vs DXY

Note: The skewed-t GARCH model is described as follows:

ri,t= μi+ εi,t, 0

0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1

MSCI Far East Innovations

MSCI Pacific Innovations

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1

MSCI Bank Innovations

MSCI Energy Innovations

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1

MSCI Latin America Innovations

CRB Innovations

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1

DXY Innovations

S&P500 Innovations

21 hi,t= ωi+ βihi,t−1+ αiεi,t−12 ,

εi,t|ℱt −1 = hi,tzi,t , zi,t~skewed − t zi ηi, ϕi

Then the standardized GARCH innovations for each pair of underlying assets are εi,t hi,t, for 𝑖 ∈ 1,2 and 𝑡 ∈ 1, … , 𝑇 .

We observe that there exists strong positive dependence between the innovations of

first two pairs of assets, particularly in the tails. On the other hand, the innovations of

last two pairs of underlying assets are quite irrelevant and scattered all over the figure.

The dependence structures are dissimilar among these four pairs of assets.

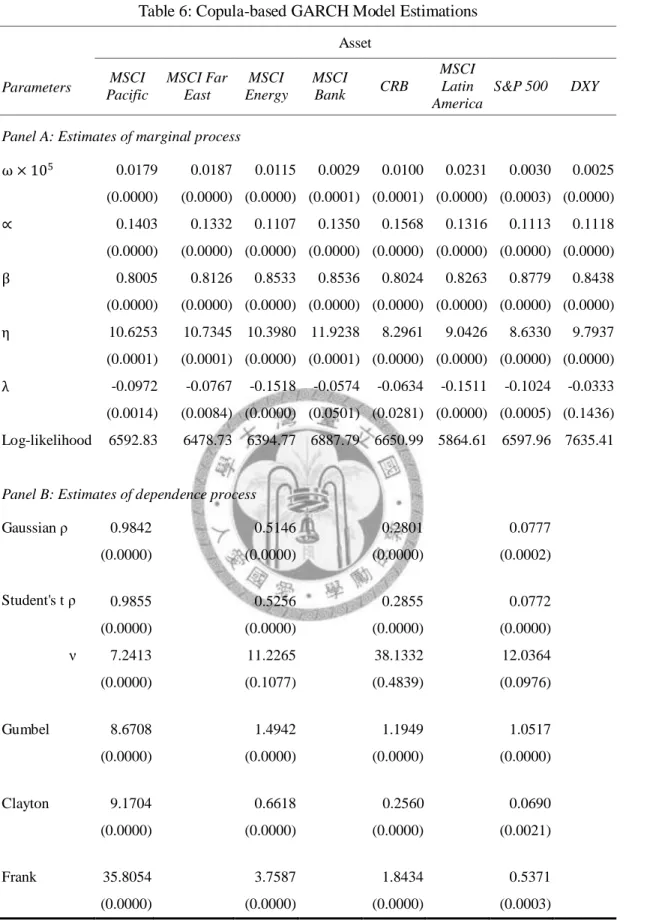

The following Table 6 reports the maximum likelihood estimation results of the

copula-based GARCH model. The estimates of parameters for marginal skewed-t

GARCH process are presented along with the P-values in parentheses in the panel A,

where 0.0000 indicates that the P-value is less than 0.00005.

The value of ω, α and β are all nonnegative that ensure the conditional variance hi,t is positive, and the sum of α and β is close to one for all pairs of assets, which

implies the shocks between the underlying assets have high persistence in volatility and

stationary process. For the estimation of skewed-t distribution, the kurtosis parameter η

and the asymmetry parameter φ show that the conditional process of all assets is

fat-tailed and asymmetric, and this is consistence with previous studies.

The panel B of Table 6 reports the estimates of parameters for different types of

copula functions. All of these estimates are significant under 5% level, except for the

degrees of freedom ν of the last three pairs of Student’s t copulas.

22

Table 6: Copula-based GARCH Model Estimations Asset

Parameters MSCI Pacific

MSCI Far East

MSCI Energy

MSCI

Bank CRB

MSCI Latin America

S&P 500 DXY

Panel A: Estimates of marginal process

ω × 105 0.0179 0.0187 0.0115 0.0029 0.0100 0.0231 0.0030 0.0025 (0.0000) (0.0000) (0.0000) (0.0001) (0.0001) (0.0000) (0.0003) (0.0000)

∝ 0.1403 0.1332 0.1107 0.1350 0.1568 0.1316 0.1113 0.1118 (0.0000) (0.0000) (0.0000) (0.0000) (0.0000) (0.0000) (0.0000) (0.0000) β 0.8005 0.8126 0.8533 0.8536 0.8024 0.8263 0.8779 0.8438 (0.0000) (0.0000) (0.0000) (0.0000) (0.0000) (0.0000) (0.0000) (0.0000) η 10.6253 10.7345 10.3980 11.9238 8.2961 9.0426 8.6330 9.7937 (0.0001) (0.0001) (0.0000) (0.0001) (0.0000) (0.0000) (0.0000) (0.0000) λ -0.0972 -0.0767 -0.1518 -0.0574 -0.0634 -0.1511 -0.1024 -0.0333 (0.0014) (0.0084) (0.0000) (0.0501) (0.0281) (0.0000) (0.0005) (0.1436) Log-likelihood 6592.83 6478.73 6394.77 6887.79 6650.99 5864.61 6597.96 7635.41

Panel B: Estimates of dependence process

Gaussian ρ 0.9842 0.5146 0.2801 0.0777

(0.0000) (0.0000) (0.0000) (0.0002)

Student's t ρ 0.9855 0.5256 0.2855 0.0772

(0.0000) (0.0000) (0.0000) (0.0000)

ν 7.2413 11.2265 38.1332 12.0364

(0.0000) (0.1077) (0.4839) (0.0976)

Gumbel 8.6708 1.4942 1.1949 1.0517

(0.0000) (0.0000) (0.0000) (0.0000)

Clayton 9.1704 0.6618 0.2560 0.0690

(0.0000) (0.0000) (0.0000) (0.0021)

Frank 35.8054 3.7587 1.8434 0.5371

(0.0000) (0.0000) (0.0000) (0.0003)

Note: The values in parentheses are P-values, where 0.0000 indicates that the value is less than 0.00005.

23

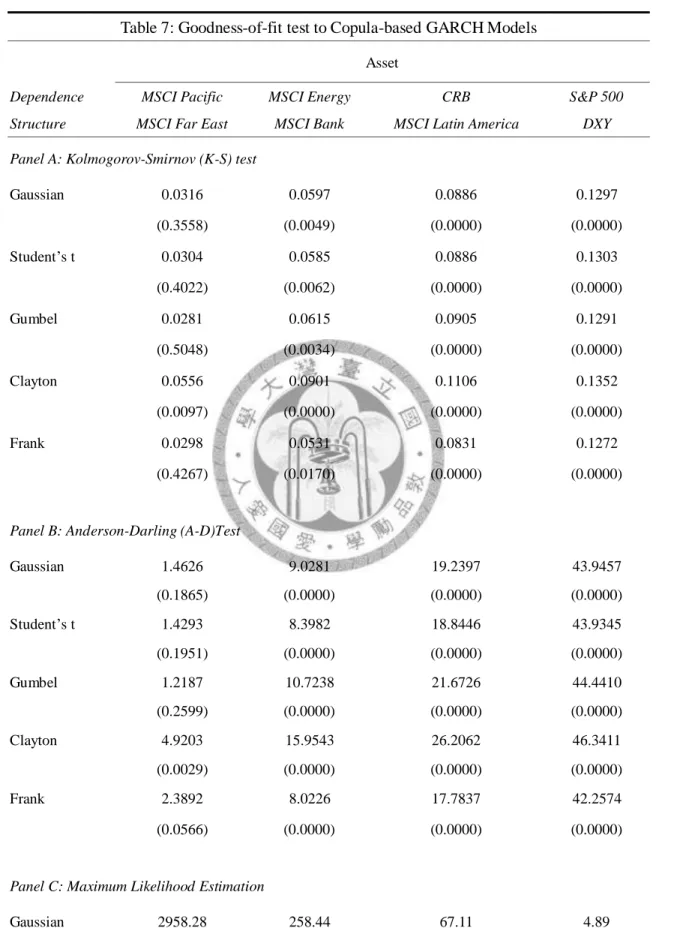

We compare the model goodness-of-fit through the Kolmogorov-Smirnov (K-S)

test and Anderson-Darling (A-D) test along with the P-values in parentheses in Panel A

and B of Table 7. The log-likelihood estimator and Akaike Information Criterion (AIC)

of the above copula estimates are also reported in the Panel C and D of Table 7. The

lower values of the K-S test statistics, A-D test statistics and AIC information criterion

represent better goodness-of-fit. On the contrary, the larger of log-likelihood estimates

indicate better fit.

According to both of the K-S test and A-D test, the first pair of assets, which

components are MSCI Pacific and MSCI Far East Index, has the largest P-value that

means the best model fit under the Gumbel copula function. The Frank copula is the

most ideal model for the second pair of assets, which components are MSCI Energy and

MSCI Bank Index. Although the P-values of these five dependence structures are not

significant enough for the third and fourth pair of assets, the Frank copula is still the

model that relatively describes the dependence structure best based on the empirical

distribution under the K-S and A-D test statistics.

Nevertheless, the inferred conclusion from log-likelihood estimator and AIC

information criterion indicates that the Student’s t is the best dependence structure for

all of these four pairs of asset returns, which obviously contradicted to our above

induction by the K-S and A-D tests. We still choose to apply the K-S and A-D test as our

24

basis to the following bivariate option pricing comparison.

Table 7: Goodness-of-fit test to Copula-based GARCH Models Asset

Dependence Structure

MSCI Pacific MSCI Far East

MSCI Energy MSCI Bank

CRB MSCI Latin America

S&P 500 DXY Panel A: Kolmogorov-Smirnov (K-S) test

Gaussian 0.0316 0.0597 0.0886 0.1297

(0.3558) (0.0049) (0.0000) (0.0000)

Student’s t 0.0304 0.0585 0.0886 0.1303

(0.4022) (0.0062) (0.0000) (0.0000)

Gumbel 0.0281 0.0615 0.0905 0.1291

(0.5048) (0.0034) (0.0000) (0.0000)

Clayton 0.0556 0.0901 0.1106 0.1352

(0.0097) (0.0000) (0.0000) (0.0000)

Frank 0.0298 0.0531 0.0831 0.1272

(0.4267) (0.0170) (0.0000) (0.0000)

Panel B: Anderson-Darling (A-D)Test

Gaussian 1.4626 9.0281 19.2397 43.9457

(0.1865) (0.0000) (0.0000) (0.0000)

Student’s t 1.4293 8.3982 18.8446 43.9345

(0.1951) (0.0000) (0.0000) (0.0000)

Gumbel 1.2187 10.7238 21.6726 44.4410

(0.2599) (0.0000) (0.0000) (0.0000)

Clayton 4.9203 15.9543 26.2062 46.3411

(0.0029) (0.0000) (0.0000) (0.0000)

Frank 2.3892 8.0226 17.7837 42.2574

(0.0566) (0.0000) (0.0000) (0.0000)

Panel C: Maximum Likelihood Estimation

Gaussian 2958.28 258.44 67.11 4.89

25

Student’s t 2999.23 268.76 68.08 13.49

Gumbel 2940.42 238.37 52.00 8.17

Clayton 2322.66 187.30 52.07 5.52

Frank 2854.21 244.85 62.38 5.30

Panel D: Akaike Information Criterion (AIC)

Gaussian -5914.57 -514.89 -132.23 -7.77

Student’s t -5996.46 -535.52 -134.16 -24.98

Gumbel -5878.84 -474.74 -102.00 -14.33

Clayton -4643.33 -372.59 -102.14 -9.03

Frank -5706.42 -487.69 -122.76 -8.60

Note: The test statistics of K-S test and A-D test are described as follows:

DKS= max

t FE xt − FH(xt) DAD = F[FE x −FH x ]2

H x [1−FH x ]

x dFH x .

The copula estimates in Table 5.1 are implemented in the hypothetical cumulative distribution FH and the empirical cumulative distribution FE is defined as

FE(x) =1

T Tt=1 Nj=1I(xj,t≤ xj uj∙T )

where I(∙) is the indicator function, u is a vector of marginal probabilities, and xj uj∙T is the uj∙ T th order statistic. Besides, the values in parentheses are P-values, where 0.0000 indicates that the value is less than 0.00005.

After we derive all desired parameter estimates, we simulate the asset return

process that given the parameters of skewed-t GARCH model and copula functions.

Especially we apply the parameter estimates of each marginal skew-t GARCH process

with initial conditional volatility hi,0 equals the long-term variance level ωi 1 − αi− βi . The estimates of Gaussian, Student’s t, Gumbel, Clayton and Frank

copula functions are also implemented to simulate different types of dependence

26

structure. To ensure the convergence of simulated option prices, we simulate 10,000

times and assume that the initial underlying asset return equals one for each return

process.

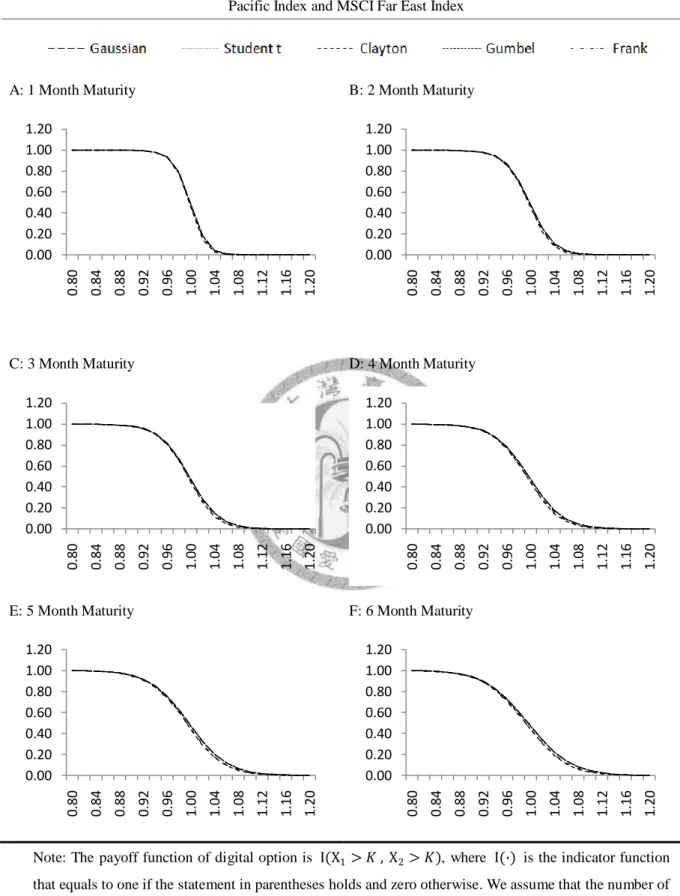

The following Figure 2 reports the simulation results of digital option pricing of

MSCI Pacific Index and MSCI Far East Index with different strike prices K from 0.80 to

1.20 and different time-to-maturity T from one to six months. We also fix the strike

price K to divide them into three groups of in-the-money (ITM), at-the-money (ATM)

and out-of-the-money (OTM) respectively in Figure 3.

The differences of digital option price between each type of dependence structure

tend to become wider when the maturity increases and the initial bivariate option prices

are around at-the-money. However, the tendency of price change is not very obvious,

and the same situation happens both for the spread options and rainbow options

displayed in Figure 4 to 6.

In order to confirm whether the differences among these bivariate option prices are

significant or not, we perform a paired t-test of the null hypothesis that the 10,000 times

simulated asset returns in the difference between each pairs of dependence structures are

a random sample from a normal distribution with mean zero and unknown variance,

against the alternative that the mean is not zero.

27

Figure 1:Digital Option Pricing Result Under Different Copulas vs. Different Strike Prices - Pair 1- MSCI Pacific Index and MSCI Far East Index

A: 1 Month Maturity B: 2 Month Maturity

C: 3 Month Maturity D: 4 Month Maturity

E: 5 Month Maturity F: 6 Month Maturity

Note: The payoff function of digital option is I(X1> 𝐾 , X2> 𝐾), where I(∙) is the indicator function that equals to one if the statement in parentheses holds and zero otherwise. We assume that the number of trading days for a month is twenty days.

0.00 0.20 0.40 0.60 0.80 1.00 1.20

0.80 0.84 0.88 0.92 0.96 1.00 1.04 1.08 1.12 1.16 1.20

0.00 0.20 0.40 0.60 0.80 1.00 1.20

0.80 0.84 0.88 0.92 0.96 1.00 1.04 1.08 1.12 1.16 1.20

0.00 0.20 0.40 0.60 0.80 1.00 1.20

0.80 0.84 0.88 0.92 0.96 1.00 1.04 1.08 1.12 1.16 1.20

0.00 0.20 0.40 0.60 0.80 1.00 1.20

0.80 0.84 0.88 0.92 0.96 1.00 1.04 1.08 1.12 1.16 1.20

0.00 0.20 0.40 0.60 0.80 1.00 1.20

0.80 0.84 0.88 0.92 0.96 1.00 1.04 1.08 1.12 1.16 1.20

0.00 0.20 0.40 0.60 0.80 1.00 1.20

0.80 0.84 0.88 0.92 0.96 1.00 1.04 1.08 1.12 1.16 1.20

28

Figure 2: Digital Option Price Result Under Different Copulas vs. Different Time to Maturities - Pair 1- MSCI Pacific Index and MSCI Far East Index

ITM (𝐾 = 0.9) ATM (𝐾 = 1) OTM (𝐾 = 1.1)

Note: ITM, ATM and OTM represent that the digital option is in-the-money, at-the-money and out-of-the-money respectively. Since both the underlying asset returns are set to start at the same value 1 in the simulation process, ATM indicates that 𝐾 equals to 1, ITM indicates that K is less than 1 and OTM indicates that K is larger than 1.

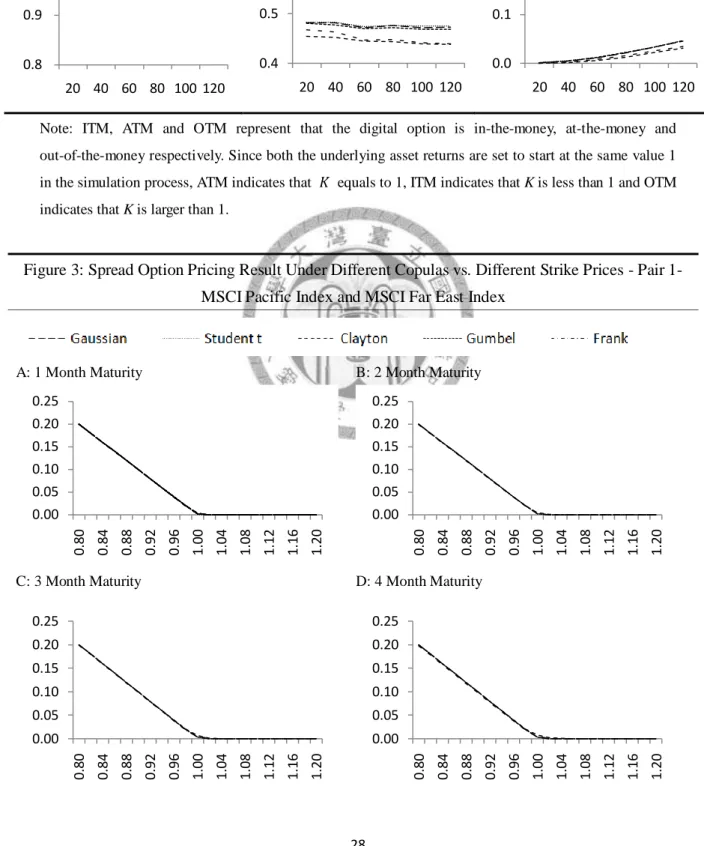

Figure 3: Spread Option Pricing Result Under Different Copulas vs. Different Strike Prices - Pair 1- MSCI Pacific Index and MSCI Far East Index

A: 1 Month Maturity B: 2 Month Maturity

C: 3 Month Maturity D: 4 Month Maturity

0.8 0.9 1.0

20 40 60 80 100 120

0.4 0.5 0.6

20 40 60 80 100 120 0.0 0.1 0.2

20 40 60 80 100 120

0.00 0.05 0.10 0.15 0.20 0.25

0.80 0.84 0.88 0.92 0.96 1.00 1.04 1.08 1.12 1.16 1.20

0.00 0.05 0.10 0.15 0.20 0.25

0.80 0.84 0.88 0.92 0.96 1.00 1.04 1.08 1.12 1.16 1.20

0.00 0.05 0.10 0.15 0.20 0.25

0.80 0.84 0.88 0.92 0.96 1.00 1.04 1.08 1.12 1.16 1.20

0.00 0.05 0.10 0.15 0.20 0.25

0.80 0.84 0.88 0.92 0.96 1.00 1.04 1.08 1.12 1.16 1.20

29

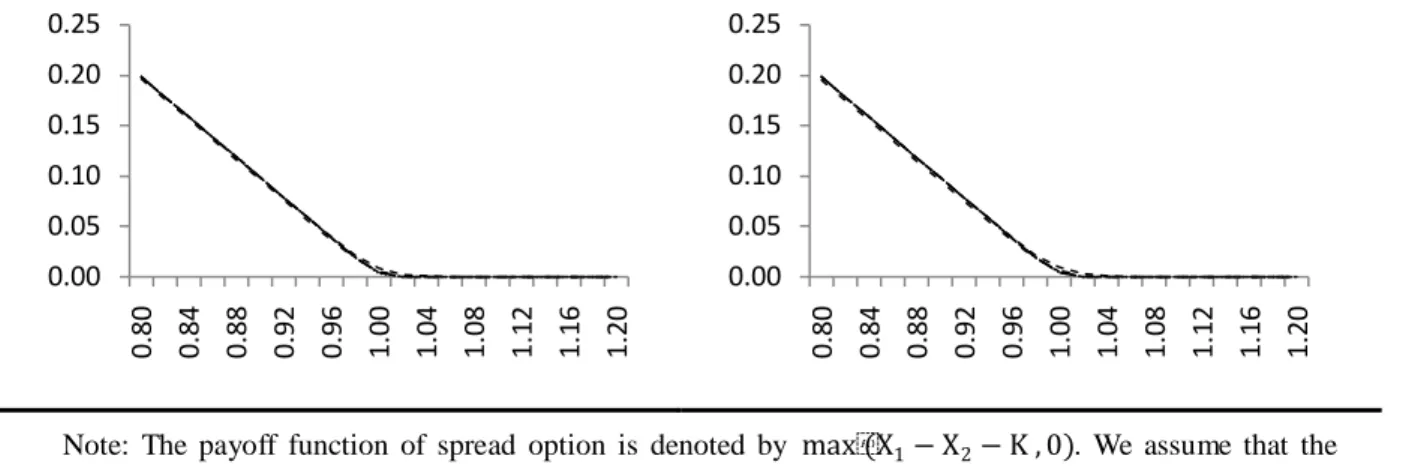

E: 5 Month Maturity F: 6 Month Maturity

Note: The payoff function of spread option is denoted by max(X1− X2− K , 0). We assume that the number of trading days for a month is twenty days.

Figure 4: Spread Option Price Result Under Different Copulas vs. Different Time to Maturities - Pair 1- MSCI Pacific Index and MSCI Far East Index

ITM (𝐾 = −0.1) ATM (𝐾 = 0) OTM (𝐾 = 0.1)

Figure 5: Rainbow Option Pricing Result Under Different Copulas vs. Different Strike Prices - Pair 1- MSCI Pacific Index and MSCI Far East Index

A: 1 Month Maturity B: 2 Month Maturity

0.00 0.05 0.10 0.15 0.20 0.25

0.80 0.84 0.88 0.92 0.96 1.00 1.04 1.08 1.12 1.16 1.20

0.00 0.05 0.10 0.15 0.20 0.25

0.80 0.84 0.88 0.92 0.96 1.00 1.04 1.08 1.12 1.16 1.20

0.09 0.10 0.11

20 40 60 80 100 120

0.00 0.01 0.02

20 40 60 80 100 120

0.00 0.01 0.02

20 40 60 80 100 120

0.00 0.05 0.10 0.15 0.20 0.25

0.80 0.84 0.88 0.92 0.96 1.00 1.04 1.08 1.12 1.16 1.20

0.00 0.05 0.10 0.15 0.20 0.25

0.80 0.84 0.88 0.92 0.96 1.00 1.04 1.08 1.12 1.16 1.20

30

C: 3 Month Maturity D: 4 Month Maturity

E: 5 Month Maturity F: 6 Month Maturity

Note: The payoff function of rainbow option is max max(X1 , X2 − K, 0]. We assume that the number of trading days for a month is twenty days.

Figure 6: Rainbow Option Price Result Under Different Copulas vs. Different Time to Maturities - Pair 1- MSCI Pacific Index and MSCI Far East Index

ITM (𝐾 = 0.9) ATM (𝐾 = 1) OTM (𝐾 = 1.1)

The paired t-test results among all of dependence structures with one and six

month time-to-maturity are reported in Table 8 and 9 respectively. According to our

previous goodness-of-fit tests, we take the Gumbel copula that best describes the 0.00

0.05 0.10 0.15 0.20 0.25

0.80 0.84 0.88 0.92 0.96 1.00 1.04 1.08 1.12 1.16 1.20

0.00 0.05 0.10 0.15 0.20 0.25

0.80 0.84 0.88 0.92 0.96 1.00 1.04 1.08 1.12 1.16 1.20

0.00 0.05 0.10 0.15 0.20 0.25

0.80 0.84 0.88 0.92 0.96 1.00 1.04 1.08 1.12 1.16 1.20

0.00 0.05 0.10 0.15 0.20 0.25

0.80 0.84 0.88 0.92 0.96 1.00 1.04 1.08 1.12 1.16 1.20

0.10 0.11 0.12

20 40 60 80 100 120

0.01 0.02 0.03

20 40 60 80 100 120

0.00 0.01 0.02

20 40 60 80 100 120

31

dependence structure between the returns of MSCI Pacific and MSCI Far East Index as

our basis model for the comparison.

In the scenario of one month time-to-maturity in Table 8, the difference between

each pairs of dependence structures are significant under 5% level, except that the

digital and rainbow option prices between Gumbel copula and Gaussian copula are not.

However, the price differences among each pairs of dependence structure become more

significant except for the rainbow option price between Gumbel copula and Frank

copula in the scenario of six months time-to-maturity. The results of paired t-test

support our previous observation that the differences between the bivariate options

prices are more significant as the time-to-maturity increases.

Table 8: T test for the distance between the ATM (K=1) option prices of different dependence structures with 1 month time-to-maturity - Pair 1- MSCI Pacific Index and MSCI Far East Index

Panel 1: Digital Option

Student’s t Clayton Gumbel Frank

Gaussian -0.0009 0.0267 0.0014 0.0138

(0.0833) (0.0000) (0.1221) (0.0000)

Student’s t 0.0276 0.0023 0.0147

(0.0000) (0.0116) (0.0000)

Clayton -0.0253 -0.0129

(0.0000) (0.0000)

Gumbel 0.0124

(0.0000)

32 Panel 2: Spread Option

Student t Clayton Gumbel Frank

Gaussian 0.0001 -0.0018 -0.0003 -0.0009

(0.0000) (0.0000) (0.0000) (0.0000)

Student’s t -0.0019 -0.0003 -0.0009

(0.0000) (0.0000) (0.0000)

Clayton 0.0016 0.0010

(0.0000) (0.0000)

Gumbel -0.0006

(0.0000) Panel 3: Rainbow Option

Student t Clayton Gumbel Frank

Gaussian 0.0000 -0.0014 0.0000 -0.0002

(0.0000) (0.0000) (0.4577) (0.0000)

Student’s t -0.0014 0.0000 -0.0002

(0.0000) (0.0001) (0.0000)

Clayton 0.0014 0.0012

(0.0000) (0.0000)

Gumbel -0.0002

(0.0000)

Note: The table reports the distance between the ATM (K=1) bivariate option prices of different dependence structures with 1 months time-to-maturity for the first pair of assets returns, which components are MSCI Pacific and MSCI Far East Index. The values in parentheses are p-values under the paired t tests.

Table 9: T test for the distance between the ATM (K=1) option prices of different dependence structures with 6 months time-to-maturity - Pair 1- MSCI Pacific Index and MSCI Far East Index

Panel 1: Digital Option

Student’s t Clayton Gumbel Frank

Gaussian -0.0014 0.0352 0.0048 0.0333

(0.0163) (0.0000) (0.0000) (0.0000)

33

Student’s t 0.0366 0.0062 0.0347

(0.0000) (0.0000) (0.0000)

Clayton -0.0304 -0.0019

(0.0000) (0.4016)

Gumbel 0.0285

(0.0000) Panel 2: Spread Option

Student t Clayton Gumbel Frank

Gaussian 0.0002 -0.0051 -0.0007 -0.0019

(0.0000) (0.0000) (0.0000) (0.0000)

Student’s t -0.0053 -0.0009 -0.0021

(0.0000) (0.0000) (0.0000)

Clayton 0.0044 0.0031

(0.0000) (0.0000)

Gumbel -0.0012

(0.0000) Panel 3: Rainbow Option

Student t Clayton Gumbel Frank

Gaussian 0.0001 -0.0035 -0.0001 -0.0002

(0.0000) (0.0000) (0.0000) (0.0009)

Student’s t -0.0036 -0.0002 -0.0003

(0.0000) (0.0000) (0.0000)

Clayton 0.0033 0.0033

(0.0000) (0.0000)

Gumbel -0.0001

(0.2549) Note: The table reports the distance between the ATM (K=1) bivariate option prices of different dependence structures with 6 months time-to-maturity for the first pair of assets returns, which components are MSCI Pacific and MSCI Far East Index. The values in parentheses are p-values under the paired t tests.