1

Using Fuzzy Regression and Neural Network to

Predict Organizational Performance

Liang-Hung Lin

11Department of International Business, National Kaohsiung University of Applied Sciences 415 Chien Kung Road, Kaohsiung 807, Taiwan, ROC.

Abstract

As everyone knows, multiple regression analysis is an important approach to prediction studies. However, regression model has some limitations and constraints in the real world practices. This study applied fuzzy regression using neural network (FRNN) to predict organizational performance, and the findings indicate that the accuracy rate analysis supported FRNN to be a better method to predict nonlinear variables.

1. Introduction

In both manufacturing and service sectors, new approaches to innovation management have become prime drivers of various industries. As product life cycles condense and substitutive product offerings expand, product innovation becomes increasingly outstanding for establishing sustainable competitive advantage. Thus, no matter scholars, managers, shareholders, and investors desire to know and to predict organizational performance on innovation and corporate profit rate. They are really critical indexes to forecast the firms’ profits and developments. As everyone knows, multiple regression analysis is an important approach to prediction studies. However, regression model has some limitations and constraints in the real world practices and

applications. For example, nonconstancy of error variance, presence of outliers, nonindependence of error terms, and nonnormality of error terms present four common constraints of multiple regression models [1]. Moreover, data scale and nonlinear relationships show two other limitations of traditional linear model for data analyses. Applying fuzzy theory and neural network, this study wishes to improve the prediction performance on organizational innovativeness.

2. Determinants of Performance

This study adopted two criteria to measure organizational performance: profit rate and organizational innovation. The former measures firms’ capability to exist; and the later measures firms’ capability to grow and develop. The definition and classification of innovation vary among the various studies. Scholars asserted that innovation involves invention and commercialization. Other studies considered that innovations include new products, services or production processes introduced by firms. From the perspective of management, they described innovation as the creation of value from knowledge or information. Recently from an organizational perspective, innovation has been defined as the adoption of an internally

4 determinants of organizational performance:

Organizational culture to innovate. Product line development.

Price of product Guanxi with other firms Employee wage

Environmental management and forecast ability for top managers

Leadership of top management

Environmental protection ability for the firm.

4. Results

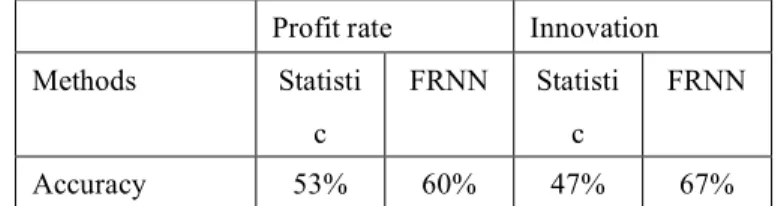

Adopting multiple regression analyses to predict organizational innovation and profit rate, we found that product line development, employee wage, and environmental management and forecast ability for top managers are three significant determinants for profit rate (with F = 1.59, p = 0.174, R-sq = 0.31); culture to innovate, product line development, and guanxi with other firms are significant determinants for innovation (with F = 1.69, p = 0.16, R-sq = 0.32). However, the linear regression results do not work well. So we applied FRNN to predict organizational performance. The results are shown in Table 1. Please note that accuracy rate for prediction means that the testing sample was include in the 95% prediction interval. 52 samples was divided into training sample (37) and testing sample (15).

This study indicates that the accuracy rate for both dependent variable supported FRNN to be a better method to predict nonlinear variables. However, only traditional linear regression can indicate which independent variable to be significant in the model. Analyzing two methods at the same time seems to provide complete

information for managers.

Profit rate Innovation

Methods Statisti c FRNN Statisti c FRNN Accuracy 53% 60% 47% 67%

Table 1. Summary report for the results of linear regression (Statistic) and FRNN

5. References

[1] J. Neter, M. Kutner, C. Nachtsheim, and W, Wasserman, Applied Linear Regression

Models. New York: McGraw-Hill, 1999.

[2] F. Damanpour, “Organizational innovation: a meta-analysis of effects of determinants and moderators,” Academy of Management

Journal, Vol. 34(3), pp. 555–590, 1991.

[3] T.M. Amabile, M.R. Conti, H. Coon, J. Lazenby, and M. Herron, “Assessing the work environment for creativity”, Academy

of Management Journal, Vol. 39(5), pp.

1154-1184, 1996

[4] J. Watada, and Y. Yabuuchi, “Fuzzy Robust Regression Analysis,” IEEE International

Engineering Management Conference,1994.

[5] J. Sanchez, and A. Gomez, “Estimating a Fuzzy Term Structure of Interest Rate Using Fuzzy Regression,” European Journal of

Operational Research, Vol. 154, pp.

154-174, 2004.

[6] H. Ishibuchi, and H. Tanaka.,“Fuzzy Regression Analysis Using Neural Networks,” Fuzzy Sets and Systems, pp.257-265, 1992