國立高雄大學國際商業管理碩士學位學程

碩士論文

台灣捷運系統對房價的影響

The Impact of Taiwan MRT System on Housing

Prices

研究生:石睿凡撰

指導教授:耿紹勛

致謝詞

就讀研究所的這段期間,有這許多人的幫忙,才能如此順利地撰寫論文並完成 學業。其中最感謝耿紹勛老師耐心地指導我這位外語系畢業的學生,在如期完成碩 士論文的同時,讓我學習了完全不同於大學所學的研究方法及思維。同時也相當感 謝余歆儀老師及陳立文老師在百忙之中,撥空當任我的口試委員,使我能夠順利完 成口試。 感謝曾經教導過我的老師,讓我能在商業管理的這個領域汲取更多知識。也感 謝所上的同學對我的照顧及扶持,我才能如此融入及適應研究所的生活。最後感謝 家人一路的支持及鼓勵,讓我求學過程十分順遂,無後顧之憂地完成碩士學位。i

Content

ABSTRACT ... ii

I. Introduction ... 1

II. Literature Review ... 2

III. Data ... 5

IV. Models ... 10

V. Empirical Analysis and Results ... 12

VI. Conclusions ... 20

ii

The Impact of Taiwan MRT System on Housing Prices

Advisor(s): Dr. Shao-Hsun Keng Department of Applied Economics

National University of Kaohsiung

Student: Jui-Fan Shih IMBA

National University of Kaohsiung

ABSTRACT

MRT system has become the most important transportation for people living in Taipei and Kaohsiung. Many studies have shown that when the distance to public transportation increases, the housing prices decline. While earlier studies examine the effect of the distance to MRT station on housing prices focusing only on one city or one transportation line, this study estimates the effect of the distance to MRT station on housing prices by including the entire MRT lines in Taipei and Kaohsiung. Moreover, we compare the difference in the effect between these two cities.

The results indicate that when the distance to MRT station increases by 1 km, the housing prices decrease by $NT158,432 per ping. When the sample expands to include houses within 3km of the MRT stations, the housing prices decrease by $NT119,468 if the distance to MRT station increases by 1 km. We also show that the relationship between the housing prices and distance to MRT stations is a U shape. The results also show that the distance to the MRT system in Taipei has a greater impact on housing prices than that in Kaohsiung.

1 I. Introduction

As cities grow, public transportation becomes a key factor that affects the urban

development significantly. With a growing number of people move to big cities, traffic

congestion has emerged to be a key issue facing many cities. The Mass Rapid Transit

(MRT) is the main strategy undertaken by many cities to mitigate the problem of traffic

congestion. MRT is an important transportation system developed over the past 20 years

in Taiwan, especially for people who live in the metropolitan areas. With the MRT, people

are able to live in suburban areas without losing the convenience of the big cities.

Consequently, MRT system can not only relieve the pressure of overcrowding in cities

but also expand the boundary of the cities.

In this study, we examine the impact of the distance to MRT station on housing prices

in Taiwan. The research is important because MRT system has become a necessity for

city dwellers and consequently affects the housing price substantially. However, previous

studies focused on the effect of the distance to MRT stations on housing prices either on

a single city or on a single transportation line. Consequently, in this study, we not only

estimate the effect of the distance to MRT stations on housing prices by including all MRT

2 II. Literature Review

The MRT system provides convenient transportation for traveling in the city. Due to

traffic congestion and the difficulty of finding a parking space in urban areas, the distance

to the MRT station has become a key determinant of property values in the city. Bajic

(1983) identified the impact of a subway line in Toronto on the housing prices. The result

showed that the direct savings in commuting from taking the subway should have been

reflected in the housing values. The average amount of savings is estimated to be around

$ US 2,273.

Coffam and Gregson (1998) estimated the impact of the railway on land prices in Knox

County, Illinois. The empirical results suggest that the value of lands increases when the

lands are closer to railroads. The value of lands closer to the railroads is 9% higher than

those that are not. Bowes and Ihlanfeldt (2001) found that proximity to the railroad station,

business activities and crime rates in the neighborhood, affect property values

significantly.

McMillan and McDonald (2004) examined the impact of the completion of rapid transit

line from downtown Chicago to Midway Airport on the prices of single-family houses.

The results show that housing prices are affected by the proximity to subway stations.

3

compared with the real estate far away from transit station between 1986 and 1999.

Armstrong and Rodriguez (2006) suggested that housing prices are 9.6% to 10.1%

higher when residential properties are located within 0.5 miles of the station in Eastern

Massachusetts. In addition, the property values decrease 1.6% for every additional minute

of driving to the railroad station. Dewee (1976) showed that housing prices in Toronto

decrease when the distance to the subway stations increases and distance is one-third of

a mile from the stations.

Debrezion et al. (2007) found that the effects of railway stations on the values of the

commercial property are limited to short distances from the stations. In their study, there

are two different effects to estimate the railway station proximity. The first one is local

station effect, which measures the effect of distance within 0.25 mile from the station.

The second one is the global station effect that measures the effect of coming 250 meters

to the stations.

The empirical results showed that within 0.25 mile from the station, the residential

property value is 12.2% less expensive than commercial property. However, they also

found that at longer distances the effect on residential property values dominates. The

estimates suggested that the value of the residential property is 2.3% higher than that of

4

Damm et al. (1980) used data from Washington Metro and found that property values

are negatively related to the distance to the station. When the distance to a station

increases by 0.1 miles, the rent of an apartment will fall by 2.5% in Washington D.C.

(Benjamin and Sirmans, 1996). Kilpatrick et al. (2007) examine the impact of transit

corridor on the housing prices and the result reveals that proximity to the transit corridor

alone without direct access has negative impact on nearby housing prices

Chernobai et al. (2011) used Spline Regression to estimate the effect of highway on

housing prices in Los Angeles. They found that housing prices show a convex relationship

to the distance to highway. Waddell et al. (1993) also showed that the relationship between

housing prices and the distance of the station is U shape. They used a nonlinear model to

estimate the effect of the distance to the station on land value. The locations of MRT

stations have a different impact on land value. For instance, in downtown Chicago, the

17% increase in the values of residential lands within 1.5 miles from the station can be

attributed to the transit. (McDonald and Osuji, 1995).

In Taiwan, previous studies have shown that MRT system has a significant effect on

housing prices. Penget al. (2009) examined the effect of the completion of Taipei MRT

Red Line on housing prices. The results revealed that the values of houses adjacent to

5

Hong and Lin (1999) estimated the impact of Taipei MRT system and the road width

on housing prices in Taipei. They found that the road width does have a positive effect on

housing prices. Moreover, housing prices increase significantly in the area close to the

MRT stations. More importantly, the relationship between housing prices and the distance

to MRT station is convex.

Tai (2011) also use Taipei MRT System to show that the price effect of MRT station is

nonlinear. Meanwhile, the impact of MRT station is not the same in each distance interval.

Also, there are differences between urban and suburb area. The result showed that the

distance to MRT is station is within 300 meters, the impact on housing prices is more

statistically significant. Moreover, the results also showed that the closer the property lies

within the suburb area, the greater the effect to the housing prices is.

Feng et al. (1994) indicated that the distance to MRT station has a greater effect on

housing prices in downtown. Housing prices in the central business district usually

increase more than the housing price in the outskirt of the central business district and

suburban area. In addition, the increase in the value of land for commercial and office

purpose is greater than that for residential use.

III. Data

6

Kaohsiung collected by Ministry of Interior (Taiwan) from September 2012 to October

2017. The data includes housing prices, the age of the house, size of the house, time

variable and the property type.

All prices are adjusted by CPI and the base year is 2017. In this study, we assume that

the farthest walking distance to the station that can impact housing prices is 3 km. When

the distance exceeds 3 km, the effect of MRT system on housing prices should be small.

To check for robustness, we also examine the impact of walk distance to MRT station on

housing prices with 1.5 km. Because we have the address of the house, we can find the

shortest distance of the property to the MRT station by using Google map.

In addition, we set five-year dummy variables to estimate the time variables from 2012

to 2017 (the base year is 2017). When the transaction year was 2012, YR2012 equals to

one and zero otherwise. Other time dummies are defined similarly. We also set a dummy

variable for Taipei and Kaohsiung. When the observation is from Taipei, then Taipei=1

and 0 otherwise.

There are eight property types listed in the data which are building higher than 11 floors,

building lower than 10 floors, condominium, single-family house, studio apartment,

storefront, commercial and office building and others. We create seven dummy variables

7

In addition, there are missing values for the age of the house. We create a missing

dummy whose value equals 1 if the age of the house is missing and 0 otherwise. At the

same time, we set the age of the house to 0 for observations with missing values. The

final sample of our analyses is 2244.

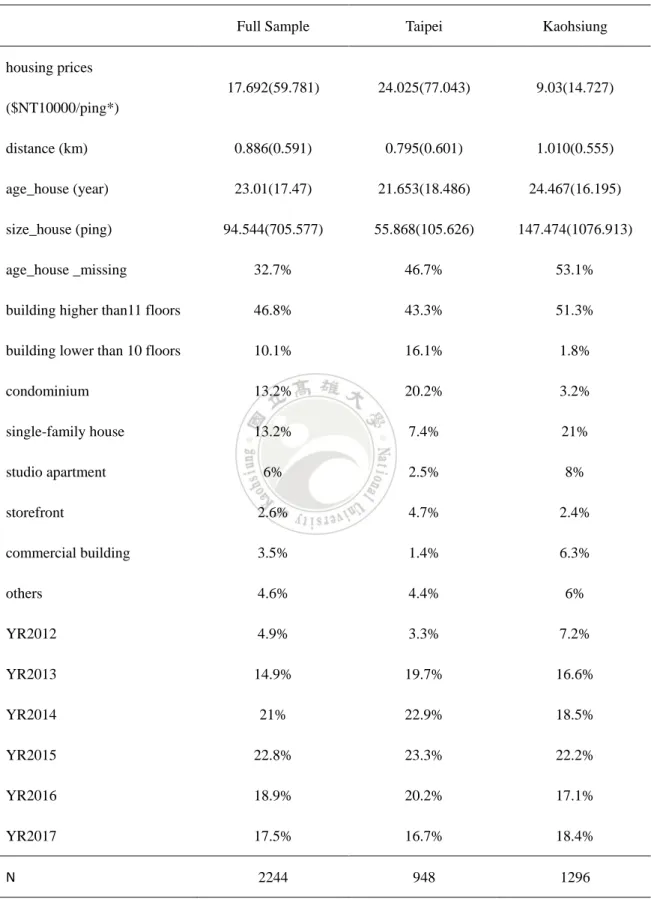

Table 1 is the descriptive statistics of the sample. The average housing prices are

$NT176,920/ping (1 ping = 3.306 square meters); the mean distance to MRT station is

around 0.886 km; the average age of the house is around 23.01 years; twenty-three percent

of our sample has a missing value in the age of the house. The average size of the house

is around 94.544 pings.

If we look at the property types, building higher than 11 floors accounts for 47% of the

sample; condominium and single-family house both account for 13.2 percent; building

lower than 10 floors accounts for 10.1 percent; studio apartment occupies 0.6 percent;

others occupies 4.6 percent; commercial and office building is at 3.5 percent and storefront

is at 2.6 percent.

When we divide the sample into Taipei and Kaohsiung, the estimates show that Taipei

has higher housing prices ($NT240,250/ping > $NT90,300/ping). The average distance

8

Table 1. Definitions, Sample means and Standard deviations of Variables

Full Sample Taipei Kaohsiung

housing prices ($NT10000/ping*) 17.692(59.781) 24.025(77.043) 9.03(14.727) distance (km) 0.886(0.591) 0.795(0.601) 1.010(0.555) age_house (year) 23.01(17.47) 21.653(18.486) 24.467(16.195) size_house (ping) 94.544(705.577) 55.868(105.626) 147.474(1076.913) age_house _missing 32.7% 46.7% 53.1%

building higher than11 floors 46.8% 43.3% 51.3%

building lower than 10 floors 10.1% 16.1% 1.8%

condominium 13.2% 20.2% 3.2% single-family house 13.2% 7.4% 21% studio apartment 6% 2.5% 8% storefront 2.6% 4.7% 2.4% commercial building 3.5% 1.4% 6.3% others 4.6% 4.4% 6% YR2012 4.9% 3.3% 7.2% YR2013 14.9% 19.7% 16.6% YR2014 21% 22.9% 18.5% YR2015 22.8% 23.3% 22.2% YR2016 18.9% 20.2% 17.1% YR2017 17.5% 16.7% 18.4% N 2244 948 1296

9

1.009 km in Kaohsiung. The reason is that the MRT system in Taipei is more extensive

as well as having more lines and stations, compare with Kaohsiung. Thus, the distance to

MRT station in Taipei is shorter.

Houses in Taipei are newer than those in Kaohsiung. The average age of the house is

21.65 years, compared with 24.46 years in Kaohsiung. On the other hand, the size of the

house in Taipei is smaller as well (55.868 pings< 147.474 pings).

The size of the houses in Kaohsiung is bigger than Taipei because the sample of

Kaohsiung contains many transactions of factories and the size of most factories are more

than 200 pings; therefore, the average size of the house is inflated in Kaohsiung

The percentage of building higher than 11 floors is 43% and 51% in Taipei and

Kaohsiung respectively. Building lower than 10 floors with elevator accounts for 16.1%

of the observations in Taipei and 1.8% of the observations in Kaohsiung. Condominium

in Taipei accounts for a higher percentage (20.2%) than in Kaohsiung (3.2%). The

percentage of a single-family house in Taipei is 7.4%, which is lower than the 21% in

Kaohsiung.

Studio apartment accounts for 4.5% and 8% of the sample in Taipei and Kaohsiung

respectively. The percentage of storefront properties in Taipei is 2.7% which is slightly

10

6.2% in Kaohsiung. Others have 4.4% in Taipei and 0.6% in Kaohsiung.

There are 948 observations from Taipei and 1296 from Kaohsiung. The reason why the

number of observation from Taipei is lower than that from Kaohsiung is that house

owners in Taipei don’t want to reveal actual selling prices to the government even though

they will be subject to a fine ranging from $NT30,000 to $NT150,000 per year for failing

to reveal actual selling prices.

IV. Models

We use multiple regression analysis to examine the relationship between housing prices

and the distance to MRT station in Greater Taipei and Kaohsiung. The basic multiple

regression models take the following form:

Price = β0 + β1distance + β2distance2+ β3distance × Taipei + β4distance2×

Taipei + β5age_house + β6age_house_missing + β7size_house + 𝛽𝛽8 Taipei +

𝛽𝛽9bht11 + 𝛽𝛽10blt10 + 𝛽𝛽11condo + 𝛽𝛽12studio + 𝛽𝛽13store + 𝛽𝛽14commercial +

𝛽𝛽15others + 𝛽𝛽16𝑌𝑌𝑌𝑌2012+ 𝛽𝛽17𝑌𝑌𝑌𝑌2013+ 𝛽𝛽18𝑌𝑌𝑌𝑌2014+ 𝛽𝛽19𝑌𝑌𝑌𝑌2015+ 𝛽𝛽20𝑌𝑌𝑌𝑌2016+ 𝜀𝜀

---(1)

Price is housing price per ping adjusted for CPI and the base year is 2017. One ping is

equal to 3.306 square meters. Distance is the distance to station measured in kilometers

11

inverse U shape. Taipei is a dummy variable that equals 1 if the observation is from Taipei

area and 0 otherwise. In addition, distance × Taipei indicates the different effects of

distance on housing prices between Taipei and Kaohsiung. Distance2× Taipei helps

us to know the different decreasing rate of housing prices between Taipei and Kaohsiung.

Age_house is the age of the house which is measured in years. Because there are 33%

of the observations with the age of the house are missing. We use a dummy variable to

cope with the missing values. When the age of the house is missing, then it equals to one

and 0 otherwise. In addition, we set the age of the house to 0 for observations with missing

age. The size_ house is the size of the property and the unit is ping.

Bht11 means the building is higher than 11 floors with elevator. Blt10 means the

building is 10 or lower than 10 floors with elevator. Condo means condominium. Studio

means studio apartment. Store means storefront. Commercial means commercial building.

Others mean other property types such as factory or warehouse. These variables are

dummy variables we create and we set single-family house as the base group. 𝑌𝑌𝑌𝑌2012 to

𝑌𝑌𝑌𝑌2016 are five year dummy variables and the base year is 2017.

According to the regression models above, we can examine the impact of distance on

12 V. Empirical Analysis and Results

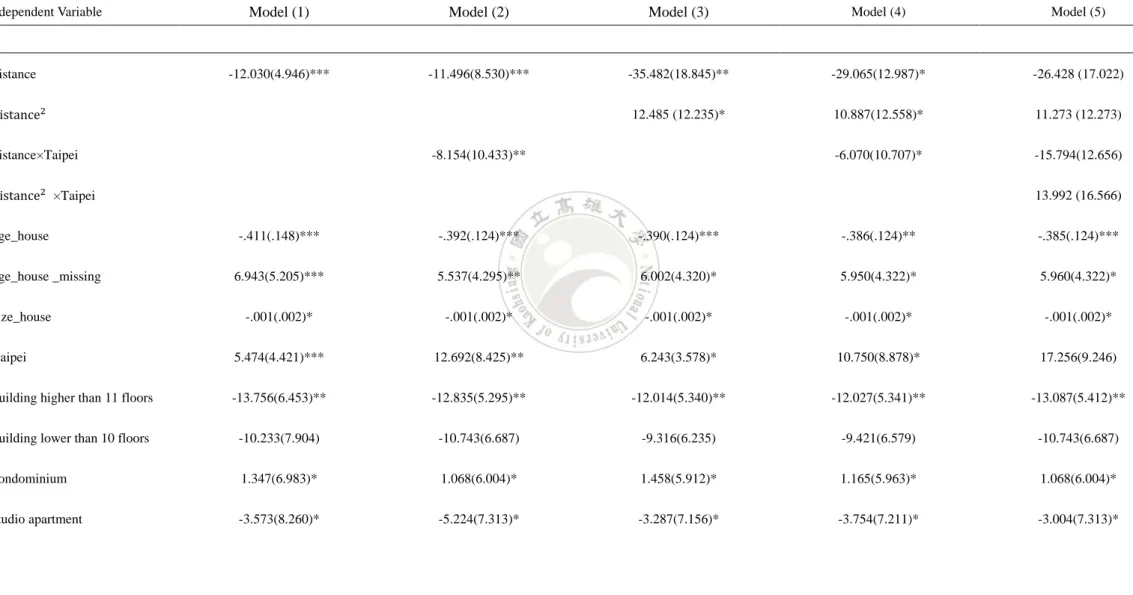

The empirical findings are reported in Tables 2 and 3. Table 2 shows the effect of the

distance to MRT station on housing prices within 1.5 km. Model (1) indicates that distance

to MRT stations, the age of the house, size of the house and Taipei are statistically

significant. More importantly, distance has a negative effect on housing prices. The

estimates show that when the distance to MRT station increases by 1 km, the housing

prices decrease by $NT120,300 per ping.

Model (2) demonstrates that when the distance to MRT station decreases by 1 km, the

housing prices in Taipei is $NT81,540 per ping higher than Kaohsiung. It means that the

MRT system in Taipei has a greater impact on housing prices, compare with Kaohsiung.

Model (3) shows the relationship of the distance to MRT stations on housing prices

between Taipei and Kaohsiung. According to the coefficient of distance2, we can

conclude that the relationship between the housing prices and distance is a U shape.

Model (4) is our main model. The estimates indicate that when the distance increases

by 1 km, the housing prices decrease by $NT158,432 per ping in Taipei, and decrease by

$NT97,732 per ping in Kaohsiung. The relationship between housing prices and distance

13

Table 2. The Effect of Distance on Housing Prices: Distance to MRT station ≦ 1.5 km)

Independent Variable Model (1) Model (2) Model (3) Model (4) Model (5)

distance -12.030(4.946)*** -11.496(8.530)*** -35.482(18.845)** -29.065(12.987)* -26.428 (17.022) distance2 12.485 (12.235)* 10.887(12.558)* 11.273 (12.273) distance×Taipei -8.154(10.433)** -6.070(10.707)* -15.794(12.656) distance2 ×Taipei 13.992 (16.566) age_house -.411(.148)*** -.392(.124)*** -.390(.124)*** -.386(.124)** -.385(.124)*** age_house _missing 6.943(5.205)*** 5.537(4.295)** 6.002(4.320)* 5.950(4.322)* 5.960(4.322)* size_house -.001(.002)* -.001(.002)* -.001(.002)* -.001(.002)* -.001(.002)* Taipei 5.474(4.421)*** 12.692(8.425)** 6.243(3.578)* 10.750(8.878)* 17.256(9.246)

building higher than 11 floors -13.756(6.453)** -12.835(5.295)** -12.014(5.340)** -12.027(5.341)** -13.087(5.412)**

building lower than 10 floors -10.233(7.904) -10.743(6.687) -9.316(6.235) -9.421(6.579) -10.743(6.687)

condominium 1.347(6.983)* 1.068(6.004)* 1.458(5.912)* 1.165(5.963)* 1.068(6.004)*

14

Notes: 2017 = 0, Single-family house = 0, Kaohsiung = 0.

*** Significant at 1% significance level. ** Significant at 5% significance level. * Significant at 10% significance level

Refer to Table 2 (continued)

storefront 12.964(12.431) 8.561(10.350) 9.775(10.303) 9.419(10.324) 9.516(10.205) commercial building -8.847(16.990) -7.907(9.129) -5.791(8.887) -6.869(9.089) -7.907(9.129) others -5.754(10.897) -8.448(8.899) -6.990(8.822) -7.127(8.832) -5.844(8.899) 2012 2.521(8.489) 4.239(7.405) 3.318(7.340) 3.606(7.388) 4.239 (7.405) 2013 13.814(6.067)** 12.569(5.144)** 12.304(5.128)** 12.173 (5.135)** 12.569 (5.144)** 2014 11.257(5.607)** 10.233(4.744)** 9.950(4.678)** 9.642(4.719)** 9.033(4.744)** 2015 5.549(5.716) 5.813(4.873) 5.790(4.865) 5.658(4.872) 5.083 (4.873) 2016 2.051(5.584) 2.274(4.742) 2.292(4.741) 2.224(4.743) 2.217 (4.744) N 1790 1790 1790 1790 1790 F-value 34.061 33.204 32.973 32.448 32.206 R2 .206 .208 .205 .206 .208

15

Model (4) also shows that the impact of MRT system in Taipei on housing prices is

greater than that in Kaohsiung when the distance increases by 1 km. The housing prices

in Taipei decline an additional of $NT60,700 per ping. Due to small sample size, the

coefficients of distance,distance2, distance×Taipei and distance2×Taipei are not

statistically significant in Model (5).

When we look at Model (1), the housing prices drop by $NT4,110 if the age of the

house increase by one year. As Model (2) shows, when the age of house increases one

year, the housing prices decrease by $NT3,920. Model (3) indicates that the housing

prices drop by $NT3,900. Model (4) reveals that the housing prices decrease by $NT3,860

when the age of house increase on year and Model (5) suggests than the housing prices

decrease by $NT3,850 when the age of house increase on year

Moreover, the size of the house has a significant effect on housing prices. All five

models suggest that when the size of the house increases by 10 pings, the housing prices

decrease $NT100. Meanwhile, when we look at Taipei, the estimate infers that the

housing prices in Kaohsiung are less than Taipei.

The housing prices in the year 2013 are higher than in other years. The reason might

be the implementation of the capital gain tax on the stock market in 2012 which redirected

16

the government implemented the Combined Housing and Real Estate Tax in 2015;

consequently, the housing prices declined significantly.

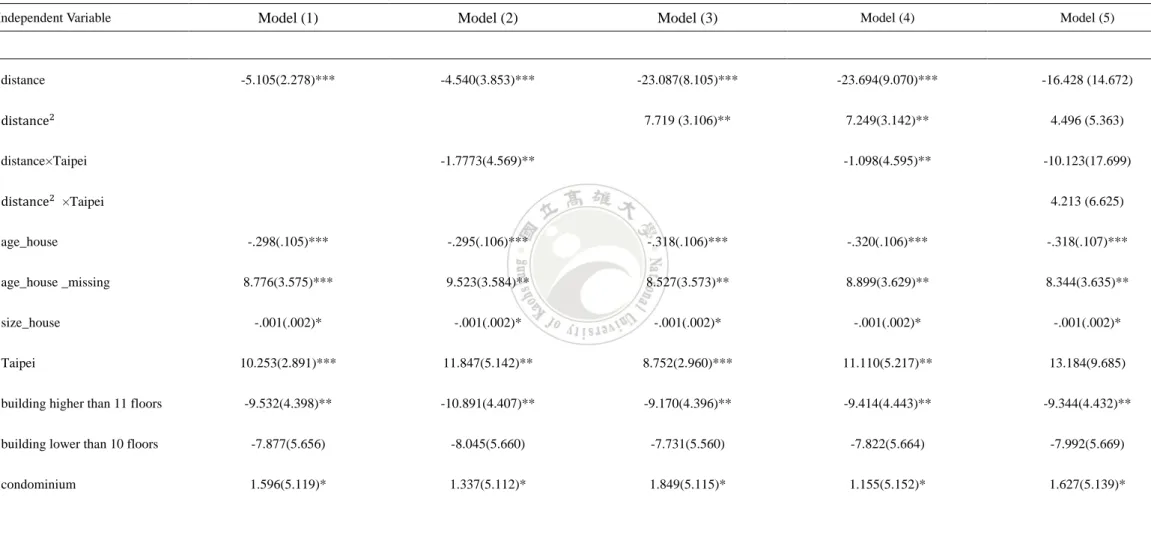

Table 3 shows the effect of the distance to MRT station on housing prices when we

limit the sample to those within 3 km from the MRT stations. Model (1) shows that the

distance to the MRT station, the age of the house, size of the house, and location of the

house are all significant determinant of housing prices. Distance to MRT stations has a

negative effect on housing prices, which means that when the distance increases, the

housing prices decrease and this result consists of the previous studies. The results suggest

that when the distance increases by 1 km; the housing prices decrease by $NT50,000/ping

Model (2) shows the different impact of the distance to MRT station on housing prices

in Taipei and Kaohsiung. The result indicates that when the distance increases by 1 km,

the housing prices in Taipei decrease by an additional $NT17,773 per ping, as opposed to

Kaohsiung.

Based on Model (3), Distance2 is statistically significant and the result indicates that

the rate of the decrease in housing prices declines as the distance increases. Model (4)

is our major model. When we have partial housing prices over partial distance, the

17

Table 3. The Effect of Distance on Housing Prices: Distance to MRT station ≦ 3 km

Independent Variable Model (1) Model (2) Model (3) Model (4) Model (5)

distance -5.105(2.278)*** -4.540(3.853)*** -23.087(8.105)*** -23.694(9.070)*** -16.428 (14.672) distance2 7.719 (3.106)** 7.249(3.142)** 4.496 (5.363) distance×Taipei -1.7773(4.569)** -1.098(4.595)** -10.123(17.699) distance2 ×Taipei 4.213 (6.625) age_house -.298(.105)*** -.295(.106)*** -.318(.106)*** -.320(.106)*** -.318(.107)*** age_house _missing 8.776(3.575)*** 9.523(3.584)** 8.527(3.573)** 8.899(3.629)** 8.344(3.635)** size_house -.001(.002)* -.001(.002)* -.001(.002)* -.001(.002)* -.001(.002)* Taipei 10.253(2.891)*** 11.847(5.142)** 8.752(2.960)*** 11.110(5.217)** 13.184(9.685)

building higher than 11 floors -9.532(4.398)** -10.891(4.407)** -9.170(4.396)** -9.414(4.443)** -9.344(4.432)**

building lower than 10 floors -7.877(5.656) -8.045(5.660) -7.731(5.560) -7.822(5.664) -7.992(5.669)

18

Notes: 2017 = 0, Single-family house = 0, Kaohsiung = 0. Standard errors are in parentheses.

*** Significant at 1% significance level. ** Significant at 5% significance level. * Significant at 10% significance level

Refer to Table 3 (continued)

studio apartment -2.783(6.257)* -3.480(6.255)* -2.079(6.528)* -2.709(6.296)* -2.617(6.316)* storefront 10.581(8.591) 10.661(8.660) 10.489(8.528) 10.469(8.569) 10.103(8.615) commercial building -3.677(7.919) -3.865(7.890) -3.38(7.899) -5.510(7.899) -4.382(8.073) others -5.406(6.846) -4.657(6.858) -5.472(6.856) -5.472(6.856) -5.340(6.872) 2012 4.477(6.376) 4.533(6.384) 3.841(6.385) 4.533(6.384) 3.699 (6.411) 2013 12.048(4.458)** 12.010(4.462)** 11.537(4.459)*** 12.010 (4.462)*** 11.491 (4.464)*** 2014 9.632(4.056)** 9.552(4.906)** 9.513(4.075)** 9.552(4.593)** 9.435 4.098)** 2015 3.276(4.078) 3.238(4.084) 2.839(4.079) 3.238(4.084) 2.722 (4.090) 2016 1.574(4.152) 1.534(4.153) 1.761(4.149) 1.534(4.158) 1.769 (4.156) N 2244 2244 2244 2244 2244 F-value 34.755 33.953 33.670 33.285 30.397 R2 .272 .276 .277 .275 .279

19

prices decrease by $NT119,467per ping in Taipei and decrease by $NT108,487 per ping

in Kaohsiung. The relationship between the distance to MRT stations and housing prices

is a U shape.

Moreover, the interaction term distance×Taipei is negative. It means that the distance

to MRT station in Taipei has a greater impact than that in Kaohsiung. It is because,

compared with Kaohsiung, Taipei has complete MRT systems; thus, people in Taipei are

more dependent on the MRT system. On the contrary, the MRT system in Kaohsiung is

less complete. Therefore, people would choose to ride a scooter instead of taking MRT.

The coefficients of distance, distance2, distance×Taipei and distance2×Taipei in

Model (5) are not statistically significant. This might be the outcome of the small

sample size. When we look at Model (1), the housing prices drop by $NT2,980 if the age

of house increases by one year. As Model (3) shows, when the age of the house increase

one year, the housing prices decrease by $NT3,180. Model (4) indicates that if the age of

house increases on the year, the housing prices drop by $NT3,200 and model (5) shows

that the housing prices decrease by $NT3,180 when the age of house increase one year.

The size of the house also affects the housing prices. All the models suggest that when

the size of the house increases by 10 pings, the housing prices per ping decrease by

20

housing prices in the year 2013 are higher than any other years in our sample, which

suggests that the housing market hit the record high in 2013 in Taiwan.

VI. Conclusions

In this study, we use the transactions data of real estate in Taipei and Kaohsiung from

the Ministry of Interior to test five regression models and estimate the impacts of the

distance to MRT stations on housing prices and test whether this effect is different

between Taipei and Kaohsiung.

The findings are as follows. First, distance to MRT station with 1.5 km and 3 km has a

significant negative impact on housing prices. Furthermore, the rate of the decrease in

housing prices declines as the distance increases. The potential reason might be people

would not choose to take MRT when they live too far away from MRT stations. Second,

the impact of distance to MRT stations on housing prices between Taipei and Kaohsiung

is different. The impact the distance to MRT stations on housing prices in Kaohsiung is

smaller than in Taipei.

Several reasons can explain why distance to MRT stations has a greater effect on

housing prices in Taipei. First, Taipei has more extensive MRT systems, compared with

Kaohsiung. As the result, it is convenient to travel in the city by taking MRT. People

21

in Kaohsiung only cover few districts and as a result, people prefer to ride a scooter

instead of taking MRT.

Second, parking space in Taipei is scarce and the parking fee is high, compared with

Kaohsiung. More importantly, the stricter law enforcement for traffic violations and

illegal parking in Taipei leads people to take MRT. Nevertheless, law enforcement is loose

in Kaohsiung, which fails to encourage people to use public transportation.

Third, the traffic is heavy especially during the rush hours in Taipei. To lower the cost

of commuting, people prefer to take MRT. On the other hand, traffic in Kaohsiung is not

as congested as Taipei. Riding scooter becomes a cheaper option people living in

Kaohsiung.

This paper is our first attempt to examine the effect of the distance to MRT stations on

housing prices. Future research can include Taoyuan MRT system and compare the

differential effect of the distance to MRT stations on housing prices in these three cities.

22 Reference

1. Armstrong, R. J., and Rodriguez, D. A. (2006). “An Evaluation of the Accessibility

Benefits of Commuter Rail in Eastern Massachusetts Using Spatial Hedonic Price

Function.” Transportation 33, no. 1: 21-43.

2. Bajic, V., (1983). “The Effect of a New Subway Line on Housing Prices in

Metropolitan Toronto.” Urban Studies 33, no. 1: 21-43.

3. Benjamin, J. D., and Sirmans, G. S. (1996). “Mass Transportation, Apartment Rent

and Property Values.” Journal of Real Estate Research 12, no. 1: 1-8.

4. Bowes, D. R., and Ihlandfeldt, K.R. (2001). “Identifying the Impacts of Rail Transit

Stations on Residential Property Value.” Journal of Urban Economics 50: 1-25.

5. Chernobai, E., Reibel M., Carney, M. (2011). “Nonlinear Spatial and Temporal

Effects of Highway Construction on House Prices.” Journal of Real Estate Finance

and Economics. 42: 348-370.

6. Coffman, C, and Gregson, M. E. (1998). “Railroad Development and Land Value.”

Journal of Real Estate Finance and Economics. 16, no. 2: 194-204.

7. Damm, D., Lerman S. R., Learner-Lam, E., and Young, J. (1980). “Response of

Urban Real Estate Values in Anticipation of the Washington Metro.” Journal of

23

8. Debrezion, G., Pels, E., and Rietveld, P. (2007). “The Impact of Railway Stations on

Residential and Commercial Property Value: A Meta-analysis.” Journal of Real

Estate Finance and Economics. 35: 161-180.

9. Dewees, D. N. (1976). “The Effect of the Subway Improvement on Residential

Property Values in Toronto”, Journal of Urban Economics. 3: 357-369.

10. Feng, C. M., Tseng, P. Y., and Wang, G. F. (1994). “Impact of Rail Rapid Transit

System on Housing Price in the Station Area.” City and Planning. 21, no. 1: 25-45

11. Debrezion, G., Pels, E., and Rietveld, P. (2007). “The Impact of Railway Stations on

Residential and Commercial Property Value: A Meta-analysis.” Journal of Real

Estate Finance and Economics. 35, Issue 2: 161-180.

12. Hong, D. Y., Lin, C. C. (1999). “A Study on the Impact of Subway System and Road

Width on the Housing Prices of Taipei.” Journal of Housing Studies. 8: 47-67.

13. Kilpatrick, J. A., Throupe, R. L., Carruthers, J. I. and Krause, A. (2007). “The Impact

of Transit Corridors on Residential Property Values.” Journal of Real Estate

Research. 29, no. 3: pp303-320.

14. Tai, K. C. (2011). “The Reexamination of the Impact of Mass Rapid Transportation

on Residential Housing in Taipei Metropolitan.” Department of Land Economics:

24

15. McDonald, J. F., and Osuji, C. I. (1995). “The Effect of Anticipated Transportation

Improvement on Residential Land Values.” Regional Science and Urban Economics.

25, no. 3: 261-278.

16. McMillian, D. P., and McDonald, J. (2004). “Reaction of Prices to a New Rapid

Transit Line; Chicago’s Midway Line, 1983-1999”, Real Estate Economics. 32, no.3:

463-486.

17. Peng, C. W., Yang, S. Y. and Yang, C. H (2009). “The Impacts of Subways on Metropolitan Housing Prices in Different Locations ─ After the Opening of the Taipei Subway System.” Journal of Transportation Planning. 38, no. 3: 275-296.

18. Reibel, M., Chernobai, E. and Carney, M. (2008). “House Price Change and

Highway Construction: Spatial and Temporal Heterogeneity”, paper presented at

Annual Meeting of the American Real Estate Society.

19. Speyer, J. and W. R. Ragas. (1991). “Housing Prices and Flood Risk: An

Examination using Spline Regression.” Journal of Real Estate and Finance

Economics. 4: 395-407.

20. Strawczynski, M. (1998). “Social Insurance and the Optimal Piecewise Linear

Income Tax.” Journal of Public Economics. 69, no.3: 371-388

25

Regression Methods.” The Review of Economics and Statistics. 60, no.1: 132-139.

22. Waddell, P., Berry, B. J. L. and Hoch, I. (1993). “Residential Property Values in a

Multinodal Urban Area: New Evidence on the Implicit Price of Location.” Journal

of Real Estate Finance and Economics. 7: 117-141.