國立台灣大學管理學院商學研究所 碩士論文

Graduate Institute of Business Administration College of Management

National Taiwan University Master Thesis

企業新創公司與母公司間之知識移轉-

吸收能力、母公司投入與彼此差異之調和效果 Knowledge Transfer between Corporate Ventures and Their

Parents - Absorptive Capacity, Parent involvement, and the Moderating Role of Inter-firm Difference

姜智予 Chih-Yu Chiang

指導教授:郭瑞祥教授、陳忠仁教授

Advisor: Ruey-Shan Guo, Ph.D. and Chung-Jen Chen, Ph.D.

中華民國九十八年七月

July 2009

國立臺灣大學碩士學位論文 口試委員會審定書

Knowledge Transfer between Corporate Ventures and Their Parents - Absorptive Capacity, Parent involvement,

and Moderating Role of Inter-firm Difference

本論文係姜智予君(R96741040)在國立臺灣大學管理 學院商學研究所完成之碩士學位論文,於民國九十八年七月 十一日承下列考試委員審查通過及口試及格,特此證明

口試委員:

(簽名)

(簽名)

(簽名)

(簽名)

系主任、所長

(簽名)

ACKNOWLEDGEMENT

For an MBA student, the value of thesis writing is often depreciated since MBA programs are expected being practical-oriented and as the gangway for real business. But the truth is that I really gained a lot from that process and sincerely appreciated it. It is a good experience to lead and complete a large and chronic project, a preliminary taste to deal with bosses who I have to report back periodically and try hard to transfer their knowledge and professionalism, and also an infrequent opportunity to peep into the academia which is astonishingly exact, constructive and procedurized. It is not only a tool for graduation and I hope everyone can realize it.

To accomplish such a very long but valuable academic journey as a freshman, sufficient support was provided by kindly people and I would like to give my gratitude to anyone who gave me the helps during it. The accompanying of my family, the idea providing of my classmates, the assistance from my friends and the devotion of my advisor professors, they are all precious to me. Either you were compelled to do or willingly and voluntarily gave me the hand, deserve my appreciation. Without your full support, this essay definitely could not be fulfilled within such a short and busy MBA program.

My master school life is concluded with this thesis, reluctantly. Getting things ready, for my next stage, I believe the enrichment from the two-year learning experience is plentiful and the gaining will surely ferment in the future. I believe that my life will authentically be shed light with those beautiful memories, the NTU school life, the thesis writing experience and all of you, involving in it. Again, my sincere gratitude is presented.

摘 要

隨著近年各種形式之公司內部創業蓬勃發展,不論在實務或學術界,CVC 活動成為一重要但複雜的討論議題。令人意外的是,過去文獻卻鮮少由子公司的

立場來看待CVC 這件事。為了彌補此學術面向上的不足,本研究延續知識基礎

與資源依賴的觀點,探討子公司由母公司處移轉知識基礎資源時,可能受到的直

接與間接影響因子。本研究由SDC、compustat 及 USPTO 等資料庫擷取橫跨 1968

年至2008 年,全球共 855 個 CVC 活動之樣本點為資料分析基礎,嘗試透過實證

的討論和分析,釐清關於母公司的投入、子公司之吸收能力與其創新績效三者間 之直接關係,以及母、子公司間差異可能為前述主效果帶來之調和影響。

研究結果大致與我們從過去文獻和理論所做出的推論假說相同。子公司之吸 收能力對齊本身之創新績效存在正向影響效果;母公司對子公司之投入對子公司

之創新績效則可能存在倒 U 型之影響關係;另外,包括母、子公司間規模與產

業差異之調和角色,亦能在統計上獲得證實。本研究承繼過去CVC 之相關研究,

嘗試拓展學術上於相關議題的全面性與發展性,同時希望提供角色為子公司之業

界經理人於面對CVC 投資時,一些關於其因應方式與母公司的選擇上可能的建

議和做法。

關鍵字:知識移轉、創新績效、吸收能力、母公司投入、公司間差異

ABSTRACT

CVC activity is such an important yet complicated issue. For solving the gap of literatures that from the view of venture firms was less paid attention, this research introduced knowledge-based view and resource dependence theory and focus upon venture firm’s knowledge based resources transferring and acquiring from their CVC parents. Data used in this research covered 855 global sample entries from 1968 to 2008, collected from SDC, compustat and USPTO database. Through empirical analyses, the relationship between parent firm’s involvement, venture firm’s absorptive capacity, its innovation performance and inter-firm differences between firms have been examined.

Complying with theories and several literatures about organizational knowledge transfer, main effects of parent firms’ involvement and venture firms’

absorptive capacity on its innovation performance and moderating role of inter-firm difference is generally statistically supported. The stream of research on CVC activities was inherited. We finally gain more understanding about parent firms’

impact on their corporate venture children in several dimensions theoretically, and also acquire practical guidance for ventures that they are searching for ideal CVC parents or are wondering how to react with CVC activities for gaining more from it.

Key Words: Knowledge transfer; Innovation performance; Absorptive capacity;

Parent involvement; Inter-firm difference

CONTENTS

CHAPTER1 INTRODUCTION ... 1

1.1 Research Background ... 1

1.2 Research Objective ... 3

1.3 Research Procedure ... 4

CHAPTER2 THEORY AND HYPOTHESIS ... 7

2.1 Corporate Venture Capital Activity ... 7

2.2 Theoretical Background ... 10

2.2.1 Knowledge-based view and Resource dependency ... 10

2.2.2 Knowledge transfer ... 13

2.3 Hypotheses Development ... 15

2.3.1 Absorptive capacity and innovation performance ... 15

2.3.2 Parent involvement and innovation performance ... 16

2.3.3 Moderating role of inter-firm difference - size ... 20

2.3.4 Moderating role of inter-firm difference - industry ... 23

CHAPTER3 RESEARCH DESIGN AND METHODOLOGY ... 26

3.1 Research Framework ... 26

3.2 Variable Measurement ... 28

3.2.1 Dependent variable ... 28

3.2.2 Independent variable ... 28

3.2.3 Moderating variable ... 29

3.2.4 Control variable ... 30

3.3 Data Collection and Sample ... 34

3.4 Statistical Method ... 35

3.4.1 Descriptive statistics and correlation analysis ... 36

3.4.2 Regression analysis ... 36

CHAPTER4 RESEARCH RESULT ... 39

4.1 Descriptive Statistics and Correlation Analysis ... 39

4.2 Regression Analysis ... 41

4.2.1 Direct effect of absorptive capacity and parent involvement ... 41

4.2.2 Moderating effect of inter-firm difference – size ... 42

4.2.3 Moderating effect of inter-firm difference – industry ... 43

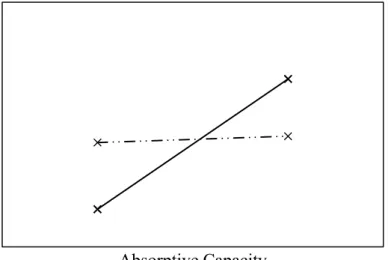

4.2.4 Diagrams of moderating effect ... 46

CHAPTER5 CONCLUSION AND SUGGESTION ... 50

5.1 Research Conclusion ... 50

5.2 Managerial Implication ... 52

5.3 Limitation and Future Research Direction ... 53

REFERENCES ... 56

TABLE LIST

Table 3-1 Summary of Variables ... 32 Table 4-1 Correlation and Descriptive Statistics ... 40

Table 4-2 Results of Regression Analysis ... 45

FIGURE LIST

Figure 1-1 Research Flow ... 6

Figure 3-1 Research Framework ... 26

Figure 4-1 Moderating Effect of Difference in Size on Absorptive Capacity ... 47

Figure 4-2 Moderating Effect of Difference in Size on Investment Amount ... 47

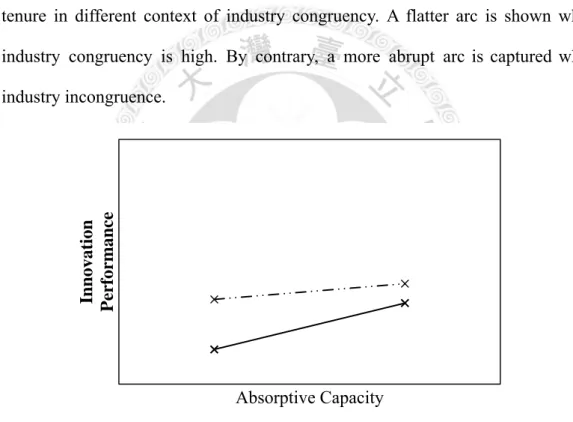

Figure 4-3 Moderating Effect of Industry Congruency on Absorptive Capacity ... 48

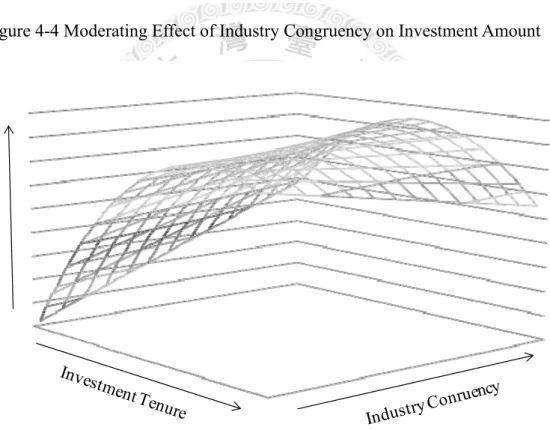

Figure 4-4 Moderating Effect of Industry Congruency on Investment Amount... 49

Figure 4-5 Moderating Effect of Industry Congruency on Investment Tenure ... 49

CHAPTER1 INTRODUCTION

1.1 Research Background

Being in competitive markets, continuous innovation maintains firms’

profitability (Arrow, 1962; Schumpeter, 1942). Innovation brings new products, processes and organizational systems to firms (Hitt et al., 1997). It facilitates the development of critical capability thus improves the profitability of firms, and helps firms succeed in market competition (Teece et al., 1997).

The major source of innovation of firms may come from their intellectual capitals, for instance, firms technological knowhow, marketing knowledge, management expertise, social capital, and even organizational climate (Barney, 1991).

It is said to be positively related to the innovation level of firms (Porter, 1980). It can improve firms’ innovation capability in product and strategy (Stopford and Baden-Fuller, 1994), and several empirical studies confirmed that (Karakaya and Kobu, 1994; Guzzo and Shea, 1992; Bantel and Jackson, 1989).

Unfortunately, it is crucial that many critical knowledge based resources needed for innovation activities may exist outside the firms (Cohen and Levinthal, 1990;

Arrow, 1974). Echoing to the concept of resource dependency, firms are compelled to stride across organizational boundaries and learn from the environment (Ulrich and Barney, 1984; Tiliquist et al., 2002), try to access external resources through inter-organizational activities (Luo, 2000; Bartlett and Ghoshal, 1986). CVC (corporate venture capital) program is one of the channels (Maula and Murray, 2001; Stuart et al., 1999; Pisano, 1991; Teece, 1986).

CVC activities construct a reciprocal relationship between parent firm and venture firm, and bring multiple benefits to both sides (Allen and Hevert, 2007; Miller,

1985; Maula and Murray, 2001; Stuart et al., 1999) including the improvements of innovations (Dushnitsky and Lenox, 2005; Stuart, 2000; Powell et al., 1996). The rising and flourishing of CVC activities appeared in last decade. In the peak of 2000, there were more than 400 CVC programs, represented $16 billion of capital, and 15%

share of venture capital market (Venture Economics, 2000). Even serious recession of whole venture capital market occurred in 2001, some renowned enterprises such as Intel, Microsoft and Merck were still engaging in it (Chesbrough, 2002).

Given that CVC activity is such an emerging issue in practical business world, many literatures have begun to devote in the relevant research domain last few years, about the benefit for each party, the survival of venture firms, and other practical issues. Not surprisingly, most of researches but selectively discuss from the perspective of large and incumbent parent firms (Yang et al., 2008; Allen and Hevert, 2007; Dushnitsky and Lenox, 2006; Hayton, 2005) since their more significant influence power. Even to those literatures focus on venture firms, many but choose to have the comparisons between CVC and IVC (independent venture capital) backed ventures (Ginsberg et al., 2003; Maula and Murray, 2001; Stuart et al., 1999; Block and MacMillan, 1993), less pay attention on the impacts of parents on venture firms, let alone the knowledge transfer process from parent firms to and how CVC-backed ventures can really benefit from their parents.

Indeed, resources acquirement is much more critical to venture firms than large and incumbent parent firms, especially for those firms were just started up and lack of crucial resources (Laitinen, 1992). Technological capabilities and innovation results are pointed out that particularly important to their survival (Lau and Ngo, 2004; Clegg, 1987; Lall and Siddharthan, 1982). Though scholars claimed theoretically that venture firms may either directly acquire the knowledge spillover from parent firms or

indirectly exploit social networks that parent firms have to connect with governance and universities (Pfeffer and Salancik, 1978), to access complementary technique (Keil, 2000), decrease the scarcity of resources (Maurer, 2003; Dubini and Aldrich, 1991) and improve their innovation capability (Ahuja, 2000; Hagedoorn and Schakenraad, 1994), there is actually little empirical evidence.

Throughout this research, our endeavors were dedicated to solve this gap. From the perspective of KBV (knowledge-based view) and RDT (resource dependence theory), we collected empirical data and attempt to verify the innovative benefits ventures can really gain from their parents, and then try to illustrate the influential factors of knowledge transfer on the innovation performance of ventures as the result.

Hope it can help to gain greater insight about this complicated but emerging issue.

1.2 Research Objective

Scholars argue that for competition and survival, firms have to construct learning relationships with external knowledge sources (Powell et al., 1996; Liebeskind, 1996; Zahra and George, 1996). For those just started up and small venture firms, the lever of integrating different knowledge is quite important (Lau and Ngo, 2004;

Laitinen, 1992). Incumbent and large parent firm is indeed one of their important sources of external resources (Maula and Murray, 2001; Stuart et al., 1999; Pisano, 1991; Teece, 1986), as the view of resource dependency.

This research tries to gain greater insight from the perspective of ventures, on the process and result of knowledge learning and transfer of ventures from parent firms. The focus will be nothing but the dedication of parent firms, the attitude venture firms took on it, and the effects of external influential factors such as the differences between two firms. We reviewed past literatures for proxies of each

variable and attempt to approach these issues by empirical data collection and verifying.

To shed light on the questions which be addressed above: whether parent firms deliver crucial benefits to venture firms through their involvement and whether venture firm’s own absorptive capacity influence this transfer, moreover, the effects of the differences between parent and venture firms that moderate the impact parent firms bring to their corporate child, there are four research objectives described below.

1. To examine the main effect of venture’s absorptive capacity on its innovation performance during CVC program period.

2. To examine the main effect of parent’s involvement on venture’s innovation performance during CVC program period.

3. To examine whether the difference between parent and venture firms will moderate the main effect of venture’s absorptive capacity on its innovation performance.

4. To examine whether the difference between parent and venture firms will moderate the main effect of parent’s involvement on venture’s innovation performance.

1.3 Research Procedure

For comprehending this research more easily, here briefly illustrates the logic and flow of the chapters as follows:

Traditionally, chapter one is the introduction of this research. It provides the background and objective of this research, mentions about the trigger and motivation for doing the research work about parent firms’ impact on innovation performance of venturing firms.

Chapter two is the literature review section, including several relative classical theories such like resource-based view, knowledge-based view, and also the development of hypotheses based on past researches. Classical theories bring this research reasonableness and enforce researcher’s confidence when developing the hypotheses; past researches clarified research directions and piled up research structure.

To continue the logic flow of preceding chapter, chapter three contains the illustration of research design and the reasons of choosing the methodologies. Research design includes the framework and measurement of variables be used in this research;

the statistical methods, data collection procedures and final sample are illustrated consecutively.

Chapter four then talks about the research result and lists the empirical statistic result includes the regression and correlation output of our variables. It is also the most critical chapter of this research, presents the major finding of this research.

Finally, we have our conclusion in chapter five, the discussion and research limitation, summarizing this research and expand the application to real business situations.

Identify research objectives

Review theories and literature

Develop hypotheses

Construct research framework

Define operational measurement

Collect data and samples

Statistical analysis

Conclusions and suggestions CHAPTER 1

CHAPTER 2

CHAPTER 3

CHAPTER 4

CHAPTER 5

Figure 1-1 Research Flow

CHAPTER2 THEORY AND HYPOTHESIS

2.1 Corporate Venture Capital Activity

Corporate venture capital (CVC) activity, an emerging issue in academia, discusses relevant activities about the financing of start-ups by large, well established corporations (Knyphausen-Aufse, 2001). Different from “corporate venturing”,

“corporate venture capital activity” has the narrower scope (Guth and Ginsberg, 1990;

Thornhill and Amit, 2001). It is actually one form of corporate venturing (Sykes, 1986), or some scholars take it more specifically as a form of external corporate venturing (Keil, 2002). It is also considered as a kind of emerging corporate entrepreneurship (Miles and Covin, 2002; Sharma and Chrisman, 1999).

Typical CVC activity has a three-stage structure between parent and venture firms (Ernst, et al., 2005). Parent firms make equity investment in CVC, and take CVC as a mediator to invest in start-ups, the venture firms. Parent firms deliver value adding to venture firms through direct capital investment and other indirect channels (Chesbrough, 2000; Block and MacMillan, 1993), to exchange the contribution to their financial and strategic objectives (Ernst, et al., 2005; Brandenburger and Nalebuff, 1996; Gompers and Lerner, 1998). To sum up in a word, CVC investment constructs a reciprocal relationship between parent firms and venture firms.

In the past, firms lack of innovative capability still focus on pure internal R&D investment (Hagedoorn, 1993). It’s different now that various instruments has been vigorously developed last few decades, includes M&A, joint venture activities and of course, CVC investment. More and more corporations try to access external resources through inter-organizational activities (Luo, 2000; Bartlett and Ghoshal, 1986). In the peak of 2000, there were more than 400 CVC programs, represented $16 billion of

capital, and 15% share of venture capital market (Venture Economics, 2000). Even serious recession occurred in 2001, some renowned enterprises such as Intel, Microsoft and Merck were still engaging in it (Chesbrough, 2002). Especially to those firms in emerging Asia, they are apt at turning back the inferior position through inter-organizational resource acquiring (Child and Rodrigues, 2005; Makino et al., 2002). They approach resources in developed country by leveraging their own asset and capabilities (Thomas et al., 2002).

Parent firms can acquire many kinds of benefits from CVC programs. As an investment activity, it surely may bring financial gains for parent firms (Allen and Hevert, 2007; Miller, 1985), some ventures further may eventually become customers of their parents and thus bring motive of growth to them (Chesbrough and Scolof, 2000).

Other than direct capital return, researchers are much more interest in strategic benefits that parents can gain from venture firms (Allen and Hevert, 2007; Dushnitsky and Lenox, 2006). Corporate venture firms help parents indirectly with monitoring the development of market and technology (Keil, 2002; McNally, 1997; Winters, 1988), acquiring techniques used by other firms (Mowery et al., 1996; Stuart and Podolny;

1996) and expanding business scope to new markets (Barkema and Vermeulen, 1998;

Mitchell and Singh, 1992). There’s also indirect benefit from venture firms that they construct complementary services and products parents need (Brandenburger and Nalebuff, 1996; Gompers and Lerner, 1998). CVC investments provide a good access to external knowledge (Chesbrough, 2002; Gans and Stern, 2003; Poser, 2003; Roberts and Berry, 1985) therefore Improve their growth and internal innovation rate (Dushnitsky and Lenox, 2005; Stuart, 2000; Powell et al., 1996). More generally, this kind of corporate entrepreneurship helps firm’s survival and renewal (Stopford and Badenfuller, 1994; Guth and Ginsberg, 1990).

On the contrary, from the perception of venture firm, some scholars try to clarify the differences between IVC (independent venture capital) and CVC invested venture.

Corporate-backed venture firm not only receive capital injection but much more benefits from different kind of resources of parent firms. Parent firms can transfer their expertise and technical know-how to their children (Day et al., 2001), share professional and social networks with venture firms (Maula and Murray, 2001; Stuart et al., 1999) that provide more opportunity to access complementary assets (Pisano, 1991;

Teece, 1986) and services (Block and MacMillan, 1993). Helps from parent firms can also facilitate the entering of new market (Hines, 1957); let the acquiring of external capital more easily and at lower cost (Heflebower, 1951). In addition, some scholars declare that corporate new ventures are more likely to emphasize marketing function (Knight, 1989), and making profit from leverage parent firm’s brand reputations or trademarks (Caves and Porter, 1977; Hines, 1957). Even more, parent’s residual capacity may utilized by venture firms and thus venture firms can more easily achieve the benefit from economies of scale (Caves and Porter, 1977; Hines, 1957). At last, CVC-backed venture firms usually can get better assessment than IVC-backed firms when IPO because of those advantages (Ginsberg et al., 2003; Maula and Murray, 2001).

Even such many benefits from receiving CVC investment, there are still drawbacks mentioned by scholars. The resources from parents are usually constrained by politicized budgetary processes, and have more focus on short-term objectives (Burgelman and Sayles, 1986). Some researches claimed that IVC-backed new ventures may have more stable and long-term source of capital (Fast, 1981). Even more, CVC-backed venture firms may have to fight for those resources with other units in parent firms, and be harmed by these activities (Sykes, 1986). Compare to IVC, CVC

managers have less compensation, less bonus but more fixed salary (Birkinshaw et al., 2002) and are thus less capable hand, having less capabilities and lower motivation (Chesbrough, 2000; Block and Ornati, 1987). Control and given orders from parent firms are not welcomed (Fast, 1981), managers of corporate new ventures are but often evaluated by it (Weiss, 1981), and troubled with conflicting political and corporate objectives (Fast, 1981). In practice, corporate-backed venture firms are usually lack of entrepreneurial talent, independent venture firms but have to face operational and financial problems more often (Knight, 1989). Be brief, contrast to independent venture firms, corporate venture firms can have abundant support from parent firms but may also lead to less autonomy, more monitorship and limitation from bureaucratic inertia (MacMillan et al., 1986; Stocking and Watkins, 1951).

Given that CVC activity is such an important yet complicated issue, most of researches about CVC activities but only had discussion from the perspective of large and incumbent parent firms (Yang et al., 2008; Allen and Hevert, 2007; Dushnitsky and Lenox, 2006; Hayton, 2005), paid less attention to resources transfer process from parent firms to venture firms that how a CVC-backed venture can really benefit from its parents. To solve this gap of past literature, this research try to clarified the relationship between parent firm’s involvement, venture firm’s absorptive capacity, its innovation performance and inter-firm difference between these two. And therefore, we can finally gain more understanding about parent firms’ impact on their corporate venture children.

2.2 Theoretical Background

2.2.1 Knowledge-based view and Resource dependency

RBV (resource-based view) scholars have mentioned that major sources of success of new firms are sufficient resources, innovative capability and

entrepreneurships (Zahra and Bogner, 2000; Christensen, 1997). They highlight the importance of resource that a firm held. The fundamental concept of RBV is that firms must develop their own competitive advantages through applying and exploiting their resources, and then can make profit from the market they compete in (Wernerfelt, 1984; Rumelt, 1984). The definition of “resource” was also discussed. Barney (1991) quoted the concept from Daft (1983) and Porter (1981) that they consider the resources of a firm include all assets, capabilities, organizational processes, firm attributes, information, knowledge, etc. They controlled by firm and enable the firm to implement strategies that improve its efficiency and effectiveness.

KBV extends the concept of RBV, which specifically emphasizes the strategic importance of knowledge based resources (Nonaka et al., 2000; Boer et al., 1999). It is initially promoted by Penrose (1959) and later inherited by Wernerfelt (1984), Barney (1991) and Conner (1991).

Knowledge is defined as those information been verified and refined (Machlup, 1983; Dreske, 1981). It is primarily embedded in firms’ intellectual capital (Edvinsson and Malone, 1997), including human capital, structural capital (Edvinsson and Malone, 1998; Roos et al., 1998) and relational capital (Youndt, 1998; Stewart, 1997). It is said positively related to innovation level of firms (Porter, 1980) and verified by several empirical studies (Karakaya and Kobu, 1994; Guzzo and Shea, 1992; Bantel and Jackson, 1989). Firms can easily leverage their knowledge when integrated with other knowledge (Demsetz, 1991), and generate knowledge heterogeneity that often becomes the critical determinant of superior corporate performance (Winter, 1984; Decarolis and Deeds, 1999). To summarize, KBV considers obtaining unique and in-imitable knowledge is the trigger of firms’

growth and profitability (Grant, 1996; Spender, 1996; Lei et al., 1996). Some scholars even take knowledge integration as the prime function of enterprises (Teece, 1998; Grant, 1996; Demsetz, 1991).

Given that knowledge based resources are so important to firms, there are several ways mentioned by scholars that how to acquire those resources firms need (Inkpen, 1996; Leonard- Barton, 1995; Helleloid and Simonin, 1994). It can be developed inside or acquired outside the firms (Wernerfelt, 1984; Barney, 1991;

Hamel and Prahalad, 1993; Das and Teng, 1998). Some scholars especially highlight the importance of external sources that claimed many critical resources may exist outside the firms (Cohen and Levinthal, 1990; Arrow, 1974) and firms must stride across organizational boundaries and learn from the environment (Ulrich and Barney, 1984; Tiliquist et al., 2002). CVC activities is one of the channel (Maula and Murray, 2001; Stuart et al., 1999; Pisano, 1991; Teece, 1986) and it is especially much important for those firms were just started up and lack of crucial resources for survival (Laitinen, 1992). That is the view point of resource dependency. Resources provided by firms themselves are not always enough for their operation. To survive, firms must rely on the interaction with environment, including other organizations (Pfeffer and Salancik, 1978). Resource dependence views organizations as being embedded in networks of interdependency and social relationships (Granovetter, 1985). It treats maximizing power of organizations in those networks to gain the control of critical resources as their goal and success (Pfeffer 1981), and thus can reduce the dependencies on environment.

For the sake of the importance of knowledge, to focus upon venture firms’

innovation performance, this research complies with KBV and RDT, and pays more attention on acquiring and transferring of knowledge-related resources. This

perspective has indeed been widely adopted in CVC relative researches (Hayton, 2005; Schildt et al., 2005; Wadhwa and Kotha, 2006).

2.2.2 Knowledge transfer

Organizations can acquire new knowledge through internal development or external transfer (Ciborra, 1991; Hagedoorn, 1993). When acquiring from external sources such like consultant, customer, national lab, university, supplier, rivals and non-rivals (Leonard- Barton, 1995), the first thing to firms for wholly exploiting the value of external knowledge is affirming whether they possess the ability to differentiate the usage of components (Zahra and George, 2002), and can capture it carefully then (Argote, 1999). It is so called knowledge transfer. Argote and Ingram (2000) define knowledge transfer as “the process through which one unit is affected by the experience of another”. Better knowledge transfer brings more knowledge base resources with better quality. That is extraordinarily favorable for firms’ innovation activities (Dushnitsky and Lenox, 2005; Stuart, 2000; Powell et al., 1996).

Passed down from the concept of resource dependency, many literatures discussed the influential factors of the knowledge transfer and acquiring process since the importance that scholars claimed the development of valuable resources and capabilities is highly related to it (Teece et al., 1997; Henderson and Cockburn, 1994). It includes the characteristics of each participants (Kogut and Zander, 1992;

Dougherty, 1995; Henderson, 1993), the relationship between knowledge sender and receiver (Simonin, 1997; 1999) covering the social network fit between participants (Weber and Weber, 2007; Scholl, 2003), the relevance between each party’s knowledge base (Lane and Lubatkin, 1998; Arrow, 1974) and the similarity of parents and their children (Festinger, 1954) that we will discuss in this research.

The efficiency of knowledge transfer is first determined by each party’s characteristics, such as the absorptive capacity of knowledge receiver and the organizational inertia embedded in each firms. Better absorptive capacity may facilitate better transferring and combination of knowledge (Kogut and Zander, 1992; Cohen and Levinthal, 1990) but while innovative activities may restrained because of organizational limits (Henderson, 1993), the pressures and rigid core incompetencies (Dougherty, 1995; Block, 1989).

Social capital is another focal point of discussion. The two dimensions of social capital, structural dimension and relational dimension, are both considered influencing firms’ knowledge transfer (Granovetter, 1992). In this research, we will pay more attention on relational social capital fit since strong tie is constructed most of time when CVC investment relationship is built up. Conative fit in relational social capital represents firms’ intention and willingness of collaboration; affective fit is besides the emotional compatibility between firms (Scholl, 2003). They are said will positively influence knowledge transfer between parent and venture firm (Weber and Weber, 2007).

From the perspective of social interaction, homophily principal may also influence the interaction between firms. It claims that people like to identified the similarity by relevance of social categories (Mehra et al., 1998), and associate others who are similar (McPherson et al., 2001). When the level of similarity is low or even firms are belong to totally different sub-groups within the environment, interactions for knowledge or resource transfer will be impeded and whittled down.

Some scholars claimed that each participant’s knowledge base may also have the influence (Lane and Lubatkin, 1998). Literatures revealed that

technological synergy from complementary technologies can increase both firms’

R&D efficiency (Gerpott, 1999). Similarity of knowledge base can assist the cooperation between each firm’s employees and bring benefit to transfer activities (Hellmann, 2001).

This research takes these perceptions and proceeds empirical verification that to clarify the relationship between parent firms and venture firms, focus upon the dependent variable, innovation performance, which KBV emphasized, trying to gain understanding of the activities about external resources acquisition and internalization.

2.3 Hypotheses Development

2.3.1 Absorptive capacity and innovation performance

From the view of resource dependency, it’s indeed a good channel for new ventures that releasing resources constraints from incumbent and large parent firms (Maula and Murray, 2001; Stuart et al., 1999; Pisano, 1991; Teece, 1986) especially as the truth is that knowledge required to process innovation is often outside firms (Cohen and Levinthal, 1990; Arrow, 1974). Taking along with this thread, knowledge transfer is highlighted and be put attention on in this research.

Past literatures pointed out that one influential factor of transferring knowledge base resources between firms is about the capability of receiver (Kogut and Zander, 1992; Cohen and Levinthal, 1990), in this research, the venture firms.

The first thing to firms who would like to wholly exploit value of external knowledge is affirming whether they possess ability to differentiate the usage of external knowledge components (Zahra and George, 2002), and then can modestly capture it (Argote, 1999). Knowledge combination process is also important. Firms,

particular younger firms, must have the capability to learn, absorb and integrate external knowledge through their own knowledge bases (Kogut and Zander, 1992;

Cohen and Levinthal, 1990) for proper assimilating and leveraging new knowledge just acquired.

To extract this concept, pioneered by Cohen and Levinthal (1990), absorptive capacity is defined as the ability of firms to acquire, assimilate and exploit knowledge for commercial needs. To be more generalized, it is organizational flexibility (Lyles and Salk, 1996) for and firms’ active attitude toward knowledge transfer and acquisition. Absorptive capacity was often captured by firms’ R&D expenditure or similar measurement in past researches (Dushnitsky and Lenox, 2005; Cohen and Levinthal, 1990) since that R&D expenditure is the most fundamental resource of a firm doing innovative activities (Narasimhan et al., 2006).

Better absorptive capacity induces better spontaneous reactions to parent-venture relationship, which generates efficient acquiring and transfer activities. Knowledge from external sources may be brought into full play that can well integrated with firms’ knowledge stock and help firms approach problems in different ways (Ahuja and Katila, 2001), thus reinforces internal R&D capability and have better innovation performance (Keil et al., 2004; Chesbrough and Tucci, 2003). The reasons lead this research to form Hypothesis 1 that predicts the positive relationship between venture firm’s absorptive capacity and its innovation performance:

Hypothesis 1: Ceteris paribus, venture firm’s innovation performance has a positive relationship with its absorptive capacity.

Another crucially influential factor of knowledge transfer is sender’s involvement. That is parent firm’s involvement under CVC construct.

Some empirical studies discovered the strength of partnership between parent and venture firms will influence venture firms’ performance and learning (Autio et al., 2004; Thornhill and Amit, 2001). Several scholars even believe that successful learning primarily comes from the close interactions of firms’

employees and information (Daft and Lengel, 1986; Arrow, 1974). It is just the concept of fit in perspective of social capital.

There are two kinds of relational social capital fit be mentioned in past literatures, conative fit and affectional fit. Conative fit represents firms’ intention and willingness of collaboration (Scholl, 2003), it is said will positively influence knowledge transfer between parent and venture firms (Weber and Weber, 2007, Hamel, 1991). Collaboration intention and willingness brings closer and more intensive interactions, facilitates the formation of knowledge sharing routines and is beneficial to firms’ knowledge transfer and acquiring (Dyer and Singh, 1998).

Higher level of parent involvement represents higher relative importance of the CVC program to parent firms. It lead to higher intention level of parents to dedicate into helping venture firms that indicating better conative fit between parent and venture firms. The fit improves knowledge transfer, brings up more innovative resources from parent firms and motivates parents to devote more into knowledge transfer activities such as building knowledge sharing routines for ensuring the performance of ventures and achieving their mutual goals.

Hypothesis 2 is therefore posited as follows:

Hypothesis 2: Ceteris paribus, venture firm’s innovation performance has a positive relationship with parent firm’s investment amount.

More specifically, conative fit can be propelled by trust (Fukuyama, 1995).

Setting with imperfect information, trust reflects the willingness to be honesty, to cooperate, to sacrifice and to achieve the mutual objectives (Sapienza et al., 1999;

Weber, 1997; Mayer et al., 1995; Ring and Van de Ven, 1994; Lindskold, 1978). It can improve the efficiency of knowledge sharing routines (De Clercq and Sapienza, 2001). It can also decrease the need of controlling provisions induced by agency risks from the view of transaction cost (Sapienza et al., 1999). Organizations incline to exchange resources and cooperate with each other under high level of trust (Nahapiet and Ghoshal, 1998; Ellickson, 1991; North, 1990). It assists firms achieving better conative fit and more efficient knowledge transfer, therefore having better organizational performance (Weber and Weber, 2007).

When parent firm’s investment tenure in ventures gets longer, trust between them is gradually built up. Closer relationship is constructed (Zahra and Covin, 1995) and encouraged the conative fit. It is favorable to knowledge transfer between parent and venture firms (Dyer and Singh, 1998; Nahapiet and Ghoshal, 1998) and finally improves venture’s innovation performance.

Even though there may be benefits generated from longer investment tenure, too long but can contrarily cause drawbacks on parent and venture firms’

knowledge transfer activities.

Autonomy brought from flexibility improves the success of venture firms (Ginsberg and Hay, 1994) so does sufficient entrepreneurship (Zahra and Bogner, 2000; Christensen, 1997). Organizational flexibility and entrepreneurship represent firms’ agility and intention to catch market opportunities. Some scholars even consider firms’ entrepreneurial activities as the commitment to innovation (Lumpkin and Dess, 1996; Miller, 1983). On the contrary, control and given orders

from parent firms are not welcomed (Fast, 1981) and the inherent rigidity and inertia of firms’ existing resource base may have negative effect on their growth and innovation (Sapienza et al., 2004). Firms’ innovation performance is often confined by their organizational limits (Henderson, 1993) that it hinders the formation of knowledge transfer and other creative activities. Pressures and core incompetencies also increase the rigidity and are unfavorable factors for innovative activities (Dougherty, 1995; Block, 1989).

In practice, corporate-backed venture firms are relatively lack of entrepreneurial talent when compared to independent venture firms (Knight, 1989).

68% CVC parents hold board seats of their ventures and 71% CVC parents conduct intensive monitoring and visiting to control their children in Europe (Bottazzi et al., 2004). Naturally, it is not salutary for innovative activities, and unfortunately, that less autonomy, more monitorship and limitation from bureaucratic inertia (MacMillan et al., 1986; Stocking and Watkins, 1951) may even be reinforced by time passing and especially to those CVC investments for strategic objectives.

To sum up these two opposite effects, when parents’ investment tenure gets longer, it is first expected to benefits ventures’ knowledge transfer and innovative activities because of establishing conative fit between parent and venture firms, then may be harmful since less and less entrepreneurship, autonomy in venture firms but more bureaucratic inertia is progressively formed by parents’ order and control. It leads to following hypothesis:

Hypothesis 3: Ceteris paribus, venture firm’s innovation performance has a curvilinear (inverted U-shaped) relationship with parent firm’s investment tenure.

2.3.3 Moderating role of inter-firm difference - size

Parent firms can provide various non-pecuniary helps to venture firms (Chesbrough, 2000; Block and MacMillan, 1993) since its relative abundant resource base and stock. To focus on venture firms’ innovation performance, this research pays more attention upon knowledge base resources can be transferred from parent firms, which will positively influence innovation level of ventures (Porter, 1980) and is verified by several empirical studies (Karakaya and Kobu, 1994; Guzzo and Shea, 1992; Bantel and Jackson, 1989).

Knowledge base resources of a firm is primarily embedded in its intellectual capital (Edvinsson and Malone, 1997), including human capital, structural capital (Edvinsson and Malone, 1998; Roos et al., 1998) and relational capital (Youndt, 1998; Stewart, 1997). Structural capital is those routines and processes be embedded in firms that can directly integrate and internalize knowledge in organizational level (Brooking, 1996), covering organizational culture, organizational structure and information systems (Stewart, 1997). Human capital is employees and managers’ knowledge, skill and ability to complete goals that customers required (Youndt, 1998; Stewart, 1997). Relational capital is the potential external sources of knowledge. It comprises organization and employees’

regional networks, and the relations with academic and governmental research institutions (Cohen et al., 2002; Almeida and Kogut, 1999; Saxenian, 1990).

It can be directly perceived through the sense that intellectual capital may be more abundant in relative larger parent firms. Larger firm scale often comes from owning better competitive capability that leads larger firms’ growth in market competition. It further indicates the possession of quality and quantity knowledge base resources from the perspective of KBV. Therefore, larger firms

are reasonably considered having more abundant intellectual capital such as maturer knowledge sharing routines, more competitive employees and managers, and better integrated social network relationships.

Relatively strong knowledge spillover from larger parents’ plenty intellectual capital provides more innovative resources for ventures’ assimilation thus is beneficial to their innovative activities (Ahuja, 2000; Hagedoorn and Schakenraad, 1994; Stuart, 2000; Maula and Murray, 2001; Stuart et al., 1999).

That is, venture firms can actually absorb more resources from relative larger parents under the same level of absorptive capacity, and achieve better knowledge transfer from their parents. In other words, through it, the effect of venture’s absorptive capacity on its innovation performance is reinforced. The following hypothesis is thus developed:

Hypothesis 4a: Ceteris paribus, parent and venture firm’s difference in size positively moderates the relationship between venture firm’s innovation performance and its absorptive capacity.

Though relative larger parents may provide more abundant intellectual capital for ventures’ absorbing, the weakened attention and ability of parent firms to cooperate with their ventures caused by size difference but can harm the benefit be brought from parents’ involvement, the established conative fit. The more the difference between two firms, the less the integration activities would be made (Roberts and Berry, 1985). In the situation of CVC investment, there are two reasons here.

The first is that parent firms’ resources may be diversified to other business units or other CVC programs (Burgelman, 1983; Biggadike, 1979). Relatively larger firm scale may indicate simultaneous possession of more business units and

CVC programs, the attention of parents be distributed in each venture firms is then scattered (Deeds and Hill, 1996). Venture firms may even have to fight for parents’

resources with other resource-needing entities within parent firms, and be harmed by these activities (Sykes, 1986). That may cause weakened effect of involvement because of that the spirit is willing, but the flesh is weak.

The symptom of principal of homophily is the other one. Principal of homophily in social network theory implies the critical role of similarity between parties within relationships. It considers that similarity may helps people in evaluation of each party’s ideas and abilities, improves easy and smooth of interactions, especially when the consequence of association is substantial (Festinger, 1954). People then like to identify the similarity by relevance of social categories such as age and status (Mehra et al., 1998) and incline to associate others who are similar (McPherson et al., 2001). Subgroups’ existence is the instance of proof (Blau, 1984; Simmel, 1955). Positive feelings will much easier be found within groups, and negative feeling is more commonly formed between groups on the contrary (White, 1961). Applied this concept to organizational level, the difference in size between parent and venture firms may indicates different social status, diverse organizational attributes and even distinctive corporate objectives.

The heterophily may whittle down the ability of parent firms to devote themselves into the interaction and knowledge transfer activities with venture firms, thus cause weakened effect of parents’ involvement.

To summarize, from the perspective of parent firms, either the distraction or disability generated by resource dispersedness and homophily will harm the effects of parent’s involvement on venture’s innovation performance. This research hence has the hypotheses below:

Hypothesis 4b: Ceteris paribus, parent and venture firm’s difference in size negatively moderates the relationship between venture firm’s innovation performance and parent firm’s investment amount.

Hypothesis 4c: Ceteris paribus, parent and venture firm’s difference in size negatively moderates the relationship between venture firm’s innovation performance and parent firm’s investment tenure.

2.3.4 Moderating role of inter-firm difference - industry

It is empirically proofed that firms’ knowledge bases will influent their learning activities with other firms (Lane and Lubatkin, 1998). To focus upon this issue, knowledge base relatedness between firms is highlighted and widely discussed by past literatures. It represents the degree of knowledge similarity and compatibility between firms (Scholl, 2003; 1992), and is said that the level of knowledge base relatedness between firms has the positive effects on firms’

innovative activities since there may be better identification, interpretation, and assimilation of knowledge between firms (Cohen and Levinthal, 1994).

One implication of higher level of industry congruency is higher level of knowledge and technological relatedness between firms. When firms operate in similar industries, they may possess similar techniques, knowhow, and even resembling organizational structure and managerial style on account for generating capabilities required for market competition. These establish similarity and compatibility between firms’ knowledge base and create favorable environment for knowledge transfer. It creates technological synergy from complementary knowledge and increase firms’ R&D efficiency (Gerpott, 1999), allows firms to specialize their knowledge bases, promote the effect of experience curve on venture’s innovation, and most of all, assures better collaboration between

employees and managers of parent and venture firms (Hellmann, 2001) by providing better connection via common language, thus improves absorbing activities of venture firms from their parents. The hypothesis referred to this inference is stated below:

Hypothesis 5a: Ceteris paribus, parent and venture firm’s industry congruency positively moderates the relationship between venture firm’s innovation performance and its absorptive capacity.

Most of CVC programs are not executed for only financial objective (Ernst and Young, 2002; Siegel et al., 1988), thus facilitate high level of information asymmetry between CVC parents and ventures (Gans and Stern, 2003) since conflicting goal and benefits between firms. This agency problem is commonly observed by past literatures (Dushnitsky, 2004; Gans and Stern, 2003; Fast, 1981).

Industry congruency indicating the competitive relationship between firms unfortunately reinforces this kind of confliction. Competitive relationship implies raising possibility of goal and benefit conflicting. Within similar industries, firms’

activities are more easily concerned with business secret confidentiality and competitive position maintenance. It hinders the intention of parent firms to cooperate with their ventures. Competitive and substitutive relationship leads to parents’ conservative behaviors such like the reservation of critical technology in CVC learning and exchanging activities (Dushnitsky, 2004). It may even easily result to failure relationship (Sykes, 1990). That is, under the same level of parents’

involvement representing the same level of parents’ intention and willingness to cooperate with their ventures seemingly, industry congruency between firms may essentially changes the behavior of parent firms and thus weakened the effect of trust and conative fit constructed by parents’ involvements.

Base on this consecutive expectation described above, the last set of hypothesis posits conflicting goals and benefit brought from industry congruency will negatively moderate the effects of parent’s involvement in venture firms:

Hypothesis 5b: Parent and venture firm’s industry congruency negatively moderates the relationship between venture firm’s innovation performance and parent firm’s investment amount.

Hypothesis 5c: Parent and venture firm’s industry congruency negatively moderates the relationship between venture firm’s innovation performance and parent firm’s investment tenure.

CHAPTER3 RESEARCH DESIGN AND METHODOLOGY

3.1 Research Framework

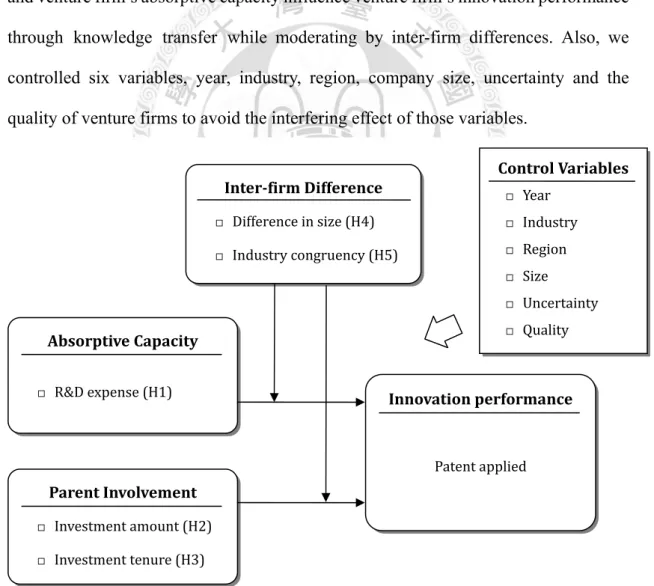

After each hypothesis developed from literature reviewing, following is the whole picture of this research combined all hypotheses and be displayed in simple figure (Figure 3-1) containing five constructs.

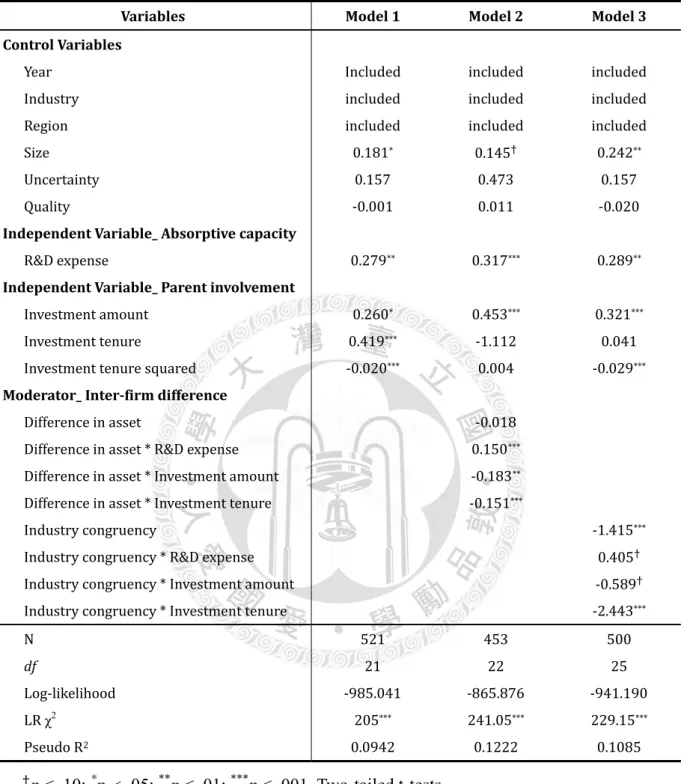

Generally speaking, this research tried to know how parent firm’s involvement and venture firm’s absorptive capacity influence venture firm’s innovation performance through knowledge transfer while moderating by inter-firm differences. Also, we controlled six variables, year, industry, region, company size, uncertainty and the quality of venture firms to avoid the interfering effect of those variables.

Based on this framework, six sets of hypotheses will be tested through empirical Innovation performance

Patent applied Interfirm Difference

Difference in size (H4)

Industry congruency (H5)

Parent Involvement

Investment amount (H2)

Investment tenure (H3) Absorptive Capacity

R&D expense (H1)

Control Variables

Year

Industry

Region

Size

Uncertainty

Quality

Figure 3-1 Research Framework

validation:

Hypothesis 1: Ceteris paribus, venture firm’s innovation performance has a positive relationship with its absorptive capacity.

Hypothesis 2: Ceteris paribus, venture firm’s innovation performance has a positive relationship with parent firm’s investment amount.

Hypothesis 3: Ceteris paribus, venture firm’s innovation performance has a curvilinear (inverted U-shaped) relationship with parent firm’s investment tenure.

Hypothesis 4a: Ceteris paribus, parent and venture firm’s difference in size positively moderates the relationship between venture firm’s innovation performance and its absorptive capacity.

Hypothesis 4b: Ceteris paribus, parent and venture firm’s difference in size negatively moderates the relationship between venture firm’s innovation performance and parent firm’s investment amount.

Hypothesis 4c: Ceteris paribus, parent and venture firm’s difference in size negatively moderates the relationship between venture firm’s innovation performance and parent firm’s investment tenure.

Hypothesis 5a: Ceteris paribus, parent and venture firm’s industry congruency positively moderates the relationship between venture firm’s innovation performance and its absorptive capacity.

Hypothesis 5b: Parent and venture firm’s industry congruency negatively moderates the relationship between venture firm’s innovation performance and parent firm’s investment amount.

Hypothesis 5c: Parent and venture firm’s industry congruency negatively moderates the relationship between venture firm’s innovation performance and parent firm’s investment tenure.

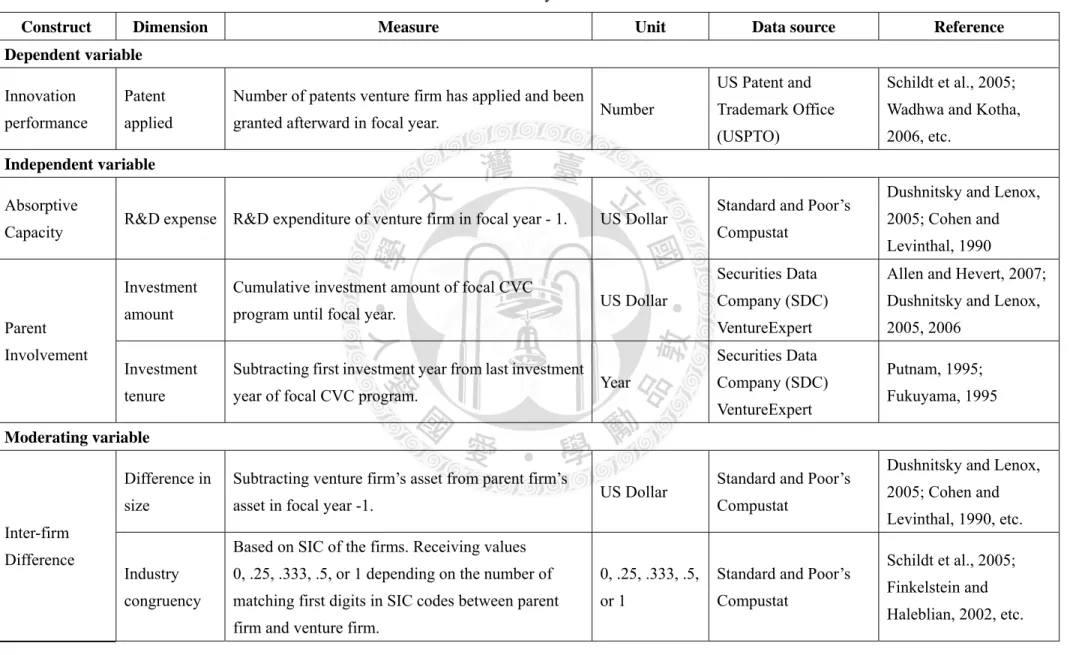

3.2 Variable Measurement

3.2.1 Dependent variable

To measure innovation performance of venture firms, followed previous researches (Schildt et al., 2005; Wadhwa and Kotha, 2006; Ahuja and Katila, 2001;

Sørensen and Stuart, 2000), we not using the patent issued number but the patent applied number in target year as the proxy.

Because it takes time to process the evaluation procedures by U.S. patent review committee and so exists the time lag between applied year and issued year of each patent, scholars used patent applied number instead of patent issued number to more accurately operationalized the innovation performance of firms (Griliches, 1990). To be mentioned, patent applied must be granted afterward to be considered in our counting.

To be consistency and credibility, this research focuses on the patents granted in the U.S.. and acquired Our patent data from U.S. Patents and Trademarks Office (USPTO), it is an agency in the United States Department of Commerce that issues patents to inventors and companies for their inventions for the intellectual property identification.

3.2.2 Independent variable

R&D expenditure is the most fundamental resource of a firm doing innovative activities (Narasimhan et al., 2006). To capture the absorptive capacity

of venture firms, the natural log of R&D expenditure is used. It is very common to use R&D expenditure as the proxy of firms’ absorptive capacity (Dushnitsky and Lenox, 2005 ; Cohen and Levinthal, 1990), it represents that can a venture firm acquire the knowledge or other resources from parent firms and combined with their own, then reinforce their knowledge and capability through this organizational learning process. To be simplified, it is the organizational flexibility (Lyles and Salk, 1996) and active attitude of venture firms toward resource transfer from parent firms.

Parent involvement was the concept that the level of parent firms involve in venture firms’ operation activities, including innovation or other learning activities (Wadhwa and Kotha, 2006). Natural log of cumulative investment amount of CVC program between the specific parent and venture firm pair is operationalized as one of our proxy of involvement. It is commonly used to evaluate the input of parent firm in venture firms (Allen and Hevert, 2007; Dushnitsky and Lenox, 2005, 2006).

The more the parent firm invested in a specific venture firm, the relative importance of venture firm to parent firm was higher, and the more intention and attention will be put on that venture firm. Parent firms make higher involvement to venture firms to ensure their investment performance.

The other measurement of parent involvement being used in this research is investment tenure. To capture the social network fit between parent and venture firms (Putnam, 1995; Fukuyama, 1995), it is the cumulative investment time and calculated by subtracting the year of the first investment relationship of each specific parent and venture firm pair was constructed from the last investment year that was made by same parent firm.

3.2.3 Moderating variable

Inter-firm difference is taken as the moderator in this research. There are two measurements of it in different dimensions being used in this research, difference in asset and industry congruency.

Firm size is often been used as a control variable to control the total strength of a firm (Dushnitsky and Lenox, 2005). Larger firms may have more resources and have inequality capabilities in many facets (Schumpeter, 1942; Cohen and Levinthal, 1990), and may represent different social status, organizational attributes and corporate objectives. We take the natural log of the difference in asset between parent and venture firms as our first measurement of Inter-firm difference to reflect the generalized similarity between them.

The other measurement we use here is industry congruency. It represents the dimension of knowledge relatedness (Wadhwa and Kotha, 2006) and potential interest confliction between parent and venture firms. Instead of using dummy variable to show that wholly different or wholly the same industry between focal firms (Wadhwa and Kotha, 2006), this research calculates the continuous index of industry congruency by receiving values 0, .25, .333, .5, or 1 when having the number of first digits matched between parent and venture firm in four-digit Standard Industry Codes (SIC) (Schildt et al., 2005) to fix the disadvantage caused by attribute of discrete variable. There are also similar measures been commonly used in academia (Finkelstein and Haleblian, 2002; Haleblian and Finkelstein, 1999;

Villalonga and McGahan, 2003).

3.2.4 Control variable

This research also controlled six variables to extract their effect on venture firm innovation performance, let us more clearly observe the relation we focus on between absorptive capacity, parent involvement, inter-firm difference and the

dependent variable.

To control the effect of macroeconomic situation on CVC investment, we include year, venture firms’ industry and region in this research. A set of dummies to control year effect (Schildt et al., 2005) that five year a blanket are included.

Because the sample’s diversity of industry is too high, directly generating dummies through firms’ SIC code (Schildt et al., 2005) is not appropriate for us. Instead, we have ten industry divisions according to USPTO division structure and they are included via dummy variables for removing industrial effect. Similarly, the operation region of each firm that was in the U.S. or else in other countries is presented through dummy variable (Hill and Birkinshaw, 2008) in our model.

The other three control variables refer to venture firms’ firm specific factors covering size, uncertainty and the quality of the firm. Firm size is often been used as a control variable to control total strength of a firm (Dushnitsky and Lenox, 2005), here we control it through natural log of venture firms’ assets. Uncertainty of a firm indicates the variability of future performance and development. We take venturing stage at the time the last investment has been made by the specified parent firm, stage categories of seed/startup stage and early stage vs. not, as a dummy variable (Yang et al., 2008). Earlier stages of venture firm often indicate that the firm is more risky and unpredictable. Quality of venture firm was finally been controlled to eliminate other parent firms’ effect. It is evaluated through counting how many venture capitalists had invested in the focal venture firm by the time our focal parent firm invested in it (Wadhwa and Kotha, 2006).

Table 3-1 Summary of Variables

Construct Dimension Measure Unit Data source Reference

Dependent variable

Innovation performance

Patent applied

Number of patents venture firm has applied and been

granted afterward in focal year. Number

US Patent and Trademark Office (USPTO)

Schildt et al., 2005;

Wadhwa and Kotha, 2006, etc.

Independent variable

Absorptive

Capacity R&D expense R&D expenditure of venture firm in focal year - 1. US Dollar Standard and Poor’s Compustat

Dushnitsky and Lenox, 2005; Cohen and Levinthal, 1990

Parent Involvement

Investment amount

Cumulative investment amount of focal CVC

program until focal year. US Dollar

Securities Data Company (SDC) VentureExpert

Allen and Hevert, 2007;

Dushnitsky and Lenox, 2005, 2006

Investment tenure

Subtracting first investment year from last investment

year of focal CVC program. Year

Securities Data Company (SDC) VentureExpert

Putnam, 1995;

Fukuyama, 1995 Moderating variable

Inter-firm Difference

Difference in size

Subtracting venture firm’s asset from parent firm’s

asset in focal year -1. US Dollar Standard and Poor’s

Compustat

Dushnitsky and Lenox, 2005; Cohen and Levinthal, 1990, etc.

Industry congruency

Based on SIC of the firms. Receiving values 0, .25, .333, .5, or 1 depending on the number of matching first digits in SIC codes between parent firm and venture firm.

0, .25, .333, .5, or 1

Standard and Poor’s Compustat

Schildt et al., 2005;

Finkelstein and Haleblian, 2002, etc.

Table 3-1 (continued)

Construct Dimension Measure Unit Data source Reference

Control variable

Macro -economic Situation

Year Year the last investment has been made between the

focal parent and venture firm pair. year Standard and Poor’s

Compustat Schildt et al., 2005 Industry Ten industry divisions according to USPTO division

structure. Nominal Standard and Poor’s

Compustat Schildt et al., 2005 Region 1 = Firm operated in the U.S.

0 = Firm operated in region out of the U.S. 0/1 Standard and Poor’s Compustat

Hill and Birkinshaw, 2008

Firm-specific Factor

Size Firm’s asset in focal year - 1. US Dollar Standard and Poor’s

Compustat

Dushnitsky and Lenox, 2005

Uncertainty

1 = Firm’s stage categories of seed/startup stage and early stage at the.

0 = Firm’s stage categories are not listed before.

0/1

Securities Data Company (SDC) VentureExpert

Yang et al., 2008

Venture quality

Number of venture capitalists invested in a venture

firm by the time focal parent firm put money into it. Number

Securities Data Company (SDC) VentureExpert

Wadhwa and Kotha, 2006

All variables be measured in US dollar were transferred into natural logarism of the variable.

3.3 Data Collection and Sample

This research constructed a large panel of worldwide corporate venture unit data during the period of 1968 to 2008 from Securities Data Company (SDC) VentureExpert, Standard and Poor’s Compustat and US Patent and Trademark Office (USPTO) database. The financial data was all adjusted by focal year exchange rate to American Dollars for comparing in equivalent bases.

SDC VentureExpert database is offered by Venture Economics, a division of Thomson Financial, was famous in researches about venture capital industry; it has often been used in several academic studies about the venture capital topic (Bygrave, 1989; Gompers, 1995; Dushnitsky and Lenox, 2005, 2006) before this research was conducted. This research used this database to help define the CVC investment venture unit list. The follow-up data and variable augmentation was based on this specified list.

The venture list of all kind of ventures drown from VentureExpert was first sieved by the criterion that the type of the fund invested in must be the following VentureExpert categories (Dushnitsky & Lenox, 2005): Non-Financial Corp Affiliate or Subsidiary Partnership, Venture/PE Subsidiary of Non-Financial Corp., Venture/PE Subsidiary of Other Companies NEC, Venture/PE Subsidiary of Service Providers, Direct Investor/Non-Financial Corp, Direct Investor/Service Provider, SBIC Affiliate with non-financial Corp. This step helped us to define the corporate backed venture units.

Simultaneously, venture activity related variables including investment amount, investment tenure, venture firm quality and uncertainty are also collected.

Another criterion was set that the investing fund must be the primary shareholder (have the largest cumulative investment amount within all investors) to manifest the influence from single CVC investment parent firm. Besides, all parent and

venture firms were demanded that having IPO before our research to ensure financial data is accessible.

Financial data be used in this research were then collected from Standard and Poor’s Compustat database and patent data were extracted from USPTO database through PatentGuider, a software that was designed to acquire patent data in several patent offices of the world. The augmentation in different dimension variables is in accordance with the specified venture list developed from VentureExpert through common company identification CUSIP and GVKEY.

To redeem the drawback came from less sample size, this research collected five observation years each firm, it was arouse from our stricter data sieving criteria.

Covering the year that last CVC investment has been made by specific parent to venture firm to four year after that, we believe that it may contain different information in different observation year due to different states of parent firm and venture firm even though the data was drown from the same pair of firms. In addition, One year time lag has been preserved between independent and dependant variables, it means, for instance, we will have parent firm data in t - 1 year when t year venture firms’

performance data was drown. It is confirmed and used in some relative papers (Dushnitsky and Lenox, 2005; Hall and Zedonis, 2001).

After steps of sieves and combination of the data described above, the resulting data set includes 855 firm-year observations (171 corporate venture units), where be invested by 111 parent companies during the focal period of this research. This data set covers several well-known enterprises like AT&T, Oracle, General Electronic, Merck

& co., IBM, Exxon, Johnson & Johnson and Intel, etc.

3.4 Statistical Method