碩士論文

Graduate Institute of Agricultural Economics College of Bio-Resources and Agriculture

National Taiwan University Master Thesis

薩爾瓦多吳郭魚產業發展策略研究

Study on Development Strategies of Tilapia Industry in El Salvador

研究生:海赫柏

Student: Herbert Francisco Aguilar

指導教授:雷立芬 Advisor: Li-Fen Lei, Ph.D.

中華民國 104 年 7 月 July 2015

Acknowledgements

I would like to express the deepest appreciation to the government of Taiwan, which gave me the opportunity to study here. Immeasurable appreciation and deepest gratitude for the help and support to member of Embassy of El Salvador here in Taiwan, Mr. Jaime Badia who in one way and another have contributed in making this study possible, by facilitating information through members of important organizations in El Salvador.

My gratitude is also extended to Professor Dr. Li Fen Lei for her generous advice, guidance and encouragement throughout my research for this work. Finally, I express the most wholehearted gratitude to my family and parents for their financial aid and lasting support without question. Last but not least I would like to thank my beloved girlfriend Huang Jing Yi for giving me her full support and love.

Abstract

Tilapia Aquaculture in El Salvador could play an important role in terms of national economy, job opportunities and food security. This study aims to analyze development strategies for tilapia production in order to maximize and to increase added value to the commercial chain, in a way to increase exports and open new markets worldwide v. The study applies a descriptive macro approach of SWOT analysis and Porter’s Diamond model, which are based on secondary data sources.

El Salvador’s tilapia industry appeared to have a positive view regarding the natural sources and aquaculture structure. Since aquaculture in El Salvador is a young industry. It is weaknesses in the responses was especially for demand conditions, as well weakness in supporting industry, capital invest, management and administration. The major challenges are to reduce the production cost and conciliate the economic performance to increase the competitive situation of El Salvador tilapia industry. Finally, it is necessary to develop a value chain where different stakeholders coming from private and public sector are involved to become the industry key factors.

Keywords: Tilapia, Strategies, SWOT analysis, Diamond Model, El Salvador, Development

Table of Contents

Acknowledgements………ii

Abstract……….iii

List of Tables………...…...v

List of Figures………vi

Abbreviations……….…1

Chapter I: Introduction……….………..……….2

1.1 Background and Motivation of the Study……….……….……2

1.2 Objectives of the Study……….……….…....4

Chapter II: Literature Review………..6

2.1 Overview of Tilapia Industry………….……….………...…6

2.2 Global View of Tilapia Industry……….…...7

2.3 Tilapia Industry in Latin America………....12

2.4 Tilapia Production and Development El Salvador……….………..16

Chapter III: SWOT Analysis……….……….31

Chapter IV Development Strategies………...40

4.1 Porter's Diamond Model ……….………...………40

4.2 Management Strategies………..…………..45

4.3 Finance Strategy.………...………...…………....53

Chapter V: Conclusions………...……….……..56

References ………..……...……….,.60

Table 2.1. Top ten Culture tilapia on the world………..11

Table 2.2. Distribution of area by farming………...22

Table 2.3. Composition of aquaculture, 2001-2003………....27

Table 3.1. SWOT Analysis of tilapia Industry in El Salvador………....36

Table 4.1. Niche markets for tilapia products……….45

Table 4.2. Projects for technological renovation………....48

Table 4.3. Suggested tilapia presentation with offered quality ……….51

Table 4.4. Possible institution that can grant funds for financial support………..54

Table 5.1. Integration of the prioritized projects ………...56

Figure 2.1. Volume and Value of different marine species ……….7

Figure 2.2 Volumes and value of tilapia 1984-2008………..…8

Figure 2.3. Aquaculture production of tilapia by continent, 1970-2002………...………10

Figure 2.4. Tendency of production in Tilapia 1984 - 2012 ………..17

Figure 2.5 Following we have the lineal projection of imports and Exports in USD 2011 -2014..18

Figure 2.6 Exports from El Salvador 2012………. ………...28

Figure 4.1. Diagram of Porter´s Diamond Model ………...40

Figure 4.2. Sustainability chart ………....………....…41

Figure 4.3. Interaction of Diamond Model………..….….45

Abbreviations

AECID Agencia Española de Cooperación

CAFTCA Central America Free Trade Agreement CENDEPESCA National Center of Fisheries

CIDA Canadian International Development Agency FAO Food and Agriculture Organization

JICA Japan International Cooperation Agency

KOICA Korean International Cooperation Agency

NOAA National Oceanic Aquaculture Administration MARN Environment and Natural Resources Ministry MINEC Ministry of Economics

OSPESCA Central America Fisheries and Aquaculture Organization USAID US Agency for International Development

Chapter I Introduction 1.1 Backgrounds and Motivation of the Study

Aquaculture started in El Salvador in 1962 with the assistance of the FAO in a governmental program, which aimed to promote agricultural diversification. Marine aquaculture started in 1984 with the construction of three shrimp culture farms. Species introduced are: tilapia (Oreochromis mossambicus, O. niloticus, O. melanopleura, O.

Hornorum), Chinese carps, grass carp (Ctenopharyngodon idellus), silver carp (Hypophthalmichthys molitrix), bigheaded carp (Hypophthalmichthys nobilis), common carp (Cyprinus carpio), black bass (Micropterus salmoide), jaguar guapote (Parachromis managuense), giant river prawn (Macrobrachium rosenbergii), oyster (Crassostrea gigas), and ornamental fish. The native cultured species include the marine shrimp (Penaeus vannamei) and the black mojarra (Amphilophus macracanthus). Marine aquaculture consists mainly of the farming of marine shrimp (Penaeus vannamei) which started around 1982- 1984 with a program sponsored by the US Agency for International Development (USAID) and executed by the El Salvador Foundation for Economic and Social Development (FUSADES).

Relevant facts related to aquaculture are: the international cooperation started by the FAO in 1967, and later with the cooperation of the USAID in a programme for training of specialized technicians, the establishment of a research programme on freshwater fish

farming and extension. In 1976 the Canadian International Development Agency (CIDA) supported a project on the evaluation of social aspects of fisheries and aquaculture, and the reintroduction of diverse tilapia species. In 1980 the General Directorate of Fisheries Resources was created, assuming the laws of fisheries and aquaculture through the General Law of Fisheries Activities. Taiwan starts its cooperation introducing Chinese carps and the freshwater prawn. In 1995, with the help of the European Union, the Regional Programme for the Support of Fisheries Development in the Centro American Isthmus (PRADEPESCA Agreement ALA/90/09) was executed. It promoted the formation of staff, refitted aquaculture facilities and infrastructure and strengthened research activities., the legal framework was updated with the promulgation of the General Law on the Management and Promotion of Fisheries and Aquaculture in 2001 whilethe Code of Conduct for Fisheries and Aquaculture was approved in 2004.

Aquaculture yields vary according to the technology used. Thus, intensive tilapia farming attain yields that exceed 10 tonnes/ha; semi-intensive 2.5-5.0 tonnes/ha; and extensive farming in reservoirs produce less than 1.5 tonnes/ha. Yields for marine shrimp farming per hectare are: artisanal, 142kg/ha; extensive, 230kg/ha; semi-intensive, 2 900kg/ha;

and intensive, over 6 tonnes/ha (production statistics of the Aquaculture Stations, CENDEPESCA, 2004). The national aquaculture production has increased, from 395 tonnes in 2001 to 1.130 tonnes in 2003, which is equivalent to a 286 percent increment, while total fisheries production has varied from 7.818 tonnes to 13 711tonnes, only a 175.37 percent increment (Annual Fisheries Statistics, CENDEPESCA, 2001, 2002 and 2003). The significant increment in production is due to the farming of tilapia and marine shrimp.

In accordance to the Director of CENDEPESCA an organization for the development of aquaculture, based on the production statistics, imports and exports of Fishery products for human consumption its calculated that in Central America the country that consumes more fishery products is Panama with a 47.7%, followed by Costa Rica and Honduras with 18%, El Salvador Finds itself with 5% of Gross consumption this equals to 11 pounds of fish.

In order to contribute to strengthen of tilapia industry, it is worthy to reply the following problems:

i. In order to meet new challenges and opportunities under current circumstances and the process to devise different development strategies, can this study guarantee a better local and international scenario for the tilapia Industry?

ii. What are the reasons for undertaking such development strategies and who the ultimate beneficiaries are, and how the benefits of strategies are generated?

iii. Are the introduction of new aquaculture technologies could be beneficial for increasing production and consumption of Tilapia?

iv. Would Innovation in tilapia could improve significantly the demand on tilapia

If above questions cannot be solved as soon as possible, local disadvantages in terms of food security, lack of innovation in the area and unemployment will severely influence on sustainable development for the tilapia industry. However, development strategies should be analyzed based on the economic development, environmental conditions and policies of the country related to the industry. This provides a basis for interpreting the result. Includes and observatory approach on previous research works on Tilapia Industry. Assuming that results obtained elsewhere under similar environmental conditions can be replicated locally. This approach is also practical and in many cases, the cost of the experimental units that might be

built for demonstration, “if any”, is paid by the company willing to take the risk. This way the study helps to gain relevant advantage in relation to those that join later on and introduce new aquaculture technologies using and being based on the demonstration projects raised or analyzed in this document.

1.2 Objectives of the Study

This study would like to discuss current dilemma of El Salvador’s tilapia industry and try to find a way of how to improve farming techniques production efficiency in order to enhance the competitiveness in the global market Based on Historically events and current situation in the aquaculture area, aquaculture has being a marginal economic activity in the agricultural sector due to a traditionally agricultural attitude in terms of the main economic activity. It was until 2000 that aquaculture policies were formulated in the context of fisheries development. In this study SWOT analysis and Porter’s Diamond Model are used to understand role-plays of tilapia industry in El Salvador and to initiate the development strategies.

This research applies a descriptive approach that formulates a qualitative analysis of the data obtained from market analysis from different sources that will help identify opportunities for tilapia management in development strategies. Some of the sources are documents published by FAO, as well as independent researches from other organizations related to Tilapia Culture and development. Reference Contacts in El Salvador from Organization such as CENDEPESCA and OSPESCA contributed to facilitate the information analyzed and gathered about Tilapia industry in El Salvador. As learned from the substantiation of the fish farmer samples, current difficulties were categorized and analyzed.

Further, some possible solutions are provided to solve problems in production and marketing obstacles.

Well planned strategies must optimize growth, the execution of this study might help policy makers and Chain developing actors to identify how to increase Tilapia production and diversify production in El Salvador in order to increase share in the international trade revenue and consumption.

Even if it’s tried to model their farming activities applying knowledge already gained in more developed areas, such as Brazil, Chile, Ecuador or Mexico, it is reasonable to believe that local demonstration projects for innovative aquaculture activities in Tilapia industry can have a noticeable effect on prospective investors and governmental agencies. Specific objectives are shown as follows:

i. To examine the industry of Tilapia and its characteristics in El Salvador.

ii. To analyze the current demand of tilapia

iii. To propose and analyze developing strategies for El Salvador Tilapia Industry.

iv. To conduct an analysis of strengths, weaknesses, opportunities, and threats (SWOT) as perceived by producers.

This study is organized in this way: Chapter I introduces the motivation behind this study as well as the objectives. The second chapter introduces the profiles of Tilapia industry at the Global level and in El Salvador as a literature review. The third chapter presents the results of SWOT analysis to tilapia industry in El Salvador. The fourth chapter explains the development strategies based on Diamond model. The last chapter contain summary and conclusion of the study.

Chapter II Literature Review Overview of Tilapia Industry

2.1 Global Tilapia Industry

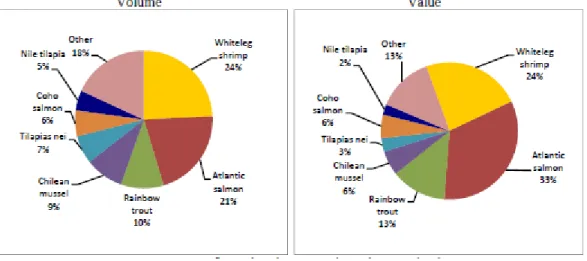

Fish and fish products constitute a major source of income, food and recreation in the global economy. Fish products originate from two main modes of production: harvesting of wild fish (marine and freshwater) and aquaculture. Aquaculture now accounts for almost half of total fish supply for human consumption (FAO 2010). The volume and value of different marine species are shown in Figure 2.1.

Figure 2.1 Volume and Value of Different Marine Species Source: FAO, 2010

Tilapia is the most widely produced fish in global export aquaculture and second only to carps as the most widely farmed freshwater fishes in the world (Naylor et al. 2000). The world harvest of farm-raised tilapia surpasses 800 000 tonnes (FAO 2004). Tilapia is grown in more than 75 countries, and China is the leading producer with 706 585 tonnes in 2002, or 47 percent of total world production (FAO 2004). Although a freshwater fish, tilapia can tolerate some salinity and so is hardier than many other breeds. This increases the range of possibilities for culture. Depicted on the walls of Egyptian tombs, tilapia in Biblical times was known as musht, Arabic for “comb.” More recently known as “St. Peter's fish,” it is understood that tilapia (Tilapia galilaea) from the Sea of Galilee were used to miraculously feed the multitude. Some attribute the naming of tilapia to Aristotle, from Greek for “distant,”

a fitting etymology for a globalized fish (FAO Fisheries and Aquaculture Circular No.

1061/3).

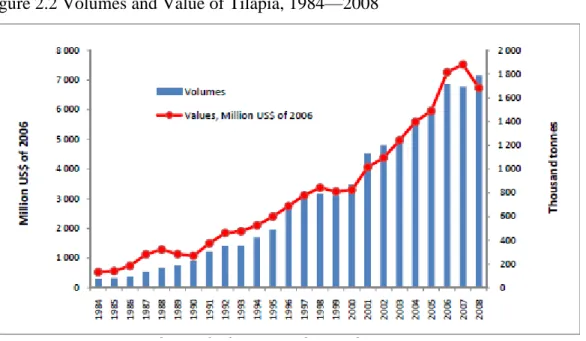

Figure 2.2 Volumes and Value of Tilapia, 1984—2008

Source: FAO, 2008

Culture practices of tilapias in the world are very diverse, perhaps the most diverse among all aquaculture species in the world. It is a group of fish that could be cultured at many desired intensities, thus, appealing to all socio-economic strata, enabling the culture practices to be adjusted to suit their economic capabilities. Oreochromis niloticus is commonly cultured in backyard and/or home garden ponds to supplement the income of poor households as well as provide a fresh source of animal proteins to the family.

In such situations, the cultured stock is often fed with kitchen waste and supplemented by relatively readily available, often low cost agricultural by-products such as rice bran.

However, the direct nutritional value of the latter to the stock is not known and in all probability rather low; the inputs act more as a fertilizer.

Oreochromis niloticus is cultured in relatively poor quality waters, including: (a) sewage fed ponds (e.g. commercial culture in Calcutta, India) (Edwards. 1990; Edwards et al., 1990); and (b) primary and secondary treated waste effluents (e.g. Egypt) (Khalil and Hussein, 1997). So far, there have not been any reports of detrimental effects of consumption of fish reared in sewagefed farms on human health even as the practice has been in operation since the 1930s (Nandeesha, 2002).

The growth of tilapia culture in Asia and the Pacific however, lagged slightly behind to that of the world. For example, the percent annual increase in tilapia culture in Asia and the Pacific for the 20 (1982 - 2002), 10 (1992 - 2002) and 5 (1997 - 2002) year periods was 12.5 (vs. 12.6), 10.9 (vs. 11.9) and 7.7 (vs. 10.0), respectively. This lower rate of growth in Asia and the Pacific is more a reflection of increased tilapia production in countries such as Egypt, where O. niloticus production increased from 9 000 tonnes in 1980 to 168 000 tonnes

in 2002. Also the rate of growth observed, in all three groups of fish is considerably higher than that witnessed in the sector as a whole (De Silva, 2001b).

Although a number of tilapia species has been introduced into the region, only a small number of these are cultured. Oreochromis mossambicus and O. niloticus are the most widely cultured tilapias in the world. In 15 countries in Asia and the Pacific, only four tilapia species are cultured, dominated by O. mossambicus (five countries) and O. niloticus (10 countries); the later accounts for more than 90 percent of the production and its contribution to aquaculture production has been increasing steadily.

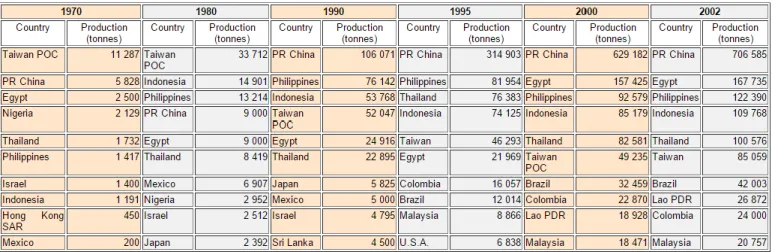

Figure 2.3 Aquaculture Production of Tilapia by Continent, 1970-2002

Source: FAO, 2002

The principal nations in Asia and the Pacific which have adopted tilapia culture are PR China, Indonesia, the Philippines, Thailand and Taiwan. Changes in Tilapia production in

these countries indicate that PR China currently accounts for over 70 percent of the region's production, an increase from 39 percent of Asia and the Pacific production in 1988, before the reported rapid increase in Nile tilapia culture in PR China.

This has led to a decreased share of production from the other countries of the region, even when production has exhibited growth.

For example, in the Philippines, the proportional contribution to regional Nile tilapia production was 27% in 1988 and only 10% in 2002, even though production increased from 27 000 tonnes to 104 000 tonnes over the period . Indonesia continues to dominate O.

mossambicus culture, accounting for nearly 50 000 tonnes and more than 90 percent of the global total in 2002. Over 60 percent of this production is reported as originating in brackish waters.

Table 2.1 Top Ten Culture tilapia on the world

Source: FAO, 2002

Cultured tilapia became an international commodity relatively recently, when frozen farmed tilapia fillets found their way into the mainstream food services and retail establishments of the American food-chain followed by expansion into Europe (Picchietti,

1996). Initially, frozen fillet imports to America exceeded fresh fillet imports by 30 percent and the author predicted that with time, increasing acceptance of tilapia will eventually outweigh frozen fillet imports. It has been suggested that tilapia would have a place as a generic white fish because of its mild taste and lends itself to industrial preparations better than most other white fish (Picchietti, 1996).

The main export market for cultured tilapia is the United States of America. In 2000, imports of tilapia (whole frozen, fresh and frozen fillet forms) in the United States amounted to 40 553 tonnes valued at US$ 101 377 853 and has since been increasing steadily.

According to Harvey (2001), tilapia imports to the United States of America increased by 394 percent by between 1993 and 2000. The main tilapia exporting countries are Taiwan Province of China, PR China, Ecuador and Costa Rica. Fresh fillet are currently supplied by Ecuador, Costa Rica and Honduras; frozen fillet and whole frozen fish comes from Asia (Vannuccini, 2001). Chinese imports have been increasing almost exponentially over the past few years. Harvey (2001) predicts that PR China will become the leading exporter of tilapia to the United States.

The European market for tilapia is still rather limited; UK is considered to be the major outlet. Vannuccini (2001) reckoned that the main markets in Europe are the big cities where large communities of African, Chinese and Asian communities live. However, an increase in tilapia consumption has been a recent trend also among non-ethnic communities.

European markets prefer larger-sized frozen tilapia. There are growing markets for tilapia in Canada, the Middle East and even in a rather sophisticated market such as in Japan (Vannuccini, 2001). In Japan, high quality tilapias are being used for sashimi and as a substitute to sea bream in traditional Japanese cooking.

It is thus evident that tilapias, commonly considered as the poor man's fish, are now beginning to make major entry to the sophisticated markets of the world. It has also become a popular and sought fish after freshwater fish in countries such as the Philippines and Indonesia, replacing milkfish and gourami, respectively. These trends are positive signs for all producers and can potentially influence a significant upsurge in tilapia culture

worldwide

(FAO,2002).

2.2 Tilapia Industry in Latin America

Tilapia farming in the LAC Region started in Mexico in 1970, and quickly reached 10 000 tonnes by 1981 (81 percent from Mexico, and most of the rest from Cuba). In 1996, production surpassed 50 000 tonnes with 26 countries involved. By 2007, production reached 212 000 tonnes, harvested by 25 countries or territories, headed by five nations (Brazil, Honduras, Colombia, Ecuador and Costa Rica) accounting for 90.2 percent of production.

Brazil produces about 95 000 tonnes; Honduras and Colombia, around 28 000 tonnes each, and Ecuador and Costa Rica, close to 20 000 tonnes each. The remaining twenty countries, each has a wide range of production with an annual average of about 1 000 tonnes (FAO, 2000).

In Central America By the end of December 2013, Honduras was a top producing country of fresh tilapia fillets with a 41% share, exporting 8 200 tonnes worth USD 65 million in foreign exchange for the year. In the first two months of 2014, Honduras’ export volume amounted to 1 832 tonnes, compared with 1 550 tonnes exported during the same period last year (+18.2%). However, prices decreased from USD 7.83 to USD 7.19 per kg.

In the domestic market, the wholesale price for whole tilapia (pounds) in Honduras ranges between USD 1.43 and USD 2.00, as reported by SIMPAH, (Sistema de Información de Mercados de Productos Agrícolas de Honduras). This price is stronger relative to other neighbouring countries; in Guatemala prices vary between USD 1.41 and USD 1.15. FAO

Brazil in 2009 reported a production of 133.000 tons of Tilapia that places it as a mayor producer in Latin America and sixth in the world with a sustainable growth of 14% in the past 5 years. Honduras continues to get the gap being the top exporter of fresh fry in Latin America to EU, mainly by production on red Tilapia. The industry in 2010 reached US$57.1 million and it finds itself on the top ten products being mainly exported.

It’s noticeable, that by this data, the commercialization of Tilapia grows day by day and in Central America, Honduras is the biggest producer. In this neighbor country not only the environmental conditions are in favor for aquaculture, but also the Government joins its development. The daily outputs of 65,000 to 75,000 daily pounds, towards United States talks for itself about the importance in the economic growth (FAO Fisheries and Aquaculture Circular No. 1061/3). The value of aquaculture production in the LAC Region has also evolved rapidly, reaching US$6 736 million in 2008, and the equivalent of US$7 175 million of 20064 per year during 2006–2008. The 2006–2008 value represents 8.1 percent of the world farmed production value for that period. The value of aquaculture products in the LAC Region is higher than the value of farmed fisheries products worldwide (8.1 percent versus 2.7 percent in 2006–2008). This clearly indicates that the average value of aquaculture products in this region exceeds that of world products.

To share Experiences in the culture of sweet water species such as Tilapia, a group of Aquaculture team of the region gather and participated in an affair of aquaculture production made by the Organización del Sector Pesquero y Acuícola Centroamericano del Istmo Centroamericano (OSPESCA), in conjunction with the Ministry of Agriculture of El Salvador, Through an Organization called CENDEPESCA.

This is really important for the development of Tilapia Culture, because the exchange of knowledge between regions can help to increase the Tilapia Development. In such activities 30 producers attended the meeting, which form part of the regional program of support on political enforcement of fishing and aquaculture (Belize, El Salvador, Guatemala, Honduras, Nicaragua, Costa Rica, Panama and Dominican Republic).

The purpose of this is to develop projects with the objective of duplicate them on a regional scale. El Salvador is the first one to conclude such projects. They said in an Interview that they are satisfied with the regional producers in El Salvador, which are showing commitment and responsibility, this project will generate capital which will allow to create and produce species with more quality in proteins.

The main topics and objectives here are:

- Continuity and transfer of knowledge and Technical assistance.

- Develop eco-tourism.

- Analyze the market.

- Promote the consumption of tilapia trough mouth to mouth.

- Encourage the use of clean technologies.

- Direct support to every organism in each country so this way the producers develop their own tilapia fry and could provide other producers.

The Committee of Ministers of OSPESCA, has been very interested in the strength of concretes actions to emphasize the responsible use of sea resources, those from inland waters and the hydro biological culture, implying harmonic decisions, particularly in those resources that because their condition freely moves in the Central American oceans and in international waters.

2.3 Tilapia Production and Development El Salvador

In conditions the production of Tilapia in El Salvador seems favorable for:

a) The biggest producer Honduras, in willing to increase its participation in North American market and thrive in the European market. Both markets are oriented by its preference toward products with added value.

b) For now, Honduras, it is being stimulated by the Salvadoran market and there are no Indications, until this day, that the country is willing to supply the Salvadoran market.

This two conditions have allowed, that the domestic production of El Salvador could be channeled towards Guatemala in a greater percentage. Although, it is of great importance to make a significant development in the local market of tilapia, to increase the levels of local production and as a measure of preparation for any eventualities that may occurred in the Guatemalan market (FAO Fisheries and Aquaculture Circular No. 1061/3).

During this last years, aquaculture production has varied substantially, from 395 tonnes 1 130 tonnes. The value of such production increased from US$ 1.8 to 5.4 million. In terms

of volume, the growth of aquaculture has been of the order of 286 percent. The most important cultivated species are the Tilapia (Oreochromis spp), the whiteleg shrimp (Penaeus vannamei) and the giant river prawn (Macrobrachium rosenbergii).

Inside Fish category the main fish produced is Tilapia, which is a specie that each day becomes a popular fish in the region. Inside Central America, Honduras is the leader of exports with 60 million. In the following figure we can appreciate the tendencie of tilapia production in El Salvador from the periods 1984 to 2012.

Figure 2.4. Tendency of production in Tilapia 1984 - 2012

Source: From FAO database 2012

Figure 2.5. Following we have the lineal projection of imports and Exports in USD 2011 - 2014

Source: Central Reserve Bank 2015 (www.bcr.gob.sv)

Three farming systems are mainly used to grow tilapias. The most common one is the farming in earthen ponds with a stocking density of 4-8 fingerlings/m2 and artificial food of 25-32 percent protein. The yields of this farming system are from 5 000–8 000 kg/ha.

Extensive farming is practiced in reservoirs and in small production units with stocking densities of 1 to 2 fish per square meters; yields do not exceed 700 kg/ha. Tilapia is also cultivated under intensive systems, either in raceways or in aerated ponds. The average yield is 25 kg/m3. The farming of tilapia in cages is another production practice with an average stocking density of 75 fingerlings per cubic meter.

Three systems are practiced in the production of white-leg shrimp: the most frequent one is the extensive farming with uncontrolled population densities and yields below 430 kg/ha. In the semi-intensive farming, stocking densities vary from 10 to 18 post larvae per square meter; artificial food is used in this system and yields reach 3 000 to 4 000 kg/ha. One farm uses the intensive system with a stocking density of 100 post larvae/m2 (MINEC, 2010 Desarrollo de la cadena de valor para los productos de acuicultura continental y sus derivados. Modelo productivo para la mipyme acuícola).

Approximately 500 people are employed in aquaculture, of which 16.5 percent are women. Only the larger businesses employ aquaculture professionals and administrative staff. Overall, tilapia aquaculture generates 234 jobs and shrimp farming generates 228.

The Centre of Fisheries and Aquaculture Development, through the Aquaculture Division, has at its disposal human resources and infrastructure in four stations which support producers. Major services provided are training, production assistance, seed supply and assistance for external cooperation and financing for projects.

The total population of the country is 6 874 926 individuals. The consumption of fishery products is estimated at 5.0 kg per inhabitant. The GDP was 15 823.9 million dollars for the year 2004.

During 2004, 229.8 tonnes of tilapia were exported, mainly to the United Status and 177.6 tonnes of white shrimp were exported to China, The Virgin Islands, Japan and Taiwan.

The total value of exports was US$ 2 252 800. Aquaculture contributed with 11 percent or total exports registered in 2003.During 2004, 2 415.83 tonnes of concentrated feeds were imported for aquaculture. Pellet was the most frequent presentation, with levels of 25-32 percent protein. Fresh feeds are not currently used for aquaculture.

The most important problems faced by aquaculture producers are: water quality, the cost of the land, the quality of the seeds, production capacity, and diseases associated to the white leg shrimp, and the effect of the reduction of prices caused by the uncontrolled importation of shrimp. Aquaculture faces economic threats due to the effect of price distortions in the market and the rise of production costs; sanitary threats caused by new diseases; and environmental threats due to pollution.

Strengths arise from public policies that support aquaculture, the accumulated experience in culture, favorable climate conditions, high commercial value and fast growth of the cultured species. There are great opportunities in the association of producers along the chain of value, the opening of new conditions for external trade, the development of new production technologies.

Aquaculture yields vary according to the technology used. Thus, intensive tilapia farming attain yields that exceed 10 tonnes/ha; semi-intensive 2.5-5.0 tonnes/ha; and extensive farming in reservoirs produce less than 1.5 tonnes/ha. Yields for marine shrimp farming per hectare are: artisanal, 142kg/ha; extensive, 230kg/ha; semi-intensive, 2 900kg/ha; and intensive, over 6 tonnes/ha (production statistics of the Aquaculture Stations, CENDEPESCA, 2004). The national aquaculture production has increased, from 395 tonnes in 2001 to 1.130 tonnes in 2003 which is equivalent to a 286 percent increment, while total fisheries production has varied from 7.818 tonnes to 13 711tonnes, only a 175.37 percent increment (Annual Fisheries Statistics, CENDEPESCA, 2001, 2002 and 2003). The significant increment in production is due to the farming of tilapia and marine shrimp.

The availability of professionals in aquaculture is limited to approximately 15 professionals distributed amongst the public sector, universities and the private sector. The

incorporation of the of aquaculture as a subject matter within the syllabus of biology and agronomic engineering careers offered by the University of El Salvador and the National School of Agriculture, as well as the training through Diploma courses offered by the University Matías Delgado, have contributed to the formation of 40 professionals in the field of aquaculture.

Aquaculture generates benefits in terms of direct employment for 509 people of which 16.5 percent corresponds to women distributed in 156 units of production. The skills of staff personnel consist in the management of fishing equipment, sampling and water analysis.

Field workers seldom exceed the six years of primary school education; coordination staff generally are technicians with basic education up to technical levels; and managerial staff reach university levels of education.

The units of production are based on community associations, generally linked to external cooperation. Only industrial level companies count with professionals as part of their staff.The distribution of the area by farming type is the following: tilapia in ponds: 48.78 ha (139 ponds); freshwater prawn: 4.75 ha (30 ponds), tilapia in reservoirs: 10.39 ha (27 reservoirs); ornamental fish: 2.09 ha (165 tanks and ponds); marine shrimp: 691 ha; and tilapia in cages 9 056 m3 (122cages).

Tilapia culture, in its various production methods, generates employment for 234 people, freshwater prawn culture generates 34 employments, ornamental fish production generates 13, and marine shrimp culture generates 228 employments. The opportunities for women to participate in aquaculture are greater in the culture of tilapias in cages in which 29 women currently work, and in marine shrimp farming with 55 women currently employed

m2 (MINEC. 2010 Desarrollo de la cadena de valor para los productos de acuicultura continental y sus derivados. Modelo productivo para la mipyme acuícola).

. Table 2.2 Distribution of area by farming

DEPARTMENT SPECIES FARMING SYSTEM AREA (Ha)

Ahuachapan Marine shrimp Ponds 40

Tilapia Ponds 6.5

Santa Ana

Tilapia Canals 0.1

Tilapia Canals 1.5

Tilapia Ponds 5.0

Sonsonate

Marine shrimp Intensive pond 37

Ornamental fish Ponds 4.9

La Libertad

Tilapia Ponds 16.8

Ornamental fish Tank 1.5

San Salvador

Tilapia Cage 3 870 m3

Tilapia Intensive pond 37

Cuscatlán

Freshwater prawn Ponds 2.0

Tilapia Cage 3 836 m3

Cabañas Freshwater prawn Ponds 2.7

La Paz Sea shrimp Ponds 8.2

San Vicente Tilapia Reservoir 5.1

Usulután Marine shrimp Ponds

18 58 16 14 7.0 4 2 7.5 9.3 5.7 7.5 9.8 8.4 35

La Unión Marine shrimp Ponds 50

Source: Annual Fisheries Statistics, CENDEPESCA, 2000.

It is estimated that the complete process chain of aquaculture production, including marketing, generates employment benefits for 1 200 people.

2.3.4. Farming Systems, Distribution Characteristics

The principal production areas are related to the culture of tilapia in ponds, tilapia in cages and marine shrimp culture. It is estimated that 20 percent of the production units cultivate reversed-male tilapia. There is an extensive distribution of small production units, generally smaller than 0.2 ha.

According to the aquaculture method and the scale of production, aquaculture production units are distributed as follows: 15 production units of tilapia cages, 26

reservoirs for household consumption, 50 small and medium scale units, 1 industrial scale unit; 2 ornamental fish production units, 23 units of fresh water prawns, and 39 marine shrimp farms.

Currently there are two national companies that manufacture feeds for aquaculture.

Total manufactured animal feeds in 2004 was as follows: poultry, 333 581 tonnes; cattle, 29 621 tonnes; swine, 11 862 tonnes. The production of feeds for aquaculture is not registered at the General Directorate of Plant and Animal Health (DGSVA, 2005.).

The database of the Registry and Statistics Office of the DGSVA reports that in 2004, 2 415.83 tonnes of feeds for aquaculture were imported: 287.88 tonnes of shrimp feeds from Guatemala and 2 127.95 tonnes of tilapia feeds from Honduras (DGSVA, 2004).

The two most important species cultured in the country are: Nile tilapia (Oreochromis niloticus) and the whiteleg shrimp (Penaeus vannamei).Tilapias are cultivated in all freshwater environments; in cages, in small reservoirs and at an industrial scale. At present, varieties of this species include the grey tilapia, red tilapia and improved varieties for higher meat yields. The production of tilapia has increased since 2001 when 28.86 tonnes were obtained, to 654.1 tonnes at present as a result of the increment in the number of farming units, particularly cages, and the establishment of an industrial scale farm.

The farming of marine shrimp has increased from 363 tonnes to 472.9 tonnes in that same time period as a result of the implementation of external cooperation projects.

At a smaller scale, the production of giant river prawn (Macrobrachium rosenbergii) follows in third place, with a volume of 3.5 tonnes (CENDEPESCA, 2003).

Extensive

Its main traits are the low stocking densities and the limited management or control of water quality. This system is practiced in the 26 reservoirs used for tilapia farming and in 25 production units of marine shrimp. The stocking densities of tilapia do not exceed 1 to 2 fish per square meter and the yields reach 700kg/ha. In the case of marine shrimp, there are two modalities: in the first one post-larvae are trapped in a tidal pond which has a water intake and walls. Water exchanges are subject to tide levels; fertilizer is used to improve natural food productivity. The stocking density is not predetermined, and yields are of the order of 430 kg/ha. The second modality consists in trapping shrimp brought in by the tides and then keeping it in minimal water exchange conditions until harvest. This is only done during the

rainy season because this same ponds are used for salt production during the dry season.

Yields may reach 142 kg/ha (CENDEPESCA, 2003).

2.3.5. Competitiveness in the local Market

Consumption of tilapia in El Salvador has been noticeable, it has increased for more than half pound per capita in the year 2001 to 2013, and this condition of growth allows to project that the local market has the capacity to absorb the double of its consumption.

For the local direct consumer the price has increased from $ 2.25 (2002) to $ 2.75 (2013). In the local market tilapia has a big negative competitor, which is the wild tilapia, that grows in a natural way in continental waters, first of all golfs, this has particular mud flavor which makes sometimes population reject this fish, so the goal of the producers is to take away this negative image. The elaboration of a brand is a good strategy for this. In the following figure we can appreciate the local consumption of tilapia:

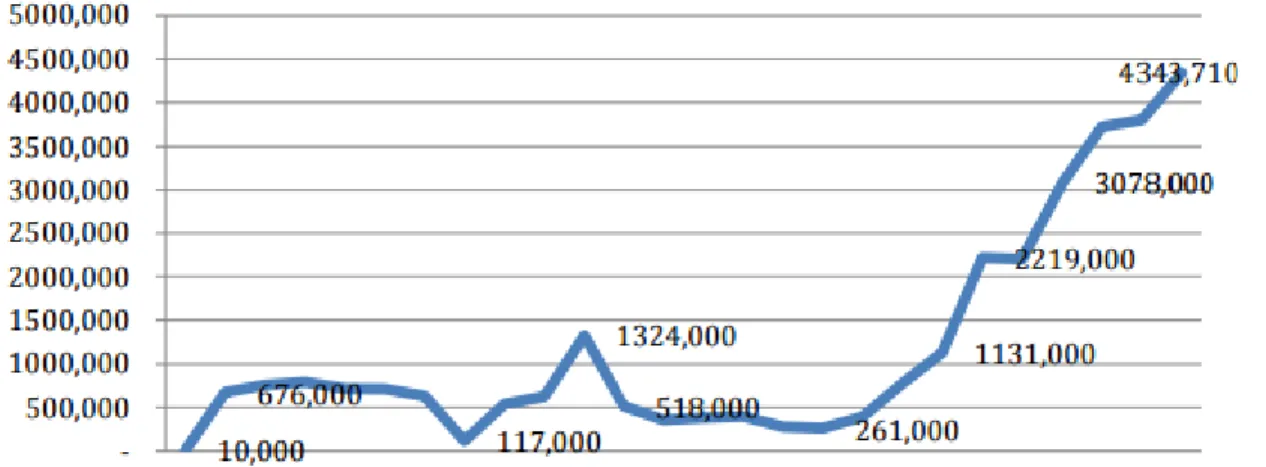

Figure 2.6 Local consumption of tilapia in Kg in El Salvador

Source : IIICA 2013

Semi-intensive

This system is practiced both for tilapia and the two types of shrimp (marine and freshwater). The stocking densities of tilapia vary from 4 to 8 per square meter; the main source of food is formulated feeds with 25-32 percent protein. The yields of this farming system are of the order of 5 000 to 8 000 kg/ha. Ponds are not aerated and water quality is control exerted by periodic exchanges of water. For freshwater prawns, stocking densities vary from 5 to 8 per square meter and formulated feeds with 28-35 percent are used. The production cycle lasts 6 months, with yields of 2 000 to 3 500 kg/ha. The stocking densities of marine shrimp are 10 to 18 per square meter; hatchery produced post larvae are used and disease prevention measures are put to practice. Production cycles last 3 to 4 months, with yields in the order of 3000to4000Kg/ha.

Intensive

There are two farms, one for the farming of tilapia and another of marine shrimp, which apply this technology in which the system depends on aerators to maintain high levels of biomass with stocking densities in the order of 75 fingerlings per square meter to obtain yields that exceed 12 tonnes/ha; and in the case of shrimp, 100 post larvae per square meter to obtain yields above 6.4 tonnes/ha. These two farms operate at an industrial scale, vertically integrated adding value by processing their products to gain access to specialized markets.

Cage culture is also practiced under this system as stocking densities are of the order of 75 fish per square meter.

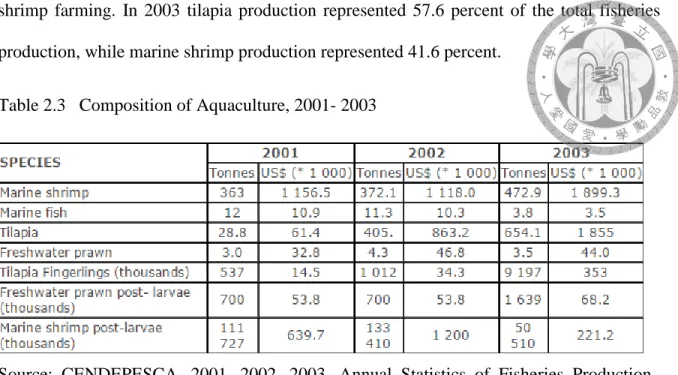

Production of aquaculture is presented in Table 2.4.One of the factors that have contributed to the increment of aquaculture production is investments in tilapia and marine

shrimp farming. In 2003 tilapia production represented 57.6 percent of the total fisheries production, while marine shrimp production represented 41.6 percent.

Table 2.3 Composition of Aquaculture, 2001- 2003

Source: CENDEPESCA, 2001, 2002, 2003. Annual Statistics of Fisheries Production.

The supply of aquatic production to markets is carried out by wholesale traders who transport the product from farms to the marketing points. Production is concentrated at the wholesale market La Tiendona from where it is distributed to retail traders of the different public markets. The public market system operates similarly in the cities of Santa Ana and San Miguel. Produce for these markets are under the presentation of whole and fresh.

The other marketing modality is the sale of live fish. A group of producers is invited to participate and concur to a single marketplace which has been previously promoted in different localities. It is estimated that during 2015 approximately 60-70 tonnes of tilapia were sold under this modality, right.

The third practice is the sale of processed fish and shrimp which is distributed to consumers through supermarket chains. The major part of aquaculture produce is sold through public markets.

The Export Centre of the Central Reserve Bank of El Salvador reports that the exports of aquaculture products consisted primarily of tilapia and shrimp. The final destination of fresh tilapia exports was Guatemala; while that of tilapia fillets was the United States of America. Aquaculture produced shrimp is exported to Taiwan and The Virgin Islands.

The certification of the products corresponds to the Inoquity Division of the General Directorate of Plant and Animal Health (Ministry of Agricultura and Husbandry).

Certification regulations are approved by the National Council for Science and Technology (CONACYT 2010).

Figure 2.6. Exports from El Salvador of Tilapia 2012

Source: Central Reserve Bank 2012 (www.bcr.gob.sv)

Out of the 156 aquaculture units under production, 90 percent have surface areas under 5 hectares, Now a days this percentage has grown. All tilapia culture cages belong to groups of fishermen or inhabitants of riverine communities alongside reservoirs or inland bodies of water. Total national production for internal consumption of tilapia is 273.7 tonnes. It is

noteworthy that the production of small units is destined to neighbouring communities thus contributing to increasing rural consumption levels. The per capita annual consumption of fishery products in the country is estimated to be 5 kg. (PRADEPESCA, 1995).

A noticeable fact is that small ponds (under 0.05 ha) and reservoirs for multiple water usage are being constructed in the central and oriental zones of the country with the support of NOGs and private initiatives. 1 368 families derive direct benefits from these production units: 765 from the culture of marine shrimp, and 603 from tilapia culture (of which 197 correspond to cage culture units owned by community organizations. The General Directorate of Statistics and Surveys indicates that in 2004, 603 305 (19.3 percent) households are in a state of extreme poverty. Most of them are located in zones where the before mentioned reservoirs and small ponds are being built. The contribution of industrial scale aquaculture is reflected in exports, which in 2004 reached 407.4 tonnes with a declared value of US$2’252.800. This production requires resources such as food, energy, and direct and indirect manpower. The contribution of aquaculture to the Gross Domestic Product is of the order of 0.4 percent, which is not considered to be significant to the national economy (CENDEPESCA. 2005).

The organization responsible for the administrative control of aquaculture is the Fisheries and Aquaculture Development Centre (CENDEPESCA), which depends of the Ministry of Agriculture and Husbandry. Its specific responsibilities are to establish a research and promotion programme for the development of aquaculture, to register all aquaculture production units, to grant permits for aquaculture, to authorize the introduction of new species for aquaculture and to punish the non-fulfillment of the General Law for the Management and Promotion of Fisheries and Aquaculture (Legislative Assembly, 2001).

The Aquaculture Division has two Areas: Generation and Transfer of Technology and Promotion and Extension. The four aquaculture stations of CENDEPESCA: Santa Cruz Porrillo, Atiocoyo, Izalco and Los Cóbanos belong to this Division. Several private sector aquaculture producer associations have been constituted. The Chamber of Fisheries and Aquaculture (CAMPAC) has a national coverage and groups industrial fishing and aquaculture companies. This Chamber maintains a close liaison with CENDEPESCA because its delegates are members of the National Commission of Fisheries and Aquaculture.

This Commission was established by the Law and acts as consultative body. There is also the Aquaculture Association of Atiocoyo formed by tilapia producers and which has promoted the construction of earthen ponds in the Atiocoyo region. Results have been very encouraging since tilapia production has increased three-fold. In the case of marine shrimp aquaculture, the organization SOCOPOMAR groups twenty producers and is currently promoting an external cooperation project for the strengthening the production technology of its members.

Existing laws related to aquaculture are the following: 1) General Law of Management and Promotion of Fisheries and Aquaculture. It is executed by the Fisheries and Aquaculture Development Centre (CENDEPESCA). This law defines concepts, the procedures for accessing to aquaculture and the obligation and duty rights for this activity. The Director General of CENDEPESCA has the faculty to apply it through resolutions. Judicially, it belongs to the field of administrative law.2) Environmental Law. It is applied within the scope of punitive law. It regulates aspects related to the environmental impact of each productive unit. The institution responsible for its execution is the Environment and Natural Resources Ministry (MARN), which also executes the Law of Natural Protected Areas, which regulates the economic activities within fragile areas. It is particularly relevant for

aquaculture in state leased areas, amongst which the albino lands of the salty forests stand out, being legally considered as fragile environments and national heritage.3) The Law of Plant and Animal Health establishes the procedures and authorizations for the importation and exportation of aquaculture products, in addition to the laws related to the innocuous processing of fisheries products for human consumption. In relation to the same matter, the Health Codex is executed by the Ministry of Public Health.

Chapter III SWOT Analysis

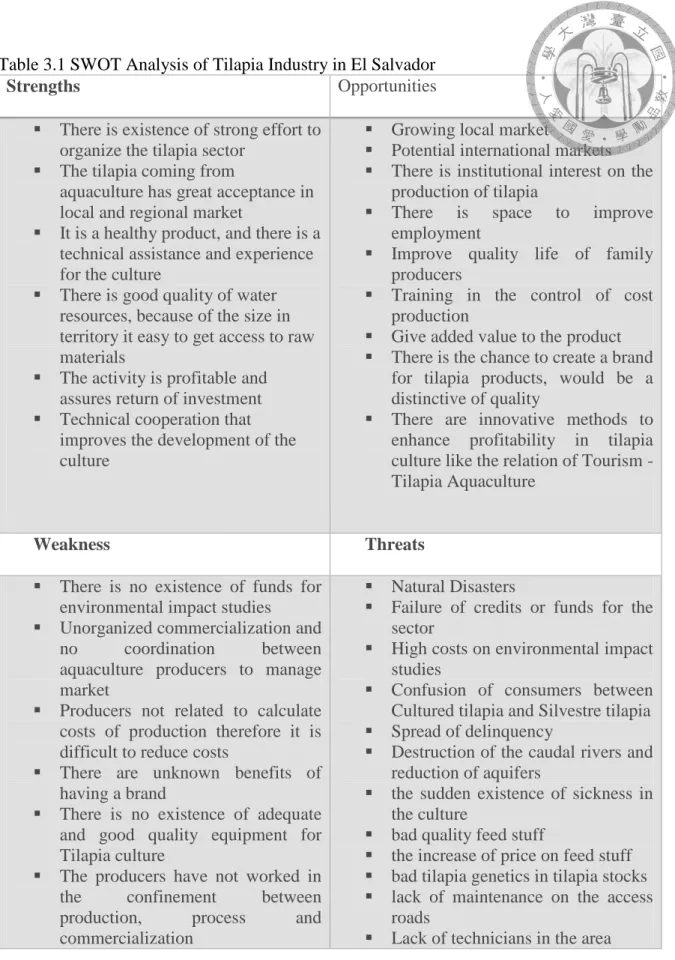

This SWOT Analysis for El Salvador will make possible to make important qualitative data analysis in order to end up with valuable conclusion on factors that determine the development of tilapia industry in El Salvador. In order to minimize the internal unfavorable conditions weaknesses and opportunities were analyzed, and finally the threats and weaknesses will help to reduce the internal and external unfavorable conditions that this industry is currently facing. In response to the problem approach using the data gathered and SWOT analysis we can evaluate that In order to meet new challenges and opportunities under current circumstances and the process to devise different development strategies, this study can give or provide a better local scenario because the ultimate beneficiaries are the families in need of food and the people who needs employment which is the main purpose of this study. The strategies generated integrate all the advantages has in terms of tilapia industry development. As well the introduction of new technologies as proposed in the study can be beneficial for small producers in the industry in terms of increasing production. As well

innovation of production and commercialization will give an added value to the final product making a significantly improve in demand. This method has been adapted in order to discuss internal strengths of tilapia industry in El Salvador as summarized in Table 3.1. Historically, aquaculture has being a marginal economic activity in the agricultural sector due to a traditionally agricultural attitude in terms of the main economic activity. It was until 2000 that aquaculture policies were formulated in the context of fisheries development. (Ministry of Agriculture and Husbandry, 2000). At present, the agricultural policy establishes the following actions:

Institutional, productive and commercial reconversion of the fisheries sector.

To reconvert productively and commercially industrial fisheries and aquaculture.

To promote the national consumption of fisheries and aquaculture products.

To promote innovative aquaculture with new species and technology.

To create the Fisheries and Aquaculture Warrant Fund.

Institutional planning of aquaculture has evolved from actions based on the operation of aquaculture stations, essentially the production of tilapia fingerlings for restocking of reservoirs, continuing with the adoption of aquaculture technologies of freshwater prawn and marine shrimp, to the introduction of new species (oysters) to begin research on their culture.

Institutional planning is oriented to the cornerstones of zone management, production and coverage. In relation to management, proposals have been put forward for the updating of the Aquaculture Registry which at present records only 40 producers and which should also contain a databank on the characterization of their aquaculture practices. Regarding coverage, several strategies have been considered, including the participation of Producer’s Associations, NGOs, education and training institutions and external cooperation to assist

the largest possible number of producers by means of training and extension on specific themes. To promote the increase in production, actions are oriented to upgrade culture practices, in particular those in which infrastructure is being under-utilized due to the application of extensive and artisanal technology.

Financing

Except for the actions impelled by the government with the participation of cooperation organizations, there is no governmental plan encompassing a specific allocation for aquaculture development within the ordinary budget. This can be observed in the yearly assignment to CENDEPESCA, which on average does not exceed one million US dollars per year and which is designated namely to salaries and basic services (Ministry of Finance, 2005). In summary, there is no financing for investment allotted by the ordinary institutional budget; neither have external cooperation projects financed investment in aquaculture.

However, it should be pointed out that with external assistance, some NGOs do provide support to communities dedicated to small-scale aquaculture, particularly in cages, reservoirs and sea shrimp.

Planning

The Office of Policies and Strategies blames the anti-agricultural and anti-rural bias of the macroeconomic policies as part of the internal environment elements which have affected the performance of the agricultural sector, and in consequence fisheries and aquaculture.

Even though FAO and EU-sponsored technical documents have been prepared for the development of aquaculture (Salgado, R. 1997; FAO, 1995), the institutional planning does

not include strategic actions to prompt aquaculture development, being rather dependent on the financing capability of the State. However there is potential for synergy by channeling the various available sources of resources for the execution of rural development project, support to marketing, small-scale cottage industries, etc.

The Market

The increase of cultured tilapia production was affected by low prices and the commercialization structure of the internal market. The introduction of tilapia fisheries in inland waters drove prices down, due mainly to their mud off-flavor, and thus diminished the value and acceptance of cultured tilapia. Prices in the beginning of the 90’s did not exceed US$ 0.50/pound for whole fish.

The post-war effect

In the decade of the 80’s during which war took place in the country, there was no investment in economic activities. This had negative effects, particularly in marine shrimp farming. The peace agreements established the commitment of reinserting ex-fighters in productive activities. Part of this process consisted in their relocation in the salt pans and marshes areas at Jiquilisco Bay. The process of converting salt pans into shrimp ponds and the developing of human skills, -initially supported by the EU-, has taken several years to begin showing positive results. Also, the upgrading of infrastructure for shrimp farming suffered design failures which still affect production yields and the capability to operate facilities effectively.

The natural environment

The location of the country in natural disaster occurrence areas and the high levels of vulnerability constitute high risk scenarios that have adversely affected the development of aquaculture.

Interaction with the environment

In 1995 PRADEPESCA undertook a study for the territorial management and development of marine shrimp. (Currie, J. 1995); the document recognizes the potential for the development of between 3 000 to 4 000 hectares for shrimp farming. Of these, 2 000 hectares would be located in Jiquilisco Bay as long as the monitoring assessment programme does not show negative effects on the environment. Since salt works have not been yet converted into shrimp ponds, and extensive areas are still utilized for artisanal farming of shrimp, environmental restraints have not been imposed that could constitute a limiting factor for the development of shrimp culture.

Credit

Even though lines of credit for aquaculture have been in place, producers are restrained in their capability to comply with the requirements to gain access to such funds since they normally lack the guarantees or collateral required by the financial system. This deeply affects the growth of production units located in leased national lands and waters which cannot be pledged as collateral.

Table 3.1 SWOT Analysis of Tilapia Industry in El Salvador

Strengths Opportunities

There is existence of strong effort to organize the tilapia sector

The tilapia coming from

aquaculture has great acceptance in local and regional market

It is a healthy product, and there is a technical assistance and experience for the culture

There is good quality of water resources, because of the size in territory it easy to get access to raw materials

The activity is profitable and assures return of investment

Technical cooperation that improves the development of the culture

Growing local market

Potential international markets

There is institutional interest on the production of tilapia

There is space to improve employment

Improve quality life of family producers

Training in the control of cost production

Give added value to the product

There is the chance to create a brand for tilapia products, would be a distinctive of quality

There are innovative methods to enhance profitability in tilapia culture like the relation of Tourism - Tilapia Aquaculture

Weakness Threats

There is no existence of funds for environmental impact studies

Unorganized commercialization and no coordination between aquaculture producers to manage market

Producers not related to calculate costs of production therefore it is difficult to reduce costs

There are unknown benefits of having a brand

There is no existence of adequate and good quality equipment for Tilapia culture

The producers have not worked in the confinement between production, process and commercialization

Natural Disasters

Failure of credits or funds for the sector

High costs on environmental impact studies

Confusion of consumers between Cultured tilapia and Silvestre tilapia

Spread of delinquency

Destruction of the caudal rivers and reduction of aquifers

the sudden existence of sickness in the culture

bad quality feed stuff

the increase of price on feed stuff

bad tilapia genetics in tilapia stocks

lack of maintenance on the access roads

Lack of technicians in the area

There is no existence of good planning of sowing and production

There is no monitoring plan for the sustainability and quality on water resources

Require of consolidation of the organization of producers

Lack of business education

No formalized accounting

Susceptibility of plagues and sickness in tilapia

Inefficient quality inputs

Lack of promoting to population to consume Tilapia, where can be shown the benefits of the nutritional advantages

Lack of credit lines

Climate change Source: based on information from Tercer informe técnico MINEC 2013

With this results we can determine that the resources available inside El Salvador can improve the quality of life of some families and enforce the aquaculture, some of the direct benefits found in this study are as follow:

a) Employment b) Distribution c) Health

Some of the indirect benefits found are:

a) Education

In terms that opportunities increase in rural areas, child labor will be reduced, in the way that parents that satisfied their needs could send its Childs to school.

b) Basic services

The coming of a company to a rural area takes an improvement in services of transport, electricity, illumination, water.

c) Substitution in imports

In 2010 77 tonnes of fish were imported in El Salvador, hence the implementation or analysis of this study could help to satisfy this situation.

Tilapia is produced using a wide variety of production systems determined by the socioeconomic characteristics of the producer. As Molnar et al. (1996:9) stated, “The kind of technology used is closely linked to the socioeconomic

circumstances of the farmer, as the intensity of production often corresponds to the amount of capital investment (Molnar et al. 1996:9).” Consequently, the proper understanding of tilapia culture compels the analysis of the socioeconomic factors using multiple sources of data. However, the task is not easy, since in aquaculture, quantitative and qualitative data usually are unavailable because aquaculture is in its early stages of development (Engle et al. 1997).

Cage production is an intensive management system that facilitates the use of water bodies unsuitable for conventional production systems that require draining or seining for the period of harvest (Lazur 2000). Thus, cage culture makes possible the exploitation of public or communal water reservoirs, lakes, irrigation systems, village ponds, rivers, cooling water discharge canals, and estuaries (McGinty &

Rakocy 1989, Watanabe et al. 2002). Other economic advantages of cage

production over pond production are that the level of initial capital investment is low compared with open ponds (Watanabe et al. 2002), and that by concentrating fish, the farmer has better control over feeding and harvesting. However, the disadvantages include higher risk of poaching and water quality problems, and reliance on commercial feeds s (Lazur 2000, Watanabe et al. 2002).

The study has several limitations given the nature of the data source. In general, producers do not keep written records of production costs, sales, and in most cases do not verbalize perceptions regarding the opportunity cost of land and

other assets. FAO (1996:35) noted, “Because the products of small-scale rural aquaculture are only partially marketed, and objectives relating to the production of fish are only part of the story, quantification is inherently problematic.” Small producers, in fact, only market a fraction of their production and do not keep records of their transactions.

Chapter IV

Development Strategies

4.1 Porter´s Diamond Model

Offers a model that can help understand the competitive position of a nation, enables a better understanding of needs and desires of a home country demand, can help shape the attributes of products and creates pressure for innovation and quality. The concept is shown in Figure 4.1.

Figure 4.1 . of Porter´s Diamond Model

Source: Porter (1991)

The development of the aquaculture sector, dedicated to the production of Tilapia in El Salvador implies a series of strategic actions that must go in a concatenated manner that allows the sustainable development. It means that trough programed management natural resources should be used properly, it is also necessary to obtain the base and orientation to make the technological changes of producer and institutions in the government, that would assure the economical befits of the population without affecting the environment.

The sustainability in the sector depends on including at least three components:

economic sustainability, Social and Environmental. Each of this components counts with determining characteristics: Human capital, natural resource and economic capital that it is generated through the activity. The adequate interaction and regulation between this factors it is what allows that the sector properly develops, generating dynamism in the regional and national economy. Sustainability is a key point in development, must be accomplished through planning and controlling producers to take care natural resources, in a way that there is well usage of natural resources without impacting negatively the nature but as well that allows appropriate economic use.

Figure 4.2 Sustainability Chart

Source: made by this study.

Control and planning

Social and Territorial Order

Conservation Social

Environmental Economic Sustainability

Factor conditions

Land, location, natural resources, labor, local population size. Specific resources in the industry can be created to compensate some of the disadvantages in this factors.

Countries such as El Salvador with growing consumption power had the advantage of the large coastline and also water resources in land. Tilapias are cultivated in all freshwater environments; in cages, in small reservoirs and at an industrial scale. At present, varieties of this species include the grey tilapia, red tilapia and improved varieties for higher meat yields.

Hence the key factor here is the environment were the country is located and the availability of workers for the area, which makes possible the culture of tilapia to develop adequately.

Demand conditions

In the home market of tilapia can help develop advantage environment, analyzing the trend on the demand of fishery products to innovate faster and create new trends.

Growing consumption power, the country’s population is increasing therefore the demand of sustainable food such as tilapia plays an important role. This can be increased by applying new technologies and innovative strategies to promote tilapia sales in El Salvador.

The production of tilapia has increased since 2001 when 28.86 tonnes were obtained, to 654.1 tonnes at present as a result of the increment in the number of farming units, particularly cages, and the establishment of an industrial scale farm.

Related and Supporting Industries

Can help produce inputs that are important for innovation and internationalization of tilapia industry. These industries provide cost-effective inputs, but they also participate in the upgrading process, thus stimulating other producers in the chain to apply the same innovative techniques.

Related industries like Shrimp industries in El Salvador are also of great importance for the development of aquaculture, Marine aquaculture mainly consists of the farming of marine shrimp (paneus vannamei) with a program sponsored by the US Agency for international development (USAID) and Tilapia developed by Taiwan ICDF cooperation by establishing marine Net Cage culture, producing all male tilapia fingerlings, and promoting household fish farming for Tilapia. This has stimulated with great extent the production, innovation and development techniques for the industry.

Industry Strategy and Structure

Constitute the fourth determinant of competitiveness in the industry of fisheries. Set the goals and are managed for important success. Creates pressure to innovate.

Finance strategic projects

Strategic positioning in niche markets

Strategic planning

Management strategies