國

立

交

通

大

學

科 技 管 理 研 究 所

碩

士

論

文

An Examination of the Remittance Process for Foreign Workers in

Taiwan

研 究 生:William Jeannet

指導教授:袁建中 教授

An Examination of the Remittance Process for Foreign Workers in Taiwan

研 究 生:威廉 Student:William Jeannet

指導教授:袁建中 Advisor:Benjamin Yuan

國 立 交 通 大 學

科 技 管 理 研 究 所

碩 士 論 文

A ThesisSubmitted to Graduate Institute of Management of Technology College of Management

National Chiao Tung University in partial Fulfillment of the Requirements

for the Degree of

Master of Business Administration in

Management of Technology

December 2008

Hsinchu, Taiwan, Republic of China

An Examination of the Remittance Process for Foreign Workers

in Taiwan

Author: William Jeannet Advisor: Dr. Benjamin Yuan

Institute of Management of Technology

National Chiao Tung University

Abstract

Why is it so inefficient and costly to send money? Public policies and poor management of technology hinder the movement of money, provide inadequate services, hurt the

development of remittance and ignore a large market segment. The policies and technologies that are in practice today are harmful to the industry by driving money towards informal channels and keeping transaction costs at an unnecessarily high level. Taiwan is one of the most attractive destinations for migrant workers because of its relatively attractive wages. The minimum-wage regulation has made the average wage offered to migrants higher than that in other Asian host countries (Lan, 2006). A sample of foreign workers will be surveyed to better understand the channels, customers and dynamics of the remittance industry in Taiwan. Foreigners will be asked if and how they remit or receive funds, and if they are satisfied with the level of service.

Acknowledgements

The completion of the Master’s degree and of the Master’s thesis was not done without the support of others. I needed guidance, ideas, challenges and encouragement of many to be successful. I was lucky enough to receive this kind of aid from many sources. First, I appreciate all the input that I received from my classmates. I leaned on and learned a lot from everyone that I worked with during the program. Those experiences enriched my life. I will try to take knowledge and the friendships with me wherever I go.

I want to thank the staff and teachers at National Chiao Tung University, especially those who helped me on the journey toward the completion of my thesis. I would like to single out, Dr. Li who gave me a basic road map. Dr. Hsiao-Cheng Yu, who provided me with some great advice about my experiment, offered encouragement and of course, Dr. Grace Lin, who has been very helpful during my tenure at NCTU by providing me with “look at it from another angle”. I thank my advisor, Dr. Benjamin Yuan who showed me again that encouragement and small pushes can be fantastic motivating tools. Thank you for all your help and guidance.

A heartfelt thanks goes to my family in America, who have always supported my goals and ambitions no matter what the size.

Table of Contents

1. INTRODUCTION... 1 1.1 MOTIVATION... 1 1.2 FROM AN ENGINEER’S PERSPECTIVE... 2 1.3 PURPOSE OF THIS STUDY... 2 1.4 METHODOLOGY... 3 1.5 FLOW CHART OF FORMAL AND INFORMAL REMITTANCES... 6 2. BACKGROUND... 10 2.1 REMITTANCE DEFINED... 10 2.2 HOW DOES REMITTANCE WORK? ... 11 2.3 FORMAL VS. INFORMAL... 12 2.4 SCALE OF GLOBAL REMITTANCE... 13 3. LITERATURE REVIEW ... 14 3.1 SHAPING THE REMITTANCE ENVIRONMENT IN ASIA... 14 3.2 REGIONAL MARKET AND FINANCIAL ACCESS... 15 3.3 TAIWAN’S ESTIMATED MARKET SIZE... 16 3.4 THE DRAW TO TAIWAN... 16 3.5 MISSING FOREIGN WORKERS AND “GUESTS” ... 17 3.6 FORMAL CHANNELS... 18 3.61 BANKS, CREDIT UNIONS AND MICROFINANCE INSTITUTIONS (MFIS)... 19 3.62 MONEY TRANSFER OPERATORS... 20 3.63 TECHNOLOGY... 21 3.64 CARDS... 23 3.65 CELL PHONES... 23 3.66 MONEY ORDER... 24 3.7 INFORMAL CHANNELS... 24 3.71 TRUSTED FRIENDS AND FAMILY... 25 3.81 COST USING INFORMAL CHANNELS... 25 3.82 COSTS USING FORMAL CHANNELS... 27 4. FINDINGS AND ANALYSIS: ... 30 AGE, GENDER AND LEGAL STATUS... 30 PRODUCT AWARENESS... 30 WHAT DO YOU VALUE?... 31 REGIONAL REMITTANCE... 32 5. FUTURE RESEARCH ... 33 MARKETING OF DIFFERENT CHANNELS AND TECHNOLOGIES... 33 REFERENCES... 34 JOURNAL REFERENCES... 34 OTHER SOURCES:... 37 APPENDIX ... 38 MOBILE REMITTANCES IN PRACTICE: THE PHILIPPINE SUCCESS STORY... 38 CANADA’S SURVEY RESULTS... 40 ASIAN DEVELOPMENT BANK: JAPAN’S SURVEY RESULTS... 41 REMITTANCE SURVEY ... 43 REMITTING FROM UK:... 50 REMITTING FROM JAPAN:... 50 REMITTING FROM UK TO THE PHILIPPINES... 511. Introduction

1.1 Motivation

Every month, I make a student loan payment to a bank in the United States. The paper work process at a Taiwan bank takes about 20-30 minutes and I am charged $300 NT. The funds are sent within 2-3 business days to another bank in the U.S. where that bank charges $400 NT. Finally, the funds are sent to my bank, minus a $400 NT incoming wire fee. In the end, the remittance can cost over $1100 NT, waste as many as 7 days to reach its destination and consume a considerable amount of a day to start the process. I am not alone in feeling this frustration and inconvenience. So why is it so inefficient with our existing policies and technology to transfer money? Is there a better way to transfer money?

As a global aggregate, workers’ remittances are the largest source of foreign

financing after FDI, exceeding both official development assistance and portfolio investment by a wide margin. In 2004, remittances to India, China, and Mexico alone amounted to $60 billion, compared to $80 billion in official development assistance worldwide. For a number of developing countries, remittances beat merchandise exports as the prime foreign exchange earner and some 20 countries reported remittances equivalent to 10 percent of GDP or more (Lueth & Ruiz-Arranz, 2006). Given remittances’ scale, trend, and impact on the global economy, their determinants need to be better understood.

The purpose of this paper is to better understand the remittance environment for migrant workers in Taiwan. In doing so, I will examine how remittance firms operate in Taiwan and the customers that use them. I will collect new data on the cost of sending money home and explore how transaction costs vary with source and home country features. In addition, it is important to look at the factors driving these transaction costs and the policies that regulate and burden the industry.

1.2 From an Engineer’s Perspective

If we look at this problem from an engineering design standpoint, we can see there is a lot of variance from the ideal position. Ideal conditions would allow remitters to

immediately send money (or credit) at a low cost and convenient way while allowing transparency for governments to combat illegal activities, such as money laundering and terrorism.

The famous engineer and statistician, Genichi Taguchi argued that quality engineering should start with an understanding of the cost of poor quality in various

situations. Taguchi insisted that companies broaden their horizons to consider cost to society. Though the short-term costs may simply be those of non-conformance, any product or service away from nominal would result in some loss to the customer or the wider community

through poor access to other financial products, higher fees, use of informal channels, or the need to build-in safety margins (Phadke, 1989). These losses are externalities and are usually ignored by the remittance companies and policy makers. Taguchi argued that such losses would inevitably find their way back to the originating corporation and that by working to minimize them; companies would enhance brand reputation, ensure customer satisfaction and generate profits. It is considered a powerful method to reduce product cost, improve quality, and simultaneously reduce development interval (Phadke M. S., 2008).

1.3 Purpose of this Study

I hypothesize that different nationalities use channels that are in line with the policies of their nation of origin. I expect to find that migrant workers from North America, Europe

and Africa use mostly banks or some monetary transfer operator, such as Western Union. I expect to find these remitters are not satisfied with the level of service due to long transfer times, security risks, high fees and inconvenient processing.

I hypothesize that migrant workers from the Asia Pacific area are more satisfied with the remittance process due to lower transaction costs, convenience government policies in their home country and fascinating technological resources, such as Smart Cards, Internet and the use of cell phones.

This study is important because so far, the study of the macroeconomic determinants of remittances has been severely constrained by the lack of data. Every year, the International Monetary Fund (IMF), publishes, Balance of Payments statistics for inward and outward remittances for a given country. It is considered the main data source on remittances.

According to the IMF, Taiwan falls under the Peoples Republic of China therefore no data is available to clearly describe the remittance environment for migrant workers in Taiwan. (Lueth & Ruiz-Arranz, 2006),

Taiwan's economy is a major draw for many migrant workers, therefore

understanding the “who, where, why and how” is significant. I will model a 2006 British, Department for International Development, remittance survey study and a similar study that was conducted in Canada. This study is different in that I'm including some fascinating improvements in technology and public policy. For example, the rise of some internet

remittance companies such as Paypal and Moneybookers.com and the adoption of cell phones as a means to remit in the Philippines.

1.4 Methodology

Design Summary Performance Indicators/Targets Monitoring Mechanisms Assumptions and Risks Goal Reliability of projections of Acceptance by NCTU faculty of the

Establish ways and means for foreign workers to remit funds (i) formal and informal, (ii)

evaluate the cost, speed, frequency, volume and satisfaction level the magnitude of actual fund flow Number of formal and informal channels used study’s findings. Purpose

Identify factors in the policy, regulatory, and institutional framework that have an impact on remittance flows Consistent activities of remittances sent and received Comprehensive study on the (i) movement of remittance through formal and informal channels; (ii)

remittance issues in the remitting countries and recipient countries; and (iii) economic, policy, institutional and regulatory factors affecting choice of remittance method Assumptions: · All stakeholders are interested in and support cooperating with the study.

Risk:

· All stakeholders are not interested in and do not support cooperating with the study.

Outputs

Provide data on estimated fund flow from foreign workers in Taiwan through formal and informal channels. Gauge level of satisfaction, speed, cost, differences in country of origin, Comprehensive data on fund flow in Taiwan is presented in the paper.

Issues and actors affecting selection of fund flow channels are identified. Feedback on the proposals, from foreign workers, MTOs, NCTU professors , banking and microfinance units · The proposal presentation, advisor meetings, final presentation, and final report are of high quality and submitted on time.

Design Summary Performance Indicators/Targets Monitoring Mechanisms Assumptions and Risks Activities: Review remittance flows from overseas workers in Taiwan

Analyze relevant laws and regulations of the remitting and receiving countries within the region.

Consult NCTU professors, foreign workers and conduct field visits and empirical analysis. Evaluate formal remittance channels to identify means to improve their

reliability, speed, and cost.

Survey sample size is large enough to be statistically valid. Information on the subject is relatively abundant, easy to locate and can be analyzed effectively.

Feedback from NCTU advisors, foreign workers and remittance officials.

Risks:

· Qualified subjects are not available.

· Data are not

available and research findings are not relevant.

· Survey subjects do not follow the

instructions.

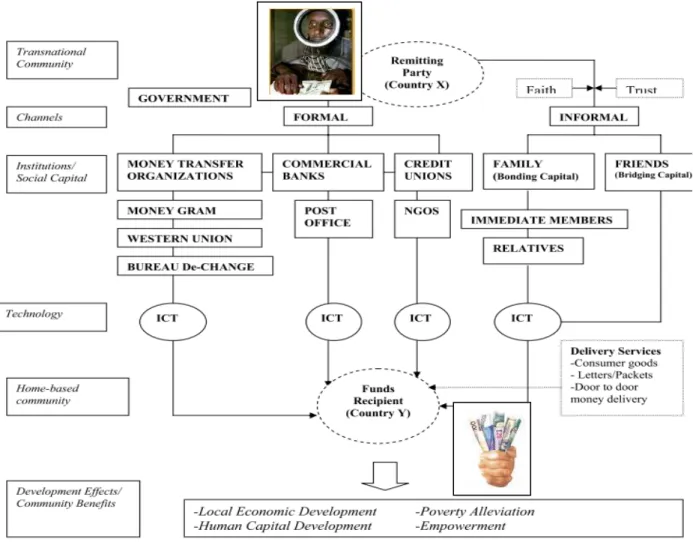

1.5 Flow Chart of Formal and Informal Remittances

Figure 1. Framework for International Remittance Income Transfers, 2006. (Maumbe & Owei, 2006)

The main objective of this paper is to contribute to the efforts aimed at harnessing the potential of remittances to countries from Taiwan by looking into the remittance flows. I want to better understand the nation of origin patterns in remittance flows within remittance-sending households and communities.

In order to achieve the objectives, a survey was conducted to identify differences in remittance sending: Amount of money, channels, frequency, reasons, preferred channels for outgoing remittances, problems and overall satisfaction of the remittance process.

The results of a qualitative methodology are not based on statistical representation but rather on structural representation. In foreign worker cases, several key variables include the country of origin, type of work performed, level of knowledge and legal status in Taiwan. For this reason, the exact number of “interviews” that need to be conducted cannot be determined.

According to the 2008 Taiwan Census, there are over 322,000 legal foreigners in Taiwan. Of those, 327,000 were employed (National Statistics, Republic of China (Taiwan), 2008). Statistics show that by the end of March 2006, the number of illegal or "missing" foreign workers in Taiwan has surpassed 23,000 (Headlines, 2006).

In order to evaluate the dynamics of the remittance industry this research was guided by the following ideas:

• Establish a basic portrait of those people most likely to remit money

• gauge the experience of those sending remittances and understand the whole process of sending money abroad

• understand motives for sending money

• look at the incidence of use of various remittances services (volume and frequency) • examine if there is a lack of transparency and understanding in the market by users; • get a better picture of the the infrastructure that is used to provide remittance services; • the possibility of adverse effects from poor or disproportionate regulation or a weak

legal framework (could be the factor driving use towards informal channels • look at competitive market conditions; and risk.

The questionnaire is designed on the basis of a self-completion format rather than the more classical face-to-face in-home interview. There are two main reasons for this approach: • The anticipated low population of willing foreigners implies that the interviewer would spend considerably more time searching for survey respondents than interviewing them. The

interviewer will leave questionnaires with the foreigner, for them to complete in their own time while the interviewer continued the search for the next eligible respondent. The

interviewer will return at a pre-arranged time/date to retrieve the completed questionnaire.

• Second, the subject matter may be perceived to be personal, or the respondent may (wrongly) feel that the survey is some form of official inspection of their residential status. The self-completion element is therefore partially an attempt to assure potential respondents that this is a legitimate research exercise and that their participation is completely

confidential.

In an effort to reach a larger population, an online survey has also been created and will be distributed to a number of foreigner based organizations, such as the Taiwan Celts Soccer League, numerous groups on Facebook.com, Taiwan Hash House Harriers, Taiwan Hockey Club, Chung Hua University, National Chiao Tung University and National Tsing Hua Univerisity foreign students, the medical center at MacKay Hospitals for foreign workers. Replies are automatically sent to a spreadsheet and the sender is antonymous. The survey can be found at:

http://spreadsheets.google.com/gform?key=pcrBge6wlr9s0BUQStUoGSQ#invite

The confidentiality of all responses will be assured to all respondents.

Fieldwork:

I, Will Jeannet, the interviewer will interview a random sample of 300 employed foreigners. Interviewing will take place November 18th – December 1st. All questionnaires will be completed by the respondent without the participation of a field interviewer.

2. Background

2.1 Remittance Defined

Each year, the IMF (International Monetary Fund) publishes Balance of Payments Statistics Yearbook, which gives the three streams of monetary transfers flowing into

countries. These are workers’ remittances, compensation of employees and migrant transfers and their sum is what the IMF uses to calculate the remittance flow (Baruah, 2007).

Remittances are broadly defined as the monetary transfers that a migrant makes to the country of origin and this paper is limited to the monetary transfers of Taiwan migrants.

It is widely acknowledged by scholars and organizations such as The World Bank and IMF that procedures, definitions, policies and collection of information have been vague and difficult to obtain. In September of 2008, the IMF released a 108 page guide called,

INTERNATIONAL TRANSACTIONS IN REMITTANCES: GUIDE FOR COMPILERS AND USERS, to help

countries define remittance and help shape the way data is collected and reported.

Remittances generate both micro and macroeconomic effects. In microeconomic terms, remittances:

• make an important welfare contribution to the receiving household and often provide emergency stopgap monies;

• tend to increase during an economic downturn or following natural disasters; • improve the standard of living through funds that are typically

• Invested in human and social capital (e.g., health care, nutrition, education) and in building assets (e.g., real estate, business, savings); and

• Generate ripple effects that impact the extended family and community beyond the receiving households, due in part to the increased consumption.

• provide a stable flow of funds that is often counter-cyclical (they increase during times of economic downturn);

• offer an important source of foreign exchange for many countries; and

• create upward pressure on the value of the local currency in cases of high inflows of remittances.

(International Fund for Agricultural Development, 2006)

2.2 How Does Remittance Work?

The remittance process involves multiple money transfer actors: the money transfer company, the agent that the company contracts to sell remittance transfers, the agent that provides the distribution on the receiving side, and the financial institution used by the

money transfer company to make transactions. Thus, in order to guarantee the transmission of money, data and money streams need to flow from a point of sale into a point of delivery, passing through a series of stages and players that ensure the success of the remittance (Orozco D. M., 2004).

An agent typically collects a commission from the fee charged to the customer in the transaction. Usually, there is also a fee added to cover the cost of currency exchange risk. The cost structure of a money transfer business thus depends on the number of agent contracts and the commissions paid to each or in the case of firms that dispatch remittances from their own offices or branches, the costs of maintaining and staffing those establishments. In some cases, expanding the number of company-agent agreements to cover a large

geographic area may lead to an increase in costs. Also, agents may bargain for higher commissions if their business becomes a magnet for remittance transfers. One method that agents might employ to increase their commissions is to take advantage of a profitable foreign exchange differential by bargaining for a percent of the differential instead of the fee.

Remittances can be sent and received at widely different types of establishments. Formal remittance economy involves MTOs (i.e. include Western Union, Money-gram, and Foreign Exchange Bureaus), commercial banks, and credit unions among others. For example, money dispatched by an agent for a wire transfer service operating out of a butcher shop in Ireland might be picked up at a bank in Taipei. Recipient country distributors also play an important role in pricing and in defining the nature of the competitive landscape. In many cases, distribution agents have agreements with more than one company. Agents thus compete to attract companies to utilize their distribution networks, and in doing so also influence pricing. They charge a commission on the fee and exchange rate charges; should these players raise their commissions, costs to customers would increase, too (Maumbe & Owei, 2006).

Moreover, banks also play a direct and indirect role in money transfers, not simply by functioning as agents, but also because they serve as intermediaries; they operate as

depositories for the money transfer companies and distributor agents. Banks likewise charge to keep money deposited in an account owned by the company or distributing agent. If a bank raises the cost for the deposit transaction, the company ultimately will pass on the costs to the sender (Orozco D. M., 2004).

2.3 Formal vs. Informal

Remittances can be sent through either formal or informal channels. We define informal remittances as money transfer services that do not involve formal contracts and hence are unlikely to be recorded in national accounts. Formal channels include money transfer services offered by banks, post office, non-bank financial institutions, foreign exchange bureaus, and money transfer operators (MTO’s) like Western Union and MoneyGram (Baruah, 2007). Informal channels include cash transfers based on personal

relationships, carried by unofficial courier companies, friends or relatives. This channel, known as “underground banking” and often operates on both sides of the law.

2.4 Scale of Global Remittance

Although it is widely acknowledged that the global flows of remittances are

increasing, a reliable estimate of the country-to-country flows, and consequently of the global value of remittances, remains elusive. Officially reported statistics on remittances seriously underestimate total flows. Migrants use various methods to remit their money and many transfers are informal and unrecorded. But even for those transfers made through formal channels and recorded, there are incompatibilities and inconsistencies among the available data sets that impede data disaggregation, comparative analysis and in-depth research (Orozco, 2007).

The latest World Bank data reveals that remittance flows to developing countries reached $251billion in 2007, up 11% on 2006 and more than double those of 2002. Mexico and the Philippines, which are among the top four remittance recipients in the developing world, reported remittance inflows for 2007 of $25billion and $17.2 billion (Timewell, 2008). These numbers are seen by some scholars as conservative since the informal market is so difficult to calculate. Other estimates put the 2007 global remittance flow around $300 billion USD (Orozco, 2007).

According to the World Bank’s Neil Ruiz, “More than 8.2 million native Filipinos work or live abroad, equivalent to almost 25% of the total labor force. About 75,000 Filipinos are deployed for overseas employment every month. Filipinos also comprise 30% of all sea-based workers in the world. Remittances from these migrants amounted to about $17bn or 13% of GDP in 2007 (Timewell, 2008). “

The World Bank states that international remittances accounted for 60 percent of income for households in the lowest income bracket. Remittances primarily pay for health services, education and food in such impoverished homes. The benefits and impact of remittance is beyond the scope of this paper.

3. Literature Review

3.1 Shaping the Remittance Environment in Asia

Dr. Manuel Orozco, a leading expert in migration and remittances; has stated that that Intermediation and transaction costs associated with a marketplace structure results from the interplay of three major factors: the type of player in the industry, the regulatory environment, and competition. These three elements help explain market behavior in the sending and

3.2 Regional Market and Financial Access

The marketplace for money transfers is mixed, with a competitive industry sending money predominantly from China (Hong Kong), the Russian Federation and Singapore, and with a less competitive and overly regulated corridor sending from Japan and Malaysia. Parallel to these industries are informal money transfer businesses, coupled with the

widespread practice of hand-carrying money when travelling. Consequently, transaction costs vary significantly. Remittance costs to Central Asia, for example, are among the lowest (if not the lowest) in the world, at an average of 3 per cent per transaction. In some parts of Asia, transfers are influenced by technological innovation, as in the case of mobile phone transfers in the Philippines (International Fund for Agricultural Development, 2008).

3.3 Taiwan’s Estimated Market Size

In 2005, Western Union estimated that there was an annual demand of up to USD 56 billion for foreign currency remittances by individuals, not including business remittances, in Taiwan. Most banks will only conduct foreign currency remittances for their own customers Although some foreign banks in Taiwan also provide foreign currency remittance services to their customers, it is difficult for many foreigners in Taiwan to meet the banks' requirements for setting up banking accounts (Department of Investment Services, MOEA, 2005).

In its Annual Report, the Bank of China (Taiwan) reported that Current Transfers Total current transfer receipts amounted to US$3,837 million in 2006, US$374 million more than in the previous year. Total current transfer payments for the year increased by US$45 million to US$7,772 million, reaching a historic high, on account of the increase in outward remittances by cross-border workers (Central Bank of the Republic of China (Taiwan), 2006).

3.4 The Draw to Taiwan

Remittances are an outcome of migration and are the most direct link between migration and development. Taiwan’s economy offers an excellent opportunity for migrant workers. The U.S.-based Business Environment Risk Intelligence ranked Taiwan sixth globally and third best in Asia in its second quarterly Business Environment Risk Report of 2007. The Business Environment Risk Report is composed of three main indices: the Operations Risk Index, Political Risk Index, and Remittance and Repatriation Factor Index. Taiwan remains ranked third globally with a score of 84 on BERI's Remittance and

Repatriation Factor. Among Asian nations, Taiwan ranks second tied with Singapore, while Japan is the regional and global leader with a RRF score of 95.

Moreover, Taiwan's economy ranked as the 22nd largest in the world in 2006 with a gross domestic product (GDP) totaling US$355.7 billion, according to the latest tallies from

the International Monetary Fund (Taipei Representative Office in the UK, 2007). This makes Taiwan a very attractive location for migrant workers.

3.5 Missing Foreign Workers and “Guests”

An interesting point of discussion but beyond the scope of this paper is the number of missing / illegal foreign workers in Taiwan. Some migrant workers are charged excessive placement fees and tied to their non-transferable employers stipulated in the contract. The financial burden, coupled with uncertainties in the renewal of contracts, contributes to the increasing number of “runaway” migrants (Lan, 2006). According to Taiwan’s National Immigration Agency, there were over 11,226 missing foreign workers in 2007 (Taiwan National Immigration Agency, 2008).

According to the police, the accumulated number of runaway contract workers in Taiwan from 1994 to 2004 is 87,198. More than 75 percent of these workers have been repatriated or left the country voluntarily, and 19,435 still reside in Taiwan (Lan, 2006).

This is significant because illegal workers tend to avoid formal methods of remittance. Where are these workers and are they still in Taiwan sending money? Also, it would be interesting to know how many foreigners come to Taiwan on “Tourist Visas” but are really here to work. Cheap flights and friendly immigration policies, allow for “workers” to go on “visa runs”.

In 2005, the UN reported there are some 300,000 thousand Thai workers living in Taiwan who continue to remit their earnings through informal financial services because of convenience. Formal institutions require formal identity, which is something that illegal emigrants cannot provide. For customers using money transmission services, accessibility is critical. With no credit history, or perhaps no experience in using a bank, the only option is the informal sector (Unitied Nations, 2008). The UN’s figures are interesting but are

inconsistent with Taiwan’s on the matter. None the less, the important point is that migrant workers are remitting funds out of Taiwan through informal channels because it is easy to do so.

3.6 Formal Channels

Remittance services are found in virtually any country, either formally or informally organized. Remittance companies play a major role here due to the following factors. Most remittance companies focus solely on remittances, so they are tailor-made for these needs If they offer other products, these are very often geared towards the same customer base (travel services, phone services, parcel services), which then gives the customers more than one reason to visit that remittance company (Ratha & Riedberg, 2005). For example, in Taiwan, some Indonesian and Filipino grocery stores can remit money but only to those two countries.

They offer locations in the cities and neighborhoods where the customers need them. Their marketing and service is conducted in a language the customers speak. In Taiwan, these shops can be found quite easily.

3.61 Banks, Credit Unions and Microfinance Institutions (MFIs)

Banks only play a major role in remittances if the legislation in place limits remittance services to banks and financial institutions, as this is the case in France for instance. In countries like the United States and the United Kingdom, banks play only a minor role in remittances.

Some banks are then focused on some very specific markets like India or the Philippines, where the legislation in the receiving country and the important banking network prove to be a major asset (Ratha & Riedberg, 2005).

The majority of banks offer money transfer services, but in most cases you must hold an account with the bank you wish to use. It is usually necessary for the person receiving the money to have a bank account also. Banks tend to be expensive and take longer to transfer your money however they do offer additional security and opens the door for additional financial products such as loans, mortgages and savings accounts (SendMoneyHome.org, 2008). The World Bank

Several factors explain why these large banks do not consider remittances to be their core business and hence only offer it as a marginal product, if at all:

• Larger loans and investments are more profitable than small remittances.

• Remittances are mostly sent by the kind of customers the bank does not consider to be prime customers, as these are mostly low net value customers.

• From the remitter’s point of view, large banks are often intimidating.

• Remittances are often sent to developing countries and rural areas, while large banks tend to be present in the more affluent countries and areas.

3.62 Money Transfer Operators

Money transfer operators (MTO) are formal remittance channels available worldwide. Western Union operates in over 200 countries (Western Union). The main advantages

perceived by users are the access, speed, reliability and simple procedures. MTO’s like Western Union and MoneyGram, have good brand recognition (the have enormous marketing budgets) however they are one of most expensive channels to use (Baruah, 2007).

As money transfers are being subjected to more intense scrutiny by regulators, the remittance industry has experienced a shift in remittances from informal to formal

channels. But the same regulations have also increased the documentation requirements for opening bank accounts. Large money transfer operators (MTOs) have therefore benefited from the shifting flows (Ratha, Mohapatra, Vijayalakshmi, & Xu, 2008).

There are a few smaller firms like BTS, Vigo and Ria Envia that offer remittance services but are not widely availble. Some smaller firms offer service at lower costs and can do so because they focus on a single or few corridors and either have no desire or means of expansion. One example is First African Remittances of Maryland and Virginia which offers services only to Ghana (Ratha & Riedberg, 2005).

There are a substantial number of Wesntern Union and MoneyGram locations in Taiwan. Most agencies are stratigically partnered with a major Taiwan bank. For example, there are over 50 Western Union locations in Taipei City. And there are 43 cities in Taiwan that have at least one Western Union location.

Western Union and MoneyGram are just beginning to implement online remittance and telephone services to send money. While these companies are trying to make the

remittance process easier, the fees are still among the highest and not without other problems. As I will discuss later, MTOs are burned by government policies and regulations which can

cause delays and increase transaction costs. Some complaints have involved security issues. This will be covered under the section, “Time Constraints”.

MoneyGram charges a flat rate of USD $12 to send money from Taiwan expect to countries with high volume such as the Philippines and Mexico (MoneyGram, 2008) The website claims the funds will be available within 10 minutes but some customer complaints say it can take up to 10 days. Western Union has also received a number of complaints regarding, poor customer service, time delays and high fees (Review Center, 2008). Are there any restrictions on sending money?

Yes. The maximum amount you can send varies by country and how often you use our service. Also, online service is not available to all the countries. Keep that in mind if you don't see your country in the list.

3 Subject to applicable taxes, if any. In addition to the remittance charge, licensed Taiwanese foreign exchange banks may collect the exchange difference when converting the remittance into foreign currency through Western Union Remittance System or at the locally posted exchange rate.

4 Payouts in US dollars cash in Taiwan may be subject to a surcharge imposed by Taiwanese licensed foreign exchange banks. Please contact the banks for details.

– Western Union, https://wumt.westernunion.com

3.63 Technology

There are more and more companies offering new ways to transfer your money and use new technologies for remitting money. The main ICT that currently supports the

remittance economy include internet, email, cell-phones, high frequency radio communication, Voice over Internet Protocol, (VoIP), smart cards, cash passport and Automated Teller Machines (ATM) debit cards for family members (Maumbe & Owei, 2006).

Money can be sent over the internet through secure online services, often for a very small fee, but you will need to have a bank account or credit card and access to the internet to transfer the money; you will also have to register your details online. The person you are sending the money to may also need a bank account and access to the internet, but this is not always the case.

There are also some technologically very advanced methods of sending transfers. Remittance systems like ikobo.com essentially use the Internet as a means of transferring remittances. Other services like PayPal do not focus on immigrants to transfer money, but technically move money between virtual accounts. Most of these sites are regulated so you are only allowed to have one bank account linked to one person. For

example, I wanted to link my US account with my Taiwan account but PayPal, Revolutionary Money and MoneyBookers.com will not allow it. In addition, the movement of the funds can take up to 3-7 business days to upload to your account. They say the transaction is “real-time” and maybe it’s fast, but it’s not cash in hand in “real-“real-time”. There is usually a wait time to withdraw the funds and there is also a fee for doing so, although the fees are minimal. Moneybrokers.com charges up to .5 EUR to withdraw the funds. PayPal can take 3 business days to move money from your brick and motor bank to your online account

3.64 Cards

Prepaid cards have evolved and are now starting to become recognized as a

convenient alternative to the traditional methods. A prepaid card operates in the same way as a credit card or debit card and tends to have many benefits. The cardholder would have to load funds onto the card before using it and can only spend what you have on the card. Prepaid cards are available in selected shops, or can be ordered through the company's website online.

For instance a debit card (such as VISA or MasterCard) is sent to the recipient that can then be topped up by the sender whenever necessary. Money can be withdrawn as and when it is needed through any ATM without the recipient needing a bank account.

3.65 Cell Phones

This advanced technology is being used in the Philippines, where remittances can be sent using a cell phone20. Many cell phones are operated by pre-paid cards, which effectively are stored value cards. In the Philippines, it is possible to use the money stored on these card in many stores. This system is very efficient, as it virtually gives beneficiaries access to their money anywhere and around the clock, as well as a multitude of ways of spending the money directly on goods. Unfortunately, in many developing countries, the necessary telecom infrastructure is not in place (Smart Communications, 2008).

The mobile remittance services introduced by the Philippines’ operators in recent years have proven highly successful for all parties concerned: the operators are taking commissions on cash transfers upwards of US$100m per day, while expatriate Filipino workers are sending money home to their families faster, more cheaply, and more securely than previously possible. In the Middle East, however, millions of expatriate workers must still decide between sending money home using

both slow and very expensive), or trust their hard-earned cash to a homeward-bound friend or relative.

By PYRAMID RESEARCH

3.66 Money Order

Another method of remitting money is buying a money order, and then mailing it to the beneficiary, who then either deposits it in an account or cashes it at a check cashier, who deposits it for settlement within the bank clearing system (SendMoneyHome.org, 2008). These services are only as fast as the systems that are put in place to handle them. Mailing a money order from Taiwan to the United States can take up to 10 days and cost up to 300 NTD.

3.7 Informal Channels

Informal remittances as all types of money transfer services that do not involve formal contracts, and are unlikely to be recorded in national accounts. The choice of provider for remitting money depends on a number of factors. The most prominent among these are: the cost of the transaction, speed, security of funds, geographic proximity/ accessibility, convenience in terms of familiarity and language. The attractiveness of formal and informal channels varies greatly across these factors. Globally, studies indicate that informal channels

are cheaper than formal ones (Freund & Spatafora, 2005).

3.71 Trusted Friends and Family

It’s not uncommon to give money to trusted friends and relatives to deliver money across borders. The transaction cost is zero and the delivery time is as fast as an airplane. This option is more practical for destinations within the region, however finding trusted friends that fly frequently between Europe, North America and Africa is not.

For some, time is not an issue and using a money order and posting the funds is a low cost option. The transaction cost is low but for those that need to move money fast, waiting 3-10 business days for the mail and 2-5 business days for a foreign check to clear is not

practical. One could use an overnight delivery system but that will only increase the overall transaction cost.

3.81 Cost Using Informal Channels

There will almost always be a fee to pay to transfer money, whichever type of provider you decide to use. This will vary depending on which provider is used, the method,

the amount sent and often the country you are sending to. Some providers may offer an express service, which will cost more.

Either the money is exchanged when sending the money or when collected. Exchange rates can change on a daily basis and providers usually offer different rates from each

other. This will affect the amount of money received, so you should always check with the provider you are using before sending money.

The exchange rate spread is the difference between the retail foreign exchange rate that the MTO charges the sender and the more favorable wholesale foreign exchange rate that the MTO actually pays. Although the sender can usually obtain the specific exchange rate to be used in a transaction, the size of the spread is not available from the sending agent and requires time and some degree of sophistication to calculate. In this sense, the foreign

exchange spread is a form of “hidden” foreign exchange commission. (Kalan & Aykut, 2005) Sometimes the person picking up the money you send might need to pay another fee when they collect the money. If there is a fee, it will vary depending on the amount sent and the account the money was sent to. MTOs might not charge at all but you should check with the provider you are using. If you are sending the money to a bank account you should contact that bank about their fees (SendMoneyHome.org, 2008).

Cost has a large impact on a remitter when deciding whether to use a formal or informal channel. Globally, studies indicate that informal channels are cheaper than formal ones. The pure monetary cost (transaction cost) of remitting money across borders using official channels is estimated at approximately 13 percent of the remittance value (Freund & Spatafora, 2005).

The pure monetary cost (transaction cost) of remitting money across borders using official channels is estimated at approximately 13 percent of the remittance value. Orozco

estimates the cost of a Hawala transaction to be less than 2 percent of the value of the principal. For the informal remittance channels as a whole, Sander (2003) reports the average cost of remitting at 3-5 percent globally, although they can be higher in specific cases. Swanson and Kubas (2005) report costs from less than 1 to 5 percent. Similarly, remittances through friends, taxi drivers, etc., are also low-cost.

The costs of informal channels in Bangladesh are about 45 percent of formal costs. Apart from the general perception and anecdotal evidence of low cost of informal remittance channels, not much is known about how these costs vary with the amount transferred and the geographical location of the senders and receivers.

3.82 Costs Using Formal Channels

Formal remittance channels are typically more expensive especially banks and money transfer operators (MTOs) like Western Union and MoneyGram. At times the cost of

remitting small amounts can be prohibitively high due to a minimum fee charged by most service providers. Sanders and Maimbo (2003) report that fees for major MTOs start at about $15 and are usually structured by brackets of transfer values. Similarly, minimum fees at banks range from $5 to $50 depending on the sending and receiving countries as well as the product (Freund & Spatafora, 2005).

MoneyGram normally charges a flat rate of $12.00 USD per transaction however that can vary between corridors. Customers have options of sending $100 USD from Taiwan to the Philippines, with home delivery for approximately $3 USD. The 10 minute service costs about $12 USD.

4. Findings and Analysis:

Age, Gender and Legal Status

Consistent with a similar Canadian survey, the majority of remitters in Taiwan are between 25 and 34 years of age. It is not statistically valid, but this survey shows more males then females have remitted funds. In Canada, their survey concluded that there are 12 % more male remitters. In Taiwan, it is possible that more males completed the survey then females and thus the reason for this conclusion.

Of those surveyed, 70% said they are legally allowed to work in Taiwan. This number does not have much weight because many illegal workers that were interviewed would not complete the survey because of their legal status and fear that it could harm them.

In an attempt to gauge foreign worker’s financial capacity or products, they were asked to which products they have or use. 75% have an active Taiwanese bank account, 41% have a Taiwanese savings account, 60% have an overseas bank account and 53% have at least one active credit card.

Product Awareness

When asked which methods of sending money to family and friends abroad (remittance services) are customers aware of, 97% said they were aware they could send money via a Taiwanese bank. It’s not understood why “via friends and family” is not 100%. Apparently some don’t know that they can give money to friends or family members. What is strikingly interesting is only one person was aware of sending money using a cell phone, the quickest and one of the most cost effective way of sending money, perhaps because this service is not offered for sending money to “Western” countries, only from.

What Do You Value?

The results are interesting. Most everyone values security, don't like high transaction cost, want things to be easy for them but don't care much about the receiving end.

Security is obviously listed as the main reason for using a trusted Taiwanese bank. Just about every remittance channel has some form of security measure in place so what is the big deal? The security is there but seems to be a lack of trust. This question goes beyond the scope of this paper but would be an interesting research project.

Subjects also strongly want the cost of their transaction to be low. The majority claim their transaction costs are between $300 and 400 TWD. Some subjects commented that this question is confusing because there are many other costs associated with the transaction but most only considered the bank fee of $400 TWD. There is sometimes a “middle-man” bank fee, $300 to $400 TWD, for banks that don’t have a direct line with the receiving bank. Most banks also charge a receiving fee of $300 to $400 TWD. Also, this question does not factor in the exchange rate fees. The overall cost of remitting funds is much hire then most subjects believe.

The next factor for selection is “easy to use”. 98% of the subjects said they would prefer to use a Taiwanese or foreign bank to remit funds. The banking system is not very “easy” at all or convenient compared to using a cell phone, credit card or internet. The third

criterion for a customer’s selection is “fast transfer”. This is shocking because EEC, MOTs, cell phones, Online Banking is faster. About the only thing slower then a bank is a money order.

Customers want the transaction to go fast. The interesting part is almost everyone sending money to the "western world" uses a Taiwan bank. Three subjects, while sending money to North America, use the post or friends to send money and avoid transaction fees and they don't care too much about time or security. The banking system is one of the most expensive ways, besides Western Union, to send money and it takes a long time but everyone uses it. Why?

Regional Remittance

An interview was conducted with the remittance manager at Land Bank on Xiemen Street. She made it clear that most money sent through her bank is sent to America. An almost insignificant amount is sent to regional countries such as, Indonesia or the Philippines. This makes sense because informal channels can offer a much cheaper and faster way to send money to these places.

Asian workers, sending money home will use informal channels and their money is in the pocket of someone else within an hour for only $100 NT. They also send money home more often. Filipino workers that were surveyed

5. Future Research

Marketing of Different Channels and Technologies

The marketing for remittance; Western Union’s budget for marketing is enormous yet people are not using it. Reviews suggest that people think Western Union is an emergency only option that is normally too expensive. It’s fast and reliable but not cheap.

This paper does not look at the specific bank that a customer uses, however I don’t believe there is any preference over which bank someone uses. I suspect that very few people, for the sake of convenience, drive around to compare fees and exchange rates for banks. Especially when the frequency for money being sent to “Western” countries is lower compared to regional transfers.

References

Journal References

Taipei Representative Office in the UK . (2007, September 02). Taiwan ranks as world’s 22nd largest economy: IMF. Retrieved November 25, 2008, from ROC- Taiwan.org : http://www.roc.taiwan.org/UK/ct.asp?xItem=40225&ctNode=3244&mp=132&nowPa ge=1&pagesize=1000

Asian Development Bank. (2004). Technical Assistance for Southeast Asia Workers' Remittance Study. Japan Special Fund.

Australian Customs Service. (2008, January). Australian Customs Service. Retrieved January 2008, from rules of origin - non-preferential:

http://www.customs.gov.au/site/page.cfm?u=4400

Bank, T. W. (2006). GEP 2006 RENDS, DETERMINANTS, AND MACROECONOMIC EFFECTS OF REMITTANCES. Washington D.C.: The World Bank.

Baruah, N. (2007). REMITTANCES TO LEAST DEVELOPED COUNTRIES. Geneva: International Organization for Migration.

Cantwell, S. (2008, January 10). Press Release of Senator Cantwell. Retrieved January January 10, 2008, 2008, from United States Senator Maria Cantwell:

http://cantwell.senate.gov/news/record.cfm?id=242789&

Central Bank of the Republic of China (Taiwan). (2006). Annual Report 2006. Retrieved October 20, 2008, from Central Bank of China:

http://www.cbc.gov.tw/NewSearch_eng/marker.exe?s=3&o=4&t=0&a=15&k=1,&g=

0&MERGEFIELD=-&CODECONVERT=-&SORTFIELDS=-&SIM_START=1&SIM_NUM=10&REL_START=1&REL_NUM=10&CLS_STAR

T=1&CLS_NUM=20&LINK=-&REDIRECTTO=-&PATHLINK=-&p=remittance&c=19,1&i=http%3A%2F%2Fwww.cbc

Department of Investment Services, MOEA. (2005, August 25). Invest in Taiwan. Retrieved October 19, 2008, from MOEA:

http://investintaiwan.nat.gov.tw/en/news/200508/2005082501.html

Freund, C., & Spatafora, N. (2005). Remittances: Transaction Costs, Determinants, and Informal Flows. Washington D.C.: World Bank.

Funch, F. (2006, Septmeber 05). Ming the Mechanic: Western Union sucks. Retrieved November 15th, 2008, from The NewsLog of Flemming Funch:

http://ming.tv/flemming2.php/__show_article/_a000010-001689.htm

Grynberg, A. H. (2005). Preferential Rules of Origin and WTO Disciplines with Specific Reference to the US Practice in the Textiles and Apparel Sectors. In Legal Issues of Economic Integration (pp. 26-63). New York: Kluwer Law International.

Headlines, T. (2006, May 11). Taiwan.com.au. Retrieved May 1, 2008, from Taiwan.com.au: http://www.taiwan.com.au/Polieco/Labor/Foreign/2006/0511.html

Hernandez-Coss, R. (2006). The Impact of Remittances: Observations in Remitting and Receiving Countries. G24 XXIII Technical Group Meeting (pp. 1-44). Singapore: World Bank.

Houle, R., & Schellenberg, G. (2008). Remittance Behaviours Among Recent Immigrants in Canada. Ottawa: Minister responsible for Statistics Canada.

International Fund for Agricultural Development. (2008). Remittance Forum. Retrieved 10 31, 2008, from IFAD: http://www.ifad.org/events/remittances/maps/asia.htm International Fund for Agricultural Development. (2006). Remittances: Strategic and

Operational Considerations. Geneva: IFAD.

Kalan, G., & Aykut, D. (2005). Assessment of Remittance Fee Priciing. New York City: Developmentt Prospects.

Lueth, E., & Ruiz-Arranz, M. (2006). A Gravity Model of Workers’ Remittances. International Monetary Fund , WP/06/290.

Martínez, J. d. (2005). Workers’ Remittances to Developing Countries: A Survey with Central Banks on Selected Public Policy Issues. Washington D.C.: The World Bank. Matsas, R. (2007). Global Forum on Migration and Development. Belgium : GFMD.

Maumbe, B., & Owei, V. (2006). The Rmittance Economy in Africa: Information Communication Technology (ICT), Socio-Economica Development and Poverty Alleviation for Community Benefits. Community Infomatics in Developing Countires (CIDC) Conference (pp. 1-9). Cape Town, South Africa: CDIC.

Medani, K. M. (2002). Financing Terrorism or Survival?: Informal Finance and State Collapse in Somalia, and the US War on Terrorism. Middle East Report , 2-9. MoneyBrokers.com. (2008). MoneyBrokers.com. Retrieved November 10th, 2008, from

http://www.moneybookers.com

MoneyGram. (2008). MoneyGram International. Retrieved June 24th, 2008, from MoneyGram International: http://www.moneygram.com

National Statistics, Republic of China (Taiwan). (2008, May 17). Retrieved May 17, 2008, from Statistical Analysis :

http://eng.stat.gov.tw/lp.asp?ctNode=1608&CtUnit=758&BaseDSD=7 Nguyen, L. (2008, July 23). Cagary Herald. Retrieved August 1, 2008, from

http://www.canada.com/calgaryherald/news/story.html?id=b6b4bd2a-1e8e-46d8-a14c-8889e9adbda2

Office, U. S. (2006). INTERNATIONAL REMITTANCE: Different Estimation

Methodologies Produce Different Results. Washington DC: United States Goernment. Ofreneo, R., & Samonte, I. (2005). Empowering Filipino Migrant Workers: Policy Issues and

Challenges. GENEVA: INTERNATIONAL LABOUR OFFICE.

Orozco, D. M. (2007). Estimating Global Remittance Flows:A Methodology. Rome: International Fund for Agricultural Development.

Orozco, D. M. (2004). The Remittance Marketplace: Prices, Policy and Financial Institutions. Washington , D.C.: Pew Hispanic Center.

Phadke, M. S. (2008, May 28). Introduction to Robust Design. Retrieved May 28, 2008, from Six Sigma: http://www.isixsigma.com/library/content/c020311a.asp

Phadke, M. S. (1989). Quality Engineering Using Robust Design. New Jersey: Prentice Hall. PYRAMID RESEARCH. (2007, April 07). The Economist. Retrieved August 28, 2008, from

Global Technology Forum: Philippines: Revisiting mobile remittances:

http://globaltechforum.eiu.com/index.asp?layout=rich_story&doc_id=10527&title=P hilippines%3A+Revisiting+mobile+remittances&categoryid=30&channelid=4 Ratha, D., & Riedberg, J. (2005). On Reducing Remittance Costs. Washington DC: World

Bank.

Ratha, D., Mohapatra, S., Vijayalakshmi, K., & Xu, Z. (2008). Migration and Development Brief 3. The World Bank.

Review Center. (2008). Review Center. Retrieved November 01, 2008, from ReviewCenter.com: http://www.reviewcentre.com/products3376.html

SendMoneyHome.org. (2008, November 10). SendMoneyHome.org. Retrieved November 15, 2008, from Sendmoneyhome.org: www.sendmoneyhome.org

Smart Communications. (2008, October). Smart Padala. Retrieved November 10, 2008, from www.smart.com.ph

Taiwan National Immigration Agency. (2008, November 25). Missing Foreign Wokers. Taipei, Taiwan.

Taiwan WTO Center. (n.d.). Chung Hua Institute for Economic Research. Retrieved January 2008, from Chung Hua Institute for Economic Research:

http://taiwan.wtocenter.org.tw/www/issue/issue0109_intro1.asp

The International Bank for Reconstruction and Development / The World Bank. (2007). GEP 2007 Managing the Next Wave of Globablization. Washington D.C.: The World Bank. Timewell, S. (2008, October 06). Economics: Time to go home . Retrieved October 20, 2008,

http://www.thebanker.com/news/fullstory.php/aid/6055/Economics:_Time_to_go_ho me__.html

Unitied Nations. (2008). International Year of Microcredit 2005. Retrieved November 15th, 2008, from International Year of Microcredit 2005:

http://www.yearofmicrocredit.org/pages/whyayear/whyayear_learnaboutyear.asp#wh atisyear

Washington File. (2003, June 20). Washinton File. Retrieved January 10, 2008, from Find Law: http://news.corporate.findlaw.com/wash/s/20030620/2003062003clt.html Western Union. (n.d.). Western Union. Retrieved November 15, 2008, from Western Union:

http://corporate.westernunion.com/services.html

WTO. (n.d.). WTO ANALYTICAL INDEX: RULES OF ORIGIN. Retrieved January 10, 2008, from Agreement on Rules of Origin:

http://www.wto.org/english/res_e/booksp_e/analytic_index_e/roi_01_e.htm#p

Other Sources:

Financing Terrorism or Survival?: Informal Finance and State Collapse in Somalia, and the US War on Terrorism, by Khalid M. Medani Middle East Report © 2002 Middle East Research and Information Project.

Lan, P. , 2006-08-10 "Legal Servitude and Free Illegality: Migrant "Guest" Workers in Taiwan" Paper presented at the annual meeting of the American Sociological Association, Montreal Convention Center, Montreal, Quebec, Canada Online <APPLICATION/PDF>. 2008-10-22 from

http://www.allacademic.com/meta/p101846_index.html

Loveband, Anne (2004). Positioning the product: Indonesian migrant women workers in Taiwan. Journal of Contemporary Asia, 34 (3), 336-348. Retrieved November 15, 2008, from http://www.informaworld.com/10.1080/00472330480000141

Remittance Behavior among Salvadoran and Filipino Immigrants in Los Angeles, by Cecilia Menjivar, Julie DaVanzo, Lisa Greenwell and R. Burciaga Valdez International Migration Review © 1998 The Center for Migration Studies of New York, Inc.. Seddon, David, Adhikari, Jagannath & Gurung, Ganesh (2002). Foreign Labor Migration and

the Remittance Economy of Nepal. Critical Asian Studies, 34 (1), 19-40. Retrieved November 15, 2008, from

Appendix

Mobile Remittances in Practice: The Philippine Success Story

• SMART, the leading mobile operator in the Philippines with 22.6m subscribers has been offering an SMS-based remittance service known as “SMART Padala” since 2004. This service allows expatriates to deposit money with partnering banks in areas where high concentrations of Filipinos live, such as Hong Kong, Yokohama, and Abu Dhabi, and to specify the SMART subscriber in the Philippines who is to receive the money. The service sends a text message to both the sender and the recipient, notifying them that the money has been transferred. The recipient can then use his/her mobile account to specify the desired withdrawal amount and pick it up at a partnering institution in the Philippines. Remittances sent on the “SMART Padala” service are charged a 1 percent commission on all transactions, and subscribers pay US$0.04 per minute for airtime used in the transaction. This price is considerably less expensive than that of traditional wire services and related courier costs. The service generated 45,000 transactions in its first month, creating additional revenues for SMART via increased usage and commissions.

• The Philippines’ second mobile operator, Globe Telecom, offers a similar service known as G-Cash. At participating remittance companies in the US, the UK, Australia, and Taiwan, Filipino workers can send money via an SMS message to Globe subscribers in the Philippines. The recipient can pick up the cash from any Globe Telecom store by showing his mobile phone (with the SMS message) and a form of personal identification. The remittance companies pay a

commission to Globe of approximately US$0.97 per transaction, and the recipient, upon collecting the money, pays US$0.21 for transactions below US$21 (Php 1,000), or 1 percent of the

transaction amount for larger transfers. The service can also be used to send money within the Philippines. As of March 2006, approximately 1.3m of Globe’s subscribers had registered as G-Cash users, and the G-G-Cash system was handling about US$100m per day. Globe plans to make the service even more convenient for users in the near future by allowing many of its Mobile Communications 700,000 airtime loading retailers in the Philippines to dispense G-Cash to clients, thus obviating the need for a trip to a Globe Telecom store.

Western Union complaints:

I experience exactly the same thing. A friend had an emergency in Santo Domingo (was mugged and had no money even to eat). I tried sending money and after all the security questions the transaction was denied. Basically told to go to a local retailer to send the money. But now I was screwed because the money was placed on a hold and it would take 3-5 business days to be released. I explained my situation to them and it was like talking to a brickwall.. Basically treated like human garbage.

I have used them in the past atleast over 10 times. The agents response was that NO! I have never used them. They refused to offer any kind of assistance whatsoever. I had to call my bank and the agent was nice enough to place a conference call to their accounting department to release the hold on the funds. You cant even complain on their CONTACT US link on their site!! The text box doesnt allow enough characters. It saddens me to see how others in here have experience similar problems. But I hope more and more people read this so others can see how WESTERN UNION conducts business.

2 Oct 2006 @ 19:02 by russell @12.0.177.36 : Western Union What a hassle. The web based transfer, includes an address book.

But guess what, the fields it stores the names in are long enough

For any normal Spanish surname. So it cuts the name off without warning.

Not a bib problem if you catch the mistake. But is was a big problem for my recipient. She had to travel a long way to make the pickup, and them could not receive the Money because the middle name was missing two letters.

She instant messengeedr me, from an internet café. (only 5 blocks away) And I was able to correct the problem in less than one hour, unfortunately the delay caused my friend to travel (walking mostly) home after dark. Very scary when anyone seeing you leave the Western Union office, would know you are carrying money.

7 Oct 2006 @ 10:06 by Little Dragon @74.114.149.248 : Western Union Sucks

Western Union Sucks. THE WESTERN UNION WEBSITE SHOULD BE TAKEN DOWN. They should have a disclaimer on their site before sending "instant" money online, saying that you should be careful, there is a security system in place that will most likely decline you from sending any money, YET will still tie up your money up due to authorization holds for "upto 15 days".

Why can't they attempt their stupid verification process BEFORE putting a hold on your credit card? People send money via western union and pay this rediculous FEE for this reason: it's fast and convenient. Tieing up people's money like this is BULLSHIT. IT DEFEATS THE VERY

PURPOSE OF USING WESTERN UNION IN THE FIRST PLACE. Sadly, some people, including myself, learn the hard way: NEVER USE WESTERN UNION'S WEBSITE TO "INSTANTLY" SEND MONEY.

Send your money instantly. Yeah right. Instantly into a black hole, that is.

Website did not work in my normal browser. Very expensive. You have to call anyway to confirm, so you might as well just call! Took three attempts to send US$18 which took 30 minutes and cost US$12. Website crashes when trying to track if money has been collected. I would urge people to use PayPal at much less cost and very little hassle and MORE safe.

Canada’s Survey Results

• Immigrants arriving from poorer countries, with a per-capita GDP of less than $5,000, were more likely to send money (36 per cent) than immigrants from richer countries that have a GDP of $15,000 per person or more (11 per cent), the study found. • Newcomers from the Philippines, Haiti, Jamaica, Nigeria, Romania, Guyana and

Ukraine were more likely to transfer money back home than people from France, the United Kingdom and South Korea.

• New arrivals from Southeast Asia and the Caribbean were more likely than any other groups of immigrants to send money back home to friends and family,

• Immigrants with three or more children were also considerably less likely to send money than families with no children, the study found.

• The practice was also 12 per cent more common among men than woman. • Newcomers between 25 and 44 years of age were the most likely group to send

remittances.

• The average amount of funds sent within six months to two years of arriving was $2,500, and $2,900 after two years.

• The data used for the study were representative of 157,600 new arrivals during 2000-2001. More than 100,000 of those were immigrants permitted into Canada on the basis of their economic contributions, 42,600 were allowed in to reunite families, and 9,700 were refugees.

Asian Development Bank: Japan’s Survey Results

• The study concluded that bank and nonbank remittance procedures and remittance costs are affected significantly by legal, banking, and regulatory environments in the Philippines and the remitting countries, formal and informal transfer agencies, Philippine payment systems, anti-money-laundering issues, taxation, and other concerns.

• In analyzing remittance fund flow, typically, there is a need to examine migrant workers’ access to various remittance channels both in the country where migrant is employed and in the country where the remittances are transmitted. Also, there is a need to study costs and efficiency of remittances and availability of financial institutions or fund transfer agents, to receive funds that were sent to them by the migrant workers. Official fund transfer mechanisms have innovations such as ATM cards, credit cards and the use of cellular phones. International document courier companies also facilitate official fund transfer. Little is known, however, about the organizations and agencies involved in informal remittance and access to them. • In the recent ADB Philippine remittance study, survey results indicated that a

high percentage (80%) of Filipino remitters regularly channel their remittances, averaging $340 a month, through the banking or regulated channels. Sending through unregulated channels has been reduced, and these are accessed mostly by

workers where banking channels are inadequate or who have irregular status. • The study revealed that developments in the remittance industry allowed for

vibrant competition in the remittance market between the Philippines and

remitting countries. With the help of technology and marketing, coupled with reliable image, banks have managed to reduce costs to levels that may be considered competitive with informal channels. These costs could still be pushed down with the entry of more regulated channels and new technology-based products.

REMITTANCE SURVEY

INTRODUCTION: Thank you very much for agreeing to take part on this survey. I would like to assure you that everything you say will be held in the strictest confidence, and your details will NOT be passed to any other organization. The answers that you give will be added together with the answers from everyone else who participates to form the survey data. THIS SURVEY IS ANONYMOUS AND YOUR CONTACT INFORMATION IS NOT RECORDED!

If you would like more details about this survey, please contact: Will Jeannet

National Chiao Tung University – Management of Technology 1001 University Road, Hsinchu, Taiwan 300, ROC

Telephone: 886 0930286972

THANK YOU.

1. What is your age?

2. GENDER

3. Are you legally allowed to work in Taiwan? PLEASE SELECT ONE

4. Which, if any, of the following financial products do you currently have? PLEASE MARK ALL THE BOXES THAT APPLY

• Active account at a Taiwan bank

• Deposit (savings) account at a Taiwan bank • Other bank account

• Credit cards

• Loans

• Medical/health insurance • None of these