In this issue:

China-US Trade War: Crisis or Opportunity?

中美貿易戰:是危還是機?

Wealth Management in Hong Kong and Robo-Advisory

香港的財富管理及自動化理財顧問

│

China-US Trade War: Crisis or Opportunity?

中美貿易戰:是危還是機?

Introduction

簡介

Since 2018, the two superpowers, China and the United States, have been embroiled in trade and Intellectual property rights disputes as each has increased tariffs on the other’s imports. Further tariffs on Chinese goods and retaliatory tariffs on US goods were postponed for 90 days until March of 2019. Yet, most experts expect the specter of trade dispute to remain in the long run. This so-called ‘trade war’ has attracted heated discussions for its far-reaching repercussions around the globe and has created much uncertainty for the industries engaging in global trade. Hong Kong, in particular, as a global trading hub adjacent to mainland China, face both heightened risks but there are also opportunities. 自2018年起,中美兩國捲入貿易與知識產權 爭端,互相提高對方貨品的入口關稅。雖然其 後雙方將進一步加徵對方關稅的措施推遲90天 至2019年3月,但多數專家認為,貿易爭端的 陰霾在短時間內難以驅散。貿易戰已經在全球 範圍內帶來了深遠的影響,並對國際貿易相關 產業帶來諸多的不確定性。香港作為接壤中國 內地的國際貿易中心,也正面對著隨之而來的 風險與機遇。

Uncertainty created by disputes between the two giants

兩國爭端帶來的不確定性

Though the conflict between the US and China are mainly in global trade, the tension is not only a result of trading imbalance. As China has been eager to assert itself on the global stage in global trade, technology development, politics and even military in recent years, and the US is under pressure to remedy its long-running trade imbalance with China and find a solution to the intellectual property rights issue to maintain its position as technology leader. In fact, the imposed tariffs are used by both parties to gain concessions in the negotiations. In the long list of demand during the trade talks in Beijing, US objectives include trade deficit reduction, protection of American technology and intellectual property, and market access improvements. However, even with a signed agreement, it is uncertain whether the terms can be implemented.

中美之間的衝突主要源自國際貿易,但這種緊張關係並非單單由貿易逆差造成。近年來,中國在 國際貿易、科技、政治及軍事等領域均積極提升自己的國際影響力,而美國既要扭轉對中國的長 期貿易逆差,又要設法解決知識產權保護問題,以維持其在科技領域的領導地位。雙方均透過加 徵關稅來迫使對方在貿易談判中作出讓步。在北京進行談判時,美方提出了多項要求,其中包括 減少貿易逆差、保護美國的科技與知識產權,以及進一步開放市場等。但即便雙方能夠達成共識 並訂立協議,協議能否得到貫徹執行仍然有很大變數。

Overall impact (risks and opportunities)

整體影響(風險與機遇)

Because of time lag, until the end of 2018, the overall impact on the GDP of the countries being affected has been minor . Nevertheless, certain industries, such as the agricultural and financial industries, are already feeling the impact within a rather short period. If the bilateral disputes persist, the overall damage to the economy can be significant due to ripple effect.

由於時間的滯後性,截至2018年底,捲入貿易戰各國的國民生產總值所受影響有限,但某些行 業,如農業及金融業等卻在短時間內受到嚴重的衝擊。倘若雙方的緊張關系持續下去,將會產生 連鎖反應,對整體經濟造成巨大衝擊。

Focus study on Hong Kong

香港的形勢

Hong Kong has been an important import and re-export hub for China due to its close geopolitical ties with the mainland. Hence, it is inevitable that Hong Kong will be hard hit by the escalating trade tension between the two major economies. According to Hong Kong government figures, about 17 per cent – or HK$60 billion (US$7.6 billion) – of Chinese goods destined for the US were exported via Hong Kong, and about 9 per cent – HK$6 billion – of US exports passed through the city on their way to mainland China. The exports in question accounted for 1.4 per cent of Hong Kong’s overall trade. As such, businesses in the re-export and transshipment trade will be caught in the crossfire.

香港鄰近中國內地,一直以來都是一個重要的入口及再出口貿易中心。中美兩大經濟體的貿易戰 升溫,香港亦難以獨善其身。香港特區政府的數據顯示,中國內地約有17%的出口商品(約港幣 600億元)經香港運往美國。而美國則有9%的出口商品(約港幣60億元)徑香港運往內地。現時受 影響的出口貨量佔香港貿易總額的1.4%。因此,從事再出口及轉運貿易的企業將會首先受到衝 擊。

China-US Trade War: Crisis or Opportunity?

中美貿易戰:是危還是機?

Text 撰文: CHONG, Hui Ying Jamie (Year 2 二年級學生) DU, Yumeng Tina (Year 2 二年級學生)

│

│

ISSUE 16 May 2019

Effects of trade disputes on Hong Kong 貿易戰對香港的影響

The imposition of tariffs on each other’s goods by China and the US has been a burden for both businesses and consumers. The subsequent price inflation in consumer goods would depend on how exporters deal with the extra costs as Hong Kong relies heavily on imports for food and daily necessities from the mainland. On the other hand, due to Hong Kong’s role as a “gateway” to China, a reduction in trade activities between China and the US will

indirectly reduce the size of Hong Kong’s global supply chain market. Furthermore, Hong Kong is also vulnerable to a rise in tension on both sides. Nevertheless, the overall impact on Hong Kong hasn’t been as severe as anticipated due to the time lag between ordering and delivery. In addition, firms have been purchasing in advance to enjoy lower costs to avoid heavy tariffs. In light of the depreciation of both USD and RMB, some firms might be able to benefit from this. 中美互徵關稅對雙方的企業及消費者都帶來壓力。由於香港的食品及日常用品均非常依賴進口, 因此消費品價格會上漲多少,要視乎出口商如何應對成本的增加。另一方面,由於香港擔當著 中國市場的“門戶”角色,因此,中美兩國貿易活動減少將會間接影響香港在國際供應鏈市場的地 位。而雙方緊張關係升溫更會進一步衝擊香港。由於訂購至付運之間有時間差,香港現時受到的 影響並未如預期嚴重。另外還有很多公司搶在開徵關稅之前提前下訂單,以享受較低的進口成 本。而美元及人民幣貶值亦可能令一些公司從中受益。

Potential adverse impacts on Hong Kong

對香港的潛在衝擊

The post-trade war effect is expected to last for approximately 1-2 years even with a trade agreement. Some firms plan to bring forward plans to relocate their supply chain networks to other parts of Asia to lower costs and enhance efficiency. In addition, a reduction in import orders from the mainland will offset Hong Kong’s benefits of economies of scale from bulk purchase. Hong Kong will eventually lose its competitiveness derived from being on the route of large vessels and high volume traffic which allow last-minute orders.

Hence, Hong Kong’s role as an intermediary of value-added service providers is being challenged by competitors such as Singapore, Malaysia, Thailand and countries which are more cost-effective.

即使中美達成協議,估計貿易戰的影響仍會持續一至兩年。有些企業計劃將供應鏈

遷移至亞洲其他地區,以減低成本和提升效率。另外,內地進口訂單減少亦會削弱

香港的規模經濟優勢。香港原本具有高效處理大型貨物的優勢,因此更擅長處理緊

急訂單,但這些優勢亦將被逐漸削弱。作為提供增值服務的中間商,香港的地位將

受到其他競爭對手的嚴峻挑戰,例如新加坡、馬來西亞、泰國,以及其他更具成本

效益的國家。

Possible solutions 可能的解決方案

To reduce the adverse effects of the trade war and alleviate the dire situation, Hong Kong should diversify its trade and seek more trading partners. Hong Kong needs to be less dependent on China and position itself to be a better international trading hub, this can be achieved through initiatives such as continuous research and development of high technology and its large scale implementation to improve efficiency. Furthermore, the Government should provide more support to vocational training and upgrade the city’s infrastructure to maintain Hong Kong’s competitiveness and position as a world-class free port.

為減輕貿易戰給香港帶來的負面影響,香港宜在貿易方面作多元化發展,以及吸納更多貿易夥 伴。香港應減少依賴中國內地,並將自身發展成更具競爭力的貿易中心。加強發展高科技及透過 大規模應用這些技術來提升效率,將有助於達成這個目標。另外,政府還需加強支援職業訓練及 提升基礎設施,以來維持香港作為世界級自由港的優勢和地位。

Future outlook 未來展望

The crux of the matter is, the China-US trade war serves as an early “warning” for Hong Kong, it needs to rethink its position in the global stand. Over the years, Hong Kong has been overly dependent on its close and exclusive tie with China as its most important trading partner. In the aftermath of the trade war, more pain is expected, the effects of an economic downturn in China, recession or rising unemployment will gradually spread to the four main industries of logistics, tourism, trading, and financial services. In the long run, companies that fail to adapt will not survive while others will continue to strive and grow stronger. This can be a filtering process, eliminating inefficient firms and allowing productivity gains for the rest of the market. Regardless of the outcome of the trade war, Hong Kong should prepare for the uncertainties ahead.

中美貿易戰對香港而言是一個警號,香港應重新檢視其在全球市場的定位。多年來,香港均過分 依賴其與中國內地的特殊貿易合作關系。經過貿易戰之後,香港將因中國經濟下行而引發更多問 題,行業萎縮及失業率上升問題將逐漸在香港各支柱行業中呈現出來,包括物流業、旅遊業、金 融業等。長遠而言,不能適應變化的企業將會倒閉,另一些企業則會發展得更好,這有助於汰弱 留強,進一步提升市場的生產力。無論貿易戰未來走向如何,香港均應做好充分的準備,應對面 臨的風險與機遇。

China-US Trade War: Crisis or Opportunity?

中美貿易戰:是危還是機?

Interview with Dr Wong Wai Hung, Collin at Hang Seng University of Hong Kong. Skype interview with Professor David

Stephen Zweig.

Source:

1. Interview with Professor David Stephen Zweig (Chair Professor of Division of Social Science, Associate Dean of School of Humanities and Social Science, HKUST)

2. Interview with Dr Wong Wai Hung, Collin ( Associate Dean of School of Decision Sciences, Director of Policy Research Institute of Global Supply Chain, HSUHK)

3. https://www.scmp.com/economy/china- economy/article/3003715/australias- huawei-5g-ban-hedge-against-future-chinese/

│

ISSUE 16 May 2019

Wealth Management in Hong Kong and Robo-Advisory

香港的財富管理及自動化理財顧問

Wealth Management in Hong Kong and

Robo-Advisory

香港的財富管理及自動化理財顧問

Introduction 簡介

Wealth management is one of the major sectors of the financial services industry. It generally includes investment advisory, personal portfolio management and financial planning. Depending on the service provider, wealth management may also encompass pension, insurance, mortgage and other personal financial services. Traditional wealth management services providers include retail banks, private banks and insurance companies.

財富管理是金融服務業的一個主要範疇,其範圍通常涵蓋投資顧問、個人投資組合管理以 及財務策劃等;有些服務供應商的財富管理則進一步涵蓋退休金、保險、按歇及其他個人 金融服務。傳統的財富管理服務供應商包括零售銀行、私人銀行和保險公司。

Thriving Wealth Management Industry in Hong Kong

香港蓬勃發展的財富管理行業

Economic and Private Wealth Growth in China and East Asia中國內地及東亞的經濟和

私人財富增長

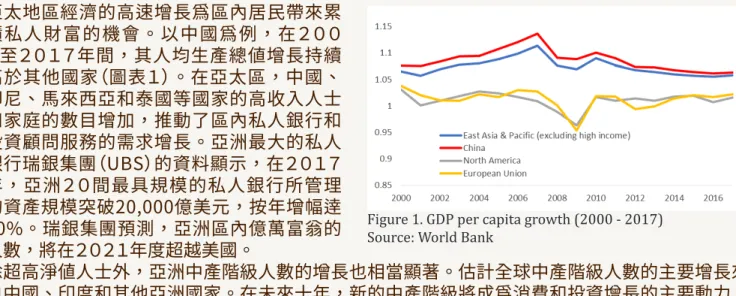

Rapid economic growth in Asia Pacific has led to private wealth accumulation in the region. China has consistently outpaced other countries in GDP per capita growth during the period from 2000 to 2017 (Figure 1).

High income individuals and family expansion in countries such as China, Indonesia, Malaysia and Thailand have boosted the demand for private banking and investment advisory services in APAC. In 2017, the asset under management (AUM) of Asia’s top 20 private banks surged by about 30% (over the previous year?), surpassing US$2 trillion, according to Asian Private Banker. UBS, the largest private bank in Asia, predicted that the number of Asian billionaires is likely to exceed that in the US in 2021.

Apart from the increase in ultra-high net worth individuals, the middle-class boom in the region is also significant. China, India and other Asian countries are estimated to be the largest contributors to global middle-class growth. The emerging middle class will be a main driver of consumption and investment growth in the following decade. This will lead to increasing demand for personal banking services such as mortgage, investment and credit card.

亞太地區經濟的高速增長為區內居民帶來累 積私人財富的機會。以中國為例,在200 0至2017年間,其人均生產總值增長持續 高於其他國家(圖表1)。在亞太區,中國、 印尼、馬來西亞和泰國等國家的高收入人士 和家庭的數目增加,推動了區內私人銀行和 投資顧問服務的需求增長。亞洲最大的私人 銀行瑞銀集團(UBS)的資料顯示,在2017 年,亞洲20間最具規模的私人銀行所管理 的資產規模突破20,000億美元,按年增幅逹 30%。瑞銀集團預測,亞洲區內億萬富翁的 人數,將在2021年度超越美國。 除超高淨值人士外,亞洲中產階級人數的增長也相當顯著。估計全球中產階級人數的主要增長來 自中國、印度和其他亞洲國家。在未來十年,新的中產階級將成為消費和投資增長的主要動力, 並同時帶動按揭、投資和信用卡等個人銀行業務的發展。

Thriving Wealth Management Industry in Hong Kong

香港蓬勃發展的財富管理行業

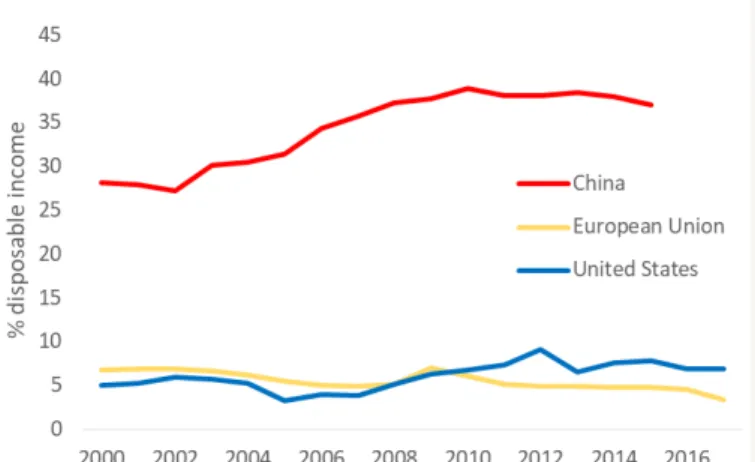

Savings Culture in China and Asian Countries中國和亞洲國家的儲蓄文化

High savings rates in Asian countries, especially China, may be another driver for wealth management industry growth. The gross national savings rate in China and East Asian countries have stayed above 35% since 2000, doubling the savings rate of developed countries (Figure 2).

A similar pattern is found when the household savings rate is compared with those of the US and EU (Figure 3). The savings rate of Chinese households is around 25% to 40% while families in the US and EU save around 5% to 10% of their earnings.

From an economic perspective, savings level is an indicator of investment level. The high savings figures and the sustaining income growth imply an enormous demand for personal investment services in China.

A report by Oliver Wyman states that RMB 104 trillion out of RMB 145 trillion in financial assets in China was in the form of bank deposits. The consulting institute expects a shift from savings to investment as a form of wealth management in China as a result of RMB internationalization and retail investors becoming more sophisticated. The huge savings of Chinese will undoubtedly fund the growth of the wealth management industry in Asia.

Text 撰文: CHAN, Ming Yan Nicholas (Year 4 四年級學生)

Figure 1. GDP per capita growth (2000 - 2017) Source: World Bank

Figure 2. Gross national savings rate Source: World Bank

│

作為大中華地區的國際金融中心,香港有絕對的優勢發展成為中國的財富管理中心。 中國內地對資本有嚴格的管制,香港的資金則具有高度的自由。2018年及2019年,香港兩度 獲美國傳統基金會評為全球最自由的經濟體。其低稅率環境和高效的政府運作均有助吸納和保障 個人財富。 相比於其他金融市場,香港在人民幣資產管理方面獨具優勢。RQFII(人民幣合格境外投資者)、 滬港通及深港通計劃為中國和全球投資者提供了接觸彼此市場和投資工具的途徑。這些政策和機 制加大了香港資金池的規模,有助促進香港財富管理業的發展。香港作為其中一個人民幣離岸中 心,在人民幣資金交易、結算和支付方面為投資者提供了不少便利。 Robo-advisory

自動化理財顧問

Robot Wealth Advisors

自動化投資顧問

Robo-advisory is an alternative to traditional private wealth management services. It requires no or minimal human input. Robo-advisory delivers investment or portfolio management services via a digital or online platform. These delivery channels are more cost effective and accessible to individuals or families whose asset value does not meet the requirement of private banking or private advisors. 自動化理財顧問為傳統私人財富管理服務提供了另一個選擇,其透過電子化或網上平台提供理財 和投資服務,以節省人力資源。這種理財方式營運成本較低,因此可降低門檻,惠及資產額達不 到私人銀行或私人顧問服務要求的個人或家庭。

Renminbi Qualified Fund Institutional

Investors (RQFII)

人民幣合格境外投資者

RQFII are permitted to channel RMB funds raised in Hong Kong to China and invest in

China’s Security market.

人民幣合格境外投資者容許中國境外的基金 使用在香港募集的人民幣資本在內地證券市

場投資

Shanghai-Hong Kong Stock Connect

滬港股票市場交易互聯互通機制

Shenzhen-Hong Kong Stock Connect

深港股票市場交易互聯互通機制

Two similar mechanisms enable mutual retail investment between the Hong Kong stock market

and the Shanghai or Shenzhen stock markets 兩個分別容許港滬兩地投資者和港深兩地直 接雙向投資內地和香港股票市場的機制

Y = C+I+G+X-M

Household Savings (SH) = Y - T - C

Government Savings (SG) = T - G

SH + SG = I + X - M

Economic implication of saving

Wealth Management in Hong Kong and Robo-Advisory

香港的財富管理及自動化理財顧問

Figure 3. Household savings Source: OPEC 亞洲人的儲蓄率較高,這在中國尤其如此。這 令區內的財富管理業存在較大的增長空間。自 2000年以來,中國和東亞國家的總國民儲蓄 率維持在35%以上,高出發逹地區一倍。 家庭儲蓄率的狀況亦類似(圖表3)。亞洲家庭 儲蓄率介乎25%至40%,遠高於歐美家庭的 5%至10%。 從經濟學角度來看,儲蓄率是量度投資水平的 其中一個指標。中國個人及家庭的高儲蓄率及 持續的收入增長,均顯示個人投資服務的需求 龐大。奧緯諮詢公司發表的報告指出,在中國 總值1,450,000億元人民幣的金融資產中,有 1,040,000億元為各種銀行存款。奧緯估計, 隨著中國的投資者逐漸成熟和人民幣走向國際 化,大量存款將轉化為投資資金,推動亞太地 區財富管理業的發展。

Thriving Wealth Management Industry in Hong Kong

香港蓬勃發展的財富管理行業

The role of Hong Kong as an international financial center

香港作為國際金融中心的角色

As an international financial center in the Greater China region, Hong Kong has an absolute advantage in developing itself into a wealth management hub of China.

In contrast to China’s capital control, Hong Kong has the highest degree of economic freedom in the world. In 2018 and 2019, it is ranked top by the Heritage Foundation’s Economic Freedom Index. Hong Kong has always had a low tax rate and boasts an efficient government which attracts and protects individual wealth.

Compared with other financial markets, Hong Kong has an edge in RMB denoted asset management. RQFII, Shanghai-Hong Kong Stock Connect, Shenzhen-Hong Kong Stock Connect are mechanisms that allow global and Chinese investors to access their desired investment tools. These policies increase the flow of capital into and the pool of funds in Hong Kong, fostering the growth of the wealth management industry. The city is also an offshore RMB clearing center, meaning that RMB funds can be traded, cleared and settled in Hong Kong easily.

│

│

ISSUE 16 May 2019

Wealth Management in Hong Kong and Robo-Advisory

香港的財富管理及自動化理財顧問

Low cost to start and to run

降低入場門檻及管理費

Private banks traditionally target high-net-worth and ultra-high-net-worth individuals only, those with at least US$ two million in liquid assets for investments. Figure 4 lists the top private banks in Asia ranked by AUM. The minimum asset value for account opening in these banks range from US$ two to ten million. Figure 5 is a list of robo-advisory service providers based in Hong Kong. The initial investment needed to set up an account with robo-advisors is much lower than that of a private bank. Robo-advisory companies pool funds from investors, regardless of their size, and make investment. Since the strategies and portfolios are managed by computers, the cost of investment management is lower. 私人銀行通常只為高淨值及超高淨值個人或家庭提供理財服務,這些客戶通常有200萬美元以上 的流動資產可供投資。圖表4按管理資產規模列出了亞洲的主要私人銀行。在這些用戶開立帳戶 的最低資金要求為200萬至1,000萬美元不等。圖表5則列出部分於香港營運的機械人理財顧問, 其開立帳戶的最低資金要求僅為數百至數千美元,遠低於私人銀行。 這些自動化理財顧問公司集合投資者的資金,然後以演算法決定資產配置和投資組合,因此有助 減低資產管理的成本。 Robo-advisory

自動化理財顧問

Digital Experience電子化的用戶體驗

The digital experience is what distinguishes robo-advisors from human advisors. Without meeting human advisors or relationship managers, investors could consult a robot advisor through a mobile app or online platform by entering personal particulars and other information such as investment goals and horizon.

A survey of high-net-worth individuals in Asia by RBC Wealth Management in 2014 found that they prefer digital contact over direct contact for wealth management services. This reveals that even in private banking, digital experience is crucial in retaining customers.

電子化的用戶體驗亦是自動化理財顧問的一大特徵。投資者無需親身接觸投資顧問或客戶經理, 而是透過應用程式或網上平台輸入個人資料及其他相關資訊,如投資年期等,以向自動化理財顧 問諮詢投資意見或管理帳戶。加拿大皇家銀行財富管理部門在2014年進行的一項調查發現,亞 太區(日本以外)有較多的高淨值客戶傾向以電子平台理財,這有別於其他地區的高淨值人士。這 項調查反映出即使在強調客戶關係的私人銀行業中,電子化的服務和體驗亦有助於挽留客戶。 Disputes

爭議

Emerging technologies have always had criticism and robo-advisory is no exception. One common concern of those who are against robo-advisors is the issue of algorithm. Because robo-advisors are automated, the algorithms behind the user interface are not transparent to the users which is a cause for concern. Monitoring and supervision of robots are also underdeveloped. Bankers and investment advisors are registered to sell funds or give recommendations on clients’ portfolio while robots are not. Who should be held accountable in case of fraud is under discussion as well.

新科技的面世都難免引發爭議,自動化理財顧問亦不例外。反對自動化理財的其中一個主要理據 是電腦演算法的透明度。由於自動化理財顧問的操作高度自動化,顧客往往無從了解投資平台背 後的演算法,因此難免有所顧慮。此外,相關法規和監管亦未成熟。銀行和投資顧問需要申領相 關牌照才能提供投資顧問服務,但自動化理財顧問並無類似的監管安排。出現問題時責任誰屬仍 然有待釐清。 Future development

未來發展

The wealth management industry in Hong Kong is a vivid picture? comprised of growing Chinese wealth, mature financial infrastructures and a sound legal system. Yet, technological transformation has to be embraced and properly monitored so as to sustain the growth of this sector.

隨著中國私人財富持續增長、金融基建及司法制度日趨健全,香港的財富管理行業前景一片光 Figure 4.

Source: Asian Private Banker League Table 2017. SCMP Private Bank Listing

Figure 5. Robo-advisory services provider in Hong Kong Source: Companies website and online sources

Figure 6.

Source: CapGemini, RBC Wealth Management and Scorpio Partnership Global HNW

Advisors 顧問

Prof. Raymond Wong (Program Director) 黃智榮教授 Prof. Lancelot JAMES (Program Co-director) 在林壽教授 Prof. Kani CHEN (Program Co-director) 陳卡你教授

Dr. Jiying WANG (Undergraduate Program Coordinator) 王繼英博士

All contents and information are subjected to copyright protection.

Republication, redistribution or unauthorized use of any content is expressly prohibited without the prior written consent.

Risk Management and Business Intelligence Program The Hong Kong University of Science and Technology Phone: 3469 2399 Fax: 3104 0026 Email: [email protected] Website: http://www.rmbi.ust.hk