Department of Business Administration

I-Shou University

MASTER THESIS

Factor Analysisof theCustomer’s Intentionof UsingElectronic

Banking Services: Case Study ofBank for Investment and

Development of Vietnam (BIDV)

Advisor :Ph.D. Jesse Yu-Chen Lan Advisor : Dr. Ngo Trung Hoa Student : Do Thi Thu Hang

Acknowledgement

I could not complete my final thesis without valuable supports of the great people around me. First of all, I would love to express my sincere thanks to my advisor – Mr. Ngo Quang Hoa, Ph.D.Jesse Yu-Chen Lan, who shared with me a lot of experience and guidance. He spent a lot of time on guiding me and was very patient to correct my mistakes. He also gave me a lot of motivation to complete this thesis.

Secondly, I extend my gratefulness to the customers who had spent their time on answering my long questionnaires and shared with me a lot of experience during them using service at BIDV.

Next, I would love to send my warm thank to director of 5 branches and the staffs there who supported me during my points of view and such directors also provided me a lot of information in relationship between affecting factors and intention behavior of customers when using BIDV’s service.

Abstract

This research is aim to study the intention behavior of customer in using the internet banking service ofBank for Investment and Development of Vietnam(BIDV) by using the TAM model. There were 250 questionnaires that were sent to customer who are using the service of BIDV, 210 questionnaires returned in which 176 questionnaires is valid questionnaire, there were 34 Invalid questionnaires due to lack of information have been removed from the system. Valid questionnaires reached 83.8% rate of the sample size. Data collected after the design, coding and data entry via SPSS 22.0 software. The result indicates that there are 02 factors are not significance affected on intention behavior to EB with P- value> 0.05 (Perceived Ease (PE) and cost (COST). The four remaining factors have impacted on intention behavior to EB: Perceived usefulness (beta = .375), risk awareness (beta = .261), subjectivenorms (beta = .259) and perceived behavioral control (beta = .221). From the result of t-test and ANOVA test, it can be concluded that H7 is not supported with the statement that “There are different intention behavior in using electronic banking service among customer demographic”. The result also indicates that the intention behavior of customer in using electronic banking service is not so high with mean value is just above 3 score. The conclusion, recommendation, limitation and future research suggestion also discussed in this study.

Keywords: Behavioral theory, Technology acceptance model (TAM), Electronic Banking Services, Vietnam Banking industry, BIDV.

Table of contents

Acknowledgement ... ii

Abstract ... iii

Table of contents ... iv

List of Tables ... vi

List of Figure ... vii

Chapter I Introduction ... 1

1.1 Backgroud ... 1

1.2 Objectives of research ... 3

1.3 Research question ... 3

1.4 Research contribution ... 3

Chapter II Literature review ... 5

2.1 Electronic banking definition ... 5

2.2 The development of electronic banking in Vietnam ... 5

2.3 Behavioral theory ... 6

2.4 The theory of technology acceptance model ... 8

2.4 The research model for factor impact on Customers behavior intention in electronic banking service at BIDV ... 9

2.4.1 Perceived usefulness ... 9

2.4.2 Perceived Ease to use ... 10

2.4.3 Risk awareness ... 10

2.4.4 Cost ... 11

2.4.5 Subjective norms and perceived behavioral control ... 11

Chapter III: Methodology ... 13

3.1 Research Procedures ... 13

3.1.1 Preliminary studies ... 13

3.1.2 Official studies ... 13

3.2 Method of collecting materials ... 13

3.2.1 Secondary data collection ... 13

3.2.2 Primary data collection ... 14

3.4 Questionnaire construction ... 14

3.5 Method of analysis. ... 16

Chapter IV Data analysis ... 17

4.1 Respondent profile ... 17 4.2 Reliability Analysis ... 18 4.3 Factor analysis ... 19 4.4 Variables correlation ... 22 4.5 Regression ... 22 4.6 ANOVA/T-test result ... 25

Chapter V Conclusion and recommendation ... 27

5.1 Conclusion ... 27 5.2 Recommendation ... 27 5.3 Research implication ... 30 5.4 Limitation of research ... 31 Reference ... 32 Appendix ... 32

List of Tables

Table 3.1 The variable and item of questionnaire... 15

Table 4.1: Respondent profile ... 17

Table 4.2 Cronbach's Alpha result ... 19

Table 4.3. KMO and Bartlett's Test for the independent variables ... 19

Table 4.4. Factor analysis results of the independent variables ... 20

Table 4.5 Rotated factor matrix of the independent variables ... 21

Table 4.6 Variable correlation ... 22

Table 4.7. Model summary variable regression ... 23

Table 4.8. ANOVA result of Multiple variable regression model ... 23

Table 4.9 Multiple variable result ... 24

Table 4.10 Differences between gender and intention behavior ... 25

Table 4.11 The differences of intention behavior among age group ... 25

Table 4.12 The difference of customer satisfaction among Education level ... 26

List of Figures

Chapter I Introduction

1.1 Backgroud

The development of technology, “especially information technology industry, has affected all aspects of people life: economic and social, cognitive and alter production methods of many business sectors, many different economic sectors, including the banking sector. The concept of e-banking, online trading, online payment, ... began to become the trend of development and competitiveness of the commercial banks in Vietnam from 2000s” as mentioned by Turban and King (2003). services development based on information technology - electric from in banking industry is the inevitable trend, objectively in “era of international economic integration”. The benefits of electronic banking are great for customers, banks and the economy, its inculde: convenience, quickness and accuracy of transactions.

As commneded by Turban and King (2003) “Electronic commerce has left significant impacts on our market and industry structure along its way of developing. Not only does it alter products and services, it also brings numerous changes to consumer behavior and the labor market”.Bhatia and Sethi (2007)shows that “banks and other financial institutions have applied Internet-based services along with their traditional approaches. Most services and business of financial institutions globally are now accessible online , marking the beginning of an electronic banking era”.

The popularity of the Internet and mobile phones are “opening up a potential market for the provision of electronic banking services in Vietnam”. According to data from the General Statistics Office (GSO) of Vietnam and the Vietnam Internet Network Information Center – (VNNIC, 2012), “In 2012, there are more than 31 million Internet users (up 3.2% compared to the same period in 2011), Internet subscribers nationwide is estimated at 4.4 million subscribers (13.9% compared to the same period of 2011), and the number of mobile subscribers reached 120.9 million subscribers (up 5.2 % compared to the same period in 2011)”. This is a great potential for the development of e-banking services. In addition, the Government and the State Bank of Vietnam has promulgated the Law, Circular, Decree, Decision to create a legal framework to encourage the development of electronic banking services. Notably, the adoption of the Law Day 2005 electronic transactions 29/11/2005, National Assembly of the Socialist Republic of Vietnam has approved the Law on electronic transactions No.51 / 2005 / QH11 and officially introduced on April 03/01/2006. Electronic

Transactions Act was introduced, which created the basic legal framework for electronic transactions.

Under E-Commerce Report Vietnam in 2011, showed that by the end of 12/2011, “there are 50 banks operating in Vietnam market (excluding foreign bank branches in Vietnam) has 45 banks have implemented online trading systems at different levels. The electronic banking services commonly provided by banks widely, which may include Internet Banking services are provided by 45 banks (90%), Mobile Banking provides 38 banks ( accounting for 82%)”. Banks' resources are limited. Regarding human resources, banks in general still lacks of quality of manpower-intensive with high-level information technology and e-commerce. Regarding infrastructure elements, although this factor was development investment but remaining restrictions also inhibit the growth of e-banking services. ATM network and the connection of the POS card payment through the banking system is incomplete and inconsistent. Some issues related to technical safety has yet to make customers happy, phenomena such as electrical leakage ATMs, issue information stolen while using an ATM. The telecommunications network in Vietnam increasingly appeared many vendors, but the quality is not guaranteed use. Wave or loss due to overloading network congestion occurs frequently affect the quality of services.

The benefits of e-banking services have not yet been fully exploited, such as customers use ATM services mainly serve the purpose of withdrawing cash. In addition, the utility of e-banking services have yet to fully satisfy the needs of customers, such sending cash to account, sign up to use the service also have to direct transactions in the trading room.

Therefore, in order to survive and develop, BIDV is striving the utmost to catch up modernization process in banking sector , not only imprrove the perfection of the traditional business, but also set on the development of modern banking applications focusing electronic banking services, meet the requirements of enhanced competitiveness, integration and development. However, practical development of electronic banking services of BIDV also showed that there are difficulties and limitations. Study the intention behavior in using electric banking is nessesary to help BIDV Bank affirm the customer behaviour with BIDV electric banking service and give the solotion to improve the electric banking service and affirmed its position and brand. Althought there are some study about electric banking service such as Turban and King (2003)Bhatia and Sethi (2007), and Martin Hilb (2006). Beside with the academic side, there are still limited research on this electronic banking and consumer

behavior intention in using the electronic banking service. From the situation that lack of knowledge, practice study in this area, this study is going to conduct the research related to consumer behavior and electric banking service at BIDV.

1.2 Objectives of research

From the limited study of electric banking service, this study is aimed to:

- Identification the factors that affect electronic banking service behavior intention of customers

- developed a model of the relationship between the factors electronic banking service and behavior intention of customers

- Introduce solution to raise awareness in the usingof electronic banking service

1.3 Research question

To obtain the research objective, this study is going to answer flowing questions

- Does Perceived usefulness expectancy have an impact on behavior intention of customers in using electronic banking service?

- Does Perceived Ease to use have an impact on behavior intention of customers in using electronic banking service?

- Does Risk awareness have an impact on behavior intention of customers in using electronic banking service?

- Does Cost have an impact on behavior intention of customers in using electronic banking service?

- Does subjective norm have an impact on behavior intention of customers in using electronic banking service?

- Received behavioral control have an impact on behavior intention of customers in using electronic banking service?

- Is there any different intention behavior in using electronic banking service among customer demographic?

Academic contribution: Adding knowledge to people about services and electronic banking in generally and customer behavior intention in particular.

Management implication: Help the banking managers in implementing a campaign to introduce the characteristics of the electronic banking system, its benefits and how to use it. Raising awareness about the benefits of using the system, diversifying the types of services, improve services, provide value-added services such as paying utility bills, implementing marketing one on one.

Chapter II Literature review

2.1 Electronic banking definition

According to Clause 6 and Clause 10 of Article 4 Electronic Transaction Law by the National Assembly of Vietnam on 29/11/2005, electronic transactions are transactions done by electronic means. In particular, electronic media as a means of activity-based computing technology, electronics, digital, magnetic, wireless transmission, optical, electromagnetic, or similar technology.

Pursuant to the above provisions, purchases at the counter and pay by credit card, or swipe to the vending machine to automatically print the card statement and bill of sale shall be considered as electronic transactions credit card is the electronic media.

Realizing the concept of electronic transactions not confined within the Internet and other information networks, but also extended to all transactions are done by electronic means. Therefore, electronic transactions in banking transactions by means of electronic banking services, in other words, banking services traded by electronic means (called "electronics banking services ").

2.2 The development of electronic banking in Vietnam

Along with the new era of electonics and internet, ebanking in Vietnam has been a new potential market for banking industry. However, this kind of service is still new service with both side customer and sppliers.As EB banking services on the market only a few banks offer banking services in the "home-banking" (Vietcombank, Incombank, ACB, Eximbank) and 2 banks ANZ foreign goods and Citibank are offering. Phone-banking services, the bank has provided the VCB, ACB, Techcombank, HSBC, ANZ and Citibank ... Mobile-banking service, the bank has Incombank, ACB and Techcombank ..., in addition, other banks have only just stop at the site set to introduce major banks and providing information services. Private Bank for Agriculture and PTNTVN ongoing trials E-banking project.

In addition, to cater for e-commerce payment system, VDC has built VASC Payment payment gateway to provide a basis for the payment system through the Internet and the management system certificate number - VASC CA (Certificate Authority), to provide electronic signatures and digital certificates to the legal basis for electronic transactions,

creating confidence for customers and service providers, is the backbone for the development of e-commerce mail in the near future.

2.3 Behavioral theory

Predicting human behavior is the fundamental objective of the theories in the field of social psychology study (Chang, 1998). Many theories have been formed to serve this goal, including the theory of rational action. Rational theory of action (Fishbein & Ajzen, 1975; Ajzen & Fishbein, 1980) along with its expansion theory as the theoretical behavior plans are theoretically be used in many previous studies and appreciated the usefulness in predicting the different behavior of humans (Madden et al, 1992). These theories are applicable in many research areas such as understanding the behavior ethical or unethical (eg. behavioral studies gambling, gaming), the study of human behavior people at work (for example, job satisfaction), behavior of customers in marketing (for example, the reaction of customers with coupons, online shopping behavior) and learn behaviors related to information technology (eg. ecommerce acceptable behavior)

Reasoned action of Fishbein & Ajzen reasonable (1975) was introduced to help respond to issues related to human behavior in general. This theory explains and predicts intention behavioral to perform as well as predictions of human behavior in situations and different fields, especially in psychology - sociological and marketing. This theory helps a lot of research to find out why people there are certain behavior and what should be done to change these behaviors. Rational action theory to consider the relationship between 'faith', 'attitude', 'intend' and 'behavior'. In this theory, 'intend' as factors that affect the 'behavior'. 'Intent' is affected by these factors as 'attitude' and 'subjective standard'; 'Confidence' to affect 'attitude'. Thus, using the theory of rational action will help researchers determine the impact of these factors, leading to the implementation of a certain behavior, and predicting what a person will do or not do. Understanding this will help to develop the ways and measures to change behavior if necessary. These measures are designed not only to change the behavior, but also to influence change beliefs, and thus will change behavior.

Rational action theory (Theory of reasoned action - TRA) said that before deciding to perform a certain behavior people will consider and review the results or consequences can occur if the conduct of the latitude. Then, people will choose to perform any acts likely bring the desired results. Rational action theory is modeled in Figure 1. In this model, intending to make a person's behavior will lead to the implementation of such acts. In other words, the

behavior is explained simply: the intention to commit acts of higher ability to perform such acts as adults.

'Attitude' and 'subjective standard' is defined as follows:

• Attitudes toward the behavior is defined as 'general comments about a person's approval or disapproval of certain acts' (Ajzen & Fishbein, 1980).

• Standard subjectivity is defined as 'a person's perception of the most important ones for this individual thinks that he / she should or should not perform certain acts' (Ajzen & Fishbein, 1980). Standard subjective factor, as a factor affecting the behavior, measuring the social impact of the behavior of an individual (eg. the expectations of the members of individual families which for implementing acts).

If someone said that a particular behavior will yield positive results, and if you feel that the people who matter to them (those who have personal impact on them as parents, friends, etc.) will encourage and support the implementation of this act, the intention to carry out their acts will be formed.

According to the theory of rational action, 'attitude' is affected by two factors: one's beliefs about the effects and results/consequences brought if implemented and evaluated the behavior of that person on the impact and results/consequences. The belief is based on the understanding or based on what the individual thinks is right.

According to the theory of rational action, there are two factors affecting the 'subjective standard', including normative beliefs: refers to an individual's beliefs about people important / influential to personal underlines that he / she should or should not do such acts and the reason or motivation to comply, listen to this influential people.

Theory of planned behavior (TPB) is theoretically extend from TRA (Ajzen & Fisbein, 1980;Fishbein & Ajzen, 1975). As stated above, the TRA said that acts can be done (or not done) entirely under the control of reason. This limits the application of theoretical research TRA for certain behaviors (Buchan, 2005). To overcome this, was born TPB (Ajzen, 1985; 1991). The birth of the theory of planned behavior TPB (Theory of Planned Behavior) comes from the limits of human behavior that has little control. A third factor is that Ajzen to affect the intent of human factors awareness behavioral control (Perceived Behavioral Control). Cognitive behavioral control reflects the ease or difficulty in implementing acts and implementing acts which may be controlled or limited or not (Ajzen, 1991, p. 183).

TPB shows that the intention is influenced by three factors: the attitude toward the behavior, perceptions of social pressure or social impact with individual behavior, and perception of behavioral control (PBC- Perceived Behavioral Control). The difference between the two models is in the TPB and TRA TPB model adds the influence of factors PBC intends to act, in addition to the two factors is' attitudes toward behavior 'and' social influence 'or' subjective standards'. Also, in the TPB model also shows the impact of the factors 'confidence & convenience' to 'awareness of behavioral control'.

Both TRA and TPB model is used to predict fairly common behavior in many different research situations. There have been many studies apply TPB model (in business areas, the study of ethical behavior) and the results of the study confirmed the significant impact of the above 3 factors in predicting behavioral intentions.

2.4 The theory of technology acceptance model

Technology acceptance model (TAM) by Davis first proposed in 1986. The model theory origin TRA (Fishbein & Ajzen, 1975; Ajzen & Fishbein, 1980) and theoretical TPB (Ajzen, 1991). TAM launched to explain the behavior acceptable use of information technology system.

TAM model has created the foundation for a lot of theoretical research on information systems. TAM models that 'perception of usefulness' (PU) and 'perception of ease of use' perception of ease of use are the variables affecting technology acceptance (Keat& Mohan, 2004). PU refers to the user's perception of the degree to which the system will improve the results of their work; perception of ease of use referring to comments of users on the level of effort required to use the system.

Currently, in order to reduce power usage load of customers, many found themselves, electrical equipment using modern technologies (use of high-tech electrical equipment such as solar energy, appliances Household uses inverter technology, environmental protection technology, to avoid power loss). One useful tool in explaining the intention to adopt a new product is accepted technological model TAM. According to Teo, et al (2008, p. 266), TAM model has successfully predicted 40% of the use of a new system. The usefulness perceived as "the degree to someone who believes that using specific systems to enhance the implementation of their own work." The easy to use comments as "the degree to which a person believes that using specific systems without the effort"

use Acquirer services. However, TPB studied that have a better ability to forecast the TAM but more complex models for introducing many factors can affect the use (Hsu and Chiu, 2004) and Predictability not much better (proven in previous studies conducted by Chau and Hu, 2001; Taylor and Todd, 1995).

TAM is considered more detailed and easy to apply in practice, than TPB (Mathieson, 1991). According Lin and Luarn (2004). TPB is the general theory of human behavior while TAM is used to predict the use of technology / information systems. Thus, TAM characterize information systems. McKechnie, Winklhofer and Ennew (2006) suggested that TAM is very useful when used to evaluate the factors affecting the level of Internet use in the financial services.

Additionally, TAM is the research model is the most widely accepted in the field of technology and benefit both elements feel and ease of use. The comments are empirically verifiable and conclusions are appropriate. But the DOI, most studies show that only some of the relevant factors relevant to acceptable behavior (Agarwal and Prasad, 1998; Taylor and Todd, 1995). Thus, based on the above reasons, TAM proved to be the most appropriate model to study the factors that affect the intended use of the service Acquirer.

2.4 The research model for factor impact on Customers

behavior intention in electronic banking service at BIDV

2.4.1 Perceived usefulness

Perceived as useful or convenience is an extent of people believe that using such a system, a specific product will enhance the implementation of their own work (Davis, 1989). Some studies have shown that one of the factors affecting the decision to use the convenience Acquirer (Gerrard and Cunningham, 2003; Lichtenstein and Williamson, 2006; Sohail, & Shanmugham, 2003 ). In it, Lichtenstein and Williamson (2006) concluded at the Australian bank, convenience factors, specifically through time can access the 24/7 has decided to use the influence Acquirer. Besides, Sohail and Shanmugham (2003) report that saves time in implementing the acquirer transactions through the most important aspects of convenience, thus affecting the decision to use the service Acquirer. Lee et al (2005) showed that customers feel comfortable is the most important element of intent to use the Internet banking service. Similarly,Podder (2005)survey found that the convenience to have a positive impact on the decision to use the acquirer. Besides, Sari, and Rofaida (2015)found that the convenience significantly influence the actual behavior of the customers to decide to use

acquirer.

Therefore, the following hypotheses are proposed:

H1: There is a positive relationship between Perceived usefulness and customer intention behavior to EB

2.4.2 Perceived Ease to use

Ease to use is the "degree to which a person believes that the system can be used without special effort." (Davis, 1989). Ease to use factor, or also known as the Friendly Website for users is one of the main factors to be considered in the technology acceptance model (TAM). In the study by Shih et al in 2004, when the TAM model used to determine the factors that influence the decision to use online shopping services have shown that the ability to easily use the site identified consumer attitudes toward online shopping from decisions affecting the use of online shopping services. Lichtenstein and Williamson (2006) argues that the user-friendly ease of use or the ability of customers through the website will be judged by the complexity and design of the site. The complexity of a bank's website to prevent customers using the service Acquirer. In the study by Lee et al (2009) point out that the speed of the Internet and the difficulty in implementing online transactions that affect the ability of customers to use online banking services. A friendly site with customers, there are many features, rapid implementation time, content information and interaction to meet with customers to create favorable conditions for the use of services Acquirer.

In the study by Sohail & Shanmugham (2003) showed that easily perform online transactions is one of the main variables affecting the decision to use the service Acquirer. Besides, Liao and Cheung (2002) have made the investigation and the results show a website user friendly is the most important factor for deciding to use online banking services.

In addition, research by Jaruwachirathankul and Fink (2005) has concluded a well-designed website and user friendliness will easily attract potential customers.

Therefore, the following hypotheses are proposed:

H2: There is a positive relationship between Perceived Ease to use and customer intention behavior to EB

2.4.3 Risk awareness

learn intend to use the service users as well as the decision to accept use of the customer service (Im, Kim and Han , 2008; Kim, Ferrin and Rao, 2008; Lopez-Nicolas and Molina-Castillo, 2008).

In the study of Featherman and Pavlou (2003), risks related to the uncertainty of the service, can not predict and control the process using the service. Besides, Cooper (1997) defined risk as an important feature of the consumer in the application of innovation, here is the use of a new service like EB. O'Connell and Tremethick, (1996) discovered that the level of security risk is one of the important reasons explain the slow development of the EB in Australia. In addition, a number of other experimental studies showed that risk perception is defined as having a positive impact directly and significantly to the intention of the consumer to use the EB service (Nguyen, 2012) Therefore, the following hypotheses are proposed:

H3: There is a positive relationship between risk awareness and customer intention behavior to EB

2.4.4 Cost

Cost is understood that the cost of customer has to pay when using EB service, the cost of money and the cost of time. Liao and Cheung (2002) conducted a study on consumer attitudes toward online banking services and pointed out that prices influence the attitude of customers with online banking services. When the last transaction acquirer if service charges low or no fees collected any sort that might push consumers to use Internet banking. On the other hand, the study of Sathye et al (1999) argued that the cost of the service unreasonably Acquirer has a negative impact on the decision to accept service users Acquirer. At the same time, the report Wallis (1997) has pointed out, to consumers using the new technology, the technology must have a reasonable price compared to older technologies they replace. Besides, accordingKarjaluoto, Mattlia and Pento (1999), factor the price of fish is considered an important criterion for the acceptance of using online banking services.

Therefore, the following hypotheses are proposed:

H4: There is a positive relationship between low cost and customer intention behavior to EB

2.4.5 Subjective norms and perceived behavioral control

According to Theory of intended behavior (Ajzen, 1985, 1991), the factors that promote the actual behavior is intention perform such acts. Intent to be determined by three factors: attitude, subjective norms and perceived behavioral control. That factors reflect the

appreciation of the positive or negative individuals of a certain behavior.

Empirically, there is many evidences that the subjective norms and perceived behavioral control have an impact on consumer behavior intention in using the electric (Hori et al 2013; Sardianou, 2007; Scasny & Urban, 2009; Urban & Scasny, 2012; Wang et al, 2011).

Therefore, the following hypotheses are proposed:

H5: There is a positive relationship between subjective norms and customer intention behavior to EB

H6: There is a positive relationship between perceived behavioral control and customer intention behavior to EB

H7: There are different intention behavior in using electronic banking service among customer demographic.

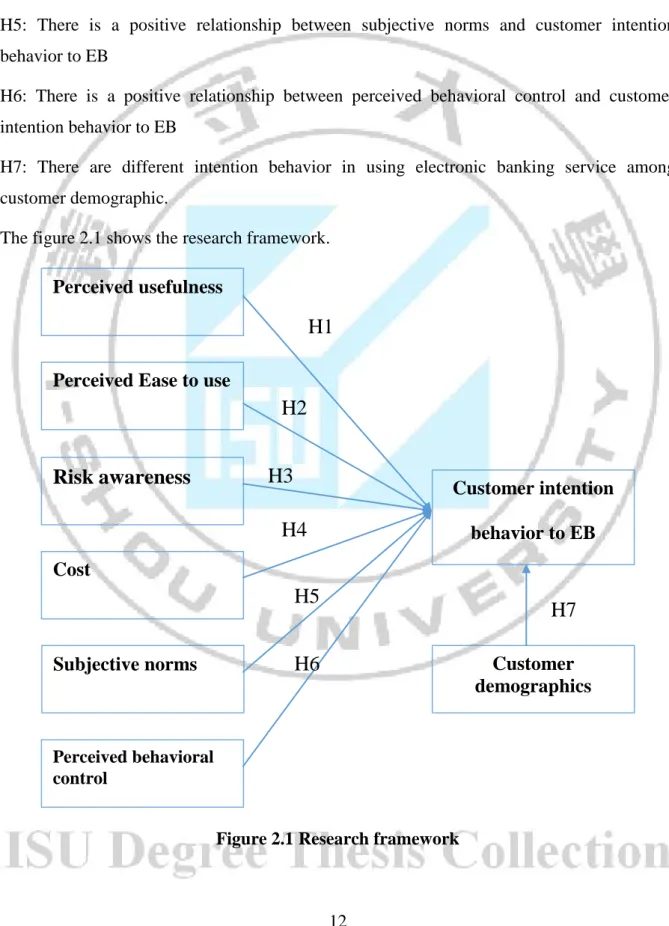

The figure 2.1 shows the research framework.

Figure 2.1 Research framework

Perceived usefulness

Perceived Ease to use

Risk awareness

Cost Subjective norms Perceived behavioral control Customer intention behavior to EB Customer demographicsH1

H2

H3

H4

H5

H6

H7

Chapter III: Methodology

3.1 Research Procedures

The study was implemented from the date of 02/01/2016 include following steps:

3.1.1 Preliminary studies

- Through qualitative methods it is aimed at discovering, adjust and supplement the general observation variables to measure the concepts studied.

- Qualitative research conducted at BIDV through investigation 30 individual customer transactions at bank branches to gather opinions on the review of the customer intends to use BIDV Online services, based on the perceived of easy to sue aspect, the usefulness of services, risk awareness.... from that questionnaire design based on the opinions collected, officially launched the research variables.

3.1.2 Official studies

- Using quantitative research methods. Quantitative research was conducted through direct interviews of individual customers with accounts at the bank. Official results of research used to test the theoretical model.

The steps are:

- Design questionnaires, investigators try and make adjustments so that the questionnaire is clear as to obtain results that can achieve the research objectives.

- Official Interview: using direct interviews, the interviewer should explain the contents of the questionnaire for respondents to understand and answer questions correctly according to their assessments.

3.2 Method of collecting materials

3.2.1 Secondary data collection

Secondary data collected by BIDV providing content such as organizational structure department departments, business results of the bank in the period 2015 to help basic assessment of the situation of the bank.

Also subject also uses a number of documents as well as information about the bank from a number of newspapers, magazines, the Internet about development history of banking practices for e-banking services as well as the limitations of the service exist in Vietnam and the Asian banks.

3.2.2 Primary data collection

Primary data collection by conducting surveys with 200 individual customers with accounts at BIDV.

3.3 Method of sampling

According to Ngoc and Trong (2008), for cases of non-random sampling, if the sampling is taking place according to certain principles and fair, the sample can be considered as random method. This may be acceptable in terms of research. Subjects of investigation are customers of BIDV account. Because of the difficulty to get a full listing of the bank's customers to access customers directly for investigation by the questionnaire was made based on the customer accessible and according to certain principles ensure randomness.

According to the experience of many previous studies, to perform discovery factor analysis EFA effectively, the number of samples need to select a minimum of 5 times the total number of variables. Based on the total variation of the official questionnaire will select the sample size is greater than 5 times the number of variables to implement direct customer surveys. Specifically, questionnaire has about 27 items so the minimum required number of samples is 140 samples. The more the number of samples collected, the information is useful as it emits 200 select the questionnaire based on the conditions of time and the ability to reach my customers during practice at department customer service bank branches.

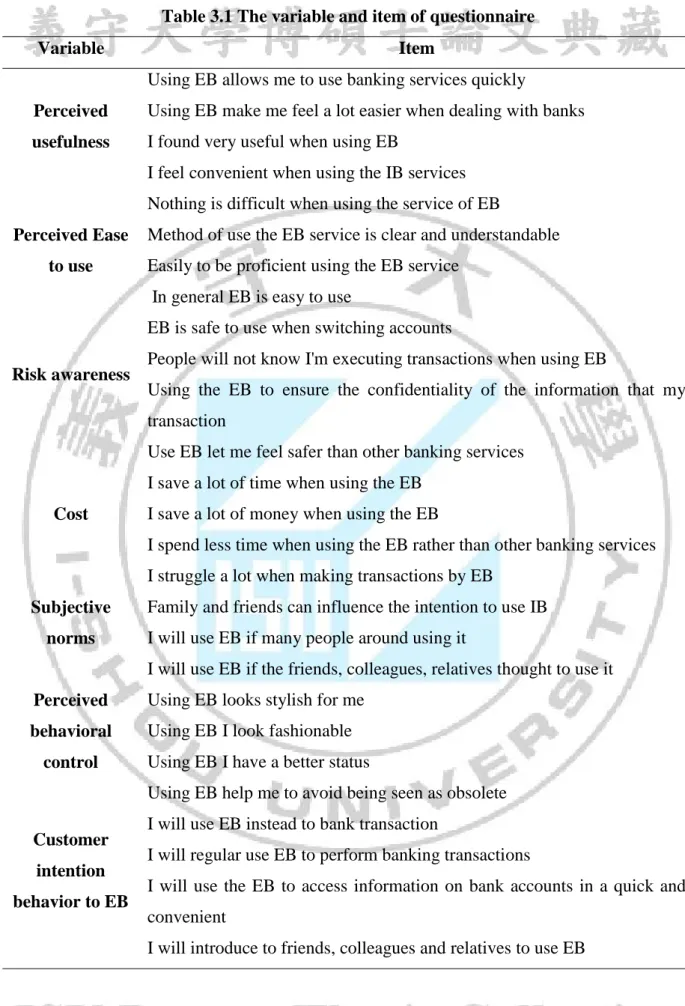

3.4 Questionnaire construction

The questionnaires are based on the study of TAM model in the field of banking in several countries around the world such studies. Especially studies in Thailand, Korea, Malaysia, because there have conditions similar to Vietnam on geographically and culturally. Also, after reviewing several studies in Vietnam, researchers have come up with the factors that influence the intention to use the services used based on the scale of David et al, (1989).

Table 3.1 The variable and item of questionnaire

Variable Item

Perceived usefulness

Using EB allows me to use banking services quickly

Using EB make me feel a lot easier when dealing with banks I found very useful when using EB

I feel convenient when using the IB services

Perceived Ease to use

Nothing is difficult when using the service of EB

Method of use the EB service is clear and understandable Easily to be proficient using the EB service

In general EB is easy to use

Risk awareness

EB is safe to use when switching accounts

People will not know I'm executing transactions when using EB

Using the EB to ensure the confidentiality of the information that my transaction

Use EB let me feel safer than other banking services

Cost

I save a lot of time when using the EB I save a lot of money when using the EB

I spend less time when using the EB rather than other banking services I struggle a lot when making transactions by EB

Subjective norms

Family and friends can influence the intention to use IB I will use EB if many people around using it

I will use EB if the friends, colleagues, relatives thought to use it

Perceived behavioral

control

Using EB looks stylish for me Using EB I look fashionable Using EB I have a better status

Using EB help me to avoid being seen as obsolete

Customer intention behavior to EB

I will use EB instead to bank transaction

I will regular use EB to perform banking transactions

I will use the EB to access information on bank accounts in a quick and convenient

3.5 Method of analysis.

The study is using the following research methods:

- Methods of descriptive statistics to determine the characteristics of the study sample, the factors of age, income, gender, occupation, sources of customer information access services, the reasons do not intend to use the service.

- Analysis of the factors explored EFA to consider factors affecting the intention of using BIDV Online service of individual customers.

- Regression correlation factors affecting the intention of using BIDV individual customer to conclude the main factors have a direct impact on customers and the impact of each factor. - ANOVA and t-test is used to analysis thedifferent level of agreement of customer demographic related to behavior of intention in using EB factors.

Chapter IV Data analysis

4.1 Respondent profile

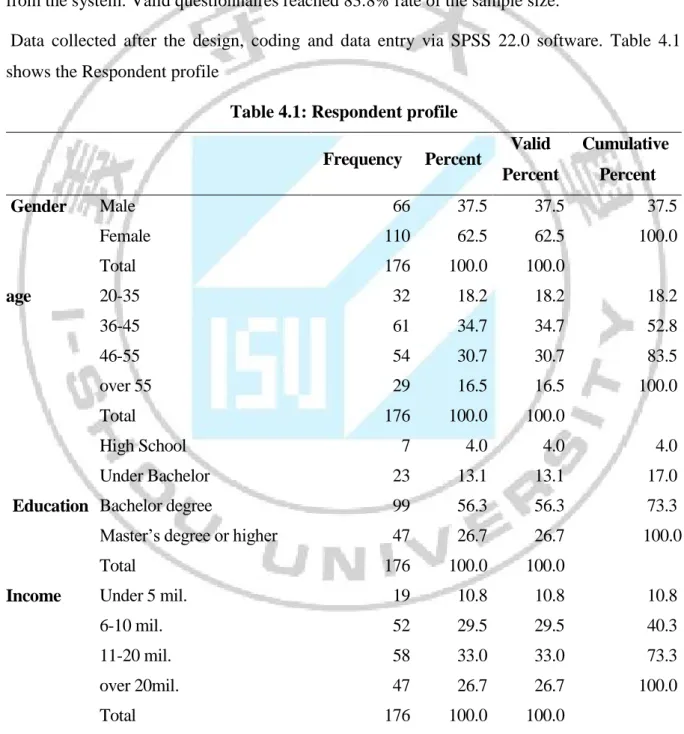

There were 250 questionnaires that were sent to customer who are using the service of BIDV,210 questionnaires returned in which 176 questionnaires is valid questionnaire (83.8); there were 34 Invalid questionnaires (16.2%) due to lack of information have been removed from the system. Valid questionnaires reached 83.8% rate of the sample size.

Data collected after the design, coding and data entry via SPSS 22.0 software. Table 4.1 shows the Respondent profile

Table 4.1: Respondent profile

Frequency Percent Valid Percent Cumulative Percent Gender Male 66 37.5 37.5 37.5 Female 110 62.5 62.5 100.0 Total 176 100.0 100.0 age 20-35 32 18.2 18.2 18.2 36-45 61 34.7 34.7 52.8 46-55 54 30.7 30.7 83.5 over 55 29 16.5 16.5 100.0 Total 176 100.0 100.0 Education High School 7 4.0 4.0 4.0 Under Bachelor 23 13.1 13.1 17.0 Bachelor degree 99 56.3 56.3 73.3

Master’s degree or higher 47 26.7 26.7 100.0

Total 176 100.0 100.0

Income Under 5 mil. 19 10.8 10.8 10.8

6-10 mil. 52 29.5 29.5 40.3

11-20 mil. 58 33.0 33.0 73.3

over 20mil. 47 26.7 26.7 100.0

Total 176 100.0 100.0

From the table 4.1 the result shows that, there are 37.7% customer in this study is male and female is 62.5%. Related to age of customer, the result shows that customers, customer with

the age from 20-35-year-old is 18%, from 36-45-year-old is 34.7%, from 46 – 55-year-old is 30.7% and customer who is over 55-year-old reach 16.5% in this study.

Related to education level of customer, this study shows that customer who has High School level is 4.0%, Under Bachelor is 13.1%, customer who have Bachelor degree is 56.3% and the customer who has the Master’s degree or higher reach 26.7%. From the table 4.1 shows that customer who has income per month under VND 5 million is 10.8%, from VND 6-10 mil. is 29.5, from VND 11-20 mil. is 33.0 and customer who have the income per month is over VND 20mil. reach 26.7 % in this study.

4.2 Reliability Analysis

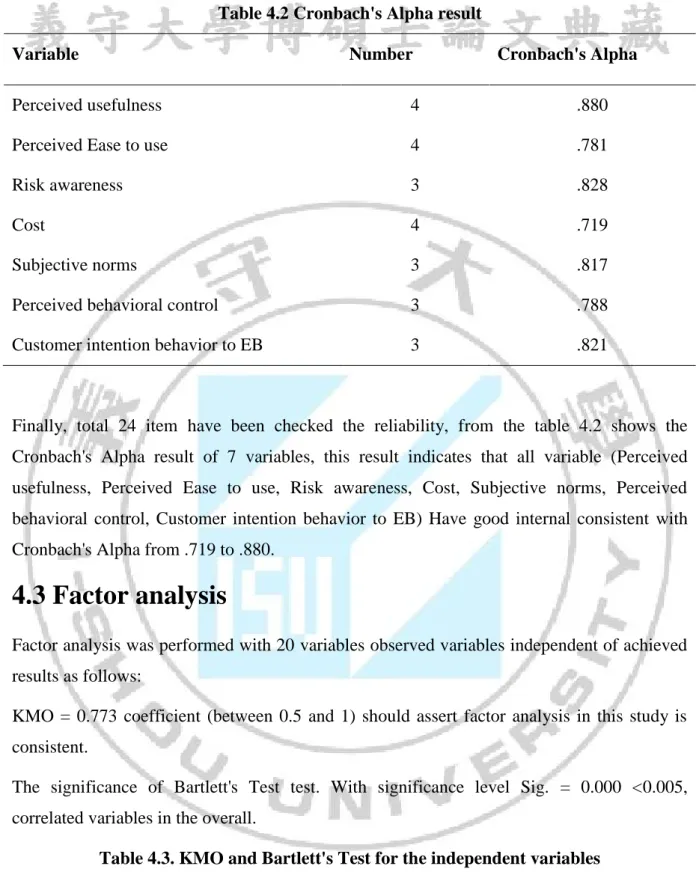

According to Nunnally and Bernstein (1994), the scale research should be a preliminary assessment by Cronbach's alpha coefficient. Cronbach's alpha coefficient of variation value in the range [0-1]. Cronbach's alpha coefficient as high as possible, however if Cronbach's alpha coefficient is too large (> 0.95) showed more variation in scale no different from each other. Scale reliability Cronbach's Alpha well as variability in the range of 0.70 to 0.80. If Cronbach's Alpha is > = 0.60 is acceptable scale in terms of reliability. The variables used Cronbach's alpha measure correlation coefficient of total variable> = 0.30 is satisfactory, if a variable has a correlation coefficient of total variation <0.30, the variable measuring unsatisfactory.

In the analysis result shows that 3 item is not meet the require of reliability with the Cronbach's Alpha is > = 0.60 and have to remove from the analysis system include (RA1: EB let me safer than other banking service, PBC4: using EB help me to avoid being seen as obsolete and IB3: I will use the EB to access information on bank account in a quick and convenience.)

Table 4.2 Cronbach's Alpha result

Variable Number Cronbach's Alpha

Perceived usefulness 4 .880

Perceived Ease to use 4 .781

Risk awareness 3 .828

Cost 4 .719

Subjective norms 3 .817

Perceived behavioral control 3 .788

Customer intention behavior to EB 3 .821

Finally, total 24 item have been checked the reliability, from the table 4.2 shows the Cronbach's Alpha result of 7 variables, this result indicates that all variable (Perceived usefulness, Perceived Ease to use, Risk awareness, Cost, Subjective norms, Perceived behavioral control, Customer intention behavior to EB) Have good internal consistent with Cronbach's Alpha from .719 to .880.

4.3 Factor analysis

Factor analysis was performed with 20 variables observed variables independent of achieved results as follows:

KMO = 0.773 coefficient (between 0.5 and 1) should assert factor analysis in this study is consistent.

The significance of Bartlett's Test test. With significance level Sig. = 0.000 <0.005, correlated variables in the overall.

Table 4.3. KMO and Bartlett's Test for the independent variables

Kaiser-Meyer-Olkin Measure of Sampling Adequacy. .773 Bartlett's Test of

Sphericity

Approx. Chi-Square 1517.050

df 210

Sig. .000

following factors when Cronbach's Alpha test is included in the analysis EFA.

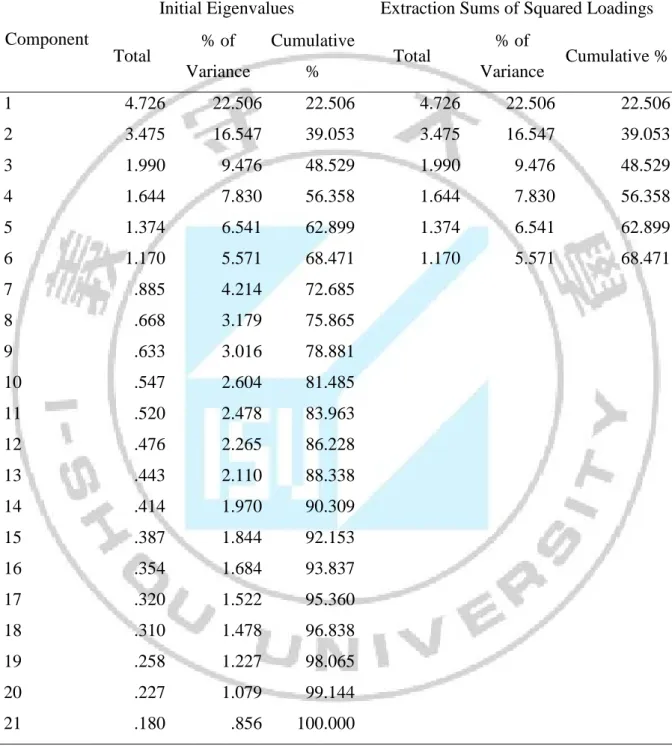

Total 68.471% variance extracted by> 50% said 06 factors extracted explain 68.471% variation of the data set.

Table 4.4. Factor analysis results of the independent variables

Component

Initial Eigenvalues Extraction Sums of Squared Loadings Total % of Variance Cumulative % Total % of Variance Cumulative % 1 4.726 22.506 22.506 4.726 22.506 22.506 2 3.475 16.547 39.053 3.475 16.547 39.053 3 1.990 9.476 48.529 1.990 9.476 48.529 4 1.644 7.830 56.358 1.644 7.830 56.358 5 1.374 6.541 62.899 1.374 6.541 62.899 6 1.170 5.571 68.471 1.170 5.571 68.471 7 .885 4.214 72.685 8 .668 3.179 75.865 9 .633 3.016 78.881 10 .547 2.604 81.485 11 .520 2.478 83.963 12 .476 2.265 86.228 13 .443 2.110 88.338 14 .414 1.970 90.309 15 .387 1.844 92.153 16 .354 1.684 93.837 17 .320 1.522 95.360 18 .310 1.478 96.838 19 .258 1.227 98.065 20 .227 1.079 99.144 21 .180 .856 100.000

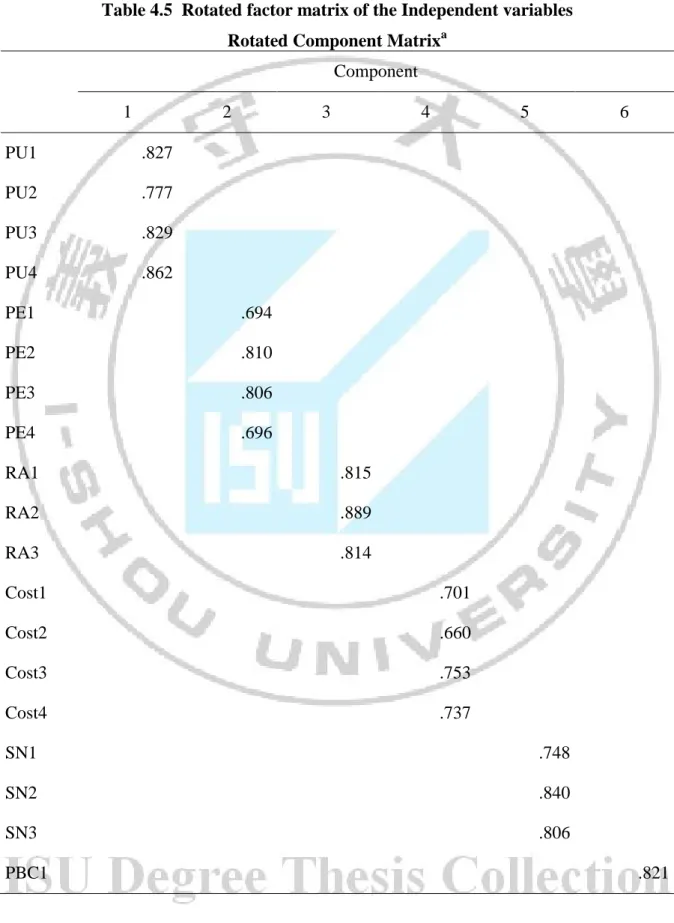

Rotated Component Matrixa removed the variable with loading factor coefficient less than 0.5. The remaining factors are factors loaded > 0.5: ensure the practical implications of EFA. Looking at the table 4.5 we see the influence of 06 factors were extracted from the observed

variables of the scale components.

Thus, after analyzing the factors explored EFA, with all 06 factors were extracted based on 21 variables observed similarities with the elements after testing was included in the analysis EFA. 6 factors will be included in the regression.

Table 4.5 Rotated factor matrix of the Independent variables Rotated Component Matrixa

Component 1 2 3 4 5 6 PU1 .827 PU2 .777 PU3 .829 PU4 .862 PE1 .694 PE2 .810 PE3 .806 PE4 .696 RA1 .815 RA2 .889 RA3 .814 Cost1 .701 Cost2 .660 Cost3 .753 Cost4 .737 SN1 .748 SN2 .840 SN3 .806 PBC1 .821

Component

1 2 3 4 5 6

PBC2 .839

PBC3 .796

Extraction Method: Principal Component Analysis. Rotation Method: Varimax with Kaiser Normalization. a. Rotation converged in 6 iterations.

4.4 Variables correlation

Pearson correlation analysis to determine the linear relationship between the dependent variable and the independent variables before conducting regression analysis. Correlation analysis was performed between the dependent variable is Customer intention behavior to EB and the independent variables are: Perceived usefulness, Perceived Ease to use, Risk awareness, Cost, Subjective norms and Perceived behavioral control Correlation analysis results presented in Table 4.6 .

Table 4.6 Variable correlation

PU PE RA COST SN PBC IB

PU Pearson Correlation 1

PE Pearson Correlation .055 1

RA Pearson Correlation .295** -.010 1

COST Pearson Correlation -.019 .468** -.037 1

SN Pearson Correlation .456** .057 .356** -.068 1 PBC Pearson Correlation .279** .111 .088 .054 .293** 1 IB Pearson Correlation .634** .058 .485** -.068 .593** .424** 1 **. P< 0.01

4.5 Regression

Regression analysis will determine the linear regression equation, with the beta found to confirm a causal relationship among the dependent variable:intention behavior to EB and the independent variables are: Perceived usefulness (PU) Perceived Ease (PE) risk awareness (RA), cost (COST), subjective norms (SN) and perceived behavioral control (PBC) . Analyzed using multiple linear regression of SPSS 22.0 software with the method put into a turn (Enter). Assumptions and factors influencing the cost of the service unit in apartment buildings with linear correlation, regression equation for theoretical models as follows:

IB = β0 + β1 PU + β2 PE + β3 RA + β4 COST + β5 SN + β6 PBC + є

Results of regression analysis with SPSS 20.0 software with regression results are as follows:

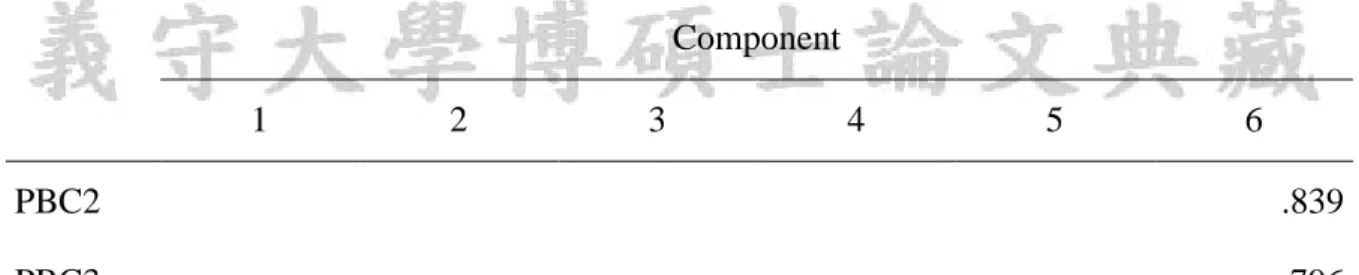

Table 4.7. Model summary variable regression

Model R R Square Adjusted R Square Std. Error of the Estimate

1 .786a .617 .603 .48634

The analytical results show that models the correlation coefficient R2 = .617 and R2 adjusted is .603. The index is to ensure safety in the assessment of the suitability model (not to exaggerate the relevance of the model). With adjusted R2 = .603> 0.3, the model is considered suitable by 60.3%, it means 60.3% of intention behavior to EB is explained by the independent variables.

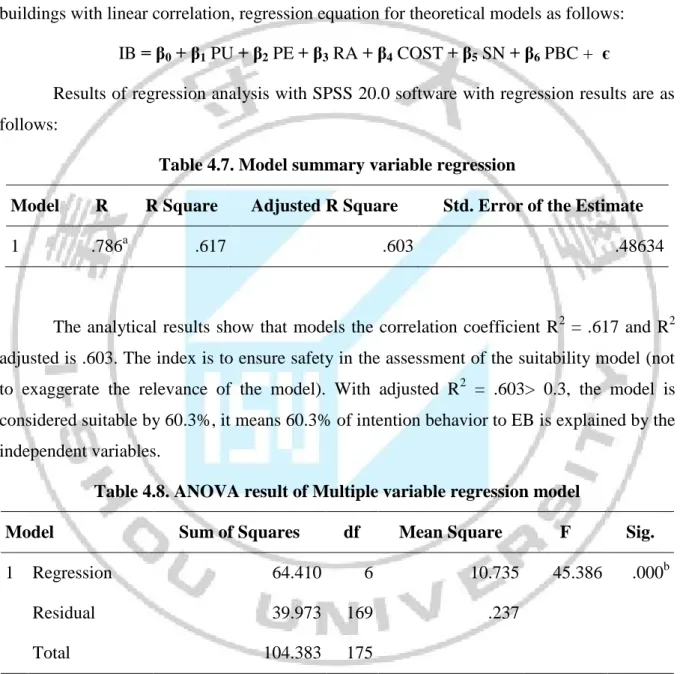

Table 4.8. ANOVA result of Multiple variable regression model

Model Sum of Squares df Mean Square F Sig.

1 Regression 64.410 6 10.735 45.386 .000b

Residual 39.973 169 .237

Total 104.383 175

ANOVA analysis showed that F =45.386 is significant at 0.000 level, suggesting that building the regression model is consistent with the data collected and the factors are statistically significant at the 5% significance. Thus, the factors for the independent variable in the model with factors related to the dependent variable.

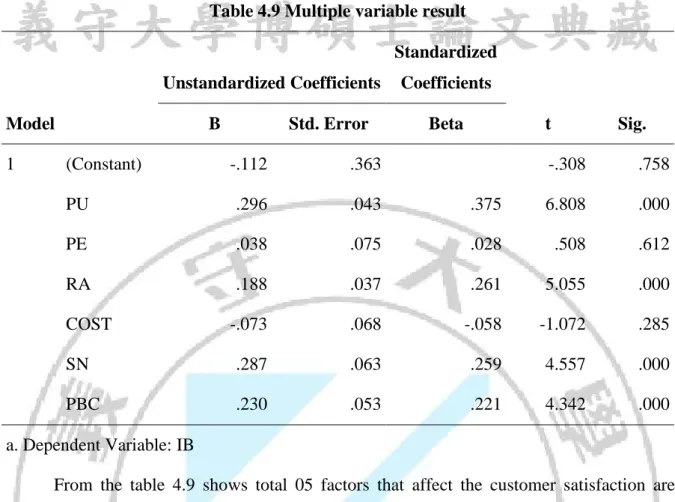

Table 4.9 Multiple variable result Model Unstandardized Coefficients Standardized Coefficients t Sig. B Std. Error Beta 1 (Constant) -.112 .363 -.308 .758 PU .296 .043 .375 6.808 .000 PE .038 .075 .028 .508 .612 RA .188 .037 .261 5.055 .000 COST -.073 .068 -.058 -1.072 .285 SN .287 .063 .259 4.557 .000 PBC .230 .053 .221 4.342 .000 a. Dependent Variable: IB

From the table 4.9 shows total 05 factors that affect the customer satisfaction are included in the regression model, deeming that there are 02 factors are not significance affected on intention behavior to EB with P- value> 0.05 (Perceived Ease (PE) and cost (COST). The four remaining factors have impacted on intention behavior to EB: Perceived usefulness (beta = .375), risk awareness (beta = .261), subjective norms ( beta = .259) and perceived behavioral control (beta = .221)

IB = -.112 + .375PU + .028PE + .261 RA-.058COST + 259SN +.221PBC + є The degree in order of impacted level from high to low as follows: 1) Perceived usefulness (beta = .375), 2) risk awareness (beta = .261). 3) subjective norms ( beta = .259), 4) perceived behavioral control (beta = .221) and This means, in the context of other factors constant, then when factors of Perceived usefulness improved by 1 unit, the intention behavior to EB level will increase 0.375units; the factor risk awareness improved by 1 unit, the intention behavior to EB level will increase 0.261units, when factor perceived behavioral control improved by 1 unit, the intention behavior to EB of customer level will increase 0.221 units and when subjective norms improved by 1 unit, the intention behavior to EB of customer level will increase 0.259 units. So this study indicates that hypothesis H1; H3, H5 and H6 are supported by the model while H2 and H4 are not supported.

4.6 ANOVA/T-test result

H7: There are different intention behavior in using electronic banking service among customer demographic.

For testing the hypothesis H7, t-test and ANOVA is used to test the differences between Socio-demographics (gender, age, education, and income) and intention behavior in using electronic banking service of BIDV

+ The difference between gender and intention behavior

To test the difference between gender and intention behavior, t-test is used. Using the alpha of 0.05, the independent t-test indicates that the average level of intention behavior of male (M= 3.3131, SD=.69400) is not difference from female (M= 3.2697, SD=.81836), t (1) = .360, p>0.05 (table 4.10). It can be concluded that there is not significant difference between male and female in intention behavior.

Table 4.10 Differences between gender and intention behavior

Gender N Mean Std. Deviation Std. Error Mean t Sig. (2-tailed)

IB Male 66 3.3131 .69400 .08543 .360 .719

Female 110 3.2697 .81836 .07803 .375 .708

+ The difference of intention behavior in using electronic banking service of BIDV among age group

To test the difference of intention behavior among age group, the ANOVA with 0.05 sig. is taken ( table 4.11) age group include: > 20 year old, 20 - 35 year old, 36 - 45 year old; 46 - 55 year old and < 55 year old. The result indicates that customer in different age group do not have different level of intention behavior in using electronic banking service (F=1.236; P>0.05).

Table 4.11 The difference of intention behavior among age group

Sum of Squares df Mean Square F Sig.

Between Groups 2.203 3 .734 1.236 .298

Within Groups 102.180 172 .594

The difference of intention behavior in using electronic banking service among Education level

To test the difference of intention behavior among Education level, the ANOVA with 0.05 sig. is taken ( table 4.12) Education level include: Master or more, Bachelor and Below bachelor and high school . The result indicates that customer in different Education level do not have different level of intention behavior in using electronic banking service (F= .245; P>0.05)

Table 4.12 The difference of customer satisfaction among Education level Sum of Squares df Mean Square F Sig.

Between Groups .445 3 .148 .245 .865

Within Groups 103.938 172 .604

Total 104.383 175

+ The difference of customer intention behavior in using electronic banking service among income

To test the difference of customer intention behavior among income, the ANOVA with 0.05 sig. is taken ( table 4.13) income per month include: Under VND 5 mil., VND 5 to 10 mil., VND 11- 20 mil., and over VND 20 mil. The result indicates that customer in different income have different level of intention behavior in using electronic banking service (F= 1.553; P<0.05)

Table 4.13 The difference of customer satisfaction among income per month Sum of Squares df Mean Square F Sig.

Between Groups 2.753 3 .918 1.553 .203

Within Groups 101.631 172 .591

Total 104.383 175

From the result of t-test and ANOVA test, it can be concluded that H7 is not supported with the statement that “There are different intention behavior in using electronic banking service among customer demographic”. The result also indicates that the intention behavior of customer in using electronic banking service is not so high with mean value is just above 3 score.

Chapter V Conclusion and recommendation

5.1 Conclusion

This research is aim to study the intention behavior of customer in using the internet banking service of BIDV by using the TAM model. This study have conduct the survey with customer of BIDV there are 176 valid questionnaires that is imputed in the model. The result indicate that there are 02 factors are not significance affected on intention behavior to EB with P- value> 0.05 (Perceived Ease (PE) and cost (COST) ). The four remaining factors have impacted on intention behavior to EB: Perceived usefulness (beta = .375), risk awareness (beta = .261), subjective norms ( beta = .259) and perceived behavioral control (beta = .221). This result is consistent with the Podder (2005) survey found that the convenience to have a positive impact on the decision to use the acquirer. Besides, The convenience significantly influences the actual behavior of the customers to decide to use acquirer. In the study by Lee et al (2009) point out that the speed of the Internet and the difficulty in implementing online transactions that affect the ability of customers to use online banking services. As Featherman and Pavlou (2003), risks related to the uncertainty of the service, cannot predict and control the process using the service. Urban, Zvěřinová, & Ščasný, (2012) state that there is many evidences that the subjective norms and perceived behavioral control have an impact on consumer behavior intention. From the result of t -test and ANOVA test, it can be concluded that H7 is not supported with the statement that “There are different intention behavior in using electronic banking service among customer demographic”. The result also indicates that the intention behavior of customer in using electronic banking service is not so high with mean value is just above 3 score.

5.2 Recommendation

- Diversification of utility features and services E-BANKING:

Although present, customers know and use E-BANKING service is not much, but in time to demand the use of modern banking services will increase. Therefore, banks are required to make advance plans to deal with the problem.

First of all, banks need to complete the E-BANKING service its existing customers to retain existing and attract new customers.

Second, banks need to further study some new products, provide services with higher technological level as financial leasing, not only registration but also borrowed a loan online. Once more new electronic products will maximize the customer saves time and costs, while also saving the cost of the bank concerned.

Third, the current payment through E-BANKING services as well as other electronic banking is still limited, causing by inconvenience to the payment, inter-bank transfer. This fact requires banks to collaborative research to develop this important feature.

- Increase the confidence of customers to use the service

The users with better self-awareness would be less risky than individual autonomy less than (Chan and Lu, 2004; Wang et al, 2003).Increase user experience: promote the use of incentives to try the product for no charge, and may have certain rewards. Design website content not advertise much, but mainly to introduce the product distribution process. Such websites will make customers easy to use more functions without assistance.

BIDV should implement a campaign to introduce the characteristics of the IB system, its benefits and how to use it. Raising awareness about the benefits of using the system, diversifying the types of services, improve services, provide value-added services such as paying utility bills, implementing marketing one on one.

- Increase awareness of the usefulness of the service

Banks should implement a campaign to introduce the characteristics of the IB system, its benefits and how to use it. Raising awareness about the benefits of using the system, diversifying the types of services, improve services, provide value-added services such as paying utility bills, implementing marketing one on one.

According to Tony Chew, head of risk management technology, the Central Bank of Singapore: There will be no problems in the development of E-BANKING if banks have programs to suit customer training and implement appropriate programs.

- Construct customers a positive attitude towards service

ELECTRONIC BANKING is a service bringing more benefits to customers, but not deployment services widely. There are many channels of information to help customers access to E-BANKING such as: internet, television or through the recommendation of the staff at the counter, but to know and understand the new online banking stop at a small number of customers. Therefore, the work of Marketing for this service rather be focused,

promote promote more services are needed to provide customers with a basic understanding of this service, which has a positive attitude towards ELECTRONIC BANKING:

BIDV should organize seminars, international customer conference E-BANKING service customers with the necessary knowledge on services, raising awareness, gradually changing habits have traditionally used their cash. About Website, hotline support, answer questions for customers to know more to customer service can find out easily, in greater detail. Play leaflets on more services, more active staff in introducing the service to customers.From the enthusiastic introduction, consultancy services, utilities, customers can understand and start approach to services, stimulate the understanding and use of the client.

BIDV should put hoardings, posters, banners and large-format advertising in branch offices or investments located in crowded places such as supermarkets and the intersectionhelp bring efficiency to the work of the services to customers. The Bank should also arrange flyers on products in the transaction in a conspicuous location, convenient for the customer. In addition, the survey results also show that resources from the media have very low efficiency, whereas, this is the means of providing information about the products to each customer an easy and Main most accurate, especially from TV. Banks should regularly have ads on E-BANKING services on local TV stations as HVTV, TRT or a local newspaper.

In addition, banks need to focus on training of professional staff with style, customer service attitude is friendly, enthusiastic and always equip yourself with knowledge about E-BANKING service so that as well as counseling, referral services to customers. Helping customers find service is an easy to use, very useful to help customers save time and money when making transactions through internet baking. Some banks might organize some promotional events to bring online banking services closer to each client, or making of promotional as: free of charge E-BANKING service for those customers registered to use online banking services, free account opening when customers open a personal account at the bank.

- Upgrade technology to increase the accuracy and safety, the security of the system.

BIDV should endeavor to improve the system, regularly upgrade computer technology to increase the accuracy and safety, the security of information systems as well as online transactions. Ensure the provision of safe utility services to customers as well as reasonable alternatives to address thoroughly the risks that may occur, preserve the confidence of customers. However, perfecting such systems need to proceed throughout the banking

system and the loss of a long time. Thus, the sight of the bank branch can make a commitment to its customers, while using online banking services if an error from the bank, bank customers will pay damages. This gives customer’s peace of mind and ease of use to accept E-BANKING service.

The website design simple, friendly interface is important solutions, necessary to attract the attention of customers as well as service learning improve comfort for customers to manipulate. Each utility services should be detailed instructions, how to manipulate the system must be simple. The information and instructions on the website should be available in both Vietnamese and English to facilitate for our customers. The bank managers should regularly surveys customers on service procedures to the maximum simplification and upgrading operations, web site development. In addition, the bank can equip a personal computer system at branches and transaction offices so that employees can directly NH introduce E-BANKING services as well as customers can easily spread test E-BANKING service.

- Focusing on human resources:

Although electronic banking services are developed on the basis of information technology, but people always still play a decisive role. Therefore, banks need to have a clear plan for development of human resources, effective measures for the recruitment, training of personnel in a basically.

In addition, the branch will also need appropriate policies to attract the workforce in the sector of information technology and communications. Good treatment regime as well as a strength to retain qualified staff and qualifications. Therefore, the branch should have policies salary, bonus competitive with banks in the locality.

In addition, BIDV have to plan in conjunction with the universities in the province to recruit collaborators for promotional campaigns and affiliate marketing. These are resources with low wage costs and maintain the marketing program. Based on collaboration, the banks can recruit the best individuals to future training and recruitment become permanent employees.

5.3 Research implication

This study has two implications: academic implication and managerial implication. Base on the TAM model, this study have added the knowledge of intention behavior of customer in banking service since there are lack of research in this area in Vietnam banking industry.

Also this study with the results will make banks manager in decision making to give the solutions to improve customer intention behavior using the electronic banking service.

5.4 Limitation of research

Although this study has the implication, there are some limitation have to discussion in this study. This study is use the TAM model, however the scale is translating from the English and it may have some limitation. Beside the sample size is just reasonable and it is conducted survey in Hanoi and with the BIDV only. The bigger sample size and with other city and other bank should be conduct for next research.

Reference

Agarwal, R., & Prasad, J. (1998). A conceptual and operational definition of personal innovativeness in the domain of information technology. Information systems

research, 9(2), 204-215.

Ajzen, I. (1985). From intentions to actions: A theory of planned behavior. In Action

control (pp. 11-39). Springer Berlin Heidelberg.

Ajzen, I. (1991). The theory of planned behavior. Organizational behavior and human

decision processes, 50(2), 179-211.

Ajzen, I., & Fishbein, M. (1980). Understanding attitudes and predicting social behaviour.

Bhatia, S., & Sethi, N. (2007). History and theory of community psychology in India: An international perspective. In International Community Psychology (pp. 180-199). Springer US.

Buchan, H. F. (2005). Ethical decision making in the public accounting profession: An extension of Ajzen’s theory of planned behavior. Journal of Business Ethics, 61(2), 165-181.

Chan, S. C., & Lu, M. T. (2004). Understanding Internet banking adoption and user behavior: A Hong Kong perspective.

Chang, M. K. (1998). Predicting unethical behavior: A comparison of the theory of reasoned action and the theory of planned behavior. Journal of business ethics,

17(16), 1825-1834.

Chau, P. Y., & Hu, P. J. H. (2001). Information technology acceptance by individual professionals: A model comparison approach. Decision sciences, 32(4), 699-719.

Cooper, C. (1997). The crippling consequences of fractures and their impact on quality of life. The American journal of medicine, 103(2), S12-S19.

Davis, F. D. (1989). Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS quarterly, 319-340.

Featherman, M. S., & Pavlou, P. A. (2003). Predicting e-services adoption: a perceived risk facets perspective. International journal of human-computer studies,

59(4), 451-474.

Fishbein, M., & Ajzen, I. (1975). Belief. Attitude, Intention and Behavior: An

Introduction to Theory and Research Reading, MA: Addison-Wesley, 6.

Gerrard, P., & Barton Cunningham, J. (2003). The diffusion of internet banking among Singapore consumers. International journal of bank marketing, 21(1), 16-28. Hilb, M. (2006). Transnationales Management der Human-Ressourcen. CCTP.

Hori, S., Kondo, K., Nogata, D., & Ben, H. (2013). The determinants of household energy-saving behavior: Survey and comparison in five major Asian cities. Energy

Policy, 52, 354-362.

Hsu, M. H., & Chiu, C. M. (2004). Internet self-efficacy and electronic service acceptance. Decision support systems, 38(3), 369-381.

Im, I., Kim, Y., & Han, H. J. (2008). The effects of perceived risk and technology type on users’ acceptance of technologies. Information & Management, 45(1), 1-9.

Jaruwachirathanakul, B., & Fink, D. (2005). Internet banking adoption strategies for a developing country: the case of Thailand. Internet research, 15(3), 295-311.

Keat, T. K., & Mohan, A. (2004). Integration of TAM based electronic commerce models for trust. Journal of American Academy of Business, 5(1/2), 404-410.