行政院國家科學委員會專題研究計畫 成果報告

科技事業的業外投資、能耐更新與成長策略關係之研究:理

論探索與實證

計畫類別: 個別型計畫 計畫編號: NSC91-2416-H-002-033- 執行期間: 91 年 08 月 01 日至 92 年 07 月 31 日 執行單位: 國立臺灣大學國際企業學系暨研究所 計畫主持人: 李吉仁 計畫參與人員: 劉恆逸 報告類型: 精簡報告 處理方式: 本計畫可公開查詢中 華 民 國 92 年 12 月 5 日

Corporate Venturing Investment, Resource Reconfiguration and Competence-based Growth Strategy

Principal Investigator: Ji-Ren Lee Professor

Department of International Business National Taiwan University

Email: [email protected]

Project Assistant: Heng-Yih Liu Doctoral Student

Department of International Business National Taiwan University

Email: [email protected]

October 2003

Paper submitted for the conclusion of NSC project (91-2416-H-002-033). A portion of this paper has been presented at the 2003 International Conference of Strategic Management Society held in Baltimore, Maryland, USA, and the 5th Globalization Forum held in Taipei, Taiwan. Please do not quote without the author’s permission.

Corporate Venturing Investment, Resource Reconfiguration and Competence-based Growth Strategy

ABSTRACT

Dynamic capability enables resource reconfiguration, which is important when the environment constantly changes in an unanticipated way. However, it may be difficult for current existing management to build new competence because of learning myopia, and external search of new competence provides an alternative way to achieve this end. From competence-based and organizational learning views, we offer a typology of corporate venturing investment that consists of competence replicating, competence leveraging, competence upgrading and competence building activities. This paper proposes that corporate venturing investment can be regarded as a strategic ways to achieve resource reconfiguration.

Resource reconfiguration has synergistic and learning purposes. A synergistic type of resource reconfiguration involves competence replicating and leveraging, and a learning type contains competence upgrading and building activities. When the environment features high level of uncertainty, a learning type of resource reconfiguration is more than a synergistic type because the existing competence may be outdated. By integrating competence-based, transaction cost economics and real options theory, we further discuss the adequate governance structure for each type of corporate venturing investment. Managerial implications and further research directions based on the current work are also discussed.

KEY WORDS: Corporate Venturing Investment, Resource Reconfiguration, Competence-based View, Real Options Theory.

INTRODUCTION

Dynamic capability has received substantial research attention in the extant literature of strategic management. The concept of dynamic capabilities basically highlights the evolutionary nature of a firm’s resource management processes, which refers to a firm’s strategic and organizational efforts in integrating, building and reconfiguring its internal and external competencies to cope with rapidly changing environments (Eisenhart and Martin, 2000; Teece, Pisano and Shuen, 1997). In their view, resource reconfiguration can be regarded as a new combination of resources that creatively destructs the old ones (Schumpeter, 1934), and it consists of retention, addition and deletion of resources (Capron, Dussauge, and Mitchell, 1998). The services provided by a redeployment of resources will be enhanced in a more productive way (Penrose, 1959), and wealth creation to enable firm growth is more feasible. The effort of resource reconfiguration is even more critical to the firm’s success when the current resource combination starts to experience a flat or diminishing return due to environmental change. The quest and pace for resource reconfiguration will be accelerated if the surrounding environment features technological and demand uncertainty. Despite the central role of resource reconfiguration plays in the formation of dynamic capabilities, the extant literature seems to pay less than sufficient attention on how a firm could make competence change more effectively in a context where technology changes apace and demand fluctuates, which motivates the present research exploration.

If the environment is so volatile that firms should respond by reconfiguring resources (Eisenhart and Martin, 2000; Teece et al., 1997) to create new source of rents, competence building becomes the key to sustain competitive advantage. However, building a new competence is a difficult task, and it requires effective organizational processes for new learning (Crossan, Lane and White, 1999). Nevertheless, organizational learning is viewed as a routine-based and path dependent process (Levitt and March, 1988: 319). A firm once successfully builds a competence of which the embedded and path dependent nature may

cause organizational inertia (Hannan and Freeman, 1989), competence trap or core rigidities (Abetti, 1996; Leonard-Barton, 1992; Levinthal and March, 1993). Existing managers may be constrained by their own expertise (Penrose, 1959). Firms need to be wary of learning myopia (Levinthal and March, 1993), which sets limits to sustaining their competitive advantage in the long run. Thus, competence change cannot be easily effectuated within a firm’s boundary, and external search of new competencies becomes important.

An outward search of new competencies to achieve resource reconfiguration mainly has three alternative routes, namely merger and acquisition, contract based alliances and corporate venturing investment. Extant research has focused on how acquisitions provide a means to overcome the constraints on change that existing routines create (Capron and Mitchel, 1998; Singh and Zollo, 1997). In a study on U.S. medical sector, Karim and Mitchell (2000) found that acquisitions play an important role on obtaining substantially different resources. However, mergers and acquisitions can hardly be justified unless the business fit allows a combination of growth and cost reductions that overcomes the acquisition premium and other associated costs (Finnie, 1998). The management hubris in the acquiring firm may be overconfident and overpay for the acquired firm (Roll, 1986; Hayward and Hambrick, 1997). Corporate acquisitions can offer an effective way to maintain growth in conditions of technological uncertainty, but typically suffer very high failure rates (Minshall and Garnsey, 1999). Regarding contract-based alliances, if the transaction contains an exchange of non-marketable know-how, such as firm specific technological competence, it would be susceptible to opportunistic behavior, which in turn incurs high transaction cost under conditions of high demand uncertainty (Hennart, 1988). The associated transaction costs may be too high to allow firms to combine their resources and exploit mutually beneficial opportunities.

An alternative and less explored way to achieving resource reconfiguration is corporate venturing investment. Corporate venturing investment (CVI, hereafter), similar to corporate

venture capital (Chesbrough, 2002), has been defined as a firm’s direct equity investment on an external entrepreneurial firm that is currently not under the focal firm’s discretionary control (Miles and Covin, 2002). Few researchers have addressed the drivers and importance of external corporate ventures (Kanter, 1983; Block and MacMilan, 1993; Chesbrough, 2002). However, recent literature has started to focus on the role of corporate venture capital, making equity investments in entrepreneurial ventures, as a means to generate innovations within the firm (Dushnitsky and Lenox, 2003). CVI could be seen as a means for firms to reach new resources, by which the firm could observe and deploy a new series of resources and, a new source of potential value is likely to generate from the new combinations with the existing competence.

To formalize the linkage between CVI and resource reconfiguration, we first distinguish four types of CVI that a focal firm could pursue (Liu and Lee, 2003), namely competence

replicating, competence leveraging, competence upgrading, and competence building, based

on different types of organizational learning (March, 1991). With this typology, we are able to conceptually define the competence distance between the existing competence and the competence to be engaged from the static synergistic type to a more dynamic learning type of resource reconfiguration (Christensen and Foss, 1997). On the one hand, a synergistic type resource reconfiguration focuses on exploiting the value potential of current competencies within the focal firm. The joint utilization and reinforcement of the same competence will allow the focal and target firms to enjoy economies of scope. On the other hand, a learning type of resource reconfiguration confers the focal firm a great opportunity to scan new and leading competencies, which in the long run makes reconfigure resources more possible.

Based on this typology, we further postulate the decision logic of governance structure between the focal and the target firm for each type of CVI. To achieve this goal, we suggest an integrative view which combines decision considerations of competence-based view, real options theory and transaction costs theory on the differential degree of equity link with

respect to different CVIs. Overall, this paper demonstrate a conceptual endeavor dealing with the motivation, typology and the design of governance structure for CVI as a viable strategic approach to resource reconfiguration, upon which the focal firm’s dynamic capabilities could be constructed and its competitive advantage could sustain.

This paper is organized as follows. First, we elaborate the concept of CVI. Second, through the lens of competence-based view, we offer a typology of resource configuration to explain its underlying rationale. Third, by taking an integrative view, we propose the extent to which the focal firm’s governance structure is designed in each type of CVI. While incorporating contingency into a firm’s decision logic of resource reconfiguration, we will see how these contingent factors affect each proposition. This paper will end up by discussing the potential contributions and providing suggestions for future research in this potential topic area.

CVI AND RESOURCE RECONFIGURATION Purpose of CVI

Having said that external search of investment opportunities offers a possible way for the firm facing technological and demand uncertainty to enjoy synergy and learn new competencies, we need to unveil the black box of these investments that may take many forms and impose different effects on firms’ performance. Firms conduct all sorts of investments. Mainly, their purposes are twofold and probably mixed. On the one hand, firms may pursue financial goals. On the other hand, these investments may carry strategic purposes such as realizing economies of scope or helping the focal firm build new competencies for its longevity. Needless to say, investments that can achieve both objectives are always welcome. However, if firms take into account both technological and demand uncertainty, it seems that both objectives can hardly be fulfilled at one time and their choices are then limited. This paper is focused on those investments that bear strategic purposes, which we call them CVI.

(Dushnitsky and Lenox, 2003). It represents the focal firm’s ownership and commitment in the target firm’s business, which in turn lessens the focal firm’s opportunistic behaviors. In the meantime, relinquishing control of the target firm to its entrepreneurs preserves high power incentive to drive its own business. Though this is a common knowledge among firms, it is seldom studied and emphasized in a systematic way.

Importance of CVI

According to Venture Economics, the activities of CVI dramatically fluctuated almost in accordance with economic changes. However, some companies still pursue external start-ups and persist even in bad times (Chesbrough, 2002). We regard these firm behaviors as strategically viable and worth examining. Some empirical research proposes that entrepreneurial firms may be highly innovative, especially through their interactions with large firms in the same industry (Pavitt, Robson and Townsend, 1987). These target firms can be thought of as the focal firm’s external resources in terms of equity ownership involved, but relinquishing control of the target firm to its managers will preserve high power incentives, which motivate management team to a higher level of achievement. For example, Philips early invested in TSMC to gain economies of manufacturing, but TSMC, led by Morris Chang, always has high level of control by its own management team. TSMC, thanks to its successful business model, excellent process technologies and convincing leadership, has ever since delivered quite an outstanding performance with which Philips also shares.

By following Eisenhardt and Martin (2000) who argue the focus of dynamic capability will be more on changing and redeploying resources under highly uncertain market, we acknowledge the positive relationship between uncertainty and resource reconfiguration, but like to further this discussion by exploring the mechanism by which the firm facing high level of uncertainty manages its competencies. When technology changes apace and demand fluctuates, accelerating the pace of resource reconfiguration becomes important. While internal development of new competencies may be constrained by organizational inertia

(Hannan and Freeman, 1989) and organizational learning is very likely to be trapped by the existing stock of competencies (Levinthal and March, 1993), an external competency sourcing through CVI activities is imperative to resource reconfiguration which leads to a sustainable growth.

Resource Reconfiguration

To address a fast change of environment, firms need to constantly reconfigure resources in order to sustain competitive edge. It is a new combination of resources that involves retaining, addition and deletion of resources (Capron, Dussauge, and Mitchell, 1998), by which the firm can generate new source of rents to keep ahead of competition. In this paper, we conceptually define resource reconfiguration as the qualitative and quantitative changes of both firm-specific and firm-addressable resources for achieving its strategic goals (Sanchez, Heene, and Thomas, 1996). This definition encompasses a firm’s strategic initiative in generating static synergy by an array of product applications based on the same competencies, which are quantitative changes of resources, and enabling dynamic learning to gain different competencies, which are qualitative changes of resources.

A tenet of competence-based view prescribes that it is essential for the firm to consistently build new competencies in order to sustain its long-term growth while leveraging current ones to exploit value potential. From this perspective, our study proposes that resource configuration helps the focal firm realize two strategic goals. First, it is to leverage current competencies into an array of products in order to capture value potential (Prahalad and Hamel, 1990). In such types of resource reconfiguration, synergy is the main theme. Second, it is to build new competencies that enable resource reconfiguration, which can generate new source of rents and sustain competitive advantage. Learning new competencies to help reconfigure resources is the main objective.

Competence-based View on CVI

understanding the source and sustainability of competitive advantage (Barney, 1991; Penrose, 1959; Wernerfelt, 1984), competence-based view conceives of firms as repositories of competencies and posits that firms are able to accumulate, protect and deploy competencies to product markets (Foss, 1996: 1). Competence is defined as “an ability to sustain the coordinated deployment of resources (both tangible and intangible) in a way that helps a firm achieve its goal” (Sanchez, Heene, and Thomas, 1996). It can be envisaged in a firm’s technology, organization process, and management. Once built, it helps the firm establish a clear corporate identity and image, and it becomes an invaluable asset to the firm that differentiates from other competitors. For instance, 3M is equipped with innovative competence, and Sony has a competence of “miniaturization”, which embodies in all of its products.

CVI offers another broad opportunity for competence leveraging and building because of its flexible design of governance structure coupled with relinquishment of control to the target firm, which effectively lessens both parties’ opportunism and preserves entrepreneurial spirits. Moreover, if we follow the traditional concept of dynamic capability (Teece et al., 1997), which are regarded as routine-based processes that engender efficiency, it would lead us to falsely conclude that it is so path dependent to form structural inertia (Hannan and Freeman, 1989), which in turn does harm to innovation. However, by revisiting dynamic capabilities under different level of market uncertainty, Eisenhart and Martin (2000) further a “dynamic” concept of dynamic capabilities, or what we shall call competencies, by proposing that it has different implication and emphasis when firms are under different settings.

TYPOLOGY OF CVI

To provide a systematic view on CVI activities from the competence-based perspective, we will postulate a typology of CVI based on the extent to which exploitative and explorative types of learning (March, 1991) are involved. Different from previous literature, we regard these two types of learning will co-exist, with different degree, in a firm’s competence-based

activities. Based on these two dimensions, we are able to distinguish four types of CVI, as shown in Figure 1, which have different implications in competence-based management. These four types of CVI are competence replicating, competence leveraging, competence

upgrading and competence building. While a detailed elaboration can be found from Liu and

Lee (2003), we will briefly explain the different characteristics of these CVI activities. --- Insert Figure 1 Here ---

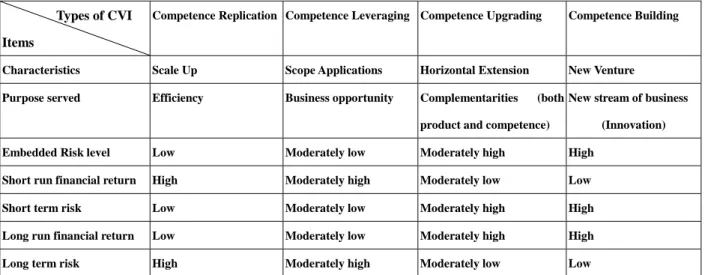

Competence replicating type of CVI has very low degree of explorative and exploitative learning. The target firm has almost the same competencies as the focal firm. The focal firm basically scales up its businesses and the purpose served is efficiency. Competence leveraging type of CVI has low degree of explorative learning but high degree of exploitative learning because it largely applies the focal firm’s existing competencies to enjoy economy of scope. The target firm has some competencies the same as the focal firm, and the focal firm’s purpose is to find out more businesses opportunities by leveraging its current competencies. Please refer to Figure 2.

--- Insert Figure 2 Here ---

Overall, both replicating and leveraging types of CVI convey almost the same or some common competencies between the focal and target firms. It is likely to create static synergy among its resource reconfiguration, which is generated from joint adoption of the same competencies. Thus, a resource reconfiguration that tends to generate static synergy consists

of competence replicating and leveraging types of CVI.

Competence upgrading type of CVI has high level of explorative and exploitative learning. The focal firm upgrades new competencies based on current ones, and the competencies the target firm has are complementary to the focal firm. The degree of interdependence depends on the extent to which complementary assets exist between the focal and target firms. Finally, competence building type of CVI has very high degree of explorative but low extent of exploitative learning. The target firm has no competencies as the

same as the focal firm, so the embedded risk level is the highest among all. However, it perhaps represents the possibility of competence renewal and it may turn out as a great chance to create new businesses. In general, both upgrading and building types of CVI provide dynamic learning benefits. Therefore, a resource reconfiguration that tends to generate

dynamic learning benefits consists of competence upgrading and building types of CVI.

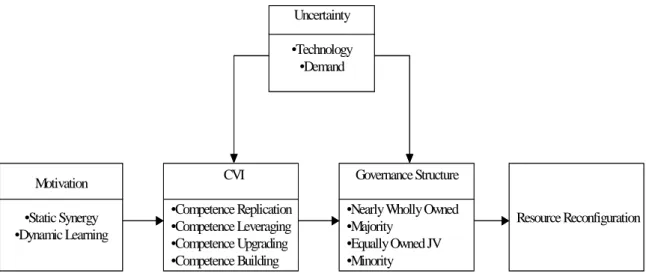

Our conceptual framework of resource configuration is illustrated as Figure 3. Resource reconfiguration that excludes wholly owned subsidiaries, in its completeness, can be achieved through four types of CVI. Next, we like to explore the effect of uncertainty on CVI.

--- Insert Figure 3 Here --- The Role of Uncertainty in CVI

When the environment is more stable, the outcome of each action is more predictable (Eisenhart and Martin, 2000). Competence replicating and leveraging types of CVI is more effective to enable static synergy and strengthen market position because it is more likely to foresee successful applications on an array of products. The firm, all by itself, can even follow its path of development, build upon its repertoire and fully appropriate economic rents. Both types of CVI intend to fully appropriate economic rents generated from joint applications of current competencies in a more stable market, where they are more like routine operation and will be more emphasized by the focal firm (Eisenhart and Martin, 2000). The firm will put more efforts on exploiting its current competence to maximize profits.

On the contrary, in uncertain markets, the firm’s dynamic capabilities, or what we call competencies, involving a set of simple, highly experiential and fragile processes with unpredictable outcome (Eisenhart and Martin, 2000), such as product design competencies, conversion process competencies and commercialization competencies, will be quite susceptible to qualitative change and selection. There is a strong need for the firm to upgrade and build new competencies to sustain its competitive advantage in case it foresees a diminishing return on its current competencies. The firm will put more efforts on dynamic

learning.

Hence, in a more stable market, dynamic capabilities resemble the traditional concept of routines where the firm emphasizes more on replicating or leveraging existing stock of competencies. In contrast, firms confronting highly uncertain market will focus more on change of organizational process, which is actually a qualitative change of competencies and labeled as competence upgrading or building. We suggest the following

Proposition 1a: The focal firm will conduct more of synergistic type of resource reconfiguration in a more stable market. In other words, more competence replicating and leveraging types of CVI will be conducted in a more stable market.

Proposition 1b: The focal firm will conduct more of learning type of resource reconfiguration in a highly uncertain market. In other words, more competence upgrading and building types of CVI will be conducted in a highly uncertain market.

GOVERNANCE STRUCTURE FOR CVI

This paper further explicitly examines how the focal firm devises the associated governance structure in each CVI. By integrating competence-based view, transaction cost economics and real options theory, we are able to have a holistic picture of CVI and suggest some propositions.

The Need for Integrative Views on CVI

Though competence-based view pinpoints the growth direction by which the firm can develop its businesses, it seems incomplete to dictate the governance structure in each CVI by the focal firm facing high uncertainty. On the other hand, real options perspective is valid and important in strategy field in the sense that it deals with uncertainty and concerns more of strategic purpose than simply a financial goal. However, this lens, by contrast, does not relate the extent to which the focal firm leverages or builds competencies. If real options theory hinges on strategic purpose more than financial one, the question arises: how likely will it be

for the focal firm facing high level of uncertainty to proceed CVI without concern of its historical path of development. Business practitioners perhaps will be keen to reply by saying ‘no’. However, after proposing an integration of competence-based view and real options theory, we may find out there is possibility for the focal firm to seriously consider an early and minority entry into a nascent business of which competence is totally new to its own. In other words, in most CVI, we may find competence relatedness existing between the focal firm and its target to some extent. Few of these investments, though small stake at the first place, may carry a pioneering mission that builds a foundation for future growth.

In each CVI, the focal firm seldom ignores the competence it already possesses. In the literature of diversification, the question is always posed like related or unrelated in terms of product market. Nevertheless, in its parlance of competence-based view, we may argue how related the competence is between the focal firm and the target firms. Somehow, competence-based view neglects the level of entry mode which real options theory is dealing with, and the latter ignores the competence implication on which the former actually focuses. Most importantly, one issue in common between these two views is uncertainty.

Transaction cost theory suggests that opportunistic behavior depends on and decreases with the percentage to which each party’s equity holding is committed in their collaborative relationship (Hennart, 1988). Thus, the higher the ownership of the focal firm, the lower the opportunistic behavior of the focal firm. Likewise, the higher the ownership level that confers the focal firm residual right and residual claimant (Chi, 1994), the higher the power incentive that motivates the focal firm great commitment and contribution. On the contrary, the ownership of the focal firm cannot be too high to jeopardize incentives of entrepreneurial firms, especially while building a new competence. The equity mode issue will be further complicated if the environment where the focal firm operates envisages high level of uncertainty. In the later section, we will demonstrate that an integration of competence-based, transaction cost economics and real options view will explain and predict the extent to which

focal firm’s governance structure is designed in each type of CVI. Moreover, the embedded risk level for each type of CVI is different.

Competence Replicating Type of CVI

Competence replication type of CVI involves very low degree of exploitative learning as well as explorative learning. Firms scale up their business in order to economize on their costs of operations. Efficiency is the purpose served. A firm grows by the replication of its technology, which can be better achieved through internal development instead of CVI. Hopefully, learning effects may be realized under a stable environment. Thus, embedded risk level is very low and the firm may enjoy short run benefits rather than long term ones. However, without new knowledge, the replication type of CVI enhances the potential for imitation (Kogut and Zander, 1992) and substitution (McEvily, Das and McCabe, 2000), which may dilute the focal firm’s competitive advantage in the long run.

In general, the management team in the focal firm is very familiar with competence replicating type of CVI. Because the target firm has exactly the same competence as the focal firm, the latter’s management with dominant logic (Bettis and Prahalad, 1995) believe the business they invest will perform as well as they do. Moreover, the focal firm has ownership advantage. For example, Lite-On Electronics Inc. has a major share holding in Lite-onit, which was originally a DVD-ROM product division within Lite-On Electronics Inc. Thus, we have the following suggestion

Proposition 2: In competence replicating type of CVI, the focal firm will be more likely to have a nearly wholly owned equity position.

Competence Leveraging Type of CVI

Competence leveraging type of CVI consists of low level of exploitative learning as well as explorative learning. The focal firm leverages existing competencies to seek more business opportunities, so firms are exploiting the value of their current competencies to enjoy scope of economy (Sanchez and Heene, 1997). The focal firm has some common and horizontal

competencies with the target firm, and embedded risk level is low. Thus, we suggest

Proposition 3: In competence leveraging type of CVI, the focal firm will be more likely to have a major equity position.

Contingent Factors Moderating Competence Leveraging Type of CVI

Uncertainty in general makes firms in favor of hierarchy more than market (Masten, 1984). However, an important research by Balakrishnan and Wernerfelt (1986) claims that technological uncertainty, in contrast, makes full ownership of the relevant technologies more inefficient because these specific technologies may become obsolete at a later stage. In today’s business environment, many have agreed that product life cycle is increasingly shortened by the advent of new products either featuring more sophisticated functionalities or appealing customer preferences that frequently change. It is fairly difficult to predict which technology will be a rising star later on. Though the embedded risk level is low in competence leveraging type of CVI, external environment due to technological change, competition, and demand fluctuation may cause a diminishing return on its existing competencies, which in turn put its long run survival in danger (Chesbrough, 2002). The focal firm may then take a risk reduction approach, and the predicted equity position will be as follows:

Proposition 3a: In competence leveraging type of CVI, the focal firm will be more likely to have a minority equity position in an uncertain environment.

In competence leveraging type of CVI, some of but not all competencies are the same between the focal and target firms. There exists a certain amount of technological uncertainty. The focal firm may take into account some other contingent factors, such as size of the focal firm, value chain position and market position, while considering the governance structure in competence leveraging type of CVI.

Competence Upgrading Type of CVI

learning. Firms upgrade complementary competencies based on current ones. Through the lens of competence-based perspective, the firm is seen as a repository of knowledge and learning device, which enables the firm to learn new routines (Nelson and Winter, 1982). Some of these individual firm networks embodying in the form of investment target firms collectively deliver convincing performance contributing to the focal firm in which we can observe substantial heterogeneity. A successful firm is inclined to create a network context that enables to make diverse competencies visible and concrete, thus new combinations become feasible (Shumpeter, 1934). To pursue this end, the firm needs to have certain level of technological competencies, which will determine what it sees in the external world (Penrose, 1959). As Cohen and Levinthal (1989, 1990) have documented, the ability of a firm to assimilate and use new knowledge is largely a function of its prior knowledge. Therefore, the course of learning adventure for the firm is very much path-dependent on its prior repertoire of competencies.

Due to complementary assets that entail intensive inter-collaboration and mutual trust, embedded risk level and the degree of complementary asset are believed to be so high that there exists a high degree of interdependence between the focal and target firms. Thus, we have

Proposition 4: In competence upgrading type of CVI, the focal firm will be more likely to form a equally owned joint venture.

Competence Building Type of CVI

Competence building type of CVI has very high degree of explorative but low extent of exploitative learning. To grow, firms need to develop certain new competencies on which they can compete in new product markets. Certainly, this turns out a strategic choice about which competencies a firm needs to build and how many competencies a firm should have. A new competence is, by definition, that a firm does not know what it is ex ante, and neither to say how effective it will be for the firm. Further, this so-called ‘new competence’ may be so

nascent that is out of a firm’s current repertoire. Therefore, it exacerbates internal uncertainty within the firm. Firms build new competence that is unrelated to their current businesses. Why Equity? A Transaction Cost Economics View

Some may argue that those entrepreneurial firms will not easily let their specific technological competencies be easily revealed to or appropriated by the focal firm on the grounds that the latter’s opportunistic behavior may be induced wherever better off. In general, two remedies can be adopted to deal with opportunistic behavior. One is social network approach, which highlights the importance of relational asset and needs not necessarily ownership control. The other is economic approach that tends to align individual’s interest with group’s goal through economic organizing (Sanchez, 2003). Claimed by the former perspective, a good relationship among partners in the past, direct or indirect, will be more likely to form another alliance in the future (Gulati, 1995). Relationship per se is an important resource, and whether equity is involved or not in the relationship is not an issue. Though infusing social element between partners may ease tensions and resolve the serious issue of rent appropriation, this socialization approach is generally viewed as an evolving process that perhaps eventually succeeds by discarding opportunism (Ghoshal and Moran, 1996) but could possibly fail in the midway by one single action considered as threat or distrust. Social network theory is convincing in its ability to explain the opportunity set from which firms usually choose target firms for investment because the past relationship offers the focal firm valuable information about who is trustworthy.

However, socialization process normally takes time, which is fine between business units within an organization, but seems economically inefficient between firms especially under a highly uncertain setting. To this end, this paper, by taking economic perspective, suggests that the design of equity-linked form of collaboration can be made to discharge opportunistic behaviors in the collaborative relationship between the focal firm and target firms. If two parties, from transaction cost perspective, connected to a transaction that involves specific

assets, such as specific technological competencies, unexpected contingency that might happen in the future because of firms’ bounded rationality (Simon, 1961) could invoke opportunistic behavior acting in one’s own favor. It is correct because transaction cost perspective assumes of no any equity holding on one another between two parties. In contrast, if one party has equity stake in another, the former puts its own interest in the latter’s hand. The latter’s interest is thus effectively protected because opportunistic behavior of the former will do harm to itself as well. The interests of both parties are intertwined and thus aligned. Equity Holding to What Extent? A Real Options Theory View

The risk ahead is quite uncertain, which includes rapidly technological change and demand fluctuation. Real options theory that is similar to the concepts of financial options but different in its focus on real assets concerns the investments that create capabilities to address future opportunities (Bowman and Hurry, 1993). By adopting a minority investment and subsequently deciding whether go or not go based upon gradually revealing information, scholars argue that the firm implicitly incorporates the logic of real options since this is an economic way of hedging risk nevertheless offers firms tremendous growth opportunities and market value (Chi and McGuire, 1996; Kulatilaka and Perotti, 1998).

Investment in real options gives management the opportunity of continued investment, and the cost of failure is limited (Dixit and Pindyck, 1994; McGrath, 1999). In industries where technology changes rapidly, companies tend to seek alliances to cooperate in the market as well as technology development in an attempt to hedge their risk of technology obsolescence. Using a sample of transactions in the biotechnology industry, Folta (1998) finds strong support that the company will seek minority ownership or joint ventures at the initial stage when the environment is characterized by high technology uncertainty and where investment activity is dominated by growth opportunities. Along this line of argument, initial minority ownership suggested in real options theory not only reduces uncertainty but also helps to create the opportunities for continued investment in the future.

Bounded with rationality, managers cannot foresee all the contingencies in the future (Simon, 1961). It is very common to see companies that are strategically wary of future business often pay attention to market opportunities inherent in emerging technology while they are currently at the stage of prosperity. Hence, it is needless to say how important it should be for those companies stuck in staggering business to come up with right formula. However, one who incorrectly interprets the trend in technology and irreversibly invests in the wrong track will find itself muddling with poor performance and an even worse result. It is a tough decision whether the firm should commit in technologies that are still in the early stage of development. Unfortunately, competitive pressure often facilitates this decision process. Top management will be forced to analyze what is the cost of late entry when competitors go for the pursuit of new capabilities once there is scarce resource in that particular area. Under conditions of uncertainty, the literature applying a real options theory also emphasizes its advantage over traditional approaches, like what BCG approach claims, such as discounted cash flow calculation (Hurry, Miller, and Bowman, 1992; Kogut, 1991; Kogut and Kulatilaka, 1994; Trigeorgis, 1996). Real options theory similar to the concepts of financial options but different in its focus on real assets concerns the investments that create capabilities to address future opportunities (Bowman and Hurry, 1993).

Companies are not only focusing on their primary business in which they commit a great portion of capital resources, but also looking for other new businesses that can possibly be the source of future growth. By adopting a minority investment and subsequently deciding whether go or not go based upon gradually revealing information, scholars argue that the firm implicitly incorporates the logic of real options since this is an economic way of hedging risk nevertheless offers firms tremendous growth opportunities and market value (Chi and McGuire, 1996; Kulatilaka and Perotti, 1998).

After taking an integrative perspective of competence-based view, transaction cost economics and real options theory, we thus suggest

Proposition 5: In competence building type of CVI, the focal firm will be more likely to take a minority equity position.

DISCUSSION AND CONCLUSION

To achieve its organizational goal, the focal firm supported by its management team strategically builds new competencies as well as leverages the existing ones by way of CVI. However, firm’s existing managerial capabilities may be constrained to some extent that building a totally new and unrelated competence is not economically viable. CVI is regarded as a strategic vehicle to bridge this gap by creating a network of competencies by which the focal firm can exploit static synergy (Christensen and Foss, 1997; Zahra and George, 2002) and explore new competencies. To have a profitable growth, firms not only leverage current competencies to exploit resource value but also build new ones to enable resource reconfiguration that generates new rents in an attempt to address rapid change in the environment.

A resource reconfiguration comprising an array of CVI carries two strategic purposes: dynamic learning and static synergy to enhance growth momentum. Learning new competencies from partners helps a focal firm upgrade its own competencies to a more broad level or build a totally new one, which will be beneficial towards the focal firm’s long term growth. With regard to the purpose of static synergy, it will be realized from an array of multi businesses, which normally surround a specific form of technological competence. In fact, this is what competence leveraging is about: leveraging competencies in all sorts of applied products. We suggest these strategic purposes should be tested in the future research. As we have argued, if a learning mechanism can be properly devised between the focal firm and its partner firms, the focal firm can learn and benefit from obtaining new technological competencies that in turn provide opportunities to create new businesses for the focal firm. However, how to implement an effective learning mechanism is worth further study.

the future. An equity stake in these entrepreneurial firms enables the focal firm to be informed of what constitutes their competencies, and it helps the focal firm evaluate the importance of partners’ competencies. However, minority investment hardly ensures the focal firm of successful learning from these entrepreneurial firms because they may release their secret of recipe to the extent to which the focal firm commits more resources in the target firm. Otherwise, there is a potential threat of value appropriation and competition problems by the focal firm as far as these entrepreneurial firms are concerned. Thus, if the focal firm wants to effectuate its learning from these firms, it is more likely to increase equity involvement, which in turn not only shows its commitment but also exercises its control over the target firm. Notice that these entrepreneurial firms are, by definition, likely to maintain a certain degree of discretion. For this reason, we may not see a dominant control on these entrepreneurial firms by the focal firm if the latter wants to rely on its partners’ competencies without the loss of high power incentive. Thus, there exists research potential to see how likely the focal firm, who intends to learn from its partners, increases its equity stake in these entrepreneurial firms without frustrating the extent to which partners’ incentives are sustained. Otherwise, the transfer of competencies is not feasible. Thereafter, two options remain. First, if the new competencies are transferred through the target firm to the focal firm, then we may expect the focal firm get involved in different businesses and undergo a process of diversification, which is defined as a resource reconfiguration of the focal firm where businesses and organization structure are changed. Thus, in our view, resource configuration precedes diversification. Alternatively, if the transfer of new competence is effectuated outside the focal firm, we may observe a new venture that is addressable by the focal firm.

According to Sanchez (2003), an integration of transaction costs theory and real options theory can better capture the problem of economic organizing, which predicts several forms of economic organization under different combinations of supply side and demand side uncertainty. This study, starting from competence-based view, contributes by integrating

transaction cost economics and real options theory, to suggest the way a firm can conduct CVI. This effort has clearly addressed our inquiry into governance structure in each CVI. The value of this integrative view is worth further empirical testing. To note, several variations may also need to be taken into account. For example, human factors may influence the decisions to reconfigure resources, and subsequent governance structure may also be different. Thus, this paper also dictates important managerial implications that enable the focal firm to more precisely delineate its growth foundation.

Conventional wisdom tells us that it is very difficult for the focal firm to self satisfy all its needs. This reality inevitably necessitates collaboration with partnering firms from which the focal firm not only leverages and maximizes the value of its current competencies but also has more opportunities to learn new ones. Among all, as we propose in this paper, a popular collaborative firm behavior is that a firm often conducts CVI that builds their resource configuration more effectively, which in turn enlarges the scope of the firm. Simply put, a well balance of developing new capabilities while managing the existing ones enables the focal firm to grow in a sense that it is so unique as to make imitations less possible and sustain competitive advantage more likely in the market (Kogut and Zander, 1992). Thus, it erects isolating mechanisms that protect the focal firm from imitation and preserve their rent streams (Rumelt, 1984).

To sum up, CVI is viewed as a strategic means to generate profits and establish growth foundation. Once built, all these target firms of venturing investments can be considered as the focal firm’s resource configuration by which the focal firm actually creates an inimitable barrier that is an evolutionary process featuring high level of causal ambiguity and time compression diseconomy.

Extent of Exploitative Learning

High Low High

Extent of Explorative Learning

Low

Figure 1: Corporate Venturing Investment Strategy

Source: Liu and Lee (2003).

Types of CVI Items

Competence Replication Competence Leveraging Competence Upgrading Competence Building

Characteristics Scale Up Scope Applications Horizontal Extension New Venture

Purpose served Efficiency Business opportunity Complementarities (both

product and competence)

New stream of business

(Innovation)

Embedded Risk level Low Moderately low Moderately high High

Short run financial return High Moderately high Moderately low Low

Short term risk Low Moderately low Moderately high High

Long run financial return Low Moderately low Moderately high High

Long term risk High Moderately high Moderately low Low

Figure 2: Typology of Corporate Venturing Investment

Source: Liu and Lee (2003).

Competence Upgrading Competence Building

CVI •Competence Replication •Competence Leveraging •Competence Upgrading •Competence Building Resource Reconfiguration Governance Structure

•Nearly Wholly Owned •Majority •Equally Owned JV •Minority Uncertainty •Technology •Demand

Figure 3: CVI, Resource Reconfiguration and Governance Structure Motivation •Static Synergy •Dynamic Learning CVI •Competence Replication •Competence Leveraging •Competence Upgrading •Competence Building Resource Reconfiguration Governance Structure

•Nearly Wholly Owned •Majority •Equally Owned JV •Minority Uncertainty •Technology •Demand

Figure 3: CVI, Resource Reconfiguration and Governance Structure Motivation

•Static Synergy •Dynamic Learning

REFERENCES

Abetti, P. A. (1996), “The Impact of Convergent and Divergent Technological and Market Strategies on Core Competencies and Core Rigidities: An Exploratory Study,”

International Journal of Technology Management, 11 (3-4), pp. 412-24.

Balakrishnan, S. and B. Wernerfelt (1986), “Technological Change, Competition and Vertical Integration,” Strategic Management Journal, 7, pp. 347-59.

Barney, J. B. (1991), “Firm resources and sustained competitive advantage. Journal of Management, 17(1), pp. 99-120.

Bettis, R.A. and C.K. Prahalad (1995), “The Dominant Logic- Retrospective and Extension,”

Strategic Management Journal, 16(1), pp. 5-14.

Block, Z. and I.C. MacMillan (1993), Corporate Venturing, Boston, MA: Harvard Business School Press.

Bowman, E., and D. Hurry (1993), “Strategy through the Option Lens: An Integrated View of Resource Investments and the Incremental Choice Process,” Academy of Management

Review, 18(4), pp. 760- 82.

Cantwell, J. (2002), Innovation, Profits and Growth: Penrose and Schumpeter, In Pitelis, C. (Eds), The Growth of the Firm: The Legacy of Edith Penrose, Chapter 13: 215-24, New York: Oxford University Press.

Capron, L. and W. Mitchel. (1998), “Bilateral Resource Redeployment Following Horizontal Acquisitions: A Multi-dimensional Study of Business Reconfiguration,” Industry and

Corporate Change, 7, pp. 453-484.

Capron, L., P. Dussauge and W. Mitchell. (1998), “Resource Redeployment Following Horizontal Acquisitions in Europe and North America, 1988-1992,” Strategic

Management Journal, 19(7), pp. 631-61.

Chesbrough, H. W. (2002), Making Sense of Corporate Venture Capital, Harvard Business Review, March, pp. 4-11.

Chi, T. (1994), “Trading in Strategic Resources: Necessary Conditions, Transaction Cost Problems, and Choice of Exchange structure,“ Strategic Management Journal, 15, pp. 271-90.

Chi, T., and D. J. McGuire (1996), “Collaborative Ventures and Value of Learning: Integrating the Transaction Cost and Strategic Option Perspectives on the Choice of Market Entry Modes,” Journal of International Business Studies, 2nd quarter, pp. 285-307.

Christensen, J.F. and N.J. Foss (1997), Dynamic Corporate Coherence and Competence-based Competition: Theoretical Foundations and Strategic Implications, In Heene, A. and Sanchez, R. (Eds), Competence-Based Strategic Management, Chapter 13, pp. 287-312, New York: John Wiley & Sons.

Cohen, W. M. and D. A. Levinthal (1989), “Innovation and Learning: the Two Faces of R&D,” Economic Journal, 99, pp. 569-96.

Cohen, W. M., and D. A. Levinthal (1990), “Absorptive Capacity: A New Perspective on Learning and Innovation,” Administrative Science Quarterly, 35(1), pp. 128-52.

Crossan, M. M., H. W. Lane and R. E. White (1999), “An Organizational Learning Framework: From Intuition to Institution,” Academy of Management Review, 24, pp. 522-37.

Dixit, A.K., and R.S. Pindyck (1994), Investment under Uncertainty, Princeton, NJ: Princeton University Press.

Dushnitsky, G. and M. Lenox (2003), “Investing in New Ventures as a Strategy to Generate Innovations,” paper to be presented at the 23rd Annual Conference of Strategic Management Society held in Baltimore, Maryland, USA.

Eisenhardt, K. M. and J. A. Martin (2000), “Dynamic Capabilities: What are They?” Strategic

Management Journal, 21, pp. 1105-121.

Finnie, W. C. (1998), “Strategic Partnering: Three Case Studies,” Strategy and Leadership, 26(4), pp. 18-22.

Folta, T. B. (1998), “Governance and Uncertainty: The Trade Off between Administrative Control and Commitment,” Strategic Management Journal, 19, pp. 1007-1028.

Foss, N.J. (1996), Introduction: The emerging competence perspective. In Foss, N. J. and Knudsen, C. (Eds), Towards a Competence Theory of the Firm, pp. 1-12, London and New York: Routledge.

Ghoshal, S. and P. Moran (1996), “Bad for Practice: A Critique of the Transaction Cost Theory,” Academy of Management Review, 21, pp. 13-47.

Gulati, R. (1995), “Social Structure and Alliance Formation Patterns: A Longitudinal Analysis,” Administrative Science Quarterly, 40, pp. 619-52.

Hannan, M. and J. H. Freeman (1989), Organizational Ecology, Cambridge: Harvard University Press.

Acquisitions: Evidence of CEO Hubris,” Administrative Science Quarterly, 42(1), pp. 103-127.

Hennart, J-F. (1988), “A Transaction Costs Theory of Equity Joint Ventures,” Strategic

Management Journal, 9(4), pp. 361-74.

Hurry, D., A. T. Miller and E. H. Bowman (1992), “Calls on High Technology: Japanese Exploration of Venture Capital Investment in the United States,” Strategic Management

Journal, 13, pp 8-101.

Kanter, R.M. (1983), The Change Masters: Innovation and Entrepreneurship in the American

Corporation, New York: Simon and Schuster.

Karim, S.Z and W. Mitchell (2000), “Path-Dependent and Path-Breaking Change: Reconfiguring Business Resources Following Acquisitions in the U.S. Medical Sector, 1978-1995,” Strategic Management Journal, 21(10-11), pp. 1061-81.

Knudsen, C. (1996), “The Competence Perspective: A Historical View, In Foss, N. J. and Knudsen, C. (Eds), Towards a Competence Theory of the Firm, pp. 13-37, London and New York: Routledge.

Kogut, B (1991), “Joint Ventures and the Option to Expand and Acquire,” Management

Science, 37(1), pp. 19-33.

Kogut, B. and U. Zander (1992), “Knowledge of the Firm, Combinative Capabilities, and the Replication of Technology,” Organization Science, 3, pp. 383-97.

Kogut, B., and N. Kulatilaka (1994), “Operating Flexibility, Global Manufacturing, and the Option Value of a Multinational Network,” Management Science, 40, pp. 123-39.

Kulatilaka, N., and E. C. Perotti (1998), “Strategic Growth Options,” Management Science, 44(8), pp. 1021-31.

Leonard-Barton, D (1992), “Core Capabilities and Core Rigidities- A Paradox in Managing New Product Development,” Strategic Management Journal, Summer special issue, 13, pp. 111-25.

Levinthal, D. A. and J. G. March (1993), “The Myopia of Learning,” Strategic Management

Journal, 14, pp. 95-112.

Levitt, B. and J. G. March (1988), “Organizational Learning,” Annual Review of Sociology, 14, pp. 319-40.

Liu, H. Y. and J-R. Lee (2003), “Exploring Corporate Venturing Investment Strategy: A Competence and Organizational Learning Perspective,” paper presented at the 23rd

Annual Conference of Strategic Management Society held in Baltimore, Maryland, USA.

March, J. G. (1991), “Exploration and Exploitation in Organization Learning,” Organization

Science, 2, pp. 71-87.

Masten, S.E., (1984), “The Organization of Production: Evidence from the Aerospace Industry,” Journal of Law and Economics, October.

McEvily, S. K., S. Das, and K. McCabe (2000), “Avoiding Competence Substitution through Knowledge Sharing,“ Academy of Management Review, 25(2), pp. 294-311.

McGrath, R.G. (1999), “Falling Forward: Real Options Reasoning and Entrepreneurial Failure,” Academy of Management Review, 24(1), pp. 13-30

Miles, M. P. and J. G. Covin (2002), “Exploring the Practice of Corporate Venturing: Some Common Forms and their Organizational Implications,” Entrepreneurship Theory and

Practice, Spring, pp. 21-40.

Minshall, T. H. W. and E. W. Garnsey. (1999), “Building Production Competence and Enhancing Organizational Capabilities through Acquisition: The Case of Mitsubishi Electric,” International Journal of Technology Management, 17(3), pp. 312-33.

Nelson, R.R. and S.G. Winter (1982), An Evolutionary Theory of Economic Change, Cambridge, MA: The Belknap Press.

Pavitt, K. L. R., M. Robson and J. Townsend (1987), “The Size Distribution of Innovating Firms in the UK: 1945-1983,” Journal of Industrial Economics, 35, pp. 291-316.

Penrose, E. (1959), The Theory of the Growth of the Firm, London: Basil Blackwell.

Prahalad, C. K. and G. Hamel (1990), “The Core Competence of the Corporation,” Harvard Business Review, 68(3), pp. 79-91.

Roll, R. (1986), “The Hubris Hypothesis of Corporate Takeovers,” The Journal of Business, 59(2), pp. 197-216.

Rumelt, R. (1984), Towards a Strategic Theory of the Firm, in R.B. Lamb (Eds.), Competitive

Strategic Management, Upper Saddle River, New Jersey.

Sanchez, R. (2003), “Integrating Transactions Costs Theory and Real Options Theory,”

Managerial and Decision Economics, 24: 267-282.

Sanchez, R. and A. Heene (1997), Competence-based Strategic Management: Concepts and Issues for Theory, Research, and Practice, In Heene, A. and Sanchez, R. (Eds.),

Competence-Based Strategic Management, Chapter 1, pp. 3-42, New York: John Wiley

Sanchez, R. and A. Heene and H. Thomas (1996), Towards the Theory and Practice of competence-based Competition. In Sanchez, R., Heene, A. and Thomas, H. (Eds),

Dynamics of Competence-Based Competition: Theory and Practice in the New Strategic Management, Oxford: Elsevier.

Sanchez, R. and Heene, A. 1996. “Strategic product creation: Managing new interactions of technology, markets and organizations, European Management Journal, 14(2), 121-138. Shumpeter, J. A. (1934), The Theory of Economic Development, Cambridge, MA: Harvard

University Press.

Simon, H. (1961), Administrative Behavior, 2nd ed. New York, NY: Macmillan.

Singh, H. and M. Zollo. (1997), “Knowledge Accumulation and the Evolution of Post-acquisition Management Practices,” Paper Presented at the Academy Management Conference, Boston, MA.

Teece, D.J., G. Pisano and A. Shuen (1997), “Dynamic Capabilities and Strategic Management,” Strategic Management Journal, 18, pp. 537-56.

Trigeorgis, L. (1996), Real options: Managerial Flexibility and Strategy in Resource

Allocation, Cambridge, MA: MIT press.

Wernerfelt, B. (1984), “A Resource-based View of the Firm,” Strategic Management Journal, 5(2), pp. 171-80.

Williamson, O. E. (1991), “Strategizing, Economizing, and Economic Organization,” Strategic Management Journal, 12, pp. 75-94.

Zahra, S.A. and G. George (2002), “Absorptive Capacity: A review, Reconceptualization and Extension,” Academy of Management Review, 27, pp. 185-203.