科技部補助專題研究計畫成果報告

期末報告

雙向人脈資源累積與創業投資績效衡量: 以中國大陸,台

灣及南韓等新興工業國家之教育網絡對高科技創業為例

計 畫 類 別 : 個別型計畫 計 畫 編 號 : NSC 102-2410-H-004-020- 執 行 期 間 : 102 年 08 月 01 日至 103 年 07 月 31 日 執 行 單 位 : 國立政治大學經濟學系 計 畫 主 持 人 : 李文傑 計畫參與人員: 此計畫無其他參與人員 報 告 附 件 : 移地研究心得報告 出席國際會議研究心得報告及發表論文 處 理 方 式 : 1.公開資訊:本計畫可公開查詢 2.「本研究」是否已有嚴重損及公共利益之發現:否 3.「本報告」是否建議提供政府單位施政參考:是,經濟部,教育部 中 華 民 國 103 年 10 月 29 日中 文 摘 要 : 目前既有的文獻在探討經濟體間的新創事業發展績效的差距 時,完全忽略了創業投資投入對於創業績效所造成的影響。 晚近的研究雖已考慮各經濟體間,創業投資產業投入所造成 的創業家生產力改善效果,然而由於創業投資案的形成模式 眾說紛紜,以及個別創業投資案細部資料、創業案兩造雙方 的個別資料難以取得,此二原因造成探討不同程度的教育網 絡連結關係對創業投資案的績效之研究仍付諸闕如。針對這 個缺失,本研究計畫從新假設驗證的設定及建構創投案雙方 的團隊個人資料庫著手改善,如:(1)定義狹義 (創業投資連 結)及廣義的創業投資案 (第二輪持續注資) 形成,以及狹義 創業績效 (被投資公司初次公開發行)和廣義的創業績效衡量 (加入被投資公司的併購事件)的假設檢驗(2)本計畫對台灣的 高科技創業投資案,建構創業投資案以及創投案雙方的教育 網絡資料庫。如此,可以檢驗創業家以及創投經理人之教育 網絡連接關係,其不同程度的雙向連結,是如何影響創業投 資案之標的公司成功公開上市 (IPOs) ,本文結果顯示-教 育網絡衡量越緊密之創業投資案,其成功 IPO 之機率越高, 因此本計畫研究成果也直接證實了教育網絡連結對創業投資 案之資訊不對稱問題以及代理成本的解決有其不可或缺的地 位。 中文關鍵詞: 創業投資、創業家團隊、創業投資經理人團隊、初次公開發 行、創新能力、 教育網絡

英 文 摘 要 : This project sets out to analyze the relationship between start-up entrepreneurial performance in the IT industry and venture capital investment. Most Taiwanese start-up entrepreneurs are experienced engineers repatriating from Silicon Valley during the 80s-90s. They receive sizable investments from either the domestic or Silicon Valley venture capitalists. Using a hand-collected sample of Taiwanese venture capital deals, the importance of social network ties and accumulated human capital is approved. Measures of educational link obtained by having the same degree at the same time better predict venture capital fund performance than do measures of educational link obtained through having

undergraduate or graduate studies at the same school and obtaining the same degree. We also find the distinct demand over the team composition of the venture capital teams as well as start-up firm

management teams. Perhaps counter-intuitively, we find that fund management teams that have more

general human capital in business administration, as measured by more managers having MBAs in either sides of venture capital teams or start-up firm management teams, manage funds with worse performance of

portfolio company exits. Overall, measures of educational link having the same degree and IT industry-specific human capital are stronger

predictors of fund performance than are measures of general human capital. This provides new insights on how the social network interactions as well as the accumulated human capital through education between start-up entrepreneurs and venture capitalists fuel the development miracles of the IT manufacturing industries in Taiwan.

英文關鍵詞: Venture Capital, Entrepreneurial Teams, Educational Network, Venture Capital Investment, High-technology Ventures.

行政院國家科學委員會補助專題研究計畫

□期中進度報告

█期末報告

雙向人脈資源累積與創業投資績效衡量:

以中國大陸,台灣及南韓等新興工業國家

之教育網絡對高科技創業為例

計畫類別:█個別型計畫 □整合型計畫 計畫編號:NSC 102-2410-H-004-020- 執行期間:102 年 8 月 1 日至 103 年 7 月 31 日 執行機構及系所:國立政治大學經濟系 計畫主持人:李文傑 共同主持人: 計畫參與人員:王平 本計畫除繳交成果報告外,另含下列出國報告,共 2 份: ■移地研究心得報告 ■出席國際學術會議心得報告 □國際合作研究計畫國外研究報告 處理方式:除列管計畫及下列情形者外,得立即公開查詢 □涉及專利或其他智慧財產權,□一年□二年後可公開查詢目 錄

中文摘要 ... 1 Abstract ... 2 1、 Introduction ... 錯誤! 尚未定義書籤。 2、 Data ... 3 3、 Hypothesis ... 8 3.1 Major Hypothesis ... 錯誤! 尚未定義書籤。3.2The Descriptive Statistics... 錯誤! 尚未定義書籤。

4、 Regression and Result ... 錯誤! 尚未定義書籤。 5、 Conclusion ... 14 6、 Reference ... 15

表目錄

Table 1 Summary Statistics ... 19 Table 2 Regression Results ... 20 Appendix ... 21

雙向人脈資源累積與創業投資績效衡量:

以中國大陸,台灣及南韓等新興工業國家

之教育網絡對高科技創業為例

Bilateral Network Link and Venture Capital Performance :

the Importance of Educational Network on High-Tech Ventures

in China, Taiwan and Korea.

李文傑 Wen-Chieh, Lee摘要

目前既有的文獻在探討經濟體間的新創事業發展績效的差距時,完全忽略了創業投 資投入對於創業績效所造成的影響。晚近的研究雖已考慮各經濟體間,創業投資產 業投入所造成的創業家生產力改善效果,然而由於創業投資案的形成模式眾說紛紜, 以及個別創業投資案細部資料、創業案兩造雙方的個別資料難以取得,此二原因造 成探討不同程度的教育網絡連結關係對創業投資案的績效之研究仍付諸闕如。針對 這個缺失,本研究計畫從新假設驗證的設定及建構創投案雙方的團隊個人資料庫著 手改善,如:(1)定義狹義 (創業投資連結)及廣義的創業投資案 (第二輪持續注資) 形 成,以及狹義創業績效 (被投資公司初次公開發行)和廣義的創業績效衡量 (加入被 投資公司的併購事件)的假設檢驗(2)本計畫對台灣的高科技創業投資案,建構創業投 資案以及創投案雙方的教育網絡資料庫。如此,可以檢驗創業家以及創投經理人之 教育網絡連接關係,其不同程度的雙向連結,是如何影響創業投資案之標的公司成 功公開上市 (IPOs) ,本文結果顯示-教育網絡衡量越緊密之創業投資案,其成功 IPO 之機率越高,因此本計畫研究成果也直接證實了教育網絡連結對創業投資案之 資訊不對稱問題以及代理成本的解決有其不可或缺的地位。 關鍵詞: 創業投資、創業家團隊、創業投資經理人團隊、初次公開發行、創新能力、 教育網絡Abstract

This paper sets out to analyze the relationship between start-up entrepreneurial performance in the IT industry and venture capital investment. Most Taiwanese start-up entrepreneurs are experienced engineers repatriating from Silicon Valley during the 80s-90s. They receive sizable investments from either the domestic or Silicon Valley venture capitalists. Using a hand-collected sample of Taiwanese venture capital deals, the importance of social network ties and accumulated human capital is approved. Measures of educational link obtained by having the same degree at the same time better predict venture capital fund performance than do measures of educational link obtained through having undergraduate or graduate studies at the same school and obtaining the same degree. We also find the distinct demand over the team composition of the venture capital teams as well as start-up firm management teams. Perhaps counter-intuitively, we find that fund management teams that have more general human capital in business administration, as measured by more managers having MBAs in either sides of venture capital teams or start-up firm management teams, manage funds with worse performance of portfolio company exits. Overall, measures of educational link having the same degree and IT industry-specific human capital are stronger predictors of fund performance than are measures of general human capital. This provides new insights on how the social network interactions as well as the accumulated human capital through education between start-up entrepreneurs and venture capitalists fuel the development miracles of the IT manufacturing industries in Taiwan.

Keywords: Venture Capital, Entrepreneurial Teams, Educational Network, Venture Capital Investment, High-technology Ventures.

1. Introduction

One of the biggest problems faced by entrepreneurs especially those fall in high technology category is to get their start-up funding. In a complete financial market, a talented entrepreneur with a promising project and good reputation usually draws in a long queue of fund providers across all funding sources. However, studies on incomplete contracts by Grossman and Hart(1986) and Hart and Moore(1988) have proved the inability to specify the full contingencies regarding the unpredictable entrepreneurial process. The new entrepreneurs without sufficient backups (i.e. collaterals) would face gigantic borrowing constraints to fulfill the new investment plan. Questions regrading how to facilitate the information dissemination revealing the true qualities of entrepreneurs turn out to be the core in the new venture event. Cohen, Frazzini and Malloy(2008) has pointed out the importance of the educational network in the successful mutual fund performance. This paper; thus, bridges the gap between the researches on the successful entrepreneurial event and the social network in the venture capital market. We discuss the functioning of the educational network and accumulated human capital between venture capitalists teams and the start-up firm management teams. Among various factors leading to the entrepreneurial milestone (i.e. IPO), the educational networks building on top of the correct team composition would distinct out as an indispensable key to success.

Taiwan in the 80s falls in the developing category and decides to develop the IT industry roughly at the same time. The IT industry had long been thought of as a high-growth potential businesses for the upgrade of local industry structure. However, IT industry is so riskier that typically relied on financing from sources other than traditional lenders such as banks during their early growth phases. Saxenian (1994)

argues that venture capitalists can do well by providing capital to early stage ventures in fostering domestic economic growth. Altar (2009) talks about the determinant factors that determine venture capital firms’ size distribution and how venture capital helps to enhance the production efficiency of invested industries. Moreover, in another empirical work of Altar (2009), the constructed structural estimation model empirically supports the idea that clustering of venture capital helps to improve venture capitalists’ skills and productivities through network positive spillovers. Bernhardt and Krasa (2008) agree with venture capital’s contribution to industry development by the fact that venture capitalists are the experts at identifying profitable projects and raising the profitability of the identified projects.

With the above mentioned works stressing the contribution of venture capital on the IT start-up entrepreneurship, the real question regarding the venture capital investments; however, falls on the identification of promising start-up ventures that can be publicly listed in the future. The identification of good venture investment projects should take heavy information flows bilaterally between venture capitalists and start-up entrepreneurs. How the information disseminates through agents in venture capital market and into final successful IPO events, though, is not as well understood. We study a particular type of this dissemination in the form of social networks. Social networks are network structures composed of nodes (usually people or institutions) that are connected through various social relationships ranging from casual to close bonds. In the context of information flow, social networks allow a piece of information to flow, often in predictable paths, along the network. Thus, one can test the importance of the social network in disseminating information by testing its predictions on the flow of information. One convenient aspect of social networks is that they have often been formed ex-ante, sometimes years in the past, and their

formation is frequently independent of the information to be transferred. In this paper we explore a specific type of social network that possesses exactly this feature: connections based on shared educational backgrounds. The nodes of our social networks are venture capital fund managers and senior officers of IT start-up companies in Taiwan between 1980-2010. We believe these two agents provide a useful setting because one side likely possesses private information, while the other side has a large incentive to access this private information.

This research focuses on educational networks as a basis of social networks. We use academic institutions attended for both undergraduate and graduate degrees as our network measure, and test the hypothesis that venture capital investment projects perform significantly better on these connected projects than on non-connected projects, and tend to have more exits (IPOs) on these investments. The use of educational institutions is motivated in the following sense. The connection of educational network could serve as a direct transfer from start-up firm officers to venture capital fund managers as well as the cost reduction of gathering information for venture capital fund managers. Thus the formed educational networks could make it cheaper to access information on start-up venture projects, and so assess managerial quality and new venture quality.

We test the hypothesis that the connected venture investment projects will perform better in terms of exits of the venture backed start-up firms. By the creation of a unique dataset, we overcome the limitation that no database contains comprehensive information on founders and VC partners education history. Our dataset allows us to quantify how close the educational backgrounds are to both venture funds and start-up entrepreneurial firms. Here, a connection to an academic university is defined as: (1)

for start-up firms, any of the major officers ( CEO, CFO and Chairman ) having attended the university and received a degree, and (2) for venture capital funds, any of the managers having attended the university for a degree. Therefore, we can have a numeric measure to define four types of connections between the venture capital managers and the startup firm, based on whether the venture capital managers and a senior official (CEO, CFO or Chairman) of the start-up firm: attend the same school ( type 1 connection ), attended the same school and received the same degree ( type 2 connection ), attended the same school at the same time (type 3 connection) and attended the same school and received the same degree at the same time ( type 4 connection ). Our results support the major hypothesis, that the connected venture investment projects will perform better in terms of exits of the venture backed start-up firms. In addition to the major result, we also observe that the accumulated team human capital functions differently in venture capitalists and the start-up management teams. The start-up management composed of more MBAs are believed to facilitate the better communication with venture capitalists. However, the general human capital embedded in MBAs are not sufficient indicators for venture capitalists to identify promising new ventures. It is legible to deduce that the proper team composition of education backgrounds in both VC and start-up firms generates remarkable synergy in the start-up venture capital investment.

The rest of the paper is structured as follows. Section 2 introduces the data and describes the characteristics of educational networks between venture capitalists and start-up entrepreneurs. Section 3 discusses the hypotheses to be tested and show the descriptive statistics of all the used variables. Section 5 presents the empirical analysis and the main findings. Section 6 concludes.

2. Data

The main empirical challenge with studying the educational network of VC entrepreneurial investment is that no database contains comprehensive information on founders and VC partners education history. To overcome this limitation we create our own data by first merging information from several sources and then hand collecting the variables relevant for our analysis. The dataset are constructed from several sources. The first data source we use is VentureXpert, which is one of the largest and most complete databases on VC investments. VentureXpert includes all the self-reported registered venture capital funds filing with the Taiwan Venture Capital Association (tvca). We focus on the analysis on actively managed Taiwanese venture capital funds by including funds with investment records listed in the VentureXpert. Additionally, we manually screen all funds and exclude those funds without any investment records in Taiwan. VentureXpert provides details on portfolio companies of VC investments by VC funds as well as firm level.

We focus on the historical investment link between VCs and start-up entrepreneurs in the Taiwan venture capital market. We obtain the names of individual board members of venture capital funds as well as venture-backed startups from Commerce Industrial Services Portal data link provided by the Ministry of Economic Affairs in Taiwan. The biographical information of venture capital managers as well as start-up company officers is collected from web pages, news reports, press releases and proprietary surveys from telephone interviews or in-depth personal interviews conducted by us. Our final dataset includes 79 active VC management firms and 162 VC funds. The constructed dataset comprises more than 1100 investment deals which includes more than 400 venture-backed start-up companies in Taiwanese venture capital markets.

Our dataset also includes the biographical information of more than 40000 personal Curriculum Vitae details in venture capitalists as well as company officers. The data contain all the undergraduate and graduate degrees received, the year in which the degrees were granted, and the institutions authorizing the degree. The social networks investigated in this paper are defined on educational backgrounds . Thus the social network link is made by the universities that the venture capital managers and the company officials have attended. Thus, we can match the universities and degrees in our dataset between January 1984 and December 2012. Our dataset allow us to quantify how close the educational backgrounds are to both venture funds and start-up entrepreneurial firms. Here, a connection to an academic university is defined as: (1) for start-up firms, any of the major officers ( CEO, CFO and Chairman ) having attended the university and received a degree, and (2) for venture capital funds, any of the managers having attended the university for a degree. Therefore, a given start-up firm or venture capital fund can be connected to more than one academic institutions.

3. Hypothesis

3-1、 Major Hypothesis

In this paper we assess the impact of educational link on the performance of venture capital investments. Venture capital managers may utilize the comparative advantage in collecting information through their network. Thus, our focus is the connected venture investment project tends to perform better in terms of exit (IPO events of the venture backed start-up firms). Here we can set up the following hypothesis for the further test.

Hypothesis : The connected venture investment projects will perform better in terms of exits of the venture backed start-up firms.

3-2、 The Descriptive Statistics

In order to examine the above hypothesis, we first need a metric to define “connected” venture investment deals. We define four types of connections between the venture capital managers and the start-up firm, based on whether the venture capital managers and a senior official (CEO, CFO or Chairman) of the start-up firm: attend the same school ( type 1 connection ), attended the same school and received the same degree ( type 2 connection ), attended the same school at the same time ( type 3 connection ) and attended the same school and received the same degree at the same time ( type 4 connection ). Here we do not take a strong stand on the relative strength of each type of connection due to the complexity of the interpersonal network link in the IT industry in Taiwan. For example, the National Chiao Tung university (NCTU) have a very well-functioning alumni reunion system at the school level. Thus, the NCTU alumni always share with each other the best IT industrial knowledge. However, we do view type 4 connection as the strongest type of link, and the one that previous classmates provides the most frequent social interactions at school as well as after the graduation.

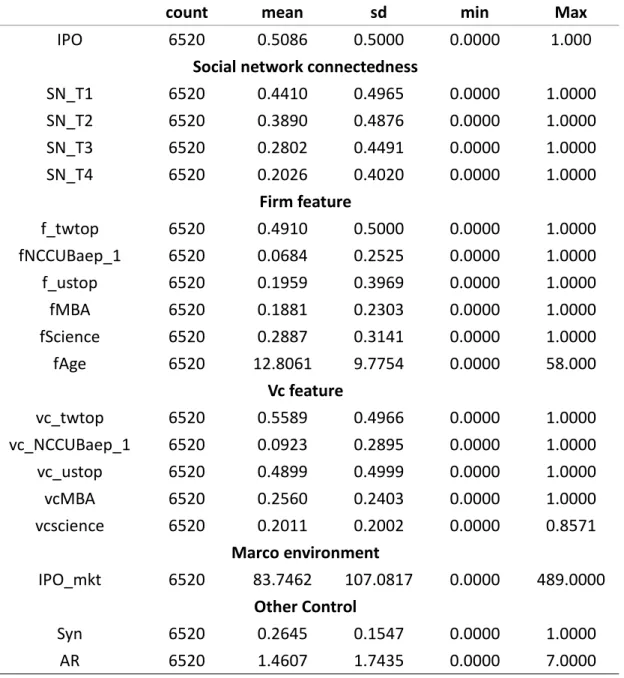

The following Table 1 summarizes the educational network connection measures based on the hand-collected biographical data for the venture capital investment deals in Taiwanese venture capital market targeting at the IT start-up firms. Table 1 also summarizes the IPO events of the venture investment deals as well as the other controlled independent variables that we will use in the regression analysis.

investment deals. The second column of Table 1 reports the mean of each of the dummy variables except for firm age (fage), fMBA, fScience, vcMBA, vcScience, AR and IPO mkt. Dummy variables equal one if an individual venture investment deal possesses a particular characteristic. Details regarding the variable explanations can be found in the Appendix.

Focusing on the first and second column of Table 1, we see most of the venture capitalists and start-up teams comes from either one of the listed Taiwanese universities: NTU, NCTU, NTHU, and NCKU indexed as the f twtop for startup firms and vc twtop for venture capitalists. These four universities are the four best engineering academic institutions in Taiwan. However, venture capitalists are more US-linked with one of the managers graduating from the Ivy League schools and the University of California. The variables: ScienceDegree and MBADegree are computed as the ratio of managers holding Science or MBA degrees in the individual venture capital team or start-up firm.

[ Insert Table 1 Here ]

4. Regression and results

We now turn to the empirical tests of the hypotheses posited in Section 3. We regress the performance of venture investment in which a start-up firm exits and has IPO event in the Taiwan Stock Exchange (TSE) market, on the connection measures and other educational history controls detailed in the descriptive statistics as in Eq. (1).

The subscript i indexes each venture investment deal in the sample. The main variables of interest in testing Hypotheses a are the Connection Measures variables that are summarized in Table 1 and defined in the code book presented in the Appendix. The other variables are venture capital fund-level and start-up firm-level controls - the educational history and the degree background variables on each venture investment i.

Table 2 reports regression results for Eq. (1) estimated using the sample of all the venture capital investments targeting at the IT start-up firms in Taiwan. Regression coefficients and standard errors are reported in each entry of the result of individual regression. The specification in column 1 to column 4 regresses the VC fund’s portfolio companies that are exited on the educational history variables that are directly related to the main Hypothesis. Each of the regression specifications in Table 2 records the distinct measures of educational link between venture capitalists and start-up firm teams that variates in the bilateral connection in the school, degree and the time overlap. In particular, the second specification in Table 2 with regressor which measures whether the venture capital managers and a senior official (CEO, CFO or Chairman) of the start-up firm: attended the same school and received the same degree ( type 2 connection ). The last specification in Table 2 uses independent variable which measures whether the venture capital managers and a senior official (CEO, CFO or Chairman) of the start-up firm: attended the same school and received the same degree at the same time ( type 4 connection ).

[ Insert Table 2 Here ]

Table 2 presents an interesting fact that more human capital accumulated by having science and engineering education may have indeterminate effects on fund performance. The amount of general human capital as measured by having a degree from an ivy league university and the University of California does not significantly predict the portfolio company IPOs on the VC side. Having more IT specific human capital in science and engineering, as measured by having a degree in the area, negatively predicts the portfolio company IPOs in the start-up firm side in all the specifications. The strongest and most robust coefficient on the educational history variables is the coefficient on the fraction of fund managers with a MBA degree. However, contrary to our understanding which posits that more general human capital accumulated from having an MBA degree should be positively correlated with the portfolio company exits, the coefficient on the fraction of managers with an MBA is positive in the firm side while negative in the VC side. An increase in the fraction of fund managers with an MBA from zero to one worsens portfolio companies that exit with IPO and acquisition. Thus, the evidence on the impact of more general human capital on venture capital fund performance is mixed. In the competitive IT industry, the techniques equipped in the start-up firms do not guarantee the successful IPOs. The IPO event involves deep understanding of the capital market and the mere understanding of the techniques cannot be a effective predictor to successful business milestones in the start-up firm side. Alternatively, the educational knowledge brought about by having functional degrees matters less in the good performance of the investment projects. The high information asymmetry embedded in the new venture investments would requires either the risk diversification via syndications (positive syn) or step-wise evaluation based on the previous entrepreneurial performance

(positive AR). We can reaffirm the contributions of educational network on successful IPOs via the above-mentioned summarized effects of the accumulated human capital in start-up firms and Venture capitalists. The frictionless information flow between start-up management teams and venture capitalists would be best predictor to foresee the future successful IPOs in the stock trading markets.

Examining the second to the fifth column in Table 2, we see that the coefficients

on the connection measures of educational backgrounds are similar across the four different specifications. The venture investment deals used in the regression here show that type 1 to type 4 connections explain most of the successful IPOs among the new venture samples used here. However, having tight type 4 link would signal less demand on risk diversification by having smaller coefficients attached to Syn and AR. Besides, close educational network link would complements top university educational history as we have decreasing coefficients attached to variable of f twtop. The impact of having close educational link is robust across different specifications in table 2.

The predicted sign of coefficients in Table 2 strongly support hypothesis , that the connected venture investment projects will perform better in terms of exits of the venture backed start-up firms. The closest educational link of type four connection effectively reduce the cost of information asymmetry as reflected from the smaller coefficients of Syn and AR. As shown in Table 2, the venture investment projects of type 4 connection held by venture capital managers and start-up firms outperforms the venture investment projects in terms of the less demand over risk diversifications. We can also observe in Table 2 that science degree or MBA degrees may not be positively related to the IPOs of venture capital investment. To illustrate an increase in the

fraction of fund managers with an MBA from zero to one worsens portfolio companies that exit with IPO and acquisition. Thus, the evidence on the impact of more general human capital on venture capital fund performance is still mixed as the traditional regression specification without educational link measure across all specifications , with only support that start-up management teams with more MBAs manage better IPO outcomes. Overall, the analysis of Table suggests that measures of past accumulated human capital are not strong predictors of venture capital fund performance than are measures of educational links.

5. Conclusion

Collecting and supplementing data on venture capital funds and their portfolio companies with data on the educational histories of the venture capitalists and start-up entrepreneurs, this paper investigated the hypotheses about the impact of educational network in both VCs and their portfolio companies. Measures of close educational link performs better than do measures of educational history obtained through attending top engineering schools. IT industry-specific human capital related to the science knowledge by more managers having science and engineering degrees are not strong predictors of superior fund performance in the IT entrepreneurial investment. IT Industry-specific human capital does not plays a necessary role in explaining venture capital fund performance here. Furthermore we find that close educational network links would serve as the facilitator over information flow that contributes successful IPOs in the sense of VC’s less demand over risk diversification.

Reference

1. 《Taiwan Venture Capital Industry 2012 Yearbook》, Taiwan Venture Capital Association, Taipei, Taiwan.

2. Akerlof G. A., 1970, “The Market for Lemons:Quality Uncertainty and the Market Mechanism.”,

Quarterly Journal of Economics 84(3):488-500.

3. Alter A., 2009, “Estimating the Return to Organizational Form in the California Venture Capital Industry.”, Working Paper

4. Alter A., 2009, “The Organization of Venture Capital Firms.” Working paper

5. Barnea A. and Guedj I., 2007, “Director Networks and Firm Governance.” Working Paper

6. Beckman C.M., Burton M.D., Reilly C.O., 2007, “Early teams: The impact of team demography on VC financing and going public.”, Journal of Business Venturing22(2):147–173

7. Bengtsson O. and Hsu D., 2013, “Ethnic Matching in the U.S. Venture Capital Market”, Working Paper.

8. Bernhardt D. and Krasa S., 2008, “A Quantitative Theory of Venture Capital” Working paper 9. Chemmanur T. J., Krishnan K., Nandy D.K., 2011, “How Does Venture Capital Financing

Improve Efficiency in Private Firms? A Look Beneath the Surface. ” , working papers

10. Cohen L., Frazzini A., Malloy C., 2008, “The Small World of Investing:Connections and Mutual Funds Returns”, Journal of Political Economy 116(5):951-979.

11. Cumming D., 2008, “Contracts and Exits in Venture Capital Finance.” Review of Financial

Studie 21(5):1947-1982.

12. Gavish B. and Kalay A., 1983, “On the Asset Substitution Problem.”, Journal of Financial and

Quantitative Analysis 26:21-30

13. Giannetti M. and Simonov A., 2009,”Social Interactions and Entrepreneurial Activity.” , Journal

of Economics & Management Strategy 18(3):665–709

14. Gomper P., 1995, “Optimal Investment,Monitoring,and the Stage of Venture Capital”, The

15. Gompers P. and Lerner J., 2004, “The venture capital cycle.” the MIT Press.

16. Grossman S., Hart O., 1986, “The Costs and Benefits of Ownership:A Theory of Vertical and Lateral Integration”, Journal of Political Economy 94(4):691-719.

17. Hall B., Jaffe A., Trajtenberg M., 2001, “The NBER Patent Citations Daya File:Lessons, Insights and Methodological Tools”, NBER Working Paper No. 8498.

18. Hall B., Jaffe A., Trajtenberg M., 2005, “Market Value and Patent Citations”, The RAND Journal

of Economics, Vol. 36, No.1 (2005 ), 16-38.

19. Hamilton B., “Does Entrepreneurship Pay ? An Empirical Analysis of the Returns to Self-Employment”, Journal of Political Economy 108(3):604-631.

20. Hart O., Moore J., 1988, “Incomplete Contracts and Renegotiation”, Econometrica, Vol. 56, N0.4 (Jul. 1988), P.755-785.

21. Hellmann T. and Puri M., 2002, “Venture Capital and the Professionalization of Start-Up Firms:

Empirical Evidence”, Journal of Finance 57(1) : 169-197

22. Hellmann T., 1998, “The Allocation of Control Right in Venture Capital Contracts”, The RAND

January of Economics 29(1):57-76

23. Hirshleifer D., Hsu P. H., Li D., 2013, “Innovations Efficiency and Stock Returns”, Journal of

Financial Economics 107 (2013):632-654.

24. Hochberg Y.V., Ljungqvist A., Y.LU., 2007, “Whom You Know Matters: Venture Capital Networks and Investment Performance.” , The Journal of Finance 62(1) : 251-301

25. Hsu P. H., 2009, “Technological Innovations and Aggregate Risk Premium”, Journal of Financial

Economics 94 (2009):264-279.

26. Hurst E., Pugsley B. W., 2011, “What Do Small Businesses Do?”, NBER Working Paper No. 17041.

27. Jensen M.C. and Meckling W.H., 1976, “Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure”, Journal of Financial Economics 3(4):305-360.

28. Jiang N., Wang P., Wu H., 2009,”Ability-Heterogeneity, Entrepreneurship, and Economic Growth.” , Journal of Economic Dynamics & Control34(3):522-541

29. Kaplan S. N., Stromberg P., 2002, “Financial Contracting Theory Meets the Real World:An Empirical Analysis of Venture Capital Contracts”, Review of Economics Studies 70:281-315. 30. Kramarz F. and Thesmar D., 2006, “Social Networks in the Boardroom.” , Journal of the

European Economic Association 11(4):780-807

31. Lanjouw J., Schankerman M., 2004, “ Patent Quality and Research Productivity:Measuring Innovation with Multiple Indicators”, The Economics Journal 144 (Apr.):441-465.

32. Lee W. C., Hsu H.C., Lin T.C. and Wang S.S., 2014, “Venture Capital and Business Milestones: A Study of IT Entrepreneurship”, Working Paper.

33. Lerner J. and Malmendier U., 2012, “With a little help from my (random) friends: success and failure in post-business school entrepreneurship”, Working Paper.

34. Lerner J., 2012, 《Boulevard of Broken Dreams》.:Why Public Efforts to Boost Entrepreneurship and Venture Capital Have Failed and What to Do About It. Princeton University Press

35. Lucas R. E., 1978, “On the Size Distribution of Business Firm.” The Bell Journal of Economics 9(2).

36. Nanda R., Sorensen J., 2010, “Workplace Peers and Entrepreneurship”, Management Science, Vol. 56, No. 7 (Jul. 2010), P.1116-1126.

37. Noldeke G., Schmidt K. M., 1995, “Option Contracts and Renegotiation:A solution to the Hold-up Problem”, The RAND Journal of Economics, Vol. 26, No.2 (Sep. 1995), P.163-179. 38. Pakes A., Griliches Z., 1980, “Patents and R&D at the Firm Level:A First Look”, NBER

Working Paper No. 561.

39. Rogerson W. P., 1992, “Contractual Solutions to the Hold-up Problems”, Review of Economic

Studies 59:777-94.

40. Romer P., 1990, “Endogenous Technological Change“, Journal of Political Economy 98(5): 71-102.

41. Salanie B., 2005, 《The Economics of Contracts》, Chapter.6-7.

42. Sanjib C., 2005, “Demographic diversity for building an effective entrepreneurial team: is it important?” Journal of Business Venturing 20(6), :727–746

43. Saxenian A. and Hsu J. Y., 2001, “The Silicon Valley-Hsinchu Connection : Technical Communities and Industrial Upgrading”, Industrial and Corporate Change 10(4):893-920. 44. Saxenian A., 1994, “Regional Advantage:Culture and Competition in Silicon Valley and Route

128”, Harvard University Press, Cambridge, MA.

45. Saxenian A., 2002, “The Silicon Valley Connection:Transnational Networks and Regional Development in Taiwan”, China and India. Science Technology & Society 7(1).

46. Shane S., 2000, “Prior Knowledge and the Discovery of Entrepreneurial Opportunities”,

Organization Science, Vol.11, No. 4 (Jul.-Aug. 2000), P.448-469.

47. Steven N. K. and PER Stro¨ mberg P., 2002, “Financial Contracting Theory Meets the Real World: An Empirical Analysis of Venture Capital Contracts. ”, Review of Economic Studies 70(2):281-315

48. Trajtenberg M., 1990, “A Penny for Your Quotes:Patent Citations and the Value of Innovations”,

The RAND Journal of Economics, Vol. 21, No. 1 (1990), 172-187.

49. Zarutskie R., 2008, “The role of top management team human capital in venture capital markets: Evidence from first-time funds.” , Journal of Business Venturing 25(1):155–172

Table 1: Summary Statistics

count mean sd min Max

IPO 6520 0.5086 0.5000 0.0000 1.000

Social network connectedness

SN_T1 6520 0.4410 0.4965 0.0000 1.0000 SN_T2 6520 0.3890 0.4876 0.0000 1.0000 SN_T3 6520 0.2802 0.4491 0.0000 1.0000 SN_T4 6520 0.2026 0.4020 0.0000 1.0000 Firm feature f_twtop 6520 0.4910 0.5000 0.0000 1.0000 fNCCUBaep_1 6520 0.0684 0.2525 0.0000 1.0000 f_ustop 6520 0.1959 0.3969 0.0000 1.0000 fMBA 6520 0.1881 0.2303 0.0000 1.0000 fScience 6520 0.2887 0.3141 0.0000 1.0000 fAge 6520 12.8061 9.7754 0.0000 58.000 Vc feature vc_twtop 6520 0.5589 0.4966 0.0000 1.0000 vc_NCCUBaep_1 6520 0.0923 0.2895 0.0000 1.0000 vc_ustop 6520 0.4899 0.4999 0.0000 1.0000 vcMBA 6520 0.2560 0.2403 0.0000 1.0000 vcscience 6520 0.2011 0.2002 0.0000 0.8571 Marco environment IPO_mkt 6520 83.7462 107.0817 0.0000 489.0000 Other Control Syn 6520 0.2645 0.1547 0.0000 1.0000 AR 6520 1.4607 1.7435 0.0000 7.0000

Appendix

Variable name Variable explanation

Dependent variable:

IPO The invested company achieved IPO . True: 1 ; False: 0

Independent variable:

-Social network connectedness

SN_T1 At least one of the top five managers in the invested company and the venture capital firm graduated from the same school. True: 1 ; False: 0

SN_T2 At least one of the top five managers in the invested company and the venture capital firm graduated from the same school and received same degree. True: 1 ; False: 0 SN_T3 At least one of the top five managers in the invested company and the venture capital

firm graduated from the same school at the same time. True: 1 ; False: 0

SN_T4 At least one of the top five managers in the invested company and the venture capital firm graduated from the same school and received same degree at the same time. True: 1 ; False: 0

-Firm feature

M&A The invested company was merged. True: 1 ; False: 0

LBO The invested company was acquired by leverage. True: 1 ; False: 0 Close The invested company was out of business. True: 1 ; False: 0

f_twtop At least one of the top five managers in the invested company graduated from the National Taiwan University, National Tsing Hua University, National Chiao Tung University, and National Cheng Kung University. True: 1 ; False: 0

fNCCUBaep_1 At least one of the top five managers in the invested company graduated from Baep of the National Chengchi University. True: 1 ; False: 0

flvy_1 At least one of the top five managers in the invested company graduated from the Ivy League schools. True: 1 ; False: 0

The Ivy League schools include Brown University, Columbia University, Cornell University, Dartmouth College, Harvard University, University of Pennsylvania, Princeton University and Yale University.

fUC_1 At least one of the top five managers in the invested company graduated from the University of California. True: 1 ; False: 0

f_ustop At least one of the top five managers in the invested company graduated from the Ivy League schools and the University of California. True: 1 ; False: 0

fMBA The ratio of the top five managers having a MBA degree in the invested company fScience The ratio of the top five managers having an engineering degree in the invested

Appendix (cont.)

Variable name Variable explanation

Independent variable:

-Firm feature

fTaipei The registered place of the invested company is in Taipei. True: 1 ; False: 0 fHsinchu The registered place of the invested company is in Hsinchu. True: 1 ; False: 0

fAge Company Age(yr), the age of the company f_1 Manufacturing industry, True: 1 ; False: 0 f_2 High-tech/Biotech Industry, True: 1 ; False: 0 f_3 Service/Financial Industry, True: 1 ; False: 0

AR Accumulated Rounds, the accumulated times of investment for the invested company -VC feature

vc_twtop At least one of the top five managers in the venture capital firm graduated from the National Taiwan University, National Tsing Hua University, National Chiao Tung University, and National Cheng Kung University. True: 1 ; False: 0

vcNCCUBaep_1 At least one of the top five managers in the venture capital firm graduated from Baep of the National Chengchi University. True: 1 ; False: 0

vclvy At least one of the top five managers in the venture capital firm graduated from the Ivy League schools. True: 1 ; False: 0

The Ivy League schools include Brown University, Columbia University, Cornell University, Dartmouth College, Harvard University, University of Pennsylvania, Princeton University and Yale University.

vcUC At least one of the top five managers in the venture capital firm graduated from the University of California. True: 1 ; False: 0

vc_ustop At least one of the top five managers in the venture capital firm graduated from the Ivy League schools and the University of California. True: 1 ; False: 0

vcMBA The ratio of the top five managers having a MBA degree in the venture capital firm vcScience The ratio of the top five managers having an engineering degree in the venture capital

firm

vcTaipei The registered place of the venture capital firm is in Taipei. True: 1 ; False: 0 vcHsinchu The registered place of the venture capital firm is in Hsinchu. True: 1 ; False: 0

Syn Syndication, more than two venture capital firms jointly fund in the same investment project. True: 1 ; False: 0

-Macro environment

行政院所屬各機關因公出國人員出國報告書

(

出國類別:其他)

「赴美國聖路易華盛頓大學

執行多元入學研究」

心得報告書

服務機關:國立政治大學經濟系 職稱:助理教授 姓名:李文傑 出國地區:美國密蘇里州聖路易市 出國期間:102 年 8 月 23 日 至 102 年 9 月 16 日 報告日期:103 年 10 月 30 日出國成果報告書(格式)

計畫編號 執行單位 政大經濟系 出國人員 助理教授李文傑 出國日期 102 年 8 月 23 日至 102 年 9 月 16 日 , 共 25 日 出國地點 美國密蘇里州聖路易市 出國經費 新台幣 3 萬元 報告內容摘要(請以 200 字~300 字說明) 在國科會計畫以及王平院士的支持下,本研究團隊得以委派經濟系李 文傑助理教授得以至聖路易華盛頓大學的動態經濟研究中心與王平院 士共同針對國科會計畫「雙向人脈資源累積與創業投資績效衡量」,發 展計劃中所需的人脈選擇網絡中的入學選擇相關之理論模型,並且進 一步推導相關的參數動差估計式,此次研究成果豐碩,已完成理論模 型設定並分析,透過第一階段學測錄取的學生(包括「推薦甄選」以及 「申請入學」) 管道入學學生較優異學業成績的可能影響機制。根據 理論模型縮減式之分析討論,我們認為有六個主要原因,包括了:學校 排名差異,準備考試的成本,城鄉差距,考試設計及運氣成分,參與 考試的學生成分組成,學生的風險趨避程度等。下一階段此計畫將延 伸並且區分這六個原因,需要對一理論模型的參數加以估計以精確分 析學生選擇推甄和考試的行為,如此方能深入瞭解「推薦甄選」學生 成績優秀原因。目 錄

壹、 前言………3

貳、 研究過程………3

參、 本次出國目的………5

肆、 本次出國研究之理論模型的重要結論………8

伍、 心得與建議………16

陸、 附錄……… 18

壹、 前言:

本年度國科會計畫之子計畫「雙向人脈資源累積與創業投資績 效衡量」,須以一精密理論模型支持主要推論,由於研究時程設定 相當緊迫,因此研究團隊指派經濟系助理教授李文傑前往美國聖路 易華盛頓大學動態經濟研究中心,與王平院士針對研究議題入學管 道和學生學習及生活表現的關聯性探討,密集討論並設定一精密的 理論模型以供後續政策分析建議及評估做一確實推估,在與王平院 士的 25 天密切互動中,完成核心理論模型的推導,得出了與兩階 段錄取學生素質息息相關的 6 大解釋因素以及其對應之個別參 數,出國學者帶回的寶貴研究成果將供研究團隊後續之參數估計及 供政策推論之用。除此之外,出國學者也得以將此一寶貴研究成 果,廣泛徵詢聖路易華盛頓大學的著名學者,以確實改進本理論模 型的可能缺失,在這 3 周的緊密研究形成中,相信對此一子計畫的 品質及未來發表方向都有了更進一步的掌握,以下則針對與王平院 士完成的研究成果做詳細說明。

貳、 研究過程:

美國聖路易華盛頓大學的動態經濟研究中心為聖路易地區 內動態經濟學領域的最高層級學術交流及研討中心,其成立主旨 在於鼓勵方法及發展對於人力資本,區域經濟,國際經濟,經濟 體內重要人力資本累積等各類美國及世界重要經濟體面對的當 前重要經濟議題之關注及進一步提出解決方法之高階研究場 所,因此本次國科會計畫研究團隊因子計畫「多元入學管道成果 分析」,與動態經濟研究中心之研究主旨切合,故透過國科會計畫主持人王平院士以及連賢明教授的申請,經半個多月的行政申 請作業程序後,由動態經濟研究中心的秘書 Carissa 發給研究成 員經濟系助理教授李文傑邀請函,即期動身前往美國密蘇里州聖 路易市。 總計本次在美國動態經濟研究中心主要在與王平院士處理 多元入學管道的 1. 各項文獻整理以及分析 2. 設定及發展兩階 段入學的理論模型 3.推導理論模型的縮減式 4. 發展參數估計 方法的動差估計式 5.提出目前現階段的結論及建議等。總歸來 說,除了出國學者義務必須完全參與的與王平院士的討論及工作 之外,仍盡力貢獻所學及研究知識與國際學者積極交流,了解最 新發展人力資本累積的經濟學領域的明日之星,並在出國人研究 領域資源錯置問題以及創業研究上讓與會的各國同領域研究者 了解國科會計畫目前研究進展,使其他學者了解此際計畫的研究 資料,獨有的模型設定,以及模型運算的結果,相信在同行加持 下,研究成果會更加豐富。

參、 本次出國研究目的:

在研究計畫發想之初,計畫主持人李文傑即針對目前各研 究文獻及新聞媒體指出的申請入學對於錄取學生能力有正向提 升的論點之因果關係相當存疑,此種事後諸葛的論斷,對於學校 採行多元入學後的政策制定及校務的永續發展並沒有幫助,因此 由民國 100 年時即發想一多元入學成效的研究提案,在國科會計 畫的支持下,目前相關資料陸續到位,在本年度 102 年度度年中, 以在校內各處室幫助之下將資料延伸至繁星計畫範疇之下,因此 本子計畫在資料來源無虞之下,必須立刻進行理論模型的設定即推導,以建立下一階段政策分析的準據,因此研究團隊立刻選定 李文傑助理教授著手請假並動身至美國,並將此子計畫之目的進 成列示如下。 教育和人力資本投資在每一個國家的經濟發展上,都扮演者 舉足輕重的角色,其中高等教育更是重要的一環。台灣高等教育 在過去二十年間內產生了巨大的變革,在「教育鬆綁」的理念下 無論是在數量及品質方面皆解除了嚴格的管制。在數量方面,為 了緩和升學競爭,大學院校數目從 1994 年的 50 所增至 2012 年 的 162 所。而在學校品質層面,為了面對國內外學校間教學及研 究的競爭壓力,各大專院校都根據本身特色與既有強項進行品質 改革與創新。以本校而言,為吸引優秀學生就讀並提供更友善的 學習環境,近年來實施許多重要政策諸如鼓勵多元入學、書院制 度、加速國際化等,讓本校從學生的選擇至人才的培育皆更具效 率性,期望在日益競爭的高教環境中能提供學生一個頂尖的學校 選擇。 瞭解新制度的有效性能提供未來學校及政府政策更堅實的 基礎。本研究計劃將使用本校完整的學生學習及生活層面的資 料,透過嚴謹的計量分析和理論模型來研究兩個在理論和實務上 皆非常重要的議題。例如入學管道和學生學習及生活表現的關聯 性探討。 感謝王平院士及校內各單位的協助及支持,本研究計畫得以

使用政大完整的學生學習及生活資料,比較來自不同入學管道的 學生,其在校學業及非學業表現、甚至畢業後在職場的表現的差 異。我們目前仍先以在校期間表現為主要依據。過去文獻透過個 別學校(例如清華大學、成功大學、中山大學等)的統計敍述結 果主要觀察到經過學校推薦或個人申請入學的學生其在校成績 表現優於指定考試分發入學學生,而我們的結果同樣顯示政大不 同入學管道的學生有類似的現象。然而大學中智育並非唯一的教 學目的,本研究進一步比較不同入學管道學生在生活其他層面的 積極程度是否有差異。我們同樣發現學校推薦或個人申請入學的 學生其工讀情形較普遍,且個人申請學生其擔任社團幹部的比例 也明顯較高。上述結果似乎仍意味著學校推薦或個人申請入學的 學生其生活積極度亦較高。 如何解釋不同管道入學的學生其在學表現的差異?為此我 們建立一個理論模型討論這些採用不同管道入學同學的選擇行 為,期望能藉由這個理論模型,瞭解現有「推薦甄選」入學學生 具有相對優異表現的機制。在我們的模型架構下,學生在經歷過 第一階段學測後得以選擇是否要接受申請入學的結果或是繼續 參加接下來的指考分發,而學生選擇的依據主要取決於:其對於 個人第一階段申請入學的主觀滿意程度、其準備大學指考的能力 及成本、及各校系分配給不同管道入學的名額等。這些因子的強 度會直接影響到各系所在兩階段間招收學生品質的差異。我們建 構此一模型的目的主要是為了提供一個完整的分析架構幫助我

們瞭解學生入學的選擇行為,並提供未來校系設定各入學管道最 適招收名額的基礎。

肆、 此次出國研究之重要結論

一. 實證結果 既有文獻針對不同入學管道學生的比較,主要是從學業成績上 進行評斷,而多數文獻以及各校研究團隊的研究結果中皆發現推甄生 與申請生其學業表現大致上皆優於一般考試分發生。和既有文獻相 比,政大資料庫的主要優勢在於學生資料的完整性,因此我們除了能 針對學生的學業表現進行更細緻的分析外,因此以下本計畫針對政大 學生在學校以及其他的生活層面進行分析,並整理結果如下。 1. 在學業表現方面,我們首先如一般文獻比較不同入學管道學生的 平均成績和成績不及格比例。依據表一我們可以看出,平均而言 透過「推薦甄選」管道入學學生平均成績最高且不及格比例最 低,「申請入學」次之,而「大學聯考」則表現最差。除了平均 數之外,我們增加對於不同入學管道學生的學測成績和在校成績 其分配情形的探討,並進一步同時探討學生在校成績隨著在學期 間的增加,其差異情形是否存在變化?我們的結果(圖一)顯示 「申請入學」學生的學測成績之分配較其他兩種管道入學學生的 學測分數存在一階隨機優勢(first-order stochastic dominance)的學生的學測分數存在一階隨機優勢。在校成績方面(圖二),我 們則發現「推薦甄選」學生的在校成績之分配較其他兩種管道入 學學生的在校成績存在一階隨機優勢(first-order stochastic dominance)的特性。我們另外發現學生的學期成績逐年上升, 同時「推薦甄選」學生各學期的成績皆優於其他兩種管道入學學 生的成績,而此差異程度則逐年減少(圖三)。而就大學總和成 績而言,「推薦甄選」,以及「申請入學」學生之成績皆較偏向高 分群,「大學聯招」學生中下成績分布者的比例較高 (圖四)。 2. 家庭背景: 以政大學生而言,「推薦甄選」,以及「申請入學」學 生的家庭經濟狀況,據學生申請就學貸款比例來推論,應較為寬 裕 (圖十),而「推薦甄選」,以及「申請入學」的學生在爭取獎 學金以及工讀機會的積極程度也勝過「大學聯招」入學的學生 (圖八,圖九)。 3. 課外活動參與:就政大資料而言,「申請入學」的學生表現較為積 極,而「推薦甄選」以及「大學聯招」的學生無明顯區別(圖十 一)。 據此,政大學生資料分布,我們可以之對應各校研究團隊以及 現有文獻的研究成果,主要結果仍反映出第一階段 (推薦甄選以及 申請入學)錄取的政大學生在各方面學業表現以及課外活動積極參

與程度都較第二階段聯招入學的政大學生表現優秀,但這仍然無法 確切回答為何第一階段的學生的各方面能力指標皆較第二階段聯 招錄取學生優秀的根本問題,所以我們於下一節簡介我們的理論模 型的衡量面向,並將以建構完成待行模型參數估計的預期成果簡述 如下。

二、兩階段入學的理論模型 除了透過實際資料呈現各類型學生的表現之外,我們另外設定 理論模型來解釋臺灣地區開始實施大學多元入學制度,其中包含學 科能力測驗(大學甄選入學)以及指定科目考試等入學管道對各大 學錄取學生平均素質的影響。相較於民國 82 年以前實施的大學聯 考,多元入學制度除了提供不同的入學管道之外,也提供了額外的 入學機會。然而在分析多元制度上一個較複雜的因素在於透過不同 入學管道獲得入學的時間是不一致的,因此我們必須在模型中考量 學生在不同時間點的決策行為。這些決策將取決於學生在第一階段 申請入學的成績結果及其對未來表現的預期。本研究團隊的目前設 定的理論模型將可用以衡量兩階段入學學生能力的差異及其表現 差異形成的原因,我們詳列模型指出的能力差異的解釋原因如下: (1) 學校排名差異問題: 如果該校的排名越高,不管是在第一階段或 是第二階段的優秀學生都會傾向接受最頂尖的大學院校的錄 取,也因此,模型可以推估此類學校在第二階段招收的學生素質 會與第一階段相近。學生對第一階段錄取學校排名的在意程度高 低,直接影響了優秀學生參與第二階段考試的意願,也因此本模 型可解釋為何中間等級的國立大學第一階段錄取的學生表現會 較為優異。

(2) 準備考試的成本: 模型指出在第二階段考試的競爭激烈程度以及 學生在第二階段的努力程度,會造成學生本身的準備成本大幅提 高,因此學生也傾向接受第一階段錄取。 (3) 城鄉差距:偏遠區域的學生於準備指定科目考試的資源遠遜於都 會區,因此於第一階段錄取的學生較傾向接受,因此第一階段錄 取學生的素質將被拉高,此一推論與各地區學生準備考試的能力 息息相關,也直接引導各區域學生是否較易於接受第一階段錄取 結果而迴避參與大學聯招。 (4) 考試的運氣成分: 考試的設計機制會影響學生於考試時是否能充 分發揮實力,因此試題設計要是不能精準測定學生能力,則學生 考試表現的誤差將頗大,而造成兩階段入學的學生能力差距擴 大。 (5) 參與各個階段考試的學生之能力分布: 頂尖學校在第一階段很容 易收到表現優異的學生,因為學生即使在第二階段表現再好也是 會選擇就讀此一頂尖學校,所以頂尖的學校在第二階段時的受試 學生母體和第一階段時不同,有可能因為上述各類原因綜合,使 得非特別優秀學生也能在第二階段錄取頂尖大學,因此容易在頂 尖大學中造成兩階段錄取的學生能力差距頗大的問題。 (6) 學生的風險趨避程度: 風險趨避程度較高的學生較為傾向接受第

一階段考試的結果,而有所謂的「低就」的問題,因此也直接造 成兩階段學生的素質差異。

伍、 心得與建議

本次出國研究,發展以及推倒出的模型的強項在於可實際利

用資料計算或估計出各項能力差異的解釋因子的強度如

何,也可以用以衡量政大在兩階段入學的風潮下是否能真正

招收到所謂的「適才適性」的優秀好學生,本模型設定在校

長及學校各處室支持及通力合作下,已取得部分估計所需的

學生資料,下一步將實際進入模型參數運算以及估計的程

序,結合團隊成員各自專業以及一年來設定以及目前運算出

的模型縮減式和動差估計式,這些差異成因的相對模型參數

一但刻畫完成,預計將對各項差異成因有一通盤解釋,並進

一步補足目前研究難以深入探討的兩階段學生表現差異的

真正原因探討。因此統整此次研究心得即建議如下:

1. 主要心得:

透過第一階段透過學測錄取的學生(包括「推薦甄選」以及「申

請入學」) 管道入學學生較優異學業成績的可能影響機制。

根據團隊討論,此次出國研究推導出的模型,認為有六個主

要原因,包括了:學校排名差異,準備考試的成本,城鄉差距,

考試設計及運氣成分,參與考試的學生成分組成,學生的風

險趨避程度等。下一階段此計畫將延伸並且區分這六個原

因,需要對一理論模型的參數加以估計以精確分析學生選擇

推甄和考試的行為,如此方能深入瞭解「推薦甄選」學生成

績優秀原因。

2. 建議事項:

在現有入學制度中,繁星計畫的成效一直是一個討論重點。

一般新聞媒體指出,繁星計畫入學學生表現甚至優於按推薦

甄選入學學生。礙於現有資料僅涵蓋至 2006 年,無法比較

繁星計畫與不同推薦制度下的學生表現是否不同?這些成

績差異機制為何?本年度學校已提供本團隊相關資料並將

資料延長到 2009 年資料(仍不會包括在學學生資料)

,本研

究計畫納入繁星計畫,瞭解不同入學管道的學生學習成效差

異。

陸、

附錄

理論模型附錄 臺灣地區自民國 82 年實施大學多元入學制度,包含學科能力測驗(大學 甄選入學)以及指定科目考試等入學管道。相較於民國 82 年以前實施的 大學聯考,多元入學制度除了提供不同的入學管道之外,也提供了額外 的入學機會。我們打算比較在多元入學制度之下的學生平均素質和大學 聯考的學生之平均素質,並設定了以下的理論模型來解釋。假設測驗分數Si服從常態分配,學校想要招收排名前x比例的學生。因 此,我們可以求出學校錄取學生的分數門檻S。亦即 ( )i i S f S dS x ∞ =

∫

, 1−F S( )=x,−f S dS( ) i =dx,S=S x( )。其中F( )⋅ 表示累積分配函數。由此可 知學校設定的分數門檻S是其打算招收學生比例的函數。 當學校設立了錄取的分數S之後,我們接著找出會選擇該校就讀學生的邊 際素質。假設學生在第一階段選擇去該校就讀,他的錄取分數為 1 i i i S = +q ε ,其中qi 與εi 表示學生的素質和考試的隨機干擾。 學生i 獲得的效用為Ui =max{AU E DU, [ ]}。如果學生在第一階段選擇該校 就讀,他的效用為AU。如果學生拒絕該校的入學許可,他的效用 2 ( ) [ i i] E DU =β S −C 。其中Si2 = +(1 δp qi) i+εi, 2 0 2 i i i p C C γ = + 。Ci為學生準備考 試的成本,pi為學生的努力程度。學生最適的努力水準為 ( ) 0 i E DU p ∂ = ∂ , i i i p q δ γ = , * i i i p =δ γp 。 若選擇在該校就讀,學生的效用為 * AU =S。若選擇不去該校就讀,學生 的效用為 * 2 2 0 1 ( ) [ ] 2 i i i E DU =β q + δ γ q −C 。令AU* =E DU[ *] 就可以得到學生的 邊際素質 2 0 * 2 1 1 2 i( ) i i S C q δ γ β δ γ − + + + = 。 最後,我們算出第一階段錄取學生的平均素質,* 0 ( )i q i ( , )i i i i S E q =

∫ ∫

q ∞ f S q dS dq 。將聯合分配函數代入,即可得到下式。 * 1 2 2 2 2 0 (log( ) ) 1 1 exp( ) exp( ) 2 2 2 2 i i q i q i i S q i i q i q q q d dq q ε ε µ ε ε σ σ pσ pσ ∞ − − − ⋅ −∫ ∫

= * 2 1 2 0 (log( ) ) 1 [1 ( )] exp( ) 2 2 i q i q i i i q i q q q F S q dq q µ σ pσ − − − ⋅ −∫

。 第二階段錄取學生的平均素質為 2 ~ ~ 2 2 2 2 2 0 (log( ) ) 1 [1 ( ) (1 ) ( )] exp( ) 2 2 i i q i i i i i q i q q q F S q F S q q dq q µ q q δ γ σ pσ ∞ − − − − − − − −∫

。 給定qi,S1=S2, ~ ( )i ( )i F S =F S ,得到 ~ ~ 2 2 1 2 2 ( i) ( i) (1 ) ( i i ) F S −q ≥q F S −q + −q F S − −q δ γq 。因此, ~ ~ 2 2 1 2 2 1−F S( −qi) 1≤ −q F S( −qi) (1− −q) (F S − −qi δ γqi)。兩邊同時乘qi, ~ ~ 2 2 1 2 2 [1 ( )] [1 ( ) (1 ) ( )] i i i i i i q −F S −q ≤q −q F S −q − −q F S − −q δ γq 。 根據積分的結果,得到參加多元入學學生的平均素質小於或等於參加大 學聯考學生的平均素質。1