國

立

交

通

大

學

財務金融研究所

碩

士

論

文

國家層級公司治理與現金持有部位之研究

─以美、英、德、法為研究樣本

Country-level Governance and Corporate Cash Holdings: Evidence in

the United States, United Kingdom, Germany, and France

研 究 生:黃馨儀

指導教授: 王淑芬 博士

國家層級公司治理與現金持有部位之研究─以美、英、德、法為

研究樣本

Country-level Governance and Corporate Cash Holdings: Evidence in

the United States, United Kingdom, Germany, and France

研 究 生:黃馨儀 Student:Hsin-Yi Huang 指導教授:王淑芬 博士 Advisor:Dr. Sue-Fung Wang

國 立 交 通 大 學

財務金融研究所

碩 士 論 文

A ThesisSubmitted to Graduate Institute of Finance College of Management

National Chiao Tung University in partial Fulfillment of the Requirements

for the Degree of Master in Finance

June 2011

Hsinchu, Taiwan, Republic of China

國家層級公司治理與現金持有部位之研究─以美、英、德、法為研究樣本

研 究 生:黃馨儀

指導教授: 王淑芬 博士

國立交通大學財務金融研究所碩士班

摘要

依據自由現金流量假說認為企業自由現金流量越多將容易產生代理問題,然而文獻指 出一個國家層級的公司治理程度愈好,其股東權利將獲得較高保障且融資限制也較低, 將有助於提升該國企業的公司治理,也不至於有代理問題的爭議。由於英美法系與大陸 法系國家對股東權利的保障程度不同,因此本研究利用多元回歸與 panel 回歸分析來檢 視美、英、德、法,四個國家之公司治理程度是否會影響企業現金部位。結果顯示英美 法系的國家較大陸法系的國家持有較多的現金部位,其也說明國家層級的公司治理程度 愈高將可以降低企業的代理問題對現金部位的敏感性。 關鍵字:現金持有部位、國家層級公司治理、自由現金流量Country-level Governance and Corporate Cash Holdings: Evidence in the

United States, United Kingdom, Germany, and France

Student:Hsin-Yi Huang Advisor: Dr. Sue-Fung Wang

Graduate Institute of Finance

National Chiao Tung University

ABSTRACT

Based on the free cash flow hypothesis, firms that have more free cash flow are prone to agency problem. However, previous empirical studies suggest that a country with better country-level governance has higher shareholder rights and lower financial constraints; therefore, it is able to improve its corporate governance and avoid agency problem. Because the level of protection to shareholders in the common-law and in the civil-law countries is different, we use ordinary least-squares regression and panel regression to analyze whether country-level governance affects corporate cash holdings in the United States, United Kingdom, Germany, and France. We find that the common-law countries have more cash holdings than the civil-law countries. Our study reveals that higher country-level governance can decrease sensitivity between agency problem and corporate cash holdings.

誌謝

終於寫到誌謝這一部分了,這也代表著這兩年來的研究生生涯即將結束,要面臨人 生的下一個挑戰。回首寫論文的這一過程,面臨了不少的挫折與困難,但總算是撐過來 了。在這段期間,有一群師長親友在背後不斷督促與鼓勵,我才能順利完成論文,我將 藉由這篇誌謝,向他們表達我衷心的謝意 首先要感謝我的指導教授─王淑芬博士,感謝老師在我撰寫論文的過程中,非常有 耐心地指導我、鼓勵我,並且給予我許許多多的建議,除了論文指導外,老師也教我一 些做人處事上應有的態度,在他的指導下,獲益良多,非常地感謝老師。 其次,我要感謝的是我的口試委員─俞海琴博士、杜玉振博士與王衍智博士,感謝 他們在百忙之中能抽空前來參加學生的口試,並且以其豐富的學術經驗給予寶貴的建議, 使本論文更加完善,由衷地感謝各個口試委員。此外,也非常感謝交大財金所所有的教 授這兩年所給予的教導,令學生永感於心。 接著,我要感謝吳堃瑋、邱盟翔、陳英茵以及黃光萍,很高興與大家在同一個指導 老師下學習,感謝大家適時地提供協助,能與大家同生死共患難,這份革命情感實為可 貴,有你們真好。另外,也感謝財金所的所有同學,適時地提供協助與鼓勵,這兩年因 為有大家在,才能使我的研究生生涯過得如此多采多姿。 最後,我要感謝我的家人,在我煩躁的時候,包容我;在我低潮時,鼓勵我,因為 有你們的鼓勵與支持,讓我更加堅強、勇敢。現在,我要將我的喜悅分享給你們,讓我 們一起分享這份成果與榮耀。在此,我也要特別感謝我的外祖父與外祖母,感謝你們對 我和哥哥從小到大的照顧,由於有你們的照顧,使得我們更加地茁壯,希望外祖父能夠 保佑大家皆能平安、順利,外祖母能夠身體健康、長命百歲。 黃馨儀 謹誌 國立交通大學財務金融所碩士班 中華民國一百年六月List of Contents

摘要 ... i ABSTRACT ... ii 誌謝 ... iii List of Contents ... iv List of Tables ... v List of Figures ... vi 1. Introduction ... 12. Data and Methodology ... 4

2.1 Data ... 4

2.2 Descriptive statistics ... 6

2.3 Methodology and hypothesis ... 11

3. Results ... 12

3.1 Univariate analysis ... 12

3.2 Explaining firm cash holdings ... 13

3.3 Robustness tests ... 16

4. Conclusion ... 17

List of Tables

Table 1 Firm-year samples by country ... 6

Table 2 Description of variables ... 8

Table 3 Summary statistics ... 10

Table 4 Whole sample firms t test of important variables by legal system ... 13

Table 5 Pooled cross-country regression ... 15

Table 6 Pooled cross-country regression with country and industry random effects ... 16

List of Figures

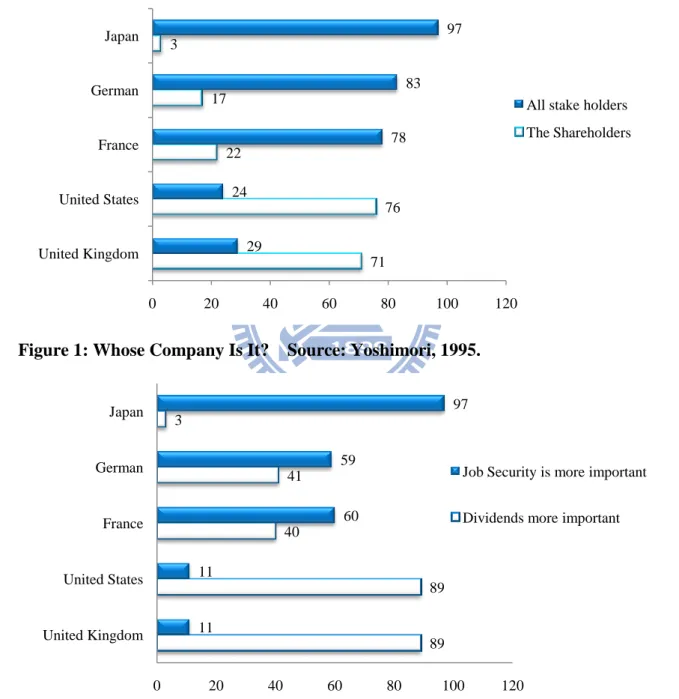

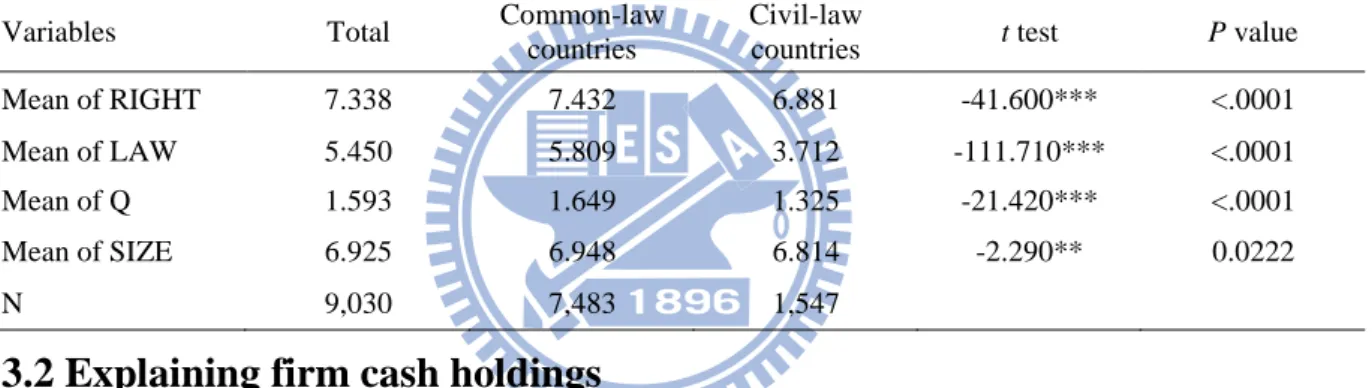

Figure 1: Whose Company Is It? ... 2 Figure 2: Job Security or Dividends? ... 2

1. Introduction

According to financial literature, agency problem has been a controversial issue. Many studies show that firms with weaker corporate governance structure have severe agency problem (Core, Holthausen, and Larcker, 1999). Due to separation of ownership and control in modern corporations, agency problem exists between managers and shareholders when they have conflicting interests (Berle and Means, 1933). Jensen (1986) suggests that firms with excess cash are forced to pay out funds to finance all positive net present value (NPV) investments to minimize the agency cost of free cash flow. In other words, firms keep less cash holdings to avoid agency problem between managers and shareholders.

However, Hillier et al. (2011) show that agency problem is less sensitive to corporate cash holdings of firms with better country-level governance. Harford, Mansi, and Maxwell (2008) suggest that country-level governance is more important than firm-level variation determinants of managerial incentives in controlling agency conflicts, and demonstrate that firms with weaker corporate governance structures have smaller cash reserves because the weakly controlled manager chooses to spend cash quickly on acquisitions and capital expenditures, rather than hold it. Therefore, we expect that country-level governance may reduce the impact of agency problem on corporate cash holdings.

Different countries have different views on what the aims should be, and the different legal rules protecting the investor and the quality of their enforcement result in different corporate governance structures. Researchers contrast two dichotomous model of Anglo-American and continental European corporate governance (Becht and R el, 1999; Bergl f, 1991; Hall and Soskice, 2001; La Porta et al., 1998). Anglo-American countries are labeled common-law countries and shareholder-centered, whereas Continental European countries are considered civil-law countries and stakeholder-centered (Aguilera and Jackson, 2003; Shleifer and Vishny, 1997).

From Figures 1 and 2, we can observe that the United States (US) and the United Kingdom (UK), which are common-law countries, both maximize shareholder wealth, whereas Germany and France, which are civil-law countries, both maximize firm value. Thus, we divide our samples into two groups, common-law and civil-law countries, in order to examine the impact of the country-level governance on cash holdings.

Figure 1: Whose Company Is It? Source: Yoshimori, 1995.

Figure 2: Job Security or Dividends? Source: Yoshimori, 1995.

In addition, developed debt and equity markets contribute to economic growth (King and

71 76 22 17 3 29 24 78 83 97 0 20 40 60 80 100 120 United Kingdom United States France German Japan

All stake holders The Shareholders 89 89 40 41 3 11 11 60 59 97 0 20 40 60 80 100 120 United Kingdom United States France German Japan

Job Security is more important

Levine, 1993; Levine and Zervos, 1998). Rajan and Zingales (1998) and La Porta et al. (2002) find that countries with lower financial constraints have more active capital market. Pinkowitz, Stulz, and Williamson (2004) show that cash is worth less in countries with low investor protection. Similarly, Mikkelson and Partch (2003) find that persistent extreme cash holdings do not lead to poor performance and do not represent conflicts of interests between managers and shareholders. Furthermore, La Porta et al. (1998) suggest that the common-law countries with better legal protections against expropriation by insiders provide more external finance to investors in positive capital. Thus, the common-law countries with better legal protections provide more external finance to investors in positive capital markets, thereby enabling firms to raise funds easily with lower financial constraints and pursue better investment opportunities and enhance their firm value. Therefore, the common-law countries with better country-level governance and lower financial constraints have much more investment opportunities so that their cash value is higher, and they can hold more cash holdings for precautionary motive.

Moreover, stockholders of firms have higher shareholder rights, they can monitor managers and reduce agency problem between managers and stockholders. According to the free cash flow hypothesis, agency problem is positively related to cash holdings. However, Hillier et al. (2011) show that higher country-level governance can decrease sensitivity between agency problem and corporate cash holdings. Hence, firms can use cheaper internal funds (i.e. cash holdings) to make investment, without worrying about agency problem, and it also can reduce the idiosyncratic risk for lower leverage.

Many studies focus on the country-level governance to cash holdings. For example, La Porta et al. (2002) find evidence of higher valuation of firms in countries with better protection and higher cash flow ownership by the controlling shareholder. Dittmar, Mahrt-Smith, and Servaes (2003) evaluate country-level governance to examine the corporate cash holdings among 45 countries, including the emerging, the developing and the developed

countries, and find that firms with poor corporate governance structure hold up to twice as much cash as those with good shareholder protection. Cross-country evidence shows that firms in countries with greater shareholder rights are associated with lower cash holdings (Lins and Kalcheva, 2007; Pinkowitz, Stulz, and Williamson, 2006).

To conclude, we learn that the agency problem is significantly negative to cash holdings; however, firms with better country-level governance can reduce the sensitivity between corporate cash holdings and agency problem with higher shareholder rights to monitor managers and lower financial constraints to raise funds easily. Although cross-country evidence, including both the emerging and the developed countries, shows that shareholder rights are negatively related to cash holdings (Dittmar, Mahrt-Smith, and Servaes, 2003; Lins and Kalcheva, 2007; Pinkowitz, Sulz, and Williamson, 2006), the top four economic markets (i.e., US, UK, Germany and France) we choose in this paper have so strong external capital markets that the investors have more protection than emerging countries; thus, the country-level governance in these four developed countries is much better and they could hold more cash to enhance firm value without worrying about agency problem when they face good investment opportunities. Therefore, we expect that the country-level governance is positively related to cash holdings.

The remainder of the present paper is organized as follows. Section 2 describes the methodology, including the sample selection and research models. Section 3 presents and discusses the results. Section 4 provides the conclusions.

2. Data and Methodology

2.1 Data

We obtain data from the Compustat Global Vantage database from 2002 to 2008. The sample data are drawn from publicly traded firms in four developed countries (i.e., the US, the UK, Germany, and France). We further remove the following sets of firms from the sample: (i)

financial firms (SIC codes 6000–6999), (ii) firms considered governmental or quasi-governmental (SIC codes starting with 9 and SIC codes 4900–4999), (iii) firms with a missing value during this period, and (iv) firms that do not present consolidated financial statements. We exclude financial firms because they carry cash to meet capital requirements, rather than for the economic reasons studied here. We also exclude utilities because their cash holdings are subject to regulatory supervision. In total, our original data comprise 1,737 sample firms and 12,159 observations for the seven firm-years of the four developed countries.

In addition, a few outliers among the sample data may lead to incorrect results. To avoid being misled by these outliers, we winsorize the data. Outliers in firm-year variables are winsorized as follows. LEVERAGE, computed as the debt ratio, is winsorized such that it is between 0 and 1. The bottom tail of NWC, computed as the working capital minus cash and marketable securities to net assets, is winsorized at the 1% level. The top tail of Q, computed as the ratio of the market value of equity plus the book value of liability to the book value of assets, is winsorized at the 1% level. The degree of operating leverage (DOL), which is measured as the percentage change in earnings before interest and tax (EBIT) to the percentage change in sales, is winsorized at the 0.5% and 99.5% levels. Therefore, the remaining sample, the effective data without outliers, consists of 1,290 companies from four countries, and there are 9,030 observations for the seven firm-years of the four developed countries.

Table 1 shows the observations of the original data and the observations of the effective data without outliers.

Table 1 Firm-year samples by country

The original firms and original firm-year are the original data. The effective firms and effective firm-year are the data without outliers.

Germany France United

States

United

Kingdom Total

Original firms 173 202 1,077 285 1,737

Original firm-year observations 1,211 1,414 7,539 1,995 12,159

Effective firms 105 116 861 208 1,290

Effective firm-year observations 735 812 6,027 1,456 9,030

Firm-level accounting data are collected from Compustat Global Vantage, which provides fundamental financial and price data for publicly traded companies. Country-level governance data, such as rule of law and shareholder rights, are collected from the IMD World Competitiveness Online. IMD World Competitiveness Online provides a global reference point on the competitiveness of nations, rankings, and analyses on how an economy creates and sustains the competitiveness of enterprises. These indices from the IMD World Competitiveness Online are all scored from 0 to 10.

2.2 Descriptive statistics

In the present paper, we define the cash ratio of cash and marketable securities to net assets, which are computed as total assets less cash and marketable securities as the proxy for cash holdings. The main reason for netting out from assets is that cash holdings are mainly held for the transaction and precautionary motive, not for a firm’s profitability, which is mainly related to assets without cash and marketable securities. Although not reported in the present paper, we also use cash and marketable to sales ratio as cash ratio to measure, and find that this alternative measure does not affect our main conclusion. This result is also similar to those by Dittmar, Mahrt-Smith, and Servaes (2003) and Opler et al. (1999).

Next, shareholder rights (RIGHT) and rule of law (LAW), as proxies for the country-level governance, are the main explanatory variables in our samples. These data are from the IMD World Competitiveness Online. Shareholder rights index is scored from 0 to 10, which presents the best protection. Rule of law is the legal and regulatory framework index, which is scored from 0 to 10; the higher the score, the higher the legality.

corporate cash holdings. For example, Kim, Mauer, and Sherman (1998) report that firms facing higher costs of external financing with higher financial constraints have more volatile earnings; thus, they should hold more cash holdings. Opler et al. (1999) and Bates, Kahle, and Stulz (2009) find that small firms with strong investment opportunities and riskier cash flows hold larger liquid assets. Hence, investment opportunities, financial constraints, and firm specifics are also factors that affect corporate cash holdings.

How do financial constraints and firm specifics affect corporate cash holdings? First, the existence of asymmetric information between firms and investors makes external financial costly; thus, firms with severe asymmetric information should have more cash holdings to avoid passing up valuable investment opportunities that could earn more cash, which could enhance corporate governance (Myers and Majluf, 1984). Brennan and Hughes (1991) and Collins, Rozeff, and Dhaliwal (1981) suggest that large firms have less information asymmetry than small firms; thus, small firms have higher financial constraints. Thus, we use firm size (SIZE), which is computed as the natural logarithm of total assets, as the proxy for the financial constraints. In addition, we use Tobin’s q (Q), which is computed as the ratio of market value of equity plus book value of liability to book value of assets, as the proxy for the investment opportunities.

Second, firm specifics also affect cash holdings. Firms with higher idiosyncratic risk face higher cost of external financing; thus, they should hold more cash to avoid giving up valuable growth opportunities (Kim, Mauer, and Sherman, 1998; Bates, Kahle, and Stulz, 2009). Because DOL1 is used to measure the idiosyncratic risk of a firm, we use it as the proxy for the idiosyncratic risk. Although not reported in the present paper, we also use standard deviation of cash flows divided by average total assets as idiosyncratic risk, and find

1

Firms with higher idiosyncratic risk need to accumulate more cash to solve a higher frequency of cash flow shortfalls. This implies that firms with more volatile cash flows have higher idiosyncratic risk so that they would hold more cash (Bates, Kahle, and Stulz, 2009; Ferreira and Vilela, 2004; Harford, Mansi, and Maxwell, 2008; Opler et al., 1999). In addition to the cash flow volatility, the degree of operating leverage (DOL) is also a method to measure the firm’s idiosyncratic risk. Hence, we use DOL, computed as the percentage change in EBIT to the percentage change in Sales, as the proxy for idiosyncratic risk.

that this alternative measure does not affect our main conclusion. Next, Baskin (1987) argues that the cost of funds used to invest in liquidity increases as the ratio of debt financing increases, which implies a reduction in cash holdings with increased debt in capital structure. We therefore use leverage (LEVERAGE), computed as the ratio of total debt to total assets, as a substitute for cash. In addition to cash, another substitution effect is due to other liquid assets of firms because firms with sufficient liquid assets may not have to raise funds through the capital markets when they experience cash shortage. Hence, we use non-cash liquid assets (NWC), computed as the ratio of working capital minus cash and marketable securities to total assets minus cash and marketable securities, as substitutes for cash.

All the firm-level financial and country-level governance variables are defined in Table 2.

Table 2 Description of variables

This table shows the definition of variables. The full sample period is from 2002 to 2008. Firm-level accounting data are collected from Compustat Global Vantage. Country-level governance data, such as rule of law and shareholder rights, are collected from the IMD World Competitiveness Online. Net assets are computed as assets less cash and equivalents.

Measurement item Proxy

variable Definition Reference Dependent variable

Cash holdings CASH The ratio of cash and marketable securities to net assets

Bates et at., 2009; Dittmar, Mahrt-Smith, and Servaes, 2003; Opler et al., 1999; Ozkan and Ozkan, 2004.

Explanatory variables

Country-level governance

LAW The index of rule of law is collected from the IMD World Competitiveness Online. The index is from 0 to 10 (best).

La Porta et al., 2002. RIGHT The index of shareholder rights is collected

from the IMD World Competitiveness Online. The index is from 0 to 10 (best).

La Porta et al., 2002.

Control variables

Investment opportunities

Q (Market value of equity+book value of liability ) /book value of assets

Bates et at., 2009; Dittmar, Mahrt-Smith, and Servaes, 2003; Opler et al., 1999; Ozkan and Ozkan, 2004. Financial constraint SIZE The natural logarithm of book value of

assets

Firm specifics NWC The ratio of working capital less cash and marketable securities to net assets

DOL Degree of operating leverage = % change in EBIT/% change in Sales

LEVERAGE The ratio of total debt to total assets

Other variables included in the main analysis but not reported in the table are (i) industry dummies and (ii) a common law dummy (Common). We compute the ratio of cash and

marketable securities to net assets within the Fama and French 48 industry categories (similar with Dittmar and Mahrt-Smith, 2007). There remain 42 industry categories in our paper for firms with missing values and for financial firms and utilities. The common law dummy is a dummy equal to 1 for the common-law countries and 0 for the civil-law countries.

Table 3 provides mean, median, and standard deviation of whole variables in our analysis for the period 2002–2008.

On average, firms of four countries hold 13.8% of CASH. This ratio is highly skewed, with a median of 6.9%. US firms have the largest standard deviation of CASH. The common-law countries (i.e., the US and the UK), on average, receive higher score than civil-law countries, such as Germany and France. This is similar with the findings of La Porta et al. (1998). Next, the common-law countries also have higher LAW and RIGHT than the civil-law countries.

Furthermore, firm specifics and financial constraints also affect cash holdings (Bates, Kahle, and Stulz, 2009; Dittmar, Mahrt-Smith, and Servaes, 2003; Dittmar and Mahrt-Smith, 2007; Faulkender and Wang, 2006; Opler et al., 1999; Ozkan and Ozkan, 2004; Pinkowitz, Stulz, and Williamson, 2006). According to previous empirical studies, we can expect that small firms with better investment opportunities, more idiosyncratic risk, and less liquidity will hold more cash holdings.

In this table, we find some conditions of control variables as follows. First, the common-law countries have higher Q than the civil-law countries; however, the civil-law countries have higher SIZE than the common-law countries. Second, NWC and LEVERAGE are substitutes for cash; firms can use them when they have cash shortfalls. Among these counties, we find that both LEVERAGE and NWC of the civil-law countries are higher than those of the common-law countries. Third, firms with higher idiosyncratic risk need to accumulate more cash to deal with a higher frequency of cash flow shortfalls. In Table 3, it reveals that the civil-law countries have higher idiosyncratic risk (DOL) than the

common-law countries.

Table 3 Summary statistics

This table provides mean, median, and standard deviation of whole variables in our analysis. The data are from 2002 to 2008. There are 735 samples for Germany, 812 for France, 6,027 for the US, and 1,456 for the UK. The US and the UK are common-law countries. Germany and France are civil-law countries. The total samples contain 9,030 observations. The detailed variable definitions are defined in Table 2.

Country Germany France United

States

United

Kingdom Common Civil

N 735 812 6,027 1,456 7,483 1,547 Dependent variable Cash holdings CASH Mean 0.103 0.145 0.149 0.104 0.127 0.124 Median 0.066 0.108 0.066 0.062 0.064 0.087 Standard 0.152 0.138 0.278 0.125 0.202 0.145 Explanatory variables Country-level governance LAW Mean 3.900 3.541 6.009 4.983 5.496 3.721 Median 3.900 3.300 6.230 4.300 5.265 3.600 Standard 0.727 0.526 0.482 1.049 0.766 0.627 RIGHT Mean 7.310 6.493 7.499 7.156 7.328 6.902 Median 7.350 6.520 7.480 7.020 7.250 6.935 Standard 0.194 0.292 0.453 0.318 0.386 0.243 Control variables Investment opportunities Q Mean 1.319 1.330 1.689 1.480 1.585 1.325 Median 1.156 1.230 1.476 1.345 1.411 1.193 Standard 0.531 0.426 0.800 0.652 0.726 0.479 Financial constraints SIZE Mean 6.619 6.992 7.188 5.954 6.571 6.806 Median 6.358 6.734 7.153 5.781 6.467 6.546 Standard 2.139 2.087 1.771 2.090 1.931 2.113 Firm specifics LEVERAGE Mean 0.229 0.237 0.246 0.225 0.236 0.233 Median 0.226 0.234 0.226 0.207 0.217 0.230 Standard 0.135 0.144 0.167 0.148 0.158 0.140 NWC

Mean 0.121 0.039 0.096 0.027 0.062 0.080 Median 0.123 0.033 0.084 0.010 0.047 0.078 Standard 0.175 0.185 0.171 0.179 0.175 0.180 DOL Mean 16.925 12.347 10.377 12.939 11.658 14.636 Median 3.431 2.398 2.190 2.338 2.264 2.915 Standard 58.699 41.116 32.183 51.590 41.887 49.908

2.3 Methodology and hypothesis

Many studies suggest that the different legal rules protecting the investor and the quality of their enforcement cause the different corporate governance structure. Hence, in the present paper, we divide our sample into two groups, the common-law countries (i.e., the US and the US) and the civil-law countries (i.e., Germany and France), by different national legal systems, and we focus on the effect of the country-level governance to the corporate cash holdings.

As control variables in our sample, three factors (i.e., investment opportunities, financial constraints and firm specifics) affect corporate cash holdings. We expect that investment opportunities and idiosyncratic risk are positively related to cash holdings and that firm size, leverage, and non-cash liquid assets are negatively related to cash holdings.

In the present paper, we have two predictions:

Hypothesis 1 : The relation between country-level governance and corporate cash holdings is positive.

Hypothesis 2 : Firms in the common-law countries have more cash holdings than those in the civil-law countries.

We use two regression models in our study (similar with Dittmar, Mahrt-Smith, and Servaes, 2003). First, we use the ordinary least-squares (OLS) regression to examine the effects of the factors to the cash holdings with whole samples and the two groups (i.e., the common-law and civil-law countries). Second, we use random effects regression to ensure that our findings persist after controlling for these interdependencies.

and the common law dummy variable as proxies for country-level governance, and the other variables are control variables. We also include industry dummies in our models.

In the end, to avoid possible spurious relationship on panel regressions and to increase credibility on regression coefficients, we use clustered robust standard errors model proposed by Petersen (2009) as robustness to check it.

We use the following models to test the predictions in the present study:

3. Results

3.1 Univariate analysis

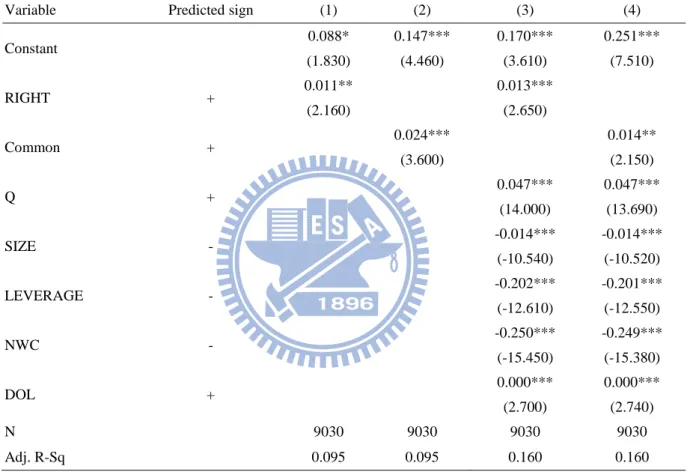

Table 4 presents the mean statistics and t-test of important variables such as RIGHT, LAW, Q, and SIZE, by groups of legal system.

The mean of RIGHT is 7.432 for common-law countries group, and the difference of RIGHT between common-law and civil-law countries group is statistically significant with P value less than 0.0001. We also find that the difference of LAW between common-law and civil-law countries group is statistically significant with P value. This is similar with previous studies that show firms in common-law countries have better country-level governance than those in civil-law countries (La Porta et al., 1998).

Next, the difference of Q and SIZE between common-law and civil-law countries group is also statistically significant with P value. This indicates that firms in common-law countries have more investment opportunities to pursue the corporate value than those in civil-law countries because large firms with lower financial constraints can raise funds easily without

1 , , 7 , 6 , 5 , 4 , 3 , 2 , 1 0 , t i t i t i t i t i t i t i t i t i Industry DOL NWC LEVERAGE SIZE Q RIGHT CASH

2 , , 7 , 6 , 5 , 4 , 3 , 2 , 1 0 , t i t i t i t i t i t i t i t i t i Industry DOL NWC LEVERAGE SIZE Q Common CASH Collins, Rozeff, and Dhaliwal, 1981).

Overall, the univariate statistics show that common-law countries have stronger country-level governance than do civil-law countries; therefore, their stockholders have higher shareholder rights, and firms in common-law countries have lower financial constraints. Hence, firms in common-law countries have more investment opportunities to pursue corporate value than those in civil-law countries.

Table 4 Whole sample firms t test of important variables by legal system

This table presents the mean statistics of important variables and tests the differences of important variables, such as RIGHT, LAW, Q, and SIZE, with t test between common-law and civil-law countries. The data consist of 9,030 firm-year observations (firms in common-law countries = 7,483; firms in civil-law countries = 1,547) for the period 2002–2008. The RIGHT is the index of shareholder rights. The LAW is the index of rule of law. Both RIGHT and LAW are collected from the IMD World Competitiveness Online, and the index is from 0 to 10 (best). The Q here is (market value of equity+book value of liability) divided by book value of total assets. The SIZE is natural logarithm of firms’ total assets. P value represents P values from t tests for difference in means with unequal variances. *, **, and *** indicate significance at 10%, 5%, and 1%, respectively.

Variables Total Common-law

countries

Civil-law

countries t test P value

Mean of RIGHT 7.338 7.432 6.881 -41.600*** <.0001

Mean of LAW 5.450 5.809 3.712 -111.710*** <.0001

Mean of Q 1.593 1.649 1.325 -21.420*** <.0001

Mean of SIZE 6.925 6.948 6.814 -2.290** 0.0222

N 9,030 7,483 1,547

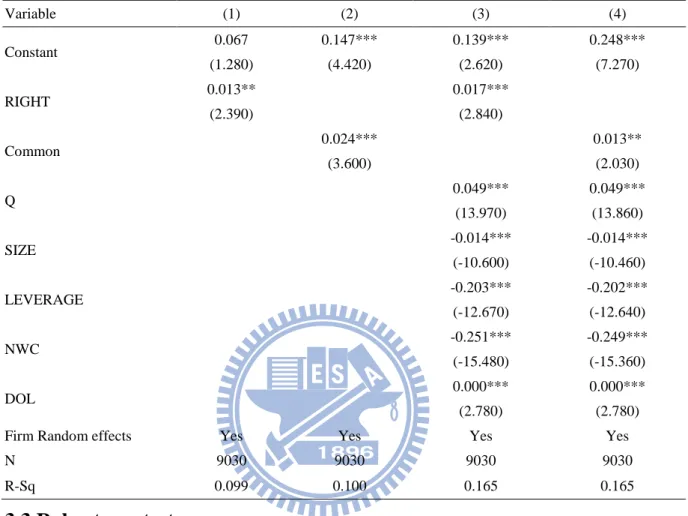

3.2 Explaining firm cash holdings

In the present paper, we use OLS regression and random effects regression to consider cross-sectional and time-series effects. The dependent variable in our models is CASH. The explanatory variables are RIGHT, and the common law dummy. The other variables, which have been shown to be statistically significant in explaining CASH in previous empirical studies, are control variables in our models.

Table 5 reports the OLS regression results. To avoid multicollinearity, we do not place these explanatory variables into the same model because the shareholder rights and the rule of law, as proxies for country-level governance, are highly correlated.

Model (1) in Table 5 contains only the level of the shareholder rights and industry dummies, defined at the two-digit SIC code level, as explanatory variables. Consistent with

our expectation, RIGHT is positively related to cash holdings. According to previous empirical studies, firms with weaker corporate governance structures have smaller cash reserves (Harford, Mansi, and Maxwell, 2008).

Model (2) in Table 5 also contains only the industry dummies and the common law dummy (Common), which is defined as 1 for common-law countries and 0 for civil-law countries, as explanatory variables. The coefficient of Common is significantly positive to cash holdings at 0.024, which indicates that the common-law countries hold more cash holdings than do civil-law countries. This is consistent with previous studies that firms with better country-level governance reduce the sensitivity between cash holdings and agency problem because the stockholders of firms with better country-level governance have more shareholder rights to monitor managers and to avoid agency problem between managers and shareholders (Hillier et al., 2011).

Next, Models (3) and (4) repeat the previous analysis; however, they include another three factors (i.e., investment opportunities, financial constraints and firm-specific characteristics) as control variables in models. The coefficient on RIGHT increases from 0.011 in model (1) to 0.013 in model (3). In addition, all our control variables are significant and have the expected sign. Thus, controlling for industry alone is not sufficient to capture the dispersion in the cash ratio.

Consistent with previous evidence, small firms with higher investment opportunities have higher information asymmetry than large firms; thus, they have more cash holdings than large firms (Bates, Kahle, and Stulz, 2009; Dittmar, Mahrt-Smith, and Servaes, 2003; Opler et al., 1999).

Moreover, because leverage (LEVERAGE) and non-cash liquid assets (NWC) are substitutes for holding high levels of cash, firms can use them when they have cash shortfalls. Hence, LEVERAGE and NWC are significantly negatively related to cash holdings (Baskin,

idiosyncratic risk as proxy for firm specifics in our samples. Consistent with previous evidence, firms with higher idiosyncratic risk are expected to hold more cash to avoid passing up the valuable investment opportunities (Minton and Schrand, 1999; Ferreira and Vilela, 2004).

Table 5 Pooled cross-country regression

This table reports the OLS regression results of explanatory variables, such as RIGHT and the common law dummy, on CASH for the period 2002–2008. All regressions include industry dummy variables, defined at the two-digit SIC code level. Next, we divided our sample into two groups: common-law and civil-law countries. *, **, and *** indicate significance at 10%, 5%, and 1%, respectively. The values of t statistics are in parentheses.

Variable Predicted sign (1) (2) (3) (4)

Constant 0.088* 0.147*** 0.170*** 0.251*** (1.830) (4.460) (3.610) (7.510) RIGHT + 0.011** 0.013*** (2.160) (2.650) Common + 0.024*** 0.014** (3.600) (2.150) Q + 0.047*** 0.047*** (14.000) (13.690) SIZE - -0.014*** -0.014*** (-10.540) (-10.520) LEVERAGE - -0.202*** -0.201*** (-12.610) (-12.550) NWC - -0.250*** -0.249*** (-15.450) (-15.380) DOL + 0.000*** 0.000*** (2.700) (2.740) N 9030 9030 9030 9030 Adj. R-Sq 0.095 0.095 0.160 0.160

Because the OLS regression may have interdependencies of observations within an industry and within a country, we use random effects regression to make sure that our findings persist after controlling for these independencies (Wooldridge, 2002, p. 169).

The results of this analysis are reported in Table 6 using the same structure in Table 5. After examination, we find that the coefficients of our explanatory variables, such as RIGHT and the common law dummy, remain highly significant in all models. In addition, the coefficients on the control variables are also similar in magnitude and significance to those reported in Table 5.

Table 6 Pooled cross-country regression with country and industry random effects

This table reports random effects regression results of explanatory variables, such as RIGHT and the common law dummy, on CASH for the period 2002–2008. All regressions include industry dummy variables, defined at the two-digit SIC code level. Next, we divide our sample into two groups: common-law and civil-law countries. *, **, and *** indicate significance at 10%, 5%, and 1%, respectively. The values of t statistics are in parentheses. Variable (1) (2) (3) (4) Constant 0.067 0.147*** 0.139*** 0.248*** (1.280) (4.420) (2.620) (7.270) RIGHT 0.013** 0.017*** (2.390) (2.840) Common 0.024*** 0.013** (3.600) (2.030) Q 0.049*** 0.049*** (13.970) (13.860) SIZE -0.014*** -0.014*** (-10.600) (-10.460) LEVERAGE -0.203*** -0.202*** (-12.670) (-12.640) NWC -0.251*** -0.249*** (-15.480) (-15.360) DOL 0.000*** 0.000*** (2.780) (2.780)

Firm Random effects Yes Yes Yes Yes

N 9030 9030 9030 9030

R-Sq 0.099 0.100 0.165 0.165

3.3 Robustness tests

In many situations, data are observed in clusters, such that observations within a cluster are correlated, whereas observations between clusters are uncorrelated; these are so-called cluster-correlated data. A major statistical problem with cluster-correlated data arises from intracluster correlation or the potential for clustermates to respond similarly. This phenomenon is often referred to as overdispersion or extravariation in estimated statistics beyond what is expected under independence (Williams, 2000).

To avoid possible spurious relationship on panel regressions and to increase credibility on regression coefficients, we use clustered robust standard errors model proposed by Petersen (2009) as robustness to check it.

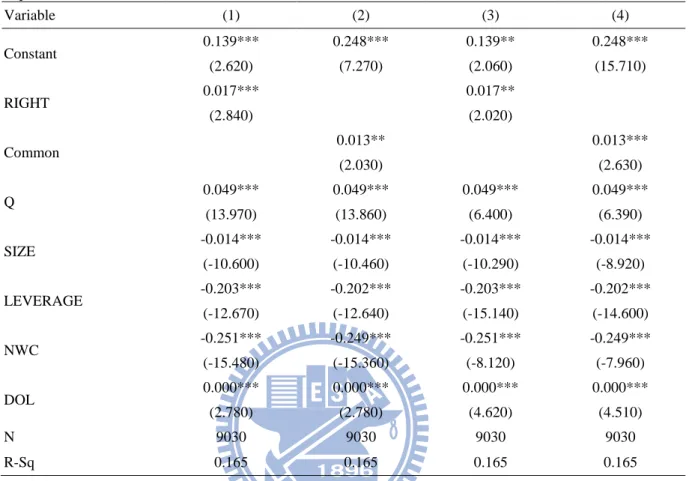

Table 7 Robustness tests of pooled cross-country regression

This table reports the original panel regressions and the panel results adjusted by clustered robust standard errors as robustness check. Models (1) and (2) are random effects models. Models (3) and (4) are robustness tests after adjustments. *, **, and *** indicate significance at 10%, 5%, and 1%, respectively. The values of t statistics are in parentheses. Variable (1) (2) (3) (4) Constant 0.139*** 0.248*** 0.139** 0.248*** (2.620) (7.270) (2.060) (15.710) RIGHT 0.017*** 0.017** (2.840) (2.020) Common 0.013** 0.013*** (2.030) (2.630) Q 0.049*** 0.049*** 0.049*** 0.049*** (13.970) (13.860) (6.400) (6.390) SIZE -0.014*** -0.014*** -0.014*** -0.014*** (-10.600) (-10.460) (-10.290) (-8.920) LEVERAGE -0.203*** -0.202*** -0.203*** -0.202*** (-12.670) (-12.640) (-15.140) (-14.600) NWC -0.251*** -0.249*** -0.251*** -0.249*** (-15.480) (-15.360) (-8.120) (-7.960) DOL 0.000*** 0.000*** 0.000*** 0.000*** (2.780) (2.780) (4.620) (4.510) N 9030 9030 9030 9030 R-Sq 0.165 0.165 0.165 0.165

Table 7 reports the original panel regressions and the panel results adjusted by clustered robust standard errors as robustness check. Models (1) and (2) are random effects models. Models (3) and (4) are robustness tests after adjustments.

After adjustments, we find that most estimating errors on panel regression coefficient estimates in Table 7 are decreasing; however, the degree of decrease in the panel regression coefficient estimates is inconsistent. Empirical results are consistent with the original before adjustments.

4. Conclusion

This study has investigated the empirical determinants of corporate cash holdings among the US, the UK, Germany, and France. According to previous empirical studies, four main factors affect corporate cash holdings: country-level governance, investment opportunities,

financial constraints, and firm specifics. In the present paper, we divide our sample into two groups by different national legal systems [i.e., the common-law countries (United States and United Kingdom) and the civil-law countries (Germany and France)], and focus on the effect of the country-level governance to corporate cash holdings.

We expect that firms in the common-law countries have more cash holdings than those in the civil-law countries for two reasons. First, because the stockholders of firms in the common-law countries have high shareholder rights to monitor managers and to reduce agency problem between managers and stockholders, firms can hold more cash holdings for their precautionary motives. Second, firms in the common-law countries with better legal protection to investors have low financial constraints; thus, they have an opportunity to earn more cash without giving up any good investment opportunities that are beneficial.

Our research reveals that country-level governance is significantly positive to corporate cash holdings, and the common-law countries with better country-level governance have more cash holdings than those in the civil-law countries with weaker country-level governance. Furthermore, to avoid possible spurious relationship on panel regressions and to increase credibility on regression coefficients, we use clustered robust standard errors model proposed by Petersen (2009) as robustness to check it. After adjustment, empirical results stay close to the original before adjustments, and improve the explanatory power of dependent variables.

Overall, our results reveal that higher country-level governance can decrease sensitivity between agency problem and corporate cash holdings. Therefore, firms should establish good corporate governance structure to reduce agency problem and financial constraints, so they can have better growth opportunities to enhance their corporate values.

Reference

[1] Aguilera, R. V. and Jackson, G., "The cross-national diversity of corporate governance: Dimensions and determinants", The Academy of Management Review, 28 (3), pp.

447-465, 2003.

[2] Baskin, J., "Corporate liquidity in games of monopoly power", Review of Economics and Statistics, 69, pp. 312-319, 1987.

[3] Bates, T. W., Kahle, K. M., and Stulz, R. M., "Why do U.S. firms hold so much more cash than they used to? ", Journal of Finance, 64 (5), pp. 1985-2021, October 2009. [4] Becht, M., and R el, A., "Blockholding in Europe: An international comparison",

European Economic Review, 43, pp. 10-49, 1999.

[5] Bergl f, E., "Corporate control and capital structure: Essays on property rights and financial contracts", Stockholm: IIB Institute of International Business, 1991.

[6] Berle, A. A., and Means, G. C., "The modern corporation and private property", New York: Macmillan, 1993.

[7] Brennan, M., Hughes, P., "Stock prices and the supply of information", Journal of Finance, 46, pp. 1665-1691, 1991.

[8] Collins, D., Rozeff, M., Dhaliwal, D., "The economic determinants of the market reaction to proposed mandatory accounting changes in the oil and gas industry", Journal of Accounting and Economics, 3, pp. 37-71, 1981.

[9] Core, J. E., Holthausen, R. W., and Larcker, D. F., "Corporate governance, chief executive officer compensation, and firm performance", Journal of Financial Economics, 51, pp. 371-406, 1999.

[10] Dittmar, A., and Mahrt-Smith, J., "Corporate governance and the value of cash holdings", Journal of Financial Economics, 83 (3), pp. 599-634, 2007.

[11] Dittmar, A., Mahrt-Smith, J., and Servaes, H., "International corporate governance and corporate cash holdings", Journal of Financial and Quantitative Analysis, 38, pp. 111-133, 2003.

[12] Faulkender, M., and Wang, R., "Corporate financial policy and the value of cash", The Journal of Finance, 61 (4), pp.1957-1990, 2006.

[13] Ferreira, M. A., and Vilela, A. S., "Why do firms hold cash? Evidence from EMU countries", European Financial Management, 10 (2), pp. 295-319, 2004.

[14] Hall, P. A. and Soskice, D., "Varieties of capitalism: The institutional foundations of comparative advantage", Oxford: Oxford University Press, 2001.

[15] Harford, J., Mansi, S. A., and Maxwell, W. F., "Corporate governance and firm cash holdings in the US", Journal of Financial Economics, 87, pp. 535-555, 2008.

[16] Hillier, D., Pindado, J., DeQueiroz, V., and DeLaTorre, C., "The impact of country-level corporate governance on research and development", Journal of International Business Studies, 42, pp. 76-98, 2011.

[17] Jensen, M. C., "Agency costs of free cash flow, corporate finance and takeovers", American Economic Review, 76, pp. 323-329, 1986.

[18] John, T. A., "Accounting measures of corporate liquidity, leverage, and costs of financial distress", Financial Management, 22, pp. 91-100, 1993.

[19] Kalcheva, I., and Lins, K. V., "International evidence on cash holdings and expected managerial agency problems", Review of Financial Studies, 20 (4), pp. 1087-1112, 2007.

[20] Kim, C.-S., Mauer, D. C., Sherman, A. E., "The determinants of corporate liquidity: Theory and evidence", Journal of Financial and Quantitative Analysis, 33, pp. 335-359, 1998.

[21] King, R. G., and Levine, R., "Finance and Growth: Schumpeter might be right", The Quarterly Journal of Economics, 108 (3), pp. 717-737, 1993.

[22] La Porta, R., Lopez-de-Silanes, F., Shleifer, A., and Vishny, R. W., "Law and finance", Journal of Political Economy, 106, pp. 1113-1155, 1998.

[23] La Porta, R., Lopez-de-Silanes, F., Shleifer, A., and Vishny, R., "Investor protection and corporate valuation", The Journal of Finance, 57, pp. 1147-1170, 2002.

American Economic Review, 88 (3), pp. 537-558, 1998.

[25] Mikkelson, W., and Partch, M., "Do persistent large cash reserves hinder

performance?", Journal of Financial and Quantitative Analysis, 38, pp. 275-294, 2003. [26] Minton, B. and Schrand, C., "The impact of cash flow volatility on discretionary

investment and the costs of debt and equity financing", Journal of Financial Economics, 54, pp. 423-460, 1999.

[27] Myers, S., and Majluf, N., "Corporate financing and investment decisions when firms have information that investors do not have", Journal of Financial Economics, 13, pp. 187-221, 1984.

[28] Opler, T., Pinkowitz, L., Stulz, R., and Williamson, R., "The determinants and

implications of corporate cash holdings", Journal of Financial Economics, 52, pp. 3-46, 1999.

[29] Ozkan, A., and Ozkan, N., "Corporate cash holdings: An empirical investigation of UK companies", Journal of Banking & Finance, 28, pp. 2103-2134, 2004.

[30] Petersen, M. A., "Estimating standard errors in finance panel data sets: Comparing approaches", Review of Financial Studies, 22(1), pp. 435-480, 2009.

[31] Pinkowitz, L., and Williamson, R., "What is a dollar worth? The market value of cash holdings", Working paper, Georgetown University, 2004.

[32] Pinkowitz, L., Stulz, R., and Williamson, R., "Do firms in countries with poor

protection of investor rights hold more cash? ", Journal of Finance, 61, pp. 2725-2751, 2006.

[33] Rajan, R. G., and Zingales, L., "Financial dependence and growth", The American Economic Review, 88 (3), pp. 559-586, 1998.

[34] Shleifer, A., and Vishny, R. W., "A survey of corporate governance", The Journal of Finance, 52 (2), pp. 737-783, 1997.

Biometrics, 56, pp. 645-646, 2000.

[36] Wooldridge, J., "Econometric Analysis of Cross Section and Panel Data", The MIT Press, Cambridge, MA, 2002.

[37] Yoshimori, M., "Whose company is it? The concept of the corporation in Japan and the West", Long Range Planning, 28 (4), pp. 33-44, 1995.