CHAPTER 1 INTRODUCTION

1.1 THE TELECOM INDUSTRY HAS BEEN EMERGING

The telecommunications or communications industry is one of the most important business sectors for nations and regions. In the past ten years, many countries have to open their communications market and loosen the limit of competition. Many studies in the literature of the communications industry have discussed about liberalization and localization of telecommunications, such as the influences of liberalization and privatisation (Bortolotti et al. 2002; Zhang 2002; Makhaya and Roberts 2003; McDowell and Lee 2003; Mureithi 2003; Tang and Lee 2003). Their target is to know whether the telecom market will be more efficient if the operator is a corporation.

Because of limited spectrum resources, all economies in the world have tried their best to find out “how to divide spectrums and what kind of policy is the most beneficial to divide spectrums,” especially by efficiently controlling and allotting 3G (Third Generation Standard of Cellular Phones). How to charge license fees is also an important issue- for example, allocating spectrum rights by auctions. However, in the topic of resource allotment of spectrums, there is a debate over whether or not there should be a law limiting the amount of operators and mobile communications enterprises, because of serious competition in the Euro-American markets (Choi et al. 2001; Editorial 2003; Lee 2003). Other research topics include the policy of mutual network communications that look at the effect of competition and cooperation within communications technology. Some even wonder how to calculate the economic benefits of communications policies and laws (Yan 2001; Song and Kim 2001; Berra 2003).

According to the literature, resource allotment of spectrums decides the number of wireless telecom operators, and the number of wireless telecom operators affects the degree of competition. Moreover, the policy of wireless spectrums and standards could be a tool to promote the domestic telecom equipment industry. At the same time, a healthy domestic telecom equipment industry can support government to set up its communication standards. Therefore, allocating spectrum rights, competition of telecom operators, and the telecom equipment industry all affect each other. Based on the characteristic of the communications industry, we should observe the industry ecosystem as a whole when we discuss related issues.

(1) Liberalization and localization of telecommunications: Discussions include the influences of liberalization and privatisation (Bortolotti and D’Souza 2002; Zhang 2002; Trillas 2002; Tang and Lee 2003; McDowell and Lee 2003; Hazlett 2003; Makhaya and Roberts 2003; Chang, Koski and Majumdar 2003; Mureithi 2003).

(2) Resource allotment of spectrums: Because of limited spectrum resources, all economies in the world have tried their best to find out the rule of the spectrum allocation, especially by efficiently controlling and allotting 3G (Third Generation Standard of Cellular Phones). How to charge license fees is also an important issue- for example, allocating spectrum rights by auctions. Moreover, there is still a debate over whether or not there should be a law limiting the amount of operators and mobile communications enterprises, because of serious competition in the Euro-American markets (Lee 2003; Editorial 2003; Bauer 2003; Choi and Lee 2001; Ure 2003).

(3) Others: The policy of mutual network communications looks at how to effect competition and cooperation within communications technology. Some are even wondering how to calculate the economic benefits of communications policies and laws (Yan 2001; Song and Kim 2001; Kim and Litman 1999; Zhang 2002; Berra 2003).

We can see that research covering the communications development of developing countries is still deficient. The literature focuses on the telephone telecommunications market, exchange machine, telecommunications liberalism, and frequency charts, because collecting data is difficult in developing countries such as China (Zhang 2002; Tan 2002). As for the cellular phone industry’s quick rise, there are not many related research papers. As a result, analyzing the influence of the communications industrial policy of developing countries on its domestic cellular phone manufacturing industry is quite attractive as the numbers show.

1.2 THE CELLULAR PHONE HAS BECOME MAJOR PRODUCT IN THE

HIGH TECH INDUSTRY

The mobile communications industry is one of the most important business sectors for nations and regions. The cellular phone and related product shipments and values have been expanded rapidly. This industry is effectively controlled through many countries’ industrial policy and many governments want to build up their domestic cellular phone industries through policy support.

the 2005 global quantity of cellular phone shipments reached over 700 million. Their production value surpassed personal computers to become the technology industry’s leader. That is a good chance for lately industrialized economies and industrial latecomers to catch up the leader of the technology industry. The communications field is also related to military installations, prompting many countries to support their domestic cellular phone manufacturers through their industrial policy.

As cellular phone and related product shipments and values have been expanded rapidly, communication industries need to coordinate with the communication standards that are related with local markets. Many governments as a result want to build up their domestic cellular phone industries through policy support. For example, the South Korean government combines policy subsidisation and technology acquisitions from Qualcomm to successfully support the developing/extension of its cellular phone manufacturers, Samsung, LG, and Pantech, etc.

Another case, in terms of the MII (Ministry of Information Industry) data, China is the most populous nation in the world at 1.3 billion people. Its cellular phone users numbered over 350 million at the end of 2005, making China the biggest cellular phone market in the world. When the global cellular phone market was just maturing years ago, China’s cellular phone users only took up 20% of their domestic market. China’s government also started to establish a policy to expedite competition for its domestic cellular phone manufacturers starting from 1999. Foreign cellular phone suppliers as a result began to face limitations by China’s policies when they entered China market.

CHAPTER 2 LITERATURE REVIEW

2.1 INDUSTRIAL POLICY LITERATURE REVIEW

On the manufacturing side, in recent decades, a new kind of North-South trade has begun to emerge driven by cheap labour and land cost in the South. The production of more and more basic goods and services, even IT product are being transferred from the high-wage economies of the North to the low-wage economies of the South, and the South countries take the opportunity to build up its manufacturing industries. In addition, the companies of the South gain knowledge of the manufacturing, and they may begin marketing their own brands (Prahalad and Hamel 1990). That is why the South government often establishes the protection policy for domestic industries (Krugman 1979).

As some economic theories show, if the South countries want to build up strong manufacturing industries in the long run, the South government should give the intermediate goods manufacturers investment price subsides or tax credit to enhance capacities and qualities in end products (Brander and Spencer 1985). Organizations are increasingly turning to outsourcing in an attempt to enhance their competitiveness due to globalisation, especially in IT industry. Through outsourcing, manufacturing costs as well as investment in plants and equipments can be reduced (Bettiset al. 1992). Most of EMS (Electronics Manufacturing Service)/ODMs (Original Design Manufacturing) started to move production line to lower labor cost area, such as China and Malaysia.

On the marketing side, researchers also indicated that the typically international industry has some characteristics such as economy of scale, market similarity, comparative advantage, and absence of regulatory restraints (Lessard 2003). In the ICT industry, due to globalisation and the trend in world trade, cellular phones like PCs, have become the popular product sold around the world. Major cellular phone makers, Nokia and Motorola, sell their phones in most of countries with advantage of economies of scale and a firm's comparative advantages.

That’s why although the government of developing economies wants to support its domestic industry by policy, the effect may be a question. In order to compete with foreign leading companies, domestic firms of developing economies should take advantage such as economy of scale or market niche expect policy protection. If the government wants to build up the domestic manufacturing ability in telecom industry, it cannot ignore this trend. However, this issue has been theoretically discussed without empirical evidence. Due to little existing empirical work about the policy outcomes of manufacturing, this study seeks to

cellular phone manufacturing ability, and firms’ development strategy in developing economies.

2.2 THE DIFFERENCE BETWEEN THE PC AND CELLULAR PHONE

INDUSTRY CHAIN

Figure 1 shows the difference between the PC and cellular phone industry chains. In the PC industry, there is the Wintel platform and Internet Protocol. The software firm Microsoft and the CPU firm Intel have created industrial standards to let third-party firms follow up. PC brand names and manufacturing companies show less difference in product innovations, and so any latecomer can easily catch due to low inside knowledge.

Figure 1. Comparing the PC and cellular phone industry chains

In contrast with the PC industry chain, the communication industries need to coordinate their standards related with the local markets. Therefore, European and American innovative products and applications often lack common standards due to insufficient interaction with carriers. This is why most famous cellular phone companies develop cellular phones,

Composers

Composers Content AggregatorsContent Aggregators Digital ComposersDigital Composers

Content Providers

Content Providers

Composers

Composers Content AggregatorsContent Aggregators Digital ComposersDigital Composers

Content Providers Content Providers Service Operators Service Operators Network Operators Network Operators Mobile Operators Mobile Operators

Phone Number Channel Phone Number Channel

Infrastructure Manufacturers Infrastructure Manufacturers Platform Solutions Platform Solutions Platform Solutions Platform Solutions Base band/RF Base band/RF Software Platform Software Platform Customised UI/AP Customised UI/AP

Platform Solution Vendors

Platform Solution Vendors

Base band/RF Base band/RF Software Platform Software Platform Customised UI/AP Customised UI/AP

Platform Solution Vendors

Platform Solution Vendors

Consumers Consumers Component Vendors Component Vendors Mechanic Mechanic LCM LCM Passive Passive Function Function Component Vendors Component Vendors Mechanic Mechanic LCM LCM Passive Passive Function

Function Mobile Phone ManufacturersMobile Phone Manufacturers Mobile Phone Brand Names Mobile Phone Brand Names Mobile Phone Manufacturers Mobile Phone Manufacturers

Mobile Phone Brand Names Mobile Phone Brand Names

Aftermarket Aftermarket

Protocol Standard

Protocol Standard

Mobile Phone Vendors

Mobile Phone Vendors

Content Providers

Content Providers

The Third Party Software and Content Providers The Third Party Software

and Content Providers

Network Operators Network Operators Service Operators Service Operators Network Operators Network Operators Service Operators Service Operators Intel CPU Intel CPU PC Manufacturers PC Manufacturers Windows OS Windows OS Wintel

WintelPlatformPlatform

PC Brand Names PC Brand Names Internet Operators Internet Operators Internet Protocol Internet Protocol

PC and Internet Industry Chain

PC and Internet Industry Chain

Mobile Phone Industry Chain

infrastructure equipments, and management systems at the same time, such as Nokia, Motorola, Ericsson, Siemens, and Alcatel.

With a lack of industrial standards, every company in the cellular phone industry that wants to create a new service has to take care of all operational stages. This industry ecosystem appears like a vertical integration structure and hence the cost-down issue is not the priority here. The market share seldom fluctuates extremely unless the communication protocol is revised.

On the other hand, mobile services move from voice to data ceaselessly. Package and digital services will become the future trend in the third generation of the cellular phone. Table 1 shows the major global cellular phone firms’ platform architectures. We find that most major cellular phone companies have their independent platforms, protocol stacks, and developer programs. Cellular phone manufacturers are not as similar as PC companies. They are used to researching and developing the technology and products by themselves, which seems to avoid the outsourcing trend.

In order to reduce cost, companies outsource some businesses to other companies. However, they also need to collect the related information, negotiate contracts, maintain relationships, and supervise ODMs. Therefore, outsourcing does not mean better qualify. It depends on the transaction cost and the outsourcing benefit and which one is bigger (Williamson 1979, 1981).

In the cellular phone industry, due to every telecom operators having a large enough market potential, telecom equipment makers can support by themselves if they get enough operator customers. Therefore, because of the transaction cost, it is not necessary to outsource their business unless under special conditions.

Table 1. Global major cellular phone firms’ platform architectures

Hardware Platform Protocol Stack Software Platform Developer Program

Nokia Nokia, TI Nokia Symbian Forum Nokia

Motorola Freescale (Motorola), TI

Motorola Linux, Symbian,

Microsoft

MOTOCODER developer program

Samsung Agere, Philips,

Infineon

Optimacy, Philips Palm, Symbian,

Microsoft

Samsung developer’s club

LG ADI, TI TTP com.,Condat Symbian, Microsoft Developer Portal

SEMC EMP Ericsson Symbian Sony Ericsson

Developer World

Siemens Infineon Comneon Symbian N/A

Figure 2 shows the difference between cellular phone and PC makers’ positions. Cellular phone makers will be able to enhance their competition by many ways in the future. For example, they can build up the applications and terminal platforms, and make sure the two can connect with each other. They also can support the content provider or become a developer to promote digital services.

Figure 2. The difference between cellular phone and PC makers’ positions

Based on the platform structure, in the global cellular phone industry there is a clear trend of a shortening product life cycle, and cellular phone OEMs are shifting their strategy to ‘lower volume, higher mix’ in order to use the approach of a lot of models. For example, Motorola launched over 50 new models and Samsung even launched over 150 new ones in 2004 (Hu and Hsu 2007). As a result, if someone can keep the end user demand, it will win the market. That is why the cellular phone market is highly competitive, but Nokia, Samsung, Sony Ericsson, and Motorola still have good profits.

2.3 KEY ISSUES OF THE DEVELOPMENT IN THE CELLULAR PHONE

INDUSTRY

Following second-generation cellular phone technology - e.g., GSM (Global System for Mobile Communication) - the cellular phone industry is resembling consumer electronics

N e tw o r k M a n a g e m e n t S y s te m In te g r a tio n

N e tw o r k M a n a g e m e n t S y s te m In te g r a tio n

A p p lic a tio n P la tfo r m In te g r a tio n

A p p lic a tio n P la tfo r m In te g r a tio n

C e llu la r P h o n e P la tfo r m I n te g r a tio n

C e llu la r P h o n e P la tfo r m I n te g r a tio n

M o b ile O p e r a t o r s M o b ile O p e r a t o r s S o ftw a r e P la t fo r m S o ftw a r e P la t fo r m H a r d w a r e P la tfo r mH a r d w a r e P la tfo r m C o n te n t F o r m a t a n d lite r a r y p r o p e r t y C o n te n t F o r m a t a n d lite r a r y p r o p e r t y C o n t e n t D e v e lo p e r s C o n t e n t D e v e lo p e r s D e s ig n a n d M a n u fa c tu r in g D e s ig n a n d M a n u fa c tu r in g T e r m in a l V e n d o r s T e r m in a l V e n d o r s P e r s o n a l C o m p u te r P la tfo r m In te g r a tio n P e r s o n a l C o m p u te r P la tfo r m In te g r a tio n D e s ig n a n d M a n u fa c tu r in g D e s ig n a n d M a n u fa c tu r in g T e r m in a l V e n d o r s T e r m in a l V e n d o r s W in te l P la t fo r m W in te l P la t fo r m M o b ile P h o n e M a k e r s M o b ile P h o n e M a k e r s’’P o s it io n sP o s it io n s P C M a k e r s P C M a k e r s’’P o s it io n sP o s it io n s

products by undergoing dramatic changes fuelled by rapid technological development, innovative applications, and more integrated functions. The cellular phone is the most representative of all 3C (computer, communication, and consumer) products. How have domestic cellular phone firms in the lately industrialised economies achieved success? One of the answers may be in their innovation ability. Fan (2006) studies the innovation capability development of four domestic Chinese firms - Huawei, ZTE, DTT, and GDT. Innovation capability and self-developed technologies are the key areas for Chinese firms to catch up with multinational corporations. It is found that domestic firms should focus on in-house R&D development in order to build their innovation capability, supplemented by external alliances.

Latecomers sometimes need new technology from outside firms. Hence, researchers also mentioned that firms in developing counties source their formal or informal technology from outside firms. Thus, their technological innovations have progressed by acquiring mature technology from advanced countries and at the same time have increased the absorptive capacity of these technologies (Gil, Bong and Lee 2003; Kim 1997; Kim 1998; Lee, Bae and Lee 1994). Moreover, the empirical results show that firms prefer in-house R&D strategy to technology purchasing. The firm often uses an inertial R&D strategy that keeps up with historical choice patterns (Cho and Yu 2000). This means that governments of developing countries need to do something to help firms acquire new technology or lower developing costs.

Government policy as a result is another important issue. According to the literature, if a government wants to build up a strong domestic industry in the long term, researchers suggest that it should give intermediate goods manufacturers investment subsidies or tax credits to enhance the capacities and qualities of the final goods (Brander and Spencer 1985). This is a major reason why South Korea’s manufacturing industry matured up to 1999 (Hitomi 2002).

Aside from enhancing R&D intensity, increasing R&D efficiency is also a way to increase innovative capability. With increasing pressure to create and sustain competitive advantages through technological innovation, technology-based firms increasingly depend on the efficient management of their R&D activities (Bone and Saxon 2000).

2.4 SOUTH KOREAN FIRMS HAVE CATCHED UP IN THE CELLULAR

PHONE INDUSTRY

There is still not a common consensus about how to be successful in the cellular industry. In the early stages, South Korean companies were the same as most latecomers, improving on

strengths, and competing on the basis of high quality and low cost. Even Samsung at one time believed that as long as international markets for low-cost, high technology hardware continued to expand, then they could continue to repeat the cycle of being behind the frontier and play catch up in innovation as they had done for many years in mobile telephony. In this scenario, most South Korean firms have yet to achieve international status, particularly in higher prices, more complex products and systems, capital goods, and services (Hobday, Rush and Bessant 2004).

South Korean cellular phone firms now are able to lower the risk and cost of new market creation, R&D expenses, and innovative product development. At the same time, they have improved in R&D efficiency. Samsung and LG lead in new product creation, especially in higher prices and design-intensive products, having surpassed most American, Japanese, and European firms in the cellular phone industry. South Korean cellular phone manufacturers have succeeded in catching up and leapfrogging, including global market shares, export values and company brand names.

Many research papers have provided useful insights and lessons to explain how South Korean firms have faced the changing global environment and accumulated relatively advanced technological and manufacturing capabilities within a short period. The paper also explains the technological capability development process and creates a model for technological and market “catching-up”. In this model, technological capability is determined as a function of both technological effort and the existing knowledge base (Lee and Lim 2001; Hitomi 2002).

Most of the previous contributions to this paper’s subject lack specialised analysis to South Korea’s cellular phone industry. This is especially for the subject of product innovative, since these studies rely a lot on standardised products or mass production of scale economies such as DRAM, Flash, and LCD. The cellular phone industry is a very special object of technology management, because of the integration of computer, consumer, and communications products.

Rapid technological innovations and increasing market competition have created the pressure to develop and introduce new products. To be successful, companies must provide innovative solutions using effective marketing activities, more demand forecasting and an increase in market attractiveness due to environmental changes and government policy (Ahn, Kim and Lee 2005). As the requisite capability complexity for participation in mobile telecommunications has increased, the complexity and extent of vertical and horizontal disintegration in the industry has increased. Where firms have been able to internalise all of their design, production and distribution capabilities in the past, the changing nature of

products has made this business mode impossible (Rice and Galvin 2006).

2.5 TAIWAN DEVELOPED ITS CELLULAR PHONE INDUSTRY THROUGH

RECEIVING OUTSOURCING ORDERS

Organizations in the North are also increasingly turning to outsourcing in an attempt to enhance their competitiveness due to globalization, especially in the IT (Information Technology) industry. Through outsourcing, manufacturing costs as well as investment in plants and equipments can be reduced (Bettis et al. 1992). Taiwan’s companies have taken this chance to set up their own outsourcing industry, especially in IT manufacturing. Beginning in the early 1970s, computers and the related information industry at first had only a few businesses assembling or copying others’ products. After two decades, companies’ technology developments had fostered fast-paced industrial growth. This field now forms the largest export industry in Taiwan, with Taiwan now having a world-class computer industry. Moreover, the industry enjoys more than 80% of the global market share for monitors, motherboards, keyboards, mouse, and scanners. Aside from computers, many Taiwanese companies receive outsourcing orders for consumer electronics and communication products, including DVD players, digital cameras, modems and so on (MIC 2005).

There are many factors behind the success of Taiwan’s computer industry. In addition to domestic manufacturers’ efforts, industrial policy, government-support R&D institutes, international technology transfers, foreign investments, and foreign purchases have all played roles in developing Taiwan’s computer industry (Chang et al. 1999). During this period, the ITRI (Industrial Technology Research Institute) has had an important role in promoting Taiwan’s companies’ R&D ability (Mathews 2002; Jan and Chen 2006; Chu et al. 2006).

It seems strange that Taiwan’s IT manufacturing industry has not been so successful in cellular phones, in spite of its dominant market shares in most of the computer, consumer, and communications (3C) products. For instance, Taiwan’s notebook PC industry started around 1990 and matured by the end of the 1990s. Its development background is similar to Taiwan’s cellular phone industry, but there is a big difference between their growing curves. The cellular phone industry must be a very special object of technology management.

Most previous contributions to this paper’s subject lack a specialized analysis on Taiwan’s cellular phone industry. This is especially so for the subject of product innovation, since these studies rely a lot on standardized products or mass production of scale economies such as PC, DRAM, Flash, and LCD. South Korea’s memory industry, and Taiwan’s PC and

More and more lately industrialized economies and researchers have recently turned their eyes toward non-standard products such as the semiconductor and cellular phone end product industries, because these industries have been soaring. For instance, Taiwan’s wafer foundries have selected the agile strategy to adapt changes in the semiconductor industry. It is a very different strategy compared with the down stream EMS industry that just emphasizes the scale of economies (DeCarolis and Deeds 1999). South Korea’s cellular phone industry has strengthened its R&D efficiency and has a high integrated industry chain. China’s cellular phone industry is catching up through its domestic market strength and industrial policy protection (Lin et al. 2006).

In the early stages, Taiwan’s cellular phone companies were the same as its PC companies, improving on existing product design, exploiting their cost-down ability, and focusing on their process strengths. Before 2000, Taiwan’s cellular phone industry still had not broken through the bottleneck and shipments were only 2.2 million units in 1999 (MIC 2005). Some of Taiwan’s cellular phone companies started to try new strategies and innovative activities to hold onto business opportunities. Right now there are three main Taiwanese cellular phone ODMs, Arima Communication, HTC, and Compal Communication, and three brand name companies, BenQ-Siemens, OKWAP, and DBTEL.

Hence, how did domestic cellular phone firms in the lately industrialized economies achieve success? Because of the characteristic of the communications industry, how can one enhance the competition of the market and expand the market size? How does the government use its policy to promote the domestic industry by the local market? How do domestic cellular phones or base station firms in the lately industrialized economies achieve success? All of these issues are important for latecomers.

We can learn from East Asian developing economies’ experiences by reviewing the chronological development, industry supply chain, and innovation process in the cellular phone industry of this area. China’s cellular phone users numbered over 400 million at the end of 2006, making China the biggest cellular phone market in the world. The lessons of China’s experience are very valuable. This paper also wants to discuss the R&D activities of Taiwan and Korea’s mobile industry and try to find the development pattern. This paper as such is organized as follows: In order to review the chronological development, industry supply chain, and innovation process of East Asian cellular phone industry, we break down the subject into details and examine the know-how of the local firms.

CHAPTER 3 RESEARCH DESIGN

3.1 VARIABLES AND DEFINITIONS

The research variables are defined as follows:(1) The product type definition (product mix):

In China the official definition of a cellular phone includes the standard system of in GSM, GPRS (general packet radio service), and CDMA (code division multiple access, including IS95A/B, CDMA2000 1X), etc. However, PHS (Personal Handy Phone System) is not included since PHS is considered to be a wireless fixed-line phone by Chinese authorities.

(2) Domestic manufacturers: Chinese makers hold total market share above 50%, including individual proprietorships and joint ventures. Dbtel and Inventec (OKWAP) are viewed as Taiwanese brand manufacturers.

(3) The shipment type definition (form factor):

(3.1) Full System: All components are already surface mounted on the printed circuit board. After assembling the mechanism components, the company takes delivery of goods to the customers who then use the product.

(3.2) Semi Knock Down (SKD): All components are already surface mounted on the printed circuit board. The goods are delivered together with the mechanism components to the customers, and the firm completes the simple assembly work for the customer.

(3.3) Completely Knock Down (CKD): The shipment goes to the customer in component form. The customer they does surface mount technology and assembly.

(4) The technology source for cellular phones:

Before announcing a cellular phone model, the technology of the Chinese cellular phone vendor must come mainly from the following three:

(4.1) The chipset vendor (or cellular phone manufacturer has its own technology): China’s cellular phone manufacturers use chip vendors, or reference designs of the chipset to complete

(4.2) Post the brand/SKD/CKD: China’s cellular phone manufacturer purchases the finished product/semi-finished product from Taiwanese/South Korean manufacturers.

(4.3) Cellular phone design houses: China’s cellular phone manufacturers purchase the design diagram from cellular phone design houses, and then through their own production lines or EMS factories they sell their own end products.

(5) Cellular phone brand type: One brand and two-brand

If the company does not have the licenses, then it will borrow a license from others that have one. Or did not have technology ability but own the domestic sale licenses, post the brand name to the foreign cellular phone products that have the technique but have no the domestic sale licenses. The first way is to market a cellular phone simultaneously with two brand names on it (e.g., BenQ and TCL). The second way is to market the same cellular phone model with different brand names (e.g., BenQ and CECT). Therefore, the possible brand share of a certain cellular phone manufacturer is very high, but it not concerned about the cellular phone from the design, production, or sales end. The cellular phone company only rents a license to earn profits. Therefore, this paper will not use ASP (Average Selling Price) to measure manufacturers’ development ability in China’s market.

(6) The import and export characteristics of the cellular phone supply chain:

Because China’s MII limited imports of cellular phone system products and components, and foreign or Taiwanese companies still do not have enough confidence in China’s investment environment, Taiwanese or South Korean cellular phone manufacturers’ imports to China’s market by CKD/SKD, then used the native production lines to carry on simple construction in China.

(7) Brand share: this paper partitions China’s market by the market share of each brand name. In the case of a dual brand sale, we categorize it as a foreign brand name.

(8) Shipment share: this paper calculates each manufacturer's share of full system sales.

(9) Self-production proportion: this paper calculates each manufacturer's SMT production proportion of products over the SKD and full-system levels.

(10) Self-technique proportion: This is the proportion of cellular phones produced by a manufacturer’s self-development and purchased reference design sources.

(11) Export quantity: This is each brand manufacturer’s export quantity, deducting false export volume from tax-protected zones.

(12) Customer concentration ratio: We use the biggest sales contribution of a customer’s business by total sales to evaluate the customer concentration ratio of Taiwanese PCs and cellular phones’ ODM/EMS.

(13) ASP (Average Shipment Price): Due to the policy of mobile cellular phone subsidies, if we use Average Selling Price at the retail level to measure the price of cellular phones, then there may be some mistakes about the actual price. Therefore, we use Average Shipment Price to measure the price of cellular phones.

(14) R&D intensity and R&D efficiency: R&D expenditures and R&D expenditures as a percentage of sales are commonly used to represent a film’s R&D intensity. The number of patents is often used as an indicator of a firm’s knowledge stocks (DcCarolis and Deeds 1999). In the ICT industry, R&D expenses as a part of revenue are an important index to evaluate how a company puts emphasis on innovation. R&D expenditures as a percentage of sales are commonly used to represent a firm’s R&D intensity (Lin and Chen, 2005).

Moreover, several efficiency-oriented R&D performance measures such as grant patents per R&D expenditures (Deng, Lev and Narin 1999), the number of patents granted, and R&D spending per patent (Bowonder, Yadav and Kumar 2000) are commonly used in the R&D management and finance literature (Wu, Hung and Lin 2006). The researchers also find R&D intensity has a positive impact on the degree of product diversification (Galan and Sanchez 2006). Therefore, this paper uses R&D intensity and R&D efficiency to measure R&D performance, whereby R&D intensity is measured as R&D expense as a percentage of sales, and R&D efficiency is measured as the number of patents that the firm receives divided by its R&D expenses (in millions of US dollars).

3.2 DATA SOURCES

Current Chinese authorities are still very conservative towards marketing research. A researcher must have a license to carry on investigation activities. For the cellular phone industry or market related data, it is still not easy to the find anyone to obtain data. The more complete data come from three aspects mainly at the present time:

(1) China’s State Council, Standardization Administration and MII: The MII periodically (every one to two seasons) announces to investigate data, with the data mainly entrusted to the

investigation method is that foreign and domestic vendors need to show production and sales data to the CCID periodically. Although that data are the most complete, native cellular phone manufacturers sometimes have pressure from the policy, and the arithmetic figure reliability is worse. In addition, the data mainly are from the supply side to carry out the calculation. There is no concern about channel inventory and post the brand.

(2) The China’s National Statistics Bureau: Many Chinese investigation institutions, such as Beijing All China Marketing Research (ACMR) and Beijing SinoBnet, are established by National Statistics Bureau insiders at first, and at the present time they also cooperate with China’s National Statistics Bureau. Relevant cellular phone industry and market data are investigated through the market and retail channels mainly. Although the data is gotten by the demand side, the weakness lies in that it can't control foreign manufacturer shipments of imports and exports. Posting the brand and dual-brand problems also cannot be defined effectively at the same time.

(3) ITIS system of the Taiwan’s Ministry of Economic Affairs: The Institute for Information Industry MIC and Industrial Technology Research Institution IEK carry out the investigation, with the target mainly Taiwanese cellular phone manufacturers and Taiwanese cellular phone components manufacturers. The weakness of this dataset is that variable definitions are different from those in China such as PHS is considered as a cellular phone in Taiwan.

There are some sporadic information appearing in annual reports of listed companies, international company reports, import and export data of maritime transportation, data of computer and electronics associations, and investigation reports of international research institutes in the electronics industry, such as IDC and Yano Research Economic Institute (YRI), etc.

3.3 DATA COLLECTION

(1) China’s cellular phone industry:

Based on the above resources, we collect data over 1991~2006 for China’s mobile service market and telecom equipment manufacturing industry from MII of People’s Republic of China, financial statements, and newsletters of these companies. We also collect data over 1999~2006 for China’s cellular phone market and industry from MII, Beijing ACMR (All China Marketing Research), Beijing Sino-MR, TRI (Topology Research Institute), and ITIS (Industry & Technology Intelligence Services).

The data of MII mainly entrusted to the CCID to carry out the investigation are mainly from the supply side in order to carry out the calculation. Moreover, Beijing ACMR and Beijing Sino-MR were established by National Statistics Bureau insiders first, and at the present time they also cooperate with China’s National Statistics Bureau. Their data are gotten by the demand side and are mainly investigated through the market and retail channels. Finally, TRI and ITIS are Taiwan’s research institutes whose targets are mainly Taiwanese cellular phone manufacturers and Taiwanese cellular phone component manufacturers.

We then interviewed upstream and downstream manufacturers in the cellular phone industry to confirm details. On the manufacturer side, we interviewed four Chinese vendors (ZTE, TCL, Konka, and Amoi) and six Taiwanese vendors (Dbtel, BenQ, Inventec (OKWAP), Compal Communication, Lite-On Technology, and Compal Electronics). On the components manufacturering side, we interviewed Merry Electronics which produces an electric shock component (takes delivery of goods mainly to the Chinese market). On the cellular phone channel side, we interviewed CELLSTAR to attain a total of twelve firms. The investigating objects include product managers, research and development department heads, and sales managers. The investigation and interview time period was January to May 2005 and was updated on September to October 2006.

In addition to individual firms’ data, we collected data of the major cellular phone, operators and telecom equipment firms in the world from companies’ annual reports and newsletters. Our data of cellular phone firms include four global companies, Nokia, Motorola, Samsung, and LG, whose market shares were all more than 5% in 2005, and two China’s companies, TCL and Bird, that were the first two domestic firms by market share from 2000 to 2005. BenQ-Siemens and Sony-Ericsson, even though their global market shares were also more than 5% in 2005, were not included as they had merged or been acquired.

Our data of telecom equipment firms include five global companies Nokia, Motorola, Ericsson, Lucent, and Siemens that were the major wireless infrastructure firms, and two China’s companies Huawei and ZTE that were the first two domestic firms by sales. Our data also include two of China’s mobile service providers China Mobile and China Unicom. We then use the Mann-Whitney test to examine the difference in the R&D intensity between China’s and other countries’ cellular phone and telecom equipment firms.

(2) South Korea’s cellular phone industry:

market shares were all more than 5% in 2005. BenQ-Siemens and Sony-Ericsson, even though their market shares were also more than 5% in 2005, were not included as they had merged or been acquired.

We collected the number of patents from the United States Patent and Trademark office. North America has been the main cellular phone market globally and the United States is the largest market of all countries except for China. Therefore, all the main firms have taken out American and Chinese patents for cellular phones. However, the number of patents in China includes those applying and those already applied, and so we use the number of American patents for cellular phones to measure R&D results. We use the Mann-Whitney test to examine the difference in the R&D performance between South Korean and other countries’ cellular phone firms.

(3) Taiwan’s cellular phone industry:

We also collected data of the major cellular phone firms in Taiwan from companies’ annual reports and newsletters. Our data include CCI, Arima, HTC, FIH, DBTEL, OKWAP, and BenQ. FIH was spun-off by Hon Hai/Foxconn Precision Ind. Co. and listed in Hong Kong. In fact, FIH still likes a Hon Hai/Foxconn’s cellular phone business group and includes Chi-Mei Communications and Ambits that were merged by Hon Hai/Foxconn in 2005 and 2004, respectively. Most of its R&D engineers are located in Taiwan. We still view it as a Taiwan-based cellular phone company.

All of these Taiwan’s cellular phone companies have full R&D, manufacturing, and testing abilities. Among them, CCI, Arima, HTC, FIH, DBTEL, and OKWAP’s sales are more than 90% from cellular phone products. BenQ’s product lines include cellular phones, DVD, NB PC, LCD TV, DSC, and so on. FIH and OKWAP have been set up less than 5 years. As a result, it is not suitable for using them to compare with PC companies.

We collected data of the major NB/PC firms in Taiwan from companies’ annual reports and newsletters, including Hon Hai/Foxconn, Quanta, Compal, and Inventec. Wistron was spun-off by Acer in 2001, and we can not find enough data that year. Quanta, Compal, and Inventec’s sales have more than 90% coming from NB/PC products. We use the Mann-Whitney test to examine the difference in the R&D intensity and customer concentration ratio between Taiwan’s NB/PC and cellular phone firms.

3.4 RESEARCH HYPOTHESIS

Figure 3 shows the structure of China’s mobile industrial policy as a whole including operators, infrastructure manufacturers, and handset vendors. According to the industrial policy targets, this research puts forward the following research hypothesis.

First, due to the cellular phone market being promoted with competition, this research uses the usage fee of the end user and the level of mobile service industrial concentration to measure the effect of the industrial policy.

Hypothesis 1.1: China’s mobile industrial policy (through its support of China Unicom) of reducing the level of industrial concentration has a positive influence. Hypothesis 1.2: China’s mobile industrial policy (through its support of China Unicom) of

reducing the usage fee of the end user has a positive influence.

For promoting China’s domestic telecom equipment industry, this research uses local vendors’ sales and own brand market share to measure the effect of the industrial policy.

Hypothesis 2.1: China’s mobile industrial policy of promoting the local vendors’ sales has a positive influence.

Hypothesis 2.2: China’s mobile industrial policy of promoting locals’ own brand market share has a positive influence.

For supporting China’s cellular phone industry, this research uses brand share and cellular phone shipments as research variables.

Hypothesis 3.1: China’s mobile industrial policy (restriction to produce and licenses to sell) of promoting the domestic brand manufacturer has a positive influence. Hypothesis 3.2: China’s mobile industrial policy (restriction to produce and licences to sell)

of promoting domestic manufacturers’ shipments has a positive influence.

To raise China’s cellular phone ability through technology, this research tests the hypothesis with the proportion of self-assembly and self-R&D.

Hypothesis 4.1: China’s mobile industrial policy (restriction to produce and licenses to sell) of raising domestic manufacturers’ development and ability has a positive influence.

Hypothesis 4.2: China’s mobile industrial policy (restriction to produce and licenses to sell) of promoting domestic manufacturers’ production technology has a positive influence.

Finally, for enhancing the exporting ability of China’s domestic cellular phone industry to export products, this research uses domestic vendors’ export shipment volume as a variable for testing.

Hypothesis 5: China’s mobile industrial policy (restriction to produce and licenses to sell) of raising domestic manufacturers’ export ability has a positive influence.

Figure 3. The structure of China’s mobile industrial policy Infrastructure Venders

Infrastructure Venders

End User Market

End User Market

Spectrum Policy Spectrum Policy China FDI Policy China FDI Policy No.18 Document No.18 Document No.5 Document No.5 Document Mobile Operators Mobile Operators Handset Venders Handset Venders

Key Component Venders

Key Component Venders

The Ninth and Tenth Five year Economic and Social Develop Plan The Ninth and Tenth Five year Economic and Social Develop Plan

•To promote domestic IC industry

•To promote native handset industry

•To raise the R&D ability and manufacturing ability •To enhance the handset export strength

•End Users: 2,600~2,900 M

•Handset Shipments: 100M (Domestic: 50%)

•To promote domestic telecom firms

•To set up TD-SCDMA Standard •To enhance the competition

Infrastructure Venders

Infrastructure Venders

End User Market

End User Market

Spectrum Policy Spectrum Policy China FDI Policy China FDI Policy No.18 Document No.18 Document No.5 Document No.5 Document Mobile Operators Mobile Operators Handset Venders Handset Venders

Key Component Venders

Key Component Venders

The Ninth and Tenth Five year Economic and Social Develop Plan The Ninth and Tenth Five year Economic and Social Develop Plan

•To promote domestic IC industry

•To promote native handset industry

•To raise the R&D ability and manufacturing ability •To enhance the handset export strength

•End Users: 2,600~2,900 M

•Handset Shipments: 100M (Domestic: 50%)

•To promote domestic telecom firms

•To set up TD-SCDMA Standard •To enhance the competition

CHAPTER 4 THE POLICY EVOLUTION AND CHINA’S MOBILE

INDUSTRY ECOSYSTEM

4.1 THE DEVELOPMENT BACKGROUND OF THE CHINA’S TELECOM

INDUSTRY

For the period of China’s economic growth, China’s FDI (Foreign Direct Investment) policy was divided into three stages: FDI was not allowed before 1978. After an open-door policy in 1978, FDI was promoted in most industries except for telecommunications operations, electricity, railways, and other politically sensitive sectors from 1978 to 1986. Finally, after 1987 China’s FDI policy integrated with its industrial policy in order to join WTO (World Trade Organization).

China’s FDI policy in the telecommunications industry is synchronized with its general FDI policy. There was no FDI either in China’s telecom manufacturing sector or service providers before 1978. China’ operators had to buy old-style telecom equipment from domestic vendors. From the early 1980s, China’s FDI policy on the telecommunications industry actively encouraged domestic firms to achieve advanced technologies through joint ventures (JV) (Wu and Zhang, 1992; Pitt et al., 1996; Tan, 2002).

At about the same time, the China’s former Ministry of Posts and Telecommunications (MPT), which was renamed the Ministry of Information Industry (MII) in 1998, boosted several industrial policies to give priority to the development of telecommunications. For example, 90% of the central government’s investment is considered as un-repayable loans (Wu and Zhang, 1992). MII as a fully authorized ministry is more active in promoting the domestic telecom industry through industrial policies including spectrum management, telecom operators’ spin-offs, and supporting telecom equipment and cellular phone manufacturing firms after 1998.

4.2 THE PROGRESS OF THE POLICY OF CHINA’S SPECTRUM

MANAGEMENT AND MOBILE OPERATOR INDUSTRY

Analogue mobile service has been available in China since 1987 and MPT was the only provider of mobile services. Because of individual provincial MPT purchasing and no unified standard, different communication systems from different vendors existed in different provinces. In 1994 China’s government announced that its 2G digital cellular phone standard would follow the GSM (Global System Mobile) standard. In 2000 China’s

wireless spectrum.

As China’s mobile service emerged in the 2G standard, China’s government tried to use its 3G license policy to promote its independent 3G standard TD-SCDMA (Time Division - Synchronous Code Division Multiple Access). In June 1998 China’s Academy of Telecommunications Technology (CATT) submitted TD-SCDMA to the International Telecommunication Union (ITU) and was approved by ITU.

In the mobile operator side, in 1998 the MPT was restructured as MII, the establishment of a new independent regulator, and China Telecom was separated from MPT. Since 2000, China Telecom was further split up into four groups according to specific services, and one of them was China Mobile. From that time, China Mobile had been specifically dedicated to cellular phone services that use the GSM standard.

In 1993 due to less than one million mobile phone subscribers, the China’s government decided to establish another player, China Unicom, in the mobile industry to compete with China Mobile (the former MPT/China Telecom). The formal establishment of China Unicom was in 1994 and it launched GSM mobile service in 1995. In order to encouraging competition in the industry, China Unicom was allowed to promote CDMA service at the same time in 2000.

After China Mobile and China Unicom built up their GSM/GPRS (General Packet Radio Service), and CDMA system networks aggressively, MII started to make a decision on 3G standards WCDMA (Wideband Code-Division Multiple-Access), CDMA2000, and TD-SCDMA in the past few years. In order to further encourage competition and promote the independent 3G standard, MII plans to grant more 3G licenses to operators such as China Telecom, China Netcom, China Unicom, and China Mobile after China’s TD-SCDMA industry is mature.

4.3 CHINA’S COMMUNICATION EQUIPMENT INDUSTRIAL POLICY AND

ITS DEVELOPMENT

As Figure 4 shows, being similar with China’s FDI general policy, China’s mobile telecom equipment industry including base stations and switches is divided into four stages in the past twenty years: equipment import, JV encouragement, JV encouragement and promoting domestic suppliers, and equipment exports. Because China Mobile (the former MPT/China Telecom) had a mission to promote domestic telecom vendors by 2000, using the enormous market as a bargaining power, JV encouragement was the main way to introduce advanced technology from foreign industrial leaders such as Siemens, Motorola, and Alcatel. Based

on the China’s market size, domestic telecom vendors use the channel advantage to exchange technology.

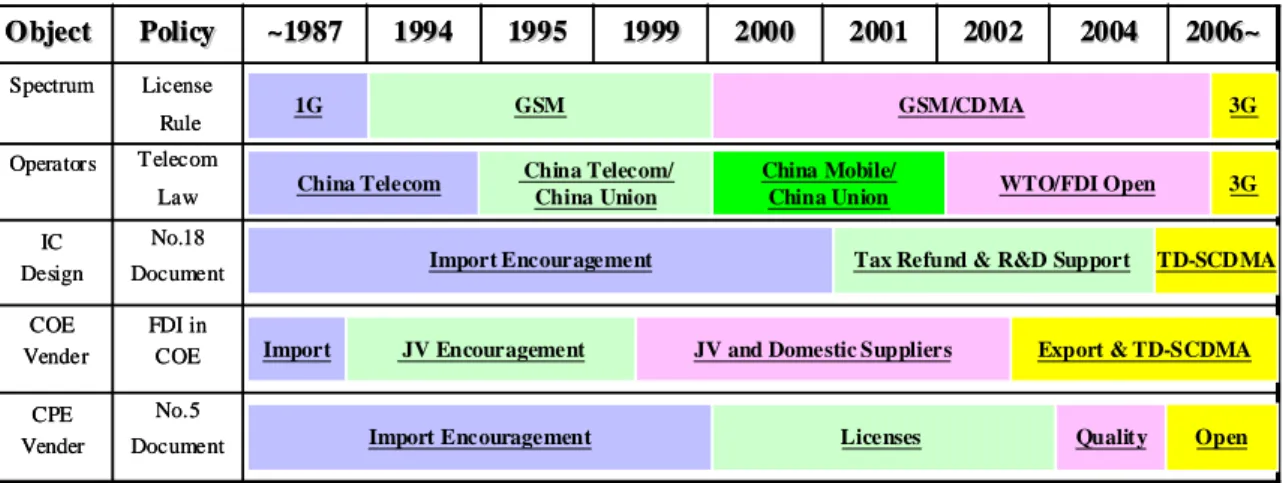

Figure 4. The development steps of China’s mobile industry by an industrial policy view

After 2000, MII started to introduce CDMA technology to further enhance domestic firms’ ability. Following up the WTO agreement and MII’s interposition, Qualcomm agreed to charge only a 2.5% license fee for China’s domestic firms such as ZTE, Huawei, and Eastern to produce and sell CDMA telecom equipment and cellular phones. This ratio is lower than Qualcomm charging 5~8% for global manufacturers.

After the process of technology transfer from foreign firms in telecom equipment, several domestic firms such as Great Dragon, Datang, ZTE, Huawei, and Eastern telecom companies have built up their R&D and sales ability. Huawei and ZTE have exported telecom equipment to developing countries actively since 2002. In the future, MII can continue to guide technology transfer by choosing 3G standards flexibly including WCDMA, CDMA2000, and TD-SCDMA. The MII policy is to ensure that TD-SCDMA is commercially operable as soon as possible and to promote domestic firms leading the TD-SCDMA industry at the same time.

As for China’s communications IC industry, its related policies are a part of China’s semiconductor industrial policy, which was named as ‘No. 18 Document’. Subsidies for R&D budgets and free interest loans are the main ways to support domestics IC design houses. China’s IC design houses have already 0.13~0.25 micron design ability in 2006. Their product lines include WLAN (Wireless Local Area Network), SIM (Subscriber Identity Module), and GSM/GPRS/TD-SCDMA IC (Integrated Circuit).

1995 1995 No.5 Document CPE Vender FDI in COE COE Vender No.18 Document IC Design Telecom Law Operators License Rule Spectrum 2006~ 2006~ 2004 2004 2002 2002 2001 2001 2000 2000 1999 1999 1994 1994 ~1987 ~1987 Policy Policy Object Object 19951995 No.5 Document CPE Vender FDI in COE COE Vender No.18 Document IC Design Telecom Law Operators License Rule Spectrum 2006~ 2006~ 2004 2004 2002 2002 2001 2001 2000 2000 1999 1999 1994 1994 ~1987 ~1987 Policy Policy Object Object 1G GSM GSM/CDMA 3G

China Telecom China Mobile/

China Union WTO/FDI Open 3G

Import Encouragement Tax Refund & R&D Support TD-SCDMA

Import Encouragement Licenses Quality Open

Import JV Encouragement JV and Domestic Suppliers Export & TD-SCDMA China Telecom/

4.4 THE PROGRESS OF THE POLICY DEVELOPMENT OF CHINA’S

CELLULAR PHONE INDUSTRY

According to the plan of Ministry of Information Technology of China, the development of China’s cellular phone industry can be traced back to 1998. The primary plan of MII was to establish a main policy for the independent knowledge property rights of the cellular phone industry in China.

After a specific meeting over the development of China’s cellular phone industry was held by China’s State Council in August 1998, MII coordinated the arrangement of various kinds of proposals covering strategy and policy. The issues included expediting technology transfers from foreign joint ventures and establishing research and development of cellular phones to promote 10 China GSM cellular phone suppliers, including Bird and TCL. In January 1999, China’s State Council approved the ‘No. 5 Document’. This was the beginning of how China’s government promoted its domestic cellular phone suppliers by setting up its industry. The three stages of China’s industrial policy on cellular phone are as follows (State Council of the People's Republic of China 1995; 2001):

(1) First stage: Using the market to exchange funds and technology (around year 2000)

The development of China’s cellular phone industry can also be divided into three stages on the whole. By 1999, huge and latent business opportunities in China and cheap labour and land attracted the foreign investment into China. This strategy was to “exchange technology with the market.” After 1999, in order to protect native manufacturers, the policy restricted foreign businesses with various investment limits and trade obstacles to help expand China’s domestic cellular phone industry.

(2) Second stage: Propping up China’s domestic cellular phone industry proactively (2000~2004)

The MII instructed seven items at the end of 1998, indicating support for domestic manufacturing abilities by attracting foreign investment. The 1998 MII policy guidelines are as follows.

(2.1) No longer allowing foreign companies to establish new individual proprietorships or joint venture factories, but still welcoming get core technology from foreign companies

(2.3) A joint venture factory must transfer technology quickly

(2.4) Import restrictions (reducing whole products as imports)

(2.5) Giving priority towards purchases of native products (establishing the laws to push national enterprises to purchase domestic products)

(2.6) Reducing taxes and giving out loans and subsidies

According to the above guides in 1999, MII carried out various control measures on the following grounds: MII once again put forward measures for propping up native manufacturers in November 1999, adopting the policy to limit foreign manufacturers of cellular phones in China’s domestic products and sales, in principle forbidding the import of any GSM cellular phones. For foreign individual proprietorships and joint ventures, MII also enhanced the technology transfers, requesting foreign companies producing cellular phones in China with at least 60% for export to source at least 50% of their product components locally by the end of 2001. A company’s sales quota is decided by its export ratio and localization of components.

(3) Third stage: Competition after market opening (2005~present)

After joining WTO in December 2001, China promised to relax the ceiling of foreign ownership in any domestic cellular phone company, increasing it from 25% in 2002, to 35% in 2003, and to 49% since 2005. China also plans to cancel foreign individual proprietorships and joint venture manufacturers in order to acquire domestic market share, such that they must transfer their technology. This will result in domestic cellular phone vendors in China losing the protection umbrella. After 2005, domestic companies with competitive ability can export their products to the overseas market (Ministry of Information Technology of China 1999).

For tariffs on key components, China’s authorities will put into practice the reduction of import tariff rates for key electronics components. The average tariff for key components in China’s communications market was 13.3% in 2000 and then declined to 0% in 2003. Since 2005 there has been no tariff imposed on telecommunications products.

4.5 CHINA’S CELLULAR PHONE INDUSTRIAL POLICY AND ITS

CURRENT CONDITION

In the past years, cellular phone manufacturers in China have faced the following regulations:

(1) Restriction of building factories:

China’s government has developed specific enterprises and established a certification system. It is also its so-called macro control policy.

(2) Restriction of production and sales:

MII distributed 50 cellular phone manufacturer licenses in total. Among these licenses, GSM cellular phone licenses were issued to 13 joint ventures and 17 domestic enterprises. Twenty licenses for CDMA were also issued. Except for Motorola as a foreign capital enterprise, all the other licensed firms are domestic enterprises.

(3) Restriction of product certifications:

Before companies can sell their products in China, cellular phone manufacturers must get approval from both the Standardization Administration of China and the Examination Centre of MII for new models’ development. The product must pass the examination of full type approval (FTA), model number approval, an electromagnetism compatible test, and an examination of connection with a network.

Therefore, the development of China’s cellular phone industry is also divided into four stages on the whole. By 1999, huge and latent business opportunities in China and cheap labour and land attracted foreign investment into the country. In January 1999, China’s State Council approved the ‘No. 5 Document’ including restriction of building factories, production, and sales. MII distributed 50 cellular phone manufacturer licenses in total. Among these licenses, GSM cellular phone licenses were issued to 13 joint ventures and 17 domestic enterprises. Twenty licenses for CDMA were also issued. Except for Motorola as a foreign capital enterprise, all other licensed firms are domestic enterprises. MII then enhanced the policy protection in 2002. Finally, MII released ‘No. 5 Document’ after 2005 to build up a fair competition environment between domestic and foreign firms (Xie and White, 2006).

CHAPTER 5 EFFECTS OF INDUSTRIAL POLICY ON R&D

ACTIVITIES AND DEVELOPING STRATEGIES OF

CHINA’S MOBILE INDUSTRY

5.1 DATA DESCRIPTION AND HYPOTHESIS TESTING

Our data provides information infrastructure on China’s cellular phone industry and market. On the supply side, China became the largest cellular phone making country in the world from 1999 to 2004. Both foreign and local vendors’ shipments in China have grown rapidly in recent years.

Our data presents China’s domestic market share by quarters, and China’s domestic vendors’ cellular phones that were manufactured by their own SMT (surface mounted technology) line and the technology sources from local vendors for each period have grown a lot. If we use the ratio concept, then we will find that domestic vendors’ total shipments and the proportion of SMT and technology are still lower. That is why after 2004, foreign vendors saw advantages of technology, with Nokia, Motorola and Samsung gaining market share quickly.

On the demand side, from 1998 to 2004, China has emerged as the largest mobile subscriber market in the world. According to an In-Stat report, mobile subscribers in China have grown to 272m in 2004, representing a hefty CAGR of over 50% for the period. The burgeoning growth of China’s mobile subscribers has resulted in a rapid rise in mobile phone shipments.

Then we use MANOVA (Multivariate Analysis of Variance) to test the influences of China’s communications industrial policy on its domestic cellular phone manufacturing industry. Each hypothesis is then tested by ANOVA (Analysis of Variance).

Hypotheses 1.1 & 1.2 Testing Results:

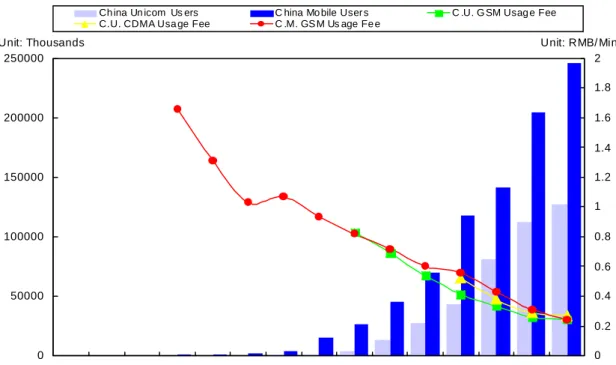

China’s mobile industrial policy supports China Unicom to compete with China Mobile in order to increase market competition. Our data shows that the industrial policy of reducing market concentration significantly reduced usage fees. Figure 5 shows that the market share of China Mobile has been decreasing. From 1991 to 2005, China has emerged as the largest mobile subscriber market in the world. The number of mobile subscribers in China has grown to be more than 350 million in 2005.

Figure 5. The growth of China’s cellular phone users and the decline of the usage fee (Source: MII; Financial statements and newsletters of these companies)

Hypotheses 2.1 & 2.2 Testing Results:

The burgeoning growth of China’s mobile subscribers has resulted in a rapid rise in building wireless infrastructure equipment including switches, base stations, network management systems, and so on. China’s domestic telecom vendors such as Huawei and ZTE exchange technology through JV and channel advantages. From the newsletters of these companies, in the advanced 3G/3.5G technology, Huawei’s WCDMA/HSPA (High-Speed Packet Access), ZTE’s CDMA 2000 1x EVDO, and Datang’s TD-SCDMA have matured.

Our data shows the effect of the industrial policy of promoting sales and the market shares of China’s local telecom equipment vendors are both significant. The data also shows that the export and sales ability of China’s major local telecom equipment vendors have been expanding quickly in the past years (Figure 6).

0 50000 100000 150000 200000 250000 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 0 0.2 0.4 0.6 0.8 1 1.2 1.4 1.6 1.8 2 Ch ina Un icom Us ers C hina Mo bile User s C .U. G SM Usag e Fee C.U. CDMA Usa ge Fee C .M. GS M Us age Fe e

Figure 6. The growth of major Chinese telecom firms’ sales (Source: MII; Financial statements and newsletters of these companies)

Hypotheses 3.1& 3.2 Testing Results:

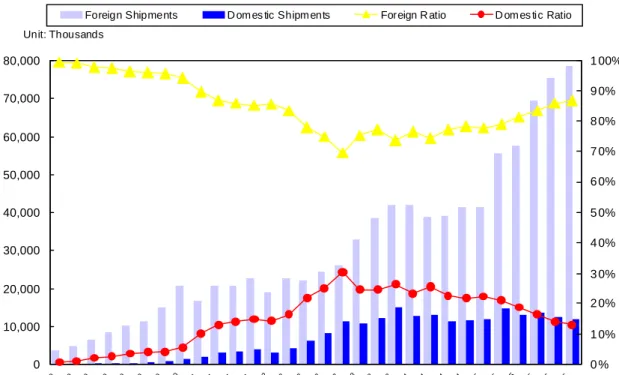

After China became the largest cellular phone making country in the world, both foreign and local vendors’ shipments in China have grown rapidly in recent years. The total shipments grew to more than 300 million in 2005 (Figure 7).

On the own brand shipment side, China’s cellular phone industrial policy of supporting its native brand manufacturers does have a positive influence, and according to our data it is significant. If we use local vendors’ market share to check, our test also shows that the influence of the policy is significant.

On the shipment volume side, China’s cellular phone industrial policy of supporting its domestic manufacturers does have a positive influence, and according to our data it is significant. If we use local maker shipments to account for total shipments, our test also shows that the influence of the policy is significant.

0 100,000 200,000 300,000 400,000 500,000 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Datang ZTE HuaWei

Figure 7. The production shipments and shipment ratio of China’s local vendors

Hypotheses 4.1 & 4.2 Testing Results:

For the shipments by local vendors’ SMT-Line self-assemble, China’s cellular phone industrial policy of supporting its domestic manufacturers to develop their own ability is a positive influence, and according to our data it is significant.

If we use local makers’ SMT-Line self-assemble shipments to account for total local maker shipments, due to local vendors depending on outsourcing or posting a brand strategy, we think the ratio will be lower. Our test shows a negative influence of the policy being significant.

On the technology source from the local vendor side, China’s cellular phone industrial policy has a positive influence of supporting domestic manufacturers to develop their own technology ability, and according to our data it is significant.

If we use local makers’ own technology shipments to account for total local makers’ shipments, due to local vendors depending on outsourcing or posting a brand strategy, we think the ratio will be lower. Our test shows that the negative influence of the policy is significant. 0 10,000 20,000 30,000 40,000 50,000 60,000 70,000 80,000 1Q9 9 2Q 99 3Q9 9 4Q9 9 1Q 00 2Q0 0 3Q 00 4Q 00 1Q0 1 2Q0 1 3Q 01 4Q 01 1Q 02 2Q 02 3Q0 2 4Q 02 1Q0 3 2Q 03 3Q0 3 4Q 03 1Q 04 2Q 04 3Q 04 4Q 04 1Q 05 2Q0 5 3Q 05 4Q 05 1Q 06 2Q 06 0 % 1 0% 2 0% 3 0% 4 0% 5 0% 6 0% 7 0% 8 0% 9 0% 1 00% Foreign Shipments D om es tic Shipm ents Foreign R atio D om es tic Ratio Unit: Thousands

Combining the result of Hypotheses 3 & 4 Testing, during the 1999~2006 period, China’s cellular phone industrial policy of promoting its domestic brand manufacturers has some significantly positive influences such as promoting the shipment volume, own brand shipment, and local vendors’ market share. However, because of the industrial policy protection, gaining market share was a top priority for China’s cellular phone manufacturers. China’s cellular phone industrial policy meant that domestic vendors ignored enhancing their innovative capacities.

We also find that domestic vendors’ total shipments and the proportion of SMT and technology are still low. Since local vendors depend on outsourcing or posting a brand strategy, the ratio of local makers’ SMT-Line self-assemble shipments to total local makers’ shipments significantly declines. Similarly, because local vendors heavily depend on strategies of outsourcing or posting a brand strategy, the ratio of local makers’ own technology shipments to total local makers’ shipments significantly decreases.

Hypothesis 5 Testing Results:

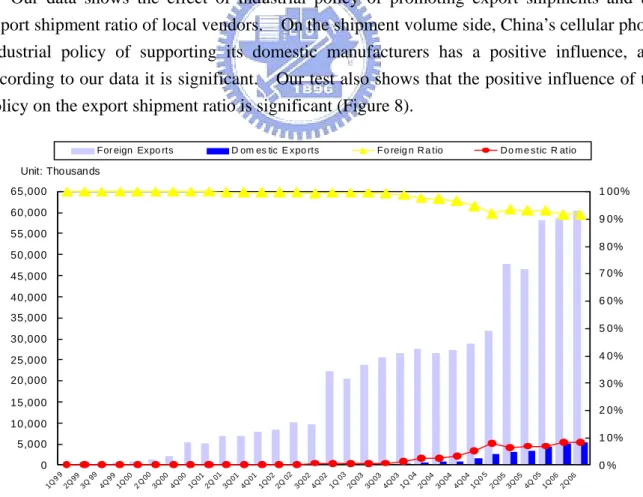

Our data shows the effect of industrial policy of promoting export shipments and the export shipment ratio of local vendors. On the shipment volume side, China’s cellular phone industrial policy of supporting its domestic manufacturers has a positive influence, and according to our data it is significant. Our test also shows that the positive influence of the policy on the export shipment ratio is significant (Figure 8).

Figure 8. The export shipments and shipment ratio of China’s local vendors

0 5,000 10,000 15,000 20,000 25,000 30,000 35,000 40,000 45,000 50,000 55,000 60,000 65,000 1Q9 9 2Q993Q 99 4Q9 9 1Q002Q0 0 3Q004Q001Q0 1 2Q 01 3Q014Q011Q0 2 2Q 02 3Q024Q021Q 03 2Q033Q034Q0 3 1Q 04 2Q0 4 3Q044Q041Q0 5 2Q053Q054Q 05 1Q0 6 2Q06 0 % 1 0% 2 0% 3 0% 4 0% 5 0% 6 0% 7 0% 8 0% 9 0% 1 00%

For eign Expo rts D om es tic E xpo rts F o reig n R a tio D o m e stic R atio

5.2 R&D ACTIVITIES

After China Unicom and China Mobile became the largest CDMA and GSM operators in the world, MII promoted its domestic manufacturing industry aggressively. Because of industrial policy support, both domestic cellular phone and telecom equipment industries have grown rapidly. However, aside from gaining market share, China’s cellular phone and telecom equipment firms have different R&D activities in this period. Comparing with telecom equipment firms, China’s cellular phone industrial policy pushed domestic vendors to ignore enhancing their innovative capacities.

There has been a gap in R&D intensity between China’s and global major cellular phone firms in the past years. For example, TCL Communication and Ningbo Bird, the first two leaders of China’s domestic cellular phone industry, saw R&D expenses between 5.10% and 0.82% as a part of revenue. During the same time, major foreign cellular phone firms have been paying more attention to R&D. Nokia, Motorola, Samsung, and LG’s R&D intensity were about 5% to 10%.

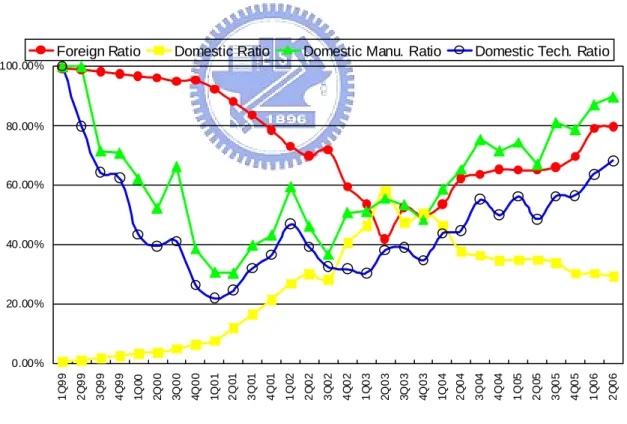

Figure 9. The market share, manufacturing and technology ratios of China’s local vendors

Related to Western and South Korean products, some key weaknesses of China’s firms include a lack of innovative experience and low R&D investments. As a result, higher defect rates damaging brand perception have become domestic vendors’ Achilles heel. That

0.00% 20.00% 40.00% 60.00% 80.00% 100.00% 1Q 99 2Q 99 3Q 99 4Q 99 1Q 00 2Q 0 0 3Q 0 0 4Q 0 0 1Q 0 1 2Q 0 1 3Q 0 1 4Q 0 1 1Q 0 2 2Q 02 3Q 02 4Q 02 1Q 03 2Q 0 3 3Q 0 3 4Q 0 3 1Q 0 4 2Q 04 3Q 0 4 4Q 0 4 1Q 0 5 2Q 0 5 3Q 05 4Q 05 1Q 06 2Q 06