國立臺灣大學工學院土木工程學系 博士論文

Department of Civil Engineering College of Engineering National Taiwan University

Doctoral Dissertation

國際營造廠之環境管理與公司業績表現

Environmental Management and Firm Performances of Multinational Construction Firms

王傳芳

CHUAN-FANG Ong

指導教授::陳柏翰 博士

Major Professor: PO-HAN Chen, Ph.D.

中華民國 107 年 7 月 July 2018

ACKNOWLEDGEMENT

For the support and freedom I was given, to improve and enhance my research skills throughout the research, I wish to express my most sincere gratitude to my supervisor, Professor Po-Han Chen. I also wish to express my appreciation to the lecturers of Construction Engineering Management division, Civil Engineering Department, who always provide useful guidance on research methods and inspiring knowledge related to construction management.

Special thanks to my beloved Taiwanese friends, Mr. Tzu-Hao Chen, Ms. Molly Hsu, and Ms. An-Chi Cheng for their generous, voluntarily and selflessness assistance in my data collection. They are the friends that always dependable when I need a helping hand anytime anywhere. Besides, Tsu-Te Peng, Nguyen Thanh-Chuong, and Chao-Hung Lin are my course mates that have rendered a lot helpful advices and information to work out my assignments and studies.

Last but not least, I wish to express my gratitude on the traveling grant provided by Kwang-Hua Education Foundation, which covered my collaborative research visit in the Hong Kong Polytechnic University. Thanks for the funding support of Research Institute for Sustainable Urban Development at the Hong Kong Polytechnic University (8-ZJJZ) for related research works.

To my parents, there are no adequate words to express my gratitude for supporting me spiritually, financially, unconditionally.

中文摘要

隨著環境課題日益受到關注,營建業無可避免的必須在組織治理上做出改變。

數份研究證實國際營造廠在環境管理上顯得比較積極主動,但是在環境管理,財 務表現,及國際化之間關係的分析卻顯得不足。這項研究將針對國際營造廠為研 究對象,主要研究目的是要探索環境管理策略和國際化之間的關聯、檢驗各個環 境管理方式和財務之間的關係、並且進一步檢驗區域多元化是否會調節環境管理 和財務之間的關係。

理論上,本項研究採用三項主要管理理論。資源基礎理論強調環境管理如何 強化公司的競爭優勢,交易成本理論和組織學習理論則解釋國際化對財務表現的 影響。

本研究從 Engineering News-Record (ENR) 2012 年度的頂尖營造廠表單中,

採用其中 61 家國際營造廠為研究對象。接著通過內容分析法來分析各家廠商的 環境報告,以此方式摘錄和評估各家的環境管理模式及其積極度。財務表現資料 的主要來源是通過 Datastream 資料庫獲取的次級資料。國際化資料則是依據營造 廠的國外銷售佔總銷售額比例,投資的地域擴張度,及地理集中度三方面來鑑定。

另外,此項研究採取三種不同的分析法解析資料以達到前述三個目標。其中 包括:反差分析及其他類似分析法、多元逐步回歸分析法、及調節回歸分析法。

在 K 均值聚類演算中歸類出三種不同積極度的環境管理策略,分別命名為被 動策略、預防策略、及積極策略。其後,從反差分析法得到結論是採用較積極環 境管理策略的國際營造廠有助於其公司國際化,但是環境管理策略對國際化的影 響是有局限的。相比採用被動和預防策略的營造廠,研究結果顯示採取積極策略

的營造廠在國際化上並沒有顯著的不同,但是採取積極策略的營造廠在國際地理 分佈上會傾向投資在發達國家中。

在財務表現的回歸分析中,有五項環境管理方式與公司財務表現明顯相關。

其中包括實地污染處理、營業環境掃描、環境管理系統、環保相關的創新、及利 益關係方參與。此外,實地污染處理和環保相關的創新都對財務表現呈現非直線 型的關係。實地污染處理是 U 型曲線,另外環保相關的創新是倒 U 型曲線的關係。

這發現有助於營造廠確立哪種環境管理方式會對財務造成影響,並且積極加強以 增加公司的競爭力。

調節回歸分析法引用地理集中度為調節變數,並與實地污染處理、營業環境 掃描、及環保相關的創新三種環境管理方式形成交互作用變數,檢驗它們對財務 表現的影響。研究結果發現地理集中度對環境管理方式呈現正負不一的影響。地 理集中度的影響是有賴於國際化的益處是否超越其成本。

綜上所述,本研究除了提供適當的理論來解釋環境管理、國際化、及財務表 現三者之間的關聯,也進一步通過量化的實驗證明其關係。對於營造廠來說,永 續環境的發展對公司治理會顯得越來越至關重要,營造廠必須採取適當的策略性 環境管理來應對挑戰,並通過強化環境管理來提高其在國際市場的競爭優勢。

關鍵字:環境管理、國際化、財務表現、永續營建、資源基礎理論、交易成本理 論、組織學習理論

ABSTRACT

Growing attention on environmental protection has triggered drastic changes in the corporate practices of construction firms. Several studies have shown that multinational construction firms have been relatively proactive in environmental management.

However, the relationships between environmental management, degree of internationalization, and financial outcomes are not fully comprehended. This study targets on multinational construction firms and the main goals of this study are to explore relationship between environmental strategy and degree of internationalization; examine the relationship between environmental practices and financial performance; and examine the moderating effect of regional diversification on the relationship between environmental practices and the financial performance.

Primarily, these relationships were established drawing from three profound management theories, Resource-based view explain how firms acquire competitive advantages from environmental management, transaction cost and organizational learning are two main perspectives that articulated firm performances with internationalization.

In total, 61 samples of multinational construction firms are drawn from the Engineering News-Record (ENR) Top International Contractor list published in 2012.

Content analysis was used to extract and measure the degree of proactivity of environmental management disclosed through environmental reporting. Financial and accounting information is collected through secondary data disclosed in Datastream database. Degree of internationalization is measured based on investment intensity, geographical extensity, and geographical concentration.

In addition, the study adopted three different analysis approaches to achieve the targeted goals. Analysis of variance (ANOVA) and other similar extension methods, stepwise regression, and moderated regression analysis are consecutively carried out to analyze the relationships that related to the goals.

Three clusters of environmental strategies have emerged from the statistical clustering which depict reactive, preventive, and proactive postures in strategic environmental management. The results denote that construction firms which are proactive in strategic environmental management would have improved internationalization to an extent where further proactivity would deem irrelevant to internationalization, and proactive firms would more likely to have greater geographical portfolio distribution in developed countries.

In regards of financial performances, five environmental management practices have been revealed to significantly associated with financial performances. These practices include pollution abatement on-site, environmental scanning, management systems and procedures, environmental innovation, and stakeholder engagement.

Nonlinear relationships have been detected on both pollution abatement on-site (U-curve) and environmental innovation (inverted U-shaped). These findings can assist construction firms in determining the key environmental management practices that are able to enhance their competitive edge.

Furthermore, regional diversification is adopted as a moderator, forming interaction terms with environmental management practices such as pollution abatement on-site, environmental scanning, and environmental innovation to examine the impacts on financial performances. The results suggest regional diversification can be either positively or negatively moderate the relationships between environmental management

and financial performances, and it depends on whether the benefits of internationalization outweigh the costs of internationalization.

In a nutshell, this study provides theoretical support and empirical evidences on the linkages between environmental management, internationalization, and financial performances. Besides, it also contributes to the growing body of evidence that environmental sustainability is becoming increasingly vital to the operations of construction firms, and proper strategic environmental management can enhance a firm’s competitive advantage in the global market.

Keywords: environmental management, internationalization, financial performance, sustainable construction, resource-based view, transaction costs, organizational learning

TABLE OF CONTENTS

Page

ACKNOWLEDGEMENT ... i

ABSTRACT ... ii

TABLE OF CONTENTS ... vii

LIST OF TABLES ... xi

LIST OF FIGURES ... xiii

LIST OF ABBREVIATIONS ... xiv

CHAPTER 1 – INTRODUCTION ... 1

1.1 Overview ... 1

1.2 Background of The Study ... 1

1.2.1 Environmental Issues in Construction Industry ... 2

1.2.2 Emergence of Sustainability Concern in Construction Industry ... 2

1.2.3 Challenges of Environmental Practices in the Construction Industry ... 5

1.2.4 Environmental Management of Construction Firms ... 7

1.3 Problem Statements ... 8

1.4 Research Questions ... 11

1.5 Research Objectives ... 12

1.6 Significance of the Research ... 13

1.7 Scope of the Research ... 13

1.8 Outline of the Thesis ... 14

CHAPTER 2 – LITERATURE REVIEW ... 17

2.1 Sustainable Construction ... 17

2.1.1 Drivers of Environmental Management in Construction ... 18

2.1.2 Environmental Performances, Practices and Strategy of Construction

Firms ... 21

2.2 Environmental Management and Firm Performances... 26

2.2.1 Measures of Environmental Proactivity ... 26

2.2.2 Environmental Disclosures and Content Analysis ... 27

2.2.3 Resource-Based View on Competitive Advantages of Environmental Management ... 30

2.2.4 Relationship Between Environmental Management and Financial Performance ... 35

2.3 Internationalization ... 39

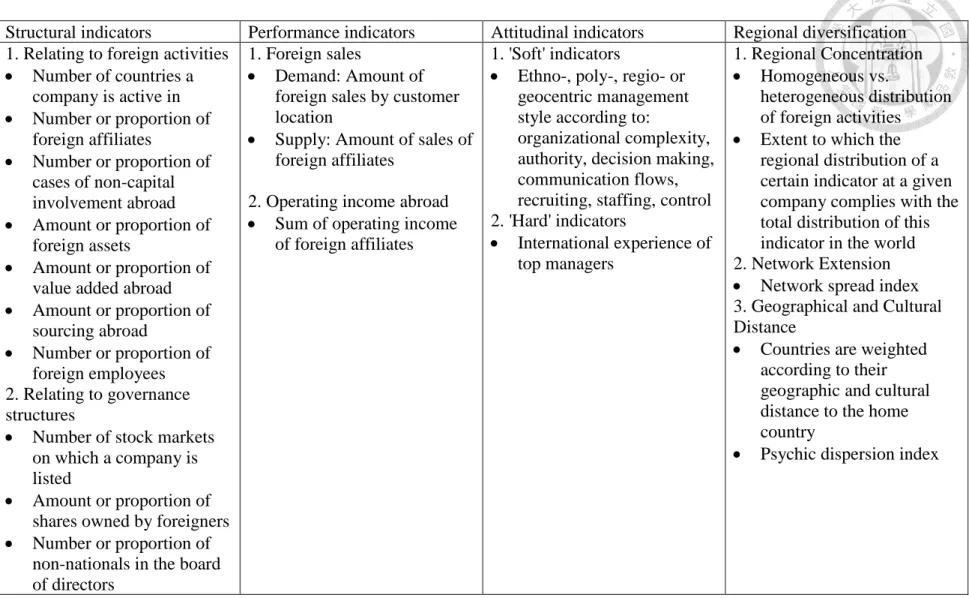

2.3.1 Dimensions of Internationalization ... 41

2.3.2 Internationalization and Firm Performance ... 44

2.3.3 Relationship Between Environmental Management and Internationalization ... 49

2.4 Moderating Effects of Geographical Diversification on Environmental-Financial Performances ... 53

2.4.1 Environmental Scanning ... 54

2.4.2 Process-Related Pollution Abatement ... 57

2.4.3 Environmental Innovation ... 61

2.5 Summary of Literature Review ... 65

CHAPTER 3 – METHODOLOGY ... 67

3.1 Introduction ... 67

3.2 Samples ... 69

3.3 Content Analysis ... 70

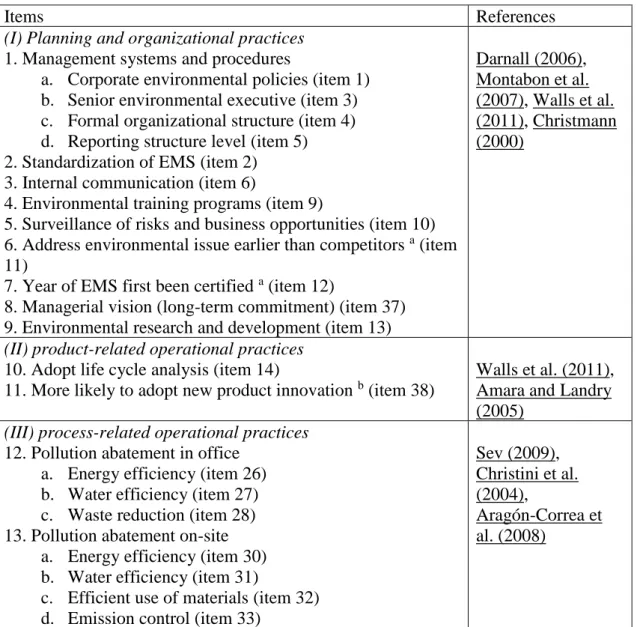

3.3.1 Construct of Environmental Strategy ... 92

3.3.2 Construct of Environmental Management Practices ... 95

3.4 Other Variables ... 97

3.4.1 Degree of Internationalization ... 97

3.4.2 Financial Performances ... 99

3.4.3 Control Variables ... 101

3.5 Analysis ... 102

3.5.1 Analysis of Variance (ANOVA) and Other Extension Methods ... 102

3.5.2 Stepwise Regression ... 103

3.5.3 Moderated Regression Analysis ... 104

CHAPTER 4 – ENVIRONMENTAL STRATEGIES AND INTERNATIONALIZATION ... 106

4.1 Introduction ... 106

4.2 Validity and Reliability of Environmental Strategy Constructs ... 106

4.3 Linkage Between Environmental Strategy and Degree of Internationalization ... 111

4.4 Environmental Strategy and Internationalization Portfolio ... 118

4.5 Discussion ... 119

4.6 Summary of Findings ... 123

CHAPTER 5 – ENVIRONMENTAL MANAGEMENT PRACTICES AND FINANCIAL PERFORMANCES ... 124

5.1 Introduction ... 124

5.2 Validity and Reliability of the Content Analysis and Constructs ... 124

5.3 Stepwise Regression on Environmental Management Practices and Financial Performance ... 129

5.3.1 Robustness of Stepwise Regression Analyses ... 129

5.3.2 Results of Stepwise Regression Analysis ... 131

5.4 Discussion ... 134

5.5 Summary of Findings ... 140

CHAPTER 6 – MODERATING EFFECT OF INTERNATIONALIZATION ... 141

6.1 Introduction ... 141

6.2 Robustness of Moderated Regression Analysis ... 142

6.3 Result of Moderated Regression Analysis ... 145

6.4 Discussion ... 148

6.5 Summary of Findings ... 155

CHAPTER 7 – CONCLUSIONS AND RECOMMENDATIONS ... 157

7.1 Research Findings and Implications ... 157

7.1.1 Implications of Environmental Strategies on Internationalization ... 158

7.1.2 Implications of Environmental Management Practices on Financial Performances ... 159

7.1.3 Implications of Moderating Effects ... 161

7.2 Limitations of the Study ... 162

7.3 Recommendations for Future Work ... 165

REFERENCES ... 168

APPENDICES ... 193

Appendix A: Top 225 International Contractors List ... 193

Appendix B: Code Form ... 199

Appendix C: Code Book ... 208

LIST OF TABLES

Table no. Page

2.1 Subjects of study and references... 18

2.2 Internationalization indicators ... 45

3.1 Sample of firms... 70

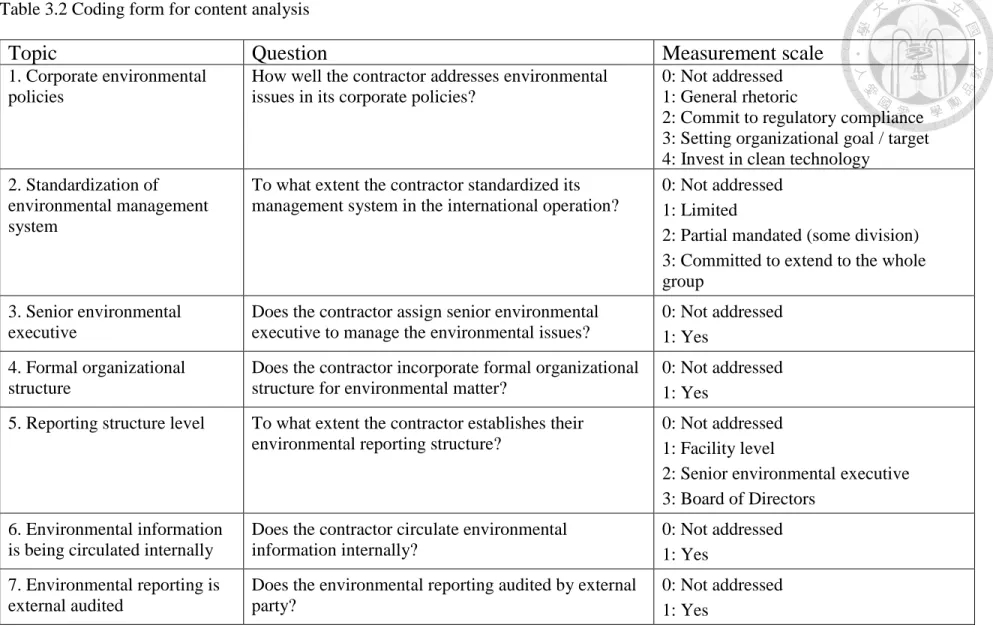

3.2 Coding form for content analysis ... 75

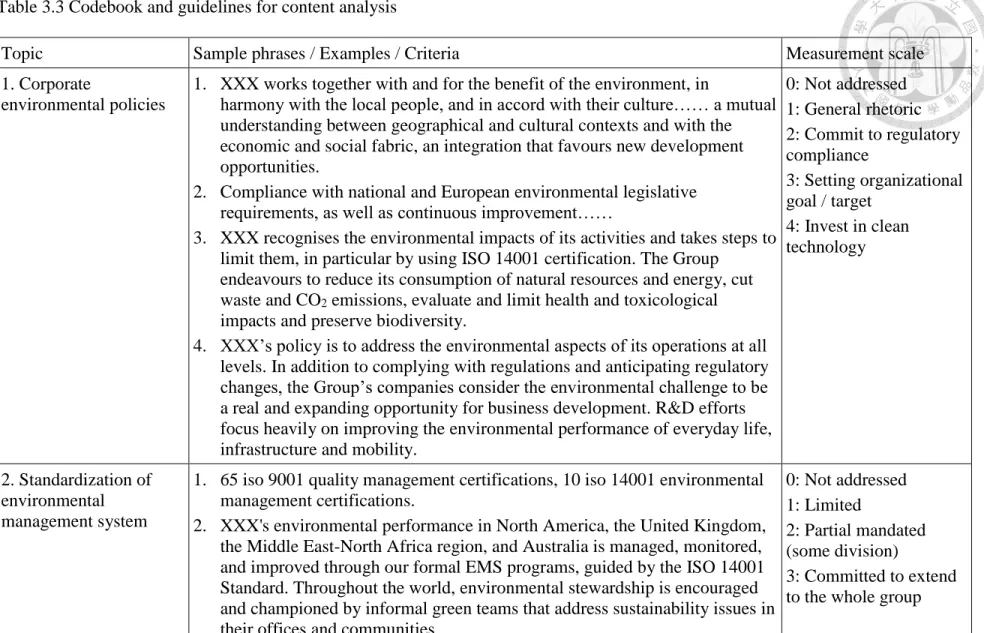

3.3 Codebook and guidelines for content analysis ... 82

3.4 List of coding items and constructs of environmental management practices ... 96

3.5 Financial performance variables ... 101

4.1 Reliability of content analysis ... 107

4.2 Construct validity... 107

4.3 Descriptive statistics of environmental strategy clusters ... 110

4.4 Descriptive statistics of firm revenue profile... 112

4.5 Effects of internationalization under three environmental strategy clusters ... 114

4.6 Pairwise comparison of environmental strategy clusters (for ANOVA) ... 116

4.7 Effects of internationalization under different environmental strategy clusters, and accounting for covariates ... 117

4.8 Paired sample t-tests for comparison of internationalization within environmental strategy cluster ... 119

5.1 Reliability of content analysis ... 125

5.2 Construct validity... 127

5.3 Descriptive statistics and correlations ... 130

5.4 Variance inflation factor (VIF) test ... 130

5.5 White test and Ramsey test ... 131

5.6 Stepwise regression analysis on financial performances (61 samples) ... 134

6.1 Summary of models ... 142

6.2 Descriptive statistics and correlations ... 143

6.3 Variance inflation factor (VIF) test ... 144

6.4 White test and Ramsey test ... 144

6.5 Regression analysis on short term financial performances ... 146

6.6 Regression analysis on long term financial performances ... 147

LIST OF FIGURES

Figure no. Page

2.1 Increasing competitive advantages ... 23

2.2 Implementation framework of sustainable construction... 23

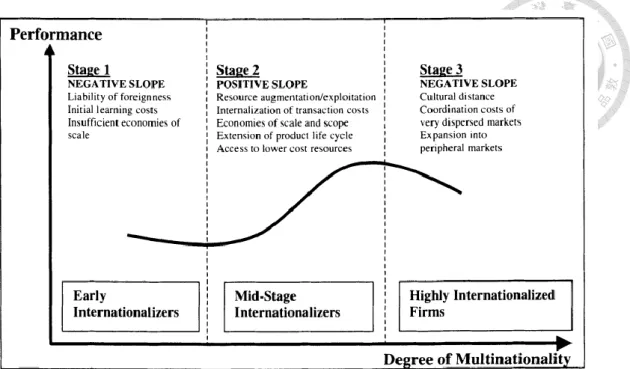

2.3 A three-stage sigmoid (S-shaped) hypothesis... 49

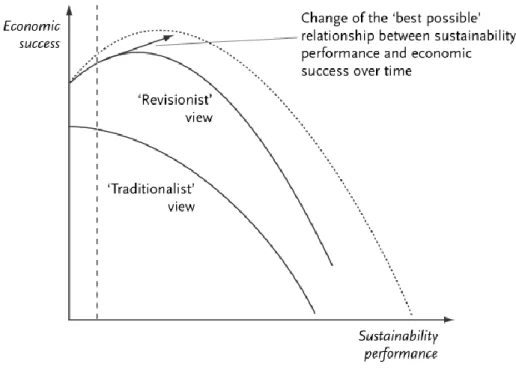

2.4 Illustration of relationship between sustainability and economic performance ... 59

3.1 Research process framework ... 69

4.1 Revenue profile of multinational construction firms ... 113

4.2 Number of firms and number of countries a firm deployed ... 114

6.1 Moderating effect of RDI on the relationship between pollution abatement and ROA ... 150

6.2 Moderating effect of RDI on the relationship between environmental scanning and ROA ... 152

6.3 Moderating effect of RDI on the relationship between environmental scanning and Tobin’s Q ratio... 152

6.4 Moderating effect of RDI on the relationship between environmental innovation and revenue growth ... 154

LIST OF ABBREVIATIONS

ANOVA Analysis of variance ANCOVA Analysis of covariance

EMS Environmental management system

ENR Engineering News Record

FSTS Foreign Sales to Total Sales MANOVA Multivariate analysis of variance MANCOVA Multivariate analysis of covariance test

MNE Multinational Enterprise

NSI Network Spread Index

ROA Return on assets

ROS Return on sales

RDI Regional Diversification Index

VIF Variance Inflation Factor

CHAPTER 1 INTRODUCTION

1.1 Overview

Growing attention to environmental protection has triggered drastic changes in the corporate practices of construction firms. Several studies have shown that multinational construction firms have been relatively proactive in environmental management and there are ample evidences indicate environmental management is crucial for business success in the international market. This study target on environmental management implemented by multinational construction firms and the its associated firm performances.

This Chapter discusses the background study, problem statements and research objectives. This Chapter also discusses the significance and scope of the research. The last part of this Chapter discusses the thesis outline for this research study.

1.2 Background of the Study

Commitment to the natural environment has become an important issue in the construction industry. Owing to the severe environmental impact of construction activities, advocates of sustainable construction strive to incorporate sustainable development principles into conventional construction practices and to accelerate the transformation of organizational management in construction firms.

The advancement of the concept “sustainable development”, first introduced in 1987 (Brundtland, 1987), can be witnessed with the subsequent emergence and adoption of environmental practices or standards either related to production (life cycle analysis,

system) in construction industry. Many studies have highlighted the drivers, drawbacks, and benefits of the implementation of these new practices, with some drawing attention to the strategic implications of adopting such practices (Fergusson and Langford, 2006;

Tan et al., 2011).

1.2.1 Environmental Issues in Construction Industry

In the United States, approximately 43% of carbon dioxide emissions result from the energy services consumed by residential, commercial, and industrial buildings (Brown and Southworth, 2008), while the construction industry itself consumes about 42% of materials entering the global economy in 2010 (OECD, 2015).

Green or ecologically sustainable construction is important because creating and operating buildings are matters that account for about 40% of global annual energy consumption (Greenwood et al., 2007; Kibert, 1994), almost 40% of the global material deployment and also 25% of global waste (Bossink, 2011; Ding, 2008; Nelms et al., 2007;

Ofori and Kien, 2004; Roodman et al., 1996; Vijayan and Kumar, 2005). Therefore becoming market responsive, minimizing waste, integrating the supply chain and engaging all stakeholders should be the aims of the construction industry (Myers, 2005).

1.2.2 Emergence of Sustainability Concern in Construction Industry

Following the emergence of sustainability discussions in the late 1980s including the Brundtland Report (Brundtland, 1987) ecologically sustainable construction has received much attention as a result of major environmental and social impacts created by the construction industry and also its lag with other sectors (Myers, 2005).

The concept of sustainable development can be traced to the energy (especially fossil oil) crisis and the environment pollution concern in the 1970s. The Rachel Carson’s book Silent Spring is considered as one of the first initial efforts to describe this topic.

The classical definition of sustainable development was defined in the Broundland’s Report 1987 as “a development that meets the needs of the present without compromising the ability of future generations to meet their own needs”. The pursuit of sustainable development throws the build environment and the construction industry into sharp relief (Bourdeau, 1999). An unprecedented sustainable construction movement is reshaping the conventional construction sector around in all aspects including planning / programming, design, construction, operation / maintenance, modification / renovation, demolition / deconstruction, financing, insurance, policy, marketing, management, etc (Xiaoping et al., 2009).

Sustainable construction as a concept encompasses the creation and management of a healthy built environment based on resource efficient and ecological principles. The results of the implementation of sustainable construction practices (i.e. building practices) are defined as practices that strive for integral quality in terms of economic, social and environmental performance. Sustainably designed buildings are designed to lessen their impact on the environment and improve environmental quality through: minimization of consumption of non-renewable resources; elimination or minimization of the use of toxins; and reduction of energy consumption (Mokhlesian and Holmén, 2012).

There are several terms about this topic, such as green building, sustainable building, sustainable construction, high performance building, and so on, and these terms are often used interchangeably. In fact, there are essential differences in these terms.

Sustainable construction most comprehensively addressed the ecological, social, and economic issues of a building in the context of its community (Kibert, 2007).

Sustainable/green buildings can be defined as the facilities which are the outcomes of sustainable construction for the purpose of promoting occupant health and resource efficiency, minimizing the impacts of the built environment on the natural ecology system.

In the opinion of Kibert, sustainable/green building is a subset of sustainable construction, representing simply the structure (Kibert, 2004).

Emerging advocacy of sustainable construction aims at incorporating the general sustainable development concepts into conventional construction practices. While the foundation of knowledge in this field is continuously expanding, sustainable construction is not yet standard industry practice. In construction industry however, a slower pace is in response to the environmental issues in contrary to other industries. To be able to reduce, to a minimum, the impact of the organization’s activities on the environment, construction managers must develop management strategies, which allow the matching of the activities of the organization, to the environment in which it operates (Johnston and Scholes, 1993). Moreover, only limited studies have investigated environmental practices as strategic management issue of construction firms which render obscurity on the output of implementation environmental practices.

Unlike financial reporting which have many standardized sources of data available, environmental data suffers for lack of consensus on how information should be presented, what indicators must be used and what their meaning is. In this regard, the problem of content standardization and uniformity was addressed by a number of global standardization associations and environmental non-governmental organizations (Jose and Lee, 2007). International Organization for Standardization (ISO) introduced ISO 14001 guidelines as a way to standardize corporate environmental management system.

United Nations Global Compact lists nine principles focus on human rights, labor rights, environmental sustainability, and corruption for firms to follow. Dow Jones Sustainability

Indexes cover and assess the leading companies with the best corporate sustainability practices. In order to provide a consistent guideline to disseminate environmental information, organizations such as CERES Report from the Coalition for Environmentally Responsible Economics (CERES), the ICC Business Charter for Sustainable Development (ICC), and the Global Reporting Initiative (GRI) have developed and promoting standard reporting practices.

Amidst the above reporting standards, GRI is pioneering among all with sample reporting items and guidelines provided specifically for construction and real estate sector.

70% of top 50 international contractors listed in ENR have reported to document their sustainability commitments in either standalone sustainability report or as a section of their annual report, and 28% have their sustainability report listed by the GRI (Zuo et al., 2012). The engagement of contractors in environmental reporting has provided an access for scholars to explore the environmental practices and performances of construction sector.

1.2.3 Challenges of Environmental Practices in the Construction Industry

The construction industry has long been criticized for its low level of innovation and efficiency. Yet innovation is essential to advance sustainable construction or environmental practices in the construction industry. In order to understand the barrier towards adoption of sustainable construction practices, the unique structures and peculiarities posed by the industry have to be comprehended.

An institutional view towards the construction industry identifies the characteristics of the industry that distinguish it from other industries as the main challenge to the adoption of green construction practices. Nam and Tatum (1988) contend that constructed products carry a high degree of social responsibility towards public safety

and health, which reinforces a greater a sense of conservatism in design and specialization.

This conservative ethos underpins the tendency of construction players to maintain their current practices despite potential innovations related to sustainability that they could otherwise adopt (Ahn et al., 2013). Furthermore, constructed products are one-of-a-kind products, with each project being unique and specific, and with individual challenges and problems, thus limiting the possibilities for production standardization (Vrijhoef and Koskela, 2005). This peculiarity poses challenges to firms in monitoring and normalizing their environmental performance over time, specifically on a year-to-year basis (Christini et al., 2004). In addition, the temporary production organization of construction projects can curtail the motivation to consider environmental impacts, which is predicated upon holding a more holistic and long-term perspective (Gluch and Räisänen, 2012; Vrijhoef and Koskela, 2005).

A structural view invokes fragmented decision processes and interactions across the players as key hindrances to the adoption of green construction practices. A construction project involves collaboration among players such as clients, regulators, architects, the principal contractor, sub-contractors, component suppliers, and different disciplines in engineering, each subject to varying interests and practice codes. These barriers result from the contradictions at the interface between the organization, the project, and the client (Gluch and Räisänen (2012). The argument is further extended to the adaptability problem, in which end users unable to utilize green features beyond what the designer and builder have made available (van Bueren and Priemus, 2002). In addition, it is argued that the uneven distribution of costs and benefits among designers, contractors, clients, and owners can discourage the realization of sustainable construction (van Bueren and Priemus, 2002), which is further frustrating if the environmental practices incur extra costs while not fully recognized by the government and clients (Ofori et al., 2000). The

extra costs can in part arise from the additional communication and coordination needed between different specialized disciplines, and the uncertainties involved when new sustainable construction concepts are introduced into the project (Demaid and Quintas, 2006). Environmental management often evokes conflicts between environmental performance and contract time and construction costs, a stalemate that could only be resolved when the government enacts new policies and incentives to shift the traditional paradigm of project organization (Zhang et al., 2014).

Neglecting this context would lead to insufficient consideration of the uncertainties and interdependencies that impede the efficient application of environmental management practices in construction.

1.2.4 Environmental Management of Construction Firms

Previous environmental management studies of construction firms can be divided into two primary categories. The first category emphasizes the technical aspects, implementation, and consequences of new environmental practices from a project-level perspective. The second category examines how these new practices necessitate major changes in the structure and production of construction firms (Ahn and Pearce, 2007), leading to a reorientation of business models and value creation (Mokhlesian and Holmén, 2012), thus having a focus more from a firm-level perspective.

In construction industry, the growth of sustainability services in the sector has been characterized by a distinct global unevenness; relative economic prosperity in the developed world has afforded market and policy expansion whilst developing countries have been unable to prioritize sustainability in the same way (Preece et al., 2011).The distinctive impetus of internationalization would have drawing the multinational construction firms towards different environmental strategic setting.

Construction firms recognize that reducing environmental risk, improving their environmental image, and saving on costs are among the benefits of environmental management (Shen and Tam, 2002). The adoption of environmental management system ISO14001 is also perceived to entail a synergy effect in entering the international construction market (Turk, 2009; Zeng et al., 2003). A study on Korean contractors concluded that global contractors are more proactive in environmental strategies than their local counterparts (Park and Ahn, 2012). Zuo et al. (2012) also indicated a high commitment of environmental reporting among international contractors. Yet, there have been no studies from the strategic environmental management perspective that articulate the interplay between a multinational contractor’s internationalization characteristics and its environmental practices.

1.3 Problem Statements

Despite there are number of studies on environmental management in other industries, particularly in the manufacturing industry, generalization to the construction industry might be limited due to the unique structures and peculiarities posed by the industry.

Unlike other industries, it is reported that construction industry exhibits a very low level of innovation (Seaden and Manseau, 2001). Many construction firms do not need to innovate in order to remain successful or viable since they are able to sustain themselves by meeting local needs, responding to regulations and drawing new technologies from their suppliers and customers (Reichstein et al., 2005). The conservatism and non- innovative behavior in construction industry raise the question whether it would be profitable for proactive in managing environmental issues like some other industries.

Besides, construction projects are complex processes and involve multiple players. Thus, the environmental information of a firm is usually dispersed across numerous players

inside and outside the firm. Unless there is an established and formal channel to gather, consolidate, and circulate environmental information, it is very challenging to obtain reliable data.

The construction industry has the highest rate of certified ISO 14000 among all industries (Marimon et al., 2011), yet construction firms are seldom sampled and studied for their business performance in the environmental management literature. The construction industry differs from manufacturing and service industries on many aspects, including the products offered, the market segments served, technology, completion structure, capital and labor market variations, and the ecological impacts of the products (Zutshi and Creed, 2014). The construction industry’s project-based business nature is different from other business models due to its limited time frame and often one-off project, involvement of adversarial relationships among actors, separation of design and production, competitive tendering, high degree of uncertainty, and standardization difficulty (Mokhlesian and Holmén, 2012). These distinguishing characteristics should be taken into account when considering how construction firms could benefit from pursuing proactive environmental management.

For construction firms, one of the perceived main impetuses to develop an environmental management system is the synergy effect when entering the international construction market (Zeng et al., 2003). A study on Korean contractors concluded that global contractors are more proactive in environmental strategies than their local counterparts (Park and Ahn, 2012). Zuo et al. (2012) also indicated a high commitment of environmental reporting among international contractors. However, recent environmental strategy studies in the construction industry (Fergusson and Langford, 2006; Park and Ahn, 2012; Tan et al., 2011), have not addressed the impacts of environmental proactivity on internationalization. It remained questionable whether

proactive environmental management strategy help construction firms in their global expansion. In addition, if the linkage between environmental management and internationalization exist, one should also understand whether construction firm would enjoy the benefits of environmental management in different regions across the world.

Multinational construction firms usually exhibit higher proactivity and compliance in environmental management practices than domestic firms (Park and Ahn, 2012). The proactiveness of multinational construction firms are articulated with greater availability of slack resources which give the firm leeway in managing environmental issues as opportunities rather than a threat (Aguilera-Caracuel et al., 2011). While, some environmental management practice would have affected firm financial performance, it is arguably these relationships are moderated by multinationality of a firm.

There are ample evidence that proactive environmental strategies are likely to be accompanied by improved financial performance, however it is crucial to understand why only some firms in an industry implement such strategies (Sharma et al., 2007) and what are the circumstances which environmental practices could contribute to competitiveness (Christmann, 2000). One of the attempts to answer pertaining to why some only some firms are more competitive through implement proactive environmental strategy while others are not, scholars have devoted to perform an integrated analysis of the influence of exogenous variables on organizational capabilities (Sharma et al., 2007), and how such variables have a moderating effect on organizational capacity and firm performances.

However, limited studies have underscored internationalization as a moderator on the relationship between environmental management practices and firm performances.

In a nutshell, this study addresses the imperatives to understand the limitations of previous studies which rendered several unclear outcomes on environmental management implemented by multinational construction firms. Through empirical study, this study

aims to answer how environmental management relates with the financial implications and international strategic management.

1.4 Research Questions

The specific research questions and research hypotheses are listed as followings:

(i) What types of environmental management practices are disclosed in the environmental reporting of multinational construction firms?

(ii) Does environmental strategy have any influence on the internationalization of a multinational construction firm?

(iii) If environmental strategy has impacts on internationalization, in which dimension that internationalization is affected by environmental strategy?

(iv) Does the environmental strategy adopted by a firm would influence its business distribution portfolio across developed and developing regions?

(v) Which of these reported environmental management practices are associated with the short-term and long-term financial performance of the firms?

(vi) Do degree of internationalization (regional diversification) moderates the relationship between environmental management practices and financial performances?

Based on research question (vi), following hypotheses have been derived in Chapter 2:

Hypothesis 1a: Regional diversification negatively moderates the relationship between environmental scanning and short term financial performances.

Hypothesis 1b: Regional diversification negatively moderates the relationship between environmental scanning and long term financial performances.

Hypothesis 2: Regional diversification positively moderates the relationship between process-related pollution abatement practices and short term financial performances.

Hypothesis 3: Regional diversification negatively moderates the relationship between environmental innovation and short term financial performances.

1.5 Research Objectives

The objective of the work reported in this thesis aim to enhance the understanding of environmental management practices implemented by multinational construction firms, and the impacts of environmental management on their international expansion and financial performances. Besides, this study attempts to adopt both strategy and multi- dimensional practices classification of environmental management in the analysis of environmental-firm performance relationships. More specifically, the research objectives of this study can be summarized as follows in response to the research questions stated in section 1.4:

(i) Identify the environmental management practices and strategy typologies implemented by multinational construction firms.

(ii) Explore the relationship between environmental strategy and degree of internationalization in multinational construction firms.

(iii) Investigate the firm geographical distribution portfolio across developed and developing regions based on the environmental strategy deployed by multinational construction firms.

(iv) Examine the relationship between environmental practices and the financial performance of multinational construction firms.

(v) Examine the moderating effect on the relationship between environmental practices and the financial performance of multinational construction firms.

1.6 Significance of the Research

Given the peculiarities of construction firms and the difficulties in obtaining environmental information in the construction industry, very few studies have examined the interplay between environmental management and business performance from a firm- level perspective. This study contributes to the literature in two-fold, first it highlights the financial implications of environmental management practices in the context of construction firms. The study attempts to empirically evidence the linking of environmental management to the financial performance from a theoretical competitive perspective, and establish the interaction factor of internationalization on the relationship between environmental management and financial performances. Second, for the practical purpose, the study exemplifies the required strategic resources and capabilities, in which a multinational construction firm could financially benefit from environmental management and international strategic planning.

1.7 Scopes of the Research

Based on the objectives, the scopes of this research have focused on:

(i) Environmental information of construction firms is sourced from environmental disclosures published by each construction firm. Due to language proficiency, only reports in English and Mandarin were accepted. The environmental data were gathered from sustainability reports, corporate social responsibility reports, online annual reports, and public information on company webpages. The main targets were environmental reports published in 2011. Therefore, the environmental information is subjected to the content availability in the disclosure and limited the selection of study samples.

(ii) The sample of multinational construction firms is drawn from ENR Top International Contractors 2012 (ENR, 2012). Only publicly listed firms from developed countries, with financial data available and environmental reporting published online, are included in the study.

(iii) While there is plenty influencing exogenous variables which adopted in the literature, not all of these variables which can be adopted as control variable are included in the study due to difficult to collect such information from the multinational construction firms that scattered across the globe. Primarily, the data is collected through content analysis method and based on secondary data disclosed in Datastream financial database.

(iv) In order to maintain consistency across different measure used in coding environmental management practices and to avoid confounding effects in the statistical analysis of financial data, most of the results are interpreted based on standardized values. Therefore, the results are best used to understand the relationship between the variables and not recommend for prediction purpose.

1.8 Outline of the Thesis

The introduction of this study, including the problem statements and objectives have been discussed in Chapter 1.

Chapter 2 provides an overview regarding the development of sustainable construction and previous studies that related to environmental management and internationalization. The literature review on environmental management are not limited to studies related to construction industry, but also include ample findings and management theory learned from business management domain. Based on the critical

review, the study proposed four hypotheses that connects moderating effect of internationalization on environmental management practices and financial performances.

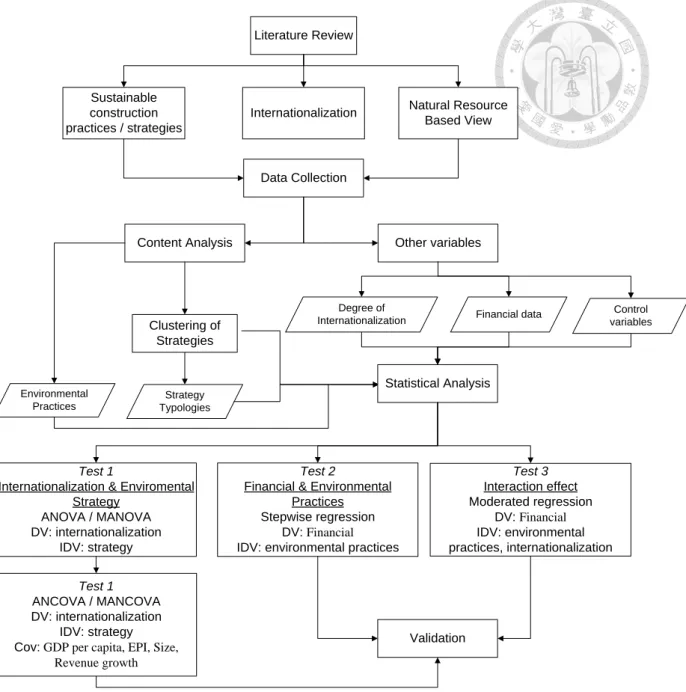

Chapter 3 depicts the methodology adopted in the study. This chapter brief on the research framework, sample used in the study, the data required to proceed for analysis, and the source of data. Besides, this chapter also expound the procedures and requirement to deploy K-means clustering, exploratory factor analysis, and content analysis. Three types of analysis methods have been expounded with details, include (i) Analysis of variance (ANOVA) and other extension methods, (ii) stepwise regression analysis, and (iii) moderated regression analysis. Last but not least, types of reliability and validity checking have been clarified in each respective section of analysis method.

Chapter 4 presents the ANOVA results of environmental strategies and internationalization. The results include: (i) three types of environmental strategy categorized based on K-mean clustering method and their construct validity, (ii) the results pertaining to the relationship between environmental strategy and degree of internationalization, (iii) the linkage between environmental strategy and internationalization portfolio of multinational construction firms across developed and developing countries.

The subsequent Chapter 5 discusses the financial implication of environmental management practices adopted by multination al construction firms. Stepwise regression is used to filter associated environmental management practices that significantly related to short and long term performances.

Chapter 6 presents the results and discussion of moderating effects of regional diversification on the relationships between environmental management practices and financial performances. The results of moderated regression are used to examine the four

hypotheses posited in Chapter 2. The implication of the moderating effects is further explained in the discussion section.

Chapter 7 discusses the overall findings of this research. The limitations and future works of the research are reported accordingly in the last section of this Chapter.

CHAPTER 2

LITERATURE REVIEW

2.1 Sustainable Construction

Following the emergence of sustainability discussions in the late 1980s including the Brundtland Report (Brundtland, 1987), ecologically sustainable construction has received much attention as a result of major environmental and social impacts created by the construction industry. The classical definition of sustainable development was defined in the Brundtland Report 1987 as “a development that meets the needs of the present without compromising the ability of future generations to meet their own needs”. An unprecedented sustainable construction movement is reshaping the conventional construction sector around in all aspects including planning / programming, design, construction, operation / maintenance, modification / renovation, demolition / deconstruction, financing, insurance, policy, marketing, management, etc (Xiaoping et al., 2009).

As yet there is little publication that analyses green construction explicitly from a business model perspective. This implies that the understanding of these processes is poor at best. Fortunately, there are a number of papers that describe or analyze green construction where changes in firms’ business models can be inferred. Thus, the purpose of this section is to review recent green construction publications to investigate what elements of the business model change when a construction-related company undertakes green construction, and ascertain whether there are any specific relations between changes in different business model elements. Table 2.1 shows the references of subjects of study in the literature.

Table 2.1 Subjects of study and references

Subjects of study References

Strategy and business modal Fergusson and Langford (2006); Tan et al. (2011);

Mokhlesian and Holmén (2012); Park and Ahn (2012)

Sustainable construction Pitt et al. (2009); Manoliadis et al. (2006) Environmental management

system

Qi et al. (2010); Ball (2002); Kein et al. (1999);

Ofori et al. (2000); Shen and Tam (2002); Zeng et al. (2003); Christini et al. (2004); Valdez and Chini (2002)

Sustainable building Ahn et al. (2013); Häkkinen and Belloni (2011);

Xiaoping et al. (2009); Bunz et al. (2006) Corporate social responsibility

disclosure

Martinuzzi et al. (2011);Myers (2005);Jones et al.

(2006)

Green Procurement Riley et al. (2003); Ofori (2000); Rwelamila et al.

(2000); Ngowi (1998)

2.1.1 Drivers of Environmental Management in Construction

In construction industry, several researches conducted on environmental study highlighted on the motivation of implementation sustainable construction, environmental management ISO 14001, and sustainable building. These studies are geographically constrained in nature, however they are able to provide some understanding from the responses of the industry.

Manoliadis et al. (2006) has identified there are 15 potential drivers that would propel a change toward sustainable construction practices, including: energy conservation,

waste reduction, indoor environmental quality, environmentally-friendly energy technologies, resource conservation, incentive programmes, performance-based standards, land use regulations and urban planning policies, education and training, re- engineering the design process, sustainable construction materials, new cost metrics based on economic and ecological value systems, new kinds of partnerships and project stakeholders, product innovation or certification, and recognition of commercial buildings as productivity assets. These driving forces for the construction firms to adopt different environmental practice can be further categorized into organizational concern, operational efficiency, competitiveness, market incentives, regulation compliance or risk aversion, and social responsibilities.

For organizational concern, construction firms initiate environmental practices by examining the organizational governance condition and its original management system, subsequently take effort to integrate new environmental practices when the internal conditions are fulfilled. The exemplary quotation of organizational concern are organizational condition that enable staffs to voice ideas and proposals; enabling condition to integrate new environmental strategy; environmental impact from prosecution or other adverse public reaction; and firm size (Fergusson and Langford, 2006). Qi et al. (2010) highlighted managerial concern is the most important driver for the adoption of green practice and business size is another concerning factor.

Firms that adopt environmental practices for improvement of operational process and managerial process are operational efficiency seeker. Energy conservation, resource conservation, waste reduction, improving indoor environmental quality, and environmentally friendly energy technologies are highlighted as motivation for changes (Ahn et al., 2013; Häkkinen and Belloni, 2011; Manoliadis et al., 2006). Ofori et al. (2000) in his study of implementation of ISO 14001 in Singapore, identified operational

efficiency factors such as enable company to reduce material wastage, help to enhance company’s productivity, reduce company’s operating costs and improve company’s procedures. Zeng et al. (2003) emphasized the potential of improvement in management.

As a matter of competitiveness, construction firms taking strategic responses in order to expand the market sharing in the industry and ease competitive pressure from their competitors. Several scholars contend reputation and corporate’s image as the main drivers of sustainable construction practice (Fergusson and Langford, 2006; Ofori et al., 2000; Shen and Tam, 2002). The competing pressure in field (Christini et al., 2004; Ofori et al., 2000; Valdez and Chini, 2002), as well as expansion and entry to foreign market (Zeng et al., 2003) are able to create impetus for the practice change in a firm.

Pitt et al. (2009) asserted the market incentives as the strong impetus for promoting sustainable practices in the field. The scholars’ study focused on factors that best promote or prevent sustainable construction practices and establish the consistency of how sustainability is measured. In their study through questionnaire surveys, financial incentives, building regulations, client awareness, client demand, planning policy, taxes/levies, investment, and labelling/measurement has been identified as main drivers in a decreasing order.

Regulation compliance or risk aversion is the most mentioned factor driving construction industry to sustainable development. The importance of regulation stem on the ability of coercive pressure to transform and compel the changing of construction activities. Almost every scholar in literature studies agreed that the regulation motivate sustainable practice (Fergusson and Langford, 2006; Kein et al., 1999; Manoliadis et al., 2006; Ofori et al., 2000; Pitt et al., 2009; Qi et al., 2010).

A few studies indicate that firms might adopt sustainable practices to account for the social benefits. Construction firm might change their practice to help improve workers’

health, safety and welfare, and contribute to efforts to protect the environment (Ofori et al., 2000). Besides, the sustainable practices also contribute to environmental protection and able to improve the public environmental standards (Shen and Tam, 2002). Myers (2005) contended the main purpose of corporate social responsibility (CSR) reporting is to inform stakeholders of a company’s environmental, social and economic performance.

However, Qi et al. (2010) in their study of contractors’ green innovation (change), indicated that perceived stakeholders’ pressures have no significant relationship with the adoption of green construction practices.

2.1.2 Environmental Performances, Practices and Strategy of Construction Firms The environmental management studies of construction have shed light on firm level as well as project management level. Firm perspective studies usually focus on aspects of environmental management that would influence the arrangement of firm’s function which aim is to sustain business or create value. As highlighted by Mokhlesian and Holmén (2012), a firm has to consider to change their business model elements since engaging in sustainable construction might alter how it create value and generate profit from changing the environmental orientation of their businesses. A firm perspective studies would encompass the functions of strategic management, environmental management system, operational practices such as green innovation of construction process and building, stakeholder engagement, and procurement system etc.

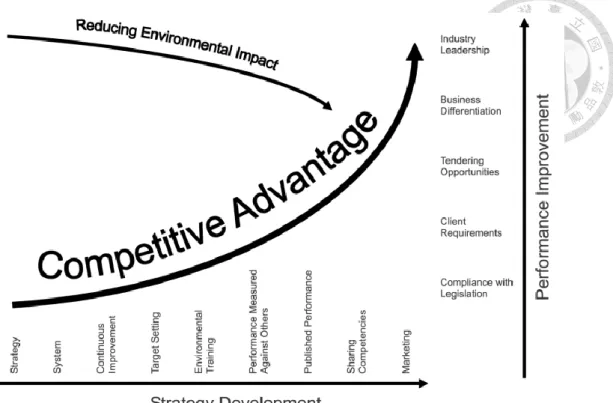

In respect of environmental strategic management, Fergusson and Langford (2006) grounded environmental practices of construction firms into 7 themes which consist of (i) policy, (ii) management status, (iii) management integration, (iv) monitoring, (v) training, (vi) environmental performance, and (vii) sharing skill. Furthermore, the environmental competencies are shown to evolve over business performance and environmental

performance improvement (Figure 2.1). Identically, Tan et al. (2011) proposed a guiding framework (Figure 2.2) to assist contractors improving their competitiveness by implementing sustainable construction practice on a continual improvement basis.

According to Park and Ahn (2012), environmental strategy of construction firms could be classified into four typologies: “exemplary,” “infrastructure-oriented,” “technology- oriented,” and “passive” which based on a firm’s technological power and implementation abilities.

Environmental management system typically consists of policies, goals, information systems, task lists, data collection and organization, emergency plans, audits, regulatory requirements, and annual reports (Christini et al., 2004). The system is implemented to address an organization’s environmental impacts and formulate proper framework to improve its environmental performance. A standardized EMS was introduced by International Standardization Organization (ISO) in 1996 and coded as ISO 14000 series of standards. It is a widely recognized standard system which aimed for continual improvement of organization–level environmental performance (Turk, 2009).

According to the current studies on ISO 14001, the certification can set up on firm level organization, construction project or site as a temporary organization. The benefits of adopt EMS or ISO 14000 are attributed to the contribution of environmental protection, minimize environmental risk, improve environmental image, cost saving, facilitate entry into international market, better on-site housekeeping etc. (Shen and Tam, 2002; Turk, 2009; Zeng et al., 2003).

Figure 2.1 Increasing competitive advantages (Adopted from Fergusson and Langford, 2006)

Figure 2.2 Implementation framework of sustainable construction (Adopted from Tan et al. 2011)

Green innovation is a vital element to create firm’s competitive advantage. Qi et al. (2010) asserts green innovation is composed of management innovation and technology innovation. The former refers to implementation of (i) ISO 14000, (ii) OHSAS 18001, and (iii) conduct research and development; whereas the latter highlights implementation of (i) investment in green equipment and technology, (ii) material saving, (iii) energy-saving, (iv) water saving, (v) land saving, (vi) noise controlling, (vii) waste abatement, and (viii) air pollution controlling. Through acquisition, assimilation, and transformation, construction firms could develop their capability to absorb green innovations and improve business performance (Gluch et al., 2009).

Nonetheless, commitment on environmental management practices usually are motivated by various source of stakeholder’s pressure and managerial concern. Thus, construction would require capability of stakeholder engagement in order to integrate stakeholder environmental perspectives into design and construction. Firm required to communicate their construction project performance with stakeholders in regards of environmental impacts and how the impacts adding value to society (Walker, 2000).

Besides, government pressure and managerial concern are driving construction firm’s green innovation (Qi et al., 2010), and financial stakeholders have increasingly engaged in financing sustainable building related activities (Lützkendorf et al., 2011).

Environmental sustainability of construction is relied on the proficiency of client in formulating relevant green specifications in the contracts and develop the procurement process (Sterner, 2002). Some examples of green specification in contract include using of recycled materials, reduction of construction waste and demolition, adopt green building design, employ contractor or consultant who possess an EMS certification, and underline project specific environmental requirement etc. (Lam et al., 2009; Varnäs et al., 2009). However, proper green supply chain should be established to ensure reliable and

flexible supply of services or materials from the standard distribution network (Lam et al., 2009).

Empirical studies on the potential financial implications of environmental management in construction firms are limited. Instead of directly analyzing firm-specific environmental management practices, previous studies resort to sustainability indices or adopt binary classifications of green versus conventional firms to measure environmental performance and investigate its impact on financial performance (Lu et al., 2013; Tan et al., 2015). Yet, both these studies denote green construction firms would expect better business performance than their counterparts.

On the other hand, the goal of environmental management practices at project scope are aimed to at least meet the requirement of environmental regulations (Gluch and Räisänen, 2012). The principals of sustainable construction practices are stemmed on resource management, life cycle analysis, and design for human (Sev, 2009). Common environmental practices in a construction project encompasses efficient use of energy and water, reduce, reuse and recycle of material, waste management, stormwater runoff and erosion control, dust control, noise control, preservation of land and ecology etc.

(Christini et al., 2004; Sev, 2009). Commitment also has been laid down on eco-labelling scheme for sustainable buildings (Ball, 2002). Some of the well-known eco-labelling guideline standards are LEED standard from United States, BREAM standard from United Kingdom, and GBTool from Canada. These standards underscore cradle-to-grave design approach and recognizes environmental consequences of the entire life cycle of the building which cover phases of programming, design, building construction, building operation, and finally building demolition (Bunz et al., 2006).

2.2 Environmental Management and Firm Performances 2.2.1 Measures of Environmental Proactivity

González-Benito and González-Benito (2005) contended two classifications of environment management studies, namely one-dimensional and multi-dimensional studies. One-dimensional studies assume environmental practices can be reduced to a single factor and follow a linear path towards higher level of proactive environmental management, for example the classification of environmental strategies by Hart (1995) and Buysse and Verbeke (2003b) which underscore embeddedness and path dependence.

In contrary, multi-dimensional studies consider that there is no single path towards proactivity and the diversity of existing environmental management practices gives rise to different manifestations of strategic proactivity.

Several studies taken multi-dimensional perspective suggests measurement of environment proactivity should account for comprehensive set of environmental management practices (González-Benito and González-Benito, 2005; Montabon et al., 2007). For example, environmental practices can be distinguishable in three categories:

planning and organizational practice; operational practices; and communicational practices (González-Benito and González-Benito, 2006), and can exert certain positive effects on performance based on portfolio of environmental practices that has been implemented (González-Benito and González-Benito, 2005). Montabon et al. (2007) covered a broad range of environmental practices in his studies. From the initial 48 sets of environmental practices, the study suggested recycling, waste reduction, remanufacturing, environmental design, and surveillance of market have positive effects on firm growth and innovation offset. Amidst the approaches for pollution reduction, King and Lenox (2002) purported only waste prevention approach leads to financial gain but not waste generation, waste treatment, and waste transfer.

Through a review, Albertini (2013) found that environmental management variables, environmental performance variables, and environmental disclosure variables are three categories of environmental measures that adopted in the environmental- financial relationship studies. In comparison, qualitative environmental variable (environmental rating) is more likely to find a positive impact on environmental-financial relationship than adopting a quantitative environmental variable (such as the volume of waste generated or the amount of air emissions) (Horváthová, 2010). However, environmental data is hard to source. Amidst environmental data that are available, U.S.

TRI, and Kinder, Lydenberg, and Domini (KLD) are two sources that most widely adopted in firm’s environmental studies (Etzion, 2007). Lack of environmental data has leads many researchers to employ surveys, conduct case studies, and recently a new alternative is to source environmental data from firm’s environmental reporting or disclosure (Etzion, 2007).

2.2.2 Environmental Disclosures and Content Analysis

Unlike financial reporting, which has many standardized sources of data available, environmental data suffers a lack of consensus on how information should be presented, what indicators should be used, and how they are interpreted. In order to provide consistent guidelines for disseminating environmental information, international voluntary organizations have developed and launched reporting frameworks to guide as well as promote corporate reporting standards. Some of the more prevalent reporting frameworks such as the Global Reporting Initiative (GRI) and the Carbon Disclosure Project (CDP) have contributed to the increased reporting of corporations around the world. Among the various reporting standards that have been advanced, GRI is pioneering the development of the world’s most widely used sustainability reporting framework, due

in part to its success in integrating with other international frameworks and principles such as CDP, the United Nations Global Compact, OECD Guidelines for Multinational Enterprises, and ISO 26000 (Hřebíček et al., 2014). In addition, GRI has provided sample reporting items and guidelines specifically for construction and real estate sectors (Lamprinidi and Ringland, 2008). 70% of top 50 international contractors listed in the ENR have been reported to document their sustainability commitments in either a standalone sustainability report or as a section of their annual reports, and 28% have their sustainability reports listed on the GRI (Zuo et al., 2012). The engagement of contractors in environmental reporting has provided an access point for scholars to explore the environmental practices and performances of the construction sector.

The disclosure of information for environmental reporting generally reflects the importance given by management to environmental issues (Wilmshurst and Frost, 2000), despite the risk that presenting such information might hurt the credibility of the firm if it is perceived as an attempt at greenwashing. Nonetheless, the rich information and progressively standardized reporting formats can establish a clearer context for evaluating the environmental performance of a firm, and provide a valuable source of data for environmental studies (Dragomir, 2012). The voluntarily disclosed information can be presented in three major ways: monetary, quantitative and narrative (Alnajjar, 2000).

Amidst these inconsistencies in reporting, Toms (2002) proposes a more theoretical way to evaluate the environmental information, which is based on the signalling theory. He asserts that a firm that has made genuine and significant environmental investments is more likely to offer the strongest possible quality signals, which are specified, quantifiable, and externally monitored, rather than being simply rhetorical statements.

Content analysis is a common methodology tool for extracting information from environmental reporting, whether the content is manifest or latent (Duriau et al., 2007).

This method reveals manifest content through a number of text statistics, while latent content analysis is more concerned with the underlying meanings implied by the text, which may require more interpretation. In executing qualitative content analysis, Neuendorf (2002) suggests that appropriate measures should be exhaustive, mutually exclusive, and of the highest level of measurement.

Content analyses have been adopted by some scholars in construction management to explore the conceptual meaning behind voluntarily disclosed information.

For example, Jones et al. (2010) employed a quantitative approach, measuring the recurrence of keywords to identify underlying concepts of sustainability within the US engineering and construction industry. Without specifying a particular approach, Zuo et al. (2012) adopted content analysis to investigate the sustainability practices of multinational contractors.

However, the use of environmental reporting and content analysis in econometric studies is quite rare. Some of the relevant studies include the work of Montabon et al.

(2007) and Chen et al. (2015), who use coded environmental management practices to examine correlations between innovation performances and financial performances.

Through the lens of RBV, Walls et al. (2011) conducted a content analysis of text extracted from various voluntary disclosures (environmental reports, corporate web pages, annual reports, etc.) from firms largely in the manufacturing industry, then performed regressions examining relationships between environmental strategy, environmental performance, and financial performance. After subjecting their construct to a battery of tests, they found it to have strong reliability and predictive validity. Nevertheless, our study underlines the predicaments faced particularly by the construction industry, which is largely due to the institutional barriers that make environmental management difficult to disseminate, and information difficult to source, rendering financial implications