‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

1國立政治大學商學院經營管理碩士學程

碩士論文

Center of Excellence –

Finance Share Service Organization in Multinational Company

Hewlett-Packard Corporation

跨國公司共享組織之規劃與結構探討

- 以惠普台灣公司為例

指導教授 : 黃秉德 博士

研究生:林淑真 撰

中 華 民 國 一 百 年 七 月 二十五 日

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

2Abstract

Nowadays, organizations are facing more competitive environment under the impacts of

globalization and rapid technology innovation. How to respond, forecast and keep the competitive

advantage and position become very important and urgent for enterprises to figure out. That impacts

to Finance / Accounting as well. The first challenge is value creation. In order to create value in

global economy, management executive must understand clearly the confluence of economic, social,

and technological forces that drive industry competition. The second challenge is value delivery. It

becomes more urgent and vital for to demonstrate its tangible impacts by aligning with and driving

the issues critical to business to deal with the pressing need. The third challenge is living value for

profession (Wright & Snell, 2005). Finance professional has to rediscover that they are not just

order takers or implementers, but are guardians of organizations. Therefore, how to create more

added-value becomes a very popular topic among Finance fields especially for share-serviced

organizations nowadays. Shared services is the idea that integrating resources in one place to reach

economic of scale and serve the rapid change to all countries of multi-national enterprise in various

regions.

This dissertation takes a qualitative approach to explore how shared-service organizations create

their value by selected case study of multi-national organizations, Hewlett-Packard.

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

3Finance role and responsibilities under the shared service organizations. There are three objectives

in this dissertation. The first objective is the impacts on structure. The second objective is the

impacts on Finance role and value creation. The final objective is delivery channel. Through the

case study of the shared-service organization at Hewlett-Packard (HP), it enables us to have more

understanding how HP creates her organization value and the impacts on resources structure and

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

4論文摘要

論文提頁內容:

在全球化與科技的衝擊下,使現今組織面對更競爭的環境與挑戰。

如何預測變化與保持其競爭優勢對組織而言相當重要且緊急。而外部

環境變化快速也使得財務組織結構遭受到巨大的改變,尤其針對資源

共享組織。現在組織資源遇到的三個挑戰。第一個是價值創造,如何

在經濟、社會、科技的影響下創造價值。第二個挑戰是價值傳遞,透

過何種管道來傳遞價值並符合組織需求。第三個挑戰是人力資源專業

的問題,如何運用專業來引導組織朝向更具競爭力的方向。因此,我

們可以清楚意識到, 如何創造組織價值對公司而言, 是非常重要且迫

切,特別是對資源共享組織而言。資源共享的想法是結合資源到一個

國家,由那個國家來提供地區的服務以達到經濟規模效應。

此論文採個案研究,藉由惠普公司之資源共享組織,來探索資源共

享組織如何創造出價值。

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

5本文結構如下:

第一章探討現今的環境與對組織的衝擊。

第二章舉出相關共享資源組織(功能性、資源共享) 文獻。

第三章為此研究之方法論,主要是以個案研討為主,藉由個案來了解

他們如何規劃與執行共享組織並營造價值。

第四章為個案討論與分析。

第五章為個案變革建議及結論。

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

6Content

Chapter 1 Introduction Content 9

1.1 Why is it important? 10

1.2 Aims and objectives 12

1.3 Disposition 12

Chapter 2 Literature review 13

2.1 Historical perspective vs. Reengineering Essential shared service center 13

2.2 Shifting Finance profile from traditional to innovation 16

2.3 Location Strategy Organization 16

Chapter 3 Research methodologies 18

3.1 Process / structure of this case study 18

3.2 Research limitation 19

Chapter 4 Discussions of the sample case 20

4.1 Introduction of the Hewlett Packard 20

4.2 The Initiation of Finance Transformation Project 21

4.3 Structure the Organizational changes 22

4.4 Supplementary plans to facilitate the transformation 33

4.5 Current Project Status 34

4.6 The value added of shared service model 37

Chapter 5 Conclusions and Suggestions 40

5.1 Comparisons on strategy location structure before and after 40

5.2 Role and responsibility in country vs. center of excellence 41

5.3 Suggestion and recommendations 42

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

7‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

8 TableTable 2-1 Shared Service Center Finance Function Table 4-1 HP APJ proposed vs. current HC in country Table 4-2 cost criteria

Table 4-3 HP Footprint Table 4-4 HP Skills

Table 4-5 HP infrastructure Quality Table 4-6 HP environments

Table 4-7 HP Recommended vs. not recommended location analysis Table 4-8 HP global footprints by function

Figure

Figure 2-1 cost reduction opportunities Figure 2-2 Key factors in location selection Figure 2-3 Top 5 locations by maturity of center Figure 3-1 Case Study Process

Figure 4-1 HP Finance Vision

Figure 4-2 Finance Benchmark Trends

Figure 4-3 HP putting the journey in perspective Figure 4-4 HP Finance work

Figure 4-5 HP Loading model approach Figure 4-6 HP Finance Concept Fan Figure 4-7 HP finance footprint

Figure 4-8 HP site talent management program Figure 4-9 HPCOE progress today

Figure 4-10 HP Taiwan Cost Saving

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

9Chapter 1: Introduction

It has been decades, researchers have attempted to find out main trends that impacts

organization most. The two major factors are globalization and technological change.

Furthermore, it has also pointed out that globalization increased competition among

organizations all over the world and technological change played another driver to

increase competition. The organizations regard globalization as their first concern and

seek to maximize their global presence. With the increase of global presence,

organizations can not only distribute and sell their products widely but also capitalize on

labor-cost advantage. Secondly, with the advanced technology, it enhances organization

to keep more competitive than others.

Facing competition, globalization, and dynamic changes in markets and technology,

organizations need to make more efforts than before in order to survive or make profit in

a very competitive market. We could clearly observe that the structure of organizations

has become much flatter, less bureaucratic, less hierarchical, faster and more responsive

ones in order to survive now and become more competitive in the future. Many

organizations focus on core competence and outsource non-core parts to keep their

competitive advantage. As for Finance department is also undergoing profound changes

right now to sustain business strategy and figure out how to create more value-added

activities to increase Company’s competitive advantage.

From survey conducted by Outsourcing Research Council in 2002, it reports that the

outsourcing market is continuing to grow rapidly and expects to grow to $1,200 billion

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

10tries to integrate resources and focus on strategic part which creates more value and

deduces administrative tasks through outsourcing or other approaches. In this way,

especially for multinational organizations, they get a lot benefits from outsourcing

administrative work at low price or service center to increase their quality of service as

well.

Under more competitive environment, multinational organizations have taken some

measures to respond. For finance and accounting, they has taken some ways to save cost

and increase their efficiency and effectiveness such as outsourcing, service center, centers

of expertise or center of excellence. Here, it is important for us to see the whole

transformation including the structure and execution and from country as well as center

of excellence. Some aspects, we need to deep dive on such as; what are the areas need

to be touched prior to the change? What happened to the impacted parties after adopting

these approaches such as outsourcing, service center or center of expertise has their own

function and supposed role. What are the key to the successful transformation? Through

these scenarios will help us to have more understanding about how large organizations

manage their resource to keep competitive in a proper way. Moreover, we also have an

opportunity to observe and discuss on what is the real benefit out of this share service

center approach.

1.1 Why is it important?

Nowadays, organizations are facing more dynamic and competitive environment, how to

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

11important for organizations to take into account.

The first challenge is value creation. In order to create value in global economy,

Executive must understand clearly the confluence of economic, social, and technological

forces that drive industry competition.

The second challenge is value delivery. It becomes more urgent and vital for Finance

Department to demonstrate its tangible impacts by aligning with and driving the issues

critical to business to deal with the immediate / pressing need.

The third challenge is living value for Finance profession. Finance profession has to

rediscover that they are not just order takers or implementers, but are guardians of

organizations.

There are already many researches discussing about reasons for shared services or

impacts after shared service center launched from organizations view or service provider

perspectives. However, few researchers pay attention to discuss what happen to Finance

organization after outsourcing transactional jobs or adopting service center perspective.

By discuss this question, it helps us clarify the assumption or philosophy behind the

decision or provide some suggestions for others who consider taking actions. Moreover,

it is also an opportunity to discuss the trend of the structure of Finance role in country vs.

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

121.2. Aims and objectives

Under the impacts from globalization and advanced technology, multinational

organizations are facing more competitive environment than before, how to create more

value is vital and urgent for them to think about now. Here, from Finance perspective,

the aim and objectives is to see how they help organizations keep competitive advantage.

What kind of approaches do they use to add more value for Finance?

There are three objectives in this dissertation, as the following:

1. Provide the latest in thinking of Finance shared service center

2. Highlight the best practices in the creation and delivery of shared service center

3. Help organizations that are beginning these shared service journey to learn from

other

1.3 Disposition

This dissertation is comprised of five chapters. The following chapters are described

below giving an overall view of this dissertation.

Chapter 2 describes the relevant literature review.

Chapter 3 describes the methodology of this dissertation. .

Chapter 4 presents the case. In this chapter, we will see how HP creates her F&A value

and have some discussions.

Chapter 5 presents a discussion of HP regard to her Finance shared service structure, the

role and value creation and value delivery approach. Then I will have some discussions

on the real value creation out of the share service organization and give some suggestions

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

13Chapter 2 Literature review

2.1 Historical perspective vs. Reengineering Essential shared service

center

The move towards shared services began in the 1980s and has been accelerating ever

since. The centralization of back office tasks that include finance, human resources, and

information technology functions, can lead to significant cost savings. Shared service

centers primarily reduce costs by eliminating redundant work and infrastructure. By

consolidating back office, non-revenue generating functions, companies can take

advantage of economies of scale, better utilization of technology, greater automation, and

standardization to achieve higher productivity with fewer resources. These benefits are

amplified if leveraged across different company business lines.

Shared service centers allow companies to take advantage of economies of scale,

delivering higher quality and productivity with fewer resources. Cost savings, which can

be significant, generally come from the elimination of redundant work and infrastructure.

A benchmarking study completed in 2001 by PriceWaterhouseCoopers confirmed the

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

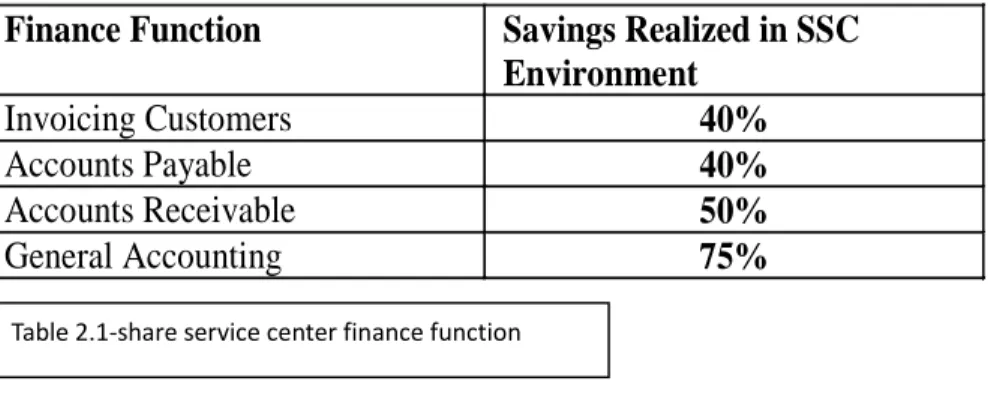

14Exhibit I. Shared Service Center Finance Function

Potential benefits of moving into a shared service environment are clear, but positive

results are contingent on a company’s ability to also implement best practices. The

Hackett Partnership concluded a recent survey on SSCs by observing that “those that

have succeeded [in realizing significant efficiency gains] have done so by making

concerted effort to improve their operations, by adopting best practices.” (Hackett

Partnership, Shared Services Survey (2002)

Reengineering is Essential

Recent surveys stress that many companies do not meet savings targets because they fail

to reengineer their processes as part of the move to adopting a shared service center

model. The majority of those who have succeeded have made a concerted effort to

improve their operations by adopting best-practices beforehand or subsequent to moving

into a shared services environment. Since the centralized nature of shared service centers

makes them more suited for standardization than individual business units, the move to a

shared service model makes future reengineering initiatives easier to implement, thereby

promoting ongoing process improvement.

Finance Function Savings Realized in SSC Environment

Invoicing Customers 40%

Accounts Payable 40%

Accounts Receivable 50%

General Accounting 75%

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

15A joint McKinsey/JPMorgan study on the cost reduction potential from a shared service

environment estimated the relative importance of three different factors: geographic

savings, scale benefits and reengineering. These findings are illustrated in the graph in

Exhibit II and demonstrate that the greatest potential for cost savings comes from

reengineering, rather than from economies of scale or off-shoring. Clearly, reengineering

plays a pivotal role in the success or failure of a shared service center.

The savings exhibited above are achieved through the following:

Geographic Savings: Conducting business in a region with rent, labor costs, and

taxes that are lower than the national average.

Scale Benefits: Leveraging system platforms and management structures, Figure 2-1 cost reduction opportunities

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

16optimizing workforce utilization, and increasing productivity.

Process Reengineering: Best practice policies and processes that include

eliminating steps and bottlenecks, simplifying processes, reducing exceptions,

prioritizing processing, and automating steps that cannot be eliminated.

2.2 Shifting Finance profile from traditional to innovation

Benefit from the technology improvement on system as well as communication easy, the

traditional finance role and responsibility (R&R) has changed from “Housekeepers for

all” that performs numbers of routine tasks and “ad hoc” tasks toward to the innovation

value added R&R.

2.3 Location Strategy Organization

Nowadays, advances in technology no longer make it necessary for all of a company’s

employees to be in one central location. Many companies are now moving to virtual

shared service center models in which physically dispersed groups follow the same

procedures and standards while all reporting to a single shared service executive.

Employees may be connected through distinct office locations, or by telecommuting from

home. Approximately 19% of companies are currently operating some type of virtual

shared service model, and as the technology improves, this number will certainly

increase.

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

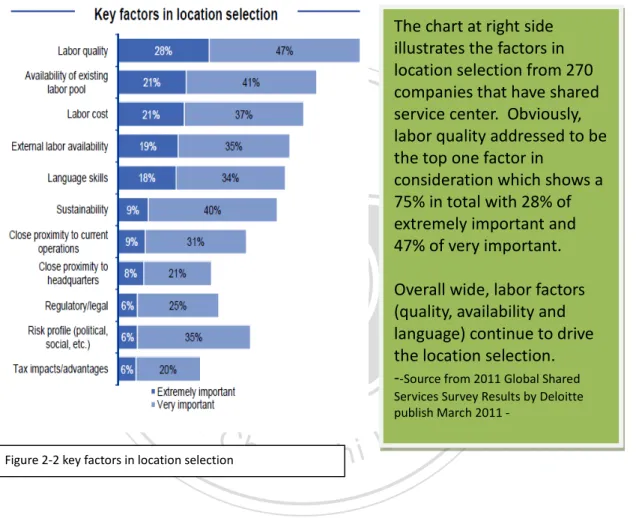

17The chart at right side illustrates the factors in location selection from 270 companies that have shared service center. Obviously, labor quality addressed to be the top one factor in

consideration which shows a 75% in total with 28% of extremely important and 47% of very important. Overall wide, labor factors (quality, availability and language) continue to drive the location selection. --Source from 2011 Global Shared Services Survey Results by Deloitte publish March 2011 -

Further to the survey, Proximity to current operations significantly dropped in

importance falling to seventh from the second factor. A drop of 50% of importance at 2009 - sourced from 2009 Deloitte Survey.

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

18Chapter 3 Research methodologies

There are two sections under this chapter. The first section analyzes the process/

structure of the case study. Another section is the limitation of research.

.

3.1 Process of this case study

The research process starts from the introduction of Hewlett Packard then follows by the

initiation of the project, structure of the share service transformation and execution. At

last, we will look at the current status and result of overall location strategy.

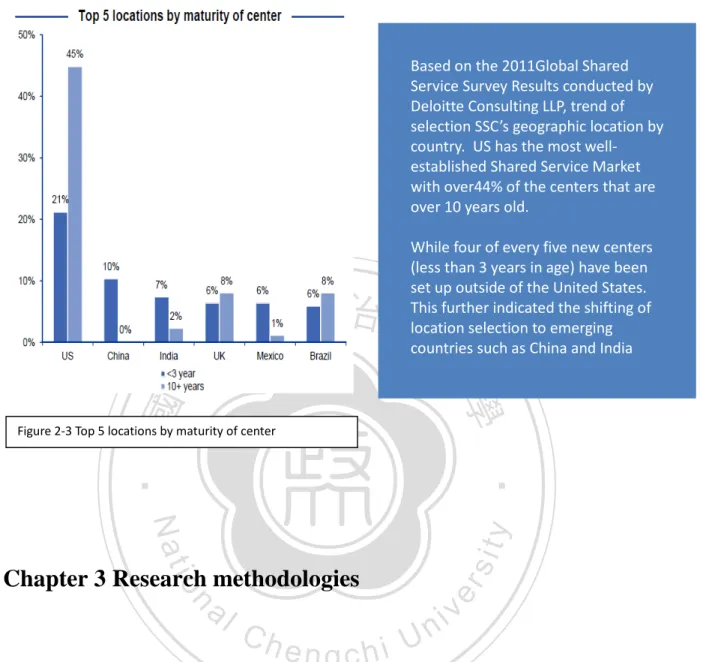

Based on the 2011Global Shared Service Survey Results conducted by Deloitte Consulting LLP, trend of selection SSC’s geographic location by country. US has the most well-established Shared Service Market with over44% of the centers that are over 10 years old.

While four of every five new centers (less than 3 years in age) have been set up outside of the United States. This further indicated the shifting of location selection to emerging countries such as China and India

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

193.2 Research limitation

There are two limitations of this research as explained and analyzed below:

i) Conclusion reference restriction:

This paper focuses only on a single case for further exploration. The selected case is the

US technology company - Hewlett Packard. Lacking of diversity of various industry

examples, the reference is limited due to insufficient scope. Figure 3-1 Case Study Process

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

20ii) Data collection methods restrictions:

The majority of the data collection is from Hewlett Packard, related reaches and surveys.

With minor interviewing as well as certain conferential consideration, they cannot answer

a large number of relevant and appropriate research questions.

Chapter 4 Discussions of the sample case

4.1 Introduction of the Hewlett Packard

HP is the world's largest IT Company that founded in 1939 with his corporate headquarters

in Palo Alto, Calif. The current CEO and President is Léo Apotheker. HP ranked No 11

by Fortune 500 at 2010. It has more than 304,000 employees and operates in more than

170 countries around the world. With company vision and mission to explore how

technology and services can help people and companies address their problems and

challenges, and realize their possibilities, aspirations and dreams.

HP provides infrastructure and business offerings that span from handheld devices to some

of the world's most powerful supercomputer installations. With a portfolio that covers

printing, personal computing, software, services and IT infrastructure, HP offers

consumers a wide range of products and services. This comprehensive portfolio generated

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

214.2 The Initiation of Finance Transformation Project – Location

Strategy

In view of the globalization and competition, Finance in HP has further aligned their

vision to promote the concepts of one team, one time and one trusted partner. (Refer to

the fig below). In year 2008, HP global Finance launched the location strategy to further

streamline organization for more efficient support to business operation.

The Global Location Strategy is a comprehensive plan that defines where work will be

done around the world based on business partner proximity, time zone overlap, statutory

and regulatory requirements, and cost. Additionally it helps to establish sites that will have

a robust ecosystem of Finance roles providing more career opportunities.

Fig ure 4 -1 H P fian cé vis io n

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

22The company further believes it is very important

To be the best, Finance must:

– Take better advantage of our global presence: synergize the global resources – Optimize where and how our work gets done: eliminate the redundancy that leads

to efficiency

– Provide the best service at a competitive cost: – Provide outstanding career opportunities.

– Deepen our partnerships with the businesses we serve: upfront engagement to promote timely insight and analysis

– Develop our skills to flow work globally and react to changes in business climate more rapidly

4.3 Structure the Organizational changes

Due diligence is made with HP internal study as well as public domain research and

analysis done by McKinsey, PWC, Deloitte Wharton Business School and Hackett…etc,

HP Finance benchmarks themselves with other worldwide multinational company with

the result of the status of “current” indicated an approximate 0.80% total spending

(investment) on Finance vs. company’s revenue generation where the world class showed

a 0.60% vs. Revenue dollar in year 2007. The interpretation is that HP Finance was in

the position that less productivity and /or less efficiency. What would be most aligned

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

23In order to be able to benchmark with world class, HP started the transformation journey

via:

A. Moving to a Different Profile of Service

Finance support was further analyzed into two major types - Operational and Partner.

Operational portion defines the transactional activities where is the fundamental to

keep the business running and basic compliance activities, There is no real restriction

to where the task should be taken place and a need for presence in each and every

site/country that company has the footprint, such as accounting front end entries

includes bookkeeping of account payable and receivable, employee spending, Figure4-2 Finance Benchmark Trends

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

24travelling, transportation, payroll, and payments execution etc.

Partner defines those finance support that is to be close to business location to

ultimate the process needs where there is a preference to be face to face with internal

business operation units or partners and external customers. Normally, these

activities would have strong restrictions such as language, specific culture behavior

that impacts to business behavior, time zone requirements. Typical activities include

business negotiation support, business strategy and innovation etc.

B. Define baseline Fragmented processes across locations and Business Units

The project then focuses on the detail role and responsibilities of finance employees

at each and every country level. Country finance support team was requested to

identify each and every activity with time spending and whether or not it would be a

location or a partner concern to serve the baseline of Transformation to the center of Figure 4-3 HP Putting the journey in perspective

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

25 expertise.The idea was to maximize the input from country finance lead and related project

lead to quickly streamline the current status and filter out the transactional activities

to move.

Under the proposed headcounts in countries, country controllers follow the analysis

on finance activities to come up with the timeframe at country level on shifting/

swapping country Finance to COE. Within the controllership and finance analysis,

individual task force was further reviewed by controller to decide what should be

moved and how much to move. At this stage, you could easily find the transactions

defined to shift would vary very much from country to country. Target is the only

indicator to meet not the real content of the work.

BU= Business Units, GPO = Global Process Organization – center of expertise (COE) Figure 4-4 HP Finance work

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

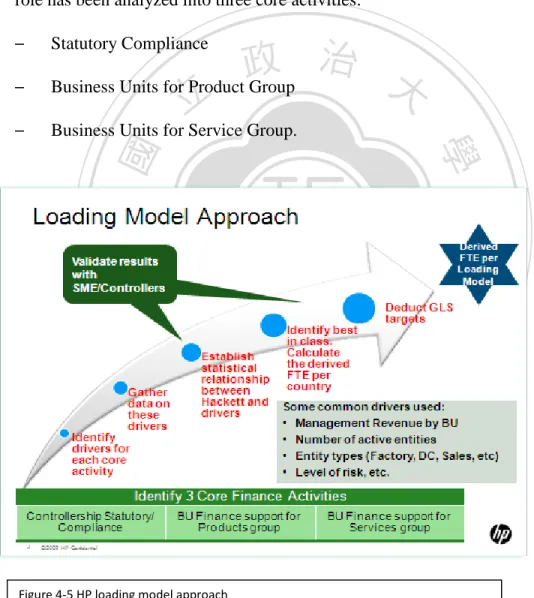

26C. Country Sizing benchmark

In order to develop a fair & objective loading model to improve and maintain HP’s

world class cost structure. Certain benchmark concepts, i.e. activities base were

analysis and put in place to build a resource loading model. Furthermore, finance

role has been analyzed into three core activities: – Statutory Compliance

– Business Units for Product Group – Business Units for Service Group.

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

27On loading analysis, some common drivers take into consideration are:

i. Revenue size – this derives the loading of business transaction both on partner

and transactional location

ii. Entities in country – certain part of finance task would be increased due to

number of entities at country level such as compliance and statutory reporting.

That would differ on actual loading at country level.

iii. Type of entities – a sales motion entity would be very different from a

manufacturing entity. So as to Research & Development entity.

iv. Risk level – this including the complexity of compliance and business

environment risk. Where would need more control and process in place to

res-assure Company is legally compliance and risk manageable.

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

28Under the loading model analysis, a rated over-all finance role and responsibility

indicated 35% of HP Finance R&R was transactional while 65% falls under operational.

Therefore, organization parameters have been set

– The proposed transformation percentage is thirty-five (35%) – Countries are categorized into large, median and small.

A high level target and goal on the project was then set to obtain a 35% geographic

shifting to build up the Center of Excellence – Finance Share Service Center. To further

execute and reach set goal, Company has decided and communicated among Finance

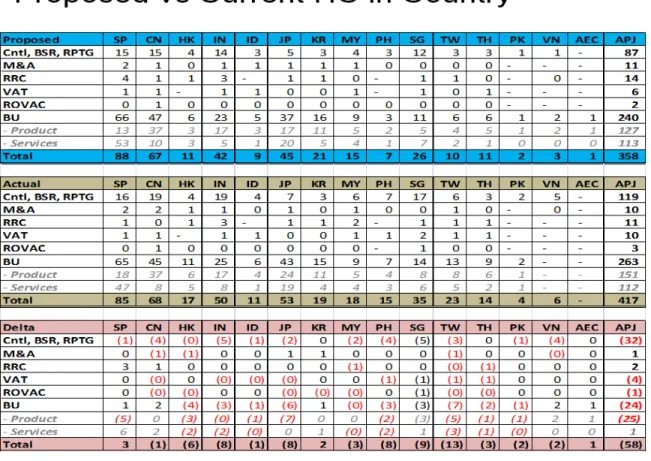

worldwide on a proposed headcount at end state. Take Asia Pacific and Japan (APJ, Asia

region) as an example, here below is the proposed headcount v.s. the actual country

headcounts at year 2007.

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

29D. Selection of suitable location of COE (center of excellence)

Few criteria and related weighting are taking into consideration for selection of COE

location:

i. Cost of Criteria: this includes Labor cost with inflation consideration,

infrastructure, real estate, taxes and incentives. One of the goal on this

project is to have world class productivities where translates to a saving on

necessary investment of Finance. Like other share service projects in the

world, low cost location is then selected. HP has identified his business

location in 170 countries and their COEs are selected in (fig # below). As

you can see the emerging counties are chose such as China Beijing and India

Bangalore.

ii. Business structure: this refers to the time zone, language where support the

max of business need. In view of the company revenue attributions, how to

fast and fully support to a general / overall needs to the partner location

among the region or worldwide. China was selected to serve population of

Chinese speaking areas such as greater China while Malaysia Cyberjaya was

selected to support the countries in Asia Pacific and Japan due to the Assessment and weighted result in HP under cost criteria Table 4-2 cost criteria

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

30language support convenience of both English and Mandarin speaking

countries like Australia, Singapore, Taiwan, Korea, and South Pacific among

Asia Pacific Area.

Table 4-3 HP Footprint

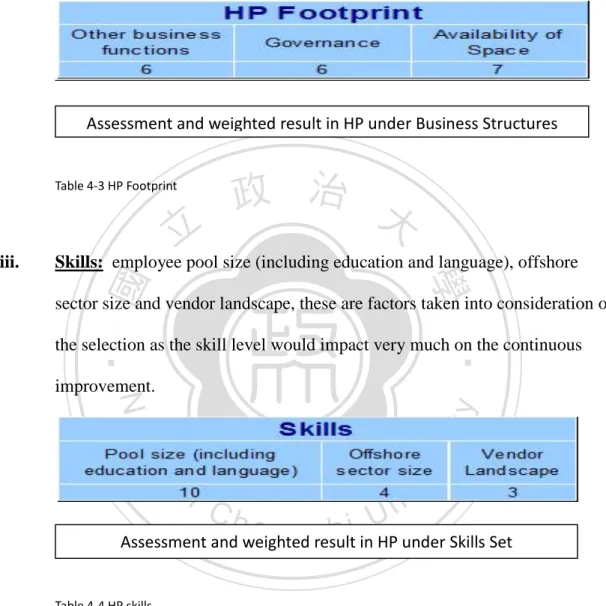

iii. Skills: employee pool size (including education and language), offshore

sector size and vendor landscape, these are factors taken into consideration of

the selection as the skill level would impact very much on the continuous

improvement.

Table 4-4 HP skills

iv. Infrastructure Quality: the readiness of overall infrastructure includes

telecoms and IT, real estate, transportation and power supply. These are

factors that matter on sustaining business continuity to eliminate the possible

interruption on operation.

Assessment and weighted result in HP under Business Structures

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

31Table 4-5 HP Infrastructure Quality

v. Environment: typical areas are government support, business environment,

quality of life and accessibility. In terms of maximize the value add on

investment, government program such as incentives is also one of the very

important consideration points. Take ride of the incentive program such as

free land, tax exemption, reimburse from government for specific investment

and/or spending to promotion or uplift the industry. Examples are China’s

free tax zone for manufacturing which associates to the finance COE setting

up and Malaysia on fully reimburse to company for the training in and out of

the country etc.

Table 4-6 HP environment

Assessment and weighted result in HP under Infrastructure Quality

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

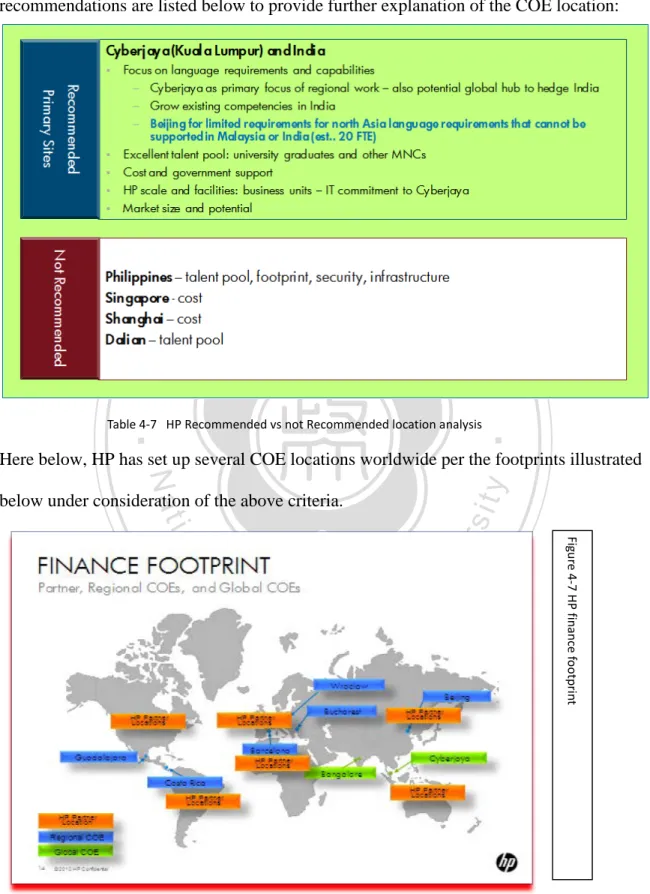

32Take example of the detail assessment in Asia Pacific, the conclusion and

recommendations are listed below to provide further explanation of the COE location:

Table 4-7 HP Recommended vs not Recommended location analysis

Here below, HP has set up several COE locations worldwide per the footprints illustrated

below under consideration of the above criteria.

Fig ure 4-7 H P f ina nc e f oo tpr int

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

334.4 Supplementary plans facilitate the transformation

Wherever changes incur, push back in place. Like most of the change project, this

transformation appears to be very sensitivity in terms of diminishing number of finance

headcounts at partner locations. To minimize the road blocks and really moving the

finance to different portfolios to value add strategic and innovation, HP has put in place

some supplementary plans in various areas to smooth the transformation, they are:

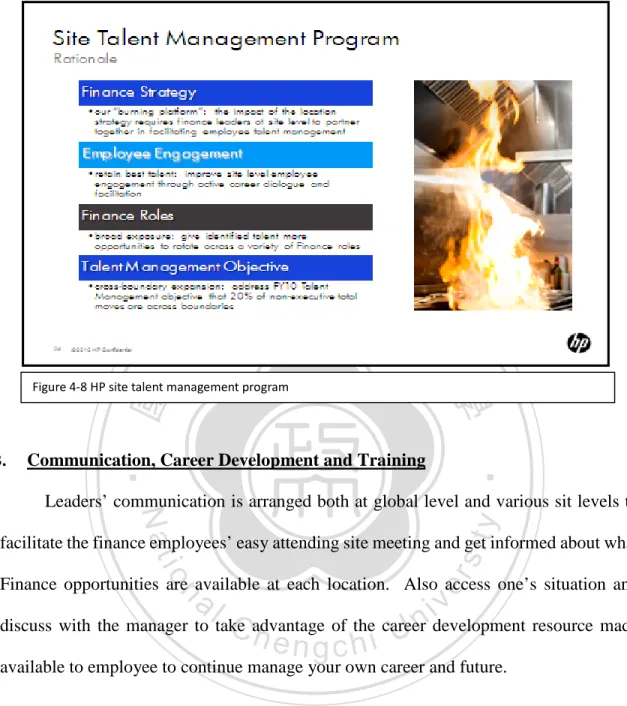

A. Talent management :

• The Site Talent Management (TM) framework is an ‘enabler’ in company

finance’s commitment to developing employees by helping facilitate rotations,

job swaps and matching the talent to open requisitions. Country finance

leaders are to roll-out the Site TM program across the 58 sites having Site

Leader presence over the next 6-9 months. Smaller sites will be addressed as a

future evolution of the program. Site leaders are accountable for the Site TM

program, s/he will drive the initial efforts to select a Site TM Council lead,

builds the Site TM council and develop the roll-out plan. The objective is to

focus on cross-boundary expansion and address that 20% of non-executive total

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

34B. Communication, Career Development and Training

Leaders’ communication is arranged both at global level and various sit levels to

facilitate the finance employees’ easy attending site meeting and get informed about what

Finance opportunities are available at each location. Also access one’s situation and

discuss with the manager to take advantage of the career development resource made

available to employee to continue manage your own career and future.

4.5 Current Project Status / Result

To further analysis on the result of company’s Finance COE transformation, we can look

at the result via different view;

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

35i. By Core Finance activities:

Today, HP has gone through the journey of global location strategy, the status by Finance

core activities are confirmed as below. The average in Finance has reached 35% global

location strategy goal. Please refer to the following table by business group and function.

The average percentage at Partner location reached 65% while COE (both regional plus

global) parks at 35% in total per ended Oct 2011. Deeper looking into the various

activities, we can see as the complexity of finance activity does lead or allow to have

different end state, such as of GPO with 25% only at partner location as majority of the

finance tasks are backend and very transactional base. You will also see an 80% in Tax

falls at partner location as high consideration of compliance specific translates to partner

location necessity. Ta ble 4 -6 H P g lo ba l fo otpr int by func tio n

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

36ii. By Project timeline:

Key progresses are summarized as below:

In FY2009 -

– Segmented Finance work into 100 discrete activities

– Mapped each activity to location types based on work attributes by business model / function

– Evaluated our existing balance of positions across locations and determined what shifts were required

– Announced the Global Location Strategy

– Started the process of moving positions to new locations

In FY 2010 –

– Continuing to shift positions in line with plan

– Established the Global Process Organization and reallocated the Global Location Strategy targets

– Clarifying our strategy at the site-level

– Continuing to enhance our ecosystem to support career opportunities – Defined Mobile Office Worker and Remote Teleworker

In FY 2011 –

Tasks completed as of April, 2011

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

37 performance indicator– Kick off deep dive on standardization role and responsibilities between COE/GPO and Country

Figure 4-9 HP COE Progress to Date

4.6 The value added of shared service model

Let’s look at the analysis on the cost impact of HP Finance before and after the Center of

Excellence - shared service center. The actual data we have now is from HP Finance

Taiwan to analyze the dollar amount saving.

For a better discussion on geographic shifting, some assumption have made to below cost

impact:

This table is the transformation result from HP Taiwan Finance With geographic change the total cost lowered down from 2007 of US$858,992 to 2010 (Oct end of 2011) $701,725.

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

38- Focus only on all in labor cost with elimination on inflation of salary

incremental

- Related compensation and benefit remains unchanged during the transformation.

- Organization efficiency if any is out of consideration on the analysis

From FY 2007, the total direct headcount cost in Taiwan finance team with the shifting of

proposed headcounts direction assigned and proposed to by Transformation Project Team

as below. 600 650 700 750 800 850 900 0 5 10 15 20 25 2007 2008 2009 2010 Partner COE TL $ 702 786 823 859 HC

How much saving in cost with a target goal of 35% headcounts shifting??

From $859K to $702K, a saving of $157K equals to 18% reduction. Based on the JPMorgan and Mckinsey

# study on cost reduction

opportunities, HP obviously did a great job on location strategy. (10% to 20%)

USD1000

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

39‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

40Chapter 5 Conclusions and Suggestions

Questions here on HP’s shared service project:1. Why it only translate to 18% saving effectiveness? Would there be a

possibility of more cost saving?

2. What can be done differently on architecture phases?

3. Where could find the miss part?

4. Direction of further synergy.

5.1 Comparisons on strategy location structure before and after

In view of the cost saving result above and the objective management on 35% direction

of COE project, HP reached overall target with minor country shifting to finish their

transformation.

As of today, the goal is reached. Take Asia Pacific and Japan as an example, we have

observed the role and responsibility at partner location to be very different from country

to country even under the same business group. A synergy was missing. This said there

was no analysis on standardization. From “How Shared Service brings cost reductions of

more than 30%” by Shane Vicser from www.Shareed –Service Org, one principle to

reach 30% saving is to eliminate non-intended task. On the HP case, prior to shifting the

headcount and task, there was no synergy but directly jump into swapping headcounts.

One suggestion here for moving from 18% saving to the next level of 60% saving # is to:

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

411. Elimination of redundancy – simplify the processes that include eliminating

steps and bottlenecks, reducing exceptions, prioritizing processing …etc.

2. Standardization process for Business units and controllership between

countries – this brings not only the efficiency but also improves and enhances

the internal control.

This is part of re-engineering mentioned and identified as essential by JPMorgan # .

5.2 Role and responsibility in country vs. center of excellence (COE)

Let’s look at the tasks at COE side, typically is all transactional activities. How to really

transform the finance employee at COE to “excellence”, the stabilization of COE

organization becomes a critical challenge. The content expert is the core of bringing to

excellence. This can be obtained by processing improvement to bring high quality of

performance, such as improve controls and processes. At country, finance would be able

to shift time on increasing data visibility to and see the new opportunities for close

engagement with business operation that says sighting directions to new growth. This is

the benefits that go beyond cost reduction.

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

425.3 Suggestion and recommendations

Observation in HP’s transformation is there are still gaps to further fill up.

Recommendations are;

Human resources wide:

The finance employees need to re-set their value proposition. It is hard to “embrace the

change”. However, commitment to new action and new thinking is essential. Company

need to focus on:

1. providing an integrated approach to encourage employee commitment and

performance of new exceptions

2. focus and raise awareness to sustaining the change made

3. have career opportunities across Finance to managing personal development

Architectural wide:

1. Utilize the scale to improve the saving – as a worldwide multi-national company,

the benefit from sale on the transformation was not seen. The root course is

lacking of standardization on process as well as horizontal calibration.

2. System Automation – among this transformation, system automation was not put

into place. Therefore, efficiency was not seen to improve. This is an area to

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

435.4 Conclusions

How to start the journey of Center of Excellence Transformation in Finance? Here is the

architecture that maximizes savings and value add to business growth

• Individual function scope of work in place: diagnose on the existing role and responsibility and put in place of Finance working Manual. That would not only

help on business continuity plan but also a quick glance to see if any redundancy

within the group. Also serves filtering the nature of work to derive partner vs.

location transactions. As the standardization already build while SOW setting,

fine tune on individual finance task is there for later execution.

• Selection of COE location – cost, talent pool, company footprint, Tax, social security, IT flexibility and other benefits like incentive… … etc.

• Readiness for move includes:

o Building employee’s awareness to the transformation to bring a better

skim of career development. At partner location, the value add of finance

team should innovate from keep the business running (KTBR) to partner

of choice.

o Management commitment – management should role modeling on driving

and willing to embrace the change. Continuous communication and

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

44o Solid project team on driving transformation

• Transformation period: Activities include: career growth opportunity for exiting employee; new hiring –match making; training and transformation.

• Service level agreement between COE and Country, once the job shifting completed, it should be followed by performance agreement. Key performance

index also need to be in place.

Under the impacts of globalization and competition, organizations are facing more urgent

need to create more value now. Profitability and cost management is the key performance

indicator for bottom up the margin. The above steps would serve a good starting toward

a better return on savings.

‧

國

立

政 治 大

學

‧

N

a

tio

na

l C

h engchi U

ni

ve

rs

it

y

45References

Moving Towards Global Shared Service Centers – JPMorgan Treasury Services, Mmay 24, 2004 Service Delivery Transformation at a glance – Deloitte, April 20, 2011

The Need for Profitability and Cost Management – Oracle, September 2008

Innovation and organizational change: Developments towards an interactive Process Perspective – Technology Analysis &Strategic Management, Vol.12, No 4, 2000

Inter-organizational Business Process – Journal of Management Information Systems, Fall 1996 Organization Structure, Individual Attitudes and Innovation – the Academy of Management review, Vol 2, No1 (Jan, 1977)

How “Shared Service” brings cost reductions of more than 30% - by Shane Vicser

Creating Business Value through Location-Based Intelligence – by David Loshin, Knowledge Integrity, Inc. October, 2010

Why “external outsourcing’ is not an element of the “Shared Service’ Concept – by Sircher Edwiz, www.Shared –Service.org

Marketing and Organizational Innovations in Entrepreneurial Innovation Processes and their Relation to Market Structure and Firm Characteristics – by Torben Schubert, March 18, 2010 HP Website,